M&A

Auto Added by WPeMatico

Auto Added by WPeMatico

In the world of robotic startups, acquisition is often as good an outcome as any. And when it comes to robotic tractor startups, you could do worse than being acquired by John Deere. The agricultural technology giant announced today that it’s set to acquire Bear Flag Robotics for $250 million.

The Bay Area-based firm, which specializes in autonomous farming heavy machinery, was founded in 2017. They first crossed our radar the following year, as a member of YC’s Winter 2018 cohort.

“We got a tour of an orchard and just how pronounced the labor problem is,” co-founder Aubrey Donnellan told TechCrunch at the time. “They’re struggling to fill seats on tractors. We talked to other growers in California. We kept hearing the same thing over and over: Labor is one of the most significant pain points. It’s really hard to find quality labor. The workforce is aging out. They’re leaving the country and going into other industries.”

In the intervening years, John Deere tapped Bear Flag for its own Startup Collaborator initiative. And the robotics firm has also begun to deploy its technology to an undisclosed (“limited,” per their wording) number of sites in the U.S.

“One of the biggest challenges farmers face today is the availability of skilled labor to execute time-sensitive operations that impact farming outcomes. Autonomy offers a safe and productive alternative to address that challenge head on,” co-founder and CEO Igino Cafiero, says in a release. “Bear Flag’s mission to increase global food production and reduce the cost of growing food through machine automation is aligned with Deere’s and we’re excited to join the Deere team to bring autonomy to more farms.”

Agricultural is one of several robotics categories that have seen a spike in interest in the past year, due to labor shortages that predate but were exacerbated by the global pandemic. Of course, that interest doesn’t make anyone immune from the difficulties of launching a robotics startup.

Last month, apple-picking robotics firm Abundant confirmed it was closing up shop, noting, “After a series of promising commercial trials with prototype apple harvesters, the company was unable to raise enough investment funding to continue development and launch a production system,” the company noted at the time.

An acquisition seems like a reasonable outcome for a company like Bear Flag. The startup gains a lot of resources from its massive new owner, and its new owner adds some new tech to its portfolio. Indeed, John Deere has been pretty aggressively looking to expand into more cutting-edge technologies like robotics and drones in recent years.

Bear Flag will retain operations in the Bay Area.

Powered by WPeMatico

Marvell announced this morning it has reached an agreement to acquire Innovium for $1.1 billion in an all-stock deal. The startup, which raised over $400 million according to Crunchbase data, makes networking ethernet switches optimized for the cloud.

Marvell president and CEO Matt Murphy sees Innovium as a complementary piece to the $10 billion Inphi acquisition last year, giving the company, which makes copper-based chips, more ways to work across modern cloud data centers.

“Innovium has established itself as a strong cloud data center merchant switch silicon provider with a proven platform, and we look forward to working with their talented team who have a strong track record in the industry for delivering multiple generations of highly successful products,” Marvell CEO Matt Murphy said in a statement.

Innovium founder and CEO Rajiv Khemani, who will remain as an advisor post-close, told a familiar tale from a startup CEO being acquired, seeing the sale as a way to accelerate more quickly as part of a larger organization than it could on its own. “As we engaged with Marvell, it became clear that our data center optimized portfolio combined with Marvell’s scale, leading technology platform and complementary portfolio, can accelerate our growth and vision of delivering breakthrough switch silicon for the cloud and edge,” he wrote in a company blog post announcing the deal.

The company, which was founded in 2014, raised more than $143 million last year on a post-money valuation of $1.3 billion, according to PitchBook data. The question is, was this a reasonable deal for the company given that valuation?

No company wants to sell for less than it was last valued by its investors. In some cases, such deals can still be accretive for early backers of the selling concern, but not always. In this case TechCrunch is not privy to all the details of the Innovium cap table and what its later investors may have built into their deals with the company in the form of downside protection; such measures can tilt the value of the sale of a company more toward its later and final investors. This is usually managed at the expense of its earlier backers and employees.

Still, the Innovium deal should not be seen as a failure. Building a company that sells for north of $1 billion in equity value is impressive. The deal appears to be slightly smaller in enterprise value terms. In the business world, enterprise value is a useful method of valuing the true cost of an acquisition. In the case of Innovium, a large cash position, what was described as “Innovium cash and exercise proceeds expected at closing of approximately $145 million,” lowered the cost of the transaction to a more modest $955 million in net outlays.

Our general perspective is that the sale is probably not the outcome that Innovium’s backers had hoped for, but that it may still prove lucrative to early workers and early investors, and still works at that lower figure. It’s also notable how in today’s market of mega-rounds and surfeit unicorns, an exit north of the $1 billion mark in equity terms can be viewed as a disappointment in any terms. Innovium is selling for around the price that Facebook paid for Instagram in 2012, a deal that at the time was so large that it dominated technology headlines around the world.

But with so much capital available today, private valuations are soaring and mega deals abound. And recent rounds north of $100 million, much like Innovium’s 2020-era, $143 million round, can set companies up with rich valuations and a narrow path in front of them to beat those heightened expectations.

What likely happened? Perhaps Innovium found itself with more cash than opportunities to spend it; perhaps it simply needed a large partner to help it better sell into its market. With expected revenues of $150 million in Marvell’s fiscal 2023, its next fiscal period, Innovium did not fail to reach scale. It may have simply grown well as a private, independent company, and stalled out after its last round.

Regardless, a billion-dollar exit is a billion-dollar exit. The deal is expected to close by the end of this year. While both company boards have approved the deal, it still must clear regular closing hurdles, including approval by Innovium’s private stock holders.

Powered by WPeMatico

Over the last couple of years, robotic process automation or RPA has been red hot with tons of investor activity and M&A from companies like SAP, IBM and ServiceNow. UIPath had a major IPO in April and has a market cap over $30 billion. I wondered when Salesforce would get involved and today the company dipped its toe into the RPA pool, announcing its intent to buy German RPA company Servicetrace.

Salesforce intends to make Servicetrace part of Mulesoft, the company it bought in 2018 for $6.5 billion. The companies aren’t divulging the purchase price, suggesting it’s a much smaller deal. When Servicetrace is in the fold, it should fit in well with Mulesoft’s API integration, helping to add an automation layer to Mulesoft’s tool kit.

“With the addition of Servicetrace, MuleSoft will be able to deliver a leading unified integration, API management and RPA platform, which will further enrich the Salesforce Customer 360 — empowering organizations to deliver connected experiences from anywhere. The new RPA capabilities will enhance Salesforce’s Einstein Automate solution, enabling end-to-end workflow automation across any system for service, sales, industries, and more,” Mulesoft CEO Brent Hayward wrote in a blog post announcing the deal.

While Einstein, Salesforce’s artificial intelligence layer, gives companies with more modern tooling the ability to automate certain tasks, RPA is suited to more legacy operations, and this acquisition could be another step in helping Salesforce bridge the gap between older on-prem tools and more modern cloud software.

Brent Leary, founder and principal analyst at CRM Essentials says that it brings another dimension to Salesforce’s digital transformation tools. “It didn’t take Salesforce long to move to the next acquisition after closing their biggest purchase with Slack. But automation of processes and workflows fueled by real-time data coming from a growing variety of sources is becoming a key to finding success with digital transformation. And this adds a critical piece to that puzzle for Salesforce/MuleSoft,” he said.

While it feels like Salesforce is joining the market late, in an investor survey we published in May, Laela Sturdy, general partner at CapitalG, told us that we are just skimming the surface so far when it comes to RPA’s potential.

“We’re a long way from needing to think about the space maturing. In fact, RPA adoption is still in its early infancy when you consider its immense potential. Most companies are only now just beginning to explore the numerous use cases that exist across industries. The more enterprises dip their toes into RPA, the more use cases they envision,” Sturdy responded in the survey.

Servicetrace was founded in 2004, long before the notion of RPA even existed. Neither Crunchbase nor PitchBook shows any money raised, but the website suggests a mature company with a rich product set. Customers include Fujitsu, Siemens, Merck and Deutsche Telekom.

Powered by WPeMatico

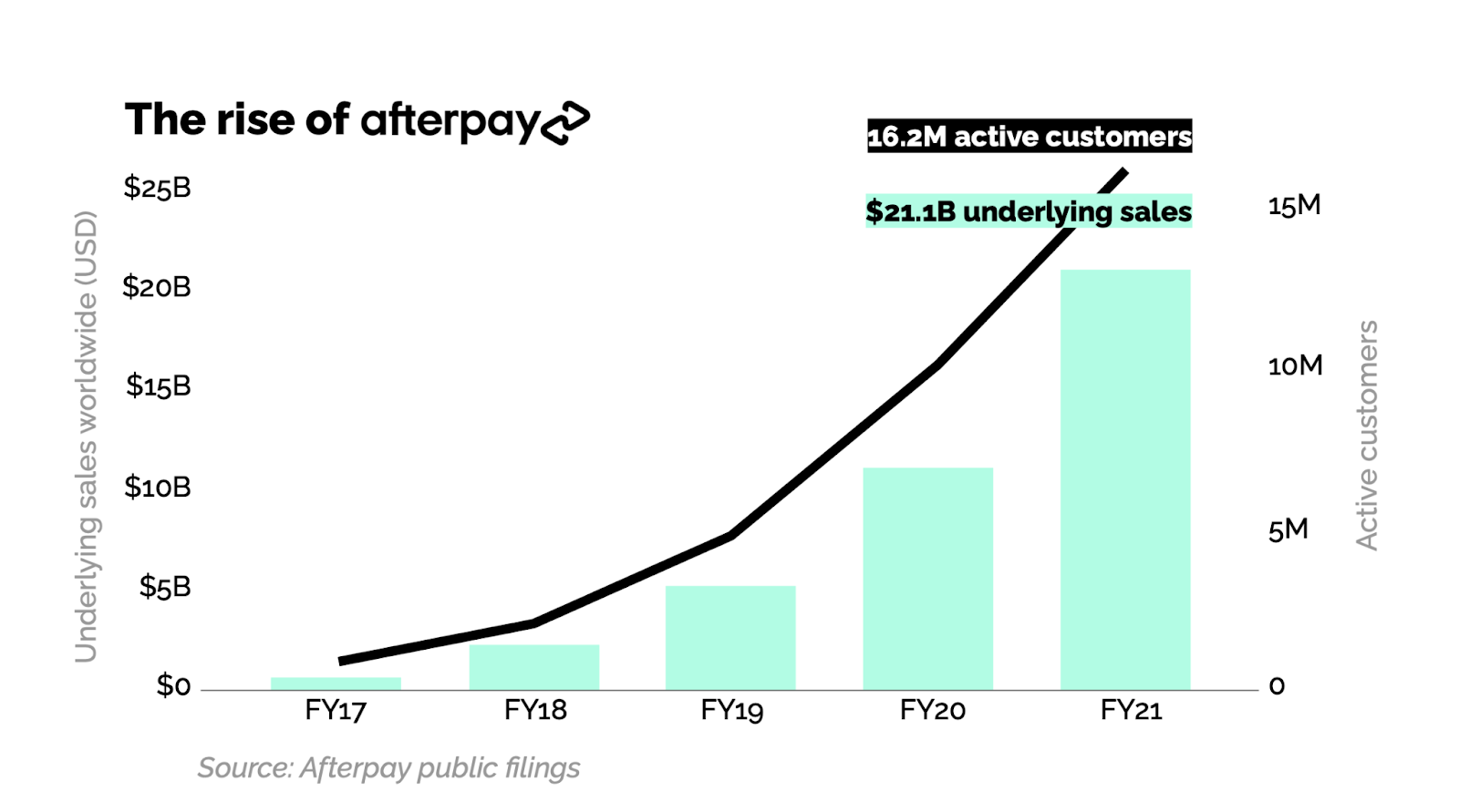

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

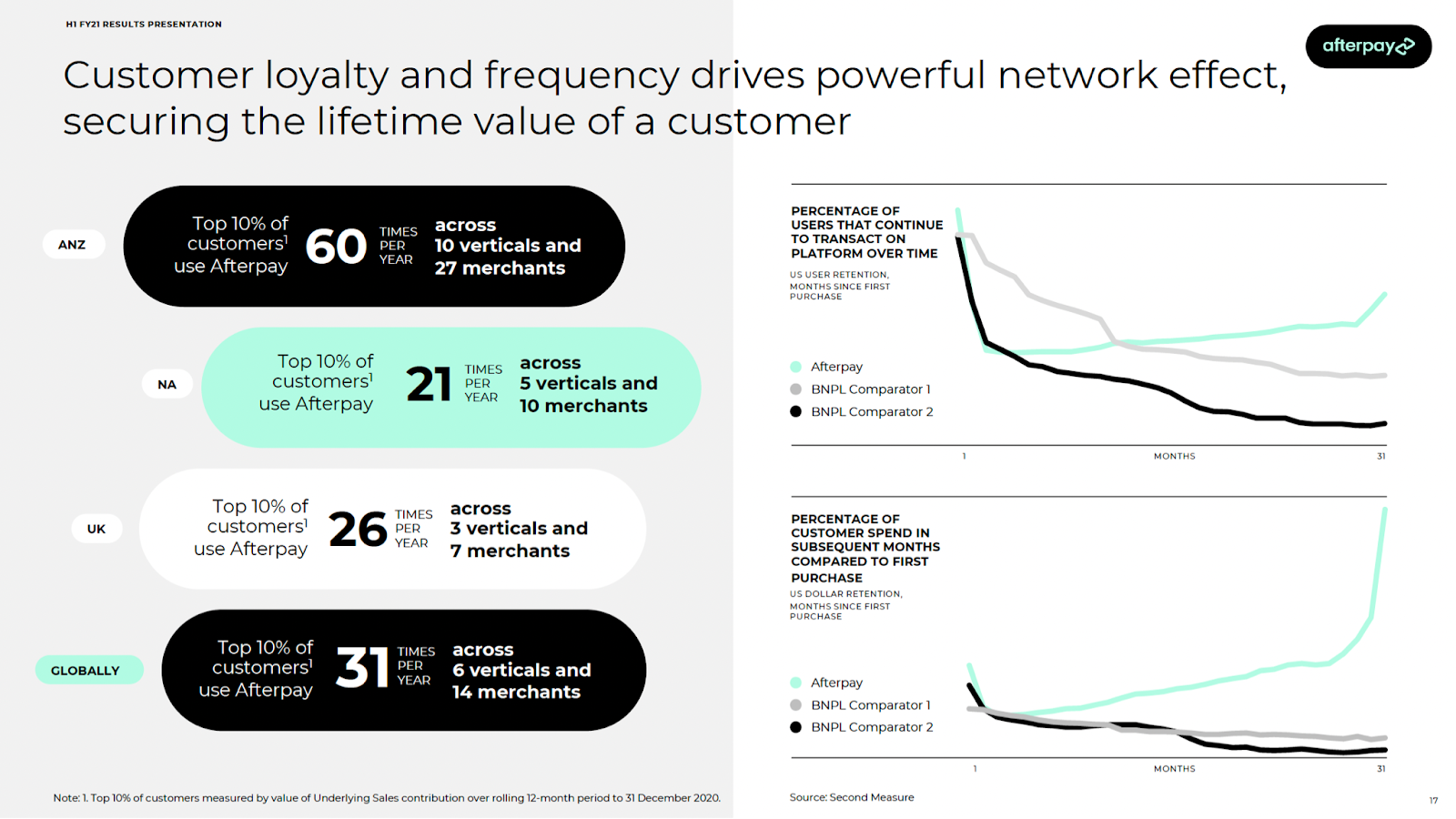

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Twitter’s recent acquisition spree continues today as the company announces it has acqui-hired the team from news aggregator and summary app Brief. The startup from former Google engineers launched last year to offer a subscription-based news summary app that aimed to tackle many of the problems with today’s news cycle, including information overload, burnout, media bias and algorithms that promoted engagement over news accuracy.

Twitter declined to share deal terms.

Before starting Brief, co-founder and CEO Nick Hobbs was a Google product manager who had worked on AR, Google Assistant, Google’s mobile app, and self-driving cars, among other things. Co-founder and CTO Andrea Huey, meanwhile, was a Google senior software engineer, who worked on the Google iOS app and had a prior stint at Microsoft.

Image Credits: Brief

While Brief’s ambitious project to fix news consumption showed a lot of promise, its growth may have been hampered by the subscription model it had adopted. The app required a $4.99 per month commitment, despite not having the brand-name draw of a more traditional news outlet. For comparison, The New York Times’ basic digital subscription is currently just $4 per week for the first year of service, thanks to a promotion.

Twitter says the startup’s team, which also includes two other Brief employees, will join Twitter’s Experience.org group where they’ll work on areas that support the public conversation on Twitter, including Twitter Spaces and Explore.

While Twitter wouldn’t get into specifics as to what those tasks may involve, the company did tell TechCrunch it hopes to leverage the founders’ expertise with Brief to build out and accelerate projects in both those areas.

Explore, of course, is Twitter’s “news” section, where top stories across categories are aggregated alongside trending topics. But what it currently lacks is a comprehensive approach to distilling the news down to the basic facts and presenting balance, as Brief’s app had offered. Instead, Twitter’s news items include a headline and a short description of the story, followed by notable tweets. There’s certainly room for improvement there.

It’s also possible to imagine some sort of news-focused product built into Twitter’s own subscription service, Twitter Blue — but that’s just speculation at this point.

Twitter says it proactively reached out to Brief with its offer. As part of its current M&A strategy, the company is on the hunt for acquiring talent that will complement its existing teams and help to accelerate its product developments.

Over the past year, Twitter has made similar acqui-hires, including those for distraction-free reading service Scroll, social podcasting app Breaker, social screen-sharing app Squad, and API integration platform Reshuffle. It also bought products, like newsletter platform Revue, which it directly integrated. The company even held acquisition talks with Clubhouse and India’s ShareChat, which would have been much larger M&A deals.

“We’re really glad we ended up at Twitter,” Hobbs told TechCrunch.

“Andrea and I founded Brief to build news that fostered a healthy discourse, and Twitter’s genuine commitment to improve the public conversation is deeply inspiring,” he said. “While we can’t discuss specifics on future plans, we’re confident our experience at Brief will help accelerate the many exciting things happening at Twitter today,” he added.

Hobbs said the team remains optimistic about the future of paid journalism, too, as Brief demonstrated that some customers would pay for a new and improved news experience.

“Brief pioneered a fresh vision for journalism, focused on getting you just the news you need rather than as much as you could withstand,” remarked Ilya Kirnos, founding partner and CTO at SignalFire, who backed Brief at the seed stage. “That respect for its readers made SignalFire proud to support founders Nick Hobbs and Andrea Huey, who are now bringing that philosophy to the top source of breaking news — Twitter.”

To date, Brief had raised a million in seed funding from SignalFire and handful of angel investors, including Sequoia Scouts like David Lieb, Maia Bittner and Matt Macinnis.

As a result of today’s deal, Brief will wind down its subscription app on July 31. The company says it will alert its current user base today via a notification about its forthcoming shutdown but the app will remain on the App Store offering new features that allow users to explore its archives.

Powered by WPeMatico

Despite the plentiful headlines about mega billion-dollar M&A transactions, record IPOs and the rapid growth of SPACs, small deals will continue to be the most likely exit for the vast majority of tech startups. In the over 30 years I’ve worked on M&A at White & Case, Barclays and my current firm Ascento Capital, I have seen too many startups that are not prepared for an exit via a merger or sale. This article will provide specific recommendations on how to prepare your startup for M&A.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Global M&A hit record highs in the second quarter with a total deal value of $1.5 trillion, but smaller transactions vastly outnumber mega billion-dollar deals. The U.S. saw a total of 16,672 deals in the year ended June 31, but only 583, or 3% of that number, were valued at more than a billion dollars (FactSet). The IPO market is healthy again, but M&A still represents 88% of exits: So far this year, there were 503 IPOs and 5,203 deals, according to the CB Insights Q2 2021 State of Venture Report. After the SEC announced in early April that it was considering new guidance on SPAC IPOs, the rate of new SPAC issuances fell by around 90%.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Here are a few recommendations that will prepare your startup for an M&A exit:

Set up an alert on Google News for M&A activity in your subsector. For example, if your startup is in the IoT subsector, search for “IoT acqui” and this will pick up news stories on acquisitions in the IoT space. Save the search so you can go to Google News on a regular basis. Also track your closest competitors on Google News, particularly to see who is selling their company.

Prepare a list of the companies or firms most likely to buy your startup. This list should include domestic and international companies, businesses in non-tech industries, private equity firms and their portfolio companies, as well as VC-backed companies. Track these likely acquirers on Google News as well.

Consider approaching the top 10 likely acquirers when you are raising the next round of capital. If your startup gets M&A offers and VC term sheets at the same time, this will provide your board of directors choices on the path ahead. Knowing the M&A activity in your startup’s subsector and the 10 most likely acquirers will impress VCs and increase the chances of being funded.

Powered by WPeMatico

New York-based startup Sketchfab has been acquired by Epic Games, the company behind Fortnite and Unreal Engine. Sketchfab has been building a platform to upload, download, view, share, sell and buy 3D assets. Essentially, it is the leading repository for 3D files on the web.

Epic Games isn’t disclosing the terms of the deal. Sketchfab will still operate as a separate brand and offering. Epic Games also says that all integrations with third-party tools will remain available, including with Unity.

The deal makes a ton of sense as Epic Games has been developing — and acquiring — some of the most popular creation tools. Unreal Engine has been one of the most popular video game engines of the past couple of decades.

More recently, Unreal Engine has been used for different use cases beyond video games, such as special effects, 3D explorations of virtual worlds, mixed reality projects and more.

But an engine without assets is pretty useless. That’s why creators either design their own 2D and 3D assets, outsource this process or buy assets directly. It led to the creation of an entire ecosystem of assets and creators.

Epic Games has its own Unreal Engine marketplace, but Sketchfab has been working on building the definitive 3D marketplace for many years with three important pillars — technology, reach and collaboration.

On the technology front, Sketchfab lets you view 3D models on any platform. The Sketchfab viewer works with all major browsers on both desktop and mobile — you can see an example on Sketchfab. It also works with VR headsets. You can upload 3D models from your favorite 3D modeling app, such as Blender, 3ds Max, Maya, Cinema 4D and Substance Painter.

Sketchfab can also convert any format into glTF and USDZ file formats. Those formats work particularly well on Android and iOS.

When it comes to reach, Sketchfab has grown tremendously over the years. In 2018, the company shared some metrics — 1 billion views, 2 million members and 3 million 3D models. Around the same time, the company launched a store so that creators can buy and sell assets directly on the platform.

Finally, Sketchfab launched an interesting feature for companies that work with 3D models all the time — Sketchfab for Teams. It’s a software-as-a-service play that lets you share a Sketchfab account with the rest of the team. Essentially, it works a bit like a shared Google Drive folder — but for 3D models.

With today’s acquisition, Epic Games is making some immediate changes. Starting today, store fees have been reduced from 30% to 12% — just like on the Epic Games Store. The company lowered commissions on ArtStation immediately after acquiring ArtStation, as well.

As for Sketchfab users paying a monthly subscription fee, everything is a bit cheaper now. All features in the Plus plan are now available for free, all features in the Pro plan are available to Plus subscribers, etc.

“We built Sketchfab with a mission to empower a new era of creativity and provide a service for creators to showcase their work online and make 3D content accessible,” Sketchfab co-founder and CEO Alban Denoyel said in the announcement. “Joining Epic will enable us to accelerate the development of Sketchfab and our powerful online toolset, all while providing an even greater experience for creators. We are proud to work alongside Epic to build the Metaverse and enable creators to take their work even further.”

With the acquisitions of ArtStation and Capturing Reality, Epic Games has been on an acquisition spree. It’s clear that the company wants to build an end-to-end developer suite for the gaming industry.

Powered by WPeMatico

When it comes to M&A in the chip world, the numbers are never small. In 2020, four deals involving chip companies totaled $106 billion, led by Nvidia snagging ARM for $40 billion. One surprise from last year’s chip-laced M&A frenzy was Intel remaining on the sidelines. That would change if a rumored $30 billion deal to buy chip manufacturing concern GlobalFoundries comes to fruition.

The rumor was first reported by The Wall Street Journal yesterday.

Patrick Moorhead, founder and principal analyst at Moor Insight & Strategies, who watches the chip industry closely, says that snagging GlobalFoundries would certainly make sense for Intel. The company is currently pursuing a new strategy to manufacture and sell chips for both Intel and to others under CEO Pat Gelsinger, who came on board in January to turn around the flagging chip maker.

“GlobalFoundries has technologies and processes that are specialized for 5G RF, IoT and automotive. Intel with GlobalFoundries would become what I call a ‘full-stack provider’ that could offer a customer everything. This is in full alignment with IDM 2.0 (Intel’s chip manufacturing strategy) and would get Intel there years before it could without GlobalFoundries,” Moorhead told TechCrunch.

It would also give Intel a chip manufacturing facility at a time when there are global chip shortages and huge demand for product from every corner, due in part to the pandemic and the impact it has had on the global supply chain. Intel has already indicated it has plans to spend more than $20 billion to build two fabs (chip manufacturing plants) in Arizona. Adding GlobalFoundries to these plans would give them a broad set of manufacturing capabilities in the coming years if it came to pass, but would also involve a significant investment of tens of billions of dollars to get there.

GlobalFoundries is a worldwide chip manufacturing concern based in the U.S. The company was spun off from Intel’s rival chip maker AMD in 2012, and is currently owned by Mubadala Investment Company, the investment arm of the government of Abu Dhabi.

Investors seem to like the idea of combining these two companies, with Intel stock up 1.59% as of publication. It’s important to note that this deal is still in the rumor stage and nothing is definitive or final yet. We will let you know if that changes.

Powered by WPeMatico

ZoomInfo announced this morning it intends to acquire conversational sales intelligence tool Chorus.ai for $575 million. Shares of ZoomInfo are unchanged in premarket trading following the news, per Yahoo Finance data.

Sales intelligence, Chorus’s market, is a hot space that uses AI to “listen” to sales conversations to help improve interactions between salespeople and customers. ZoomInfo is mostly known for providing information about customers, so the acquisition expands the acquiring company’s platform in a significant way.

The company sees an opportunity to bring together different parts of the sales process in a single platform by “combining ZoomInfo’s historic top-of-the-funnel strength with insights driven from the middle of the funnel in the customer conversations that Chorus captures,” it said in a release.

“With Chorus, the entire organization can make better decisions by surfacing insights and analytics that you would only get if you sat in on every sales or customer success call,” ZoomInfo CEO and founder Henry Schuck said in a blog post announcing the deal.

Ahead of the transaction, ZoomInfo was valued at just under $21 billion.

Chorus looks for what it calls “smart themes” in sales calls, which help managers steer sales teams toward the types of conversation and tone that is likely to drive more revenue. In fact, Chorus holds the largest patent portfolio related to conversational intelligence, according to the company.

Chorus was founded in 2015 and raised more than $100 million along the way, according to PitchBook data. The most recent round was a $45 million Series C last year.

Crunchbase News reports that at the time of its Series C round of funding, Chorus had “doubled its headcount to more than 100 employees and tripled its revenue over the past year.” That’s the sort of growth that venture capitalists covet, making the company’s 2020 funding round a nonsurprise.

Notably PitchBook data indicates that the company’s final private valuation was around the $150 million mark; if accurate, it would imply that the company’s last private round was expensive in dilution terms, and that its investors did well in the exit, quickly more than trebling the capital that was last invested, with investors who put capital in earlier doing even better.

But we’re slightly skeptical of the company’s available valuation history given the growth that it claimed at the time of its Series C; it feels low. If that’s the case, the company’s exit multiple would decrease, making its final sale price slightly less impressive.

Of course, a half-billion-dollar exit is always material, even if venture capitalists in today’s red-hot, and expensive, market are more interested in $1 billion exits and larger.

Chorus.ai will likely not be the final exit in the conversational intelligence space. Its rival Gong (often known by its URL, Gong.io) is one of the hotter startups in this space, having raised over $500 million. Its most recent raise was $250 million on a $7.25 billion valuation last month.

The implication of the Chrous.ai exit and Gong’s enormous private valuation is that the application of AI to audio data in a sales environment is incredibly useful, given the number of customers the two companies’ aggregate valuation implies.

Powered by WPeMatico

It’s easy to forget, but Salesforce bought Slack at the end of last year for almost $28 billion, a deal that has yet to close. We don’t know exactly when that will happen, but Slack continues to develop its product roadmap adding new functionality, even while waiting to become part of Salesforce eventually.

Just this morning, the company made official some new tools it had been talking about for some time, including a new voice tool called Slack Huddles, which is available starting today, along with video messaging and a directory service called Slack Atlas.

These tools enhance the functionality of the platform in ways that should prove useful as it becomes part of Salesforce whenever that happens. It’s not hard to envision how integrating Huddles or the video tools (or even Slack Atlas for both internal and external company organizational views) could work when integrated into the Salesforce platform.

Slack CEO Stewart Butterfield says the companies aren’t working together yet because of regulatory limits on communications, but he could definitely see how these tools could work in tandem with Salesforce Service Cloud and Sales Cloud among others and how you can start to merge the data in Salesforce with Slack’s communications capabilities.

“[There’s] this excitement around workflows from the big system of record [in Salesforce] into the communication [in Slack] and having the data show up where the conversations are happening. And I think there’s a lot of potential here for leveraging these indirectly in customer interactions, whether that’s sales, marketing, support or whatever,” he said.

He said that he could also see Salesforce taking advantage of Slack Connect, a capability introduced last year that enables companies to communicate with people outside the company.

“We have all this stuff working inside of Slack Connect, and you get all the same benefits that you would get using Huddles to properly start a conversation, solve some problem or use video as a better way of communicating with [customers],” he said.

These announcements seem to fall into two main categories: the future of work and in the context of the acquisition. Bret Taylor, Salesforce president and COO certainly seemed to recognize that when discussing the deal with TechCrunch when it was announced back in December. He sees the two companies directly addressing the changing face of work:

“When we say we really want Slack to be this next generation interface for Customer 360, what we mean is we’re pulling together all these systems. How do you rally your teams around these systems in this digital work-anywhere world that we’re in right now where these teams are distributed and collaboration is more important than ever,” Taylor said.

Brent Leary, founder and principal analyst at CRM Essentials says that there is clearly a future of work angle at play as the two companies come together. “I think moves like [today’s Slack announcements] are in response to where things are trending with respect to the future of work as we all find ourselves spending an increasing amount of time in front of webcams and microphones in our home offices meeting and collaborating with others,” he said.

Huddles is an example of how the company is trying to fix that screen fatigue from too many meetings or typing our thoughts. “This kind of ‘audio-first’ capability takes the emphasis off trying to type what we mean in the way we think will get the point across to just being able to say it without the additional effort to make it look right,” he said.

Leary added, “And not only will it allow people to just speak, but also allows us to get a better understanding of the sentiment and emotion that also comes with speaking to people and not having to guess what the intent/emotion is behind the text in a chat.”

As Karissa Bell pointed out on Engadget, Huddles also works like Discord’s chat feature in a business context, which could have great utility for Salesforce tools when it’s integrated with the Salesforce platform

While the regulatory machinations grind on, Slack continues to develop its platform and products. It will of course continue to operate as a stand-lone company, even when the mega deal finally closes, but there will certainly be plenty of cross-platform integrations.

Even if executives can’t discuss what those integrations could look like openly, there has to be a lot of excitement at Salesforce and Slack about the possibilities that these new tools bring to the table — and to the future of work in general — whenever the deal crosses the finish line.

Powered by WPeMatico