Market Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this week, we kicked off our Extra Crunch Live series with an interesting chat with Cowboy’s Aileen Lee and Ted Wang. Today, we will be back at 3 p.m. PST/6 p.m. EST/10 p.m. GMT with a new guest: Charles Hudson, the general partner of Precursor Ventures.

Extra Crunch members will find an AddEvent link below to drop the details directly into their calendar and folks who want to participate directly can hit up the Zoom link (also below). We’ll ask as many audience questions as we can, so please make them sharp — no pitches, please.

Charles Hudson founded Precursor Ventures to invest in pre-seed and seed-stage companies. Earlier this year, the firm filed paperwork to put together a $40 million third fund after previously raising two main funds and one $10 million “opportunity” fund.

As we await hard and accurate numbers on how COVID-19 is impacting fundraising, we’ll ask Hudson to walk us through the changes he has seen and will cover some basics: The best way to pitch him, what his to-do list looks like these days and if the pandemic has made Precursor newly bullish or bearish on certain sectors.

Then, we’ll get much nerdier: Will we see the number of party rounds fall further now that it’s harder to gather investors in real life? Do you think we’ll see pre-seed raises ask for more ownership terms? And what is the latest with the wacky world of early-stage valuations?

There’s a lot to talk about. And we haven’t even mentioned YC’s pro rata change yet.

After Hudson, we have a stacked lineup of Extra Crunch live guests, including Mitch and Freada Kapor, Mark Cuban, Roelof Botha and Kirsten Green, with more to be announced soon.

You can find information below with details for joining today’s discussion, as well as an AddEvent link to put the details directly onto your calendar.

Sign up for Extra Crunch to get access to all these episodes where you can view the talks live, participate in the Q&A with industry leaders and watch later on-demand if you can’t make the live timing. You can also see the chat via YouTube below. Talk soon!

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

While some U.S. investors might have taken comfort from China’s rebound, we still find ourselves in the early innings of this period of uncertainty.

Some epidemiologists have estimated that COVID-19 cases will peak in April, but PitchBook reports that dealmaking was down -26% in March, compared to February’s weekly average. The decline is likely to continue in coming weeks — many of the deals that closed last month were initiated before the pandemic, and there is a lag between when deals are made and when they are announced.

However, there’s still hope. A recent report concluded that because valuations are lower and there’s less competition for deals, “the best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery.” There are countless examples from the 2008 recession, including many highly valued VC-backed businesses such as WhatsApp, Venmo, Groupon, Uber, Slack and Square. Other early-stage VCs seem to have arrived at a similar conclusion.

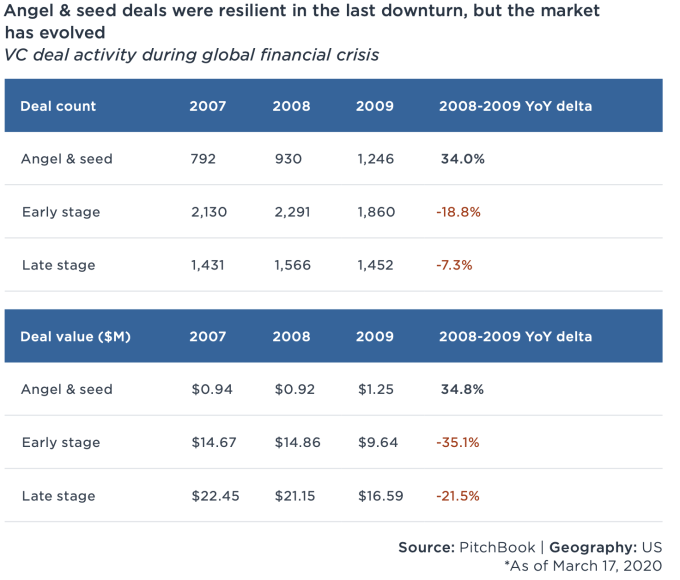

Also, early-stage investing seems more resilient. During the last recession, angel and seed activity increased 34% as interest in the stage boomed during a period of prolonged growth.

Image Credits: PitchBook (opens in a new window)

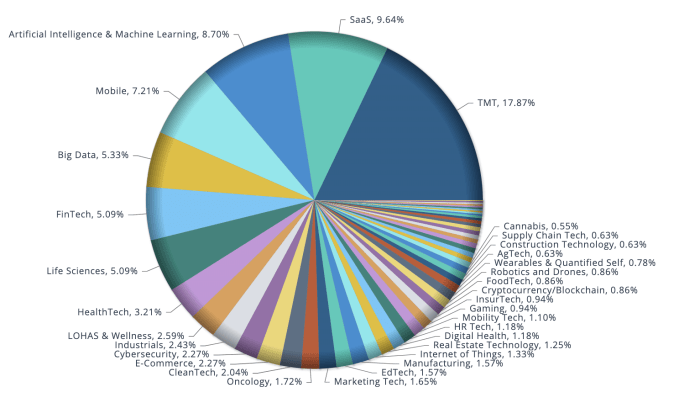

Furthermore, there is still capital to be deployed in categories that interested investors before the pandemic, which may set the new order in a post-COVID-19 world. According to data provider Preqin Ltd., VC dry powder rose for a seventh consecutive year to roughly $276 billion in 2019, and another $21 billion were raised last quarter. And looking at the deals on the early-stage side that were made year to date, especially in March, the vertical categories that garnered the most funding were enterprise SaaS, fintech, life sciences, healthcare IT, edtech and cybersecurity.

Image Credits: PitchBook

That said, if VCs have the capital to deploy and are able to overcome the obstacle of “having never met in person,” here are six investment trends that could emerge when the pandemic is over.

Powered by WPeMatico

The tech industry (and the world at large) is not experiencing temporary anxiety — the uncertainty we’re all coping with is the new normal.

Sudden shifts in behavior have made some startups targeting slow-moving, old-school industries more relevant than they could have imagined, such as those in telehealth, distance learning and remote work. Most, however are seeing massive decreases in revenue, forcing them to cut costs and even lay off teams to slash burn rates. Other startups simply won’t be here in three to six months.

Cowboy Ventures founder and managing partner Aileen Lee, who coined the term “unicorn,” says tech companies going through scenario planning need to begin thinking long-term.

“We’ve spent the last month scenario planning with our portfolio companies, and in most cases, we’ll have conversations about what these scenarios can include,” said Lee. “And when we look at the planning around those scenarios, they often don’t feel conservative enough. Most entrepreneurs are optimists, and we are, too! But it seems safer to have more conservative plans [and start expecting] that this is going to impact us for longer and be worse than we expected.”

Lee and Cowboy Ventures partner Ted Wang joined TechCrunch on Tuesday for our first episode of Extra Crunch Live, a virtual speaker series for Extra Crunch members. In a live Q&A that included questions from myself and the Extra Crunch audience, Wang and Lee covered a wide range of topics, including PPP loans, advice for business leaders around layoffs, the right time to seek funding and the right firms from which to seek that funding, how to pitch during a downturn and which sectors in particular Cowboy is interested in financing right now.

You can check out the best insights from the call, or catch up on the full conversation via the YouTube embed below.

We have several outstanding guests, including Charles Hudson, Mitch and Freada Kapor, Mark Cuban, Roelof Botha, Hunter Walk and Kirsten Green, joining us on Extra Crunch Live over the next few weeks. Sign up for Extra Crunch to get access to all of them.

Powered by WPeMatico

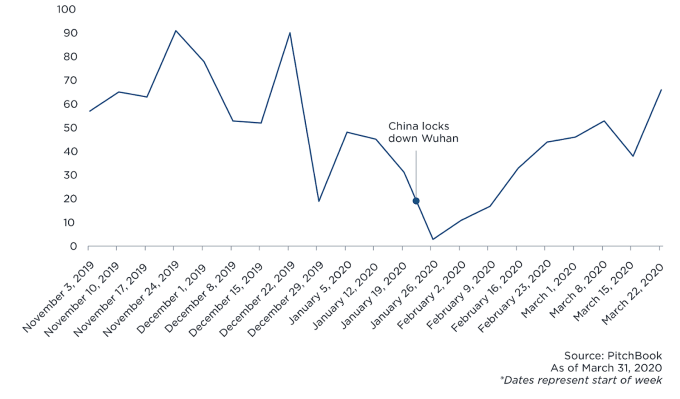

For the past month, VC investment pace seems to have slacked off in the U.S., but deal activities in China are picking up following a slowdown prompted by the COVID-19 outbreak.

According to PitchBook, “Chinese firms recorded 66 venture capital deals for the week ended March 28, the most of any week in 2020 and just below figures from the same time last year,” (although 2019 was a slow year). There is a natural lag between when deals are made and when they are announced, but still, there are some interesting trends that I couldn’t help noticing.

While many U.S.-based VCs haven’t had a chance to focus on new deals, recent investment trends coming out of China may indicate which shifts might persist after the crisis and what it could mean for the U.S. investor community.

Image Credits: PitchBook

Powered by WPeMatico

Before the COVID-19 pandemic shook up the world and reshaped the economy, Boston was quietly setting records.

According to new venture data compiled by TechCrunch, the region set what was at least a local maximum in venture capital raised in the space of a single quarter in Q1 2020.

But while Boston’s startup market announced a number of huge rounds that bolstered its total venture dollars raised in the first quarter, there were signs of weakness: Deal volume was its best since Q2 2019, according to a set of data compiled and released by PwC and CB Insights, but was still a little under the pace set in 2018.

So Boston’s startups raised lots of money, but couldn’t match prior highs when it came to the number of checks written. And those results were largely recorded before COVID-19 shuttered the city. Since then, we’ve seen a number of area startups lay off staff, something we explored last week.

Now, with fresh data in hand, we can take a closer look at the city’s first quarter of 2020. To better understand what we’re unpacking, we asked a number of local venture capitalists to weigh in. Let’s look back at Boston’s Q1 as we stride into Q2 with the help of Venture Lane, .406 Ventures, Volition Capital and Flybridge Capital Partners.

Starting with a programming note is counter-flow, but bear with us. TechCrunch is starting a regular, monthly series on Boston and its startup market. This is a second prelude of sorts. Normally we’d hold news and interviews for a later date so that we’d have plenty of material for a column. In the face of relentless change, however, we didn’t want to hold off on reporting and synthesizing new information. When things are more normal, our pace will follow.

Per PwC and CB Insights, here’s the last few quarters of data, along with a few yearly totals to draw you the picture we can now see:

Powered by WPeMatico

As silently and swiftly as it has devastated families and communities around the world, COVID-19 has also left many startups gasping for air. Emerging companies with strong 2020 revenue forecasts have seen their high-confidence plans reduced by 60%-80% in a matter of days. Even in the best of times, startups must reach value-unlocking milestones to successfully raise new capital. But today, a globally synchronized halt to business activity has made irrelevant normal benchmarks for financing rounds.

Obtaining payroll support from the recently enacted special government programs for small businesses will not resolve the cascading problems startups are grappling with, regardless of whether or not they are VC-backed.

Product development roadmaps in many innovation-driven industries are changing in ways that may permanently alter a company’s future strategic direction. Merger and acquisition discussions are being shelved. Normal financing rounds, in process and contemplated, are contracting or being abandoned altogether. Many venture funds, including corporate venture programs, have unilaterally “taken a pause” to reevaluate the radically changing landscape for their early-stage company portfolios.

I last experienced this phenomenon in the aftermath of the Great Technology Bubble: 2002-2003. And all signs show that we are at the beginning of a new round of punitive “incentives” for venture investors to keep their companies alive.

Several of my current portfolio companies have recently proposed “emergency bridge” convertible note financings of between $5 million and $15 million, each featuring a painful feature for non-participants: multiple liquidation preferences benefiting only the new money above 3x, with discounts greater than 20% on conversion in a new equity financing. Of course, these financings are open to both existing and new investors. But the likelihood of another round is actually diminished by this type of structure.

Powered by WPeMatico

As domestic and global economies grapple with the COVID-19 era, its impact on startups is coming into focus: All will be impacted, many will suffer and some will close.

Boston, a city that TechCrunch keeps tabs on, has seen a number of well-known startups struggle in recent weeks. Their misfortunes come quickly after companies in the region recorded huge venture raises, generating notable momentum.

In December, TechCrunch wrote that “despite winter’s chill, the Northeast’s tech ecosystem is white-hot,” taking into account Boston’s historical gains in the venture world. And earlier in 2020 we covered a few huge rounds that the city’s own Toast and Flywire had put together; worth $520 million as a pair, the two venture deals stood out for how large they were and how close to one another they were announced.

Indeed, looking at preliminary venture data from Crunchbase, Boston was on track to crush its 2019 tally of venture rounds of $50 million or more in 2020. That record-setting pace is now in doubt.

To get a feel for Boston’s new reality, we’ve collected the region’s recent news and spoke to area investors and founders, including David Cancel of Drift (the previous founder of Compete and other companies), Drew Volpe of First Star VC and a team of folks from Underscore VC.

TechCrunch had intended to start a monthly series on Boston and its venture capital and startup scenes later this month. We’re kicking it off early because the news is already here.

Earlier this week, restaurant management platform Toast cut 50% of its staff. The Boston-based company was valued at $5 billion in recent months, and — before the pandemic hit — was planning to spend the next few years gearing up to go public. Toast sits uniquely between fintech and restaurant tech, industries that have been arguably impacted the most by COVID-19’s spread and widespread restaurant closures.

Powered by WPeMatico

The coronavirus pandemic has pushed entrepreneurs and investors into unknown territory.

Google’s GV just led a $10 million investment in Universe, a low-friction website builder that’s venturing into the world of commerce.

The investment was in the works before COVID-19 hit America in force, but things were finalized for the Brooklyn startup in late March. I chatted with M.G. Siegler, the general partner at GV (and former TechCrunch writer) who led the deal, about how the crisis was affecting his investment work and how he was balancing portfolio work with sourcing new deals.

This interview has edited for length and clarity.

TechCrunch: This deal sounds like it was in the works before pandemic concerns really hit America, but when you saw this situation arise, did it change your thinking about this deal at all?

M.G. Siegler: The reality is we’re still going to be continuing to look for interesting opportunities to invest in. History has shown that even during great financial turmoil, many companies are still being built, although it’s certainly not easy for anyone, given that we’re all stuck inside and trying to make things work. I think Universe is in an interesting spot; they have a tool that can potentially help some of these struggling businesses move online quicker and create commerce opportunities that they really need to think about given the current realities.

So there’s no thought that we shouldn’t do something just because of the current macro environment if we’re really passionate about it to begin with. Obviously, there’s varying degrees of that for different sectors, but I do think that Universe had been in a great position before this situation, and it seems like they have different opportunities now.

Powered by WPeMatico