mastercard

Auto Added by WPeMatico

Auto Added by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

One of the biggest gripes about investing apps is that they are not acting responsibly by not educating users properly and allegedly letting them fend for themselves. This can result in people losing a lot of money, as evidenced by the number of lawsuits against Robinhood.

Today, an eight-year-old company that has been focused on nothing but financial education is now offering trading and banking services in the U.S..

Over the years, London-based Invstr has built out an educational platform with features such as an investing academy. It’s created a Fantasy Finance game, which gives users the ability to manage a virtual $1 million portfolio so they can learn more about the markets before risking their own money for real. Via social gamification, Invstr has set out to make the educational process fun.

It has also built a community around users so they can learn from each other (something another Robinhood competitor Gatsby is also doing).

Over 1 million users have downloaded the platform globally.

Invstr, according to CEO and founder Kerim Derhalli, is taking a different approach from competitors by offering education and learning tools upfront. And in addition to giving users the ability to make commission-free stock trades, it’s also giving them a way to digitally bank and invest using their Invstr+ accounts “without ever needing to move money from one place to another.”

Invstr takes it all a step further for subscribers who have access to an “Invstr Score,” performance stats and behavioral analytics among other things.

Derhalli said moving in this direction with the company was part of his business plan from day one.

“I think the most powerful trend in the U.S. is self-directed investing,” Derhalli told TechCrunch. “Younger generations have grown up in an app world and they expect to be autonomous and do things for themselves. Many distrust the banking system, and they don’t want to follow in their parents’ footsteps when it comes to banking and finance. We think this is a massive opportunity.”

In the unveiling of its new offerings, Invstr also announced Wednesday that it has closed on a $20 million Series A in the form of a convertible offering. This builds upon $20 million it previously raised across two seed rounds from investors such as Ventura Capital, Finberg, European angel investor Jari Ovaskainen and Rick Haythornthwaite, former global chairman of Mastercard.

Derhalli said he felt compelled to found Invstr after seeing firsthand how a lack of knowledge and confidence can prevent individuals from starting to invest. He worked for three decades in senior leadership roles at Deutsche Bank, Lehman Brothers, Merrill Lynch and JPMorgan before founding Invstr “so that anyone, anywhere could learn how to invest.”

Invstr is offering its new investing services in partnership with Apex Clearing, which formerly provided execution and settlement services to Robinhood. Its digital banking services are being offered through a partnership with Vast Bank. To address the security piece, Invstr said its user data is also protected by technology from Okta.

The company, which also has offices in New York and Istanbul, plans to use the new capital to launch new brokerage and analytics tools and a portfolio builder.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

Federal regulators have approved Mastercard’s acquisition of Salt Lake City-based startup Finicity, which provides open-banking APIs. The deal is expected to go for $825 million.

“We were notified that the Department of Justice completed its review of our planned acquisition of Finicity and has cleared it to move forward,” Mastercard wrote in a statement. “We are pleased to have reached this milestone.”

Finicity allows users to be able to decide how their financial information is shared and who can make money decisions on their behalf through open APIs. The buy will allow Mastercard to offer consumers and businesses more choice in these transactions, without requiring them to do heavy lifting themselves.

Finicity, according to Crunchbase, has raised nearly $80 million in known venture capital as a private company. When closed, it will be one of the largest fintech acquisitions at nearly $1 billion in 2020.

The DOJ approval comes just two weeks after the body filed an antitrust lawsuit challenging Visa’s proposed $5.3 billion buy of Plaid. Plaid, which empowers a large chunk of financial services through its data network, including Venmo and Acorns, is being accused of making Visa a monopoly in online debt services.

Plaid has denied these claims, saying that “Visa intends to defend the transaction vigorously.” The feds are also looking into Intuit’s $7 billion proposed buy of Credit Karma, which was first announced in February 2020.

The approval of the Mastercard-Finicity transaction could be a shot in the arm for fintech startup valuations. After both the Plaid and Credit Karma deals came under increasing regulatory scrutiny, it was an open questions whether big-dollar M&A was going to be an option for fintech unicorns.

If the path was closed due to regulatory concerns, fintech startups would have to either pursue earlier, smaller sales themselves, or wait for an eventual IPO. If that was the case, venture capitalists might shun putting as much capital to work in the sector. However, the Finicity approval makes it clear that not all fintech M&A worth $500 million or more is going to encounter oversight headaches. That should be welcome news for late-stage fintech valuations.

Powered by WPeMatico

Silverflow, a Dutch startup founded by Adyen alumni, is breaking cover and announcing seed funding.

The pre-launch company has spent the last two years building what it describes as a “cloud-native” online card processor that directly connects to card networks. The aim is to offer a modern replacement for the 20 to 40-year-old payments card processing tech that is mostly in use today.

Backing Silverflow’s €2.6 million seed round is U.K.-based VC Crane Venture Partners, with participation from Inkef Capital and unnamed angel investors and industry leaders from Pay.On, First Data, Booking.com and Adyen. It brings the fintech startup’s total funding to date to ~€3 million.

Bootstrapped while in development and launching in 2021, Silverflow’s founders are CEO Anne-Willem de Vries (who was focused on card acquiring and processing at Adyen), CBDO Robert Kraal (former Adyen COO and EVP global card acquiring & processing of Adyen) and CTO Paul Buying (founder of acquired translation startup Livewords).

“The payments tech stack needs an upgrade,” Kraal tells me. “Today’s card payment infrastructure based on 30 to 40-year-old technology is still in use across the global payment landscape. This legacy infrastructure is costing everyone time and money: consumers, merchants, payment-service-providers and banks. The legacy platforms require a lengthy on-boarding process and are expensive to maintain, [and] they also aren’t fit for purpose today because they don’t support data use”.

In addition, Kraal says that adding new functionality is a lengthy and expensive process, requiring the effort of specialised engineers which ultimately slows down innovation “for the whole card payments system”.

“Finally, every acquirer provides its customer with a different processing platform, which for a typical payment service provider (PSP) means they have to deal with multiple legacy platforms — and all the costs and specialised support each entails,” adds de Vries.

To solve this, Silverflow claims it has built the first payments processor with a “cloud-native platform” built for today’s technology stack. This includes offering simple APIs and “streamlined data flows” directly integrated into the card networks.

Continues de Vries: “Instead of managing a complex network of acquirers across markets with dozens of bank and card network connections to maintain, Silverflow provides card-acquiring processing as a service that connects to card networks directly through a simple API”.

Target customers are PSPs, acquirers and “global top-market merchants” that are seeing €500 million to 10 billion in annual transactions.

“As a managed service, Silverflow provides the maintenance for connections and new product innovation that users have typically had to support in-house or work on long-term product road maps with suppliers,” explains Kraal. “Based in the cloud, Silverflow is infinitely scalable for peak flows and also provides robust data insights that users haven’t previously been able to access”.

With regards to competitors, Kraal says there are no other companies at the moment doing something similar, “as far as we are aware”. Currently, acquirers use traditional third-party processors, such as SIA, Omnipay, Cybersource or MIGS. Some companies, like Adyen, have built their own in-house processing platform.

So, why hasn’t a cloud-native card processing platform like Silverflow been done before and why now? A lack of awareness of the problem might be one reason, says de Vries.

“Unless you have built several integrations to acquirers during your career, you are not aware that the 30 to 40-years-old infrastructure is still in use. This is not typically a problem some bright college graduates would tackle,” he posits.

“Second, to build this successfully, you need to have prior knowledge of the card payments industry to navigate all the legal, regulatory and technical requirements.

“Thirdly, any large corporate currently active in card payment processing will be aware of the problem and have the relevant industry knowledge. However, building a new processing platform would require them to allocate their most talented staff to this project for two-three years, taking away resources from their existing projects. In addition, they would also need to manage a complex migration project to move their existing customers from their current system to the new one and risk losing some of the customers along the way”.

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

Grow Credit, the startup that launched last year to help customers build out their credit scores by providing a credit line for online subscriptions like Spotify and Netflix, has added Mucker Labs as an investor and closed its seed round with $2 million in total commitments.

The Los Angeles startup founded by serial entrepreneur Joe Bayen, had been bootstrapped initially and then received funding from a clutch of core angel investors before signing a deal with Mucker earlier this month, according to Bayen.

Using the Marqeta platform, Grow Credit can extend a loan to customers to expand their subscription services. Using the Mastercard network for payments, and Marqeta’s tools to restrict payment access, Grow offers credit facilities to its customers to pay for their monthly subscriptions. By using Grow Credit for those payments, users can improve their credit scores by as much as 61 points in a nine-month span, says Bayen.

The company doesn’t charge any fees for its loans, but users can upgrade their service. The initial tier is free for access to $15 of credit, once a user connects their bank account. For a $4.99 monthly fee, customers can get up to $50 of subscriptions covered by the service. For $9.99 that credit line increases to $150, Bayen said.

Increases to a user’s credit score can make a significant dent in their costs for things like lease agreements for cars, mortgages for houses and better rates on other credit cards, said Bayen.

“Everything is cheaper, you can get access to a credit card with lower interest rates and better rewards,” he said. “We’re looking at ourselves as the single best route to getting access to an Apple card.”

Additional capital for the new round came from individual investors like DraftKings chief executive, Jason Robins; former National Football League player and hall of famer Ronnie Lott; and Sebastien Deguy, VP of 3D at Adobe.

Coming up, Grow Credit said it has a deal in the works with one very large consumer bank in the U.S. and will be launching the Android version of its app in a few weeks.

Powered by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

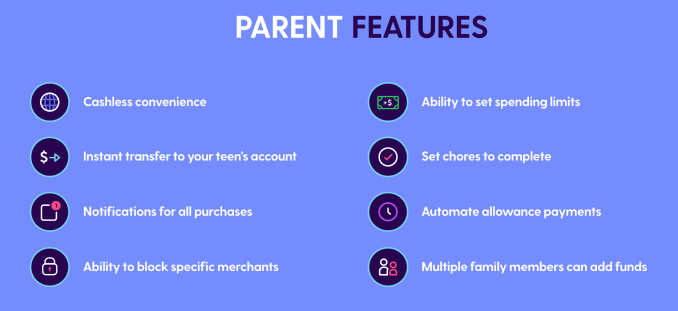

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

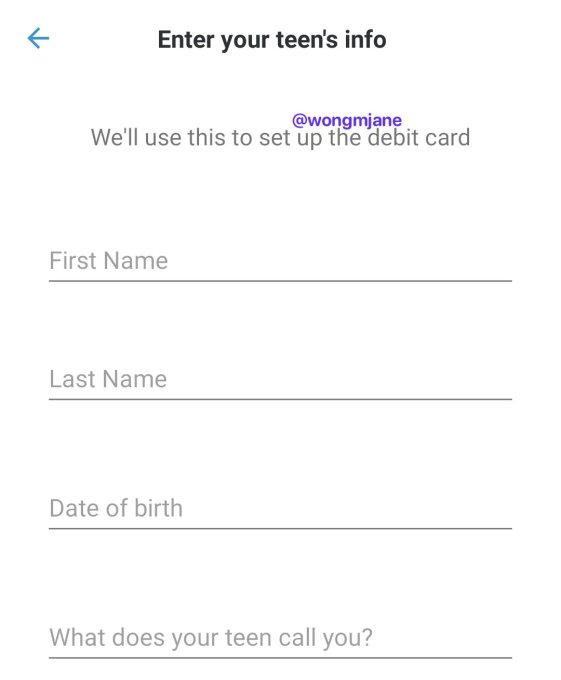

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

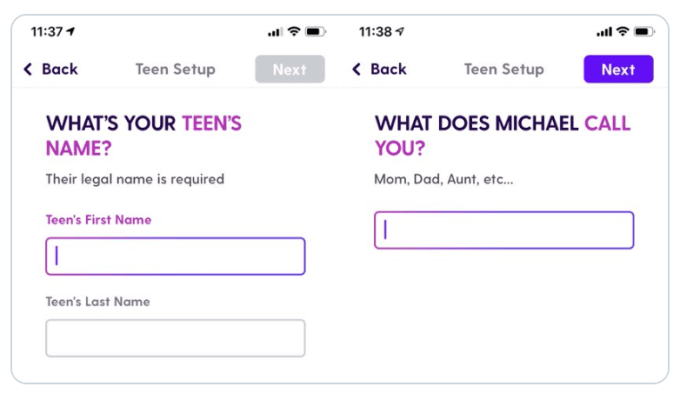

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

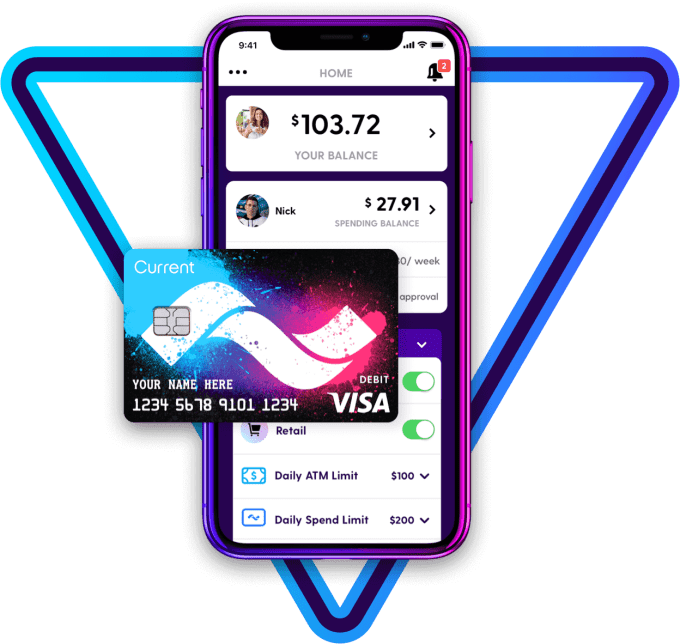

Current’s teen debit card

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

We are living through one of the nation’s longest periods of economic growth. Unfortunately, the good times can’t last forever. A recession is likely on the horizon, even if we can’t pinpoint exactly when. Founders can’t afford to wait until the midst of a downturn to figure out their game plans; that would be like initiating swim lessons only after getting dumped in the open ocean.

When recession inevitably strikes, it will be many founders’ — and even many VCs’ — first experiences navigating a downturn. Every startup executive needs a recession playbook. The time to start building it is now.

While recessions make running any business tough, they don’t necessitate doom. I co-founded two separate startups just before downturns struck, yet I successfully navigated one through the 2000 dot-com bust and the second through the 2008 financial crisis. Both companies not only survived but thrived. One went public and the second was acquired by Mastercard.

I hope my lessons learned prove helpful to building your own recession game plan.

Powered by WPeMatico

Mastercard announced today that it is acquiring RiskRecon, a Salt Lake City startup that uses publicly available data to build security assessments of organizations. The companies did not share the purchase price.

It has become increasingly important for financial services companies like Mastercard to help customers navigate cybersecurity, and RiskRecon will give customers an objective score of a company’s risk profile.

“Through a powerful combination of AI and data-driven advanced technology, RiskRecon offers an exciting opportunity to complement our existing strategy and technology to secure the cyber space,” Ajay Bhalla, president of cyber and intelligence for Mastercard, said in a statement.

RiskRecon CEO Kelly White told TechCrunch in a 2016 interview after the company’s $3 million seed round that the company looks at information that is readily available on the internet and puts it together to measure a company’s overall security risk:

RiskRecon leverages information that is available on the web from companies operating there as part of the act of doing business. “If you stand up web servers and DNS servers, these are intentionally discoverable because they are providing services on the internet. Systems reveal the software being run and version information from which you can determine security performance.”

White sees joining Mastercard as an opportunity to be a part of a larger organization and all that that entails. “By becoming part of their team, we have an opportunity to scale our solution and help companies in new industries and geographies take steps to better manage their cybersecurity risk,” he said in a statement.

RiskRecon launched in 2015 and has raised $40 million, according to Crunchbase data. Investors included Accel, Dell Technologies Capital, General Catalyst and F-Prime Capital.

It’s worth noting that the company was not alone in the space, competing with New York City-based SecurityScoreCard, which launched in 2013 and has raised over $112 million, according to Crunchbase. The last investment came in June for $50 million.

Today’s deal is subject to standard regulatory approval, but is expected to close in the first quarter in 2020.

Powered by WPeMatico