online lending

Auto Added by WPeMatico

Auto Added by WPeMatico

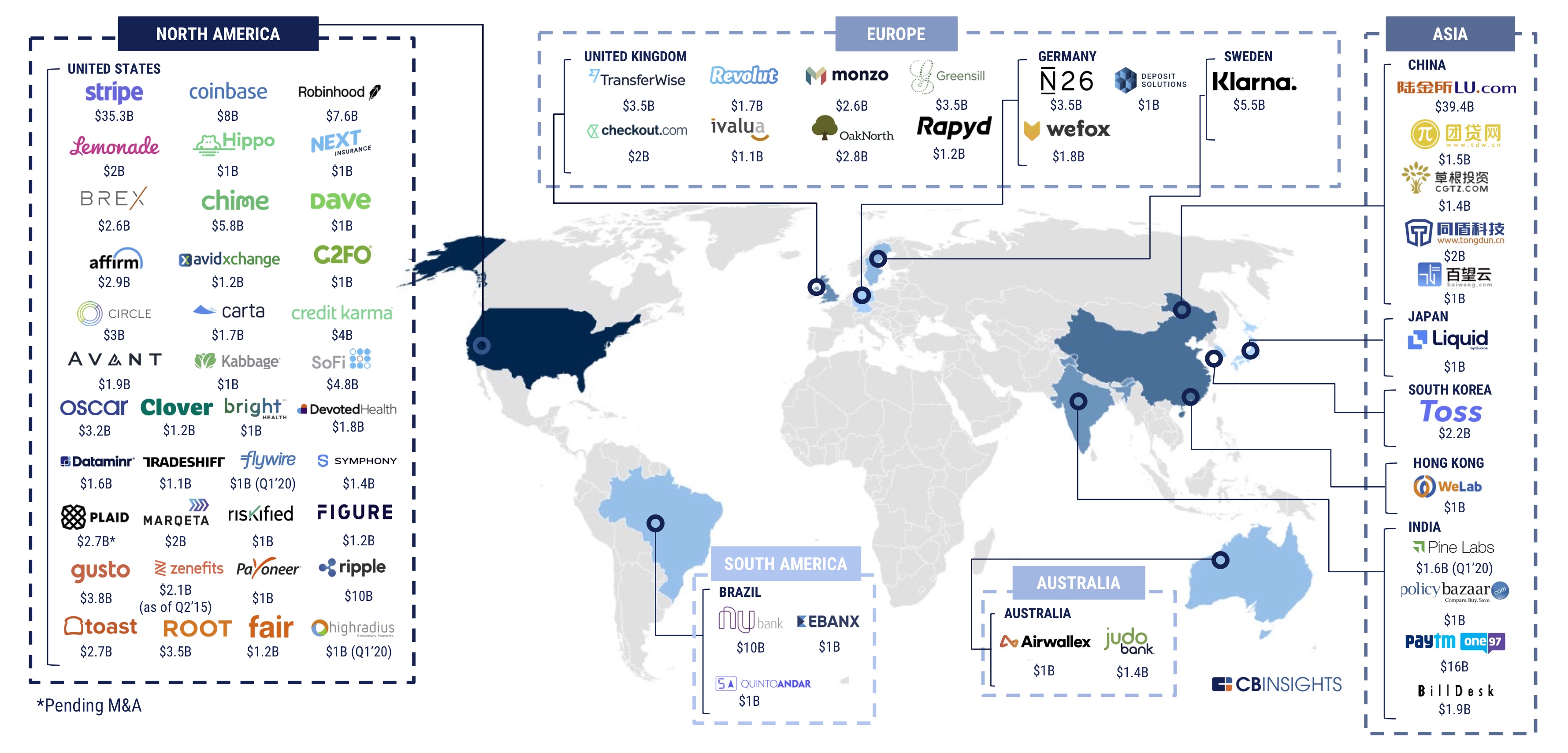

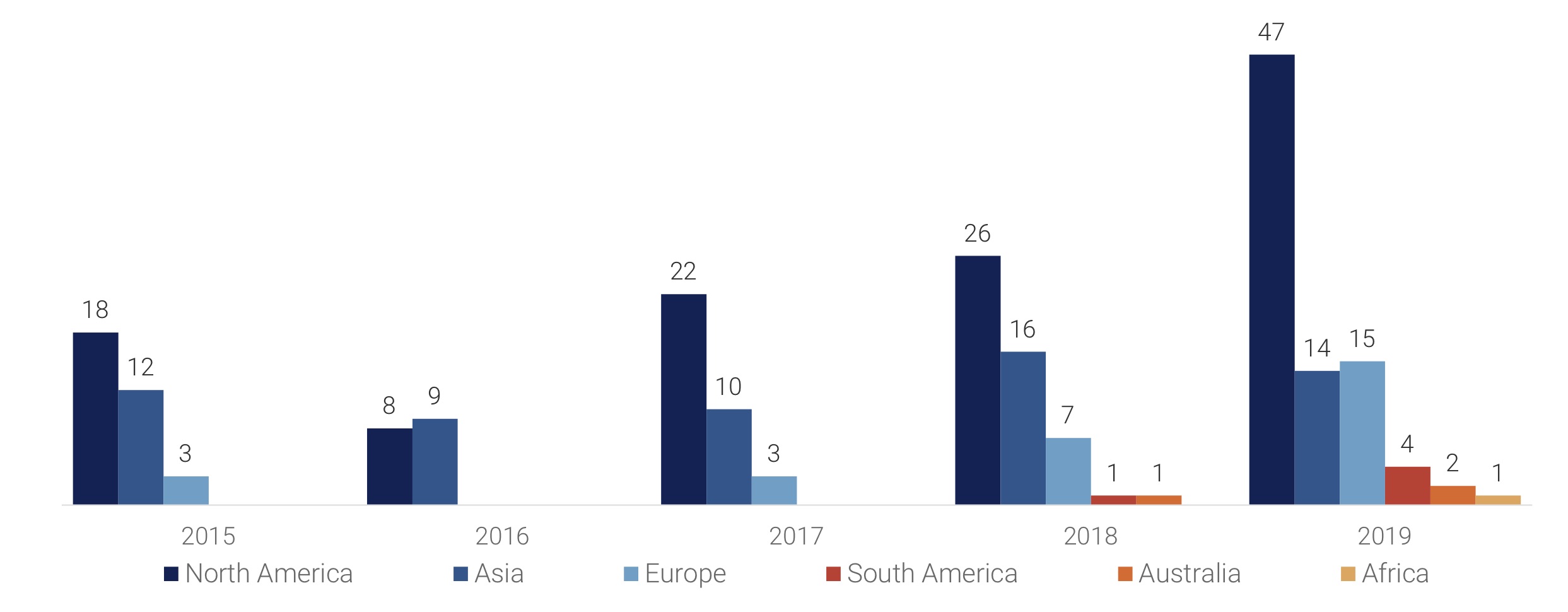

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

Two years ago, we created the Matrix FinTech Index to highlight what we saw as the beginnings of a 10+ year mega innovation wave in financial services.

The trillion-dollar financial services industry was going to be turned on its head over the next decade, and we were just getting started. At the time, the top 10 publicly traded U.S. fintech companies had just surpassed the $100 billion mark in terms of total market capitalization, 12 unicorns had emerged in the category, and the U.S. VC industry had just poured in $6.7B — a record at the time.

As we predicted last year, the innovation cycle continues, and we are transitioning into its mid-phase. So what happened in U.S. fintech in 2019? In short, monster growth.

On the public side, fintechs delivered resoundingly. PayPal alone gained $26B in market capitalization. On a return basis, the public Matrix FinTech Index continued to crush every major equity index as well as the financial services incumbents. Nicely matching our forecasts, our Index delivered 213% returns over the last three years. The Index outperformed the financial services incumbents by 151 percentage points and the S&P 500 by 170 percentage points.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today, we’re exploring fundraising from outside the venture world.

Founders looking to raise capital to power their growing companies have more options than ever. Traditional bank loans are an option, of course. As is venture capital. But between the two exists a growing world of firms and funds looking to put capital to work in young companies that have growing revenues and predictable economics.

Firms like Clearbanc are rising to meet demand for capital with more risk appetite than a traditional bank looking for collateral, but less than an early-stage venture firm. Clearbanc offers growth-focused capital to ecommerce and consumer SaaS companies for a flat fee, repaid out of future revenues. Such revenue-based financing is becoming increasingly popular; you could say the category has roots in the sort of venture debt that groups like Silicon Valley Bank have lent for decades, but there’s more of it than ever and in different flavors.

While revenue-based financing, speaking generally, is attractive to SaaS and ecommerce companies, other types of startups can benefit from alt-capital sources as well. And, some firms that disburse money to growing companies without an explicit equity stake are finding a way to connect capital to them.

Today, let’s take a quick peek at three firms that have found interesting takes on providing alternative startup financing: Earnest Capital with its innovative SEAL agreement, RevUp Capital, which offers services along with non-equity capital, and Capital, which both invests and loans using its own proprietary rubric.

After all, selling equity in your company to fund sales and marketing costs might not be the most efficient way to finance growth; if you know you are going to get $3 out from $1 in spend, why sell forever shares to do so?

Before we dig in, there are many players in what we might call the alt-VC space. Lighter Capital came up again and again in emails from founders. Indie.vc has its own model that is pretty neat as well. In honor of starting somewhere, however, we’re kicking off with Earnest, RevUp and Capital. We’ll dive into more players in time. (As always, email me if you have something to share.)

Powered by WPeMatico

This time it actually has insurance. Zero-fee stock-trading app Robinhood is launching Cash Management, a new feature that earns users 2.05% APY interest on uninvested money in their account with the ability to spend it through a special Mastercard debit card. The waitlist opens today in the U.S. with the first users to be admitted soon. “If you have $5,000 in your account while you’re thinking about what to invest in, you’d have an extra $105 at the end of the year” thanks to Robinhood Cash Management’s interest, co-CEO Baiju Bhatt tells me.

The $7.6 billion-valuation startup first attempted something similar in December with Robinhood Checking, promising a stunningly tall 3% interest rate. But the product turned into a PR disaster when the Securities Investor Protection Corporation that was supposed to insure users’ funds declared Robinhood ineligible, with its CEO noting it had never agreed to cover checking accounts. That led Robinhood to shelve the feature, scrub its site of any mention of Checking and apologize.

Robinhood Cash Management’s debit cards, featuring the same design from the scrapped Checking launch

Now despite Bhatt claiming “Cash Management is a brand new program built from the ground up,” it will offer the same debit card design and network of 75,000 ATMs. It’s even using an identical promo image for its half-translucent green, black, white and American flag debit card designs. But each user’s funds will be covered by the Federal Deposit Insurance Corporation up to $1.25 million. To get around the $250,000 FDIC limit per bank, Robinhood is partnering with six banks that it will spread a user’s cash across as necessary to bundle up to that sum. Robinhood earns money by taking a chunk of the interchange fees from transactions on its debit card run in partnership with Sutton Bank, and from a fee paid by the six banks cash gets swept into.

To help it avoid further regulatory missteps, Robinhood yesterday added former SEC commissioner Dan Gallagher as its first independent board member. He joins the startup’s recently hired COO, CFO, chief compliance officer, VP of Risk & Compliance and VP of Legal & Regulatory to bring more supervision to Robinhood.

Robinhood co-founders and co-CEOs (from left): Baiju Bhatt and Vlad Tenev

The opt-in feature prevents users from missing out on earning interest if they keep money in their Robinhood account, and makes funds from stock sales quickly accessible via the debit card for spending or withdrawal. That convenience could give Robinhood an edge as its loses one if its key differentiators. Last week, its top incumbent competitors Charles Schwab, E*Trade and AmeriTrade all dropped their $4.95 to $6.95 fees on stock trades to match Robinhood’s free offering. That makes Cash Management and Robinhood Crypto even more critical to its continued growth. That’s necessary to justify the $7.6 billion valuation from its recent $323 million Series E raise led by DST Global that brings it to $860 million in total funding.

“We decided the best thing to do is giving people the peace of mind that their money is held at these banks, while trying to pay back the very best interest rates,” Bhatt tells me. [Disclosure: I know Robinhood’s co-founders from college.]

With Cash Management, once users deposit cash into the Robinhood accounts and opt into the program, they’re eligible to earn interest. Any balance on their account, including returns from sales of securities or cryptocurrencies, is swept into the FDIC-insured partner banks via Promontory’s debit suite system. Those banks include Wells Fargo, HSBC, Goldman Sachs, Citibank, U.S. Bank and Bank of Baroda. If one of those banks folds, the FDIC will make customers whole for up to $250,000, equaling $1.25 million across all six working with Robinhood. Users are able to opt out of specific banks.

There the cash earns a variable annual percentage yield (APY) that may fluctuate based on market factors like the Fed fund’s rate. Currently Robinhood offers a 2.05% APY, but refused to compare it to competitors. However, it ranks relatively high amongst popular banking options like these, according to Bankrate, especially given it has no minimum balance:

Robinhood Cash Management will also compete directly with Wealthfront Cash that launched in February and now offers 2.07% APY interest, but lacks a debit card or ATMs. Betterment Checking & Savings does provide a Visa debit card, but its current APY is 1.79%.

Cash Management users can select from the four debit card styles that are accepted anywhere that takes Mastercard, plus 75,000 ATMs. It also works with Apple Pay, Google Pay and Samsung Pay. There are no foreign transaction fees, maintenance fees or account minimum.

A variety of new Cash Management features are being added to the Robinhood app. You can get notifications and emails for all your transactions, and lock the card from your phone if you suspect fraud. You also can opt for location protection, which alerts you if your card is used too far away from your phone. An in-app ATM finder shows users where they can get cash without a fee.

“Partially we want this to be a good business but we also want this to be a big part of customer’s lives,” says Robinhood VP of product Josh Elman. Instead of nickel and diming Cash Management users, the startup monetizes by charging its partners. But the bigger strategy is to get more users on Robinhood in hopes some will subscribe to Robinhood Gold. There users pay a variable monthly fee depending on how much they want to borrow from the startup to trade on margin.

Robinhood co-CEO Baiju Bhatt speaks with TechCrunch’s Josh Constine at Disrupt SF 2018

“I think the main takeaway over the last year has been that since last December, our company has been very committed to building an organization that has a really strong culture [of compliance]” Bhatt concludes. “We’ve grown the leadership team over the last year with experience from risk and finance backgrounds. We think that’s reflected pretty clearly in how Robinhood operates and the diligence that went into building this new program.”

No longer a scrappy startup, the budding fintech giant must now grapple with much greater regulatory scrutiny. With more than 6 million users, the SEC won’t stand for it putting people’s finances in in jeopardy.

Powered by WPeMatico

Indian mobile payments firm MobiKwik has reached a milestone very few of its local rivals can even contemplate: not burning money. The 10-year-old Gurgaon-headquartered firm said Tuesday it is now generating a profit excluding interest, taxes, depreciation and amortization.

“We have been in an ecosystem where we have seen a lot of high-growth and several regulatory changes in the payments domain. But what we realized was that payments alone is likely not going to be a very profitable business,” Bipin Singh, co-founder and CEO of MobiKwik, told TechCrunch in an interview.

To get to the path of profitability, MobiKwik has made a number of significant changes to its business in recent years. It stopped participating in the race to aggressively acquire users and fighting with heavily backed firms such as Paytm, which has raised more than $2 billion to date.

Paytm remains unprofitable and an analysis of its financial performance shows that this is not going to change anytime soon. Google, which also offers a payments service in India, has no shortage of cash, either. MobiKwik has raised about $118 million to date from Sequoia Capital, American Express and Cisco Investments, among others.

Upasana Taku, co-founder and COO of MobiKwik, said the company has taken inspiration from Kotak and ICICI banks, both of which have about 15 million to 20 million customers — a fraction of many digital payment apps — but are profitable. MobiKwik, which employs 400 people, has 110 million users, she said.

In the last two and a half years, MobiKwik has cut down on cashbacks it bandies out to users — a practice followed by every company offering a payments solution in India — and focused on building financial services on top of its wallet app to retain customers and find additional sources of revenue.

The company continues to focus on its mobile wallet and payments processing businesses that account for about 75% of its revenue, but its growing suite of financial services, such as providing credits and insurance to customers, is already bringing the rest of the revenue, she said.

That’s not surprising, as India remains alarmingly under served. Fewer than 50 million credit cards are in circulation in the nation currently, and for people with limited income, getting a loan of any size remains a major challenge.

“Even the population that has access to smartphones and cheap internet data can’t get a credit card in India. We found it a good match for the growth of our payments app. We started serving these users who have the discipline to repay money and have certain kind of income,” the couple said, who are now also donning the role of angel investors.

MobiKwik works with banks and other lenders to finance loans between Rs 5,000 ($69) to Rs 100,000 ($1,380). In the 18 months since it started offering this, MobiKwik has provided 800,000 loans and disbursed $100 million.

In late 2018, the company launched “sachet-sized” insurance plans to provide protection from cyber fraud, fire, accident and hospitalization. These sachets start at as little as Rs 20 (28 cents) and thousands of users buy these everyday. Similarly, it also allows users to buy mutual funds for as little as $1.30.

MobiKwik expects its revenue to hit $69 million in the financial year that ends in March next year, up from $28 million a year earlier. The company, which expects to turn fully profitable by fiscal year 2021, plans to go public in four to five years, Taku said.

MobiKwik competes with a number of players, many of which are increasingly adding financial services, such as loans, to their platforms. Since these digital platforms are able to process loans without the need of salespeople and support staff, it becomes feasible for banks to chase customers with weak financial power.

India’s overall retail credit demand is expected to grow 60% to $771 billion over the next four years, according to the Digital Lenders Association of India.

Powered by WPeMatico

Indifi, a Gurgaon-based startup that offers loans to small and medium-sized businesses and also operates an online lending marketplace, has raised 1,450 million Indian rupees ($20.4 million) in a new financing round to expand its business in the country.

The Series C round for the four-year-old startup was led by CDC Group, a U.K.-government-owned VC fund. Existing investors Accel, Elevar Equity, Omidyar Networks and Flourish Ventures also participated in the round, the startup announced on Tuesday (Indian Standard Time).

Indifi, which has raised about $34 million in venture capital to date, has also relied on debt to grow and finance loans on its platform. Currently, it’s in about $21 million in debt, Alok Mittal, co-founder and managing director of Indifi, told TechCrunch in an interview.

Indifi, which itself finances some loans, additionally also serves as a marketplace for banks and non-banking financial companies to participate in funding loans to small and medium-sized enterprises, said Mittal. Both the businesses are equally growing and contributing to its bottom line, he said.

A typical loan processed by Indifi is of about $7,000 in size. Overall, the startup offers between $1,400 to $70,000 in capital to businesses.

Unlike banks and many other online lenders, Indifi works with an ecosystem of companies to assess risk factors before granting a loan to a business, Mittal said. For instance, Indifi works with food-delivery startups Zomato and Swiggy and checks a restaurant’s history and feedback from their customers before issuing to a restaurant.

Similarly, if an enterprise from the travel industry were to look for a loan, Indifi checks the volatility of the market. Some of its other business partners include Oyo Rooms, MakeMyTrip, Flipkart, FirstData, Travel Booking and Riya Travel.

“We chose to invest in Indifi because of its advanced data-driven approach that enables it to reach [thousands] of underserved customers across India. By reducing the high cost of risk assessment and customer acquisition, Indifi helps formal and informal businesses to access growth finance that otherwise may not receive it,” Srini Nagarajan, managing director and head of CDC Group’s Asia business, said in a statement.

Despite its longer background check process, Mittal said Indifi has been able to finance nearly 50% of all the applications it gets, compared to about 10% deals that materialize with banks and other lenders.

Indifi, which spent the first year and a half of its existence building relationships with major companies and refining its products, has amassed more than 15,000 customers to date, Mittal said. Its client base has grown by 2.5 times in the past year, he said.

The startup will use the fresh capital to find new clients and lending partners to expand its marketplace business, Mittal said. It will also explore lending to businesses in more sectors, including logistics (so fleet-owners could also get loan).

Indifi competes with a handful of businesses, including Bangalore-based Zest Money, Five Star Finance, Capital Float and, in some capacity, Drip Capital, which recently raised $25 million.

Powered by WPeMatico

Aspire, a Singapore-based startup that helps SMEs secure working capital, has raised $32.5 million in a new financing round to expand its presence in several Southeast Asian markets.

The Series A round for the one-and-a-half-year-old startup was funded by MassMutual Ventures Southeast Asia. Arc Labs and existing investors Y Combinator — Aspire graduated from YC last year — Hummingbird and Picus Capital also participated in the round. Aspire has raised about $41.5 million to date.

Aspire operates a neo-banking-like platform to help small and medium-sized enterprises (SMEs) quickly and easily secure working capital of up to about $70,000. AspireAccount, the startup’s flagship product, provides merchants and startups with instant credit limit for daily business expenses, as well as a business-to-business acceptance and other tools to help them manage their cash flow.

Co-founder and CEO Andrea Baronchelli tells TechCrunch that about 1,000 business accounts are opened each month on Aspire and that the company plans to continue focusing on Southeast Asia, where he says there are about 78 million small businesses, leaving plenty of room to scale (applications can be made through Aspire’s mobile app and are reviewed using a proprietary risk assessment engine before getting final approval from a human). Aspire claims it has seen 30% month-over-month growth since it was founded in January 2018 and expects to open more than 100,000 business accounts by next year.

Baronchelli, who served as a CMO for Alibaba’s Lazada platform for four years, says Aspire launched to close the gap left by the traditional banking industry’s focus on consumer services or businesses that make more than $10 million in revenue a year. As a result, smaller businesses in Southeast Asia, including online vendors and startups, often lack access to credit lines, accounts and other financial services tailored to their needs.

Aspire currently operates in Thailand, Indonesia, Singapore and Vietnam. The startup said it will use the fresh capital to scale its footprints in those markets. Additionally, Aspire is building a scalable marketplace banking infrastructure that will use third-party financial service providers to “create a unique digital banking experience for its SME customers.”

Baronchelli adds that “the bank of the future will probably be a marketplace,” so Aspire’s goal is to provide a place where SMEs can not only open accounts and credit cards, but also pick from different services like point of sale systems. It is currently in talks with potential partners. The startup is also working on a business credit card that will be linked to each business account by as early as this year.

Southeast Asia’s digital economy is slated to grow more than six-fold to reach more than $200 billion per year, according to a report co-authored by Google. But for many emerging startups and businesses, getting financial services from a bank and securing working capital have become major pain points.

A growing number of startups are beginning to address these SMEs’ needs. In India, for instance, NiYo Bank and Open have amassed millions of businesses through their neo-banking platforms. Both of these startups have raised tens of millions of dollars in recent months. Drip Capital, which helps businesses in developing markets secure working capital, raised $25 million last week.

Powered by WPeMatico

Paytm, India’s largest mobile wallet app, has branched out to several businesses in recent years as threat from Google and Facebook grows. On Tuesday, it added another category to the list: credit cards.

The firm, operated by One97 Communications, today unveiled Paytm First Credit Card with lofty benefits as it races to bulk up its financial offerings. The cards, issued by Citi Bank, will be the first in the country to offer unlimited, one percent cashback on purchases, Paytm claimed in a statement. The company is hoping to rope in about 25 million credit card customers in the coming months.

The penetration of credit cards remains very low in India with under 50 million people possessing one. With people conducting most of their businesses through cash in the nation, banks have little understanding of a customer’s credit history and score. And it also doesn’t help that banks in India are still wary of issuing credit cards to those who don’t perfectly fit the traditional blue collar job.

But why is a company that made its name through a mobile payment wallet open to its customers engaging with credit card companies? Paytm itself is struggling to grow its business and retain existing customers. Some of its recent major bets haven’t exactly paid off. Its ecommerce business Paytm Mall remains tiny despite bleeding money.

Yo! The First. Paytm First. pic.twitter.com/5kAxozc2IH

— Vijay Shekhar (@vijayshekhar) May 13, 2019

But more importantly, payments itself has become a commoditized space. Users park their money in Paytm and do transactions from there. Paytm makes money from this accumulated sum. This business flourished for years, especially in the months after the Indian government invalidated much of the cash in the nation. But then the government launched its own payment infrastructure called UPI, which removes the need for a middleman.

This has made payments more convenient for users, who are increasingly jumping ship. UPI apps such as PhonePe that have emerged in the last two and a half years now see more transactions than wallet apps. To make matter worse for Paytm, Google and Facebook — two companies that have larger userbase in India — have entered the payments space. Google Pay reached 100 million installs on Google Play Store recently, and WhatsApp plans a nation-wide roll out of its payment feature in India later this year.

So Paytm is now expanding its financial offerings and credit card play fits well in it. With more than 200 million active users, Paytm rivals banks on both the number of customers and volume of transaction it processes.

“Our new offering is designed to bring utmost flexibility to our customers in their digital payment options and will help spur large-ticket cashless payments,” Vijay Shekhar Sharma, chairman and CEO of One97 Communications said in a statement.

Backed by SoftBank, Alibaba, and most recently Warren Buffett’s Berkshire Hathaway, Paytm has the capital to spur the adoption of its new credit card. As part of the package, Paytm’s credit card holders will be able to avail dining, shopping, travel and other offers that Citi Bank provides to its privilege customers. In the first four months of issuing a card, the company will offer its customers discounts worth Rs 10,000 ($142) on spending of Rs 10,000.

Paytm First Credit Card will work both in India and elsewhere and support contactless transactions. Like any other credit card, customers will be able to pay back a sum in multiple monthly instalments. Paytm First Credit Card will charge users a nominal fee of Rs 500 ($7.1) that will be waived off if their spendings through the card exceeds Rs 50,000 ($710) in a year.

If the gamble works, Paytm will be able to retain some customers and convince many to do big-ticket transactions. For Citi Bank, this partnership is just an easy ploy to acquire some customers.

In the meantime, Paytm continues to aggressively expand its financial offerings. In recent years, it has launched a digital payments bank, and has started to offer prepaid Forex cards for international purchases. It also lets customers buy gold, and employers issue food allowance wallets for their staff. Last year, the company announced Paytm Money to facilitate purchase of mutual funds.

Earlier this year, the company launched Paytm First, a subscription bundle that includes access to subscriptions from other services such as Zomato, Uber, Gaana, and Eros Now. In an interview with TechCrunch late last month, Paytm’s Sharma said payments is the moat around which you can build a number of services. “Now that’s a business model… payment itself can’t make you money.”

Powered by WPeMatico

Selling equity to buy Facebook and Google ads is a bad deal for startups. Clearbanc offers a fundraising alternative. For fast-growing businesses reliably earning sales from their marketing spend, Clearbanc offers funding from $5,000 to $10 million in exchange for a steady revenue share of their earnings until it’s paid back plus a 6 percent fee. Clearbanc picks which merchants qualify by developing tech that scans their Stripe, Facebook ads and other accounts to assess financial health and momentum. It’s already doled out $100 million this year.

“As a business successfully scales, we continue to provide them ongoing capital,” co-founder and CEO Andrew D’Souza tells me. “Our goal is to be the first and last backer of a successful business and save the entrepreneur from having to take hundreds of pitch meetings to keep their company funded.”

“As a business successfully scales, we continue to provide them ongoing capital,” co-founder and CEO Andrew D’Souza tells me. “Our goal is to be the first and last backer of a successful business and save the entrepreneur from having to take hundreds of pitch meetings to keep their company funded.”

After largely flying under the radar since being found in 2015, now Clearbanc has some big funding news of its own. It’s now raised $70 million from a seed and new Series A round from Emergence Capital, Social Capital, CoVenture, Founders Fund, 8VC and more, with Emergence’s Santi Subotovsky joining the board.

“Venture capital has shifted. Instead of funding true research and development, today 40 percent of venture capital goes directly to buying Google and Facebook ads,” D’Souza claims (that may be true for some e-commerce startups, but TechCrunch could not verify that stat for all startups). “Equity is the most expensive way to fund digital ad spend and repeatable growth. So we created something new.”

Clearbanc emerged from an angel investing alliance between two serial entrepreneurs. D’Souza built Andreessen Horowitz-funded social recruiting site Top Prospect, USV-backed education tech company Top Hat and Mastercard portfolio biometric authentication wearable startup Nymi. He helped raise more than $300 million in venture after a stint at McKinsey, when he began co-investing with Michele Romanow, a VC from Canada’s version of the TV show Shark Tank called Dragons’ Den. She’d bootstrapped shopping hub Buytopia that acquired 10 other e-commerce companies, and discount-finder SnapSaves that she sold to Groupon in 2014.

“We started investing together in some of the deals we would see from Dragons’ Den and often found that an equity investment wasn’t the right structure for these consumer product companies. They had great economics and had found a niche of customers, but often didn’t want to exit the business at any point,” D’Souza recalls. “They needed money to acquire more customers, scale up their marketing efforts and online ad spend. So we started to do these revenue share deals.”

Both engineers, they built tech to automate the due diligence and find companies with healthy unit economics and customer acquisition costs. The partnership blossomed into Clearbanc, and romance. “We’re also a couple, so we spend a lot of time together,” D’Souza writes. Inter-startup dating can be problematic, but so far seems to be working for Clearbanc.

Clearbanc’s team

Now Clearbanc has poured over $100 million into 500 companies in 2018, like Vinebox. The subscription wine box company used Clearbanc to grow its membership numbers while raising a Series A for developing new products. Clearbanc’s companies pay out 5 percent in revenue share until the investment plus 6 percent is paid back. That’s a great deal for companies that are already proven moneymakers, like Hunt A Killer, a murder mystery game subscription box that had raised $10,000 and was selling swiftly. Derisked, it didn’t need venture, and has now taken $8 million from Clearbanc to ramp its business.

Clearbanc co-founders Andrew D’Souza and Michele Romanow

Clearbanc is rising up at a time when organic growth channels are shutting down. The ruthless optimization of algorithmic feeds by Facebook, Instagram and Twitter suppress marketing content unless businesses are willing to pay. Without free virality opportunities, companies must rely on venture funding or loans just to turn around and pay that money to big ad platforms. With the new cash, which also comes from iNovia Capital, Real Ventures, Portag3, Precursor, WTI, Berggruen and FJ Labs, Clearbanc plans to expand abroad after doing deals in the U.S. and Canada. It’s also going to invest in building awareness as well as its data science capabilities.

D’Souza and Romanow must have confidence in their tech, as a wrong investment means they might never get their cash back. “We pay a lot of attention to our underwriting and decision-making process because if we make a mistake, we can lose a lot of money. Unlike a VC, we don’t expect the majority of our companies to fail and have the winners make up for the losses,” says D’Souza. One big misstep could wipe out the gains from a bunch of other investments.

Meanwhile, it has to break the norms of how businesses find funding. Startups immediately seek traditional venture or debt financing that can depend on the flashy names already on their cap table, while merchants turn to exploitative online lenders that require a personal guarantee and base their decisions on the founders’ own credit history instead of the business.

While riskier hard-tech startups that will take years to get to market will still need venture, a new crop of direct-to-consumer products and other fast-monetizing startups that are already humming can avoid diluting their team and investors by using Clearbanc. D’Souza concludes, “We’ve spent our entire careers as entrepreneurs and wanted to build a new asset class to help entrepreneurs grow.”

Powered by WPeMatico

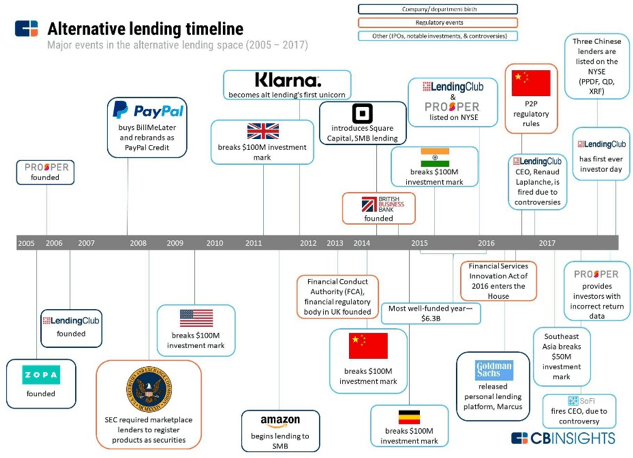

Renaud Laplanche spent ten years building LendingClub. In the process, he created an industry from scratch. Circumventing conventional banking channels for consumer credit began in 1996 when Chris Larsen started E-LOAN, which ultimately led to Prosper Marketplace. But LendingClub, which Laplanche founded in 2007, was and remains the poster child for the business of marketplace lending. The industry’s short history has been volatile, characterized by both triumphant hype and utter lack of confidence.

History of the Marketplace Lending Industry, CB Insights

While LendingClub has struggled in the public markets since their late 2014 IPO, they have managed to propel their industry into significance, while rapidly expanding their share of the personal loan market to 10%.

After his well-publicized departure in May 2016, Laplanche got started on his next venture in a hurry. Just a few months later he started Credify, ultimately renamed to Upgrade, a company that bears a striking resemblance to LendingClub. In just two years Upgrade has raised $142 million in funding, while originating more than $1 billion in loans since August 2017.

With Upgrade, Laplanche has the opportunity to start fresh with the benefit of hindsight. The initial promise of LendingClub and their competitors was unbundling the banks. Now, to persist and grow, marketplace lenders have realized they need to rebundle, providing an array of bank-like services to better serve their end customers. This post explores what Laplanche is doing differently this time with Upgrade.

There has been a general recognition across many fintech businesses that marketplace business models aren’t enough. The mutually-beneficial arrangement of marketplace lending is a perfect example. Superior customer experience, expedited loan decision, quick receipt of funds, and lower operational costs without legacy infrastructure were the selling points. Charles Moldow famously called it a “trillion-dollar opportunity” in 2014.

He may still be right, but in order to realize the opportunity, marketplace lenders need to capture a larger, more regular share of borrower’s attention. Loans may be high-volume purchases, but they’re not high-frequency transactions. So when a platform like LendingClub facilitates a loan so someone can refinance their outstanding credit card debt, is there really a relationship with the customer there? Capital is provided, customer service is available, and monthly payments are made. That’s all there is to it.

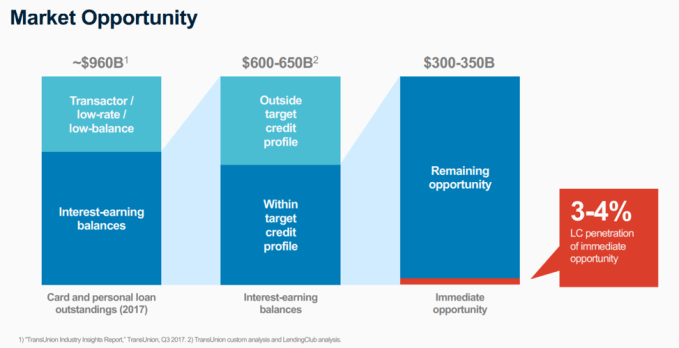

Total addressable market (TAM) is frequently used to assess opportunity. A critical part of the TAM estimation process might have been overlooked in the early assessments of the alternative lending industry. The large numbers in the figure below reflect an alluring market that LendingClub, Prosper, Avant, Upstart, OneMain, Best Egg and others have attempted to capitalize upon.

The notion of a replacement cycle, which I’ll borrow from Michael Mauboussin, is an important consideration here, particularly in a high volume, low frequency transaction relationship such as consumer lending. Just because a borrower refinances their credit card debt with a loan from LendingClub, there’s little guarantee that all of the money spent on acquiring that customer will lead to future transactions with that customer. Yet, in order for these companies to succeed, the average revenue per user (ARPU) is going to have to rise through some combination of repeat customers and complementary services to deepen the relationship and create new revenue channels.

The market opportunity for marketplace Lenders, LendingClub Investor Day 2017

With this realization in mind, fintech players across the board have focused on deepening relationships with customers to drive sales and lower SG&A costs. Customer acquisition is a major component of the income statement for these companies. The more engagement a lender has with their end customer, the greater the chance they stand to not only be called upon when a borrower needs to borrow again, but ultimately pinpoint opportunities for product recommendations.

And that’s exactly what Upgrade is doing. In many ways, they’re quite similar to LendingClub. Upgrade offers personal loans between $1,000 and $50,000 over three-to-five-year repayment periods at rates competitive with major banks. LendingClub varies a bit in the principal amount offerings and APRs, but they essentially do the same thing. Loans are originated through WebBank, the partner bank that also works with LendingClub. Operationally, there’s a blockchain component for data remediation and security purposes. However, the extent and value of this application are unclear.

The notion of financial wellness is increasingly popular among consumer fintech companies, as well as incumbent financial institutions. It reflects a transition away from a purely transactional relationship to a fiduciary one, as we’ve also seen in the wealth management industry. The tricky thing about this is that although it may be the right thing to do, late fees and overdraft penalties make up a sizeable portion of traditional bank revenue.

Where Upgrade differs from LendingClub is in their customer engagement model. Upgrade provides several features to customers that resemble a conventional personal financial management (PFM) app. Their Credit Health service offers free advice and monitoring tools, personalized recommendations, and customized updates for individual credit scores and underlying rationale. Additionally, they offer a financial education tool open to the public called Credit Health Insights, which offers tips and tricks for debt management and financial wellness. At the surface, there’s little differentiation here. A free credit score is becoming table stakes for any financial institution, and personalized insights are to be expected.

Upgrade’s borrower value proposition, LendIt 2018 Conference

In Upgrade’s case, however, the framing of the dual service is compelling. Typically, online lenders only approve 10-15% of applicants. While the credit underwriting models are looking for the most compelling borrower profiles who will pay back their loans, the majority of interested borrowers are sent back to the drawing board.

A major focus of Upgrade is to build the credit of the other 85-90% of applicants who are typically rejected so that they improve their profile and obtain a loan in the future. Credit repair and financial wellness are underserved markets today, although companies like Bloom Credit are working to change the record. This product combination helps to unify the interests of Upgrade and borrowers, both approved and rejected.

At the LendIt Conference in 2017, Laplanche concluded his presentation with a reference to the Wright Brothers. He discussed how he was enamored with their ability to combine two things to create something entirely new, which in their case was “wheeling and flying.” A year later, he returned to LendIt with a new product release that borrowed from the innovation strategy of Orville and Wilbur.

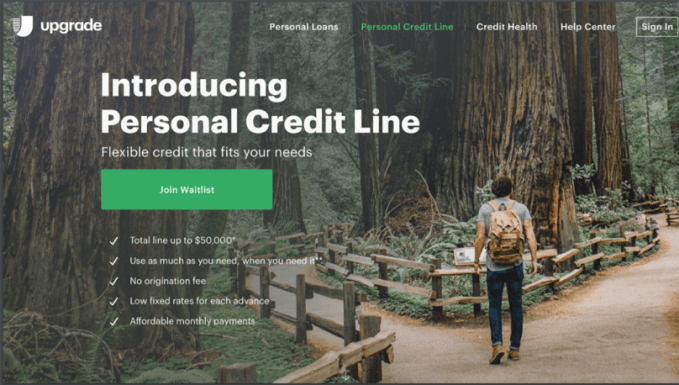

Upgrade launched a first of its kind product, a Personal Credit Line, a hybrid of a credit card and an unsecured loan. Here’s how it works: customers get approved for up to $50,000 in credit, from which they can draw down as needed. They only pay interest on what’s borrowed, over the course of a 12-60-month timeframe. The interest rate is also fixed over the term of the loan.

Upgrade’s Personal Credit Line, a hybrid of a personal loan and a credit card, Upgrade

The product is built on the premise that the level of innovation in the origination of consumer credit has been somewhat limited. Laplanche attempted to reinvent it once with the creation of LendingClub. In some ways, it worked. Personal loans originated by fintech lenders account for roughly a third of outstanding consumer loans according to Transunion. Now he’s trying to do it again.

When I first read the press release for the Personal Credit Line, I thought it was a very compelling way to expand the menu of options to qualified consumers. It puts more control in the hands of the borrower, so they can avoid the vicious cycle of consumer debt. I was also reminded of a comment made by Josh Brown, CEO of Ritholtz Wealth Management, after Wealthfront released their “Portfolio Line of Credit” product in April 2017. He said that while it might sound flashy, there’s nothing holding Schwab or Fidelity back from offering the same product tomorrow.

What’s so challenging about consumer-facing fintech companies is that customers are expensive to acquire, they’re difficult to keep, and products are easy to replicate. Providing a free credit score is easily accessible through a partnership with Equifax or Experian. It’s commoditized. The situation is similar with personal financial management tools. This Personal Credit Line seems awfully similar. What’s to stop Chase or Goldman’s Marcus from offering an identical product, perhaps with even better rates? U.S. Bank just launched a similar product, albeit for a different use case, called Simple Loan. It’s a $100 to $1,000 loan marketed as a payday lending alternative, with a roughly 20% lower interest rate than typical payday lender offers.

There is something to be said for being first to market, but ease of replication limits the defensibility of that position. There is a clear interest in an expansion into new products, which will continue to help Upgrade to differentiate the value proposition to consumers, and maybe one day small businesses. The unfortunate reality is that bigger players with an existing customer base and a lower cost of capital are on their tail.

Renaud Laplanche rings the bell with his team at LendingClub (DON EMMERT/AFP/Getty Images)

The real insight that distinguishes Upgrade from LendingClub is the profile of the users. On the supply side of the marketplace, Upgrade only welcomes institutional investors. LendingClub was, and still is, marketed to individuals and institutions.

The peer-to-peer model turned out to be a little too idealistic to serve as the foundation for a business. The concept of a marketplace is really attractive – the ability to invest in others, as cliché as that may sound, has a philanthropic twist to it that even implies a social good. Or, at the very least, an alignment of interests. Except interests aren’t aligned because of the mercurial nature of retail investors, which makes for unstable sources of capital.

LendingClub’s original business model, in the pure P2P form, was reliant on the ability to create a new asset class. The notion of investing in consumer credit may sound compelling, and return prospects may be even more appealing. But, you can’t bootstrap an asset class and base a business model around retail adoption. LendingClub had to solve for distribution of their service, as well as the dissemination of the broader concept of unsecured consumer lending as an asset class.

On Laplanche’s second go around with Upgrade, there’s no more promise of democratization of a new asset class. Instead, large multi-billion-dollar credit investors own the supply side of the marketplace. As a result, there’s a more stable capital base of institutional investors who know what they’re investing in and the reason why they’re investing in it.

What Laplanche did this time around was base his business model around stability. In this market it can pay to be a follower. LendingClub touts the notion that they have “brought a new asset class to investors,” but that education campaign came at a serious cost. It also invited boiler room-like sales behavior from competitors. Upgrade is stepping in after a decade of marketing to scale an untested industry to the masses. Fortunately, a lot of the work has already been done for them.

Upgrade is led by as experienced and forward-thinking of a leader as they come in the marketplace lending industry. They expect to originate over $2 billion loans in 2018 and hit profitability by year-end as well. They’re redefining convention when it comes to consumer credit products.

The question, however, remains: how long can the novelty last? Consumer fintech is fiercely competitive. It’s also increasingly occupied by incumbents with far lower costs of capital, large existing customer bases, and the ability to experiment in a way that a startup cannot. The unsecured consumer lending space has attracted mountains of capital in the past five years, but the opportunity is clearly defined. The number of lenders issuing more than 10,000 personal loans per year has more than doubled since 2011.

There’s a network effect component to marketplace lending businesses, particularly as lenders are able to maintain more connected relationships with consumers. But when it comes to standing apart from the rest of the pack, a differentiated product offering isn’t a very wide moat.

Powered by WPeMatico