paypal

Auto Added by WPeMatico

Auto Added by WPeMatico

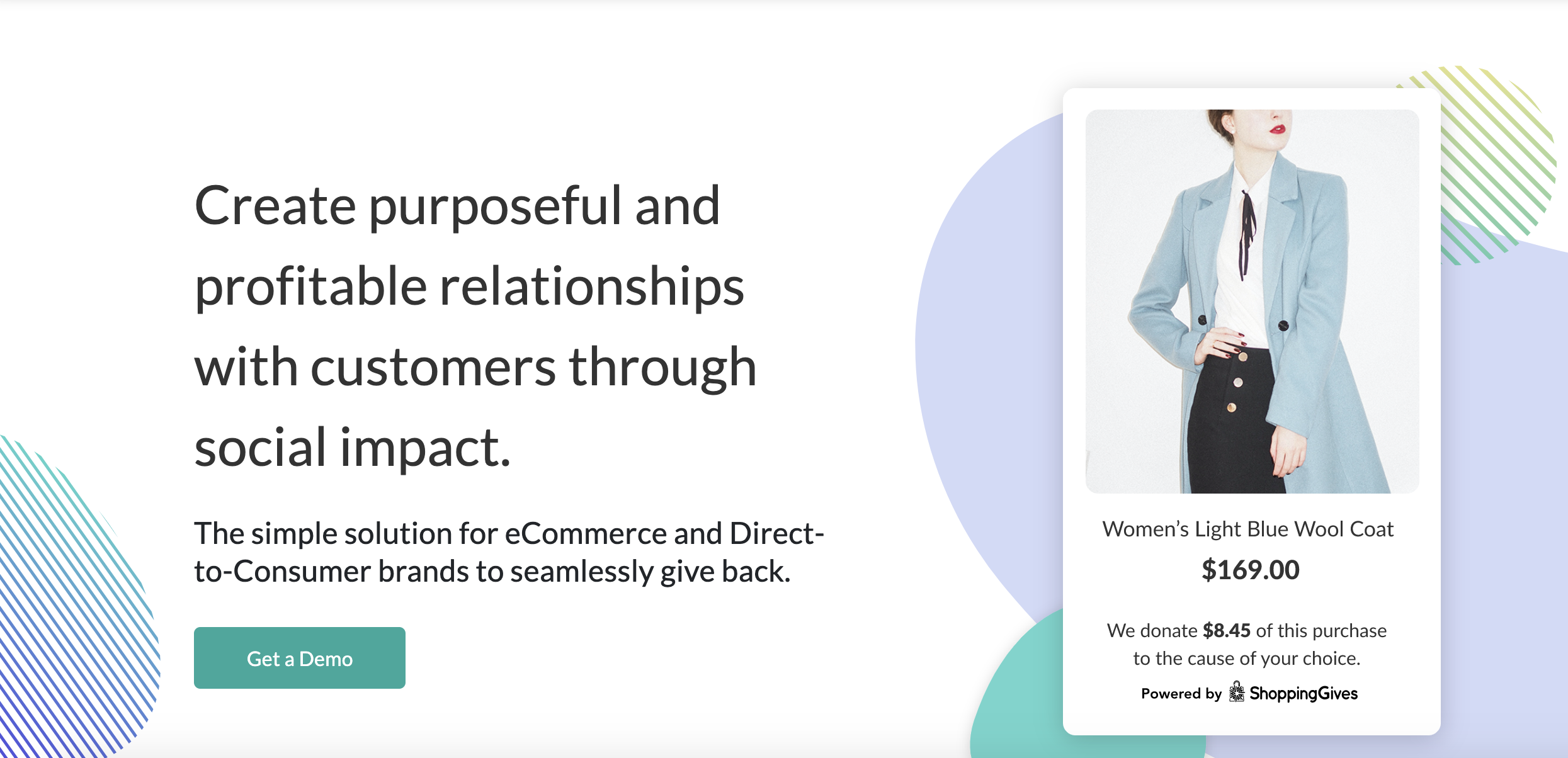

ShoppingGives, a Chicago-based startup pitching retailers a service that can integrate nonprofit donations into their sales and shopping platforms, has raised an undisclosed amount from Serena Williams’ venture capital firm, Serena Ventures, the company said.

ShoppingGives allows retailers to offer a donation on behalf of a shopper to any of over 1.5 million nonprofits that are on its list — all without leaving the retailer’s website.

The company said that retailers can use the donation data to create a more authentic and personalized engagement with customers based on the causes they support.

“ShoppingGives aligned with my values of investing in businesses and entrepreneurs who are making a difference. By creating opportunities to grow social impact with a seamless approach for retailers and brands, ShoppingGives is charting the course for all businesses to stand forth as agents of change in our society,” said Williams in a statement.

The company’s technology helps retailers manage and report donations and is already recommended by Shopify as one of a collection of apps for merchants setting up their online stores. Its service integrates with e-commerce content management systems and is already a partner for the PayPal giving fund.

ShoppingGives has already donated to more than 6,000 nonprofit organizations selected by customers, according to the company. Brands like Kenneth Cole, Natori, White + Warren, Margaux, Solstice Sunglasses, Tomboyx, Fresh Clean Tees, Blind Barber, Huron and Neighborhood Goods use the service already.

Image Credit: ShoppingGives

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Welcome to a special Thanksgiving edition of The Exchange. Today we will be brief. But not silent, as there is much to talk about.

Up top, The Exchange noodled on the Slack-Salesforce deal here, so please catch up if you missed that while eating pie for breakfast yesterday. And, sadly, I have no idea why Palantir is seeing its value skyrocket. Normally we’d discuss it, asking ourselves what its gains could mean for the lower tiers of private SaaS companies. But as its public market movement appears to be an artificial bump in value, we’ll just wait.

Here’s what I want to talk about this fine Saturday: Bloomberg reporting that Stripe is in the market for more money, at a price that could value the company at “more than $70 billion or significantly higher, at as much as $100 billion.”

Hot damn. Stripe would become the first or second most valuable startup in the world at those prices, depending on how you count. Startup is a weird word to use for a company worth that much, but as Stripe is still clinging to the private markets like some sort of liferaft, keeps raising external funds, and is presumably more focused on growth than profitability, it retains the hallmark qualities of a tech startup, so, sure, we can call it one.

Which is odd, because Stripe is a huge concern that could be worth twelve-figures, provided that gets that $100 billion price tag. It’s hard to come up with a good reason for why it’s still private, other than the fact that it can get away with it.

Anyhoo, are those reported, possible prices bonkers? Maybe. But there is some logic to them. Recall that Square and PayPal earnings pointed to strong payments volume in recent quarters, which bodes well for Stripe’s own recent growth. Also note that 14 months ago or so, Stripe was already processing “hundreds of billions of dollars of transactions a year.”

You can do fun math at this juncture. Let’s say Stripe’s processing volume was $200 billion last September, and $400 billion today, thinking of the number as an annualized metric. Stripe charges 2.9% plus $0.30 for a transaction, so let’s call it 3% for the sake of simplicity and being conservative. That math shakes out to a run rate of $12 billion.

Now, the company’s actual numbers could be closer to $100 billion, $150 billion and $4.5 billion, right? And Stripe won’t have the same gross margins as Slack .

But you can start to see why Stripe’s new rumored prices aren’t 100% wild. You can make the multiples work if you are a believer in the company’s growth story. And helping the argument are its public comps. Square’s stock has more than tripled this year. PayPal’s value has more than doubled. Adyen’s shares have almost doubled. That’s the sort of public market pull that can really help a super-late-stage startup looking to raise new capital and secure an aggressive price.

To wrap, Stripe’s possible new valuation could make some sense. The fact that it is still a private company does not.

And speaking of edtech, Equity’s Natasha Mascarenhas and our intrepid producer Chris Gates put together a special ep on the education technology market. You can listen to it here. It’s good.

Hugs and let’s both go do some cardio,

Powered by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

Cashfree, an Indian startup that offers a wide-range of payments services to businesses, has raised $35.3 million in a new financing round as the profitable firm looks to broaden its offering.

The Bangalore-based startup’s Series B was led by London-headquartered private equity firm Apis Partners (which invested through its Growth Fund II), with participation from existing investors Y Combinator and Smilegate Investments. The new round brings the startup’s to-date raise to $42 million.

Cashfree kickstarted its journey in 2015 as a solution for restaurants in Bangalore that needed an efficient way for their delivery personnel to collect cash from customers.

Akash Sinha and Reeju Datta, the founders of Cashfree, did not have any prior experience with payments. When their merchants asked if they could build a service to accept payments online, the founders quickly realized that Cashfree could serve a wider purpose.

In the early days, Cashfree also struggled to court investors, many of whom did not think a payments processing firm could grow big — and do so fast enough. But the startup’s fate changed after Y Combinator accepted its application, even though the founders had missed the deadline and couldn’t arrive to join the batch on time. Y Combinator later financed Cashfree’s seed round.

Fast-forward five years, Cashfree today offers more than a dozen products and services and helps over 55,000 businesses disburse salary to employees, accept payments online, set up recurring payments and settle marketplace commissions.

Some of its customers include financial services startup Cred, online grocer BigBasket, food delivery platform Zomato, insurers HDFC Ergo and Acko and travel ticketing service provider Ixigo. The startup works with several banks and also offers integrations with platforms such as Shopify, PayPal and Amazon Pay.

Based on its offerings, Cashfree today competes with scores of startups, but it has an edge — if not many. Cashfree has been profitable for the past three years, Sinha, who serves as the startup’s chief executive, told TechCrunch in an interview.

“Cashfree has maintained a leadership position in this space and is now going through a period of rapid growth fuelled by the development of unique and innovative products that serve the needs of its customers,” Udayan Goyal, co-founder and a managing partner at Apis, said in a statement.

The startup processed over $12 billion in payments volumes in the financial year that ended in March. Sinha said part of the fresh fund will be deployed in R&D so that Cashfree can scale its technology stack and build more services, including those that can digitize more offline payments for its clients.

Cashfree is also working on building cross-border payments solutions to explore opportunities in emerging markets, he said.

“We still see payments as an evolving industry with its own challenges and we would be investing in next-gen payments as well as banking tech to make payments processing easier and more reliable. With the solid foundation of in-house technologies, tech-driven processes and in-depth industry knowledge, we are confident of growing Cashfree to be the leader in the payments space in India and internationally,” he said.

Powered by WPeMatico

One of my favorite series of Monty Python sketches is built around the concept of surprise:

Chapman: I didn’t expect a kind of Spanish Inquisition.

[JARRING CHORD]

[Three cardinals burst in]

Cardinal Ximénez: NOBODY expects the Spanish Inquisition!

I was reminded of this today when I needed to reschedule a few stories so we could cover DoorDash’s S-1 filing from multiple angles. First, Managing Editor Danny Crichton looked at how well the company’s co-founders and many investors stand to make out. Alex Wilhelm covered the IPO announcement in depth on TechCrunch before writing an Extra Crunch column that studied the role the COVID-19 pandemic played in the home-delivery platform’s recent growth.

Our all-hands-on-deck coverage of DoorDash’s S-1 is a good illustration of Extra Crunch’s mission: timely analysis of current and future technology trends that serves founders and investors. We have a talented team, and as today’s coverage shows, they’re just as good as they are fast.

The stories that follow are an overview of Extra Crunch from the last five days. The full articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thanks very much for reading Extra Crunch this week. I hope you have a great weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Klaus Vedfelt / Getty Images

We frequently run posts by guest contributors, but two stories we published this week were written in the first person, which is a bit of a departure.

In Why I left edtech and got into gaming, Darshan Somashekar brought us inside his decision to pivot away from a sector that’s been growing hotter in 2020.

His post is a unique take on two oft-discussed categories, but it also examines one founder/investor’s thought process when it comes to evaluating new opportunities.

Andy Areitio, a partner at early-stage fund TheVentureCity, wrote What I wish I’d known about venture capital when I was a founder, a reflection on the “classic mistakes” founders tend to make when it’s time to fundraise.

“Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time,” he says. “They can also put all their eggs in one basket too early. I made that mistake.”

You can find business writing that explores best practices anywhere, which is why we hunt down stories that are firmly rooted in data or personal experience (which includes success and failure).

Image Credits: DoorDash

The coronavirus pandemic looms large in DoorDash’s S-1 filing.

According to the food-delivery platform, “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” and “the COVID-19 pandemic has further accelerated these trends.”

As in other sectors, the pandemic didn’t wave a magic wand — instead, it hastened trends that were already in play: consumers love convenience, which means DoorDash’s gross order volume and revenue were tracking well before the virus started to shape our lives.

“It’s your call on how to balance the factors and decide whether or not to buy into the IPO, but this one is going to be big,” writes Alex Wilhelm in a supplemental edition of today’s The Exchange.

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

None of us knew DoorDash would release its S-1 filing today, but Danny Crichton jumped on the story “so we can see who is raking in the returns on the country’s delivery startup champion.”

After estimating the value of the respective ownership stakes held by DoorDash’s four co-founders, he turned to the investors who participated in rounds seed through Series H.

Some growth funds are about to look very good after this IPO, and each founder is looking at hundreds of millions, he found.

But even so, their diminished haul of about $1.3 billion is “a sign of just how much dilution the co-founders took given the sheer amount of capital the company fundraised over its life.”

Image Credits: Nigel Sussman (opens in a new window)

Investors sent stacks of cash to late-stage fintech companies in Q3 2020, but these sizable rounds may also point to shrinking opportunities for early-stage firms, reports Alex Wilhelm in this morning’s edition of The Exchange.

2020 could be a record year for fintech VC in Europe and North America, but are these “huge late-stage dollars” actually “a dampener for new fintech startups trying to get off the ground?”

Devin Coldewey interviewed the leaders of three startup accelerators to learn more about the adaptations they’ve made in recent months:

Due to travel bans, shelter-in-place orders and other unknowns, they’ve all shifted to virtual. But accelerators are intensive programs designed to indoctrinate founders and elicit brutally honest feedback in real time.

Despite the sudden shift, that boot-camp mindset is still in effect, Devin reports.

“Cutting out the commute time in a busy city leaves founders with more time for workshops, mentor matchmaking, pitch practice and other important sessions,” said Fernandez. “Everybody just has more flexibility and tranquility.”

Said Ebersweiler: “People are for some reason more participative and have more feedback than physically — it’s pretty strange.”

Image Credits: Greylock

In a recent interview with Greylock partner Asheem Chandna, Managing Editor Danny Crichton asked him about the buzz around no-code platforms and what’s happening in early-stage enterprise startups before segueing into a discussion about “shift left” security:

“Every organization today wants to bring software to market faster, but they also want to make software more secure,” said Chandna.

“There is a genuine interest today in making the software more secure, so there’s this concept of shift left — bake security into the software.”

Image Credits: Nigel Sussman (opens in a new window)

If you missed Wednesday’s The Exchange, Alex scoured earnings reports from PayPal and Square to see what the near future might hold for several fintech startups currently waiting in the wings.

Using Square and PayPal’s recent numbers for stock purchases, card usage and consumer payment activity as a proxy, he attempts to “see what we can learn, and to which unicorns it might apply.”

Image Credits: jayk7 (opens in a new window)/ Getty Images

In California, non-competition agreements can’t be enforced and a court has ruled that customer contact lists aren’t trade secrets.

That doesn’t mean salespeople who switch jobs can start soliciting their former customers on their first day at the new gig, however.

Before you jump ship — or hire a salesperson who already has — read this overview of California’s trade secret laws.

“Even without litigation, a former employer can significantly hamper a departing salesperson’s career,” says Nick Saenz, a partner at Lewis & Llewellyn LLP, who focuses on employment and trade secret issues.

Image: Bryce Durbin / TechCrunch

News of a highly effective COVID-19 vaccine appeared to drive down prices of the three best-known publicly traded edtech companies: 2U, Chegg and Kahoot saw declines of about 20%, 10% and 9%, respectively after the report.

Are COVID-19 tailwinds dissipating, or did the market make a correction because “edtech has been categorically overhyped in recent months?”

Image Credits: Sophie Alcorn

What does President-elect Biden’s victory mean for U.S. immigration and immigration reform?

I’m in tech in SF and have a lot of friends who are immigrant founders, along with many international teammates at my tech company. What can we look forward to?

— Anticipation in Albany

Powered by WPeMatico

Earnings season is racing past us, with the big ride-hailing companies’ numbers in, all of the Big Five having wrapped their reporting and lots of SaaS numbers in the market. But amidst all the noise, The Exchange has kept an eye on two companies in particular: PayPal and Square.

We’re not really concerned with their overall revenue and profit metrics. Instead, we’ve been hunting around in their numbers for hints and notes about what is going on inside of fintech itself. Why? There are a host of hugely valuable fintech unicorns that have to go public in the future that also share some market space with one or both of our public charges.

What can we learn from looking at what PayPal and Square reported to their own investors?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Lots, it turns out.

As TechCrunch reported when PayPal dropped its Q3 numbers, the public company had bullish results from its Venmo service, payment processing and consumer activity metrics. The numbers pointed to strong consumer adoption of fintech services during the pandemic, something that we presumed was not unique to PayPal itself, but was likely indicative of a generally warm environment for consumer fintech services.

Square continued the trend, posting a set of results that contains nearly all positive data for consumer fintech activity — with one critical caveat for Q4 that we’ll get to at the end.

Square continued the trend, posting a set of results that contains nearly all positive data for consumer fintech activity — with one critical caveat for Q4 that we’ll get to at the end.

Still, what the majors tell us about the fintech space indicates a warmth in activity that explains why Chime, Robinhood and others have had such fun in 2020, accreting tectonic capital to keep their growth hot.

Digging through Square’s earnings gives us a window into consumer payment activity, card usage, stock purchases and more. Let’s see what we can learn, and to which unicorns it might apply.

Let’s start by talking about the broader fintech market before niching down.

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

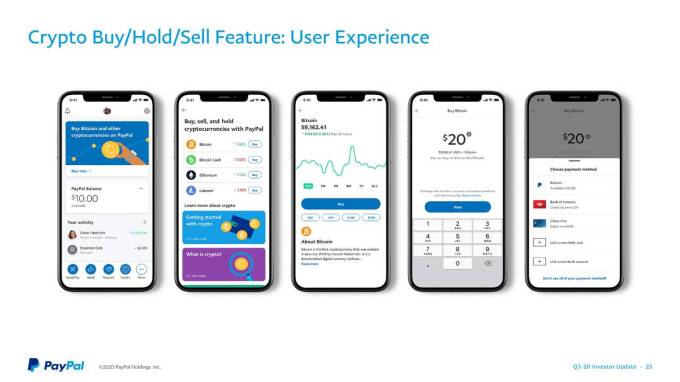

PayPal this week laid out its vision for the future of its digital wallet platform and its PayPal and Venmo apps. During its third-quarter earnings call on Monday, the company said it plans to roll out substantial changes to its mobile apps over the next year to integrate a range of new features, including enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, buy now/pay later functionality and all of Honey’s shopping tools.

While PayPal had spoken in the past about bringing Honey’s capabilities into PayPal, CEO Dan Schulman detailed the integrations PayPal has in store for the deal-finding platform it bought last year for $4 billion, as well as a timetable for both this and the other app updates it has in store.

The Honey acquisition had brought 17 million monthly active users to PayPal. These users turned to Honey’s browser extension and mobile app to find the best savings on items they want to buy, track prices and more.

But today, the Honey experience still remains separate from PayPal itself. That’s something the company wants to change next year.

According to Schulman, the company’s apps will be updated to include Honey’s shopping tools, like its Wish List feature that allows you to track items you want to buy, price monitoring tools that alert you to savings and price drops, plus its deals, coupons and rewards. These tools will become part of PayPal’s checkout solution itself.

That means the company will be able to track the customer from the initial deal-hunting phase where they’re indicating their interest in a certain product, target them with savings and offers, then guide them through its checkout experience all in one place.

PayPal will also provide “anonymous demand data” to merchants based on consumer engagement with Honey’s tools to help them drive sales, the company said.

What’s more, PayPal put timeline on the Honey integrations and the other updates it plans to roll out over the course of the next year.

Bill Pay will start to roll out this month, PayPal said, with a large redesign of the digital wallet experience expected for the first half of 2021. Much of the new functionality will be arriving in the second quarter and the second half of the year, with a goal of having the majority of the changes rolled out by the end of next year.

This also includes PayPal’s plans for cryptocurrencies, announced at the end of October. The company aims to support Bitcoin, Ethereum, Bitcoin Cash and Litecoin at first, initially in the U.S.

Speaking to investors during the earnings call, Schulman also noted when PayPal plans to bring crypto to more users and geographies. He said the ability to buy, sell and hold cryptocurrencies will first arrive in the U.S., then will roll out to international markets and the Venmo app in the first half of next year. (Currently, PayPal is offering U.S. users to join a waitlist for the new crypto features in-app).

Image Credits: PayPal

This change will allow PayPal’s users to shop using cryptocurrencies across the company’s 28 million merchants without requiring additional integrations on merchants’ part. The company explained this is due to how it will handle the settlement process, where users will be able to instantaneously transfer crypto into fiat currency at a set rate when checking out with PayPal merchants.

“This solution will not involve any additional integrations, volatility risk or incremental transaction fees for either consumers or merchants, and will fundamentally bolster the utility of cryptocurrencies,” said Schulman. “This is just the beginning of the opportunities we see as we work hand in hand with regulators to accept new forms of digital currencies,” he added.

PayPal also recently joined the “buy now, pay later” race with its new “Pay in 4” installment program that lets consumers split purchases into four payments. This debuted in France ahead of its late August U.S. launch and has since rolled out to the U.K. (as Pay in 3). This too, will become more integrated into the company’s apps in the months ahead.

Venmo — which the company expects to reach $900 million in revenues next year — will see the expansion of business profiles, and will gain crypto capabilities, more basic financial tools and shopping tools, as well as a revamp of the “Pay with Venmo” checkout experience.

Schulman referred to the company’s plans to overhaul its Venmo and PayPal apps as a “fundamental transformation,” due to how much new functionality they will include as the changes roll out over the next year as well as the new user experience — basically, a redesign — that will allow people to move easily from one experience to the next instead of having to change apps or use a desktop browser, for example.

PayPal’s earnings hadn’t excited Wall Street investors this week, sending the stock down on its lack of 2021 guidance. But the year ahead for PayPal’s digital wallet apps looks to be an interesting one.

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

Max Levchin needs little introduction in the world of tech. As an entrepreneur, he’s been the co-founder of PayPal (now public), Slide (acquired by Google) and Affirm (reportedly about to go public), some of the hottest startups to have come out of Silicon Valley. And as an investor, he’s applied his power of observation and execution also towards helping many others build huge technology businesses.

We sat down with Levchin for a recent session of Extra Crunch Live, where he spoke at length about what he sees as some of the big opportunities in fintech. Here’s an edited version of the conversation. You can watch and listen to the whole discussion — which includes stories about Levchin’s coffee and cycling habits, and how many times he’s seen “The Seven Samurai” (hint: more than once) — here, also embedded below, and you can check out the rest of the pretty cool ECL program here.

Even going as far back as PayPal I think the industry has devolved. I think fintech had the promise of really bringing simplicity, honesty and transparency to the customer. Instead, we ended up putting a really nice user interface on products that are not designed with the user’s best interest in mind. I’m a big fan of throwing shade on credit cards, because I think fundamentally, their business model is remarkably similar to that of payday loans. You are allowed to borrow some money and don’t really know exactly what the terms are. It’s all in the fine print, don’t worry about it and then you just make the minimum payments and you stay in debt. Potentially forever.

Powered by WPeMatico