Market Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to This Week in Apps, the Extra Crunch series that recaps the latest OS news, the applications they support and the money that flows through it all.

The app industry is as hot as ever, with a record 204 billion downloads and $120 billion in consumer spending in 2019. People are now spending three hours and 40 minutes per day using apps, rivaling TV. Apps aren’t just a way to pass idle hours — they’re a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus.

In this Extra Crunch series, we help you keep up with the latest news from the world of apps, delivered on a weekly basis.

This week, we’re taking a look at how the civil unrest and George Floyd protests played out across the app stores. The events led some apps — including private messaging apps, police scanners and alerting apps, and other social communication apps — to surge, and even break records. Google decided to delay the launch of Android 11 beta 1 in light of the recent events.

We’re also keeping up with COVID-19 apps and how the pandemic is changing app usage and consumer behavior. Plus, the FTC fined an app developer over privacy violations in a warning shot for the app industry; Zoom faced criticism for its encryption plans; Apple launched an open-source resource for password managers; and more.

Protests drive downloads of police scanners

Downloads of police scanner apps, tools for private communication and mobile safety apps hit record numbers last weekend in the U.S., amid the nationwide protests over the police killing of George Floyd, as well as the systemic problems of racial prejudice that plague the American justice system. According to data from app store intelligence firm Apptopia, top U.S. police scanner apps were downloaded a combined 213,000 times last weekend, including Friday — a 125% increase from the weekend prior and a record number for this group of apps.

The group of top apps included those with similar, if somewhat generic, titles, such as Scanner Radio – Fire and Police Scanner, Police Scanner, 5-0 Radio Police Scanner, Police Scanner Radio & Fire and Police Scanner +.

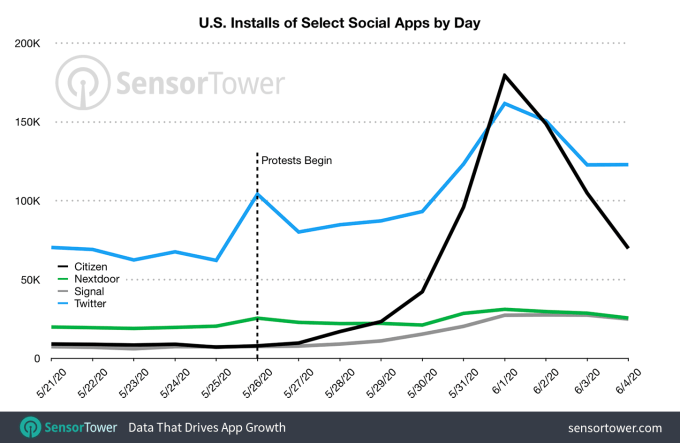

Citizen, Signal and others spike during protests

In addition to tracking police movements with scanners, protestors organized and communicated on secure messaging app Signal. Meanwhile, community safety app Citizen, which sends out police alerts, also saw a jump in usage. According to Apptopia, Citizen and Signal both set daily download records, Vox noted earlier this week.

Citizen

Citizen’s app lets users see “incidents,” based on radio communications with 911 dispatchers, police, fire departments and other emergency responders. The app uses high-powered scanners to tune into public radio channels, then digitizes and transcribes the audio, and turns those into incidents placed on the map. But the app is popular because it’s more than a police scanner; it includes a social networking layer where users can react and comment.

Based on more recent data provided to TechCrunch by Sensor Tower, Citizen was installed around 620,000 times by first-time users in the U.S. during the past week, an increase of about 916% compared to the week prior. First-time installs reached a record 150,000 on June 2, nearly 12x the app’s average of 13,000 daily first-time installs during May. On average, the app was downloaded close to 86,000 times per day, or 6.6x larger than May’s daily average. The app grew to be as high as No. 4 on Tuesday, June 2 on the U.S. App Store, and is now No. 32 Overall on the top free charts.

Signal

Image Credits: Signal

The firm also estimated that Signal had been installed by approximately 135,000 first-time users in the U.S. during the past week across the app stores. This figure represented growth of 165% from the preceding seven days, or about 2.6x that total of approximately 51,000 new installs. Signal averaged about 19,000 installs per day over the past seven days.

For comparison’s sake, Signal was downloaded around 269,000 times in all of May and its average daily number of installs was 9,000. That makes the average for the past week about 2x higher.

Signal is currently ranked at No. 137 among the top free iPhone apps on the U.S. App Store. Earlier, it was ranked at No. 107 on Tuesday, June 2.

This week, Signal also added built-in face blurring for photos, to help better secure the sharing of sensitive information across its network.

Nextdoor and Neighbors by Ring

The civil unrest also impacted neighborhood networking app installs, as communities looked to share information about the protests with one another. Social networking app for neighbors Nextdoor was installed by 185,000 first-time users in the U.S. over the past week, an increase of 26% from 147,000 installs in the week prior. The app also jumped up nearly 50 places in the U.S. App Store rankings, moving from No. 2,014 to No. 156 in the top free iPhone apps chart.

Amazon-owned Neighbors by Ring, where neighbors share alerts, including security camera footage, was installed by 36,000 first-time users in the past week, an increase of 89% from its approximately 19,000 installs the week prior.

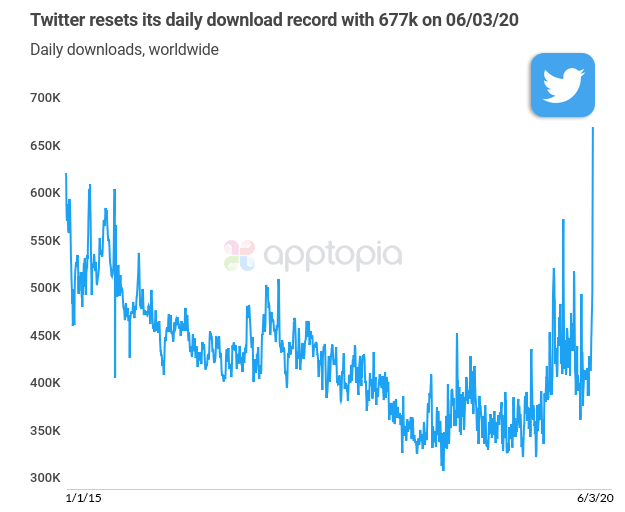

Twitter has a record-breaking week as users looked for news of protests and COVID-19

Civil unrest due to the nationwide George Floyd protests drove Twitter to see a record number of new installs this week, according to data from two app store intelligence firms, Apptopia and Sensor Tower. While the firms’ exact findings differed in terms of the total number of new downloads or when records were broken, the firms agreed that Twitter’s app had its largest-ever week, globally.

The app saw at least 677,000 installs at its highest point, Apptopia said. Sensor Tower said it topped 1 million. Twitter also broke a record for daily active users on Twitter in the U.S., when some 40 million people in the U.S. logged into the app on June 3, Apptopia noted. For comparison’s sake, Twitter reported its app had 31 million “monetizable” daily active users (mDAUs) in the U.S. in Q4 2019, which grew to 33 million in Q1 2020.

The spike in installs was attributed to the protests, which were being watched by a global audience, and COVID-19, which continued to spread in worldwide markets.

Apps turn their icons black in support of George Floyd protests

A small handful of apps did the equivalent of the Instagram black square by turning their icons black this week as a gesture of support toward the protests and civil rights. Participating apps included Reddit, Joss & Main and Shop Avani, for instance. Moves like this can be criticized as being merely performative, but one of the companies involved — Reddit — later followed up with real action. Reddit co-founder Alexis Ohanion on Friday announced he was resigning as a member of the Reddit board, and is now urging them to fill his seat with a black candidate. He also said he would use his future gains from Reddit stock to serve the black community, starting with a $1 million pledge to Colin Kaepernick’s Know Your Rights Camp.

Powered by WPeMatico

Earlier this week, TechCrunch covered a grip of earnings reports showing that some companies helping other businesses move to modern software solutions are seeing accelerated growth. Inside the Software as a Service (SaaS) world, this is known as the digital transformation. Based on how many software companies are talking about it, the pace of change is only picking up.

But since we published that first entry, a number of SaaS companies that have posted financial results seemed to disappoint investors. Seeing some companies in the high-flying sector struggle made us sit back and think. What was going on?

Today we’re going to explore how the digital transformation’s acceleration seems real enough, but how it’s not landing equally. We’ll start by going over a short run of earnings results, talk to Yext CEO Howard Lerman about what his B2B SaaS company is seeing, and wrap with notes on what could be coming next from software shops.

We all hear about digital transformation, but it’s hard to define. Generally, it’s a broad area that includes digitization of manual processes, modern software development practices like continuous delivery and containerization and a general way of moving faster via technology — especially in the cloud.

Speaking last month on Extra Crunch Live, Box CEO Aaron Levie defined the term as he sees it. “The way that we think about digital transformation is that much of the world has a whole bunch of processes and ways of working — ways of communicating and ways of collaborating where if those business processes or that way we worked were able to be done in digital forms or in the cloud, you’d actually be more productive, more secure and you’d be able to serve your customers better. You’d be able to automate more business processes.” he said.

What we’re seeing now is that the pandemic has accelerated the rate of change much faster than many had anticipated. Efforts to slow the spread of COVID-19 and its related workplace disruptions have accelerated what would have been a normal timetable. But on its own, that doesn’t mean the market is seeing equal results across every company and industry that might be part of that trend.

Lots of SaaS companies reported earnings this week, but two sets of returns stuck out as we reviewed the results, those from Slack and Smartsheet.

Powered by WPeMatico

When Larry Liu moved to the U.S. in 2003, one of the first challenges he experienced was the lack of Chinese ingredients available in local groceries. A native of Hubei, a Chinese province famous for its freshwater fish and lotus-inspired dishes, Liu got by with a limited supply found at local Asian groceries in the Bay Area.

His yearning for home food eventually prompted him to quit a stable financial management role at microcontroller company Atmel and go on to launch Weee!, an online market selling Asian produce, snacks and skincare products.

Like other players in grocery e-commerce, the five-year-old startup has seen exponential growth since the coronavirus outbreak as millions are confined to cooking and eating at home. Nearly a quarter of Americans purchased groceries online to avoid offline shopping during the pandemic, according to Statista data. Online grocery giants Instacart and Walmart Grocery boomed, both hitting record downloads.

In a Zoom call with TechCrunch, Liu, who’s now chief executive of Weee!, said that COVID-19 played a “very important role” in his company’s recent growth, and paved its way to profitability.

“It happened a lot faster than we expected, but we were growing rapidly with even more ambitious plans for expansion prior to COVID-19,” he said. “People are buying more because restaurants are closed. Many are first-time users of grocery delivery.”

The startup’s revenue is up 700% year-over-year and is estimated to generate an annual revenue in the lower hundreds of millions of dollars.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

ZoomInfo went public yesterday. After pricing its IPO $1 ahead of its proposed range at $21 per share, the company closed its first day’s trading worth $34.00, up 61.9%, according to Yahoo Finance. Then the company gained another 5.2% in after-hours trading.

Whether you feel that this SaaS player was worth the revenue multiple its original, $8 billion valuation dictated — let alone that same multiple times 1.6x — the message from the offering was clear: the IPO window is open.

This is not news to a few companies looking to take advantage of today’s strong equity prices.

Used-car marketplace Vroom is looking to get its shares public before its Q2 numbers come out, despite a history of slim gross profit generation. The company hopes to go public for as much as $1.9 billion, a modest uptick from its final private valuations.

We’ll get another dose of data when Vroom does price — how much investors are willing to pay for slim-margin revenue will tell us a bit more than what we learned from ZoomInfo, which has far superior gross margins. Investors have already signaled that they are content to value high-margin software-ish revenues richly. Vroom is more of a question, but if it does price strongly we’ll know public investors are looking for any piece of growth they can find.

This brings us to the latest news: Amwell has confidentially filed to go public. Formerly known as American Well, CNBC reports that the venture-backed telehealth company has dramatically expanded its customer base:

Telemedicine has seen an uptick in recent months, as people in need of health services turned to phone calls and video chats so they could avoid exposure to COVID-19. The company told CNBC last month that it’s seen a 1,000% increase in visits due to coronavirus, and closer to 3,000% to 4,000% in some places.

Powered by WPeMatico

COVID-19 has transformed the global business landscape.

So much so that in a matter of weeks after the onset of the pandemic in the United States, Congress provided more than $1.1 trillion in fiscal stimulus directly to businesses and distressed industries — four times more than was distributed during the 2008-09 financial crisis.

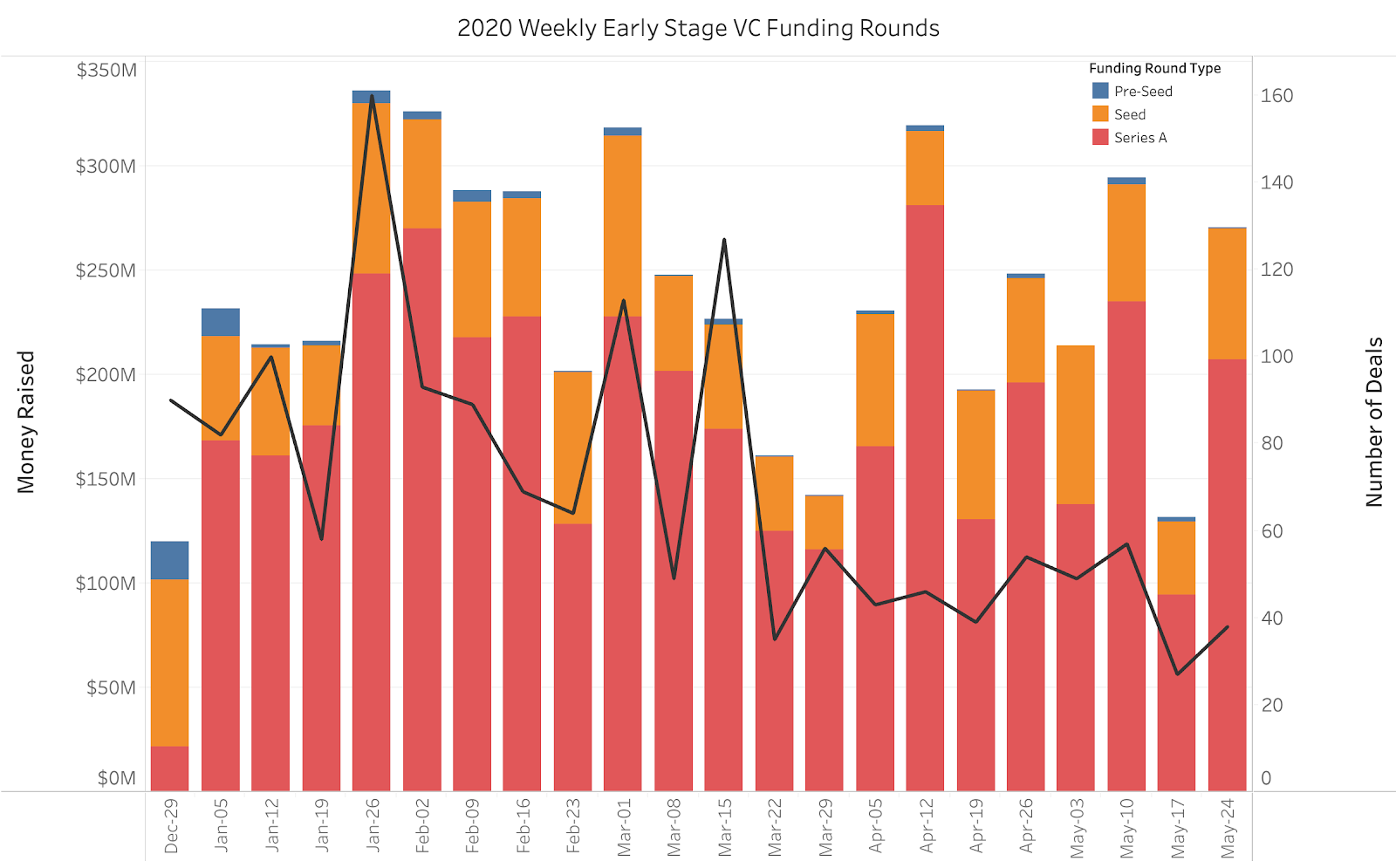

It came as no surprise when, at the start of COVID-19, venture capital investors largely went pencils-down for several weeks and shifted their focus to their existing portfolio companies. Extending company runways, preparing for longer funding cycles and managing operations in a novel business environment became the crux of company resilience. Now, moving into May, we can see this shift reflected in both the decline in number of early-stage companies funded and total capital invested.

As investors begin acclimating to this new normal, they have begun wading into new opportunities in time-proven, healthy industries and new emerging industries that are positioned to succeed during the pandemic. While we are seeing lower valuations, we believe certain B2B technology companies may be uniquely poised to thrive, and are pursuing investment opportunities in this space with a renewed focus.

Image Credits: Crunchbase Data via Tableau Public

*Excluding Biotech & Pharmaceuticals (Source: Crunchbase Data via Tableau Public)

Prior to COVID-19, early-stage B2B investors wanted to see strong growth and healthy unit economics; 3X year-over-year sales growth or 10% monthly growth was the gold standard. An LTV-to-CAC ratio over 3X signified a healthy payback cycle. There was less focus on capital efficiency; for every $1 million invested, investors were happy with $500,000 in generated revenues. Get to these numbers and your next funding round was guaranteed — but no longer.

During COVID, and likely beyond, company expectations and goalposts have been adjusted; 2X year-over-year growth may be the new 3X. While growth and unit economics are important, there are now new health indicators that will determine if a B2B company will thrive in a post-COVID world. With that in mind, we have put together a COVID reslience test that startups can use as a north star to grow their business in this new world.

This COVID-19 test is meant to be a gated checklist that will indicate where efforts should be focused, whether it be sales, product or finance. Before we leave you to your own devices, we wanted to walk through a couple of these new post-COVID questions that you should try to answer (and why they are relevant).

Powered by WPeMatico

In 2015, Atlassian was preparing to go public, but it was not your typical company in so many ways. For starters, it was founded in Australia, it had two co-founder co-CEOs, and it offered collaboration tools centered on software development.

That meant that the company leaders really needed to work hard to help investors understand the true value proposition that it had to offer, and it made the roadshow deck production process even more critical than perhaps it normally would have been.

A major factor in its favor was that Atlassian didn’t just suddenly decide to go public. Founded in 2002, it waited until 2010 to accept outside investment. After 10 straight years of free cash flow, when it took its second tranche of investment in 2014, it selected T. Rowe Price, perhaps to prepare for working with institutional investors before it went public the next year.

We sat down with company president Jay Simons to discuss what it was like, and how his team produced the document that would help define them for investors and analysts.

Powered by WPeMatico

It was a busy week in security.

Newly released documents shown exclusively to TechCrunch show that U.S. immigration authorities used a controversial cell phone snooping technology known as a “stingray” hundreds of times in the past three years. Also, if you haven’t updated your Android phone in a while, now would be a good time to check. That’s because a brand-new security vulnerability was found — and patched. The bug, if exploited, could let a malicious app trick a user into thinking they’re using a legitimate app that can be used to steal passwords.

Here’s more from the week.

Powered by WPeMatico

In business, there’s nothing so valuable as having the right product at the right time. Just ask Zoom, the hot cloud-based video conferencing platform experiencing explosive growth thanks to its sudden relevance in the age of sheltering in place.

Having worked at BlackBerry in its heyday in the early 2000s, I see a lot of parallels to what Zoom is going through right now. As Zooming into a video meeting or a classroom is today, so too was pulling out your BlackBerry to fire off an email or check your stocks circa 2002. Like Zoom, the company then known as Research in Motion had the right product for enterprise users that increasingly wanted to do business on the go.

Of course, BlackBerry’s story didn’t have a happy ending.

From 1999 to 2007, BlackBerry seemed totally unstoppable. But then Steve Jobs announced the iPhone, Google launched Android and all of the chinks in the BlackBerry armor started coming undone, one by one. How can Zoom avoid the same fate?

As someone who was at both BlackBerry and Android during their heydays, my biggest takeaway is that product experience trumps everything else. It’s more important than security (an issue Zoom is getting blasted about right now), what CIOs want, your user install base and the larger brand identity.

When the iPhone was released, many people within BlackBerry rightly pointed out that we had a technical leg up on Apple in many areas important to business and enterprise users (not to mention the physical keyboard for quickly cranking out emails)… but how much did that advantage matter in the end? If there is serious market pull, the rest eventually gets figured out… a lesson I learned from my time at BlackBerry that I was lucky enough to be able to immediately apply when I joined Google to work on Android.

Powered by WPeMatico

As investors’ appetites sour in the midst of a pandemic, a three-and-a-half-year-old Indian firm has secured $10.3 billion in a month from Facebook and four U.S.-headquartered private equity firms.

The major deals for Reliance Jio Platforms have sparked a sudden interest among analysts, executives and readers at a time when many are skeptical of similar big check sizes that some investors wrote to several young startups, many of which are today struggling to make sense of their finances.

Prominent investors across the globe, including in India, have in recent weeks cautioned startups that they should be prepared for the “worst time” as new checks become elusive.

Elsewhere in India, the world’s second-largest internet market and where all startups together raised a record $14.5 billion last year, firms are witnessing down rounds (where their valuations are slashed). Miten Sampat, an angel investor, said last week that startups should expect a 40%-50% haircut in their valuations if they do get an investment offer.

Facebook’s $5.7 billion investment valued the company at $57 billion. But U.S. private equity firms Silver Lake, Vista, General Atlantic, and KKR — all the other deals announced in the past five weeks — are paying a 12.5% premium for their stake in Jio Platforms, valuing it at $65 billion.

How did an Indian firm become so valuable? What exactly does it do? Is it just as unprofitable as Uber? What does its future look like? Why is it raising so much money? And why is it making so many announcements instead of one.

It’s a long story.

Billionaire Mukesh Ambani gave a rundown of his gigantic Indian empire at a gathering in December 2015 packed with 35,000 people including hundreds of Bollywood celebrities and industry titans.

“Reliance Industries has the second-largest polyester business in the world. We produce one and a half million tons of polyester for fabrics a year, which is enough to give every Indian 5 meters of fabric every year, year-on-year,” said Ambani, who is Asia’s richest man.

Powered by WPeMatico

Edtech is booming, but a short while ago, many companies in the category were struggling to break through as mainstream offerings. Now, it seems like everyone is clamoring to get into the next seed-stage startup that has the phrase “remote learning” on its About page.

And so begins the normal cycle that occurs when a sector gets overheated — boom, bust and a reckoning. While we’re still in the early days of edtech’s revitalization, it isn’t a gold mine all around the world. Today, in the spirit of balance and history, I’ll present three bearish takes I’ve heard on edtech’s future.

Quizlet’s CEO Matthew Glotzbach says that when students go back to school, the technology that “sticks” during this time of massive experimentation might not be bountiful.

“I think the dividing line there will be there are companies that have been around, that are a little more entrenched, and have good financial runway and can probably survive this cycle,” he said. “They have credibility and will probably get picked [by schools].” The newer companies, he said, might get stuck with adoption because they are at a high degree of risk, and might be giving out free licenses beyond their financial runway right now.

Powered by WPeMatico