Paytm

Auto Added by WPeMatico

Auto Added by WPeMatico

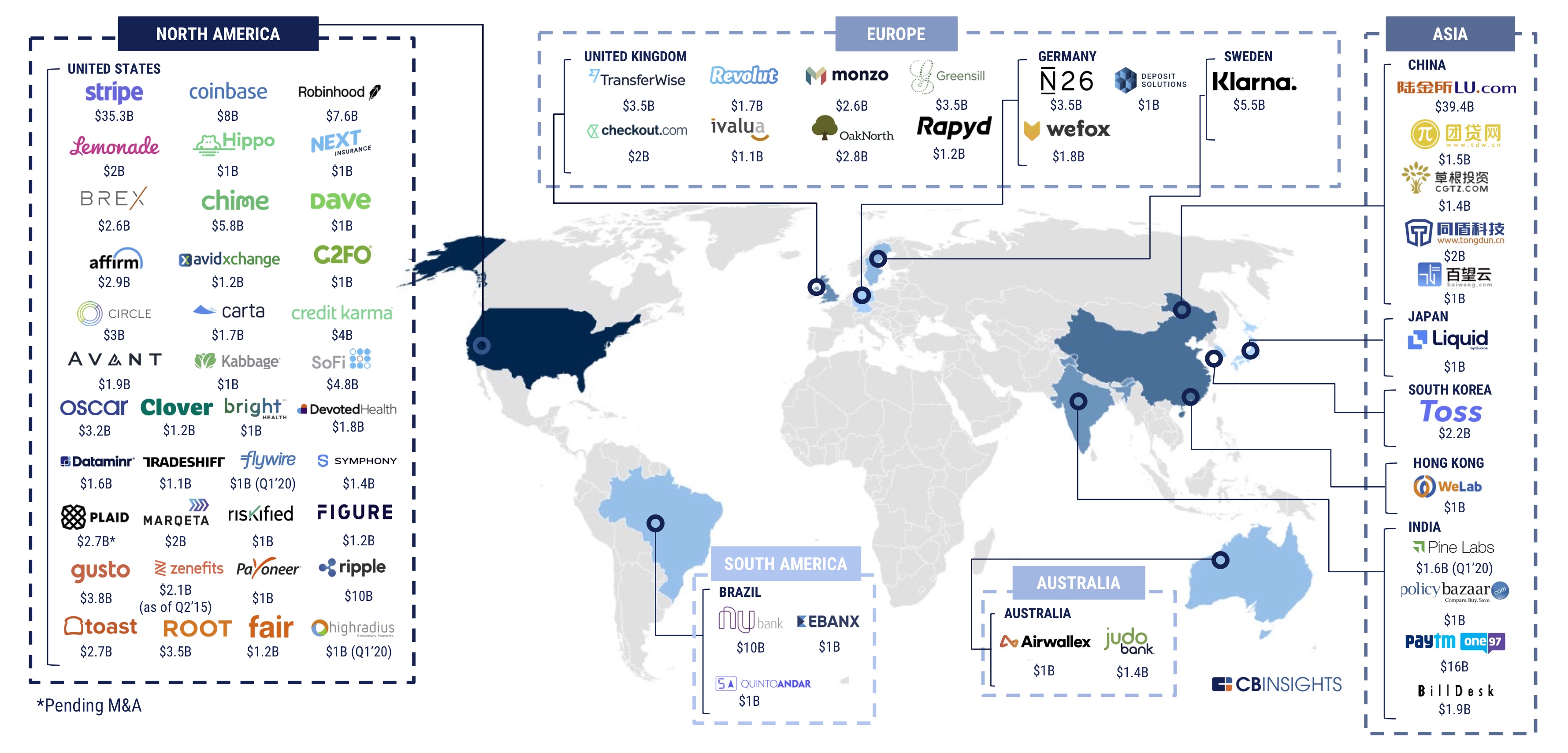

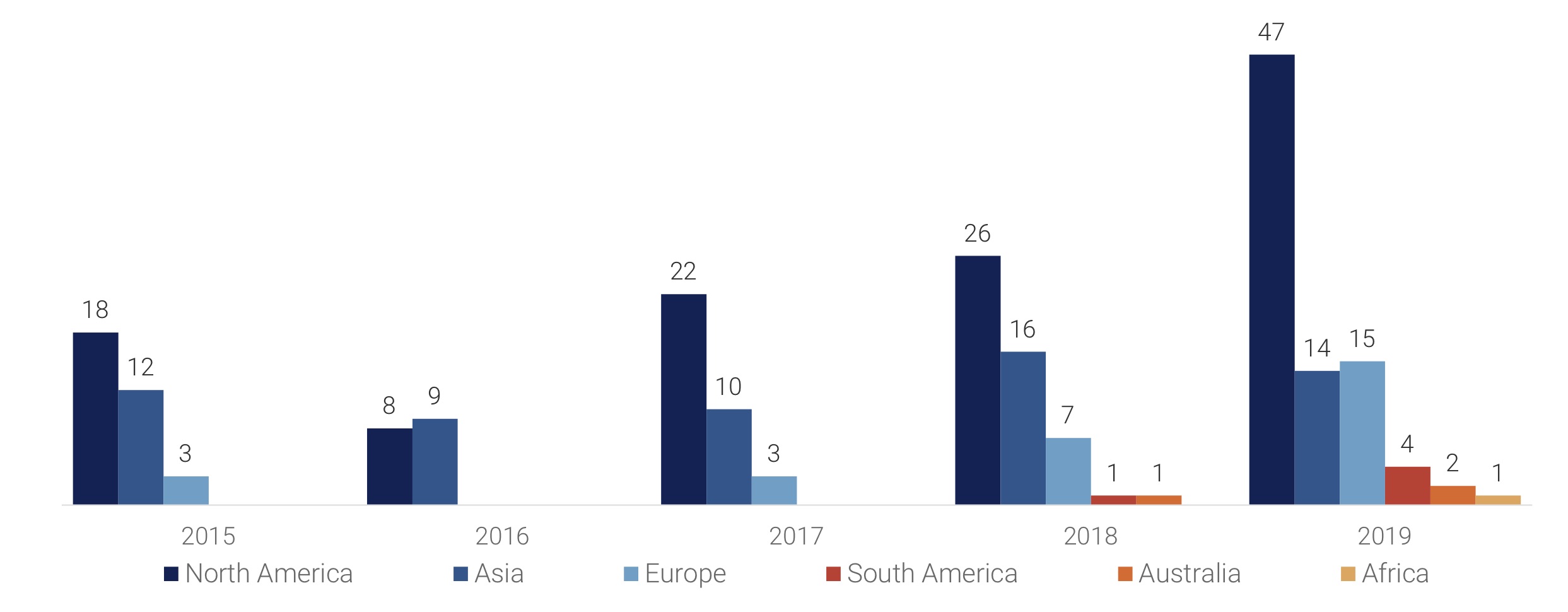

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

Simsim, a social commerce startup in India, said on Friday it has raised $16 million in seven months of its existence as it attempts to replicate the offline retail experience in the digital world with help from influencers.

The Gurgaon-based startup said it raised $16 million across seed, Series A and Series B financing rounds from Accel Partners, Shunwei Capital and Good Capital. (The most recent round, Series B, was of $8 million in size.)

“Despite e-commerce players bandying out major discounts, most of the sales in India are still happening in brick-and-mortar stores. There is a simple reason for that: Trust,” explained Amit Bagaria, co-founder of Simsim, in an interview with TechCrunch.

The vast majority of Indians are still not comfortable with reading descriptions — and that too in English, he said.

Simsim is taking a different approach to tackle this opportunity. On its app, users watch short-videos produced in local languages by influencers who apply beauty products or try out dresses and explain the ins-and-outs of the products. Below the video, the items appear as they are being discussed and users can tap on them to proceed with the purchase.

“Videos help in educating users about the category. So many of them may not have used face masks, for instance. But it becomes easier when the community influencer is able to show them how to apply it,” said Rohan Malhotra, managing partner at Good Capital, in an interview with TechCrunch.

Influencers typically sell a range of items and users can follow them to browse through the past catalog and stay on top of future sales, said Bagaria, who previously worked at the e-commerce venture of financial services firm Paytm .

“This interactiveness is enabling Simsim to mimic the offline stores experience,” said Malhotra, who is one of the earliest investors in Meesho, also a social commerce startup that last year received backing from Facebook and Prosus Ventures.

“The beauty to me of social commerce is that you’re not changing consumer behavior. People are used to consuming on WhatsApp — and it’s working for Meesho. Over here, you are getting the touch and feel experience and are able to mentally picture the items much clearer,” he said.

Simsim handles the inventories, which it sources from manufacturers and brands, and it works with a number of logistics players to deliver the products.

“Several Indian cities and towns are some of the biggest production hubs of various high-quality items. But these people have not been able to efficiently sell online or grow their network in the offline world. On Simsim, they are able to work with influencers and market their products,” said Bagaria.

The platform today works with more than 1,200 influencers, who get a commission for each item they sell, said Bagaria, who plans to grow this figure to 100,000 in the coming years.

Even as Simsim, which has been open to users for six months, is still in its nascent stage, it is beginning to show some growth. It has amassed over a million users, most of whom live in small cities and towns, and it is selling thousands of items each day, said Bagaria.

He said the platform, which currently supports Hindi, Tamil, Bengali and English, will add more than a dozen additional languages by the end of the year. In about a month, Simsim also plans to start showing live videos, where influencers will be able to answer queries from users.

A handful of startups have emerged in India in recent years that are attempting to rethink the e-commerce market in the nation. Amazon and Walmart, both of which have poured billions of dollars in India, have taken a notice too. Both of them have added support for Hindi in the last two years and have made several more tweaks to their platforms to expand their reach.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

HungerBox, an Indian food tech startup that has courted 10 of the 11 largest companies in the country to use its services, today announced it has raised $12 million from Paytm and others as it looks to sign clients in Southeast Asia.

The three-year-old startup’s new financing round, a Series C, was funded by a consortium of Indian and international investors, including payments firm Paytm and NPTK, an Asian VC fund that invests in emerging firms. Existing investors Sabre Partners and Neoplux also participated in the round, which pushes the Bangalore-based startup’s to-date raise to $16.5 million.

HungerBox offers management services to companies and institutions to improve and run their in-house cafeterias and canteens. HungerBox also enables its clients to connect with food partners through an app and get real-time updates of their order.

The startup, which also provides these firms with a point-of-sale machine, helps them get better insight into the quality of food being catered to their employees, and enables scheduled delivery and tracking of orders to address the long queues, said Sandipan Mitra, co-founder and chief executive of HungerBox, in an interview with TechCrunch.

“We all talk about the food delivery to consumers, but not many are looking to improve the quality of food and how it is being catered to tens of millions of employees in the country each day,” he said. “It’s a challenge that has not been addressed well.”

It turns out, when a startup finally looked into the space, many quickly jumped to appreciate it. HungerBox has amassed more than 126 large businesses and institutions — with more than 100,000 workforce each, across 18 Indian cities, said Mitra. Food delivery startups Swiggy and Zomato have started to explore this space, too, in recent quarters.

HungerBox is processing 560,000 orders each day, a figure that is growing 10% every month, claimed Mitra. The startup’s solutions are today employed at more than 535 cafeterias for its clients that work in IT / technology, retail, healthcare, aviation, education, financial services and manufacturing, he said. He declined to reveal the name of the clients, citing confidential agreements.

Annual food sales on the HungerBox platform have exceeded $100 million, he said.

The startup, which employs 1,500 people, will use the fresh capital to fuel its expansion in 10 additional Indian cities and to markets in Southeast Asia, said Mitra.

In a statement, Madhur Deora, president of Paytm, said HungerBox has enabled Paytm to add new use cases for the company’s payments business and digitization of offline transactions.

“HungerBox is the market leader in the institutional food tech space and we will partner closely with them and bring the benefits of Paytm’s ecosystem to HungerBox,” he said.

Powered by WPeMatico

An Indian SaaS startup, which is increasingly courting clients from outside of the country, just raised a significant amount of capital to expand its business.

Hyderabad-based Darwinbox, which operates a cloud-based human resource management platform, said on Thursday it has raised $15 million in a new financing round. The Series B round — which moves the firm’s total raise to $19.7 million — was led by Sequoia India and saw participation from existing investors Lightspeed India Partners, Endiya Partners, and 3one4 Capital.

More than 200 firms including giants such as adtech firm InMobi, fintech startup Paytm, drink conglomerate Bisleri, automobile maker Mahindra, Kotak group, and delivery firms Swiggy and Milkbasket use Darwinbox’s HR platform to serve half a million of their employees in 50 nations, Rohit Chennamaneni, cofounder of Darwinbox, told TechCrunch in an interview.

The startup, which competes with giants such as SAP and Oracle, said its platform enables high level of configurability, ease of use, and understands the needs of modern employees. “The employees today who have grown accustomed to using consumer-focused services such as Uber and Amazon are left disappointed in their experience with their own firm’s HR offerings,” said Gowthami Kanumuru, VP Marketing at Darwinbox, in an interview.

Darwinbox’s HR platform offers a range of features including the ability for firms to offer their employees insurance and early salary as loans. Its platform also features social networks for employees within a company to connect and talk, as well as an AI assistant that allows them to apply for a leave or set up meetings with quick voice commands from their phone.

“The AI system is not just looking for certain keywords. If an employee tells the system he or she is not feeling well today, it automatically applies a leave for them,” she said.

Darwinbox’s platform is built to handle onboarding new employees, keeping a tab on their performance, monitor attrition rate, and maintain an ongoing feedback loop. Or as Kanumuru puts it, the entire “hiring to retiring” cycle.

One of Darwinbox’s clients is L&T, which is tasked with setting up subway in many Indian cities. L&T is using geo-fencing feature of Darwin to log the attendance of employees. “They are not using biometric punch machine that is typically used by other firms. Instead, they just require their 1,200 employees to check-in from the workplace using their phones,” said Kanumuru.

Additionally, Darwinbox is largely focusing on serving companies based in Asia as it believes Western companies’ solutions are not a great fit for people here, said Kanumuru. The startup began courting clients in Southeast Asian markets last year.

“Our growth is a huge validation for our vision,” she said. “Within six months of operations, we had the delivery giant Delhivery with over 23,000 employees use our platform.”

In a statement to TechCrunch, Dev Khare, a partner at Lightspeed Venture, said, “there is a new trend of SaaS companies targeting the India/SE Asia markets. This trend is gathering steam and is disproving the conventional wisdom that Asia-focused SaaS companies cannot get to be big companies. We firmly believe that Asia-focused SaaS companies can get to large impact value and become large and profitable. Darwinbox is one of these companies.”

Darwinbox’s Chennamaneni said the startup will use the fresh capital to expand its footprints in Indonesia, Malaysia, Thailand, and other Southeast Asian markets. Darwinbox will also expand its product offerings to address more of employees’ needs. The startup is also looking to make its platform enable tasks such as booking of flights and hotels.

Chennamaneni, an alum of Google and McKinsey, said Darwinbox aims to double the number of clients it has in the next six to nine months.

Powered by WPeMatico

Of the 1.3 billion people who live in India, more than 100 million of whom are using digital payment apps each day, only about 20 million today invest in mutual funds and stocks. An Indian startup that is betting on changing that figure by courting millennials has just received a big backing.

Groww, a Bangalore-based startup, said today it has raised $21.4 million in a Series B financing round that was led by U.S.-based VC firm Ribbit Capital. Existing investors Sequoia India and Y Combinator also participated in the round, said the two-year-old startup that has raised about $29 million to date.

Groww allows users to invest in mutual funds, including systematic investment planning (SIP) and equity-linked savings. The app, which maintains a very simplified user interface to make it easier for its largely millennial customer base to comprehend the investment world, offers every fund that is currently available in India.

Lalit Keshre, co-founder and CEO of Groww, told TechCrunch in an interview earlier this week that the market of mutual funds is increasingly widening in India and the startup is hoping to accelerate its growth with the fresh capital. Other than that, he plans to double Groww’s headcount to 200 in the coming months.

Groww has amassed about 2.5 million registered users, two-thirds of whom are first-time investors, Keshre said. Groww is currently free to use and does not charge any commission on transactions. The startup eventually plans to offer a paid service as it looks to monetize its user base, but Keshre declined to share a timeline on how soon that would happen.

Groww will also soon begin to offer the ability to purchase stocks from its eponymous app, said Keshre, a former executive at Flipkart who co-founded Groww with three other Flipkart colleagues (Harsh Jain, Neeraj Singh and Ishan Bansal).

In a statement, Micky Malka, founder of Ribbit Capital, said, “We backed the Groww team because we believe in their mission. They have built the most trusted product in this space and are on the path to create a category-defining product.”

Ribbit Capital has made a number of investments in India in recent months. Last month, it invested in Cred, a startup that is trying to improve the financial behavior of credit card holders, and BharatPe, a payments solution for businesses.

In recent years, a number of startups such as INDWealth and Cube Wealth have emerged in India to offer wealth management platforms to the country’s growing internet population. Many established financial firms such as Paytm have also expanded their offerings to include investments in mutual funds.

Ashish Agarwal, a principal partner at Sequoia Capital India, said, “Investment products such as mutual funds and stocks were traditionally sold offline through financial advisors, who were mis-incentivized to sell high-commission products. Groww is taking a refreshing approach with a zero-commission mobile first model, enabling investors to make their own investment choices through a slick and easy user interface.”

Powered by WPeMatico

Paytm, India’s biggest mobile payments firm, now has 10 million customers in Japan, the company said as it pushes to expand its reach in international markets. Paytm entered Japan last October after forming a joint venture with SoftBank and Yahoo Japan called PayPay.

In addition to 10 million users, PayPay is now supported by 1 million merchant partners and local stores in Japan, Vijay Shekhar Sharma, founder and CEO of Paytm said Thursday. The mobile payments app has clocked more than 100 million transactions to date in the nation, he claimed. In June, PayPay had 8 million users.

“Thank you India  for your inspiration and giving us chance to build world class tech…,” he posted in a tweet.

for your inspiration and giving us chance to build world class tech…,” he posted in a tweet.

Like in India, cash also dominates much of the daily transactions in Japan. Large medical clinics and supermarkets often refuse to accept plastic cards and instead ask for cash. This encouraged Paytm, which also has presence in Canada, to explore the Japanese market.

And it has the experience, capital and tech chops to achieve it. The mobile payments app has amassed more than 250 million registered users in India. Most of these customers signed up after the Indian government invalidated much of the cash in the nation in late 2016.

PayPay competes with a handful of local players in Japan. Its biggest competition is Line, an instant messaging app that has followed China’s WeChat model to aggressively expand its offerings in recent years.

Like PayPay, Line also has no shortage of money. Earlier this year, it announced a ¥30 billion ($282 million) reward campaign to boost usage of its payments service. Line has more than 80 million users in Japan, 32 million of whom used its payments service as of February this year. There are about 120 million internet users in Japan.

PayPay maintains a ¥10 billion ($94 million) marketing campaign of its own, as part of which customers who make a certain number of transactions and participate in referral programs earn some money. In a statement, PayPay said Thursday that moving forward it “will strive to create a society where people can buy anything through cashless payments in every corner of the country with a safe and secured service for our users.”

Powered by WPeMatico

WhatsApp has amassed more than 400 million users in India, the instant messaging app confirmed today, reaffirming its gigantic reach in its biggest market.

Amitabh Kant, CEO of highly influential local think-tank NITI Aayog, revealed the new stat at a press conference held by WhatsApp in New Delhi on Thursday. A WhatsApp spokesperson confirmed that the platform indeed had more than 400 million monthly active users in the country.

The remarkable revelation comes more than two years after WhatsApp said it had hit 200 million users in India. WhatsApp — or Facebook — did not share any India-specific users count in the period in between.

The public disclosure today should help Facebook reaffirm its dominance in India, where it appears to be used by nearly every smartphone user. According to research firm Counterpoint, India has about 450 million smartphone users. (Some other research firms peg the number to be lower.)

It’s worth pointing out that WhatsApp also supports KaiOS — a mobile operating system for feature phones. Millions of KaiOS-powered JioPhone handsets have shipped in India. Additionally, there are about 500 million internet users, according to several industry estimates.

As WhatsApp becomes ubiquitous in the nation, the service is increasingly mutating to serve additional needs. Businesses such as social-commerce app Meesho have been built on top of WhatsApp. Facebook backed Meesho recently in what was its first investment of this kind in an Indian startup. Then, of course, WhatsApp has also come under hot water for its role in the spread of false information in the nation.

As ByteDance and others aggressively expand their businesses in India, Facebook’s perceived dominance in the country has come under attack in recent months. ByteDance’s TikTok, which has amassed 120 million users in India, has been heralded by many as the top competitor of Facebook.

A WhatsApp spokesperson also told TechCrunch that India remains WhatsApp’s biggest market. In 2017, Facebook said its marquee service had about 250 million users in India — a figure it has not updated in the years since.

WhatsApp, which has about 1.5 billion monthly active users worldwide, does not really have any major competitor in India. The closest to a competitor it has in the country is Messenger, another platform owned by Facebook, and Hike, which millions of users check everyday. Times Internet — an internet conglomerate in India that runs several news outlets, entertainment services and more — claims to reach 450 million users in the country each month.

At the aforementioned press conference, WhatsApp global chief Will Cathcart said WhatsApp also plans to roll out WhatsApp Pay, its payment service, to all its users toward the end of the year — something TechCrunch reported earlier.

Its arrival in India’s burgeoning payments space could create serious tension for Google Pay, Flipkart’s PhonePe and Paytm. For Facebook, WhatsApp Pay’s success is even more crucial as the company currently has no plans to bring cryptocurrency wallet Calibra to the country, it told TechCrunch on the sidelines of the Libra and Calibra unveil.

In a series of announcements this week, WhatsApp also unveiled a tie-up with NITI Aayog to promote women’s entrepreneurship. “By launching ‘gateway to a billion opportunities’ and our digital skills training program, we hope to shine a light on the amazing work already happening and build the next generation of entrepreneurs and change makers,” said Cathcart.

At a conference in Mumbai on Wednesday, Cathcart announced a partnership with the Indian School of Public Policy — India’s first program in the theory and practice of public policy, product design and management — to bring a series of privacy design workshops to future policy makers. These workshops will explore “the importance and practice of privacy-centric design to help technology make a positive impact on society,” the Facebook-owned platform said.

Powered by WPeMatico

At a conference in New Delhi early last year, Netflix CEO Reed Hastings was confronted with a question that his company has been asked many times over the years. Would he consider lowering the subscription cost in India?

It’s a tactic that most Silicon Valley companies have adapted to in the country over the years. Uber rides aren’t as costly in India as they are elsewhere. Spotify and Apple Music cost less than $2 per month to users in the country. YouTube Premium as well as subscriptions to U.S. news outlets such as WSJ and New York Times are also priced significantly lower compared to the prices they charge in their home turf.

Hastings had also come prepared: He acknowledged that the entertainment viewing industry in India is very different from other parts of the world. To be sure, much of the pay-TV in India is supported by ads and the access fee remains too low ($5). But that was not going to change how Netflix likes to roll, he said.

“We want to be sensitive to great stories and to fund those great stories by investing in local content,” he said. “So yes, our strategy is to build up the local content — and of course we have got the global content — and try to uplevel the industry,” he said, identifying movie-goers who spend about Rs 500 ($7.25) or more on tickets each month as Netflix’s potential customers.

Indian commuters walking below a poster of “Sacred Games”, an original show produced by Netflix (Image: INDRANIL MUKHERJEE/AFP/Getty Images)

Less than a year and a half later, Netflix has had a change of heart. The company today rolled out a lower-priced subscription plan in India, a first for the company. The monthly plan, which restricts usage of the service to mobile devices only, is priced at Rs 199 ($2.8) — a third of the least expensive plan in the U.S.

At a press conference in New Delhi today, Netflix executives said that the lower-priced subscription tier is aimed at expanding the reach of its service in the country. “We want to really broaden the audience for Netflix, want to make it more accessible, and we knew just how mobile-centric India has been,” said Ajay Arora, Director of Product Innovation at Netflix.

The move comes at a time when Netflix has raised its subscription prices in the U.S. by up to 18% and in the UK by up to 20%.

Netflix’s strategy shift in India illustrates a bigger challenge that Silicon Valley companies have been facing in the country for years. If you want to succeed in the country, either make most of your revenue from ads, or heavily subsidize your costs.

But whether finding users in India is a success is also debatable.

Powered by WPeMatico

Away from the limelight of the press and the frenzy of fundraising, a tech startup in India has achieved a feat that few of its peers have managed: going public.

IndiaMART, the country’s largest online platform for selling products directly to businesses, raised nearly $70 million in a rare tech IPO for India this week.

The milestone for the 23-year-old firm is so uncommon for India’s otherwise burgeoning startup ecosystem that, beyond being over-subscribed 36 times, pent up demand for IndiaMART’s stock saw its share price pop 40% on its first day of trading on National Stock Exchange on Thursday — a momentum that it sustained on Friday.

The stock ended Friday at Rs 1326 ($19.3), compared to its issue price of Rs 973 ($14.2).

IndiaMART is the first business-to-business e-commerce firm to go public in India. Its IPO also marks the first listing for a firm following the May reelection of Narendra Modi as the nation’s Prime Minister and the months-long drought that led to it.

Accounting firm EY said it expects more companies from India to follow suit and file for IPO in the coming months.

“Now that national elections are over and favorable results secured, IPO activity is expected to gain momentum in H2 2019 (second half of the year). Companies that had filed their offer documents with the Indian stock markets regulator during H2 2018 and Q1 2019 may finally come to market in the months ahead,” it said in a statement (PDF).

The fireworks of the IPO are just as impressive as IndiaMART’s journey.

The startup was founded in 1996 and for the first 13 years, it focused on exports to customers abroad, but it has since modernized its business following the wave of the internet.

“The thesis was, in 1996, there were no computers or internet in India. The information about India’s market to the West was very limited,” Dinesh Agarwal, co-founder and CEO of IndiaMART, told TechCrunch in an interview.

Until 2008, IndiaMART was fully bootstrapped and profitable with $10 million in revenue, Agarwal said. But things started to dramatically change in that year.

“The Indian rupee became very strong against the dollar, which dwindled the exports business. This is also when the stock market was collapsing in the West, which further hurt the exports demand,” he explained.

Dinesh Agarwal, founder and CEO of IndiaMart.com, poses for a profile shot on July 29, 2015 in Noida, India.

By this time, millions of people in India were on the internet and, with tens of millions of people owning a feature phone, the conditions of the market had begun to shift towards digital.

“This is when we decided to pursue a completely different path. We started to focus on the domestic market,” Agarwal said.

Over the last 10 years, IndiaMART has become the largest e-commerce platform for businesses with about 60% market share, according to research firm KPMG. It handles 97,000 product categories — ranging from machine parts, medical equipment and textile products to cranes — and has amassed 83 million buyers and 5.5 million suppliers from thousands of towns and cities of India.

According to the most recent data published by the Indian government, there are about 50 to 60 million small and medium-sized businesses in India, but only around 10 million of them have any presence on the web. Some 97% of the top 50 companies listed on National Stock Exchange use IndiaMART’s services, Agarwal said.

That’s not to say that the transition to the current day was a straightforward process for the company. IndiaMART tried to capitalize on its early mover advantage with a stream of new services which ultimately didn’t reap the desired rewards.

In 2002, it launched a travel portal for businesses. A year later, it launched a business verification service. It also unveiled a payments platform called ABCPayments. None of these services worked and the firm quickly moved on.

Part of IndiaMART’s success story is its firm leadership and how cautiously it has raised and spent its money, Rajesh Sawhney, a serial angel investor who sits on IndiaMART’s board, told TechCrunch in an interview.

IndiaMART, which employs about 4,000 people, is operationally profitable as of the financial year that ended in March this year. It clocked some $82 million in revenue in the year. It has raised about $32 million to date from Intel Capital, Amadeus Capital Partners and Quona Capital. (Notably, Agarwal said that he rejected offers from VCs for a very long time.)

The firm makes most of its revenue from subscriptions it sells to sellers. A subscription gives a seller a range of benefits including getting featured on storefronts.

4/4. So many Indian small businesses have so much to thank @DineshAgarwal for. And after the iconic IPO, so many Indian entreprenuers will have so much to thank him for – forever unlocking the Indian public markets to current & future generation of Indian internet companies

— Kunal Bahl (@1kunalbahl) July 4, 2019

There are only a handful of internet companies in India that have gone public in the last decade. Online travel service MakeMyTrip went public in 2010. Software firm Intellect Design Arena and e-commerce store Koovs listed in 2014, then travel portal Yatra and e-commerce firm Infibeam followed two years later.

India has consistently attracted billions of dollars in funding in recent years and produced many unicorns. Those include Flipkart, which was acquired by Walmart last year for $16 billion, Paytm, which has raised more than $2 billion to date, Swiggy, which has bagged $1.5 billion to date, Zomato, which has raised $750 million, and relatively new entrant Byju’s — but few of them are nearing profitability and most likely do not see an IPO in their immediate future.

In that context, IndiaMART may set a benchmark for others to follow.

“The fact that we have a homegrown digital commerce business, serving both the urban and smaller cities, and having struggled and been around for so long building a very difficult business and finally going public in the local exchange is a phenomenal story,” Ganesh Rengaswamy, a partner at Quona Capital, told TechCrunch in an interview. “It keeps the story of India tech, to the Western world, going.”

Congratulations @DineshAgarwal for an iconic IPO! @IndiaMART has set an example and hope for all Indian Internet companies looking to go public. Cheers! https://t.co/yJumFjfitS

— Vani Kola (@VaniKola) July 4, 2019

Generally, it is agreed that there are too few IPOs in India and the industry can benefit from momentum and encouragement of high profile and successful public listings.

“There is a firm consensus that in India, markets will prefer only the IPOs of companies that are profitable. And investors in India might not value those companies. Both of these issues are being addressed by IndiaMART,” said Sawhney.

“We need 30 to 40 more IPOs. This will also mean that the stock market here has matured and understands the tech stocks and how it is different from other consumer stocks they usually handle. More tech companies going public would also pave the way for many to explore stock exchanges outside of India.

“Indian market is ready for more tech stocks. We just need to get more companies to go out there,” Sawhney added, although he did predict that it will take a few years before the vast majority of leading startups are ready for the public market.

The Indian government, for its part, this week announced a number of incentives to uplift the “entrepreneurial spirit” in the nation.

Finance minister Nirmala Sitharaman said the government would ease foreign direct investment rules for certain sectors — including e-commerce, food delivery, grocery — and improve the digital payments ecosystem. Sitharaman, who is the first woman to hold this position in India, said the government would also launch a TV program to help startups connect with venture capitalists.

IndiaMART has managed to build a sticky business that compels more than 55% of its customers to come back to the platform and make another transaction within 90 days, Agarwal — its CEO — said. With some 3,500 of its 4,000 employees classified as sales executives, the company is aggressive in its pursuit of new customers. Moving forward, that will remain one of its biggest focuses, according to Agarwal.

“Most of our time still goes into educating MSMEs on how to use the internet. That was a challenge 20 years ago and it remains a challenge today,” he told TechCrunch.

In recent years, IndiaMART has begun to expand its suite of offerings to its business customers in a bid to increase the value they get from its platform and thus increase their reliance on its service.

IndiaMART has built a customer relationship management (CRM) tool so that customers need not rely on spreadsheets or other third-party services.

“We will continue to explore more SaaS offerings and look into solving problems in accounting, invoice management and other areas,” said Agarwal.

The firm also recently started to offer payment facilitation between buyers and sellers through a PayPal -like escrow system.

“This will bridge the trust gap between the entities and improve an MSME’s ability to accept all kinds of payment options including the new age offerings.”

There’s an elephant in the room, however.

A bigger challenge that looms for IndiaMART is the growing interest of Amazon and Walmart in the business-to-business space. Several startups including Udaan — which has raised north of $280 million from DST Global and Lightspeed Venture Partners — have risen up in recent years and are increasingly expanding their operations. Agarwal did not seem much worried, however, telling TechCrunch that he believes that his prime competition is more focused on B2C and serving niche audiences. Besides he has $100 million in the bank himself.

Indeed, as Quona Capital’s Rengaswamy astutely noted, competition is not new for IndiaMART — the company has survived and thrived more than two decades of it.

“Alibaba came and gave up,” he noted.

An important — and unanswered question — that follows the successful IPO is how IndiaMART’s stock will fare over the coming months. A glance to the U.S. — where hyped companies like Uber, Lyft and others have seen prices taper off — shows clearly that early demand and sustained stock performance are not one and the same.

Nobody knows at this point, and the added complexity at play is that the concept of a tech IPO is so uncommon in India that there is no definitive answer to it… yet. But IndiaMART’s biggest achievement may be that it sets the pathway that many others will follow.

Powered by WPeMatico