Market Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

Today, the U.S. exceeded three million COVID-19 cases and 132,000 deaths. In several states, new hotspots have rolled back plans to reopen businesses. The novel coronavirus has — and will continue — to profoundly impact the way we live and work.

For the moment, that includes a shift in the employment status of many Americans. More than 50 million people have filed for unemployment since mid-March. And while many states have made efforts to reopen businesses and return some sense of normality, these moves have led to a spike in cases and may prolong the pandemic and its ongoing economic impact.

Technology has been a lifeline for many, from food delivery to the 3D printing I highlighted last week, which has worked to address a nation suffering from personal protective equipment shortages. Automation and robotics have also been a constant in conversations around tech’s battle against COVID-19.

Robots don’t get sick, tired or emotionally burnt out, and unlike us, they aren’t walking, talking disease vectors. Automation advocates like to point to the “three Ds” of dull, dirty and dangerous jobs that will eventually be replaced by a robotic workforce, but in the age of COVID-19, nearly any essential job qualifies.

The robotic invasion has already begun in earnest. The service, delivery, health care and sanitation industries in particular have all opened a massive gap over the past several months that automation has been more than happy to roll right through. A recent report from The Brookings Institute notes that automation arrives in the workforce in fits and starts — most notably, during times of economic downturn.

“Robots’ infiltration of the workforce doesn’t occur at a steady, gradual pace. Instead, automation happens in bursts, concentrated especially in bad times such as in the wake of economic shocks, when humans become relatively more expensive as firms’ revenues rapidly decline,” the study found. “At these moments, employers shed less-skilled workers and replace them with technology and higher-skilled workers, which increases labor productivity as a recession tapers off.”

Powered by WPeMatico

Email is a critical tool in modern-day communications, so it’s natural that many entrepreneurs have tried to overhaul it over the years.

In the last decade, email client Mailbox came and went, Slack launched to try to give people an alternative to email and Superhuman emerged to help people more easily reach the promised land of Inbox Zero.

The latest startup to tackle email is project management software maker Basecamp, which launched Hey last month. Within its first 11 days of release, Hey received 125,000 signups, Basecamp founder and CEO Jason Fried tells TechCrunch. Those initial days also included some drama with the Apple App Store, but that’s not what this story is about. Instead, it’s about Hey’s approach, why Fried felt the need to try to rebuild email from the ground up and how he approaches product development.

“The last time people were really excited about email, really, in a broad scale was 16 years ago when Gmail came out in 2004,” Fried says. “I remember it feeling different in a lot of ways. It was really fast, they had archiving, which was a new concept at the time. It worked differently than what I was coming from, which was Yahoo Mail, which was sort of stuck in the past. And I think that’s where Gmail is today — stuck in the past and we’re trying to bring out something brand new with new thinking and new philosophies and a new point of view.”

At its core, Hey is about giving people control over their email and minimizing clutter so users can hear from the people who matter most, Fried says. But control comes at a price: Hey costs $99 per year, with additional fees for three- and two-character email addresses (two-character email addresses are $999 per year and three-character addresses are $349 per year).

“We got a taste of our own medicine because it was not cheap to buy hey.com,” Fried says. “So anything that short in the domain world just costs more. It’s like beachfront property almost, because it’s scarce — more desirable. So given that we have a three-letter domain, two- and three-letter email addresses are just going to cost more. There’s fewer of them and they’re more desirable.”

Hey’s current iteration is targeted toward individual users, but by the end of the year, the plan is to launch a formal enterprise version with collaborative features like shared messages and inboxes. In this unified Imbox (not a typo), people will be able to specify that they don’t want to see work email past a certain time or on weekends.

“A lot of email is collaborative in nature,” Fried says. “People end up forwarding emails around to show someone to get their take. We think that’s totally broken and really antiquated. So we have some stuff built into Hey for work, which lets people share threads with one another in a very different way and be able to have backchannel conversations about threads without having to have those conversations in another product or somewhere that is separate from the actual thread itself.”

There’s much more to this conversation, like how Hey landed on its hypothesis, why control is so important, how email shouldn’t feel like work and more. Below are Fried’s insights.

Powered by WPeMatico

Earlier this week, GGV Capital’s Jeff Richards and Hans Tung joined TechCrunch for an Extra Crunch Live session. During our hour-long chat, we touched on startup profitability, the global venture capital scene, why GGV doesn’t have an office in Europe, how the venture industry is responding to its stark lack of diversity and other issues.

When it comes to useful bits of information, this was perhaps the most useful Extra Crunch Live discussion in which I’ve participated. One moment that stood out came early in the chat when we were talking about COVID-19-driven headwinds and tailwinds and how many startups might be in trouble. Richards said the following (emphasis via TechCrunch):

“You know, the one thing that’s been remarkable for me — I was in Silicon Valley as an entrepreneur in the ’99, 2000 dot-com bubble, and 9/11. I was here in ’08, ’09 — I think there is a level of resiliency in Silicon Valley that we did not have 10 years ago and 20 years ago. I don’t have data to point to that. But we have been saying now for a few months that we’ve been blown away at the level of maturity, calmness, perseverance [and] resiliency that our companies and the founders and management teams have. On an emotional level, it’s been very heartwarming, because you hope to back the kind of people that are building real companies that can withstand challenges.

I think the corollary to that is you’ve seen companies that raised a ton of money and were burning a ton of cash and weren’t building very good businesses, a lot of those frankly went under in Q1 or are going under now. They haven’t been able to raise more cash and they’re just kind of dead.”

Both Richards and Tung were positive about their own portfolio companies’ recent performance and financial health (cash position, really). But it appears that not only are their portfolios doing well, but other startups are a bit more solid than in previous downturns.

On the flip side, however, there is a separate cohort of startups that were running inefficiently before and are now perhaps unfundable. Reading both points in unison, it appears that the startup market is bifurcating between the companies that will come out of the COVID-19 era unwounded, and those that are suffering. And the companies that weren’t the most cash hungry probably have the highest chance of being in the first bucket.

There’s a lot more to get to. So hit the jump for the full video and audio, and a few more of the best bits from the transcript. (You can snag a cheap Extra Crunch trial here if you need one.)

Oh, and don’t forget to stay up to date on coming chats. There’s still a lot to do.

Here’s the full video rewind. Our favorite bits of the transcript follow:

Powered by WPeMatico

Welcome back to our $100 million annual recurring revenue (ARR) series, in which we take irregular looks at companies that have reached material scale while still private. The goal of our project is simple: uncovering companies of real worth beyond how they are valued by private investors.

The Exchange is a daily look at startups and the private markets for Extra Crunch subscribers; use code EXCHANGE to get full access and take 25% off your subscription.

It’s all well and good to get a $1 billion valuation, call yourself a unicorn and march around like you invented the internet. But reaching material revenue scale means that, unlike some highly valued companies, you’re actually hard to kill. (And more valuable, and more likely to go public, we reckon.)

Before we dive into today’s new companies, keep in mind that we’ve expanded the type of company that can make it into the $100M ARR club to include companies that reach a $100 million annual run rate pace. Why? Because we don’t only want to collect SaaS companies, and if we could go back in time we’d probably draw a different box around the companies we are tracking.

Before we dive into today’s new companies, keep in mind that we’ve expanded the type of company that can make it into the $100M ARR club to include companies that reach a $100 million annual run rate pace. Why? Because we don’t only want to collect SaaS companies, and if we could go back in time we’d probably draw a different box around the companies we are tracking.

If you need to catch up, you can find the two most recent entries in the series here and here. For everyone who’s current, today we are adding Snow Software, A Cloud Guru, Zeta Global and Upgrade to the club. Let’s go!

Just this week, Snow Software announced that it has crossed the $100 million ARR mark, according to a release shared with TechCrunch. The Swedish software asset management company has raised a few private rounds, including a $120 million private equity round in 2017. But, unlike many American companies that make this list, we don’t have a historical record of needing extensive private capital to scale.

Powered by WPeMatico

It’s the summer of 1858. London. The River Thames is overflowing with the smell of human and industrial waste. The exceptionally hot summer months have exacerbated the problem. But this did not just happen overnight. Failure to upkeep an aging sewer system and a growing population that used it contributed to a powder keg of effluent, bringing about cholera outbreaks and shrouding the city in a smell that would not go away.

To this day, Londoners still speak of the Great Stink. Recurring cholera infections led to the dawn of the field of epidemiology, a subject in which we have all recently become amateur enthusiasts.

Fast forward to 2020 and you’ll see that modern software pipelines face a similar “Great Stink” due, in no small part, to the vast adoption of continuous integration (CI), the practice of merging all developers’ working copies into a shared mainline several times a day, and continuous delivery (CD), the ability to get changes of all types — including new features, configuration changes, bug fixes and experiments — into production, or into the hands of users, safely and quickly in a sustainable way.

While contemporary software failures won’t spread disease or emit the rancid smells of the past, they certainly reek of devastation, rendering billions of dollars lost and millions of developer hours wasted each year.

This kind of waste is antithetical to the intent of CI/CD. Everyone is employing CI/CD to accelerate software delivery; yet the ever-growing backlog of intermittent and sporadic test failures is doing the exact opposite. It’s become a growing sludge that is constantly being fed with failures faster than can be resolved. This backlog must be cleared to get CI/CD pipelines back to their full capabilities.

What value is there in a system that, in an effort to accelerate software delivery, knowingly leaves a backlog of bugs that does the exact opposite? We did not arrive at these practices by accident, and its practitioners are neither lazy nor incompetent so; how did we get here and what can we do to temper modern software development’s Great Stink?

Powered by WPeMatico

The first wave of AR startups offering smart glasses is now over, with a few exceptions.

Google acquired North this week for an undisclosed sum. The Canadian company had raised nearly $200 million, but the release of its Focals 2.0 smart glasses has been cancelled, a bittersweet end for its soft landing.

Many AR startups before North made huge promises and raised huge amounts of capital before flaring out in a similarly dramatic fashion.

The technology was almost there in a lot of cases, but the real issue was that the stakes to beat the major players to market were so high that many entrants pushed out boring, general consumer products. In a race to be everything for everybody, the industry relied on nascent developer platforms to do the dirty work of building their early use cases, which contributed heavily to nonexistent user adoption.

A key error of this batch was thinking that an AR glasses company was hardware-first, when the reality is that the missing value is almost entirely centered on missing first-party software experiences. To succeed, the next generation of consumer AR glasses will have to nail this.

Image Credits: ODG

Powered by WPeMatico

While many investors say sheltering in place has broadened their appetite for funding companies located outside major hubs, one firm is doubling down on backing startups in America’s heartland.

Launched in 2016 by Brett Brohl, The Syndicate Fund rebranded to Bread & Butter Ventures earlier this month (a reference to one of Minnesota’s many nicknames). Along with the rebrand, longtime Google executive and Revolution partner Mary Grove joined the team as a general partner and Stephanie Rich came aboard as head of platform.

The growth of the Twin Cities’ startup ecosystem is precisely why The Syndicate Fund rebranded. The firm, which has $10 million in assets under management, will invest in three of Minneapolis’ biggest strengths: agriculture and food, health care and enterprise software.

Agtech interest spans the entire spectrum from farming to restaurants and grocery stores. The firm is also interested in the “messy middle” of supply chain and logistics around food, said Brohl and is interested in a mix of software, hardware and biosciences. Within health care, the firm evaluates solutions focused on prevention versus treatment, female health startups working on maternal health and fertility and software focused on the aging population and millennials.

It’s also looking at enterprise software that can serve large businesses and scale efficiently.

Powered by WPeMatico

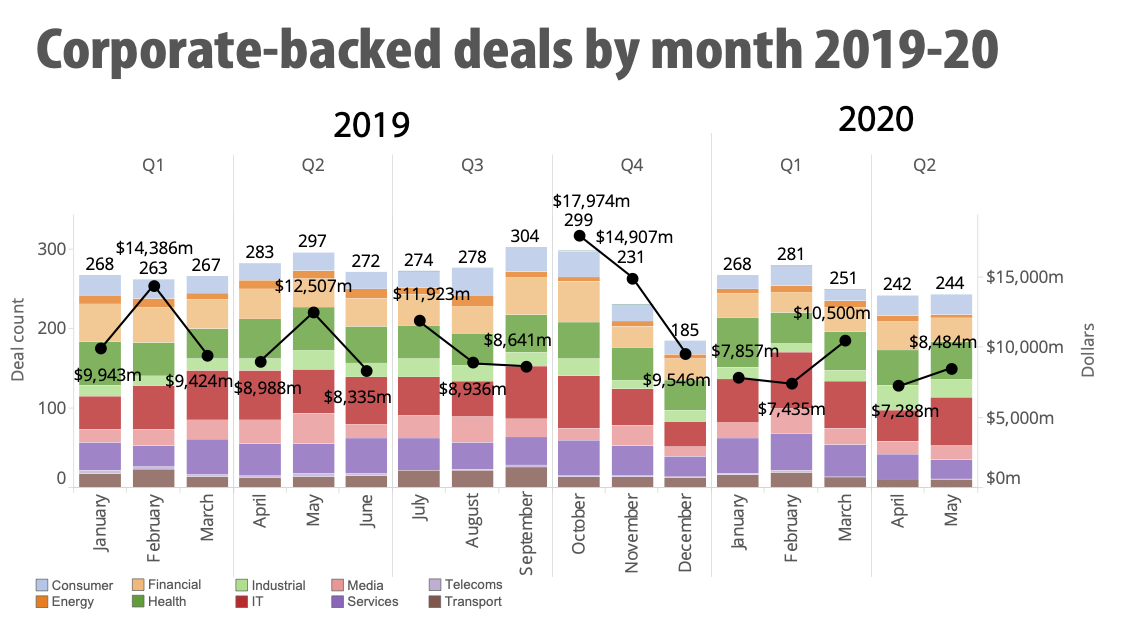

When the going gets tough, it’s common for some corporate VCs to head for the hills.

Today, it’s a narrative that’s emerging again amid the COVID-19 crisis. Global corporate venture deals fell from a total of 580 in April/May of 2019 to 486 in the same period this year, according to Global Corporate Venturing.

However, institutional VC deals are also headed for a decline, with PitchBook anticipating a drop in transaction volume over the next several quarters, as well as a downturn in valuations.

Image Credits: Global Corporate Venturing

It remains to be seen how it will play out this time, but I believe corporate venture capital (CVC) will not only stick around, but also be a vital part of the innovation ecosystem going forward.

I know that Merck Global Health Innovation Fund (MGHIF) remains fully committed to “doing” venture. Now, more than ever, health innovation is vital. Second, we understand that many of today’s most successful companies were funded in times of uncertainty. In fact, to put our money where our mouth is, we’ve recently completed two spinouts, three follow-on investments, and two new deals in 2020 — all since COVID hit. We intend to increase that pace going forward in 2020 and beyond.

It hasn’t been easy. It’s hard to do venture when you can’t venture out into the world, meet founders and do diligence the way we did in the past. But it is possible, if you do some innovating of your own and set up a smoothly functioning system to do CVC virtually.

Here’s how we’ve done it.

Powered by WPeMatico

If you have bought a house in the last decade, you likely started the process online. Perhaps you browsed for your future dream home on a website like Zillow or Realtor, and you may have been surprised by how quickly things moved from seeing a property to making an offer.

When you reached the closing stage, however, things slowed to a crawl. Some of those roadblocks were anticipated, such as the process of getting a mortgage, but one likely wasn’t: the tedious and time-consuming process of obtaining title insurance — that is, insurance that protects your claim to home ownership should any claims arise against it after sale.

For a product that is all but required to purchase a home, title insurance isn’t something many people know about until they have to pay for it and then wait up to two months to get.

Now, finally, a handful of startups are taking on the title insurance industry, hoping to make the process of buying a policy easier, cheaper and more transparent. These startups, including Spruce, States Title, JetClosing, Qualia, Modus and Endpoint, enable part or all of the title insurance buying process. Whether these startups can finally topple the title insurance monopoly remains to be seen, but they are already causing cracks in the system.

To that end, we’ve outlined what’s broken about today’s title industry; recent developments in technology and government that are priming the industry for change; and a synthesis of some key trends we’ve observed in the space, as entrepreneurs begin to capitalize on a tipping point in a century-old, $14 billion business.

To understand how startups are beginning to challenge title insurance incumbents, we need to first understand what title insurance is and what title companies do.

Title insurance is unique from other types of insurance, which require ongoing payments and protect a buyer against future incidents. Instead, title insurance is a one-time payment that protects a buyer from what has already happened — namely errors in the public record, liens against the property, claims of inheritance and fraud. When you buy a home, title insurance companies research your property’s history, contained in public archives, to make sure no such claims are attached to it, then correct any issues before granting a title insurance policy.

Powered by WPeMatico

Agora isn’t the only company headquartered outside the United States aiming to go public domestically this quarter. After catching up on Agora’s F-1 filing, the China-and-U.S.-based, API-powered tech company that went public last week, today we’re parsing DoubleDown Interactive’s IPO document.

The Exchange is a daily look at startups and the private markets for Extra Crunch subscribers; use code EXCHANGE to get full access and take 25% off your subscription.

The mobile gaming company is targeting the NASDAQ and wants to trade under the ticker symbol “DDI.”

As with Agora, DoubleDown filed an F-1, instead of an S-1. That’s because it’s based in South Korea, but it’s slightly more complicated than that. DoubleDown was founded in Seattle, according to Crunchbase, before selling itself to DoubleU Games, which is based in South Korea. So, yes, the company is filing an F-1 and will remain majority-held by its South Korean parent company post-IPO, but this offering is more a local affair than it might at first seem.

As with Agora, DoubleDown filed an F-1, instead of an S-1. That’s because it’s based in South Korea, but it’s slightly more complicated than that. DoubleDown was founded in Seattle, according to Crunchbase, before selling itself to DoubleU Games, which is based in South Korea. So, yes, the company is filing an F-1 and will remain majority-held by its South Korean parent company post-IPO, but this offering is more a local affair than it might at first seem.

Even more, with a $17 to $19 per-share IPO price range, the company could be worth up to nearly $1 billion when it debuts. Does that pricing make sense? We want to find out.

So let’s quickly explore the company this morning. We’ll see what this mobile, social gaming company looks like under the hood in an effort to understand why it is being sent to the public markets right now. Let’s go!

Any gaming company has to have its fun-damentals in place so that it can have solid financial results, right? Right?

Anyway, DoubleDown is a nicely profitable company. In 2019 its revenue only grew a hair to $273.6 million from $266.9 million the year before (a mere 2.5% gain), but the company’s net income rose from $25.1 million to $36.3 million, and its adjusted EBITDA rose from $85.1 million to $101.7 million over the same period.

Powered by WPeMatico