Media

Auto Added by WPeMatico

Auto Added by WPeMatico

Marketing software company HubSpot is acquiring The Hustle, the business and tech media startup behind the popular newsletter of the same name.

Axios broke the news of the deal and reported that it values the startup at around $27 million. HubSpot declined to comment on the deal price, and while tweeting about the acquisition, The Hustle CEO Sam Parr wrote, “Early in my career I was transparent with money. But I didn’t like the result of sharing that stuff. So we’re not disclosing the price and HubSpot has agreed. I’m taking it to the grave!”

In its press release about the acquisition, HubSpot noted that customers are finding its products through content like its YouTube videos and HubSpot Academy.

“By acquiring The Hustle, we’ll be able to better meet the needs of these scaling companies by delivering educational, business and tech trend content in their preferred formats,” said HubSpot’s senior vice president of marketing Kieran Flanagan in a statement. “Sam and his team have a proven ability to create content that entrepreneurs, startups and scaling companies are deeply passionate about, and I’m excited to bring them on board to take that work to the next level.”

BUYERS

We’ve had lots of media co’s try to buy us. We said no. Most ad 1st media companies are dying. And I don’t want to join a sinking, clickbait ship.

I always thought a b2b SAAS biz should buy us. But never thought they’d be bold enough to try.

But HubSpot came along.

— Sam Parr

(@theSamParr) February 3, 2021

HubSpot says The Hustle’s flagship newsletter has 1.5 million subscribers. It also has a subscription offering called Trends and a podcast called My First Million.

“The goal is to build the largest business content network in the world,” Parr tweeted. “Soon, we’ll expand to a variety of mediums on a bunch of different topics and will have really innovative products coming out. We’re also going to hire the best content creators in the world.”

Powered by WPeMatico

Edtech is so widespread, we already need more consumer-friendly nomenclature to describe the products, services and tools it encompasses.

I know someone who reads stories to their grandchildren on two continents via Zoom each weekend. Is that “edtech?”

Similarly, many Netflix subscribers sought out online chess instructors after watching “The Queen’s Gambit,” but I doubt if they all ran searches for “remote learning” first.

Edtech needs to reach beyond underfunded public school systems to become more sustainable, which is why more investors and founders are focusing on lifelong learning.

Besides serving traditional students with field trips and art classes, a maturing sector is now branching out to offer software tutors, cooking classes and singing lessons.

For our latest investor survey, Natasha Mascarenhas polled 13 edtech VCs to learn more about how “employer-led up-skilling and a renewed interest in self-improvement” is expanding the sector’s TAM.

Here’s who she spoke to:

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In other news: Extra Crunch Live, a series of interviews with leading investors and entrepreneurs, returns next month with a full slate of guests. This year, we’re adding a new feature: Our guests will analyze pitch decks submitted by members of the audience to identify their strengths and weaknesses.

If you’d like an expert eye on your deck, please sign up for Extra Crunch and join the conversation.

Thanks very much for reading! I hope you have a fantastic weekend — we’ve all earned it.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin

Image Credits: Nigel Sussman (opens in a new window)

After falling into yesterday’s wild news cycle, Alex Wilhelm returned to The Exchange this morning with a close look at venture capital activity across Africa in 2020.

“Comparing aggregate 2020 figures to 2019 results, it appears that last year was a somewhat robust year for African startups, albeit one with fewer large rounds,” he found.

For more context, he interviewed Dario Giuliani, the director of research firm Briter Bridges, which focuses on emerging markets in Africa, Asia and Latin America.

Image Credits: MCCAIG (opens in a new window) / Getty Images

New cybersecurity ecosystems are popping up in different parts of the world.

Some of of that growth has been fueled by an exodus from the Bay Area, but many early-stage security startups already have deep roots in East Coast cities like Boston and New York.

In the United Kingdom and Europe, government innovation programs have helped entrepreneurs close higher numbers of Series A and B rounds.

Investor interest and expertise is migrating out of Silicon Valley: This post will help you understand where it’s going.

Image Credits: NurPhoto (opens in a new window) / Getty Images

Today’s smartphones are unfathomably feature-rich and durable, so it’s logical that sales have slowed.

A phone purchased 18 months ago is probably “good enough” for many consumers, especially in times of economic uncertainty.

Then again, of the record $111.4 billion in revenue Apple earned last quarter, $65.68 billion came from phone sales, largely driven by the release of the iPhone 12.

Even though “Apple’s success this quarter was kind of a perfect storm,” writes Hardware Editor Brian Heater, “it’s safe to project a rebound for the industry at large in 2021.”

Image Credits: Randy Faris (opens in a new window) / Getty Images

Finmark co-founder and CEO Rami Essaid wrote a post for Extra Crunch that candidly describes the traps he laid for himself that made him a less-effective entrepreneur.

As someone who’s worked closely with founders at several startups, each of the points he raised resonated deeply with me.

In my experience, many founders have a hard time delegating, which can quickly create cultural and operational problems. Rami’s experience bears this out:

“I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I just got my U.S. citizenship! My husband and I want to bring my mom and her husband to the U.S. to help us take care of our preschooler and toddler.

My biological dad passed away several years ago when I was an adult and my mom has since remarried.

— Appreciative in Aptos

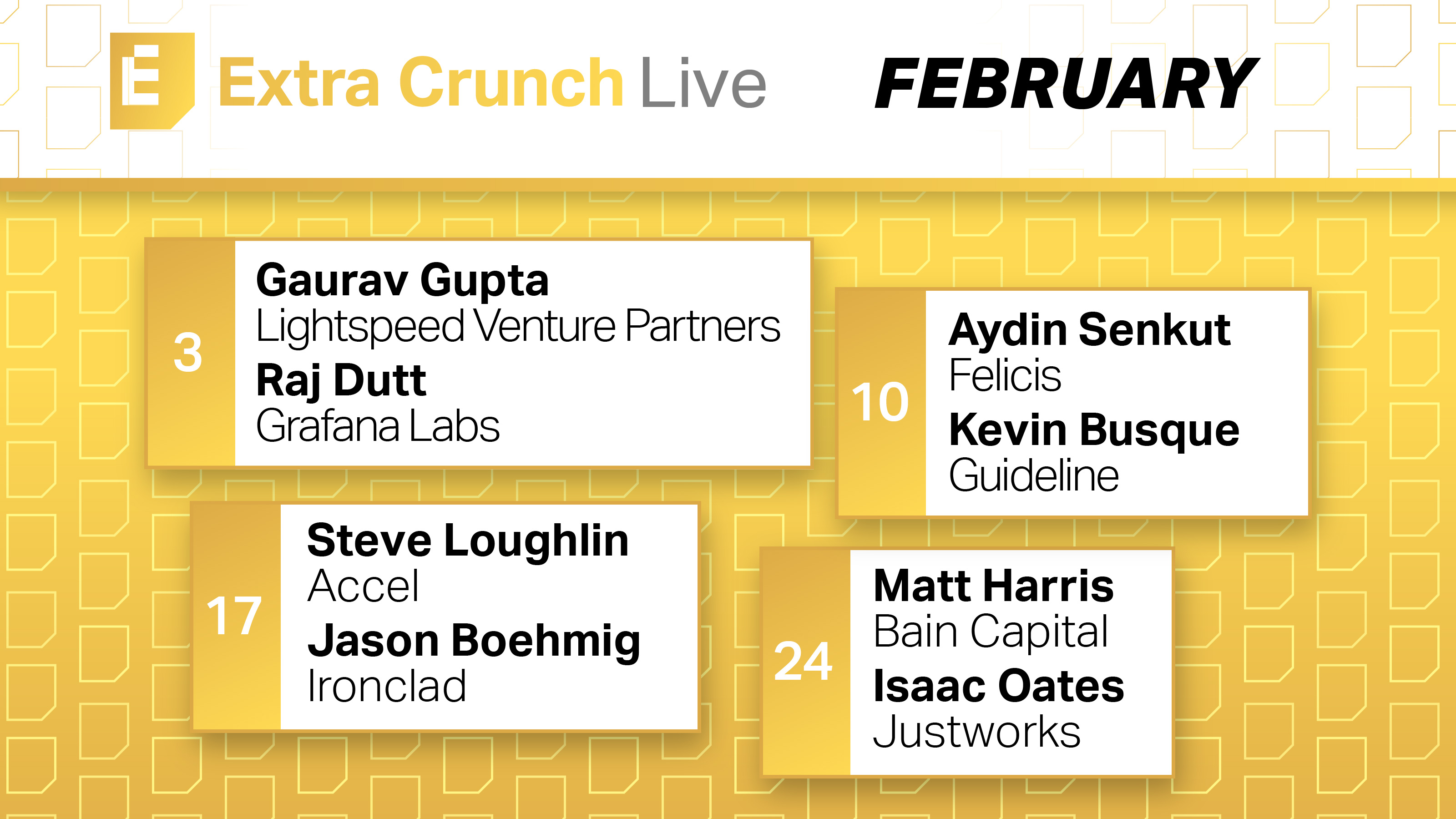

Next month, Extra Crunch Live returns with a lineup of guests who are extremely well-qualified to discuss early-stage startups.

Each Wednesday at noon PPST/3 p.m. EST, join a conversation with founders and the investors who backed their companies:

February 3:

Gaurav Gupta (Lightspeed Venture Partners) + Raj Dutt (Grafana Labs)

February 10:

Aydin Senkut (Felicis Ventures) + Kevin Busque (Guideline)

February 17:

Steve Loughlin (Accel) + Jason Boehmig (Ironclad)

February 24:

Matt Harris (Bain Capital) + Isaac Oates (Justworks)

Also, we’re adding a new feature to Extra Crunch Live — our guests will offer advice and feedback on pitch decks submitted by Extra Crunch members in the audience!

Image Credits: Aleksandar Nakic (opens in a new window) / Getty Images

Since the pandemic disrupted the social rhythms of work and school, many of us have compensated by changing our relationship to digital media.

For instance, I purchased a new sofa and thicker living room curtains several months ago when I realized we have no idea when movie theaters will reopen.

Last year, podcast sponsors spent almost $800 million to reach listeners, but ad revenue is estimated to surpass $1 billion this year. Clearly, I’m not the only person who used a discount code to buy a new product in 2020.

At this point, I can scarcely keep track of the multiple streaming platforms I’m subscribed to, but a new voice-activated remote control that comes with my basic cable plan makes it easier to browse my options.

Media reporter Anthony Ha spoke to10 VCs who invest in media startups to learn more about where they see digital media heading in the months ahead. For starters, how much longer can we expect traditional advertising models to persist?

And in a world with hundreds of channels, how are creators supposed to compete for our attention? What sort of discovery tools can we expect to help us navigate between a police procedural set in a Scandinavian village and a 90s sitcom reboot?

Here’s who Anthony interviewed:

Normally, we list each investor’s responses separately, but for this survey, we grouped their responses by question. Some readers say they use our surveys to study up on an individual VC before pitching them, so let us know which format you prefer.

Image Credits: Nigel Sussman (opens in a new window)

Data analytics platform Databricks is reportedly raising new capital that could value the company between $27 billion and $29 billion.

By the end of Q3 2020, Databricks had surpassed a $350 million run rate — a $150 million YoY increase, reports Alex Wilhelm.

At the time, he described the company as “an obvious IPO candidate” with “broad private-market options.”

Which begs the question: “Can we come up with a set of numbers that help make sense of Databricks at $27 billion?”

Image Credits: Natalia Timchenko (opens in a new window) / Getty Images

Rapid shifts in the way we buy goods and services disrupted old-school marketplaces like local newspapers and the Yellow Pages.

Today, I can use my phone to summon a plumber, a week’s worth of groceries or a ride to a doctor’s office.

End-to-end operators like Netflix, Peloton and Lemonade take a lot of time and energy to reach scale, but “the additional capital required is often outweighed by the value captured from owning the entire experience.”

Image Credits: Nigel Sussman (opens in a new window)

On January 25, Social Capital CEO Chamath Palihapitiya tweeted that he was making two blank-check deals.

Enterprise SaaS company Latch makes keyless entry systems; Sunlight Financial helps consumers finance residential solar power installations.

“There are nearly 300 SPACs in the market today looking for deals,” noted Alex Wilhelm, who unpacked both transactions.

“There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months.”

Image Credits: dan tarradellas (opens in a new window) / Getty Images

On Monday, we published the Matrix Fintech Index, a three-part study that weighs liquidity, public markets and e-commerce trends to create a snapshot of an industry in perpetual flux.

For four years running, the S&P 500 and incumbent financial services companies have been outperformed by companies like Afterpay, Square and Bill.com.

In light of steady VC investment, increasing consumer adoption and a crowded IPO pipeline, “fintech represents one of the most exciting major innovation cycles of this decade.”

Image Credits: Acquia

On January 15, 2001, then-college student Dries Buytaert released Drupal 1.0.0, an open-source content-management platform. At the time, about 7% of the world’s population was online.

After raising more than $180 million, Buytaert exited to Vista Equity Partners for $1 billion in 2019.

Enterprise reporter Ron Miller interviewed Buytaert to learn more about his 18-year journey.

“His story is compelling, but it also offers lessons for startup founders who also want to build something big,” says Ron.

Powered by WPeMatico

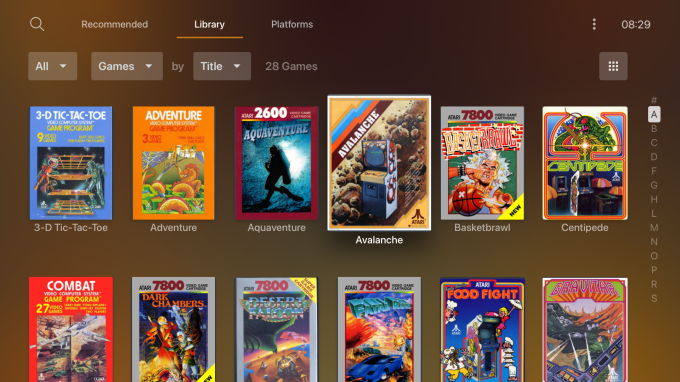

Plex, the media software maker that’s expanded into streaming in recent years, is adding to its service once again with today’s launch of game streaming. Unlike other game streaming efforts from companies like Microsoft or Google, the new “Plex Arcade” isn’t focused on top gaming titles and new releases, but rather on retro games. At launch, the service is offering around 30 games, including titles like Asteroids, Centipede, Missile Command, Adventure and Ninja Golf.

The game streaming service was spun out of Plex’s in-house incubator, Plex Labs, and represents more of a passion project for the company, rather than some larger shift in direction, we’re told. The technology to make it available was already 95% built, so the team decided to put together the game streaming service as a surprise for users, as well as a way to expand Plex’s core mission of becoming a broader entertainment platform.

The company says it actually kicked around the idea of adding games to Plex for years, but over the course of 2020 in particular, the team was drawn to the idea even more out of personal interest and a need for a distraction.

Image Credits: Plex

The game service was built with the help of new partner Parsec and its underlying, low-latency streaming technology, Plex says. This made it possible to bring fully playable game libraries to Plex.

To build the game library, Plex partnered with Atari to license a catalog of classic titles.

At launch, the full list of games include: 3D Tic-Tac-Toe, Adventure, Alien Brigade, Aquaventure, Asteroids, Avalanche, Basketbrawl, Centipede, Combat, Dark Chambers, Desert Falcon, Fatal Run, Food Fight (Charley Chuck’s), Gravitar, Haunted House, Human Cannonball, Lunar Battle, Lunar Lander, Major Havoc, Millipede, Missile Command, Motor Psycho, Ninja Golf, Outlaw, Planet Smashers, Radar Lock, Sky Diver, Sky Raider, Solaris and Super Breakout.

Due to the partnership and licensing fees involved with the project, Plex Arcade will not be a free addition.

Instead, it will be offered as a separate subscription for $2.99 per month for existing Plex Pass subscribers (Plex’s existing $4.99/mo plan). For nonsubscribers, Plex Arcade is $4.99 per month. A free, 7-day trial is also available.

Plex Arcade’s server will require either a Windows or Mac to run (due to Parsec’s limitations), which means it won’t work on Linux, NAS devices or NVIDIA Shield. Gameplay, meanwhile, is restricted to iOS, Android (mobile or TV), tvOS and the Chrome web browser.

It will also support Bluetooth and USB game controllers that are compatible with your device, or you can use a keyboard for Chrome-based gaming. Plex recommends the Sony DualShock 4 or Xbox One controller for the best results.

Image Credits: Plex

The company is taking a wait-and-see approach to expanding the service over time. If it demonstrates interest and traction in the form of subscriptions, Plex may consider growing it further.

Plex Arcade is the latest addition to what’s now a growing lineup of entertainment options for Plex users.

Over the past several years, the media software company has moved beyond being a tool to organize home media collections to also allow users to do things like stream live TV from an antenna or via the web, listen to music and podcasts, watch ad-supported movies and TV, watch the news and more.

These efforts are slowly paying off in terms of user growth. In 2017, Plex had 10 million registered users. A couple of years later, it had 15 million. Today, Plex says it has 25 million users.

Plex Arcade is available as of today.

Powered by WPeMatico

The digital media industry will give us plenty to talk about this year.

When we last surveyed venture capitalists about their media investments, the big topic was the impact that the pandemic would have on the industry, and on the prospects for new startups.

Obviously, the pandemic hasn’t gone away, but when asked to predict the biggest storylines for 2021, VCs pointed to themes as varied as new distribution models, new kinds of interactivity, new tools for creators, the return of advertising business models and even the role of media in a democratic society.

“We are headed toward a content universe where consumers’ power of choice grows to new heights — what premium content to consume and pay for, and how to consume it,” Javelin’s Alex Gurevich wrote. “The consumers will have the final choice! Not traditional media and content distribution companies.”

For this new survey, we heard from 10 VCs — nine who invest in media startups, plus a tenth who’s seeing plenty of media pitches and was happy to share her thoughts. We asked them about the likelihood of further industry consolidation, whether we’ll see more digital media companies take the SPAC route and of course, what they’re looking for in their next investment.

Here’s who we surveyed:

Read their full responses below.

Daniel Gulati: Defining media’s role in a democratic society. What accountability exists when an individual company’s pursuit of scale leads to the spread of disinformation? When a platform’s terms of service appears to collide with constitutional rights, who makes the call and what happens? To what extent should governments support the viability of local media organizations in the face of global competition and a rapidly changing digital landscape?

These are high stakes issues that will be front and center through the year.

Alex Gurevich: The continued disruption of content distribution models, whether that’s the debundling of cable via the plethora of SVOD services, or the way new content is released (i.e., on-demand at home versus movie theaters). We are headed toward a content universe where consumers’ power of choice grows to new heights — what premium content to consume and pay for, and how to consume it. The consumers will have the final choice! Not traditional media and content distribution companies. The pandemic has greatly accelerated this trend.

Matthew Hartman: The two largest social networks, Twitter and Facebook, removed the account of a sitting president and a set of related, follower accounts. This has fundamentally reset the media stack. This will accelerate action the government had already planned to take, including to reshape Section 230. The ripples will be felt throughout media, affecting how news is distributed through social media, what startups can use bigger platforms to grow, what the exit options are for small talent acquisitions and the fragmentation already occurring.

Second, the rise of synthetic media. Algorithmically enhanced or created media is a shift we identified at Betaworks in 2018 and in 2021 it will only increase in scale and scope. Yes, this affects deep fake detection (with companies like Sensity.AI leading the way) and other nefarious uses — but it will also start to fundamentally reshape the way media is created, from the cost of animation to the cost of writing stories, to editing and creating CGI.

Third, game streaming will continue to grow, with audiences that are starting to blow away those of regular TV. An enormous number of people tuned in last year to watch Alexandria Ocasio-Cortez play Among Us on Twitch with popular streamers (she hit 435,000 concurrent viewers at one point). And that wasn’t even close to the biggest event ever on Twitch, David Martinez, aka TheGrefg, hit 2.4 million concurrent viewers for the unveiling of his new Fortnite skin. Game publishers have finally started to understand the power of streamers not just to launch a new game, but to revive old ones, with games that groups of streamers can play together (like Among Us or Rust) soaring in popularity this past year.

Jerry Lu: The emergence of interactive media platforms outside of just gaming.

Because of their isolation due to COVID, people are yearning for social interaction and we’re seeing greater engagement across platforms like Twitch and Zoom, which make interactive communications possible. Previous iterations of media platforms were top-down broadcast, whereby companies produced content they thought consumers would like. Over the past five years, we’ve started to see a greater shift toward the long tail, whereby content comes straight from the consumer.

Gaming and esports were at the forefront of this shift from passive content viewing to interactive entertainment experiences. I believe that 2021 will be the year when we see platforms beginning to embrace interactivity as a form of audience participation, blurring the line between viewer and active participant. I’m excited at the prospect of seeing this form of interactive content consumption applied to other sectors, like education, childcare and commerce, to name a few.

Jana Messerschmidt: We will see a proliferation of products that enable content creators to build businesses outside of traditional media companies. These creators will leverage their existing brand, following and social media engagement to become entrepreneurs, building revenue streams across multiple different products.

There are a plethora of new tools for creators: for writers (Substack, Medium), personalized video shoutouts from creators (Cameo*, PearPop), new audio platforms (LockerRoom*, Clubhouse) or all-in-one tools for creators that include merch, subscriptions, tipping and more (FourthWall* ). Now is the time for creators to be rewarded by their fans for their content creation.

Historically, the big social platforms (Facebook, Instagram, Snap*, Twitter, TikTok) have failed to create meaningful paths for their creators to monetize. They make money from advertisers and thus their resources are focused on those advertising customer demands.

Michael Palank: If 2020 was the year every major media company either announced or grew their direct-to-consumer video/audio/gaming offering, 2021 will be the year where those offerings optimize and differentiate or die. We expect the hunger for original content to continue, but we feel the type of content will continue to diversify from both a story and IP perspective and a format perspective. It is not unthinkable that a major media company like Apple, Amazon or Disney looks to acquire Clubhouse in 2021.

As the lines between video games and filmed entertainment continue to blur we can also envision new companies popping up to take advantage of this trend. I also feel these content platforms will need to differentiate by way of better discovery and personalization.

I fully expect every major media company from Disney to Apple to Amazon to Microsoft will be looking for new and innovative ways to separate themselves from the rest of the pack in 2021.

Marlon Nichols: I think that the continued creation of streaming platforms from content creators/owners (e.g., Disney+, HBO Max, etc.) will force downward subscription pricing adjustments across the board and streaming platforms will need to revisit advertising as a revenue stream. That said, we know that watching ads on a paid platform won’t fly with consumers so I believe we’ll see contextually relevant product placement become the accepted form of brand/content collaboration going forward. I led MaC’s investment into Ryff because of this thesis.

Pär-Jörgen Pärson: Institutions and legislators will have a big effect on social media platforms. I think there will be pushes on antitrust behavior, and social networks will have to behave like media — meaning that they also need to take responsibility for the content that’s on their platform, not only from a user agreement standpoint like today but from an editorial standpoint. I think we’ll see many more editors-in-chief in this industry, as editorial becomes more and more important in our polarized world. This has the potential to change the social media platform landscape quite dramatically, and I’m not entirely sure yet on the long-term impact commercially.

M.G. Siegler: It’s sort of boring, but I wouldn’t be shocked if we see a swing back toward advertising-based models. I think there are two parts to this: First, if and when the pandemic recedes, I think a lot of traditional big advertising players like travel, will come roaring back. Second, it feels like there’s been a move away from advertising to paid subscriptions for a while now and I think these things are cyclical.

To be clear, I think both will continue to exist, I just think that after years of underindexing on paid subs, now we’re perhaps on the verge of overindexing on it … Obviously, advertising never went away, I just think it may be due for a bit of a renaissance (though I say that hoping the powers that be make those ads a better user experience — I think that’s the only way there’s not another backlash against them).

Laurel Touby: The biggest trend in digital media will be companies that don’t call themselves media companies, but that clearly draw from the business model playbook of media companies. For example: Companies that monetize their communities by giving sponsors and advertisers access to their audiences; or technology startups that sell wearable products and upsell their customers with access to premium high-value content.

Hans Tung: Contextual social networks: Video and livestreaming with the likes of TikTok and with other players like Instagram and Snap will continue to drive creativity and engagement. Clubhouse is now garnering a lot of attention as audio captures the attention of a new generation. This also creates new opportunities for established audio players like YY or Ximalaya. At the same time, apps like Clubhouse are an evolution of Snap or Twitter where influencers of all sorts gather to build a new following on new platforms.

However, one of the most interesting things we’re seeing is the emergence of contextual social networks that are focused on solving real-life problems. We see a lot more companies taking the best of audio and video experiences and experimenting with the next iteration of apps like Headspace and Calm, to solve societal issues, personal issues such as how to deal with anxiety, etc. These social networks may not scale as quickly or grab headlines like Clubhouse but they’re designed to bring people together to solve problems. We are also seeing professionalized networks such as Valence or Chief use these audio/video networks to address issues for a particular gender or underrepresented group, or apps that create virtual networking for communities.

Digital media delivered with differentiated experiences: Peloton may not immediately jump to mind as a digital-media company but they are one of the best at producing a high-value experience using extremely high-quality content that goes far beyond simple fitness or even the need for hardware. Increasingly more categories will become “Netflix-ized” where content is king and the experience is delivered through your smartphone.

As with Peloton, the experience is further enhanced with social interaction, such as leader boards, access to the best instructors, etc., which in turn expands the reach of the content. It’s a powerful loop that is driven by quality content, and the components feed off each other to make it more accessible. If you then couple it with Affirm to make it more affordable, you’ve got a flywheel on steroids. This pattern will emerge in other categories.

Consumerization of enterprise communication: Another aspect of media is communication, which we are seeing evolve in the enterprise space. It started with Slack a few years ago and Zoom more recently. Now with companies like Yak or the emergence of various conference apps, we see a higher usage frequency between companies, companies and their customers, and within the enterprise itself.

Powered by WPeMatico

Taboola is the latest company seeking to go public via special purpose acquisition company — more commonly known as a SPAC.

To achieve this, it will merge with ION Acquisition Corp., which went public in 2020 with the aim of funding an Israeli tech acquisition (Haaretz reported last month that Taboola was in talks with ION). The transaction is expected to close in the second quarter, and the combined company will trade on the New York Stock Exchange under the ticker symbol TBLA.

Founded in 2007, Taboola powers content recommendation widgets (and advertising on those widgets) across 9,000 websites for publishers including CNBC, NBC News, Business Insider, The Independent and El Mundo. It says it reaches 516 million daily active users while working with more than 13,000 advertisers.

The company had previously planned to merge with competitor Outbrain before the deal was canceled last fall, with sources pointing to the market impact of the COVID-19 pandemic, a “challenging culture fit” and regulatory issues to explain the deal’s end.

Taboola’s founder and CEO Adam Singolda (pictured above, left) told me that this didn’t lead directly to the SPAC deal. But he said, “I always wanted to go public,” which wasn’t possible while the merger was in the works. Once that deal was called off, and with 2020 turning out to be a strong year for Taboola — it’s projecting revenue of $1.2 billion, including $375 million ex-TAC revenue (revenue after paying publishers), with over $100 million in adjusted EBITDA — the time seemed right, and ION seemed like the right partner.

“We believe Taboola is an open web recommendation leader which is well positioned to challenge the walled gardens,” said ION CEO Gilad Shany in a statement. “We were looking to merge with a global technology leader with Israeli DNA and we found that in Taboola. The combination of long-term partnerships built by the company with thousands of open web digital properties, their direct access to advertisers, massive global reach and proven AI technology, allows Taboola to provide significant value to their partners while also achieving attractive unit economics as the company grows.”

The deal will value Taboola at $2.6 billion. Through this transaction, the company plans to raise a total of $545 million, including $285 million in PIPE financing secured from Fidelity Management & Research Company, Baron Capital Group, funds and accounts managed by Hedosophia, the Federated Hermes Kaufmann Funds and others.

Singolda said that the company plans to invest $100 million in R&D this year, and that he hopes to expand the technology into areas like e-commerce and TV advertising, with the goal of moving “beyond the browser.” More broadly, he said he wants Taboola to be “a strong public company that champions the open web.”

“The open web is a $64 billion advertising market [according to Taboola estimates], but there’s no Google for the open web,” he said.

Yes, Google itself spends plenty of time talking about similar ideas, but Singolda argued that while Google has consumer products like search and YouTube that compete with other publishers for time and attention, “Taboola is not in the consumer business … We serve our partners, and it’s in our identity to drive audience growth, engagement and revenue.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week we — Natasha and Danny and Alex and Grace — had more than a little to noodle over, but not so much that we blocked out a second episode. We try to stick to our current format, but, may do more shows in the future. Have a thought about that? equitypod@techcrunch.com is your friend and we are listening.

Now! We took a broad approach this week, so there is a little of something for everything down below. Enjoy!

Like we said, it’s a lot, but all of it worth getting into before the weekend. Hugs from the team, we are back early Monday.

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Podchaser, a startup building what it calls “IMDB for podcasts,” recently announced that it has raised $4 million in a funding round led by Greycroft.

In other words, it’s a site where — similar to the Amazon-owned Internet Movie Database — users can look up who’s appeared in which podcasts, rate and review those podcasts and add them to lists. In fact, CEO Bradley Davis told me that the startup’s “vibrant, exciting community of podcast nerds” have already created 8.5 million podcast credits in the database.

Davis said this is something he simply wanted to exist and was, in fact, convinced that it had to exist already. When he realized that it didn’t, he posted on Reddit asking whether anyone was willing to build the company with him — which is how he connected with his eventual co-founder and CTO Ben Slinger in Australia. (Podchaser is a fully distributed company, with Davis currently based in Oklahoma City.)

To be clear, Davis doesn’t think podcast nerds are the only ones taking advantage of the listings. Instead, he suggested that it’s useful for anyone looking to learn more about podcasts and discover new ones, with Podchaser’s monthly active users quintupling over the past year.

For example, he said that one of the most popular pages is politician Pete Buttigieg’s profile, where visitors don’t just learn about Buttigieg’s own podcast but see others on which he’s appeared. (You can also use Podchaser to learn more about TechCrunch’s Equity, Mixtape and Original Content podcasts, though those profiles could stand to be filled out a bit more.)

There has been endless discussion about how to fix podcast discovery, and while Davis isn’t claiming that Podchaser will solve it wholesale, he thinks it can be part of the solution — not just through its own database, but through the broader Podcast Taxonomy project that it’s organizing.

“I think if we are successful at standardizing a lot of the terminology, and if we do an analysis of all podcasts, of how popular they are, that [will help many listeners] to cull and find the good stuff,” he said.

Podchaser plans to add new features that will further encourage user contributions, like a gamification system and a discussion system.

While the consumer site is free, the startup recently launched a paid product called Podchaser Pro, which provides reach and demographic data across 1.8 million podcasts. It also monetizes by providing podcast players with access to its credits through an API.

Davis said the startup was “lucky” that it decided to build a database that’s “agnostic” from any specific podcast player.

“So we had a lot of latitude to work with those platforms, we integrate with many of those platforms and you’re going to see a lot of our credits showing up [in podcast players],” he said.

In addition to Greycroft, Advancit Capital, LightShed Ventures, Powerhouse Capital, High Alpha, Hyde Park Venture Partners and Poplar Ventures also participated in the round, as did TrendKite founder A.J. Bruno, Ad Results Media CEO Marshall Williams and Shamrock Capital Partner Mike LaSalle.

“Even in the face of a pandemic, the podcast market continues to grow at a breakneck pace,” said Greycroft co-founder and chairman Alan Patricof in a statement. “The demand from consumers and brands is insatiable. Podchaser’s data and discovery tools are crucial to taking podcasting to new heights.”

Powered by WPeMatico

Apple today announced a new editorial franchise called Apple Podcasts Spotlight, which aims to highlight rising podcast creators in the U.S. The editorial team at Apple will select new podcast creators to feature every month and then give them prominent screen real estate in the Apple Podcasts app and promote them across social media and elsewhere. This will allow creators to reach a wider audience, similar to how the App Store showcases a selection of recommended apps and games with large banners at the top of its screen.

The first Spotlight creator is Chelsea Devantez, who hosts the podcast Celebrity Book Club. On Fridays, Chelsea and special guests including Emily V. Gordon, Gabourey Sidibe, Ashley Nicole Black and Lydia Popovich will meet to discuss the memoirs of “badass celebrity womxn,” as an announcement describes it.

The idea for the show began a year ago when Devantez was reading Jessica Simpson’s memoir and started recapping it on Instagram. The reaction from her followers prompted her to expand the concept into a podcast.

Upcoming episodes will feature Oscar-nominated writer and producer Emily V. Gordon talking Drew Barrymore’s “Little Girl Lost;” actress Stephanie Beatriz discussing Celine Dion’s memoir “My Story My Dream;” Leighton Meester on Carly Simon’s “Boys in the Trees;” and a special Valentine’s Day episode where Chelsea and TikTok star Rob Anderson read Burt Reynolds’ and Loni Anderson’s competing divorce memoirs.

“Apple Podcasts Spotlight helps listeners find some of the world’s best shows by shining a light on creators with singular voices,” said Ben Cave, Global Head of Business for Apple Podcasts, in a statement about the launch. “Chelsea Devantez has created a fun, vibrant space with Celebrity Book Club for listeners to gain new perspectives on the celebrities we thought we knew. We are delighted to recognize Chelsea and Celebrity Book Club as our first Spotlight selection and look forward to introducing creators like Chelsea to listeners each month,” he added.

Apple says future Spotlight creators will be announced monthly from across a range of podcast genres, formats and locations, and will often focus on independent and underrepresented voices. The content is previewed ahead of selection to ensure quality, but there are no specific requirements about the podcast size and reach.

In general, the new Spotlight creators will debut toward the front of the week, but the specific days are fluid to adapt to holidays, major cultural events and others. The next Spotlight selection, for example, will launch in mid-February.

The Spotlight creators will be featured at the top of the Browse tab of Apple Podcasts and will be promoted through the Apple Podcasts social media accounts. Some form of in-app featuring will continue throughout the entire month the creators are in the “spotlight.”

Apple says it will also collaborate with the featured creators on their own channels. Over time, you’ll see promotion via additional Apple-operated channels including outdoor advertising in major U.S. metros.

The news of the new editorial program comes shortly after a report from The Information suggested Apple is working to expand its podcasts platform with the introduction of a podcast subscription service, threatening rivals like Spotify, SiriusXM and Amazon.

Though Apple Podcasts still leads the market, Spotify has been catching up by spending over $800 million on podcast companies, like Anchor, the Ringer, Gimlet Media, and more recently, podcast ad company Megaphone.

SiriusXM, meanwhile, bought podcast management and analytics platform Simplecast, ad tech platform AdsWizz, and podcast app Stitcher. Not to be left out, Amazon just a few weeks ago announced it was acquiring the podcast network Wondery.

Beyond helping the creators grow their audience, Apple says the larger goal with the program is to welcome new audiences to podcasts, in general.

Though podcasts are growing in popularity, the monthly podcast listener base is just 37% in the U.S., according to Edison Research. That means it’s nowhere near being an activity that’s popular among a majority of the U.S. population at this time. Before Apple can effectively monetize podcasts as a subscription service, it needs to help get more people listening to podcasts on a regular basis.

Apple declined to say if the program would expand outside the U.S. at a later date.

Powered by WPeMatico

Bustle Digital Group — owner of Bustle, Inverse, Input, Mic and other titles — could eventually join the ranks of startups going public via a special purpose acquisition company (SPAC).

During an interview about the state of BDG and the digital media industry at the end of 2020, founder and CEO Bryan Goldberg laid out ambitious goals for the next few years.

“Where do I want to see the company in three years? I want to see three things: I want to be public, I want to see us driving a lot of profits and I want it to be a lot bigger, because we’ve consolidated a lot of other publications,” he said.

He added that those goals connect, because by going public, BDG can raise “hundreds of millions dollars,” which Goldberg wants to use to “buy a lot of media companies.”

That might seem like bluster after a year in which many digital media companies (including BDG) had to make serious cuts. But Goldberg said that the company would be profitable in 2020, with revenue that’s “a little bit under $100 million.” And it won’t be the first digital media company to take a similar route — Group Nine created a SPAC that went public last week.

“I want to prove that we can be highly profitable,” he said. “A lot of startups don’t have that goal. A lot of VCs tell their startups: Don’t worry about profits, don’t worry about losing money. I don’t believe in that.”

In addition to his plans to go public, Goldberg also discussed how acquisitions have helped Bustle’s business, his joint venture to purchase W Magazine and digital media’s “overcapitalization” problem. You can read our full conversation, edited for length and clarity, below.

TechCrunch: The last time I caught up with someone at BDG, it was with [the company’s president Jason Wagenheim] and that was when you guys were dealing with the initial fallout [from the pandemic]. Now we’re a lot further into whatever this new world is, so what is your sense of where BDG is now, versus where it was in the early days of the pandemic?

Bryan Goldberg: It might be the craziest, most eventful six months for many of us in our lives. And certainly, for those of us in this industry, the difference between April and October, it’s really hard to fathom, it’s complete night and day. April was a very frightening time for everyone, personally and professionally across the country, across the world.

From an advertising standpoint, it was a really scary time, because we have clients across every industry, and every industry was impacted differently. We have clients who were greatly impacted — theme parks, car makers, hotel companies, airlines — and then we had clients who were not as badly affected, such as a lot of CPG clients, who everybody depended upon so much during the pandemic.

There was a huge pause in our business in in March, April and May. For a lot of clients, tossing advertising was a sort of knee-jerk reaction to the sudden shock of COVID, and so we saw a huge negative impact in our second quarter. What we started to see in the third quarter, and especially now in the fourth quarter, is now that the shock of COVID is behind us, the macro trends that were catalyzed by COVID are now moving into the forefront.

The story of media is no longer about the shock of COVID. The story of media is now about all of the changes to our world, and changes to our industry that were brought about as a consequence of COVID.

The good news for our company, and the good news for other digital media companies, is it looks like the future is being accelerated. It looks like people are watching less television, and so advertisers are moving their budgets into digital faster than they would have had it not been for COVID. Even things like live sports, [their] TV ratings are way down. And a lot of advertisers are saying, “Is there efficacy anymore in cable television or broadcast television?” And the magazine industry was heavily impaired, simply because magazines are a physical medium, and people didn’t want to pass around magazines or read magazines at the dentist’s office, so we probably saw some print budget move into digital as well.

Industry analysts now are going to take up their estimates of what digital revenue is going to look like in 2021, 2022 and beyond. I also think we’ve seen a world in which a lot of brand advertisers are starting to think about what happens when they start to spend beyond Facebook and Google. For most of the last three years, there’s been so much talk about the duopoly, the idea that Facebook and Google are going to eat almost every last dollar of advertising. What we’ve seen in the last three months is advertisers saying that this needs to be the moment in which they learn how to deploy advertising spend digitally beyond Facebook or Google.

No, it doesn’t mean they’re all pulling out of Facebook — Facebook and Google are doing just fine. But there are still tens of billions of dollars that need to be deployed outside of Facebook and Google. And you’re seeing winners such as Snapchat, Pinterest. Both had incredibly strong earnings. They’re benefiting from the same thing that benefits Bustle Digital Group and a lot of other digital media players who aren’t Facebook and Google, which is you’re seeing big ad spenders finally deciding that now’s the time to find other ways to deploy advertising spend.

I think those are the two big trends: Dollars moving to digital out of TV faster than we thought, and major advertisers using now as a time to find other channels beyond Facebook and Google.

So when you look at how that is impacting Bustle’s business, has it returned to pre-COVID levels?

For us, when we reflect upon the year 2020, we see that we had a great first quarter, we see that we’re having an incredible fourth quarter, and we have a big, epic crater in the second and third quarters. So when we look at the year, we basically have to say to ourselves, if it were not for that crater in the second and third quarters, what would this year have looked like? We would have had revenue well in excess of $100 million. Now, we’re gonna have revenue a little bit under $100 million.

But when we think about how we prepare for 2021 and set goals for 2021, we have to set goals for 2021 as though COVID had never happened, we have to set goals for 2021 without using Q2 and Q3 as a sort of excuse for lowering expectations. Because the fourth quarter, the quarter we’re currently in, has exceeded our wildest expectations.

People sort of sat up and took notice of the company because you had a pretty aggressive acquisition strategy. I imagine that strategy had to change a little bit in 2020. To what extent do you feel that ambition is something that you can pick up again?

So to be clear, not only do we feel great about our strategy, our strategy was critical in helping our company survive and ultimately thrive in the wake of the virus. You know, we made two acquisitions [in 2019] — in the science and technology category, we bought Inverse, which is a science and technology publication, and then Josh Topolsky launched a tech-and-gadget publication for us called Input Magazine that’s growing very quickly.

It’s critical that we had that strategy, because no single advertiser category has performed better for us in 2020 than tech — we more than tripled our revenue from technology clients this year, because technology has thrived through COVID. Had we not had an acquisition strategy, had we not diversified into tech media publishing, we certainly would not have had the outcome we had in 2020. That’s just the reality.

Categories like beauty, fashion, retail were very hard hit. Those have traditionally been our bread and butter, and they’re going to be great again, in 2021. But this spring, beauty companies weren’t doing so well, because people weren’t leaving the house. So the strategy worked, in part, because we diversified the categories in which we created content, which allowed us to diversify the advertiser base. And we’re gonna continue full speed ahead in 2021.

Now, you know, we did six acquisitions in 2019. I don’t know if we’ll do six acquisitions in 2021. But I want to do a lot more than one acquisition in 2021.

Powered by WPeMatico

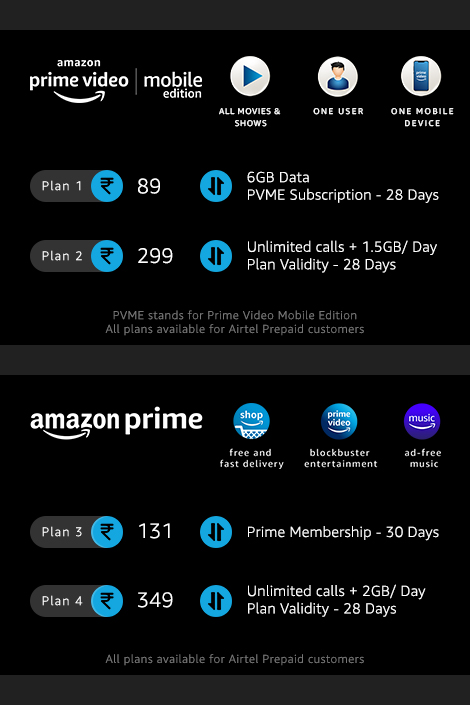

Amazon is doubling down on one of the biggest strengths of its Prime Video streaming service: aggressive pricing.

The e-commerce giant on Wednesday launched Prime Video Mobile Edition, an even more affordable tier of the on-demand video streaming service — now also bundling some mobile data.

Prime Video Mobile Edition, for which Amazon has partnered with Indian telecom network Airtel, will feature 28-day mobile-only, single-user, standard definition (SD) access to customers in India for Rs 89 ($1.22). This tier will include 6GB of mobile data that customers can consume during the subscription period. There’s also a slightly expensive plan for Prime Video Mobile Edition that will charge customers Rs 299 but will offer 1.5GB mobile data for each day of the subscription. To anyone who subscribes to Prime Video Mobile Edition, Amazon says it will pick the tab for the first month.

Amazon Prime subscription costs $1.7 a month in India and includes access to Prime Video and Prime Music.

The new Prime Video plan is currently only available in India. Its launch comes two years after Netflix unveiled a similar plan in India.

Affordable pricing is key for on-demand steaming services that are looking to make inroads in India, the world’s second-largest internet market. Even as more than 600 million users are online in the country today, only a fraction of them currently pay to access digital subscriptions. In a recent report to clients, analysts at Goldman Sachs estimated that gaming and video streaming market in India could clock as much as $5 billion in gross value transactions by March 2025.

“India is one of our fastest growing territories in the world with very high engagement rates. Buoyed by this response, we want to double-down by offering our much-loved entertainment content to an even larger base of Indian customers. Given high mobile broadband penetration in the country, the mobile phone has become one of the most widely used streaming devices,” said Jay Marine, vice president, Amazon Prime Video Worldwide, in a statement.

Airtel, the second-largest telecom operator in India, is the first roll-out partner for Prime Video Mobile Edition, said Sameer Batra, director, Mobile Business Development at Amazon, suggesting that the company may ink similar deals with other telecom operators in the country as it looks to expand the “reach of our service to the entire pre-paid customer base in India.”

Nearly every on-demand video streaming service in India, including Netflix and Disney+ Hotstar, maintain various partnerships with local telecom operators and satellite TV providers to reach more users in the country. Amazon did not explicitly say when or if it plans to extend Prime Video Mobile Edition outside of India.

Powered by WPeMatico