mastercard

Auto Added by WPeMatico

Auto Added by WPeMatico

There’s a strategic cost to the defection of Visa, Stripe, eBay, and more from the Facebook -led cryptocurrency Libra Association . They’re not just names dropping off a list. Each potentially made Libra more useful, ubiquitous, or reputable. Now they could become obstacles to the token’s launch or growth.

Fearing regulators’ inquiries not just into their Libra involvement but the rest of their businesses, these companies are pulling out at least for now. None had made precise commitments to integrating Libra into their products, and they’ve said they could still get involved later. But their exit clouds the project’s future and leaves Facebook to absorb more of the blowback.

Here’s what each of the departing Libra Association members brought to the table and how they could spawn new challenges for the cryptocurrency:

With one of most widely-accepted payment methods, Visa could have helped make Libra universally spendable. It’s also one of the most prestigious names in finance, lending deep credibility to the project. Visa’s departure leaves Libra looking more like tech companies barging into payments, conjuring fears of their move fast, break things approach that could cause financial ruin if Libra runs into problems. It also could leave Libra with a much weaker presence in brick-and-mortar shops. No one will want to own a cryptocurrency that doesn’t appreciate in value and can’t be easily spent.

The involvement of MasterCard alongside Visa made Libra look like the incumbents adapting to modern technologies. This made it less threatening, and gave cryptocurrency an air of inevitability. MasterCard would have also brought an even wider network of locations where Libra could one day be used for payment. Now MasterCard and Visa might actively work against Libra to prevent their payment methods being made obsolete by Libra and its elimination of transaction fees through the blockchain. Two of Libras biggest allies could become its biggest foes.

Facebook has repeatedly told regulators that its Calibra app plus integrations into Messenger and WhatsApp would not be the only Libra wallets, pointing to PayPal . Facebook’s head of Libra David Marcus told Congress when asked about the social network’s outsized power to exploit Libra through its own Calibra wallet that “you have companies like PayPal and others that will, of course, collaborate, but [also] compete with us”. Now Facebook won’t have a scaled payment method it doesn’t own to point to as a likely alternative for people who don’t want to trust Facebook’s Calibra, Messenger, or WhatsApp to be their Libra wallet. The Libra Association also loses PayPal’s enormous network of online merchants that accept it, plus the inroad to integration into its peer-to-peer payback app Venmo. PayPal convinced the mainstream public to trust online payments — the exact kind of trust Facebook desperately needs. The fact that Marcus was also the former president of PayPal but couldn’t keep it in the association raises concerns about the group’s coalition-building prowess.

Stripe’s enormous popularity with ecommerce vendors made it a valuable Libra Association member. Together with PayPal, Stripe facilitates a huge portion of online transactions outside of China. Its ease of integration made it a top pick for developers Facebook surely hoped would build atop Libra. Stripe’s exit destroys a critical bridge to the fintech startup ecosystem that could have helped institutionalize Libra. Now the association will have to work on engineering payment widgets from scratch without Stripe’s assistance, which could slow adoption if it ever launches.

There’s a clear reason all these payment processors bailed. Senators Brian Schatz (D-HI) and Sherrod Brown (D-OH) wrote a letter to Visa, MasterCard, and Stripe’s CEOs this week explaining that “If you take this on, you can expect a high level of scrutiny from regulators not only on Libra-related activities, but on all payment activities.”

As one of the longest standing ecommerce companies, eBay bolstered beliefs that Libra could be used to power transactions between untrusted strangers without a costly middleman. It might have also put Libra into practice on one of the top western online marketplaces outside of Amazon. Without destinations like eBay onboard, average netizens will have fewer opportunities to be exposed to Libra’s potential to eliminate transaction fees.

One of the lesser-known Libra Association members, Mercado Pago helps merchants receive payments via email or in installments. The idea of connecting financially underserved populations has been core to Facebook’s pitch for why Libra should exist. The Libra Association has been light on the details of how exactly it serves this demographic, relying on the inclusion of partners like Mercado Pago to help it figure this out later. Mercado Pago’s departure leaves Libra looking more like a financial power grab rather than a tool to assist the disadvantaged.

On Monday, the remaining Libra Association members will meet to finalize the initial member list, elect a board, and create a charter to govern the project. This forced the hands of the companies above, who had their last chance to depart this week before being pulled deeper into Libra.

UNITED STATES – JULY 16: David Marcus, head of Facebook’s Calibra digital wallet service, prepares to testify during the Senate Banking, Housing and Urban Affairs Committee hearing on “Examining Facebook’s Proposed Digital Currency and Data Privacy Considerations” on Tuesday, July 16, 2019. (Photo By Bill Clark/CQ Roll Call)

Who’s left includes venture capital firms, ride sharing companies, non-profits, and cryptocurrency companies. They are less tied up with the status quo of payment processing, and therefore had less to lose. The blockchain-specific companies were likely hoping to piggyback on financial giants like Visa to get Libra approved and create more legitimacy for their industry as a whole.

These partners could help fund an ecosystem of Libra developers, create daily use cases, spread the system in the developing world, and push for alliances between Libra and cryptocurrency players. Facebook will need to fight to keep them aboard if it wants to avoid Libra looking like a unilateral disruption of the economy.

For Libra to actually launch, Facebook needs to make serious concessions and divert from its initial vision. Otherwise if it continues to butt heads with regulators, more members could flee. One option floated by Libra Association member Andreessen Horowitz’s a16z Crypto partner Chris Dixon was for Libra to be denominated in US dollars instead of a basket of international currencies. That might lessen fears that Libra intends to compete directly with the dollar.

It’s become apparent that Facebook will not get its ideal cryptocurrency out the door. This is the brand tax of 100 scandals coming back to bite it. Now the best it can hope for is to get even a watered-down version launched, prove it can actually help the underbanked, and then hope to convince regulators it’s well-intentioned.

Powered by WPeMatico

Financial service companies like banks have seen some of their business cannibalised over the years with the rise of digital-based alternatives — often in the form of apps — that provide lower fees, faster responsiveness and more flexibility to consumers. Today, Toronto-based startup Flybits is announcing $35 million in funding for a platform that it believes can offer these banks a way of continuing to capture their users’ attention and help them pivot into the next generation of services, financial or otherwise.

Today, a typical end product for a customer of Flybits’ services will use insights to upsell a customer by offering financial services; for example, a bank providing an offer of a specific kind of loan or credit card that you are more likely to take; or to offer a loyalty program or rewards for usage. But the longer-term goal, said CEO and co-founder Hossein Rahnama, is to help its customers take on a bigger role as repositories that can be used for more than just money, and used beyond the walls of the bank.

“We don’t think banks will go away, as some do, but we think that they could have a role not just as money vaults, but as data vaults: a place where you can deposit data, which you trust,” he said in an interview. Indeed, some of the funding will be used to put into action some of the AI and machine learning patents the startup has amassed, with the building of a “data” marketplace for banks, fintechs and other data providers to partner and build more services together.

The Series C comes from an interesting group of investors that includes both strategic backers using Flybits’ services, as well as backers of the more non-strategic, financial kind. Led by Point72 Ventures (hedge fund supremo Steve Cohen’s VC fund), the list also includes Mastercard, Citi Ventures and Reinventure (the fund backed by Australia’s Westpac Banking Corporation), Portag3 Ventures, TD Bank and Information Venture Partners. Valuation is not being disclosed, and prior to this the company had raised around $15 million.

Much like another marketing tech company, Near — which today announced $100 million in funding — the premise that underpins Flybits’ technology is that there is a lot of disparate data out there that, if it’s treated correctly, can uncover a lot more insights about consumer behavior, and that by and large many companies are missing this opportunity because they haven’t found the right way of merging the data to unlock insights.

While Near is applying this to location-based data and a range of different verticals, Flybits’ primary target has been banks and the data that they and other financial services providers already possess.

Many smaller startups in the world of financial services have stolen a march on bigger incumbents by building personalization into their products from the ground up. (Indeed, some like Step, aimed at teens, are so personalised that they will actually change their service mix as their customer base grows up and needs new products.) This is something that incumbents might have been more readily able to do in the old days, when people knew their bank managers and tellers and made daily trips into branches to transact. In the digital age they have fallen behind and are now catching up.

Flybits’ investors have spotted that and this in part is why they are banking on technologies like this to help bigger companies catch up, not just in financial services (although with banking alone estimated to be a €6.9 trillion industry, this is clearly a good start).

“Personalization is mission-critical for all D2C businesses in the digital age. Flybits’ integrated platform allows financial services firms to offer contextualized experiences, driving product awareness and adding significant value to the lives of their customers,” said Ramneek Gupta, managing director and co-head of Venture Investing at Citi Ventures, in a statement. “We look forward to partnering with Flybits in its next phase of growth as it continues to set the bar for hyper-personalized customer experiences.”

Indeed, it’s not just banks that are working on upselling, or that have large repositories of data that are not used as well as they could be.

“Mastercard and Flybits share a vision on using data driven insights to enrich consumers’ experiences,” said Francis Hondal, president, Loyalty & Engagement at Mastercard, in a statement. “Our ultimate goal is to develop products and services that engage consumers in a highly contextual manner. Through this collaboration with Flybits, we’ll be able to offer rich, personalized experiences for them throughout their journeys.”

Powered by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

What if, instead of sitting on your phone on the sofa ordering stuff from Amazon, you could buy the same things locally from local stores that ultimately enliven and enrich your local neighborhood? What if by doing that, you wouldn’t be walking through deserted main streets, past boarded-up shops, dark alleys and graffiti? What if someone created a marketplace for independent businesses, local events and experiences that kept the money in the local economy rather than being siphoned off into global giants who don’t care about human-scale communities?

That’s the idea behind Pixie, a new take on the “shop-local app” startup model which, although it’s been tried before, has never quite managed to take off. Perhaps Pixie will have more luck?

Here’s how it works: The Pixie app connects people to independent businesses through a curated marketplace, incentivizing them to pay through the app and get rewarded for being loyal customers. Integrated into the app is Pixie Pay, a bespoke payment solution which keeps money in local hands.

The startup has a fascinating background. Whilst serving in the British Special Forces, Pixie’s founder Greg Barden understood that his mission was also to ‘win hearts and minds’ with the local population. Whether by buying bread from the local baker in a village in Afghanistan, or coffee from the market in Baghdad, he and his soldiers could tear down even the most hostile barriers.

He also realized that when more money stayed inside these the local economies rather than being sucked away by organized crime or large scale, globalized businesses, the local economy might flourish and the risk of the societies there becoming yet again destabilized could potentially diminish.

“Whether it was stalls in the bazaars of Baghdad or small boutiques on Bath high-street, I realized independent shop owners are linchpins in their community. They add variety to the mundane and nurture community spirit. Even local guardians need protecting sometimes, which is why we created Pixie.”

The threat to independent stores from globalization and digitization isn’t just happening in Afghanistan. Across the western world, ‘Main Street’ stores are closing at a prodigious rate. In the UK over 1,500 local stores closed in 2018. (And that was BEFORE Brexit…)

Pixie has stress-tested its idea in mid-sized town in the UK, including Bath, Frome and Sherbourne, completing transactions across 250 businesses, ranging from cafes to fashion boutiques, and spinning up 5,000 app users. It’s now going on the fund-raising trail, aiming to raise £500,000 in funding through its ‘Equity for Explorers’ campaign on Crowdcube a UK-based crowd-equity platform. The total addressable market for independent business in the UK is estimated to be £31.5bn in gross transactional value.

Barden — who last year spoke about his startup life at the launch of the military tech non-profit TechVets — says: “There might be thousands of independent businesses across the UK, but at the rate the high-street is disappearing they are severely under threat. Pixie isn’t here to turn people away from the bigger players on the high-street, but create opportunities for enriching discovery. Needless to say, in a world with increasing nationalism, Brexit, Trump and — dare I say it — Amazon, we feel Pixie has a huge part to play in countering the worst aspects of globalization.”

Pixie’s revenue comes from transaction fees taken when people use its ‘Pixie Pay’ payment mechanism. The payment system is designed to bypass Visa/Mastercard at the point of sale, whilst the loyalty scheme unites independent businesses under one umbrella, so the users can earn and spend their loyalty points (as money) across the entire Pixie community. If a store using Pixie is in Australia, a person from Bath could also use their points there. This keeps the money circulating inside local, independent stores, wherever they are on the planet.

Pixie distributes its own payment terminal that sits next to whatever the business has in place to take normal card payments (iZettle etc). The cards are contactless but don’t utilise visa MasterCard. It’s literally their own e-money system. Think PayPal where users can either add money to their balance by debit card or bank and/or link a debit card to Pixie if they don’t have a balance.

Obviously this also creates it an alternative to competitors like iZettle, Square, SumUp and WorldPay, but this time specifically aimed at local independent stores, not huge national and international chains.

The third element of Pixie is its discovery marketplace that gives its community of explorers (users) the ability to discover local businesses across the Pixie footprint of stores.

I’ve seen several startups try and tackle this problem, but it may well be that Pixie, under its charismatic leader, finally has a shot at cracking this idea around local markets.

Powered by WPeMatico

Redis Labs, a startup that offers commercial services around the Redis in-memory data store (and which counts Redis creator and lead developer Salvatore Sanfilippo among its employees), today announced that it has raised a $60 million Series E funding round led by private equity firm Francisco Partners.

The firm didn’t participate in any of Redis Labs’ previous rounds, but existing investors Goldman Sachs Private Capital Investing, Bain Capital Ventures, Viola Ventures and Dell Technologies Capital all participated in this round.

In total, Redis Labs has now raised $146 million and the company plans to use the new funding to accelerate its go-to-market strategy and continue to invest in the Redis community and product development.

Current Redis Labs users include the likes of American Express, Staples, Microsoft, Mastercard and Atlassian . In total, the company now has more than 8,500 customers. Because it’s pretty flexible, these customers use the service as a database, cache and message broker, depending on their needs. The company’s flagship product is Redis Enterprise, which extends the open-source Redis platform with additional tools and services for enterprises. The company offers managed cloud services, which give businesses the choice between hosting on public clouds like AWS, GCP and Azure, as well as their private clouds, in addition to traditional software downloads and licenses for self-managed installs.

Redis Labs CEO Ofer Bengal told me the company’s isn’t cash positive yet. He also noted that the company didn’t need to raise this round but that he decided to do so in order to accelerate growth. “In this competitive environment, you have to spend a lot and push hard on product development,” he said.

It’s worth noting that he stressed that Francisco Partners has a reputation for taking companies forward and the logical next step for Redis Labs would be an IPO. “We think that we have a very unique opportunity to build a very large company that deserves an IPO,” he said.

Part of this new competitive environment also involves competitors that use other companies’ open-source projects to build their own products without contributing back. Redis Labs was one of the first of a number of open-source companies that decided to offer its newest releases under a new license that still allows developers to modify the code but that forces competitors that want to essentially resell it to buy a commercial license. Ofer specifically notes AWS in this context. It’s worth noting that this isn’t about the Redis database itself but about the additional modules that Redis Labs built. Redis Enterprise itself is closed-source.

“When we came out with this new license, there were many different views,” he acknowledged. “Some people condemned that. But after the initial noise calmed down — and especially after some other companies came out with a similar concept — the community now understands that the original concept of open source has to be fixed because it isn’t suitable anymore to the modern era where cloud companies use their monopoly power to adopt any successful open source project without contributing anything to it.”

Powered by WPeMatico

Apple’s mobile payment technology has finally launched in Germany, some four years after it debuted in the U.S.

On its newly launched Apple Pay website for Germany, Apple lists partner banks and credit card companies at launch, with customers from the likes of Deutsche Bank, O2 Banking, N26, Comdirect, HypoVerensbank, Bunq and Boon able to tap up the payment method directly.

Some fifteen banks and services are supported at launch. A further nine banks are slated as adding support in 2019, including DKB, INK and Revolut.

iOS users in the country can now add supported debit or credit cards to Apple Pay to make contactless payments with their device, rather than having to carry cash. Apple’s Face ID and Touch ID biometrics are used to a security layer to the payment system.

The local Apple Pay site also lists a selection of retailers, with Apple writing: “Apple Pay works in supermarkets, boutiques, restaurants, hotels and many other places. You can also use Apple Pay in many apps — and on participating websites with Safari on your Mac, iPhone or iPad.”

Aside from convenience, the other consumer advantage Apple touts for the system is privacy, with Apple Pay using a device-specific number and unique transaction code — and the user’s actual card numbers never stored on their device or on Apple’s servers — which means trackable card numbers aren’t shared with merchants, so purchases can’t be tied back to the individual.

While that might sound like an abstract concern, a Bloomberg report this summer revealed details of a multi-million deal in which Google pays for transaction data from Mastercard — in order to try to link online ad views with offline purchases in the US.

Facebook has also long been known to buy offline data to supplement the interest signals it collects on users from inside (and outside) its social network — further fleshing out ad-targeting profiles.

So escaping the surveillance net of one flavor of big tech can require buying into another. Or else going low tech and paying in cash.

Apple does not say what took it so long to add Germany to its now pretty long list of Apple Pay countries but Apple Insider suggests the relatively late adoption was down to pushback from local banks over fees, noting that it’s four months after the official announcement of a German launch.

It’s also true that paying by plastic isn’t always an option in Germany, as cash remains the dominant payment method of choice — also, seemingly, for privacy purposes. So Apple Pay is at least aligned with those concerns.

Powered by WPeMatico

Airwallex, a three-year-old fintech startup focused on international payments for SMEs and businesses, is putting itself on the map after it raised an $80 million Series B round.

Based out of Melbourne, but with six offices in Asia and other parts of the world, Airwallex’s new funding round is the second-largest financing deal for an Australian startup in history. The round was led by existing investors Tencent, the $500 billion Chinese internet giant, and Sequoia China. Other participants included China’s Hillhouse, Horizons Ventures — the fund from Hong Kong’s richest man, Li Ka-Shing — Indonesia-based Central Capital Ventura (BCA) and Australia’s Square Peg, a firm from Paul Bassat, who took recruitment firm Seek to IPO and is one of Australia’s highest-profile founders.

The financing takes Airwallex to $102 million raised. Tencent led a $13 million Series A in May 2017, while Square Peg added $6 million more via a Series A+ in December. Mastercard is also a backer; the finance giant uses Airwallex to handle its “Send” product, while Tencent uses the service to power an overseas remittance service for its WeChat app.

Airwallex handles cross-border transactions for companies that do business in multiple countries using international currencies. So it’s not unlike a TransferWise-style service for SMEs that lack the capital to develop a sophisticated (and expensive) international banking system of their own.

The service uses wholesale FX rates to route overseas payments back to a client’s domestic bank and is capable of processing “thousands of transactions per second,” according to the company. A use case example might include helping a China-based seller return money earned in the U.S. or Europe via Amazon or other e-commerce services, or route sales revenue back directly from their own website.

Airwallex CEO Jack Zhang (far right) onstage at TechCrunch Shenzhen in 2017

China is a key market for Airwallex — which was started by four Australian-Chinese founders — as well as the wider Asian region, and in particular Australia, Hong Kong and Southeast Asia. With this new capital, Airwallex co-founder and CEO Jack Zhang said the company will increase its focus on Hong Kong and Southeast Asia, whilst also extending its business in Europe (where it has a London-based office) and pushing into North America.

Product R&D is shared across Melbourne and Shanghai, while Hong Kong accounts for business development, compliance and more, Zhang explained. However, Airwallex’s locations in London and San Francisco are likely to account for most of the upcoming headcount growth planned following this funding. Right now, Airwallex has around 100 staff, according to Zhang.

The company is also aiming to expand its product range.

The firm is in the process of applying for a virtual banking license in Hong Kong, a third-party payment license in mainland China and a cross-border Chinese yuan license. One goal, Zhang revealed, is to offer working capital loans to SMEs to help them scale their businesses to the next level. Airwallex is working with an undisclosed partner to underwrite deals in the future. Zhang explained that the company sees a gap in the market since banks don’t have access to critical data on clients for loan assessments.

More generally, he’s bullish for the future, despite Brexit and the ongoing trade war between the U.S. and China.

“The trade war gives the Chinese yuan a lot of vitality, and we’ve seen more demand in the market. China’s belt road initiative has really taken off, too, and we’re seeing the impact in many, many of our payment corridors,” he explained. “Business has been booming, especially as traditional offline SMEs start to move online and go from domestic to global.”

“We want to be the backbone to support these new opportunities for businesses,” Zhang added.

Powered by WPeMatico

While Henrique Dubugras and Pedro Franceschi were giving up on their augmented reality startup inside Y Combinator and figuring out what to do next, they saw their batch mates struggling to get even the most basic corporate credit cards — and in a lot of cases, having to guarantee those cards themselves.

Brex, their new startup, aims to try to fix that by offering startups a way to quickly get what’s effectively a credit card that they can use without having to personally guarantee that card or wade through complex processes to finally get a charge card. It’s geared initially towards smaller companies, but Dubugras expects those startups to grow up with it over time — and that Brex is already picking up larger clients. The company, coming out of stealth, said it has raised a total of $57 million from investors including the Y Combinator Continuity fund, Peter Thiel, Max Levchin, Yuri Milner, financial services VC Ribbit Capital and former Visa CEO Carl Pascarella. Y Combinator Continuity fund partner Anu Hariharan and Ribbit Capital managing partner Meyer Malka are joining the company’s board of directors.

“We want to be the best corporate credit card for startups,” Dubugras said. “We’re don’t require a personal guarantee or deposit, and we can give people a credit limit that’s as much as ten times higher. We can get you a virtual credit card in literally 5 minutes, versus traditional banks, in which you’d have to personally guarantee the card and get a low limit and it takes weeks to approve.”

Startup executives go to Brex’s website, sign up, and then put in their bank account info. They then use that banking information to underwrite the card, with the idea being that the service can see that the start has raised millions of dollars and doesn’t have the kind of wild liability that those banks think they might have given how young they are. Once the application is done, companies get a virtual credit card, and they can start divvying up virtual cards with custom limits for their employees. The company says it has attracted more than 1,000 customers and is now opening up globally.

The cards are designed to have better spending limits, and also offer company executives more granular ways to assign those limits to employees. The cards have to be paid off by the end of the month, and the rolling balance for those cards is dependent on the amount of capital each startup has available. The total limit available is, instead, a percentage of the company’s cash balance available. So rather than having to go through the process of getting approved for a card, the service can look at how much money is in a startup’s bank account and adjust the spending limit for all those cards accordingly.

Another aspect is automating the whole expense and auditing process. Rather than just going through typical applications like Concur and inputting specifics, card users can send a text message of a receipt through Brex associated with each transaction. Users will just get a text message about a charge — like a cup of coffee for a meeting with a potential business partner — and reply to that text with a message of the receipt to log the whole process. Everything is geared toward simplifying the whole process for startups that have an opportunity to be a bit more nimble and aren’t bogged down with complex layers of enterprise software. Each expense is looped in with a vendor, so executives can see the total amount of spending that’s happening at that scale.

The ability to have those dynamic spending limits is just one example of what Dubugras hopes will make Brex competitive. Rather than slotting into existing systems, Brex has an opportunity to recreate the back-end processes that power those cards, which larger institutions might not be able to do as they’ve hit a massive scale and get less and less agile. Dubugras and Franceschi previously worked on and sold Pagar.me, a Brazilian payments processor, where they saw firsthand the complex nature of working with global financial institutions — and some of the holes they could exploit.

“It’s not like we’re two geniuses that came up with a lot of things that no one came up with,” Dubugras said. “Implementing them with third-party processors is hard, but we didn’t have any of [those integrations], so we can rebuild them from scratch. It’s hard for banks to throw money at a problem and build those tools. We’ve rebuilt the way that these things work internally — they’d have to change fundamentally how the system works.”

While there are plenty of startups looking to quickly offer virtual cards, like Revolut’s disposable virtual card service, Brex aims to be what’s effectively a corporate card — just one that’s easier to get and works basically the same as a normal card. Users still have to pay off the balance at the end of the month, but the idea there is that Brex can de-risk itself by doing that while still offering startups a way to get a card with a high limit to start paying for the services or tools they need to get started.

Powered by WPeMatico

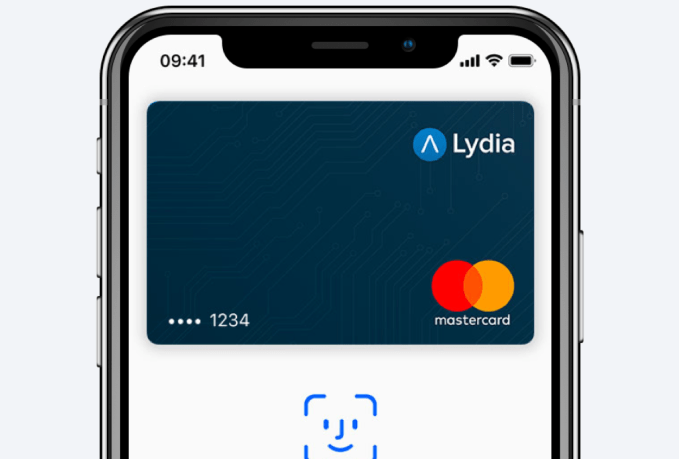

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

Powered by WPeMatico

In what amounts to a very clever brute force attack, a group of researchers has figured out how to find credit card information – including expiration dates and CVV numbers – by querying ecommerce sites. The process, which was outlined in IEEE Security & Privacy, involves guessing and testing hundreds of permutations of expiration dates and CVV numbers on hundreds of… Read More

In what amounts to a very clever brute force attack, a group of researchers has figured out how to find credit card information – including expiration dates and CVV numbers – by querying ecommerce sites. The process, which was outlined in IEEE Security & Privacy, involves guessing and testing hundreds of permutations of expiration dates and CVV numbers on hundreds of… Read More

Powered by WPeMatico