investment

Auto Added by WPeMatico

Auto Added by WPeMatico

LanzaJet, the renewable jet fuel startup spun out from the longtime renewable and synthetic fuel manufacturer LanzaTech, has inked a supply agreement with British Airways to supply the company with at least 7,500 tons of fuel additive per year.

The deal marks the second agreement between the U.K.-based airline and a renewable jet fuels manufacturer following an August 2019 agreement with the British company Velocys. It’s also LanzaJet’s second offtake agreement. The company announced itself with a partnership between the renewable fuels manufacturer and the Japanese airline ANA.

Through the deal, British Airways will invest an undisclosed amount in LanzaJet’s first commercial scale facility in Georgia. The fuel will begin powering flights by the end of 2022, the companies said.

It’s part of a broader expansion effort that could see LanzaJet establish a commercial facility for the U.K. airline in its home country in the coming years.

Back in the U.S. the plan is to begin construction on the Georgia facility later this year, which will convert ethanol into a jet fuel additive using a chemical process.

Fuel from the plant will reduce the overall greenhouse emissions by 70% versus traditional jet fuel. It’s the equivalent of taking almost 27,000 gasoline or diesel-powered cars off the road each year, according to the company.

The deal is the culmination of years of research and development work between LanzaJet’s parent company, LanzaTech, and Department of Energy’s Pacific Northwest National Laboratory.

Spun off in June 2020, LanzaJet was financed by an investment group including parent company LanzaTech, Mitsui, and Suncor Energy. British Airways now joins the two other strategic investors as LanzaJet eyes an ambitious scale-up program through 2025. The company plans to launch four large-scale plants producing a pipeline of renewable fuels.

“Low-cost, sustainable fuel options are critical for the future of the aviation sector and the LanzaJet process offers the most flexible feedstock solution at scale, recycling wastes and residues into SAF that allows us to keep fossil jet fuel in the ground. British Airways has long been a champion of waste to fuels pathways especially with the UK Government,” said Jimmy Samartzis, the chief executive of LanzaJet. “With the right support for waste-based fuels, the UK would be an ideal location for commercial scale LanzaJet plants. We look forward to continuing the dialogue with BA and the UK Government in making this a reality, and to continuing our support of bringing the Prime Minister’s Jet Zero vision to life.”

The LanzaJet fuel is certified for commercial flight up to 50% blend with conventional kerosene. “Considering the aviation market is 90 billion gallons of jet fuel a year, having 50% or 45 billion of production capacity and reaching that max blend level will be a great problem to have,” said LanzaTech chief executive Jennifer Holmgren in an email.

LanzaJet’s manufacturing facility in Georgia is designed to produce zero-waste fuels, according to Holmgren, and British Airways will receive 7,500 tons of sustainable aviation fuel from LanzaJet’s biorefinery each year for the next five years.

The partnership is between British Airways, Hangar 51 (International Airlines Group’s accelerator) and others.

In addition to its biofuel work, British Airways is also working with companies like ZeroAvia, the hydrogen fuels company that also received backing from Amazon, Shell and Breakthrough Energy Ventures.

“For the last 100 years we have connected Britain with the world and the world with Britain, and to ensure our success for the next 100, we must do this sustainably,” said British Airways chief executive Sean Doyle.

“Progressing the development and commercial deployment of sustainable aviation fuel is crucial to decarbonising the aviation industry and this partnership with LanzaJet shows the progress British Airways is making as we continue on our journey to net zero.”

Powered by WPeMatico

It’s a special day; we’re hosting the year’s final episode of Extra Crunch Live with General Catalyst’s Peter Boyce and Katherine Boyle at 4 p.m. EST/1 p.m. PST.

Extra Crunch members can join the live conversation (details below) or catch it on demand. Questions from the audience are not just allowed, they’re highly encouraged, so if you’re not yet an Extra Crunch member, sign up here and join the fun!

General Catalyst is widely recognized as one of the top venture capital firms, with portfolio companies that include Snap, Kayak, Airbnb, Stripe, HubSpot and GitLab.

Boyce has been with General Catalyst since 2013, leading investments in companies like Ro, Macro, towerIQ and Atom. He also supported some big deals, including investments in Giphy, Jet.com and Circle. He also co-founded Rough Draft Ventures, an investment arm of General Catalyst focused on funding first-time CEOs out of university.

Boyle was previously a business reporter at The Washington Post before joining General Catalyst, which gives her a unique perspective on the entrepreneurial landscape. She’s invested in several companies, including AirMap, Origin and Nova Credit and has joined us for previous events to lay out some advice for startups navigating governmental rules.

We’re amped to discuss which opportunities are exciting them these days, how tech, innovation and venture has changed amid the pandemic, what they look for in a pitch, and much, much more.

You really won’t want to miss it.

Oh, and if this is of interest, I highly suggest you check out our library of ECL episodes right here. We’ve spoken to big names like Roelof Botha, Jason Green, Alexa von Tobel, Aileen Lee, Charles Hudson and many others.

Catch the details for today’s call below.

Powered by WPeMatico

Welcome, the HR software that helps organizations make and close offers to new candidates, announced the close of a $6 million seed round today, led by FirstMark Capital. Participating investors include Ludlow Ventures, Nat Turner and Zach Weinberg, and Keenan Rice and Ben Porterfield (which were existing investors), as well as a wide array of angels.

TechCrunch last covered Welcome in August, when it announced a $1.4 million funding round. That the startup was able to raise more as quickly as it has is testament to how hot the early-stage venture capital market is today, and likely an endorsement of Welcome’s economic profile and recent growth.

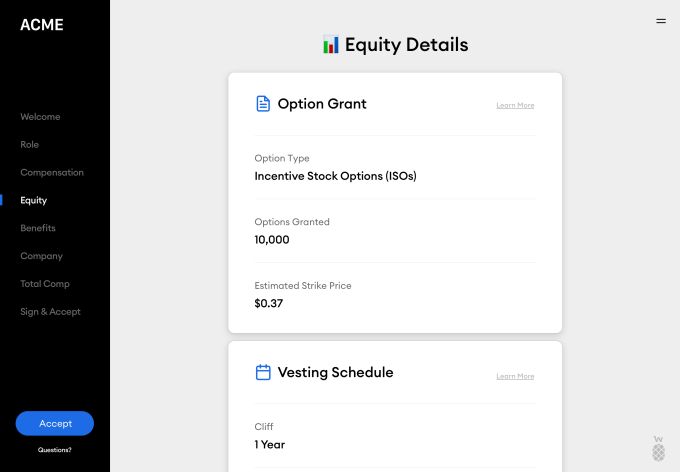

Past the new capital, Welcome is also launching a new product today called Total Rewards, which helps not just new candidates but also existing employees get a complete, easy-to-understand picture of their compensation, across salary, benefits, equity, etc.

But let’s back up.

Welcome was founded in 2019 by Nick Gavronsky and Rick Pereira, with a mission to help organizations close offers on candidates by providing a much clearer picture of compensation, particularly around equity. Co-founder and CEO Nick Gavronsky explained that many candidates don’t truly understand the value of the equity they’re offered, or how it works.

“A lot of recruiting teams aren’t well-equipped to use it as a selling tool and explain it effectively and showcase the value to candidates to help them think about their ownership at the company,” he added.

Image Credits: Welcome

Welcome allows companies to organize their compensation offers based on level and position, and deliver that information digitally to candidates in a way that makes sense.

The startup integrates with a variety of other software providers, including Slack, Lever, Greenhouse, ADP and Justworks to name a few, simplifying onboarding for Welcome clients and bringing a broad array of information into one place.

Offers sent through Welcome show a description of the role, equity details, total compensation and even include a welcome note and video. This is in stark contrast to the black and white legal PDF often sent to candidates.

Image Credits: Welcome

The next phase for the company comes in the form of the launch of Total Rewards, which is meant to help retain existing employees, helping them understand their compensation value and their potential at the company.

“Painting a better picture becomes a pre-retention tool,” said Gavronsky. “An employee will sometimes leave thousands of dollars on the table because they don’t understand what they’re walking away from. A lot of times companies will wait until that person is going to resign. Let me now bring up all the things that are great about our company and talk through your stock options. But the decision’s already made. So we wanted something that we can kind of put in with performance reviews.”

Welcome also has plans to offer a third product pillar in the form of real-time accurate industry-wide compensation data, helping companies understand where they fit into the larger ecosystem with regards to compensation.

Thus far, Welcome has 40 companies on the platform, including Uncork and Betterment, with hundreds on the waitlist, according to the co-founders. The company plans to use the funding to build out the team and the product.

Powered by WPeMatico

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

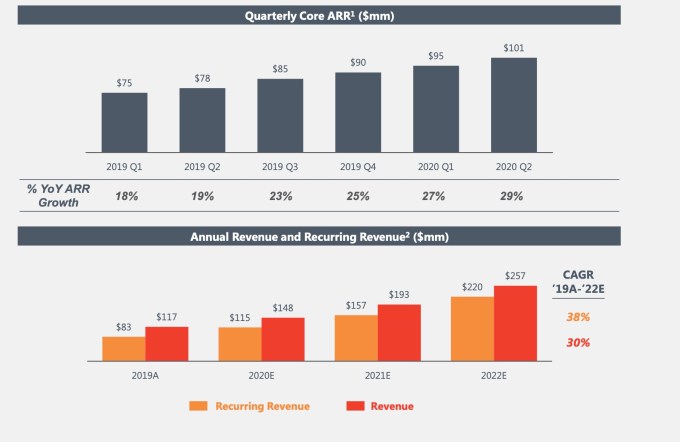

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

Yesterday, Baltimore-based fintech company Facet Wealth said it raised $25 million in financing as it readies a new business line pitching financial planning as an employment benefit to businesses looking to recruit top talent.

Employment benefit packages are expanding beyond the basic gym membership and healthcare to include subscriptions to Netflix, discounts on delivery and rideshare services, and other perks. So why not financial wellness?

The thesis certainly managed to attract a big-money backer, with Warburg Pincus, the multi-billion-dollar private equity investment firm, which doubled down on its commitment with the new financing into the company.

The company said the latest round would be used to finance the expansion of Facet Wealth’s direct-to-consumer business even as it readies its employee benefit service for launch.

Already customers are signing up for pre-launch partnerships to get their employees on the program. Early wannabe users include ClassPass, MyVest and Chili Piper, the company said.

“Since our first investment two years ago, the Facet Wealth team has proven their ability to meet a unique consumer need, evolving and expanding their offering to build a truly innovative client experience and business model,” said Jeff Stein, managing director at Warburg Pincus. “Their expansion into the employer market further solidifies them as a category-defining company that is well-positioned to disrupt the wealth management industry for years to come.”

To date, Facet Wealth has raised $62 million in funding from Warburg Pincus, Slow Ventures and other, undisclosed investors.

Powered by WPeMatico

The Miami-based startup Papa has raised an additional $18 million as it looks to expand its business connecting elderly Americans and families with physical and virtual companions, which the company calls “pals.”

The company’s services are already available in 17 states and Papa is going to expand to another four states in the next few months, according to chief executive Andrew Parker.

Parker launched the business after reaching out on Facebook to find someone who could serve as a pal for his own grandfather in Florida.

After realizing that there was a need among elderly residents across the state for companionship and assistance that differed from the kind of in-person care that would typically be provided by a caregiver, Parker launched the service. The kinds of companionship Papa’s employees offer range from helping with everyday tasks — including transportation, light household chores, advising with health benefits and doctor’s appointments, and grocery delivery — to just conversation.

With the social isolation brought on by responses to the COVID-19 pandemic there are even more reasons for the company’s service, Parker said. Roughly half of adults consider themselves lonely, and social isolation increases the risk of death by 29%, according to statistics provided by the company.

“We created Papa with the singular goal of supporting older adults and their families throughout the aging journey,” said Parker, in a statement. “The COVID-19 pandemic has unfortunately only intensified circumstances leading to loneliness and isolation, and we’re honored to be able to offer solutions to help families during this difficult time.”

Papa’s pals go through a stringent vetting process, according to Parker, and only about 8% of all applicants become pals.

These pals get paid an hourly rate of around $15 per hour and have the opportunity to receive bonuses and other incentives, and are now available for virtual and in-person sessions with the older adults they’re matched with.

“We have about 20,000 potential Papa pals apply a month,” said Parker. In the company’s early days it only accepted college students to work as pals, but now the company is accepting a broader range of potential employees, with assistants ranging from 18 to 45 years old. The average age, Parker said, is 29.

Papa monitors and manages all virtual interactions between the company’s employees and their charges, flagging issues that may be raised in discussions, like depression and potential problems getting access to food or medications. The monitoring is designed to ensure that meal plans, therapists or medication can be made available to the company’s charges, said Parker.

Now that there’s $18 million more in financing for the company to work with, thanks to new lead investor Comcast Ventures and other backers — including Canaan, Initialized Capital, Sound Ventures, Pivotal Ventures, the founders of Flatiron Health and their investment group Operator Partners, along with Behance founder, Scott Belsky — Papa is focused on developing new products and expanding the scope of its services.

The company has raised $31 million to date and expects to be operating in all 50 states by January 2021. The company’s companion services are available to members through health plans and as an employer benefit.

“Papa is enabling a growing number of older Americans to age at home, while reducing the cost of care for health plans and creating meaningful jobs for companion care professionals,” said Fatima Husain, principal at Comcast Ventures, in a statement. “

Powered by WPeMatico

One of the more salient trends in the tech world — arguably the engine that propels it — has been the recurring theme of people who hone talents at bigger companies and then strike out on their own to found their own startups.

(Some, like Max Levchin, even hire entrepreneurial types intentionally to help perpetuate this cycle and get more proactive teams in place.)

It turns out that trend doesn’t just apply to companies, but also to the investors who back them. At Disrupt we talked with three venture capitalists who have followed that path: Making their names and cutting their teeth at major firms, and now building their own “startup” funds on their own steam.

On the macro level, the whole world has been living through a challenging time this year. But as we’ve seen time and again the wheels have continued to turn in the tech world.

IPOs are returning, products are being rolled out, people are buying a lot online and using the internet to stay connected, there has been a lot of M&A and promising startups are getting funded.

Indeed, if entrepreneurs and their innovations are the engine of the tech world, money is the fuel, and that is the opportunity that Dayna Grayson (formerly of NEA, now founder at Construct Capital), Renata Quintini (formerly at Lux Capital, now founder at Renegade Partners) and Lo Toney (formerly GV, now founder at Plexo Capital) have zeroed in to address.

Grayson said that part of the reason for striking out to start Construct Capital with co-founder Rachel Holt was what they saw as an opportunity to create a firm that specifically funded startups tackling the industrial sector:

“Half the U.S. economy’s GDP, half the GDP of this country, hasn’t really been digitized,” she said. “[Firms] haven’t been tech enabled. They’ve been way under invested … The time is now to build with early stage entrepreneurs.”

While Construct is focusing on a sector, Renegade was founded to focus on something else: The stage of development for a startup, and specific the Series B, which the firm refers to as “supercritical,” essential in terms of getting team and strategy right after a startup is no longer just starting out, but before and leading to scaled growth.

“We saw through our boards over and over again companies that figured out how to scale their organizations, put in the processes,” said Quintini, who co-founded Renegade with Roseanne Wincek. “On the people side, they actually went further and captured a lot more market cap and market share faster. Once we saw this opportunity, we could not let it go.”

She compares the current imperative to really focus on how to build and scale companies at the “supercritical” stage to the focus on early stage funding that typified an earlier period in the development of the startup ecosystem 15 years ago. “You could get a million dollars and be in business, a lot more people could, and you had less time to figure out what really resonated with customers,” she said. “That really gave rise to today.”

Toney has taken yet another approach, focusing not on sector, nor stage, but using capital to help germinate a whole new demographic of founders, the premise being that funding a more diverse and inclusive mix of founders is not just good for creating a more level playing field, but also for the good of more well-rounded products that speak to a wider population of users.

“I was having a great time at GV, but I just saw this opportunity as being one that was too hard to resist,” said Toney of founding Plexo, which invests not just in startups but in funds that are following a similar investment principle to his. Investing in both funds and founders is something GV did as well, but the added ability to turn that into investing with a social imperative was important. “To have this byproduct of increasing diversity and inclusion in the ecosystem [is something] I’m super passionate about,” he said.

We are living through a time when the tech world seems to be awash in capital. One of the byproducts of having so many successful tech companies has been limited partners rushing in to back more VCs in hopes of also getting some of the spoils: Many firms are closing funds in record times, oversubscribed and that’s having a knock-on effect not just in terms of startups getting funded, but VCs themselves also multiplying with increasing frequency. All three said that the fact that they all identify as more than just “another new VC”, with specific purposes, also makes it easier for them to get themselves noticed to get involved in good deals.

Grayson said that the challenge of starting a firm in the midst of a global pandemic turned out to be a piece of good fortune in disguise in an industry that thrives on the concept of “disruption” (as we at TechCrunch know all too well … ).

“We were really lucky that we started investing in a COVID world,” she said. “So many things have been up ended. And I think, you know, software adoption and technology adoption have been moved up 10-20 years in industry. [And] the way that we work together really has changed.” She also said that they’ve found themselves almost looking for companies “created in a COVID environment,” which indeed would qualify as a battle-tested business model.

In terms of raising funds themselves, Toney also recalled the period when we saw a real surge of VCs emerging to fund companies at the seed stage and the growth of “solo capitalists” around that.

“I think what’s really interesting about solo capitalists is [how] they take their understanding of operations, and a deep network of other technologists, both from big companies as well as entrepreneurs, and … leverage access to all that deal flow by going out and actually raising capital from other sources, whether that be high net worth individuals or family offices or even institutions,” he said.

Powered by WPeMatico

While a handful of tech companies like Zoom and Shopify are enjoying massive gains as a result of COVID-19, that’s obviously not the case for most. Weaker demand, slower sales cycles, and customer insistence on pricing concessions and payment deferrals have conspired to cloud the outlook for many tech companies’ growth.

Compounding these challenges, a lot of tech companies are struggling to raise capital just when they need it most. The data so far suggests that investors, particularly those focused on earlier stage financings, are taking a more cautious approach to new deals and valuations while they wait to see how individual companies perform and which way the economy will go. With the outcome of their planned equity financings uncertain, some tech companies are revisiting their funding strategies and exploring alternative sources of capital to fuel their continued growth.

For certain businesses, COVID-19’s impact on revenue was immediate. For others, the effects of slower economic activity and tighter budgets surfaced more gradually with deals in the funnel before the pandemic closing in April and May. Either way, in the second half of 2020, technology CFOs face a common challenge: How do you accurately forecast sales when there’s very little consensus around key issues such as when business activity will return to pre-COVID levels and what the long-term effects of the crisis might be?

Unfortunately, navigating this uncertainty is just as daunting a challenge for investors. These days, equity investors’ assessment of a company’s growth potential, and the value they are willing to pay for that growth, aren’t just impacted by their view of the company itself. Equally important is their assumptions about when the economy will recover and what the new normal might look like. This uncertainty can lead to situations where companies and their potential investors have materially different views on valuation.

While the full impact of COVID was felt too late to have a material impact on Q1 deal volumes, recently released data from Pitchbook and the NVCA suggest that 2020 will see a significant decrease in the number of companies funded, possibly by as much 30 percent compared to 2019 among early stage companies. And, while it often takes several months to see evidence of broad trends in investment terms, anecdotal evidence indicates investors are seeking to mitigate risk by demanding additional protective provisions.

Powered by WPeMatico

Now that I’ve offered an overview to help you think through where concentrated stock sits in your overall plan, let’s take a closer look at why selling can be challenging for some.

In the following section, I reveal the facts of the concentrated stock “get rich” myths that reside in the minds of many first-time concentrated stock owners, and I show why it is prudent to consider greater diversification.

Keep reading to learn more about the benefits of diversification, discover how much company stock is likely too much to hold, and the options you have when it comes to diversifying strategically.

There are several hard facts to keep in mind in contemplating maintaining a concentrated position:

The odds of any new IPO being among the top 4% is just slightly better than hitting your lucky number on the roulette wheel. But is your investment portfolio success and the odds of achieving your long-term financial goals something you want to spin the wheel on?

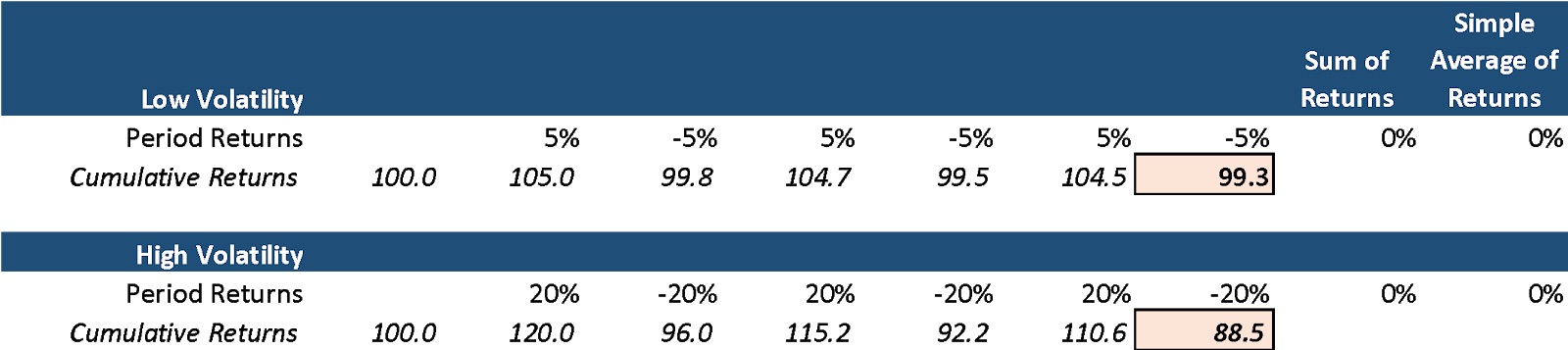

Excess volatility can harm returns. Note the example below that shows the comparison between a low-volatility diversified portfolio versus a high-volatility concentrated portfolio. Despite the same simple average return, the low-volatility portfolio below materially outperforms the high-volatility portfolio.

Image Credits: Peyton Carr

Beyond the math, unexpected spikes in volatility can cause significant price declines. Volatility increases the chances that an investor reacts emotionally and makes a poor investment decision. I’ll cover the behavioral finance aspect of this later. Lowering your portfolio volatility can be as simple as increasing your portfolio diversification.

The Russell 3000, an index representing the 3,000 largest U.S.-based publicly traded companies, has lower volatility when compared against 95%+ of all single stocks. So, how much return do you give up for having lower volatility?

According to Northern Trust Research, the 5.96% annualized average return of the Russell 3000 is 0.73% more than the 5.23% return of the median stock. Additionally, owning the Russell 3000, rather than a single stock, eliminates the likelihood of catastrophic loss scenarios — more than 20% of shares averaged a loss of more than 10% per year over a 20-year time frame.

If this establishes that the avoidance of overly concentrated portfolios is important, how much stock is too much? And at what price should you sell?

We consider any stock position or exposure greater than 10% of a portfolio to be a concentrated position. There is no hard number, but the appropriate level of concentration is dependent on several factors, such as your liquidity needs, overall portfolio value, the appetite for risk and the longer-term financial plan. However, above 10% and the returns and volatility of that single position can begin to dominate the portfolio, exposing you to high degrees of portfolio volatility.

The company “stock” in your portfolio often is only a fraction of your overall financial exposure to your company. Think about your other sources of possible exposure such as restricted stock, RSUs, options, employee stock purchase programs, 401k, other equity compensation plans, as well as your current and future salary stream tied to the company’s success. In most cases, the prudent path to achieving your financial goals involves a well-diversified portfolio.

Facts aside, maintaining a concentrated position in your company stock is far more tempting than taking a more measured approach. Token examples like Zuckerberg and Bezos tend to outshine the dull rationale of reality, and it’s hard to argue against the possibility of becoming fabulously wealthy by betting on yourself. In other words, your emotions can get the best of you.

But your goals — not your emotions — should be driving your investment strategy and decisions regarding your stock. Your investment portfolio and the company stock(s) within it should be used as tools to achieve those goals.

So first, we’ll take a deep dive into the behavioral psychology that influences our decision-making.

Despite all the evidence, sometimes that little voice remains.

“I want to hold the stock.”

Why is it so hard to shake? This is a natural human tendency. I get it. We have a strong impetus to rationalize our biases and not believe we are vulnerable to being influenced by them.

Becoming attached to your company is common, since after all, that stock has made you, or has the potential of making you wealthy. More often than not, selling and diversifying is the tough, but more rational decision.

Numerous studies have furnished insights into the correlation between investing and psychology. Many unrecognized psychological barriers and behavioral biases can influence you to hold concentrated stock even when the data shows that you should not.

Understanding these biases can be helpful when deciding what to do with your stock. These behavioral biases are hard to spot and even harder to overcome. However, awareness is the first step. Here are a few more common behavioral biases, see if any apply to you:

Familiarity bias: Familiarity is likely why so many founders are willing to hold concentrated positions in their own company’s stock. It is easy to confuse the familiarity with your own company with the safety in the stock. In the stock market, familiarity and safety are not always related. A great (safe) company sometimes can have a dangerously overvalued stock price, and terrible companies sometimes have terrifically undervalued stock prices. It’s not just about the quality of the company but the relationship between the quality of a company and its stock price that dictates whether a stock is likely to perform well in the future.

Another way this manifests is when a founder has less experience with stock market investing and has only owned their company stock. They may think the market has more risk than their company when in actuality, it is usually safer than holding just their individual position.

Overconfidence: Every investor is exhibiting overconfidence when they hold an overly concentrated position in an individual stock. Founders are likely to believe in their company; after all, it already achieved enough success to IPO. This confidence can be misplaced in the stock. Founders often are reluctant to sell their stock if it has been going up since they believe it will continue to go up. If the stock has sold off, the opposite is true, and they are convinced it will recover. Often, it is challenging for founders to be objective when they are so close to the company. They commonly believe that they have unique information and know the “true” value of the stock.

Anchoring: Some investors will anchor their beliefs to something they experienced in the past. If the price of the concentrated stock is down, investors may anchor their belief that the stock is worth its recent previous higher value and be unwilling to sell. This previous value of the stock is not an indicator of its real value. The real value is the current price where buyers and sellers exchange the stock while incorporating all presently available information.

Endowment effect: Many investors tend to place a higher value on an asset they currently own than if they did not own it at all. It makes it harder to sell. An excellent way to check for the endowment effect is to ask yourself: “If I did not own these shares, would I purchase them today at this price?” If you are not willing to purchase the shares at this price today, it likely means you are only holding onto the shares because of the endowment effect.

A fun spin on this is to look into the IKEA effect study, which demonstrates that people assign more value to something that they made than it is potentially worth.

When framed this way, investors can make more intentional decisions on whether to continue holding concentrated stock or selling. At times, these biases are hard to spot, which is why having a second person, a co-pilot, or an advisor, is helpful.

Congratulations to those of you with a concentrated stock position in your company; it is hard-earned and likely represents a material wealth. Understand, there is no “right” answer when it comes to managing concentrated stock. Each situation is unique, so it is essential to speak with a professional about options specific to your situation.

It starts with having a financial plan, complete with specific investment goals that you want to achieve. Once you have a clear picture of what you want to accomplish, you can look at the facts in a new light and gain a deeper appreciation for the dangers of holding a concentrated position in company stock versus the benefits of diversification, considering all of the implications and opportunities involved in rational decision-making and investment behavior.

Most individuals understand they can simply and directly sell their equity, but there are a variety of other strategies. Some of these opportunities may be far better at minimizing taxes or better at achieving the desired risk or return profile. Some might wonder what the best timing is to sell. I will cover these topics in the final article of the series.

Powered by WPeMatico