paypal

Auto Added by WPeMatico

Auto Added by WPeMatico

The COVID-19 pandemic has forced businesses to rethink how they accept and make payments. Paper invoices, checks and point-of-sale payments have given way to “corona-free payments” through mobile apps, electronic invoicing and ACH. Although significant, this is the sideshow to a more significant reshuffling of the payments industry.

Nearly $150 trillion in worldwide B2B and B2C transactions take place every year, but only a tiny portion are digital. A lot of technology companies want their piece of that massive pie. Until recently, though, only payment facilitators (aka, “payfacs”), gateways, banks and credit card companies had access to it.

That’s changing. Whether they know it yet or not, B2B tech platforms are becoming payments companies. Payfacs are competing to integrate their technology into these platforms, which drive an ever-growing number of transactions. Revenue-sharing deals are on the table, and payfacs are pushing the competitive advantages they can offer to the clients of these B2B platforms. Capabilities like cross-border payments, seamless customer onboarding, fraud protection, marketplace payments and B2B invoicing influence, which payfacs win in “integrated payments” (the jargon for this space) and which don’t.

B2B companies that use to leave the choice of gateway to their clients need to become savvy in payment technology, both to control the user experience and to tap this new business. There’s a massive amount of revenue on the table, and it’s just too easy to blow this opportunity and alienate clients in the process.

A decade ago, the revolution in cloud computing led to a wave of B2B tech platforms promising to “disrupt” every industry. Gyms got gym management platforms. Hospitals got clinic management platforms. Retailers got commerce management platforms. Media companies got subscription management platforms. Many of these fill-in-the-blank management platforms — all independent software vendors (ISVs) — helped clients manage their operations and interactions with consumers or other businesses.

But ISVs didn’t get involved in payments, which was odd, given how complementary payments were to their platforms and how much money was at stake. Mastercard says there is about $120 trillion annually in B2B payments worldwide, and paper checks still dominate about half of the U.S.’s $25 trillion payment volume. Meanwhile, retail e-commerce sales account for $4.2 trillion out of $26 trillion in total retail, or about 16.1%, according to eMarketer. Less than 8% of global commerce is thought to occur online.

You’d think B2B software companies would find a way to generate revenue on some of that $146 trillion in transactions, but most did not. Payment processing is its own, messy, complicated niche. Payfacs go through a grueling underwriting process to provision a merchant account, which includes know-your-customer (KYC) and anti-money laundering (AML) checks. If a merchant defaults, the payfac is next in line to make good on the transactions.

When you run a venture-backed B2B platform, you have enough to worry about already.

So, B2B platforms stayed clear. They formed integrations with a basket of payfacs (Stripe, PayPal, Square, my company BlueSnap, etc.) and then let their clients choose which one to use. That’s a lot of integrations to maintain.

Powered by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

In Asia, where I work as a partner at an early-stage VC firm, startups are regularly rolling out a minimum viable product (MVP) and then transacting on messaging apps.

Companies like shoe brand Portblue, AI e-commerce company Sorabel and Sama, an online recruitment platform for migrant workers, all started life using WhatsApp and Facebook Messenger to communicate with customers, onboard users and raise brand awareness.

For many years, WeChat has been the default app for daily life and business in China. It’s estimated that more than 30% of all internet traffic in China is through WeChat, and in 2017 they introduced “mini-programs,” where businesses could build apps inside WeChat. Now you never have to download any apps or go to a browser to access millions of services and businesses in WeChat.

We now see a similar trend in Southeast Asia. Here, WhatsApp is the dominant social platform and, while it has not built the same infrastructure for building apps, startups have found a way around that and now run many services on top of WhatsApp, validating with customers quickly and cheaply. These companies are not only mobile-first, but they are also WhatsApp-first.

Sampingan, an Antler portfolio company founded here in Singapore, provides an on-demand workforce to businesses in Indonesia. The first version of the product was on WhatsApp. The team sourced and managed more than 2,000 blue-collar workers in Indonesia who completed 25,000 jobs in the company’s first three months.

Lisa Enckell is a partner at Antler, an early-stage venture capital firm and startup generator.

Powered by WPeMatico

Nvidia today announced that it has acquired SwiftStack, a software-centric data storage and management platform that supports public cloud, on-premises and edge deployments.

The company’s recent launches focused on improving its support for AI, high-performance computing and accelerated computing workloads, which is surely what Nvidia is most interested in here.

“Building AI supercomputers is exciting to the entire SwiftStack team,” says the company’s co-founder and CPO Joe Arnold in today’s announcement. “We couldn’t be more thrilled to work with the talented folks at NVIDIA and look forward to contributing to its world-leading accelerated computing solutions.”

The two companies did not disclose the price of the acquisition, but SwiftStack had previously raised about $23.6 million in Series A and B rounds led by Mayfield Fund and OpenView Venture Partners. Other investors include Storm Ventures and UMC Capital.

SwiftStack, which was founded in 2011, placed an early bet on OpenStack, the massive open-source project that aimed to give enterprises an AWS-like management experience in their own data centers. The company was one of the largest contributors to OpenStack’s Swift object storage platform and offered a number of services around this, though it seems like in recent years it has downplayed the OpenStack relationship as that platform’s popularity has fizzled in many verticals.

SwiftStack lists the likes of PayPal, Rogers, data center provider DC Blox, Snapfish and Verizon (TechCrunch’s parent company) on its customer page. Nvidia, too, is a customer.

SwiftStack notes that it team will continue to maintain an existing set of open source tools like Swift, ProxyFS, 1space and Controller.

“SwiftStack’s technology is already a key part of NVIDIA’s GPU-powered AI infrastructure, and this acquisition will strengthen what we do for you,” says Arnold.

Powered by WPeMatico

Contract management service DocuSign today announced that it is acquiring Seal Software for $188 million in cash. The acquisition is expected to close later this year. DocuSign, it’s worth noting, previously invested $15 million in Seal Software in 2019.

Seal Software was founded in 2010, and, while it may not be a mainstream brand, its customers include the likes of PayPal, Dell, Nokia and DocuSign itself. These companies use Seal for its contract management tools, but also for its analytics, discovery and data extraction services. And it’s these AI smarts the company developed over time to help businesses analyze their contracts that made DocuSign acquire the company. This can help them significantly reduce their time for legal reviews, for example.

“Seal was built to make finding, analyzing, and extracting data from contracts simpler and faster,” DocuSign CEO John O’Melia said in today’s announcement. “We have a natural synergy with DocuSign, and our team is excited to leverage our AI expertise to help make the Agreement Cloud even smarter. Also, given the company’s scale and expansive vision, becoming part of DocuSign will provide great opportunities for our customers and partners.”

DocuSign says it will continue to sell Seal’s analytics tools. What’s surely more important to DocuSign, though, is that it will also leverage the company’s AI tools to bolster its DocuSign CLM offering. CLM is DocuSign’s service for automating the full contract life cycle, with a graphical interface for creating workflows and collaboration tools for reviewing and tracking changes, among other things. And integration with Seal’s tools, DocuSign argues, will allow it to provide its customers with a “faster, more efficient agreement process,” while Seal’s customers will benefit from deeper integrations with the DocuSign Agreement Cloud.

Powered by WPeMatico

Google Cloud announced today that its new data center in Salt Lake City has opened, making it the 22nd such center the company has opened to date.

This Salt Lake City data center marks the third in the western region, joining LA and The Dalles, Oregon with the goal of providing lower latency compute power across the region.

“We’re committed to building the most secure, high-performance and scalable public cloud, and we continue to make critical infrastructure investments that deliver our cloud services closer to customers that need them the most,” said Jennifer Chason, director of Google Cloud Enterprise for the Western States and Southern California said in a statement.

Cloud vendors in general are trying to open more locations closer to potential customers. This is a similar approach taken by AWS when it announced its LA local zone at AWS re:Invent last year. The idea is to reduce latency by moving compute resources closer to the companies that need them, or to spread workloads across a set of regional resources.

Google also announced that PayPal, a company that was already a customer, has signed a multi-year contract, and will be moving parts of its payment systems into the western region. It’s worth noting that Salt Lake City is also home to a thriving startup scene that could benefit from having a data center located close by.

Google Cloud’s parent company Alphabet recently shared the cloud division’s quarterly earnings for the first time, indicating that it was on a run rate of more than $10 billion. While it still has a long way to go to catch rivals Microsoft and Amazon, as it expands its reach in this fashion, it could help grow that market share.

Powered by WPeMatico

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

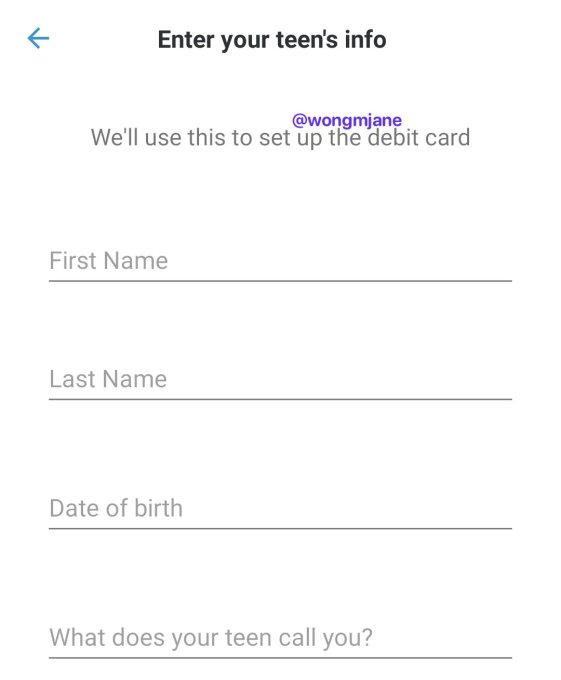

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

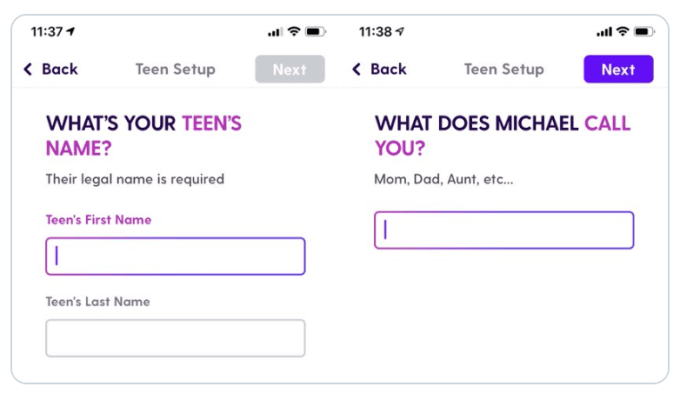

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

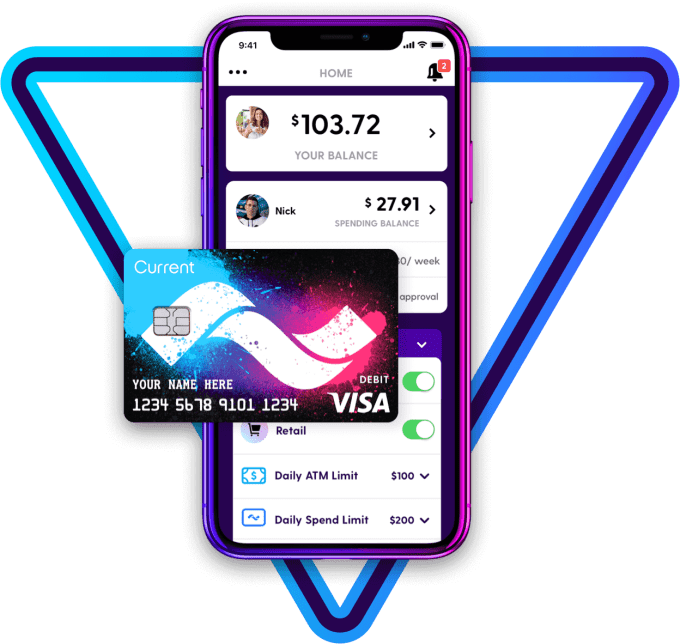

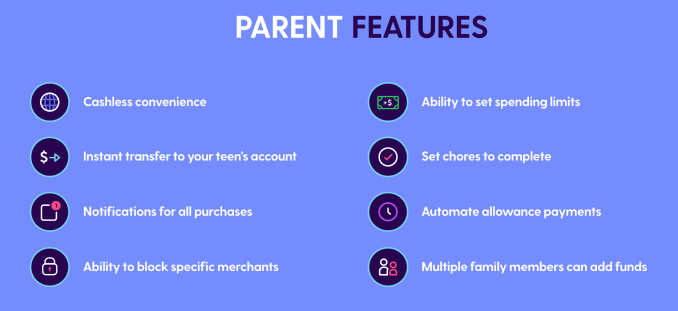

Current’s teen debit card

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

Extra Crunch is excited to announce a new community perk from automated subscription billing startup Chargebee. Starting today, annual and two-year members of Extra Crunch can receive free subscription invoicing until $100,000 in revenue is reached. You must be new to Chargebee to claim this offer.

Chargebee helps you succeed with subscription billing. Chargebee replaces in-house billing systems and spreadsheets by giving teams the ability to set up subscription plans and trials, run pricing experiments at scale, analyze accurate subscription analytics and much more, out of the box.

Chargebee integrates with payment gateways like Stripe, Braintree and PayPal and business applications such as Xero, QuickBooks and Salesforce. You can learn more about the benefits of Chargebee here.

You can sign up for Extra Crunch and claim this deal here.

Extra Crunch is a membership program from TechCrunch that features how-tos and interviews on company building, intelligence on the most disruptive opportunities for startups, an experience on TechCrunch.com that’s free of banner ads, discounts on TechCrunch events, and several community perks like the one mentioned in this article. Our goal is to democratize information for startups, and we’d love to have you join our community.

Sign up for Extra Crunch here.

New annual and two-year Extra Crunch members will receive details on how to claim the perk in the welcome email. The welcome email is sent after signing up for Extra Crunch. If you are already an annual or two-year Extra Crunch member, you will receive an email with the offer at some point over the next 24 hours. If you are currently a monthly Extra Crunch subscriber and want to upgrade to annual in order to claim this deal, head over to the “account” section on TechCrunch.com and click the “upgrade” button.

This is one of several community perks we’ve launched for annual Extra Crunch members. Other community perks include a 20% discount on TechCrunch events, 100,000 Brex rewards points upon credit card sign up and an opportunity to claim $1,000 in AWS credits. For a full list of perks from partners, head here.

If there are other community perks you want to see us add, please let us know by emailing travis@techcrunch.com.

Sign up for an annual Extra Crunch membership today to claim this community perk. You can purchase an annual Extra Crunch membership here.

Disclosure:

This offer is provided as a partnership between TechCrunch and Chargebee, but it is not an endorsement from the TechCrunch editorial team. TechCrunch’s business operations remain separate to ensure editorial integrity.

Powered by WPeMatico

Early Stage SF is around the corner, on April 28 in San Francisco, and we are more than excited for this brand new event. The intimate gathering of founders, VCs, operators and tech industry experts is all about giving founders the tools they need to find success, no matter the challenge ahead of them.

Struggling to understand the legal aspects of running a company, like negotiating cap tables or hiring international talent? We’ve got breakout sessions for that. Wondering how to go about fundraising, from getting your first yes to identifying the right investors to planning the timeline for your fundraise sprint? We’ve got breakout sessions for that. Growth marketing? PR/Media? Building a tech stack? Recruiting?

We. Got. You.

Today, we’re very proud to announce one of our few Main Stage sessions that will be open to all attendees. Reid Hoffman and Sarah Guo will join us for a conversation around “How To Raise Your Series A.”

Reid Hoffman is a legendary entrepreneur and investor in Silicon Valley. He was an Executive VP and founding board member at PayPal before going on to co-found LinkedIn in 2003. He led the company to profitability as CEO before joining Greylock in 2009. He serves on the boards of Airbnb, Apollo Fusion, Aurora, Coda, Convoy, Entrepreneur First, Microsoft, Nauto and Xapo, among others. He’s also an accomplished author, with books like “Blitzscaling,” “The Startup of You” and “The Alliance.”

Sarah Guo has a wealth of experience in the tech world. She started her career in high school at a tech firm founded by her parents, called Casa Systems. She then joined Goldman Sachs, where she invested in growth-stage tech startups such as Zynga and Dropbox, and advised both pre-IPO companies (Workday) and publicly traded firms (Zynga, Netflix and Nvidia). She joined Greylock Partners in 2013 and led the firm’s investment in Cleo, Demisto, Sqreen and Utmost. She has a particular focus on B2B applications, as well as infrastructure, cybersecurity, collaboration tools, AI and healthcare.

The format for Hoffman and Guo’s Main Stage chat will be familiar to folks who have followed the investors. It will be an updated, in-person combination of Hoffman’s famously annotated LinkedIn Series B pitch deck that led to Greylock’s investment, and Sarah Guo’s in-depth breakdown of what she looks for in a pitch.

They’ll lay out a number of universally applicable lessons that folks seeking Series A funding can learn from, tackling each from their own unique perspectives. Hoffman has years of experience in consumer-focused companies, with a special expertise in network effects. Guo is one of the top minds when it comes to investment in enterprise software.

We’re absolutely thrilled about this conversation, and to be honest, the entire Early Stage agenda.

Here’s how it all works:

There will be about 50+ breakout sessions at the event, and attendees will have an opportunity to attend at least seven. The sessions will cover all the core topics confronting early-stage founders — up through Series A — as they build a company, from raising capital to building a team to growth. Each breakout session will be led by notables in the startup world.

Don’t worry about missing a breakout session, because transcripts from each will be available to show attendees. And most of the folks leading the breakout sessions have agreed to hang at the show for at least half the day and participate in CrunchMatch, TechCrunch’s app to connect founders and investors based on shared interests.

Here’s the fine print. Each of the 50+ breakout sessions is limited to around 100 attendees. We expect a lot more attendees, of course, so signups for each session are on a first-come, first-serve basis. Buy your ticket today and you can sign up for the breakouts that we’ve announced. Pass holders will also receive 24-hour advance notice before we announce the next batch. (And yes, you can “drop” a breakout session in favor of a new one, in the event there is a schedule conflict.)

Grab yourself a ticket and start registering for sessions right here. Interested sponsors can hit up the team here.

Powered by WPeMatico

Two co-founders of Google Pay in India are building a neo-banking platform in the country — and they have already secured backing from three top VC funds.

Sujith Narayanan, a veteran payments executive who co-founded Google Pay in India (formerly known as Google Tez), said on Monday that his startup, epiFi, has raised $13.2 million in its Seed financial round led by Sequoia India and Ribbit Capital. The round valued epiFi at about $50 million.

David Velez, the founder of Brazil-based neo-banking giant Nubank, Kunal Shah, who is building his second payments startup CRED in India, and VC fund Hillhouse Capital also participated in the round.

The eight-month-old startup is working on a neo-banking platform that will focus on serving millennials in India, said Narayanan, in an interview with TechCrunch.

“When we were building Google Tez, we realized that a consumer’s financial journey extends beyond digital payments. They want insurance, lending, investment opportunities and multiple products,” he explained.

The idea, in part, is to also help users better understand how they are spending money, and guide them to make better investments and increase their savings, he said.

At this moment, it is unclear what the convergence of all of these features would look like. But Narayanan said epiFi will release an app in a few months.

Working with Narayanan on epiFi is Sumit Gwalani, who serves as the startup’s co-founder and chief product and technology officer. Gwalani previously worked as a director of product management at Google India and helped conceptualize Google Tez. In a joint interview, Gwalani said the startup currently has about two-dozen employees, some of whom have joined from Netflix, Flipkart, and PayPal.

Shailesh Lakhani, Managing Director of Sequoia Capital India, said some of the fundamental consumer banking products such as savings accounts haven’t seen true innovation in many years. “Their vision to reimagine consumer banking, by providing a modern banking product with epiFi, has the potential to bring a step function change in experience for digitally savvy consumers,” he said.

Cash dominates transactions in India today. But New Delhi’s move to invalidate most paper bills in circulation in late 2016 pushed tens of millions of Indians to explore payments app for the first time.

In recent years, scores of startups and Silicon Valley firms have stepped to help Indians pay digitally and secure a range of financial services. And all signs suggest that a significant number of people are now comfortable with mobile payments: More than 100 million users together made over 1 billion digital payments transaction in October last year — a milestone the nation has sustained in the months since.

A handful of startups are also attempting to address some of the challenges that small and medium sized businesses face. Bangalore-based Open, NiYo, and RazorPay provide a range of features such as corporate credit cards, a single dashboard to manage transactions and the ability to automate recurring payouts that traditional banks don’t currently offer. These platforms are also known as neo-bank or challenger banks or alternative banks. Interestingly, most neo-banking platforms in South Asia today serve startups and businesses — not individuals.

Powered by WPeMatico