investment

Auto Added by WPeMatico

Auto Added by WPeMatico

About 13 years ago I faced an excruciating decision: whether to sell my company, Pinnacle Systems, to a private equity firm or to another large public company. I felt that both suitors would treat my employees well (and I negotiated hard to make sure that was the case), and both offered a good asking price well above our value on NASDAQ.

After raising what at the time felt like my first child, born in my living room and nurtured into a publicly traded entity, I was ready for it to take its next step and for me to take mine. I ultimately opted for the strategic sale, but I left the process intrigued by what was already an evolving dynamic between private equity firms and tech exits.

In years past, stigma often accompanied private equity sales. I know I felt that way, even under strong deal terms. Plus, private equity exits were only available to companies generating substantial annual revenues and often profits, making this exit option inaccessible for many startups. Today, private equity buyout firms can provide a solid (and on occasion excellent) exit route — as well as an increasingly common one, accounting for 18.5 percent of VC-backed exits in 2017.

Private equity firms are investing in a broad array of technology companies, including highly valued unicorns, but also early- to mid-stage profitable and unprofitable companies that a few years ago would have been unable to secure interest from these buyout firms.

In addition, the lines between venture capital and private equity are increasingly blurring, with more private equity investments in tech, and several-late stage VC firms creating large, billion-dollar plus late-stage growth funds. Further blurring the lines, some of the late-stage VC firms are taking controlling interests in startups, a strategy typically associated with private equity. Recently, one of our portfolio companies received an investment from a late-stage VC firm that acquired a majority stake by providing liquidity to some existing shareholders and investing in the company, utilizing a strategy typically associated with PE buyout firms.

The rise of private equity buyouts within the tech sector presents a viable exit option for founders, given the reality that most startups won’t ultimately IPO. (According to PitchBook, only 3 percent of venture-backed companies in the last decade eventually went public.)

If an IPO is not a realistic long-term option, the remaining primary exit option has typically been a sale to another company (a strategic buyer, in venture parlance). However, in the past few years, private equity firms have become aggressive buyers of private companies, sometimes bidding as high as or higher than strategic buyers. With one of my portfolio companies, a private equity buyer placed the second highest bid ahead of all but one strategic buyer and helped raise the final price from the strategic buyer just by being in the bidding process.

Founders who find themselves in negotiations with strategic buyers should also reach out to PE firms to optimize the outcome. Silver Lake, Francisco Partners, Thoma Bravo and Vista are a few technology-focused PE firms, and PitchBook’s annual liquidity report lists other firms. Vista has been especially active, acquiring many technology companies, including Infoblox, Lithium and Marketo. Not all PE firms are the same, just like not all VCs and strategic buyers are the same.

Years ago, when private equity buyouts were typically only large deals, new management teams were almost always brought in to tweak the edges of already successful companies. Today, each private equity firm has its own strategy — some only buy large profitable companies, others focus on mid-size acquisitions and some only buy early-stage (typically unprofitable) companies, which brings us to the next point.

Even early-stage startups can explore a PE exit, especially if things are not going well

While most readers are familiar with private equity buyers at later stages, what’s new is the emergence of PE activity at early stages. These firms acquire majority stakes in startups that have only raised early-stage investments but are having trouble scaling or raising the next round.

After a buyout, these private equity firms typically provide value by adding the missing elements, such as marketing or sales know-how, in order to kick-start the business and achieve scale. Their goal is to increase the value of the underlying asset by augmenting founder teams with the buyout firm’s own operational experts, sometimes combining newly acquired assets with already existing assets to create a stronger whole, or doubling-down on promising products (while shedding less promising offerings) to unlock potential.

Typically, these PE firms then sell the company to another company (usually a strategic buyer) for greater value. In some cases, these early-stage PE firms sell to another PE buyout firm further up market. In some of these acquisitions, founders can maintain minority ownership in the company (though not a controlling stake), which they can carry through to their “next exit.”

Unlike PE buyouts at later stages, PE buyouts at the earlier stages are not usually high-value exits; they are mostly an avenue to provide the founders some return for their hard work, rather than the disappointing returns they can expect from an acqui-hire or, even worse, a shutdown. If negotiated correctly, a private equity deal can give founders an opportunity to play another hand to the next exit.

Few founders create companies in order to flip them. Strong entrepreneurs create companies to transform their missions into reality and positively impact the world. Steve Jobs said, “I’m convinced that about half of what separates the successful entrepreneurs from the non-successful ones is pure perseverance.” An acquisition — particularly to private equity — may not have been the original goal, but it may fuel the continued pursuit of the founder’s mission. Or, perhaps it will enable the pursuit of a new and worthy mission.

Powered by WPeMatico

Skyline AI founders Iri Amirav, Or Hiltch, Guy Zipori and Amir Leitersdorf

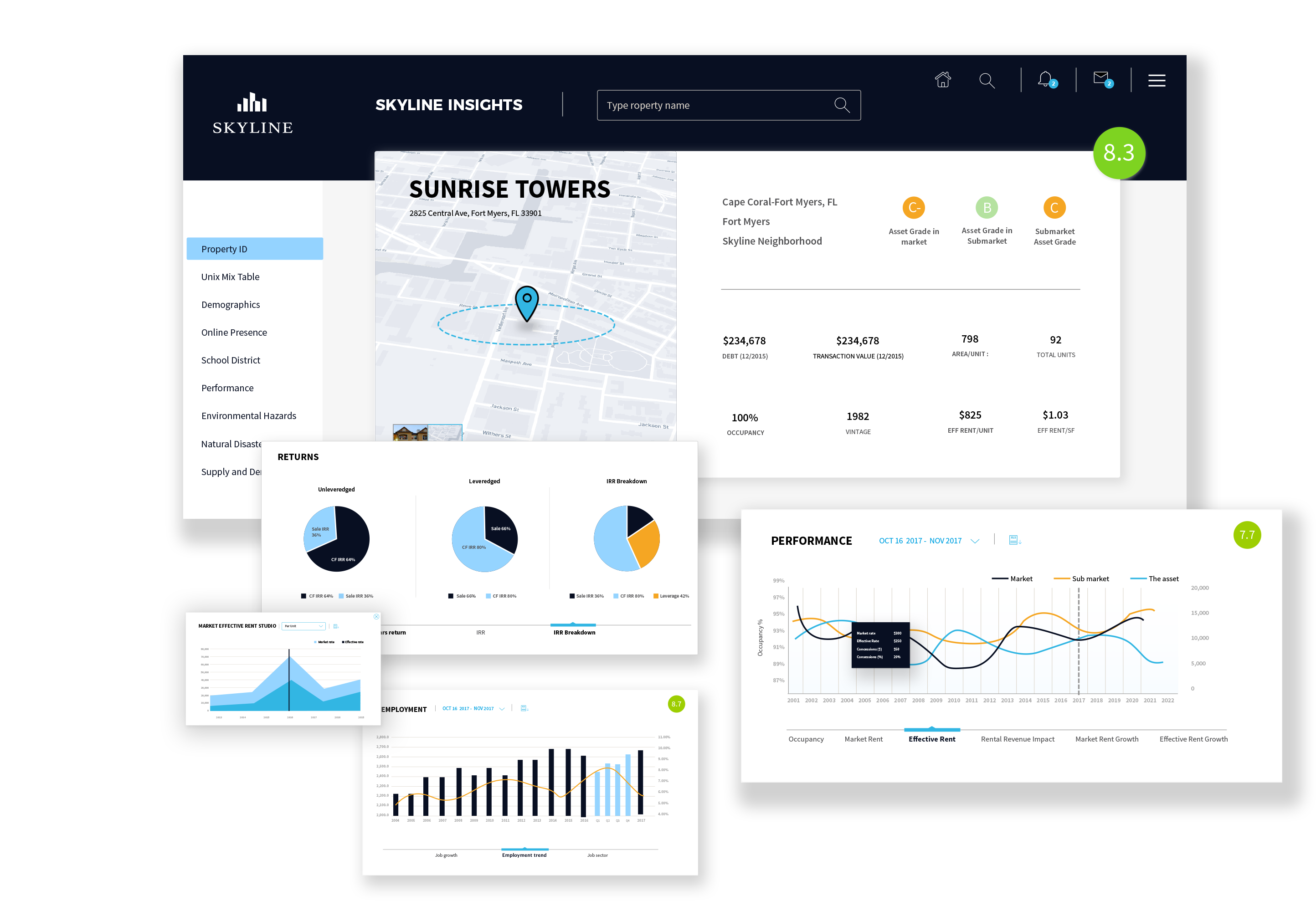

A mere four months after coming out of stealth mode with $3 million in seed funding, real estate investment startup Skyline AI announced that it has raised an $18 million Series A. The round was led by Sequoia Capital, a returning investor, and TLV Partners, with participation from JLL Spark, a division of real estate investment management firm JLL. The strategic funding will allow Skyline AI to add more asset classes to its platform, which uses data science and machine learning algorithms to help institutional investors make better decisions about properties.

Skyline AI says its technology is trained on what it claims is the most comprehensive data set in the industry, drawing from more than 100 sources, with market information covering the last 50 years. Its technology is meant to provide faster and more accurate analysis than traditional methods, so investors can react more quickly to changes in the real estate market.

Co-founder and CEO Guy Zipori told TechCrunch in an email that the startup decided to raise its Series A so soon after coming out of sleath because of positive response from investors, adding that the round was oversubscribed. “The timing of the round also worked out perfectly with our current deal flow and expansion plans. The round was significant, putting us in a great position to move forward,” he said.

Skyline AI has had a busy few months since emerging from stealth. In June, it teamed up with an unnamed partner in the U.S. to acquire two residential complexes in Philadelphia for $26 million. Zipori said they decided to make an unsolicited offer after Skyline AI’s platforms determined the properties were being mismanaged. Then in July, Skyline AI announced a partnership with Greystone, a real estate lending, investment and advisory firm, to collaborate on improving the dealmaking and loan underwriting processes.

JLL and other strategic investors in Skyline AI’s Series A will allow the startup to add analysis and underwriting for new asset classes, including industrial, retail and office properties, to its platform. “This in turn will enable us to deepen and strengthen cooperation with the leading commercial real estate investment firms across the U.S.,” said Zipori. Some of the capital will also be spent on growing its research and development, data science and AI teams in Tel Aviv, and its recently opened sales and real estate office in New York.

In a press statement, Sequoia Capital partner Haim Sadger said “Over the last few years, we’ve seen AI disrupt a number of traditional industries and the real estate market should be no different. The power of Skyline AI technology to understand vast amounts of data that affect real estate transactions, will unlock billions of dollars in untapped value.”

Powered by WPeMatico

Ian Rountree, the twenty something captain at the helm of Cantos Ventures, an SF-based micro-fund, is characteristic of a new breed of venture capitalists in tech — a group of small funds looking to go toe-to-toe with some of the valley’s most entrenched seed funds like First Round Capital and SV Angel. Rountree is experimenting with a strategy so antithetical to the venture… Read More

Ian Rountree, the twenty something captain at the helm of Cantos Ventures, an SF-based micro-fund, is characteristic of a new breed of venture capitalists in tech — a group of small funds looking to go toe-to-toe with some of the valley’s most entrenched seed funds like First Round Capital and SV Angel. Rountree is experimenting with a strategy so antithetical to the venture… Read More

Powered by WPeMatico

Major tech trends tend to draw lots of “dumb money” from investors, and machine intelligence is no exception. Some will lose money on insignificant acqui-hires while others may survive long enough to see their investments die at the hands of open source. But for a smaller list of VCs, machine intelligence presents one of the greatest opportunities for return on investment in the… Read More

Major tech trends tend to draw lots of “dumb money” from investors, and machine intelligence is no exception. Some will lose money on insignificant acqui-hires while others may survive long enough to see their investments die at the hands of open source. But for a smaller list of VCs, machine intelligence presents one of the greatest opportunities for return on investment in the… Read More

Powered by WPeMatico

Buyouts may replace IPOs as the exit of choice for tech companies in the coming months. This comes as the number of startups unable to exit into a frozen market continues to grow. With only two tech IPOs so far in 2016, and poor market returns for the majority of those already public, companies are turning elsewhere to cash in on their efforts. Just this week, analytics firm QLik was… Read More

Buyouts may replace IPOs as the exit of choice for tech companies in the coming months. This comes as the number of startups unable to exit into a frozen market continues to grow. With only two tech IPOs so far in 2016, and poor market returns for the majority of those already public, companies are turning elsewhere to cash in on their efforts. Just this week, analytics firm QLik was… Read More

Powered by WPeMatico

This morning, the law firm Fenwick & West published new findings about all the U.S.-based unicorn financings that took place during the last nine months of 2015. It’s rife with interesting nuggets, but perhaps most fascinating is that in the fourth quarter of last year, half of the 12 rounds it tracked featured valuations in the $1 billion to $1.1 billion range — and with… Read More

This morning, the law firm Fenwick & West published new findings about all the U.S.-based unicorn financings that took place during the last nine months of 2015. It’s rife with interesting nuggets, but perhaps most fascinating is that in the fourth quarter of last year, half of the 12 rounds it tracked featured valuations in the $1 billion to $1.1 billion range — and with… Read More

Powered by WPeMatico

It seems most founders believe investors asking for “extras” on the side are simply greedy and short-sighted. While it’s easy to criticize investors, I believe this behavior is driven in large part as a response to conditions founders have created in early stage investing. I believe two trends, when taken together, have eroded the “one round, one price” standard. Read More

It seems most founders believe investors asking for “extras” on the side are simply greedy and short-sighted. While it’s easy to criticize investors, I believe this behavior is driven in large part as a response to conditions founders have created in early stage investing. I believe two trends, when taken together, have eroded the “one round, one price” standard. Read More

Powered by WPeMatico

Following the bell, Fitbit announced its third-quarter financial performance, including revenue of $409.3 million, and earnings per share using normal accounting methods of $0.19. The company’s adjusted profit totaled $0.24 per share.

Following the bell, Fitbit announced its third-quarter financial performance, including revenue of $409.3 million, and earnings per share using normal accounting methods of $0.19. The company’s adjusted profit totaled $0.24 per share.

The results are notably strong. Investors had expected the company to report a far-slimmer $0.10 adjusted per-share profit off of revenue of just $350.97. Read More

Powered by WPeMatico

Samsung’s venture arm has contributed to a round of funding that adds $13 million to the total raised by BlueStacks, the virtualization startup that debuted its GamePop platform earlier this year to offer over-the-top mobile gaming for living room and TVs. Samsung’s investment backs the company’s vision of delivering GamePop as a white-label solution aimed at TV makers and… Read More

Samsung’s venture arm has contributed to a round of funding that adds $13 million to the total raised by BlueStacks, the virtualization startup that debuted its GamePop platform earlier this year to offer over-the-top mobile gaming for living room and TVs. Samsung’s investment backs the company’s vision of delivering GamePop as a white-label solution aimed at TV makers and… Read More

Powered by WPeMatico