Marc Benioff

Auto Added by WPeMatico

Auto Added by WPeMatico

Mike Sepso has joined the board of directors for 100 Thieves, an esports and content creation brand.

Sepso co-founded Major League Gaming in 2002, bringing the first true semblance of infrastructure to competitive gaming. MLG became the biggest independent esports league in the world, and played a big part in the evolution of esports as we know it today. In fact, MLG secured the first televised esports series ever with NBC sports, and eventually launched its own esports streaming platform.

MLG was acquired for $46 million by Activision Blizzard in 2016, but still lives as an esports content hub for Activision Blizzard titles like Call of Duty and Overwatch.

Sepso joins the 100 Thieves board alongside 100 Thieves founder and CEO Matthew “Nadeshot” Haag, president and COO John Robinson, Jake Cohen from Detroit Venture Partners and Scooter Braun (entertainment industry mogul who represents Justin Bieber and Ariana Grande).

“Mike is the godfather of esports,” said Haag. “The most influential thing that happened in my career was seeing Halo 2 competitions on Major League Gaming on TBS on the weekends. It was just mind-blowing that kids like me could play games competitively.”

Currently, Sepso serves as chairman and co-founder of the Electronic Sports Group, which is an advisory firm for executives across the finance, media, advertising and sports industries as they navigate esports deals.

“[Haag] been able to move quickly and build something that transcends esports and esports teams and has become an increasingly significant mainstream brand, and that opens up a lot of business opportunities,” said Sepso. “The strategy that 100 Thieves has put in place, using esports and gaming personalities as a way to bring this brand to market, I think it could eventually be much more than that.”

Before founding 100 Thieves, Haag was a decorated pro player in his own right and continues to be a popular Twitch streamer and YouTuber. Many esports orgs are founded by former pros, but Haag has taken a Silicon Valley approach to building out 100 Thieves, at least with regards to pace.

100 Thieves built out professional teams for a variety of titles very quickly. The company also secured capital from the likes of Sequoia, Marc Benioff, Drew Houston, Dan Gilbert, Tao Capital and Advancit Capital. Alongside traditional VCs and tech angels, 100 Thieves has also gotten investment from Scooter Braun and Drake.

Total funding for the org is $25 million.

Beyond titles and professional teams, 100 Thieves is diversifying its product early as well, with a content creator house and a line of apparel coming this spring.

The company recently signed a deal with Totino’s (yes, the pizza rolls) that includes an upcoming docuseries that offers a look behind the scenes at the 100 Thieves Call of Duty team.

Powered by WPeMatico

Healthy oceans are on the minds of Marc and Lynne Benioff, and they showed it today with a $1.5 million donation to the Sustainable Ocean Alliance (SOA), a new nonprofit attempting to promote and incubate conservation-focused startups. The money will considerably expand the organization’s upcoming Ocean Solutions accelerator.

Benioff appeared Wednesday on a panel at Davos about the “ocean economy,” at which he mentioned the donation and SOA. He joined rather a powerhouse lineup to address the issues of environmental dangers threatening wallets as well as whales: Michelle Bachelet (U.N. High Commissioner for Human Rights), Enric Sala (an Explorer-in-Residence at National Geographic), Nina Jensen of REV Ocean and indefatigable environmental crusader Al Gore. I certainly wish I could have attended.

It’s clear that the Salesforce founder is as concerned about environmental issues as he is about social ones, and as ready to write a check when there’s a compelling reason to do so.

Benioff at Disrupt SF in 2016

“Our oceans are in grave danger, due to the many consequences of climate change and pollution,” he said in a press release announcing the donation. “These challenges can be solved with investment and innovation. Lynne and I are proud to support [SOA founder] Daniela Fernandez and the Sustainable Ocean Alliance’s bold vision to create 100 new startups by 2021 to help heal the ocean.”

The SOA started its accelerator last year with a handful of interesting ocean- and conservation-focused startups: a device to keep fish from getting tangled in nets, wave-harvesting energy tech, materials for oil cleanups, that sort of thing. It’s got another batch planned and the Benioff’s donation will allow it to triple the number of startups included. Several will be going to the “Accelerator at Sea,” an eight-day event aboard a Lindblad Expeditions ship sailing from Alaska this summer.

Last year the organization also got a sudden cash infusion from a motivated donor: the mysterious Pine, who distributed some $86 million to charity (and nonprofits like SOA) after making a tremendous amount of money on Bitcoin. These are one-off donations, naturally — so of course financial sustainability, as well as ecological, is on Fernandez’s mind.

“We realize that we cannot simply depend on individual donors or anonymous cryptocurrency gifts. We have had difficulty finding traditional forms of funding for SOA due to the limited amount of funds that are allocated to such a niche sector,” Fernandez, who is at Davos but unfortunately not on the aforementioned panel, told me.

“Instead of only having to fundraise, we have had to create new funders by educating them about the importance of protecting the ocean. It is the typical entrepreneurial scenario of building the plane while flying it. However, in our case, we had to build the plane while simultaneously developing the aircraft market.”

As part of that the nonprofit now plans to release a yearly “State of Our Ocean” report — the first came out today. It’s not so much a scholarly or analytical report like you might have from NOAA or national fisheries or wildlife concerns. Fernandez says this one “takes into account the perspective of young people who are on the ground working to solve the issues at hand. SOA interviewed 3,000 young ocean leaders from around the world who gave their input as to what the ocean priorities should be in 2019 and graded our current world leaders on their efforts to restore the health of the ocean.”

It’s good to ask the un-jaded youngs about things like this, and SOA specifically aims to find and promote young entrepreneurs and activists, so it’s on brand. I’ve read through it and there’s a lot of info about impending disasters, many of which have to do with climate change, but plenty are caused by people as well (or rather, caused by people more recently). It’s a bit depressing, but what isn’t?

Hopefully the cash infusion will help scoop up more of those motivated young folks into the program. We’ll probably hear more from the SOA when it finds some more startups to load into the accelerator.

Powered by WPeMatico

Carbon Engineering, a Canadian company developing technology to remove carbon dioxide from the atmosphere and process it for use in enhanced oil recovery or in the creation of new synthetic fuels, has locked in financing from two big industry backers — Chevron and Occidental Petroleum — to bring its products to market.

The undisclosed amount of capital Carbon Engineering raised from the investment arms of two of the world’s largest oil and gas companies — Oxy Low Carbon Ventures and Chevron Technology Ventures — will be used to commercialize its technology at a time when legislation in California and British Columbia are making low-carbon fuels more economically viable, according to a statement from the company’s chief executive, Steve Oldham. The company had already managed to nab Microsoft co-founder Bill Gates as an investor.

Gates is one of several big-name backers to be drawn to renewable energy technologies in the face of a steadily warming planet that’s rapidly approaching a tipping point of no return when it comes to global climate change. Together with a group of other multi-billionaires, including Marc Benioff, Jeff Bezos, Michael Bloomberg, Richard Branson, Jack Ma, Masayoshi Son and Meg Whitman, Gates launched a $1 billion fund called Breakthrough Energy Ventures last year to back companies that are developing things like new energy storage and water production technologies.

The Squamish, B.C.-based Carbon Engineering isn’t in the Breakthrough portfolio, but is one of several companies working on making economically viable a technology called “direct air capture” of carbon dioxide.

At the company’s pilot plant in Squamish, air gets hoovered up by giant fans into a processing facility where it is treated with potassium hydroxide, which captures and holds the carbon dioxide. Then more chemicals and heat are added to the mix to create millions of small white pellets — which contain higher concentrations of the carbon dioxide.

After that, the pellets are heated again to create a gas that is almost pure carbon dioxide. That gas can be either sequestered underground (a proposition with no economic benefit for Carbon Engineering at the moment) or converted back into fuels or chemicals, or used in enhanced oil recovery.

Carbon Engineering and competitors like ClimeWorks or Global Thermostat claim they can remove carbon dioxide from the atmosphere for roughly $100 per ton, or a bit less once they can get to scale. To make money though, they’ll need to refine that carbon dioxide into some sort of product — likely a fuel, which will return that carbon to the atmosphere.

Other companies tackling carbon capture, like Newlight Technologies and Opus12, convert the carbon into plastics or chemicals, while companies like CarbonCure aim to turn the captured carbon into a cement replacement.

While these products from carbon emissions are available, they’re not yet commercially viable at a significant scale. Oldham told National Public Radio that the fuel Carbon Engineering manufactures is roughly 20 percent more expensive than regular gasoline.

That’s why states like California are putting incentives in place to offset the added costs of using these low-carbon products.

Carbon Engineering has already spent $30 million to develop its process, while Climeworks raised $31 million last year to develop its own version of this carbon capture technology.

Not all climate watchers are convinced that these kinds of negative emission technologies are the answer. They argue that it’s less expensive to use renewable energy and other carbon-free energy sources than to take carbon dioxide out of the air.

At this point, though, emission reductions may not be enough. Given the dire reports coming out of the Trump administration and the Intergovernmental Panel on Climate Change, it’s going to take pretty much a combination of everything that humanity’s got to avoid a pretty catastrophic fate for a pretty large portion of the world’s population.

Even the companies that have been notorious for their contributions to the climate crisis that the world faces are waking up to the need for decarbonization (even if it’s an open question of whether they’re being dragged to the table or sitting down of their own free will).

Oxy Low Carbon Ventures is a good example. Reading the writing on the wall, the firm has invested not just in Carbon Engineering, but another company called NET Power, which purports to have developed a power plant with zero emissions.

“It is a very important time for the air capture field right now,” said Oldham in a statement. “We’re seeing leading jurisdictions, like California and British Columbia, creating markets for low carbon fuels and technologies like DAC, through effective climate policy. These efficient market-based regulations, and action from energy industry leaders like Occidental and Chevron, show the power of policy in driving innovation and achieving emissions reductions while delivering reliable and affordable energy.”

Powered by WPeMatico

The good times kept on rolling this year for Salesforce with all of the requisite ingredients of a highly successful cloud company — the steady revenue growth, the expanding product set and the splashy acquisitions. The company also opened the doors of its shiny new headquarters, Salesforce Tower in San Francisco, a testament to its sheer economic power in the city.

Salesforce, which set a revenue goal of $10 billion a few years ago is already on its way to $20 billion. Yet Salesforce is also proof you can be ruthlessly good at what you do, while trying to do the right thing as an organization.

Make no mistake, Marc Benioff and Keith Block, the company’s co-CEOs, want to make obscene amounts of money, going so far as to tell a group of analysts earlier this year that their goal by 2034 is to be a $60 billion company. Salesforce just wants to do it with a hint of compassion as it rakes in those big bucks and keeps well-heeled competitors like Microsoft, Oracle and SAP at bay.

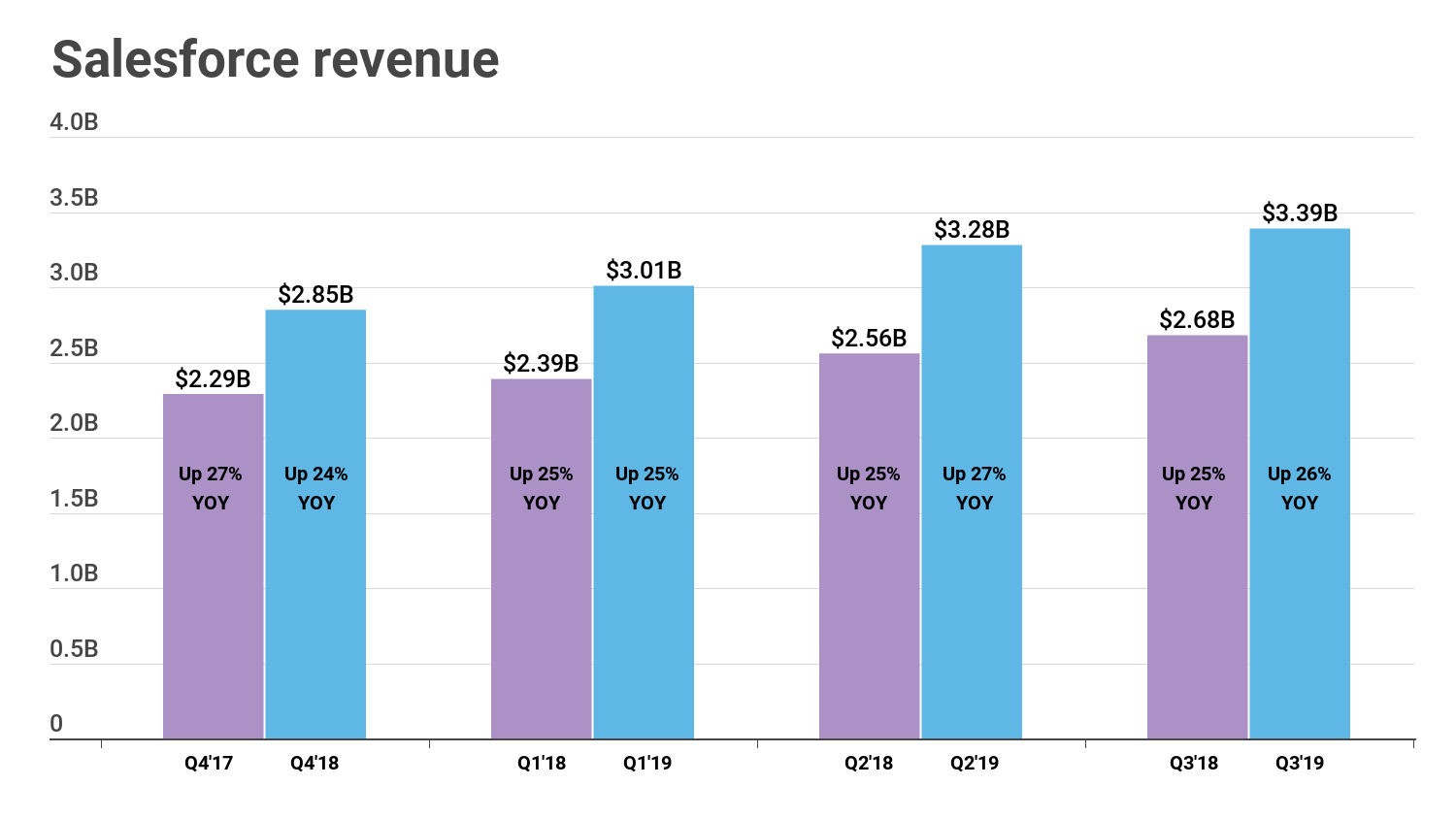

In the end, a publicly traded company like Salesforce is going to be judged by how much money it makes, and Salesforce it turns out is pretty good at this, as it showed once again this year. The company grew every quarter by over 24 percent YoY and ended up the year with $12.53 billion in revenue. Based on its last quarter of $3.39 billion, the company finished the year on a $13.56 billion run rate.

This compares with $9.92 billion in total revenue for 2017 with a closing run rate of $10.72 billion.

Even with this steady growth trajectory, it might be some time before it hits the $5 billion-a-quarter mark and checks off the $20 billion goal. Keep in mind that it took the company three years to get from $1.51 billion in Q12016 to $3.1 billion in Q12019.

As for the stock market, it has been highly volatile this year, but Salesforce is still up. Starting the year at $102.41, it was sitting at $124.06 as of publication, after peaking on October 1 at $159.86. The market has been on a wild ride since then and cloud stocks have taken a big hit, warranted or not. On one particularly bad day last month, Salesforce had its worst day since 2016 losing 8.7 percent in value,

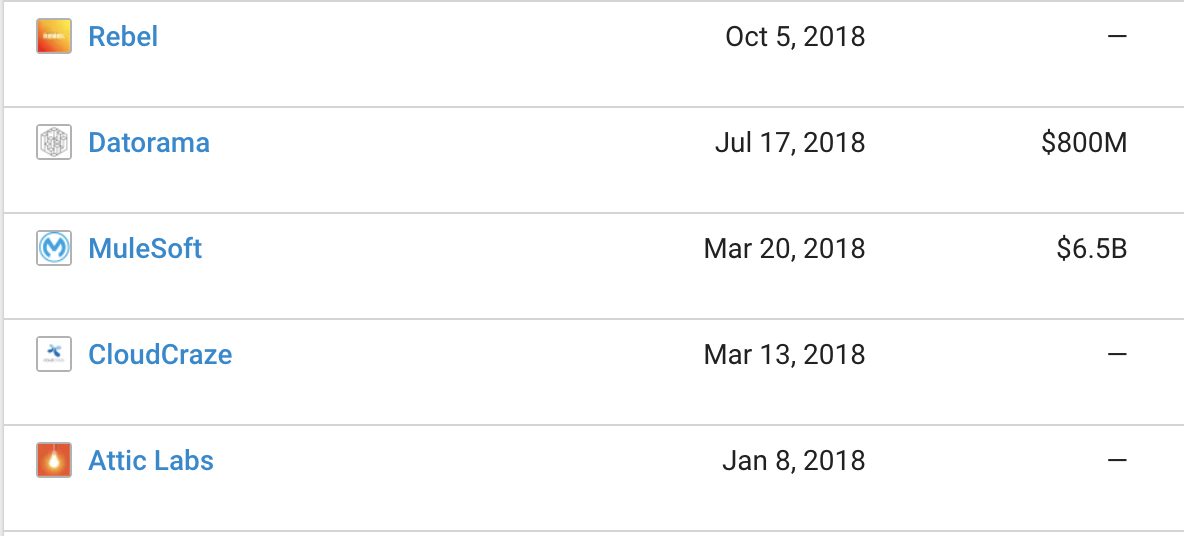

When you make a lot of money you can afford to spend generously, and the company invested some of those big bucks when it bought Mulesoft for $6.5 billion in March, making it the most expensive acquisition it has ever made. With Mulesoft, the company had a missing link between data sitting on-prem in private data centers and Salesforce data in the cloud.

Mulesoft helps customers build access to data wherever it lives via APIs. That includes legacy data sitting in ancient data repositories. As Salesforce turns its eyes toward artificial intelligence and machine learning, it requires oodles of data and Mulesoft was worth opening up the wallet to provide the company with that kind of access to a variety of enterprise data.

Salesforce 2018 acquisitions. Chart: Crunchbase.

But Mulesoft wasn’t the only thing Salesforce bought this year. It made five acquisitions in all. The other significant one came in July when it scooped up Dataorama for a cool $800 million, giving it a market intelligence platform.

What could be on board for 2019? If Salesforce sticks to its recent pattern of spending big one year, then regrouping the next, 2019 could be a slower one for acquisitions. Consider that it bought just one company last year after buying a dozen in 2016.

One other way to keep revenue rolling in comes from high-profile partnerships. In the past, Salesforce has partnered with Microsoft and Google, and this year it announced that it was teaming up with Apple. Salesforce also announced another high-profile arrangement with AWS to share data between the two platforms more easily. The hope with these types of cross pollination is that the companies can both increase their business. For Salesforce, that means using these partnerships as a platform to move the revenue needle faster.

Even while his company has made big bucks, Benioff has been preaching compassionate capitalism using Twitter and the media as his soap box.

He went on record throughout this year supporting Prop C, a referendum question designed to help battle San Francisco’s massive homeless problem by taxing companies with greater than $50 million in revenue — companies like Salesforce. Benioff was a vocal proponent of the idea, and it won. He did not find kindred spirits among some of his fellow San Francisco tech CEOs, openly debating Twitter CEO Jack Dorsey on Twitter.

Speaking about Prop C in an interview with Kara Swisher of Recode in November, Benioff talked in lofty terms about why he believed in the measure even though it would cost his company money.

“You’ve got to really be mindful and think about what it is that you want your company to be for and what you’re doing with your business and here at Salesforce, that’s very important to us,” he told Swisher in the interview.

He also talked about how employees at other tech companies were driving their CEOs to change their tune around social issues, including supporting Prop C, but Benioff had to deal with his own internal insurrection this year when 650 employees signed a petition asking him to rethink Salesforce’s contract with the U.S. Customs and Border Protection (CBP) in light of the current administration’s border policies. Benioff defended the contract, stating that that Salesforce tools were being used internally at CBP for staff recruiting and communication and not to enforce border policy.

Regardless, Salesforce has never lost its focus on meeting lofty revenue goals, and as we approach the new year, there is no reason to think that will change. The company will continue to look for new ways to expand markets and keep their revenue moving ever closer to that $20 billion goal, even as it continues to meld its unique form of compassion and capitalism.

Powered by WPeMatico

Earlier this year, Rebecca Liebman impressed a panel of high-profile investors, including Ashton Kutcher and Salesforce chief executive Marc Benioff, at a SXSW pitch competition. She won and Benioff wrote her a check for $200,000 on the spot.

Today, she’s announcing that her educational fintech startup LearnLux has closed a $2 million seed round from Kutcher’s investment firm Sound Ventures, Benioff, Underscore VC and former Wealthfront CEO Adam Nash. LearnLux operates under a SaaS model, partnering with businesses to offer access to its digital financial wellness product, which helps employees make important financial decisions.

The Boston-based startup was founded by Liebman, 25, and her brother, Michael Liebman, 22, in 2015.

“He was coding from his dorm room when we were first building the product,” Rebecca said. “We’ve had a really interesting experience from a young age. I was working at a lab at MIT with brilliant Ph.D. students and no one could figure out how to open a retirement account. Michael was working at a bank with people who studied finance who still couldn’t figure out how to open a retirement account.” LearnLux provides interactive learning tools and educational content created in-house to guide workers through their 401k, health savings accounts or stock options, for example. Rebecca says they’ve signed on 10 customers since launching in September.

LearnLux provides interactive learning tools and educational content created in-house to guide workers through their 401k, health savings accounts or stock options, for example. Rebecca says they’ve signed on 10 customers since launching in September.

“There are all these financial decisions you have to make and we allow you to have an interactive experience online where you can play out what those decisions will look like,” she said.

“Finance has been made to confuse people. We had to figure out how to break it down and explain it in a way that makes sense … Whatever kind of learner you are, you will understand more about your financial decisions with [LearnLux.]”

Powered by WPeMatico

StockX started as a marketplace for reselling sneakers but has since grown to be much more, bringing its transparent and anonymous marketplace to more verticals. Today the company is announcing a $44 million Series B that will help fuel international and domestic growth while letting the company expand to even more product categories and perhaps opening StockX stores.

The idea driving StockX is simple: Provide a marketplace with fair pricing and ensure the merchandise is authentic. The result scales to nearly day-trading in consumer goods in the same vein as oil futures. In some cases, the seller never touches the product. Sneakers and other in-demand products are priced and sold at rates set by the market rather than the seller. If a particular sneaker is in demand, the price increases.

StockX is among the fastest growing startups in Detroit and Michigan and currently employs 300 in Detroit and 50 in Tempe, Arizona. Founded in 2016 by CEO Josh Luber, COO Greg Schwartz and Dan Gilbert, founder and chairman of Quick Loans, the company has scaled to see more than $2 million in daily transactions and 800,000 users have sold or purchased items on StockX. Today, at an event in Detroit, Luber told the audience that the company is approaching a billion dollar run-rate.

The company has never been capital contrasted and CEO and co-founder Josh Luber told TechCrunch that the company never thought they would have to turn to institutional financing. That’s the comfort of having a billionaire like Gilbert as a co-founder; Luber said Gilbert was always happy to fund StockX.

“We didn’t need money,” Luber told TechCrunch the day before this announcement, adding. “It was really about having external people that that we thought added truly different values than we had around the table.”

Right now the company’s main marketplace centers around sneakers but StockX is built around a platform that works for most ecommerce. It’s a $5 billion market worldwide. Last year the company also launched marketplaces for streetwear, handbags and watches — all verticals with a strong demand in the secondary market.

Scaling the service requires more bodies. Since everything sold on StockX is authenticated — in person — it takes more hands to authenticate more items. With that comes more customer service employees and as the company grows, StockX will need more engineers.

The company is already growing fast but Luber seems ready to double down. In March StockX had 130 people. Today, it’s at 415. He thinks. He confesses it could be a slightly more.

“We have about 50 engineers today and I would quadruple that tomorrow if I could,” he said. “We have about 50 customer service people today. I think it would be safe to double that tomorrow just because the business is growing so fast and we obviously hope it continues to grow as we scale.”

If StockX is going to scale, it needs more employees to ensure the company’s core ethos does not soften. The new round of funding will go far in bringing in the people Luber is seeking including additional members of the C-suite. StockX is running without a CTO, CMO, or CFO — pretty much the entire leadership suite, Luber admits.

It seems this is part of the reasoning behind the funding. The company was not seeking funding but, as Luber tells it, as the company gained attention, investors increasing reached out requesting meetings. Of the meetings they took, there were two firms that meshed with Luber’s vision of growing a marketplace.

The new round of funding comes from GV and Battery Ventures including several high-profile investors including DJ Steve Aoki; model and entrepreneur, Karlie Kloss; streetwear designer Don C; Salesforce founder chairman and co-CEO, Marc Benioff; Bob Mylod, founder and managing partner of Annox Capital; Shana Fisher, managing partner at Third Kind Venture Capital; and Jonathon Triest, managing partner of Ludlow Ventures — only Mylod and Triest are based in the Detroit area.

StockX says it intends to use the funding to expand internationally. Right now StockX only advertises in the US and only supports purchases in U.S. dollars. Going forward it intends to open up local versions of StockX to better support key markets with support for local currency, language and marketing. The company could also open location operations to make shipping and receiving easier and faster.

“In some of these countries, we have, a pretty decent customer base where people are tendered on a VPN,” Luber said. “There are pictures of people that walk around China with a StockX tag hanging off their shoe.”

Fifteen percent of StockX sales currently come from international buyers.

Of the four product categories StockX current sells, sneakers and streetwear make up the bulk of the sales. Before expanding to different verticals, Luber tells me there’s a lot of room for growth in each of the current categories but expanding means more employees.

For instance, each streetwear brand is essentially a sub-vertical, he says, adding that if the company launches a new brand StockX has to assemble a staff around it with brand expertise to build the catalog and product authentication process.

StockX is not ready to announce what other type of products it might sell. Street art seems like one they’re exploring.

Despite the growth, Luber remains committed to Detroit. He said the company will always be headquartered in Detroit and was proud to point to the fact that StockX was the second largest tenant in Dan Gilbert’s marquee Detroit building, One Campus Martius. The company also operates a 30,000 square foot facility in Detroit’s Corktown neighborhood.

StockX could come to other cities though, Luber says. The company is talking about what a StockX “in-real-life” experience would look like: It could be retail, a brand experience, accepting products to be sold or additional operation centers. The company is exploring all the obvious candidates including LA, NYC, San Francisco and Portland.

Powered by WPeMatico

In tech circles, it would be easy to assume that the world of high-impact charitable giving is a rich man’s game where deals are inked at exclusive black tie galas over fancy hors d’oeuvre. Both Mark Zuckerberg and Marc Benioff have donated to SF hospitals that now bear their names. Gordon Moore has given away $5B – including $600M to Caltech – which was the largest donation to a university at the time. And of course, Bill Gates has already donated $27B to every cause imaginable (and co-founded The Giving Pledge, a consortium of billionaires pledging to donate most of their net worth to charity by the end of their lifetime.)

For Bill, that means he has about $90B left to give.

For the average working American, this world of concierge giving is out of reach, both in check size, and the army of consultants, lawyers and PR strategists that come with it. It seems that in order to do good, you must first do well. Very well.

Bright Funds is looking to change that. Founded in 2012, this SF-based startup is looking to democratize concierge giving to every individual so they “can give with the same effectiveness as Bill and Melinda Gates.” They are doing to philanthropy what Vanguard and Wealthfront have done for asset management for retail investors.

In particular, they are looking to unlock dollars from the underutilized corporate benefit of matching funds for donations, which according to Bright Funds is offered by over 60% of medium to large enterprises, but only used by 13% of employees at these companies. The need for such a service is clear — these programs are cumbersome, transactional, and often offline. Make a donation, submit a receipt, and wait for it to churn through the bureaucratic machine of accounting and finance before matching funds show up weeks later.

Bright Funds is looking to make your company’s matching funds benefit as accessible and important to you as your free lunches or massages. Plus, Bright Funds charges companies per seat, along with a transaction fee to cover the cost of payment processing, sparing employees any expense.

It’s a model that is working. According to Bright Fund’s CEO Ty Walrod, Bright Funds customers see on average a 40% year-over-year increase in funds donated through the platform. More importantly, Bright Funds not only transforms an employee’s relationship to personal philanthropy, but also to the company they work for.

This model of bottoms-up giving is a welcome change from the big foundation model which has recently been rocked by scandal. The Silicon Valley Community Foundation was the go-to foundation for The Who’s Who of Silicon Valley elite. It rode the latest tech boom to become the largest community foundation in eleven short years with generous stock donations from donors like Mark Zuckerberg ($1.8 billion), GoPro’s Nicholas Woodman ($500 million), and WhatsApp co-founder Jan Koum ($566 million). Today, at $13.5 billion, it surpasses the 80+ year old Ford Foundation in endowment size.

However, earlier this year, their star fundraiser Mari Ellen Loijens (credited with raising $8.3B of the $13.5B) was accused of repeatedly bullying and sexually harassing coworkers, allegations that the Foundation had “known about for years” but failed to act upon. In 2017, a similar case occurred when USC’s star fundraiser David Carrera stepped down on charges of sexual harassment after leading the university’s historic $6 billion fundraising campaign.

While large foundations and endowments do important work, their structure relies too much on whale hunting for big checks, giving an inordinate amount of power to the hands of a small group of talented fund raisers.

This stands in contrast to Bright Funds’ ethos — to lead a grassroots movement in empowering individual employees to make their dollar of giving count.

Bright Funds is the latest iteration of a lineup of workplace giving platforms. MicroEdge and Cybergrants paved the way in the 80s and 90s by digitizing the giving experience, but was mainly on-premise, and lacked a focus on user experience. Benevity and YourCause arrived in 2007 to bring workplace giving to the cloud, but they were still not turnkey solutions that could be easily implemented.

Bright Funds started as a consumer platform, and has retained that heritage in its approach to product design, aiming to reduce friction for both employee and company adoption. This is why many of their first customers were midsized tech startups with limited resources and looking for a turnkey solution, including Eventbrite, Box, Github, and Contently . They are now finding their way upmarket into larger, more established enterprises like Cisco, VMWare, Campbell’s Soup Company, and Sunpower.

Bright Funds approach to product has brought a number of innovations to this space.

The first is the concept of a cause-focused “fund.” Similar to a mutual fund or ETF, these funds are portfolios of nonprofits curated by subject-matter experts tailored to a specific cause area (e.g. conservation, education, poverty, etc.). This solves one of the chief concerns of any donor — is my dollar being put to good use towards the causes I care about? Passionate about conservation? Invest with Jim Leape from the Stanford Woods Institute for the Environment, who brings over three decades of conservation experience in choosing the six nonprofits in Bright Fund’s conservation portfolio. This same expertise is available across a number of cause areas.

Additionally, funds can also be created by companies or employees. This has proven to be an important rallying point for emergency relief during natural disasters, where employees at companies can collectively assemble a list of nonprofits to donate to. In 2017, Cisco employees donated $1.8 million (including company matching) through Bright Funds to Hurricanes Harvey, Maria, and Irma as well as the central Mexico earthquakes, the current flooding in India and many more.

The second key feature of their product is the impact timeline, a central news feed to understand where your dollars are going across all your cause areas. This transforms giving from a black box transaction to an ongoing dialogue between you and your charities.

Lastly, Bright Funds wants to take away all the administrative burden that might come with giving and volunteering — everything from tracking your volunteer opportunities and hours, to one-click tax reporting across all your charitable donations. In short, no more shoeboxes of receipts to process through in April.

Although Bright Funds is focused on transforming the individual giving experience, it’s paying customer at the end of the day is the enterprise.

And although it is philanthropic in nature, Bright Funds is not exempt from the procurement gauntlet that every enterprise software startup faces — what’s in it for the customer? What impact does workplace giving and volunteering have on culture and the bottom line?

To this end, there is evidence to show that corporate social responsibility has a an impact on recruiting the next generation of workers. A study by Horizon Media found that 81% of millennials expect their companies to be good corporate citizens. A separate 2015 study found that 62% of millennials said they’d take a pay cut to work for a company that’s socially responsible.

Box, one of Bright Fund’s early customers, has seen this impact on recruiting firsthand (disclosure: Box is one of my former employers). Like most tech companies competing for talent in the Valley, Box used to give out lucrative bonuses for candidate referrals. They recently switched to giving out $500 in Bright Funds gift credit. Instead of seeing employee referrals dip, Box saw referrals “skyrocket,” according to Box.org Executive Director Bryan Breckenridge. This program has now become “one of the most cherished cultural traditions at Box,” he said.

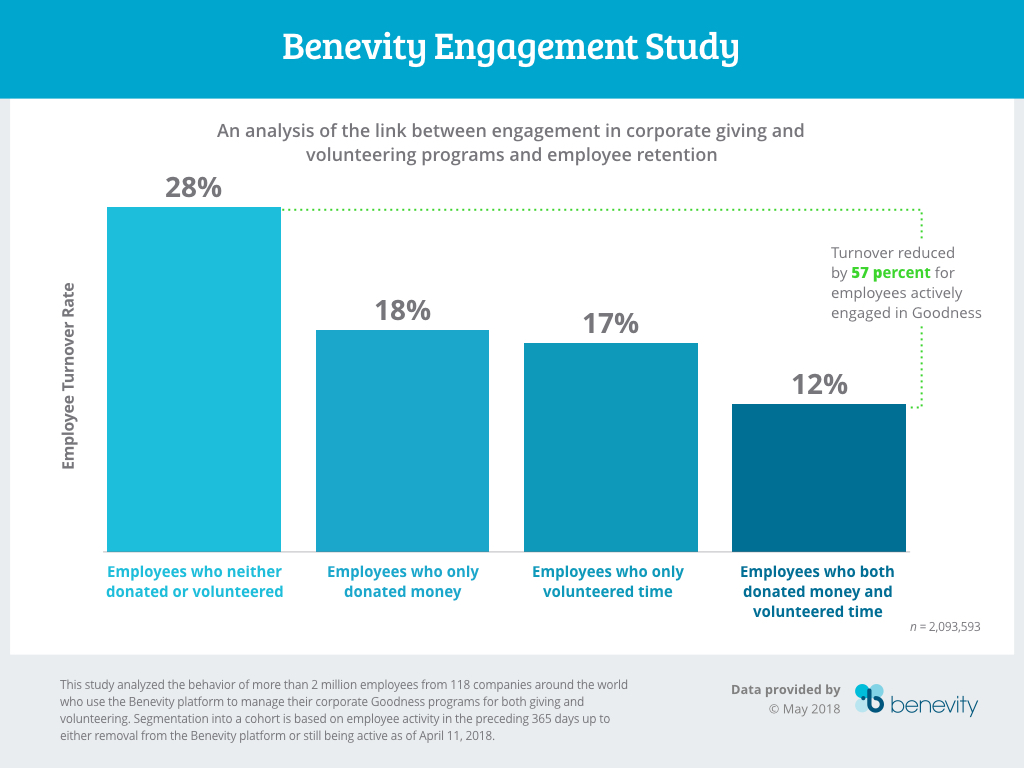

Additionally, like any corporate benefit, there should be metrics tied to employee retention. Benevity released a study of 2 million employees across 118 companies on their platform that showed a 57% reduction in turnover for employees engaged in corporate giving or volunteering efforts. VMware, one of Bright Fund’s customers, has seen an astonishing 82% of their 22,000 employees participate in their Citizen Philanthropy program of giving and volunteering, according to VMware Foundation Director Jessa Chin. Their full-time voluntary turnover rate (8%) is well below the software industry average of 13.2%.

Bright Funds still has a lot of work to do. CEO Walrod says that one of his top priorities is to expand the platform beyond US charities, finding ways to evaluate and incorporate international nonprofits.

They have also not given up their dream of becoming a truly consumer platform, perhaps one day competing in the world of donor-advised funds, which today is largely dominated by big names like Fidelity and Schwab who house over $85B of assets. In the short term, Walrod wants to make every Bright Funds account similar to a 401K account. It goes wherever you work, and is a lasting record of the causes you care about, and the time and resources you’ve invested in them.

Whether the impetus is altruism around giving or something more utilitarian like retention, companies are increasingly realizing that their employees represent a charitable force that can be harnessed for the greater good. Bright Funds has more work to do like any startup, but it is empowering the next set of donors who can give with the same effectiveness as Gates, and one day, at the same scale as him as well.

Powered by WPeMatico

Zuroa’s founder and CEO Tien Tzuo had a vision of a subscription economy long before most people ever considered the notion. He knew that for companies to succeed with subscriptions, they needed a bookkeeping system that understood how they collected and reported money. The company went public yesterday, another clear sign post on the road to SaaS maturation.

Tzuo was an early employee at Salesforce and their first CMO. He worked there in the early days in the late 90s when Salesforce’s Marc Benioff famously rented an apartment to launch the company. Tzuo was at Salesforce 9 years, and it helped him understand the nature of subscription-based businesses like Salesforce.

“We created a great environment for building, marketing and delivering software. We rewrote the rules, the way it was built, marketed and sold,” Tzuo told me in an interview in 2016.

He saw a fundamental problem with traditional accounting methods, which were designed for selling a widget and declaring the revenue. A subscription was an entirely different model and it required a new way to track revenue and communicate with customers. Tzuo took the long view when he started his company in early 2007, leaving a secure job at a growing company like Salesforce.

He did it because he had the vision, long before anyone else, that SaaS companies would require a subscription bookkeeping system, but before long, so would other unrelated businesses.

As he put it in that 2016 interview, if you commit to pay me $1 for 10 years, you know that $1 was coming in come hell or high water, that’s $10 I know I’m getting, but I can’t declare the money until I get it. That recurring revenue still has value though because my investors know that I’m secure for 10 years, even though it’s not on the books yet. That’s where Zuora came in. It could account for that recurring revenue when nobody else could. What’s more, it could track the billing over time, and send out reminders, help the companies stay engaged with their customers.

Photo: Lukas Kurka/Getty Images

As Ray Wang, founder and principal analyst at Constellation Research put it, they pioneered the whole idea of a subscription economy, and not just for SaaS companies. Over the last several years, we’ve heard companies talking about selling services and SLAs (service/uptime agreements) instead of a one-time sale of an item, but not that long ago it wasn’t something a lot of companies were thinking about.

“They pioneered how companies can think about monetization,” Wang said. “So large companies like a GE could go from selling a wind turbine one time to selling a subscription to deliver a certain number of Kw/hr of green energy at peak hours from 1 to 5 pm with 98 percent uptime.” There wasn’t any way to do this before Zuora came along.

Jason Lemkin, founder at SaaStr, a firm that invests in SaaS startups, says Tzuo was a genuine visionary and helped create the underlying system for SaaS subscriptions to work. “The most interesting part of Zuora is that it is a “second” order SaaS play. It could only thrive once SaaS became mainstream, and could only scale on top of other recurring revenue businesses. Zuora started off as a niche player helping SaaS companies do billing, and it dramatically expanded and thrived as SaaS became … Software.”

When he launched the company in 2007, perhaps he saw that extension of his idea out on the distant horizon. He certainly saw companies like Salesforce needing a service like the one he had decided to create. The early investors must have recognized that his vision was early and it would take a slow, steady climb on the way to exiting. It took 11 years and $242 million in venture capital before they saw the payoff. The revenue after 11 years was a reported $167 million. There is plenty of room to grow.

But yesterday the company had its initial public offering, and it was by any measure a huge success. According TechCrunch’s Katie Roof, “After pricing its IPO at $14 and raising $154 million, the company closed at $20, valuing the company around $2 billion.” Today it was up a bit more as of this writing.

When you consider the Tzuo’s former company has become a $10 billion company, that companies like Box, Zendesk, Workday and Dropbox have all gone public, and others like DocuSign and Smartsheet are not far behind, it’s pretty clear that we are in a golden age of SaaS — and chances are it’s only going to get better.

Powered by WPeMatico

In an interview last month with Julie Bort from Business Insider, Parker Harris and Marc Benioff told the story of how when they first launched the company, they were trying to raise money and nobody would give them a dime. Benioff said he went to every venture capital in Silicon Valley — and was turned down every single time.

This could be a lesson for every startup out there with a vision, who is not able to find conventional financing for your idea. Salesforce found the money, but it took one on one fundraising, rather than the traditional VC route.

The company famously launched in an apartment that Benioff rented, and he put up some of his own money to buy the company’s first computers. Then it was time to go downtown and ask the VCs for money and it did not go well.

“I had to go hat in hand, like I was a high tech beggar, down to Silicon Valley to raise some money…And as I go from venture capitalist to venture capitalist to venture capitalist — and a lot of them are my friends, people I’ve gone to lunch with — and each and every one of them said no,” Benioff said. “Salesforce was never able to raise a single dollar from a venture capitalist,” he added.

He suggested there were a lot of reasons for that including competitors who would call after his meetings and deliberately sabotage him or people who simply didn’t believe in the cloud as a vision of the future of software.

Whatever the reasons, Salesforce was eventually able to raise over $60 million from private individual investors, before going public in 2004. In the context of today’s venture capital environment, it is pretty tough to imagine a guy like Benioff not finding one taker, especially when you consider that he was not exactly an unknown quantity. And still no one would write him a check.

But this wasn’t now. It was in the late 1990s when nobody was thinking about cloud computing and the notion of software on the internet was a distant idea. Benioff was imagining something completely different and not one firm had the vision to see what was coming. Today, Salesforce is a $10 billion company and those folks that turned him down have to be wondering what they were thinking.

“When you start something like Salesforce, you want to surround yourself with people who do believe in you, who do believe you’re going to be successful because you’re going to have a whole bunch of people who are going to tell you that you’re not, Benioff said.

That’s something every entrepreneur should remember.

Powered by WPeMatico

Salesforce has always been a company that is looking ahead to the next big technology, whether that was mobile, social, internet of things or artificial intelligence. In an interview with Business Insider’s Julie Bort at the end of March, Salesforce co-founders Marc Benioff and Parker Harris talked about a range of subjects including how the company came to be working on one of the next hot technologies, a blockchain product.

Benioff told a story of being at the World Economic Forum in Switzerland where a bit of serendipity led him to start thinking about blockchain and how it could be used as part of the Salesforce family of products.

As it turned out, there was a crypto conference going on at the same time as the WEF and the two worlds collided at a Salesforce event at the Intercontinental Hotel. While there, one of the crypto conference attendees engaged Benioff in a conversation and it was the start of something.

“I had been thinking a lot about what is Salesforce’s strategy around blockchain, and what is Salesforce’s strategies around cryptocurrencies and how will we relate to all of these things,” Benioff said. He is actually a big believer in the power of serendipity, and he said just by having that conversation, it started him down the road to thinking more seriously about Salesforce’s role in this developing technology.

He said the more he thought about it, the more he believed that Salesforce could make use of Blockchain. Then suddenly something clicked for him and he saw a way to put blockchain and cryptocurrencies to work in Salesforce. “That’s kind of how it works and I hope by Dreamforce we will have a blockchain and cryptocurrency solution.”

Benioff is clearly a visionary and says a lot of that comes from simply paying attention as he did when he talked to this person in Davos, and recognizing an opportunity to expand Salesforce in a meaningful way. “A lot [these ideas] comes from paying attention, listening. There’s new ideas coming all the time,” he said. He recognizes that there are more ideas out there than they can possibly execute, but part of his job is understanding which ones are the most important for Salesforce customers.

Blockchain is the electronic ledger used to track Bitcoin or other digital currencies, but it also has a more general business role. As an irrefutable and immutable record, it can track just about anything of value.

Dreamforce is Salesforce’s enormous annual customer conference. It will be held this year from September 25-28 in San Francisco, and if it all works as planned, they could be announcing a blockchain product this year.

__

Check out the whole interview between Salesforce founders Parker Harris and Marc Benioff and Julie Bort from Business Insider:

Powered by WPeMatico