online lending

Auto Added by WPeMatico

Auto Added by WPeMatico

SellersFunding secured $166.5 million in a combination of Series A equity funding and a credit facility to continue developing its technology and payments platforms for e-commerce businesses.

Northzone led the round and was joined by Endeavor Catalyst and Fasanara. SellersFunding CEO Ricardo Pero did not disclose the funding breakdown, but did say the company previously raised two seed rounds for a total of $40 million in equity and more than $100 million in credit facilities, including one that the company was expanding to $200 million.

SellersFunding, with offices in Florida, New York and London, created a digital platform that delivers financial tools and resources to streamline global commerce for thousands of marketplaces, including working capital, cross-border cash management, tax solutions and business valuation.

Pero got the idea for the company after spending 20 years in the financial industry. He left JP Morgan in 2016 with a drive to start his own company. He was consulting for a friend selling on Amazon who asked him to help make sense of Amazon’s fees and to review the next year’s budget because the friend was struggling to keep up with growth.

“I helped him address the fees issue, but when I went to talk to traditional lenders, I found that they have no clue about e-commerce and the needs of SMEs,” he said.

In addition to being a lending source for businesses selling on these marketplaces, SellersFunding leverages sales data provided by the marketplaces and e-commerce platforms to create sales and cash flow estimates based on the credit limits given to clients so that owners can better understand the fees they are paying and make more informed decisions.

He founded the company in 2017, and today has over 30,000 registered users and is approaching $10 billion in sales volume that is feeding data into SellersFunding’s daily models. The company makes money as both a lender and on fees it charges for payments collected by its customers. Merchants can collect money from marketplaces and pay their suppliers in local or foreign currency.

SellersFunding has consistently grown 300% year over year, Pero said. As such, he intends to use the new funding to scale globally, expand the team, create a marketing budget and look for two small acquisitions in the U.S. and Europe.

The company will continue to invest on the payments side and to promote cross-border payments.

“When I look at the payments landscape, companies are competing on pricing and I don’t think we will ever have a focus there, but instead will compete on customer experience,” Pero added. “Our core business will always be lending and our core investments will be payments and technology, but then we will extend to other services that our clients want.”

With an eye on expanding internationally, it fit to bring on Northzone as a partner, he added. The venture firm is based in Europe and was of a similar vision for thinking globally.

Jeppe Zink, general partner at Northzone, said via email that Pero and his team “are the most experienced in this category” and are building a category leader that is “more experienced and understanding of the lending side than its competitors.”

“We have seen this massive rise in e-shopping, most of the new ones coming from marketplaces like Amazon and Shopify, and if you look at the sellers, thousands are small businesses sourcing their goods which means that they are very important customers,” Zink added. “Normal banks like Barclay can’t check credit. SellersFinding is helping small businesses get this credit, and rightly so. In the same way we thought neobanks won with accounts created when it comes to delivering credit and banking products, they are nowhere to be found yet.”

Powered by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

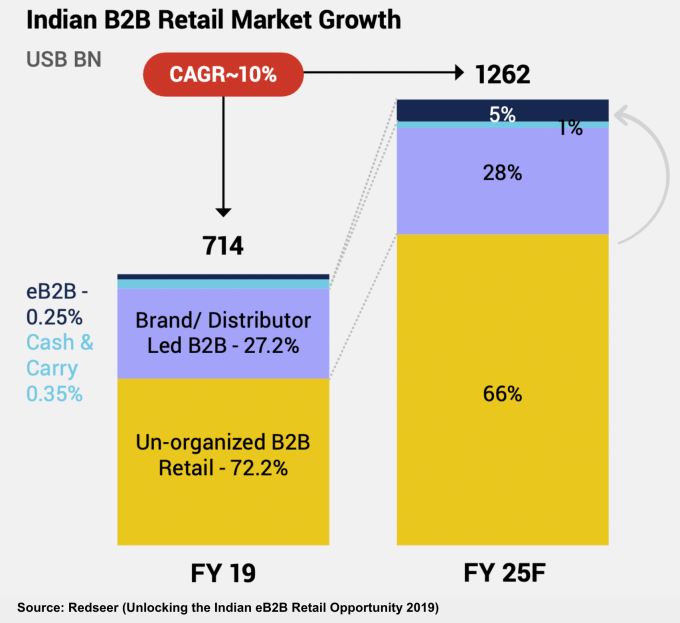

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

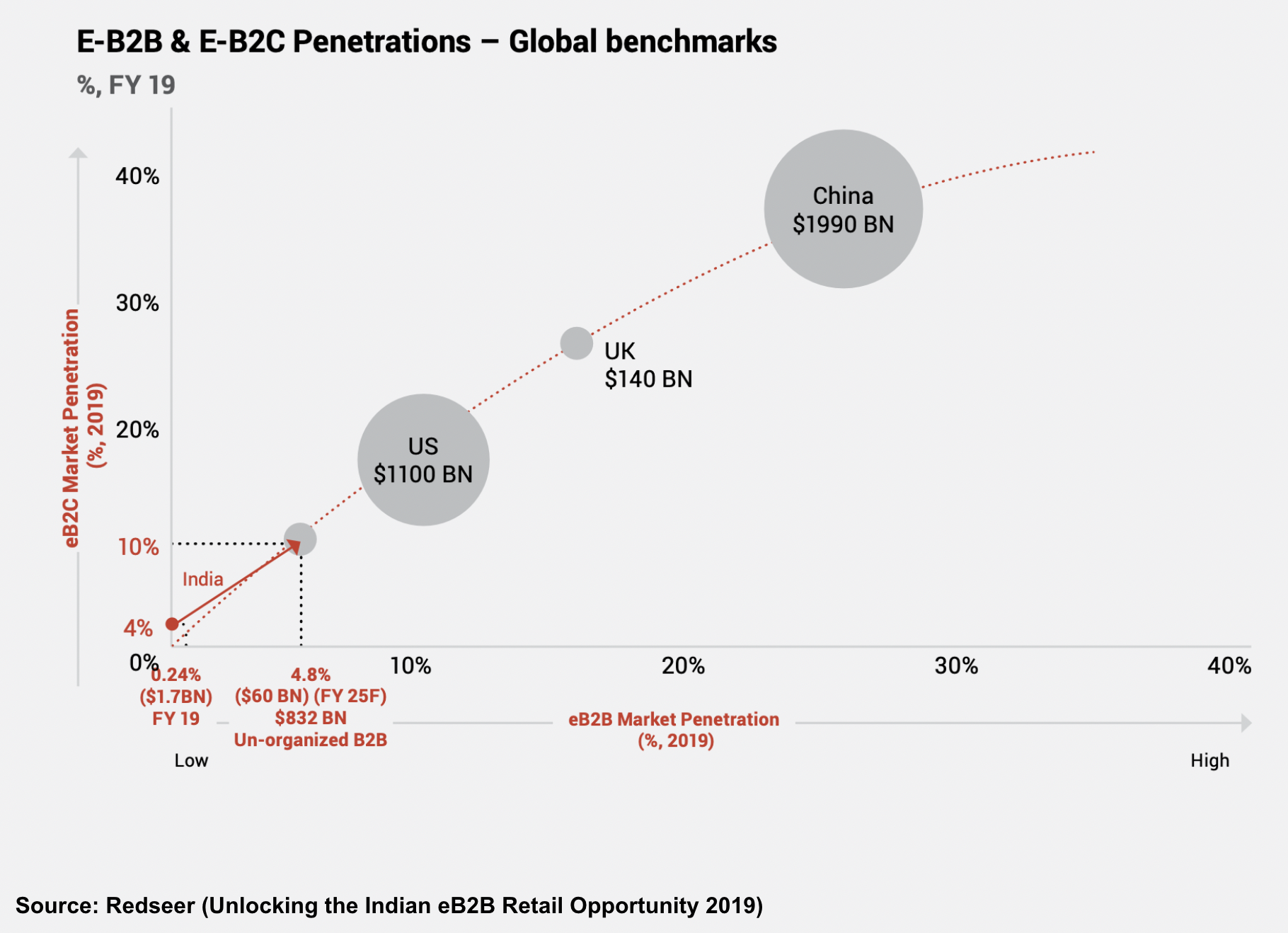

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Kavak, the Mexican startup that’s disrupted the used car market in Mexico and Argentina, today announced its Series D of $485 million, which now values the company at $4 billion. This round more than triples their previous valuation of $1.15 billion, which established them as a unicorn just a couple of months ago in October of 2020. Kavak is now one of the top five highest-valued startups in Latin America.

The round was led by D1 Capital Partners, Founders Fund, Ribbit and BOND, and brings Kavak’s total capital raised to date to more than $900 million. Kavak recently soft-launched in Brazil, and this new round of funding will be used to build out the Brazilian market and beyond, said Carlos García Ottati, Kavak’s CEO and co-founder. The company plans to do a full launch in Brazil in the next 60 days, García said, and we can expect to see Kavak in markets outside Latin America in the next 24 months, he added.

“We were built to solve emerging market problems,” García said.

Kavak, which was founded in 2016, is an online marketplace that aims to bring transparency, security and access to financing to the used car market. The company also offers its own financing through its fintech arm, Kavak Capital, and counts more than 2,500 employees and 20 logistics and reconditioning hubs in Mexico and Argentina.

“In Latin America, 90% of the [used car] transactions are informal, which leads to a 40% fraud rate,” said García, who experienced these challenges firsthand when he moved to Mexico from Colombia a couple of years ago and bought a used car.

“My budget allowed me to buy a used car, but there was no infrastructure around it. It took me six months to buy the car, and then the car had legal and mechanical issues and I lost most of my money,” he said. Kavak buys cars from individuals, refurbishes them and offers warranties to buyers.

“Instead of buying a new car, they can buy a better car that still has all the warranties. It’s a really aspirational process,” said García. The company, which really amounts to four companies in one given its areas of focus, was built to be comprehensive by design in order to meet the various gaps in the market, García said.

“When you’re building a business here [Latin America], you need to build several businesses because so many things are broken,” he said. That’s why the financing option, for example, has been a key to their success, according to García.

Financing has traditionally been hard to come by in Brazil, and as García said, the used car market lacks infrastructure there, too. That being said, Brazil is Latin America’s fintech hub, and the space has made leaps and bounds over the last 7-10 years with companies such as Nubank, PagSeguro, Creditas, PicPay, and others leading the way. As a result, credit cards and loans are more widely available today in the region, offering competition for Kavak Capital. While Kavak has localized some of its product for the Brazilian market — namely building out a Portuguese language version of the app and website — García said the markets are very similar.

“In Brazil, you still have the same problems that you have in Mexico, but Brazil is a little more developed, especially in fintech, which is light years ahead of Mexico,” he said.

With the Brazilian product heading to the races, García said they already have plans for other regions, though he declined to name them.

“80% of people in emerging markets don’t have access to a car,” García said of the global market size. “We want to go into big markets where customers are facing similar problems and where Kavak can really change their lives,” he added.

Powered by WPeMatico

FinanZero, a Brazilian online credit marketplace, announced today that it has closed a $7 million round of funding — its fourth since it launched in 2016. It has raised a total of $22.85 million to date.

The real-time online loan broker allows people to apply for a personal loan, a car equity loan or a home equity loan for free and receive an answer in minutes. A key to FinanZero’s success is that it doesn’t offer the loans itself, but has instead partnered with about 51 banks and fintechs who back the loans.

FinanZero is based in Brazil’s financial capital, São Paulo, and has 52 employees.

“From day one we said, ‘We only work with a success fee,’ so we only get paid when the customer signs the loan contract,” said Olle Widen, the company’s co-founder and CEO.

Instead of charging the customer, FinanZero gets a commission from one of its partners, and with a growing volume of credit applications — an average of 750,000 applications per month — the company has seen 61% revenue growth from 2019-2020.

Olle Widen, co-founder and CEO of FinanZero. Image Credits: FinanZero

The Brazilian finance and banking market has been ripe for disruption, as it has traditionally favored the rich.

Those with low incomes — the vast majority of Brazilian citizens — are then left with few options when it comes to financing, and which in turn forces them into compounding debt from which they’ll likely never escape. Traditionally, young Brazilians have lived with their families until they got married, and while there is a cultural aspect to it, the bottom line is that mortgages were infinitely hard to get approved.

With products like FinanZero and Nubank — Latin America’s largest digital bank — Brazilians are starting to see more economic mobility and independence from the legacy institutions that dictated their lives for so long.

Widen, who is Swedish, moved to Brazil about 10 years ago for personal reasons, and while there, was pitched the idea of FinanZero by Webrock Ventures, an investment company focused on bringing Nordic innovation to Brazil.

At the time, Swedish startup Lendo — a precursor to FinanZero — was making waves in Sweden, and the team felt that a similar model would succeed in Brazil, a country known for its bureaucracy and red tape, and thus primed for a streamlined and hassle-free approach to loans.

The original idea was to just copy Lendo, Widen said, but as others have discovered, along the way the team needed to “tropicalize” the product and the experience, meaning they had to build a custom solution for the Brazilian market and its people.

“The founder of Lendo was a childhood friend of mine,” said Widen, of his close ties to the Swedish fintech.

To apply for a loan on FinanZero you don’t need to provide your credit score. Instead, all you need is a utility bill (proof of address), proof of income and your government ID. The process is so simple, Widen said, that 92% of loan applications are initiated from a smartphone.

“Our business model is very based on the bank’s risk appetite and we saw 60% growth from 2019-2020. We are close to 3 million visits per month, about 1.5 are unique and in March of 2021, we had 800,000 people fill out the entire loan form. We have about a 10% approval rating across all products,” Widen said.

The round was led by the Swedish investors VEF, Dunross & Co, and Atlant Fonder, which are all previous investors in the company. The funding will go toward marketing — most of which will be on T.V. — product development, and talent acquisition.

Powered by WPeMatico

After spending more than a decade disrupting the neighborhood stores in the U.S. and several other markets, Amazon and Walmart are employing an unusual strategy in India to face off this competitor: Friending them.

Walmart and Amazon, both of which face restrictions from New Delhi on what all they could do in India, have partnered with tens of thousands of neighborhood stores in the world’s second-largest internet market this year to leverage the vast presence of these mom and pop stores.

In June this year, at the height of the pandemic, Amazon announced “Smart Stores.” Through this India-specific program, for instance, Amazon is providing physical stores with software to maintain a digital log of the inventory they have in the shop and supplying them with a QR code.

When consumers walk to the store and scan this QR code with the Amazon app, they see everything the shop has to offer, in addition to any discounts and past reviews from customers. They can select the items and pay for it using Amazon Pay. Amazon Pay in India supports a range of payments services, including the popular UPI, and debit and credit cards.

The world’s largest e-commerce giant also maintains partnerships that allow it to turn tens of thousands of neighborhood stores as its delivery point for customers — and sometimes even rely on them for inventory.

India has over 60 million small businesses that dot the thousands of cities, towns and villages across the country. These mom and pop stores offer all kinds of items, are family run, and pay low wages and little to no rent.

This has enabled them to operate at an economics that is better than most — if not all — of their digital counterparts, and their scale allows them to offer unmatched fast delivery.

Krishna Shah, a New Delhi-based doctor, on paper is one of the perfect customers of e-commerce services. She lives in an urban city, uses digital payments apps and her earnings put her in the top 5% income level in the country. Yet, when she needed to buy food for her cats and needed it as soon as possible, she realized the major giants would take hours, if not longer. She ended up placing a call to a neighborhood store, which delivered the item within 10 minutes.

That neighborhood store, which employs fewer than half a dozen people, was competing with over a dozen giants and heavily funded startups including Grofers and BigBasket — and it won.

At stake is India’s retail market, which is estimated to be worth $1.3 trillion by 2025, from about $700 billion last year, according to Boston Consulting Group and the Retailers’ Association India. E-commerce, by several estimates, accounts for just 3% of the retail market in the country.

If that figure wasn’t small enough already, consider this: Some of the biggest customers of Flipkart and Amazon are these small retail stores. An executive with direct knowledge of the matter told TechCrunch that during some sales, as high as 40% of all smartphone units are bought by physical stores. The idea is, the executive said, to buy the devices at a discounted price, sit on them for a few days and when Amazon and Flipkart are done with their sales, sell the same phones at their standard prices.

Sujeet Kumar, co-founder of Udaan, a Bangalore-based startup that works with merchants, said that even as smartphones and the internet have reached all corners of India, e-commerce hasn’t been able to disrupt the retail market.

“The problem is that it is very difficult for e-commerce companies to build a supply chain and distribution network that is more efficient than those established by neighborhood stores. These mom and pop stores operate on an insanely different kind of cost economics. E-commerce companies are not able to match it,” he said.

Powered by WPeMatico

While the world awaits the Airbnb IPO filing that could come as early as next week, Upstart dropped its own S-1 filing. The fintech startup facilitates loans between consumers and partner banks, an operation that attracted around $144 million in capital prior to its IPO.

First Round Capital, Khosla Ventures, Third Point Ventures, Rakuten and The Progressive Corporation led rounds in the startup, according to Crunchbase data.

There’s quite a lot to like in Upstart’s IPO filing, including rapidly advancing revenues and recent profitable period. However, the company’s revenue concentration could be a concern to some investors who recall what recently happened to Fastly shares after losing a large customer.

PitchBook data indicates that the company was last valued at $750 million thanks to its 2019 Series D worth $50 million. Can Upstart reach unicorn status with its IPO? Let’s peek at the numbers and try to answer the question.

Upstart’s technology uses what it describes as artificial intelligence (AI) to approve consumer loans. It collects consumer demand for credit and connects that demand to bank partners who fund the loans. The company’s AI-powered credit tool can give consumers “higher approval rates [and] lower interest rates,” according to its S-1 filing, which offers banks “access to new customers, lower fraud and loss rates, and increased automation.”

If Upstart’s AI tool can, in fact, more intelligently determine consumer creditworthiness, everyone could come out a winner, with consumers paying less and banks adding to their loan books without taking on outsized risk.

Powered by WPeMatico

The global legal services industry was worth $849 billion in 2017 and is expected to become a trillion-dollar industry by the end of next year. Little wonder that Steno, an LA-based startup, wants a piece.

Like most legal services outfits, what it offers are ways for law practices to run more smoothly, including in a world where fewer people are meeting in conference rooms and courthouses and operating instead from disparate locations.

Steno first launched with an offering that centers on court reporting. It lines up court reporters, as well as pays them, removing both potential headaches from lawyers’ to-do lists.

More recently, the startup has added offerings like a remote deposition videoconferencing platform that it insists is not only secure but can manage exhibit handling and other details in ways meant to meet specific legal needs.

It also, very notably, has a lending product that enables lawyers to take depositions without paying until a case is resolved, which can take a year or two. The idea is to free attorneys’ financial resources — including so they can take on other clients — until there’s a payout. Of course, the product is also a potentially lucrative one for Steno, as are most lending products.

We talked earlier this week with the company, which just closed on a $3.5 million seed round led by First Round Capital (it has now raised $5 million altogether).

Unsurprisingly, one of its founders is a lawyer named Dylan Ruga who works as a trial attorney at an LA-based law group and knows first-hand the biggest pain points for his peers.

More surprising is his co-founder, Gregory Hong, who previously co-founded the restaurant reservation platform Reserve, which was acquired by Resy, which was acquired by American Express. How did Hong make the leap from one industry to a seemingly very different one?

Hong says he might not have gravitated to the idea if not for Ruga, who was Resy’s trademark attorney and who happened to send Hong the pitch behind Steno to get Hong’s advice. He looked it over as a favor, then he asked to get involved. “I just thought, ‘This is a unique and interesting opportunity,’ and said, ‘Dylan, let me run this.’ ”

Today the 19-month-old startup has 20 full-time employees and another 10 part-time staffers. One major accelerant to the business has been the pandemic, suggests Hong. Turns out tech-enabled legal support services become even more attractive when lawyers and everyone else in the ecosystem is socially distancing.

Hong suggests that Steno’s idea to marry its services with financing is gaining adherents, too, including amid law groups like JML Law and Simon Law Group, both of which focus largely on personal injury cases.

Indeed, Steno charges — and provides financing — on a per-transaction basis right now, even while its revenue is “somewhat recurring,” in that its customers constantly have court cases.

Still, a subscription product is being considered, says Hong. So are other uses for its videoconferencing platform. In the meantime, says Hong, Steno’s tech is “built very well” for legal services, and that’s where it plans to remain focused.

Powered by WPeMatico

The economic effects of COVID-19 could delay Africa’s next big IPO — that of Nigerian fintech unicorn Interswitch.

If so, it wouldn’t be the first time the Lagos-based payments company’s plans for going public were postponed; the tech world has been anticipating Interswitch’s stock market debut since 2016.

For the continent’s innovation ecosystem, there’s a lot riding on the digital finance company’s IPO. After e-commerce venture Jumia, it would become only the second listing of a VC-backed African tech company on a major exchange. And Interswitch’s stock market debut — when it occurs — could bring more investor attention and less controversy to the region’s startup scene.

TechCrunch reached out to Interswitch on the window for listing, but the company declined to comment. The tech firm’s path from startup to IPO aspirant traces back to the vision of founder Mitchell Elegbe, a Nigerian electrical engineering graduate whose entire career has pretty much been Interswitch.

Africa’s tech scene is still fairly young, but it does have a timeline with several definitive points. An early one would be the success of mobile money in East Africa, with the launch of Safaricom’s M-Pesa in 2007. Another is the notable wave of VC-backed startups and founders that launched around 2010.

Interswitch CEO Mitchell Elegbe (Photo Credits: Interswitch)

With Interswtich, Elegbe pre-dated both by a number of years, founding his fintech company back in 2002 to connect Nigeria’s largely disconnected banking system. The firm became a pioneer of the infrastructure to digitize Nigeria’s economy.

Interswitch created the first electronic switch whereby Nigerian financial institutions could communicate and thereby operate ATMs and point of sales operations. The company now provides much of the rails for Nigeria’s online banking system.

Powered by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico