New York

Auto Added by WPeMatico

Auto Added by WPeMatico

During the days when Snapchat’s popularity was booming, investors thought the company would become the anchor for a new Los Angeles technology scene.

Snapchat, they hoped, would spin-off entrepreneurs and angel investors who would reinvest in the local ecosystem and create new companies that would in turn foster more wealth, establishing LA as a hub for tech talent and venture dollars on par with New York and Boston.

In the ensuing years, Los Angeles and its entrepreneurial talent pool has captured more attention from local and national investors, but it’s not Snap that’s been the source for the next generation of local founders. Instead, several former SpaceX employees have launched a raft of new companies, capturing the imagination and dollars of some of the biggest names in venture capital.

“There was a buzz, but it doesn’t quite have the depth of bench of people that investors wanted it to become,” says one longtime VC based in the City of Angels. “It was a company in LA more than it was an LA company.”

Perhaps the most successful SpaceX offshoot is Relativity Space, founded by Jordan Noone and Tim Ellis. Since Noone, a former SpaceX engineer, and Ellis, a former Blue Origin engineer, founded their company, the business has been (forgive the expression) a rocket ship. Over the past four years, Relativity href=”https://techcrunch.com/2019/10/01/relativity-a-new-star-in-the-space-race-raises-160-million-for-its-3-d-printed-rockets/”> has raised $185.7 million, received special dispensations from NASA to test its rockets at a facility in Alabama, will launch vehicles from Cape Canaveral and has signed up an early customer in Momentus, which provides satellite tug services in orbit.

Powered by WPeMatico

Over the past 12 months, Maven, the benefits provider focused on women’s health and family planning, has expanded its customer base to include more than 100 companies, and grown its telehealth services to include 1,700 providers across 20 specialties — for services like shipping breast milk, finding a doula and egg freezing, fertility treatments, surrogacy and adoption.

The New York-based company, which offers its healthcare services to individuals, health plans and employers, has now raised an additional $45 million to expand its offerings even further.

Its new money comes from a clutch of celebrity investors, like Mindy Kaling, Natalie Portman and Reese Witherspoon, and institutional investors led by Icon Ventures and return backers Sequoia Capital, Oak HC/FT, Spring Mountain Capital, Female Founders Fund and Harmony Partners. Anne Wojcicki, the founder of 23andMe, is also an investor in the company.

“Maven is addressing critical gaps in care by offering the largest digital health network of women’s and family health providers,” said Tom Mawhinney, lead investor from Icon Ventures, who will join the Maven board of directors, in a statement. “With its virtual care and services, Maven is changing how global employers support working families by focusing on improving maternal outcomes, reducing medical costs, retaining more women in the workplace, and ultimately supporting every pathway to parenthood.”

In the six years since founder Katherine Ryder first launched Maven, the company has raised more than $77 million for its service and she became a mother of two boys.

“You go through this enormous life experience; it’s hugely transformative to have a child,” she told TechCrunch after announcing the company’s $27 million Series B round, led by Sequoia. “You do it when your career is moving up — they call it the rush hour of life — and with no one supporting you on the other end, it’s easy to say ‘screw it, I’m going home to my family’ … If someone leaves the workforce, that’s fine, it’s their choice, but they shouldn’t feel forced to because they don’t have support.”

Some of Maven’s partners include Snap and Bumble to provide employees access to its women’s and family health provider network. The company connects users with OB-GYNs, pediatricians, therapists, career coaches and other services around family planning.

Powered by WPeMatico

Student loan debt in the U.S. totals $1.5 trillion, and more than 44 million Americans have outstanding student loan debt.

According to research by Villanova law professor Jason Iuliano, a million student loan debtors have filed for bankruptcy in the past five years. However, 99.9% of them did not include their student loan debt in their bankruptcy filing.

This research was the seed of what would become Reset Button, a new startup founded by Iuliano and Rob Hunter looking to help student loan debtors who have gone through bankruptcy find a new way to include those debts in their filing.

The only way you can include student loan debt in a bankruptcy filing is through litigation. Those cases have been historically less likely to settle out of court than other types of civil cases.

This means that the cost of including student loan debt in bankruptcy filings is, at the very least, around $10,000. Now, if there was some guarantee that you could trade hundreds of thousands of dollars of student loan debt for $10,000-$15,000, you’d obviously do it. But most folks who are already in the process of filing for bankruptcy don’t have a spare $10,000 minimum to spend on a litigator. And even if they did, there is no guarantee they’d win in court, resulting in even more debt and no relief.

This is what Reset Button is trying to change.

To be clear, Reset Button is targeted directly at folks who have already filed for bankruptcy but were told they couldn’t include their student loan debt in those filings, and so they didn’t.

Here’s how it works:

Reset Button has built a network of litigation lawyers who have experience in seeking student loan discharges. When a new user fires up Reset Button, the startup sends them through an evaluation process that collects financial information, etc. to assess whether or not one of those lawyers could litigate the discharge of that user’s student loan debt. That evaluation factors in a number of signals, including past legal cases that are comparable to the user’s situation.

That process also does a lot of the heavy lifting that makes hiring a litigator so expensive. These lawyers often have to do tons of research, tracking down statements and bills and other paperwork, before they can truly get started with the litigation.

Reset Button, as the connective tissue between debtor and lawyer, is able to automate a lot of that process for the lawyers, delivering a package of information on the case and connecting the user with the right lawyer for them.

Reset is also looking to bring down the cost for debtors. The company charges either 12% of the total debt discharged, or $10,000 (whichever is lowest). Reset also allows users to pay that sum over time, in $300 monthly installments. This is in stark contrast to people who hire their own lawyer, who would be responsible for the costs upfront.

Reset Button is able to do this through a payment process called factoring. In short, Reset buys the receivables from the attorney’s fees, and charges the debtor with their own payment plan. Reset makes money from lawyers who pay for the lead generation, the technology services and the marketing apparatus.

Factoring has come under fire from some who say that service providers sometimes raise prices to account for their fee, but Reset Button co-founders Hunter and Iuliano say their lawyers are actually charging less because of the workflow optimization provided by Reset Button.

The company also provides a Knowledge Base for debtors seeking financial guidance and resources, but the only revenue stream comes from the actual litigation of student loan debt in bankruptcy filings. Other services like refinancing, debt consolidation or income-based payments are not provided by Reset Button, and the company has no official partnerships with those types of service providers.

However, Hunter said that it may be an avenue the company explores as it grows.

Perhaps most importantly, Reset Button offers a Fresh Start guarantee. In short, if the lawyer doesn’t manage to get your debt wiped, Reset will pay your legal bills.

There has been movement in the landscape of student loan discharges with bankruptcy.

Essentially, debtors must prove in court that they pass the test of “undue hardship,” which is a notably vague framework. Though there is a bit of variability among the various court circuits, the general idea is that a debtor must prove that they can’t currently pay back the loan, that there will not be a change down the line that will allow them to pay the loan in the future and that they have made every effort to pay the loans in the past.

Historically, that’s been a difficult threshold to cross for the fraction of people who take steps to litigate their student loan debt. However, in small ways, courts seem to be opening up the interpretation of undue hardship.

“There’s a phrase that gets used in these cases that I think perpetuates this myth, and that is to call it a ‘certainty of hopelessness’,” said John Rao, attorney with the National Consumer Law Center. “And it’s almost like, as long as you’re still alive and breathing, something could improve for you. That’s just an impossible burden. It’s basically saying you could win the lottery or something. That’s just not the standard I think Congress had in mind.”

In 2015, in a case between Robert E. Murphy and the DOE/ECMC, Rao wrote to the courts arguing that they should reassess the test for undue hardship:

Rather than adopt one existing test over another, we urge this Court to provide a formulation of the undue hardship standard in simple terms, that restricts consideration of extraneous and inappropriate factors not consistent with the statutory language. A finding about whether a debtor’s hardship is likely to persist should be based on hard facts, not conjecture and unsubstantiated optimism.

More recently, a judge in the Southern District of New York ruled in favor of a debtor, wiping more than $200,000 in Kevin Rosenberg’s student debt. Of course, the lenders will be appealing the case.

However, Judge Morris, who presided over the case, wrote in her decision that “most people (bankruptcy professionals as well as lay individuals) believe it impossible to discharge student loans,” and that her “Court will not participate in perpetuating these myths.”

Reset Button has raised money from investors Craft Ventures, Slow Ventures and Jeff Morris Jr. of Lambda School, among others. The company declined to share its total amount of investment.

“Society has been led to believe something for decades that is not true, which is probably the biggest initial challenge,” said founder and CEO Rob Hunter . “One of the unfortunate things is the reason that many consumers believe incorrect information is because a lawyer told them that. So, that is a bit of an uphill battle to swim against.”

Powered by WPeMatico

Tesla appears to be ramping up installations of its solar tile roofs in the San Francisco Bay area and will eventually roll out to Europe and China, according to CEO Elon Musk, who, in a series of tweets, provided the first substantial update since the company launched the third iteration of its product in October.

The solar tile roof, which Tesla calls Solarglass, is being produced at the company’s factory in Buffalo, N.Y. Musk announced in one of the tweets plans to host a “company talk” in April at the Buffalo factory, an event that will include media and customer tours of the facility.

Tesla did not respond to a request for comment seeking more information about Solarglass, including how many installations have been made to date. We will update the article if Tesla responds.

Many Bay Area installations are ongoing now

— Elon Musk (@elonmusk) February 9, 2020

Europe & China timing will be announced soon

— Elon Musk (@elonmusk) February 10, 2020

Four months ago, Musk said the company would begin installations in the “coming weeks” and that it hopes to ramp production to as many as 1,000 new roofs per week.

Tesla’s solar roof tiles are designed to look like normal roof tiles when installed on a house, while doubling as solar panels to generate power. The company first unveiled the solar tiles in 2016 and has been tinkering with them ever since. Tesla has conducted trial installations with the first two generations of the solar tiles and opened up pre-orders in 2017.

In an earnings call last October, Musk suggested that the tiles were ready for a widespread deployment, noting that “version three is finally ready for the big time.”

The solar tile roof will initially be offered in textured black, but Musk reiterated Monday plans to offer other color and finish variants “hopefully later this year.”

Yes, but we want to focus on textured black first, then move into Earth tones & convolutions

— Elon Musk (@elonmusk) February 10, 2020

A pricing estimator on the Tesla website says a solar tile roof with 10 kW of solar on an average 2,000 square-foot home costs $42,500 before federal tax incentives. It also lists $33,950 as the price after an $8,550 federal tax incentive.

Powered by WPeMatico

Antler is a “company builder” that emerged a couple of years ago, running startup generator programs and investing from an early stage, bringing a heady mix of technologists, product builders and operators together with its own technology stack.

Now, plenty of “company builders” have come and gone. It’s a bit like Apocalypse Now: everyone goes in thinking they will come up with the major formula to spit out startups at a prodigious rate and they come out screaming “The Horror! The Horror!”

But Antler appears to have been on an interesting run. It has so far made more than 120 investments across a wide range of companies, with several going on to raise later-stage funding from the likes of Sequoia, Golden Gate Ventures, East Ventures, Venturra Capital and the Hustle Fund.

Since its launch in Singapore two years ago, Antler now has a presence across New York, London, Singapore, Sydney, Amsterdam, Stockholm, Nairobi and Oslo.

Today, it’s announcing that it has attracted investment from British investment management company Schroders, investment house FinTech Collective and Ferd, the vehicle used by Johan H. Andresen, the Norwegian industrialist and investor.

This latest investment takes the capital raised by Antler over the past six months to more than $75 million.

These investors join an existing group that includes Facebook co-founder Eduardo Saverin, Canica International and Credit Saison, the third-largest credit card issuer in Japan. The idea here is that these investors get exposure to early-stage companies as they are built.

As with most company builders and accelerators, Antler only takes 1-1.5% of the applicants

Its portfolio includes Sampingan, an on-demand workforce in Indonesia; Xailient, a computer vision technology; Airalo, a global e-sims marketplace; and FusedBone, which enables medical centers to produce bespoke, non-metal implants on-site.

Magnus Grimeland, Antler co-founder and CEO said: “With our support, our founders start refining their ideas and building new and innovative businesses. What is equally important is the deep relationship our founders build with their peers, our advisors and backers. Having accomplished investors like Schroders, Ferd and FinTech Collective on board means we can provide a more valuable network for our startups as they grow their businesses.”

Peter Harrison, Group CEO of Schroders, who will also be joining Antler’s advisory board, said: “We are in a period of unprecedented change. The visibility on venture capital activity and innovation that Antler provides is therefore leading-edge.”

Antler says more than 40% of its portfolio companies have a female co-founder and 78% of these have a female CEO.

Powered by WPeMatico

If you’ve ever entered a company’s office as a visitor or contractor, you probably know the routine: check in with a receptionist, figure out who invited you, print out a badge and get on your merry way. Brussels, Belgium and New York-based Proxyclick aims to streamline this process, while also helping businesses keep their people and assets secure. As the company announced today, it has raised a $15 million Series B round led by Five Elms Capital, together with previous investor Join Capital.

In total, Proxyclick says its systems have now been used to register more than 30 million visitors in 7,000 locations around the world. In the U.K. alone, more than 1,000 locations use the company’s tools. Current customers include L’Oréal, Vodafone, Revolut, PepsiCo and Airbnb, as well as a number of other Fortune 500 firms.

Gregory Blondeau, founder and CEO of Proxyclick, stresses that the company believes that paper logbooks, which are still in use in many companies, are simply not an acceptable solution anymore, not in the least because that record is often permanent and visible to other visitors.

Proxyclick’s founding team.

“We all agree it is not acceptable to have those paper logbooks at the entrance where everyone can see previous visitors,” he said. “It is also not normal for companies to store visitors’ digital data indefinitely. We already propose automatic data deletion in order to respect visitor privacy. In a few weeks, we’ll enable companies to delete sensitive data such as visitor photos sooner than other data. Security should not be an excuse to exploit or hold visitor data longer than required.”

What also makes Proxyclick stand out from similar solutions is that it integrates with a lot of existing systems for access control (including C-Cure and Lenel systems). With that, users can ensure that a visitor only has access to specific parts of a building, too.

In addition, though, it also supports existing meeting rooms, calendaring and parking systems, and integrates with Wi-Fi credentialing tools so your visitors don’t have to keep asking for the password to get online.

Like similar systems, Proxyclick provides businesses with a tablet-based sign-in service that also allows them to get consent and NDA signatures right during the sign-in process. If necessary, the system also can compare the photos it takes to print out badges with those on a government-issued ID to ensure your visitors are who they say they are.

Blondeau noted that the whole industry is changing, too. “Visitor management is becoming mainstream, it is transitioning from a local, office-related subject handled by facility managers to a global, security and privacy-driven priority handled by chief information security officers. Scope, decision drivers and key people involved are not the same as in the early days,” he said.

It’s no surprise then that the company plans to use the new funding to accelerate its roadmap. Specifically, it’s looking to integrate its solution with more third-party systems with a focus on physical security features and facial recognition, as well as additional new enterprise features.

Powered by WPeMatico

E-commerce phenom and D2C bright light Casper has filed to go public.

The New York-based company that raised nearly $340 million while private, according to Crunchbase data, expects to trade on the New York Stock Exchange under the ticker symbol “CSPR.” Its S-1 filing includes a $100 million placeholder figure for its possible capital raise.

The company will need the money, as it loses money and burns cash. Let’s explore just how a mattress company does that.

In the full years of 2017 and 2018, Casper recorded revenue of $250.9 million (net of $45.7 million in “refunds, returns, and discounts”) and $357.9 million (net of $80.7 million in “refunds, returns, and discounts”). That worked out to growth of 42.6% in the year.

Over the same two periods, Casper lost $73.4 million and $92.1 million on a net basis, respectively.

In the first three quarters of 2019 versus 2018, Casper put up $312.3 million in top line (net of $80.1 million in “refunds, returns, and discounts”), up just over 20% from its year-ago three-quarter tally of $259.7 million in revenue (net of $57.7 million in “refunds, returns, and discounts”).

The company’s net loss during the three-quarter period rose from $64.2 million in 2018 to $67.4 million in 2019. The company’s net losses are generally rising (though slowly so far in 2019), while its growth decelerates.

In contrast, and to the company’s favor, its operating cash burn is slowing. From $84.0 million in 2017 to $72.3 million in calendar 2018, Casper slowed its operating cash consumption further in 2019, to just $29.7 million in the first three quarters of the year, compared to $44.9 million over the same period of the preceding year.

But the company’s slowing growth and stiff losses using regular accounting methods (GAAP) could strain its valuation. Casper was valued at $1.1 billion in its most recent funding round.

While the company’s gross margins aren’t bad for a non-software company (49.6% in the first nine months of 2019), the firm spent over 73% of its gross profit last year on sales and marketing costs. That figure indicates that Casper spent heavily to generate growth, growth that came in at about 20% so far in 2019, as reported.

That fact implies that growth will remain constrained, as the firm can’t afford to spend too much more on the line item. Which begs the question: What’s the value of a firm that is showing slowing growth, non-recurring revenue and sticky GAAP losses?

The company’s adjusted losses aren’t much better. Looking at its adjusted EBITDA, a profit metric so distorted to flatter that it’s nigh a funhouse mirror, Casper only marginally improved on its 2018 tally looking at the first three quarters of that year (-$57.5 million) in 2019 (-$53.8 million).

Casper has raised from IVP, Lerer Hippeau, Target and New Enterprise Associates. The firm raised seed capital back in 2014 along with a Series A. Lerer and NEA were most active back then, looking at its funding history.

The company raised $55 million more in 2015, and a far-larger $170 million in mid-2017. A $100 million round came in 2019 that set it up for its 2020 IPO.

This company’s IPO is a pricing question. And one that will impact a host of startups that both compete directly with Casper or operate in a different vertical with a similar business. Get hype.

Powered by WPeMatico

Juro, a UK startup that’s using machine learning tech and user-centric design to do for contracts what Typeform does for online forms, has caught the eye of Union Square Ventures. The New York-based fund leads a $5 million Series A investment that’s being announced this morning.

Also participating in the Series A are existing investors Point Nine Capital, Taavet Hinrikus (co-founder of TransferWise) and Paul Forster (co-founder of Indeed). The round takes Juro’s total raised to-date to $8M, including a $2M seed which we covered back in 2018.

London is turning into a bit of a hub for legal tech, per Juro CEO and co-founder Richard Mabey — who cites “strong legal services industry” and “strong engineering talent” as explainers for that.

It was also, he reckons, “a bit of a draw” for Union Square Ventures — making what Juro couches as a “rare” US-to-Europe investment in legal tech in the city via the startup.

“Having brand name customers in the US certainly helped. But ultimately, they look for product-led companies with strong cross-functional teams wherever they find them,” he adds.

Juro’s business is focused on taking the tedium out of negotiating and drawing up contracts by making contract-building more interactive and trackable. It also handles e-signing, and follows on with contract management services, using machine learning tech to power features such as automatic contract tagging and for flagging up unusual language.

All of that sums to being a “contract collaboration platform”, as Juro’s marketing puts it. Think of it like Google Docs but with baked in legal smarts. There’s also support for visual garnish like animated GIFs to spice up offer letters and engage new hires.

“We have a data model underlying our editor that transforms every contract into actionable data,” says Mabey. “Juro contracts look like contracts, smell like contracts but ultimately they are written in code. And that code structures the data within them. This makes a contract manager’s life 10x easier than using an unstructured format like Word/pdf.”

“Still our main competitor is MS Word,” he adds. “Our challenge is to bring lawyers (and other users of contracts) out of Word, which is a significant task. Fortunately, Word was never designed for legal workflows, so we can add lots of value through our custom-built editor.”

Part of Juro’s Series A funds will be put towards beefing up its machine learning/data science capabilities, per Mabey — who says the overall plan at this point is to “double down on product”, including by tripling the size of the product team.

“That means hiring more designers, data scientists and engineers — building our engineering team in the Baltics,” he tells us. “There’s so much more we are excited to do, especially on the ML/data side and the funding unlocks our ability to do this. We will also be building our commercial team (marketing, sales, cs) in London to serve the EU market and expand further into the US, where we already have some customers on the ground.”

The 2016-founded startup still isn’t breaking out customer numbers but says it’s processed more than 50,000 contracts for its clients so far, noting too that those contracts have been agreed in 50+ countries. (“Everywhere from Estonia to Japan to Kazakhstan,” as Mabey puts it.)

In terms of who Juro users are, it’s still mostly “mid-market tech companies” — with Mabey citing the likes of marketplaces (Deliveroo), SaaS (Envoy) and fintechs (Luno), saying it’s especially companies processing “high volumes of contracts”.

Another vertical it’s recently expanded into is media, he notes.

“E-signature giants have grown massively in the last few years, and some are gradually encroaching into the contract lifecycle — but again, they deal with files (pdfs mostly) rather than dynamic, browser-based documentation,” he argues, adding: “In terms of new legal tech entrants — I’m excited by Kira Systems especially, who are working on unpicking pdf contracts post-signature.”

As part of the Series A, Union Square Ventures parter, John Buttrick, is joining Juro’s board.

Commenting in a supporting statement, Buttrick said: “We look for founders with products equipped to change an industry. While contract management might not be new, Juro’s transformative vision for it certainly is. There’s no greater proof of the product’s ease of use than the fact that we negotiated and closed the funding round in it. We’re delighted to support Juro’s team in making their vision a reality.”

Juro’s contract management platform — dashboard view

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today, we’re digging into a host of data concerning the East Coast venture capital scene, specifically looking into the performance of its two key startup markets.

It’s 12 degrees Fahrenheit as I write this in my office situated between Boston and New York City — a perfect vantage point for studying these vibrant tech ecosystems. Let’s see what the data tells us.

The information we’re examining today comes from White Star Capital (often via CBInsights), a venture capital firm that describes itself as “transatlantic” and takes part in seed, Series A and Series B rounds around the globe. The group last raised a $180 million fund that TechCrunch covered here, noting at the time that capital pool was “oversubscribed from an initial target of $140 million” and would be invested into “around 20 new companies from the new fund, writing opening cheques of between $1 million and $6 million.”

With boots on the ground in New York, White Star cares about the East Coast, so the fund’s put dossier on the region isn’t unexpected. What it includes, however, is.

We’ll start with NYC and its surprising 2019 before turning to Boston, digging into its super-giant venture totals and hearing from Founder Collective’s Eric Paley on the state of things in urban Massachusetts.

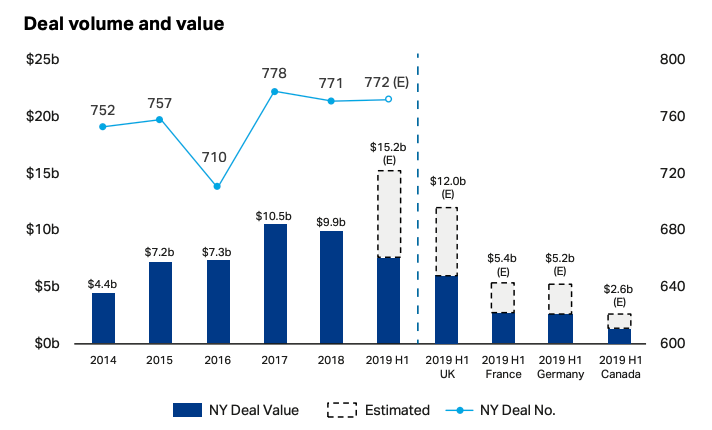

White Star’s report details record-breaking figures for NYC’s current year. Off of effectively flat deal volume (New York City sees around 775 venture deals per year at the moment, or a little more than two per day), the overgrown town should set record venture dollar volume in 2019.

Observe the following, astounding chart detailing the abnormality of 2019 from a comparative venture dollar perspective:

By smashing 2017’s local maximum, 2019 appears set to crush the city’s record — and rich — venture investment totals. The graphic also manages to point out (somewhat embarrassingly) that Gotham will manage to best a number of European countries’ aggregate venture dollar investments by itself this year.

That’s is a useful bit of context as in the United States, New York City is always Number Two to Silicon Valley. But, this chart argues, being number two in the number-one market is still a hell of a lot of capital.

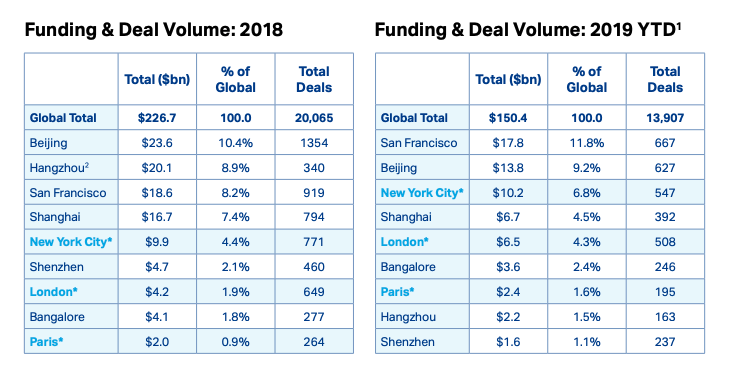

Putting New York City’s venture into even sharper comparative perspective, observe the following table:

Powered by WPeMatico

Tusk Venture Partners, the venture capital firm led by Bradley Tusk and managing partner Jordan Nof, has secured $70 million for its second flagship fund, the firm has confirmed to TechCrunch following a report by Fortune this morning.

Fundraising for the effort began in January, when the pair filed paperwork with the U.S. Securities Exchange Commission for Tusk Venture Partners II. The firm, and affiliated political advisory outfit Tusk Ventures, is behind a number of high-profile startups, including e-scooter “unicorn” Bird, cryptocurrency exchange Coinbase and Ro, a direct-to-consumer healthcare business best known for selling erectile dysfunction medication.

The New York-based firm, founded in 2011, previously raised $36 million for its debut fund — capital it used to back fantasy sports company Fanduel, insurtech business Lemonade and D2C vitamin seller Care/of.

Tusk, before launching Tusk Ventures, served as campaign manager for Mike Bloomberg, as deputy governor of Illinois and as communications director for Senator Chuck Schumer. He also penned the book, The Fixer: My Adventures Saving Startups from Death by Politics, released in 2018.

Naturally, Tusk Ventures provides companies more than just checks. The politically savvy team lends its expertise to support companies plagued with regulatory barriers and communications issues, as well as help with grassroots organizing, opposition research and partnerships.

Powered by WPeMatico