Market Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

Robinhood announced this morning that it has raised $200 million more at a new, higher $11.2 billion valuation. The new capital came as a surprise.

Astute observers of all things fintech will recall that Robinhood, a popular stock trading service, has raised capital multiple times this year, including an initial $280 million round at an $8.3 billion valuation, and a later $320 million addition that brought its valuation to $8.6 billion.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Those rounds, coming in May and July, now feel very passé in the sense that they are frightfully cheap compared to the price at which Robinhood just added new funds. D1 Partners — a private capital pool founded in 2018 — led the funding.

The unicorn’s new nine-figure tranche, a Series G, values the firm at $11.2 billion. A $2.6 billion bump in about a month is an impressive result, one that points to an inescapable conclusion: Robinhood is still growing, and fast.

How fast is the question. There are three things to bring up in this regard: Trading growth at Robinhood, the company’s soaring incomes from selling order flow to other financial institutions, and, oddly enough, crypto. Let’s peek at each and come up with a good why as to the new Robinhood valuation.

After all, we’re going to see an IPO from this company before the markets get less interesting, if it’s smart.

Robinhood is currently walking a line between enthusiasm that its trading volume is growing and conservatism, arguing that its userbase is not majority-comprised of day traders. The company is stuck between the need for huge revenue growth and keeping pedestrian users from tanking their net worth with unwise options bets.

It’s worth noting that Robinhood spent a lot of its funding round announcement email to TechCrunch talking about its users safety and education work. It makes sense given that we know that the company is seeing record trades, and record incomes from options themselves. After a Robinhood user killed themself after misunderstanding an options trade on the platform, Robinhood pledged to do better. We’re keeping tabs on how well it manages to meet the mark of its promise.

But back to the revenue game, let’s talk volume. On the trading front Robinhood has lots of darts. And by darts we mean daily average revenue trades. Robinhood had 4.31 million DARTs in June, with the company adding that “DARTs in Q2 more than doubled compared to Q1” in an email.

The huge gain in trading volume does not mean that most Robinhood users are day trading, but it does imply that some are given the huge implied trading volume results that the DARTs figure points to. Robinhood saw around 129,300,000 trades in June, which is 30 days. That’s a lot!

Powered by WPeMatico

Over the past two years, the global supply chain has been hit with two major upheavals: the United States-China trade war and, more cataclysmically, COVID-19.

When Reefknot Investments launched its $50 million fund for logistics and supply chain startups last September, the industry was already dealing with the effects of the tariff war, says managing director Marc Dragon. Then a few months later, the COVID-19 crisis began in China before spreading to the rest of the world, disrupting the supply chain on an unprecedented scale.

Almost all industries have been impacted, from food, consumer goods and medical supplies to hardware.

Reefknot, a joint venture between Temasek, Singapore’s sovereign fund, and global logistics company Kuehne + Nagel, focuses on early-stage tech companies that use AI to solve some of the supply chain’s most pressing issues, including risk forecasting, financing and tracking goods around the world.

In March, around the time the World Health Organization declared the COVID-19 crisis a pandemic, Reefknot surveyed nine shippers about the challenges they face. While there are other macroeconomic factors at play, including Brexit and the oil price war, the survey’s main focus was on the combined effect of COVID-19 and the U.S.-China trade war on the supply chain and logistics industry.

According to the study, the main things shippers want is the ability to dynamically manage supply chain risks and operations and optimize cash flow between corporate buyers and their suppliers, who often struggle with working capital.

Many of the current solutions used in the supply chain involve a lot of manual tasks, including spreadsheets to predict demand, phone calls to confirm capacity on planes and ships and checking goods to make sure orders were fulfilled properly.

Powered by WPeMatico

It’s been less than a year since Group Nine Media acquired PopSugar — but it’s been a uniquely challenging time in digital media.

Brian Sugar founded the eponymous women’s lifestyle site with his wife Lisa Sugar . Post-acquisition, he’s become president for the entirety of Group Nine (which also owns Thrillist, NowThis, The Dodo and Seeker) and also joined the company’s board.

That job probably looks very different from what he expected last fall. The company had to lay off 7% of its staff back in April, which Sugar described as “one of the worst days of my career.” At the same time, he remains confident about the online advertising business. In his view, it’s TV advertising that’s taken a “huge punch” in the face and will never recover.

“We like to think of ourselves as one of the fastest, most innovative publishers out there,” Sugar told me. “And now’s the time for us to kind of show that off.”

You can read an edited, updated and condensed transcript of our conversation below, in which I talked to Sugar about how his role has evolved, how he motivates the team during difficult times and what gets lost in the shift to remote work.

TechCrunch: Obviously, it’s been a crazy couple of months since we last talked. What does your job look like now?

Brian Sugar: Well, I feel like a data miner, searching for answers. I feel like a hackathon engineer. And I feel like a therapist. You know, we like to think of ourselves as one of the fastest, most innovative publishers out there. And now’s the time for us to kind of show that off.

[We’ve just been] looking at data on how people are consuming our content across platforms. And on our site, we’ve come up with some really interesting ideas that we’ve implemented. We’ve been having these really cool hackathon Fridays to build stuff quickly, because a lot of people feel like they have a little bit more time on their hands — because you don’t have to travel to meetings, you can get more work done. Some people feel they’re more efficient.

We’re extremely optimistic. All our brands are extremely optimistic, and so is [the whole] company.

You mentioned launching some new products to respond to how audience behavior is changing. Are there any examples?

The first one [is] the PopSugar Fitness thing. We were planning on launching a paid workout subscription service in May, but everybody was working from home [in March], and we decided to pull the launch all the way up to as fast as we can launch it. We launched it that following weekend. Since the launch in late March, over the past few months, we’ve had 200,000 people sign up, and we have 50,000 monthly active users on it.

Powered by WPeMatico

Andy Rachleff founded Wealthfront a decade ago to give investors a better and smarter way to manage their wealth, building on core academic research showing that a carefully balanced portfolio of low-fee ETFs outperformed more aggressive strategies. Since then, the company has taken in billions of dollars of invested capital under management and expanded into new banking services, including high-interest checking accounts.

Rachleff and I talked on Extra Crunch Live about where Wealthfront is heading as it speeds toward its second decade, how he sees the competition from other, more active trading platforms like Robinhood and his advice for startup founders looking to build enduring products and companies away from the daily status quo.

Rachleff began our conversation talking about the future of Wealthfront, which is increasingly moving beyond its wealth management app to new services.

“Our vision is to automate all of your finances — we call this self-driving money,” he said. That platform is expected to role out in September, and include features like easy direct deposit and automated bill pay, with any savings left over automatically moving to the right investment assets that meet a user’s chosen risk tolerance.

Powered by WPeMatico

Before the coronavirus made edtech more relevant, companies in the sector were historically likely to see slow, low exits. Despite successful IPOs by 2U, Chegg and Instructure in the United States, public markets are not crowded with edtech companies.

Some of the largest exits in the space include LinkedIn’s scoop of Lynda for a $1.5 billion in cash and stock and TPG’s purchase of Ellucian for $3.5 billion.

But both of those deals happened in 2015. Five years later, edtech is cooler and surging — but is it seeing exits? Are Lynda and Ellucian one-off success stories?

2U’s co-founder and CEO, Chip Paucek, said he is optimistic.

“We are a rare edtech IPO,” he told TechCrunch last week. “For a long time in edtech it was either ‘sell to Pearson or not.’”

Despite the sector’s slow past, Paucek said now is a good time to start an edtech company because the sector “is finally starting to hit its stride” with more back-end infrastructure and demand for online education.

This morning, let’s use some data to paint a picture of the landscape of edtech exits and bring some balance to this stodgy stereotype.

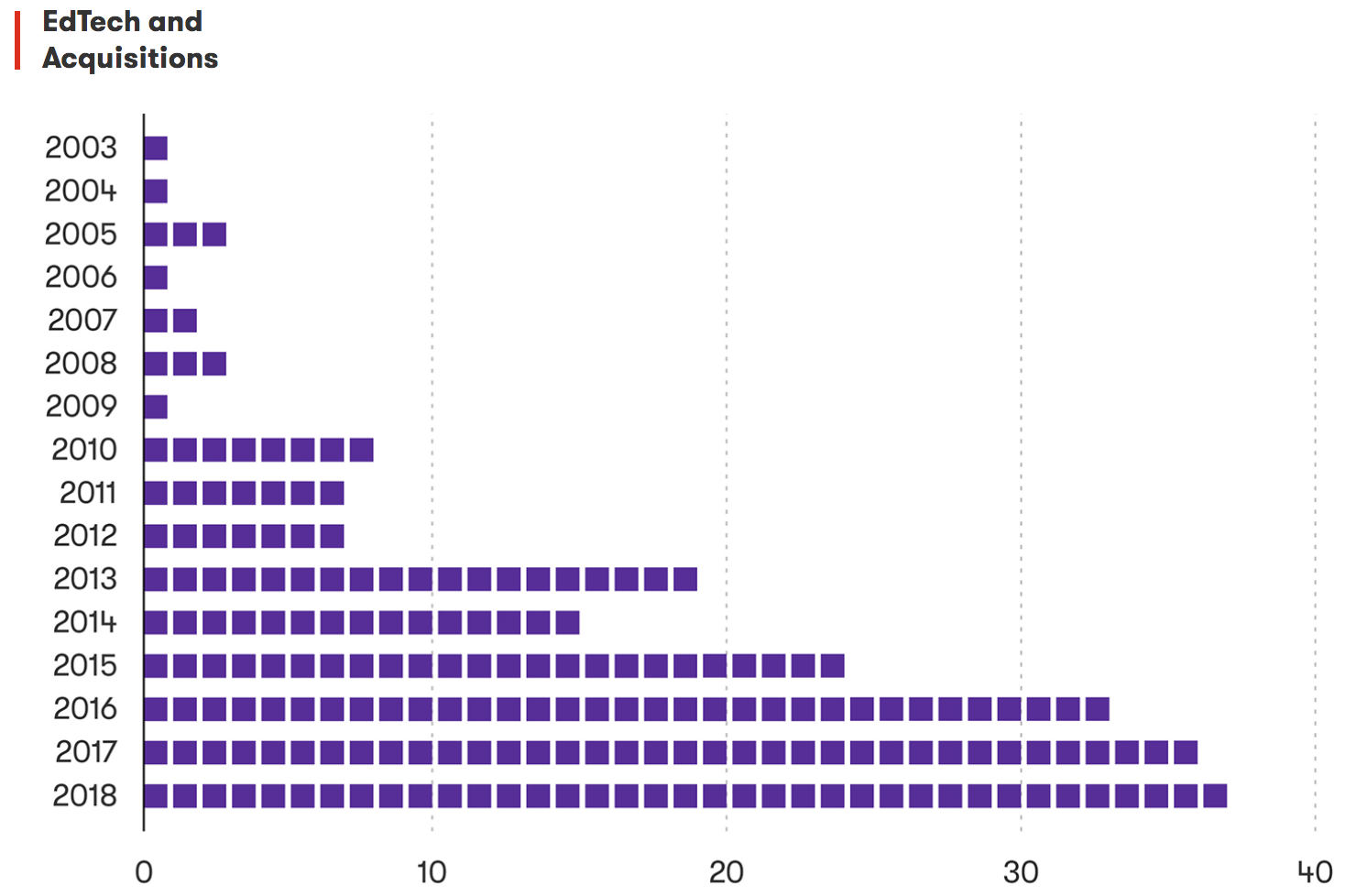

Boot the growth

Boot the growthThere have been approximately 225 acquisitions in edtech between 2003 and 2018, according to Crunchbase data. RS Components sent me a graph in March to contextualize this timeframe a bit more:

Edtech deals over time. Graph credit: RS Components.

Powered by WPeMatico

Telehealth, or remote, tech-enabled healthcare, has existed for years in primary medical care through companies like Teladoc (NYSE: TDOC), Doctors on Demand and MDLIVE.

In recent years, the application of telehealth had rapidly expanded to address specific chronic and behavioral health issues like mental health, weight loss and nutrition, addiction, diabetes and hypertension, etc. These are real and oftentimes very severe issues faced by people all over the world, yet until now have seen little to no use of technology in providing care.

We believe behavioral health is particularly suited to benefit from the digitization trends COVID-19 has accelerated. Previously, we’ve written about the pandemic’s impact on online learning and education, both for K-12 students and adult learners. But behavioral health is another area impacted by the fundamental change in consumers’ behavior today. Below are four reasons we think the time is now for behavioral health startups — followed by five key factors we think characterize successful companies in this area.

Traditional behavioral healthcare is cost-prohibitive for most people. In-person therapy costs $100+ per session in the U.S., and many mental health and substance-use providers don’t accept insurance because they don’t get paid enough by insurers.

By contrast, telehealth reduces overhead costs and scales more effectively. Leveraging technology, providers can treat more patients in less time with almost zero marginal costs. Mobile-based communications enable asynchronous care that further helps providers scale. Access to digital content gives patients on-going support without the need for a human on the other side. This is particularly useful in treating behavioral health issues where ongoing support and motivation may be necessary.

Globally, we face an extreme shortage of behavioral health providers. For example, the United States has fewer than 30,000 licensed psychiatrists (translating to <1 for every 10,000 people). Outside of big cities, the problem gets worse: ~50-60% of nonmetro counties have no psychologists or psychiatrists at all.

Even when providers are available, wait times for appointments are notoriously long. This is a huge issue when behavioral health conditions often require timely intervention.

We are seeing new platforms build large networks of certified coaches, licensed psychologists and psychiatrists, and other providers, aggregating supply in what has historically been a scarce and a highly fragmented provider population.

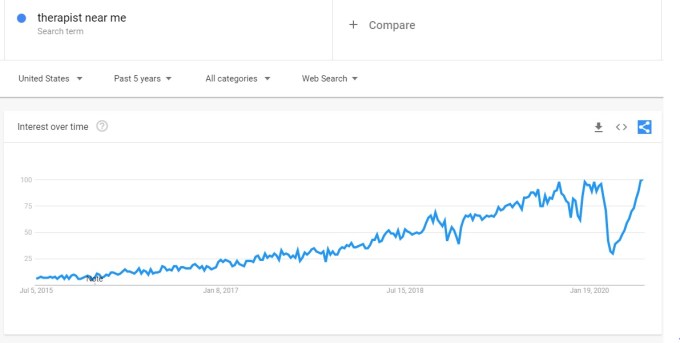

We believe the stigma associated with mental illness and other behavioral health conditions is dissipating. More and more public figures are speaking out about their struggle with anxiety, depression, addiction and other behavioral health issues. Our zeitgeist is shifting fast, and there’s an all-time high in people seeking help as the Google Trends data below demonstrates.

Image Credits: Google

Note: The anomalous dip in March/April ’20 was driven by mandatory shelter-in-place due to COVID-19.

Powered by WPeMatico

Quantum computers exploit the seemingly bizarre yet proven nature of the universe that until a particle interacts with another, its position, speed, color, spin and other quantum properties coexist simultaneously as a probability distribution over all possibilities in a state known as superposition. Quantum computers use isolated particles as their most basic building blocks, relying on any one of these quantum properties to represent the state of a quantum bit (or “qubit”). So while classical computer bits always exist in a mutually exclusive state of either 0 (low energy) or 1 (high energy), qubits in superposition coexist simultaneously in both states as 0 and 1.

Things get interesting at a larger scale, as QC systems are capable of isolating a group of entangled particles, which all share a single state of superposition. While a single qubit coexists in two states, a set of eight entangled qubits (or “8Q”), for example, simultaneously occupies all 2^8 (or 256) possible states, effectively processing all these states in parallel. It would take 57Q (representing 2^57 parallel states) for a QC to outperform even the world’s strongest classical supercomputer. A 64Q computer would surpass it by 100x (clearly achieving quantum advantage) and a 128Q computer would surpass it a quintillion times.

In the race to develop these computers, nature has inserted two major speed bumps. First, isolated quantum particles are highly unstable, and so quantum circuits must execute within extremely short periods of coherence. Second, measuring the output energy level of subatomic qubits requires extreme levels of accuracy that tiny deviations commonly thwart. Informed by university research, leading QC companies like IBM, Google, Honeywell and Rigetti develop quantum engineering and error-correction methods to overcome these challenges as they scale the number of qubits they can process.

Following the challenge to create working hardware, software must be developed to harvest the benefits of parallelism even though we cannot see what is happening inside a quantum circuit without losing superposition. When we measure the output value of a quantum circuit’s entangled qubits, the superposition collapses into just one of the many possible outcomes. Sometimes, though, the output yields clues that qubits weirdly interfered with themselves (that is, with their probabilistic counterparts) inside the circuit.

QC scientists at UC Berkeley, University of Toronto, University of Waterloo, UT Sydney and elsewhere are now developing a fundamentally new class of algorithms that detect the absence or presence of interference patterns in QC output to cleverly glean information about what happened inside.

A fully functional QC must, therefore, incorporate several layers of a novel technology stack, incorporating both hardware and software components. At the top of the stack sits the application software for solving problems in chemistry, logistics, etc. The application typically makes API calls to a software layer beneath it (loosely referred to as a “compiler”) that translates function calls into circuits to implement them. Beneath the compiler sits a classical computer that feeds circuit changes and inputs to the Quantum Processing Unit (QPU) beneath it. The QPU typically has an error-correction layer, an analog processing unit to transmit analog inputs to the quantum circuit and measure its analog outputs, and the quantum processor itself, which houses the isolated, entangled particles.

Powered by WPeMatico

On a Wednesday at 4 p.m. in June 2017, I was in a small, packed office in midtown Manhattan.

The overcrowded conference room, with at least five more people than any fire marshal would recommend, was stacked comically high with paperwork and an eclectic collection of cheap pens. As I neared the end of the third hour and the ink of my seventh pen, I realized the mortgage closing process may be somewhat antiquated.

After closing on my first home, it was inconceivable to me that every other expense in my life has gone digital, but the most significant purchase I’ve ever made required hundreds of signatures and several handwritten checks delivered in person. By comparison, I have been able to repay my student loans, comparable in magnitude to a down payment, exclusively through online portals.

The COVID-19 pandemic has changed nearly every facet of our lives. One potential silver lining for the real estate world may be a forced reckoning with the mortgage closing process. Technological advances like e-closings are accelerating this arduous process into the digital age. The U.S. Census Bureau released figures in July citing the rise in homeownership across the country as the pandemic fuels the demand for single-family properties outside of urban areas. This is confirmed by the significant spike in mortgage applications seen in the second quarter of 2020.

The first signs of digitization of the mortgage origination process were seen in mid-2010 when lenders began adopting digital disclosures. Despite the availability of technology, the market has been slower to fully embrace digital closings that enable the full loan package to be electronically reviewed, recorded, signed and notarized. A true e-closing includes a digital promissory note (“eNote”), a virtual closing appointment and the electronic transfer and recording of documents by the county, all of which can be remotely coordinated and executed by the parties involved. The market started to pick up pace in recent years, and we’ve seen the number of e-mortgages increase by more than 450% from 2018 to 2019.

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

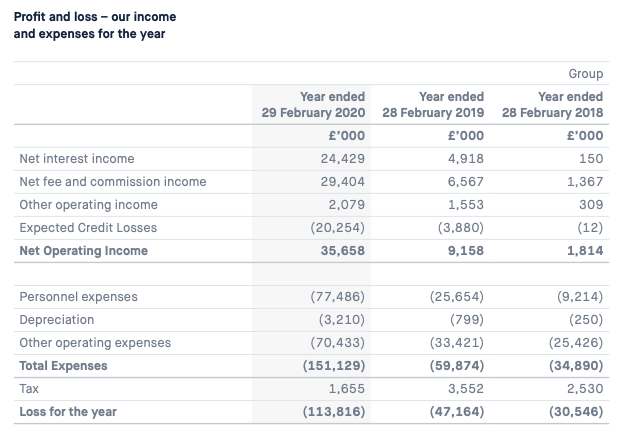

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Tech stocks retain their highs as the second quarter’s earnings season begins to fade into the rearview mirror, and there are still a number of companies looking to go public while the times are good. It looks like a smart move, as public investors are hungry for growth-oriented shares — which is just what tech and venture-backed companies have in spades.

The companies currently looking to go public are diverse. China-based real-estate giant KE Holdings — a hybrid listings company and digital transaction portal for housing — is looking to raise as much as $2.3 billion in a U.S. listing. Xpeng, another China-based company that builds electric vehicles, is looking to list in the U.S as well. Xpeng has the distinction of being gross-margin negative in every key time period detailed in its S-1 filing.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

And then there’s Duck Creek Technologies, a domestic tech company looking to go public on the back of growing SaaS revenues. This morning let’s quickly spin through Duck Creek’s history, peek at its financial results, calculate its expected valuation and see how its pricing fits compared to current norms.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

The KE IPO will be a big affair because the company is huge and profitable with $3.86 billion in H1 2020 revenue leading to $227.5 million in net income. The Xpeng IPO will be interesting because Tesla’s strong share price has given float to a great many EV boats. But Duck Creek is a company slowly letting go of perpetual license software sales and scaling its SaaS incomes while still generating nearly half its revenues from services. It’s a company we can understand, in other words.

So let’s get under the skin of the Boston-based company that also claims low-code functionality. This will be fun.

Powered by WPeMatico