initial public offering

Auto Added by WPeMatico

Auto Added by WPeMatico

Chinese electric scooter startup Niu Technologies has filed for an initial public offering on Nasdaq to raise up to $150 million. In its form, Niu said it is “the largest lithium-ion battery-powered e-scooters company in China,” according to data from China Insights Consultancy, and also a market leader in Europe based on sales volume.

Founded in 2014 and based in Beijing, Niu says it currently holds a market share of 26% in China based on sales volume. Niu’s debut will the latest in a string of recent Chinese tech IPOs, the most prominent of which include the recent Hong Kong listings of Xiaomi and Meituan.

Niu’s scooters connect with an app that give drivers maintenance and performance data and also delivers firmware updates. As of the end of June, Niu claims it had sold more than 431,500 smart electric scooters in China, Europe and other markets.

According to the CIC’s data, China is the largest market for electric two-wheeled vehicles, with retail sales expected to increase to $13 million by 2022, up from $8 billion in 2017. Niu says its growth markets also include Southeast Asia and India, where scooters are a popular form of transportation.

In its filing, Niu said its net revenue in 2017 was RMB 769.4 million ($116.2 million), an increase of 116.8% from RMB 354.8 million in 2016. Its net losses during that time decreased to RMB 184.7 million ($27.9 million) in 2017 from RMB 232.7 million in 2016. More recently, net revenue for the first six months of 2018 was RMB 557.1 million ($84.2 million), an increase of 95.4% from RMB 285.1 million the same period a year earlier. Net loss was RMB 314.9 million ($47.6 million) during that period, compared to RMB 96.6 million the year before.

Powered by WPeMatico

Eventbrite is having one hell of a debut on the New York Stock Exchange this morning.

Shares of the ticketing startup, founded back in 2006, have shot up over 50 percent in trading on the NYSE. After pricing its shares at $23 in its initial offering, investors have bid up the stock to a whopping $37, putting the company’s valuation at nearly $3 billion.

$EB prices $23, opens $36 pic.twitter.com/cYgCuqbmh8

—

(@hunterwalk) September 20, 2018

That’s well above where the ticketing company had hoped to be when it initially set terms for the public offering earlier this month.

The company started trading priced above its share price and nearly doubled its valuation. And if Eventbrite can do it, really almost any later-stage startup should be thinking about the public markets right now.

Performance for the San Francisco ticketing company has been… somewhat lackluster. As we noted when wrote about the company’s offering:

Eventbrite is not profitable and has been losing money since 2016. According to the documents, it posted losses of $40.4 million in 2016 and $38.5 million in 2017. In the first six months of 2018, the company has posted a net loss of $15.6 million. The company is making changes to make up for some of those losses — at the end of August, it announced a new pricing scheme for its customers using the “Essentials” package.

Its revenue is rising though, increasing from $133 million in 2016 to $201 million last year.

Since the beginning of the year tech public offerings have been on a tear. As The Wall Street Journal noted in July, 120 companies had raised $35.2 billion on U.S. exchanges at that point — the best showing for public markets since 2014 and the fourth busiest year since 1995, according to the financial data and analysis service Dealogic.

We’ve noted before that it’s a bit mind-boggling that investors and their portfolio companies wouldn’t be taking more advantage of these heady times. Nothing lasts forever (not even cold November rain) and certainly not markets that have been this bullish for this long.

Some of the reasoning is likely thanks to a market that’s still awash in private equity, sovereign wealth and late-stage dollars. SoftBank has hundreds of billions to invest; private equity firms are beginning to look at growth-stage companies the way that I look at banana cream pies from Cassell’s; and venture firms are beefing up big time to keep up with the Joneses (or in this case, the Blackstoneses).

However, the fun is certainly going to come to an end, and likely sooner rather than later. Early-stage investors are beginning to dole out their advice on lowering cash burn (something that happens every time they see the beginning of the end of the beginning of the end).

Low burn rates have gone out of fashion, but I expect we’ll be reminded very quickly at the beginning of the next downturn why they’re so valuable for early-stage startups.

— Sam Altman (@sama) September 19, 2018

With that in mind, later-stage companies should be looking for the exit signs wherever they can find them. Right now, that’s an IPO window that seems to be wide open.

Powered by WPeMatico

Now valued at $5.6 billion, zero-fee stock trading app and cryptocurrency exchange Robinhood is starting preparations to go public. Just a year and a half ago, it was still largely under the radar. But then it raised a $110 million Series C at a $1.3 billion valuation in April 2017 and then just a year later scored a $363 million Series D, both led by Russian firm DST Global. Combined with the growth of its premium subscription for trading on margin called Robinhood Gold, the startup now has the firepower and revenue to make a viable Wall Street debut.

Today during Robinhood CEO Baiju Bhatt’s talk at TechCrunch Disrupt SF, he revealed that his company is on the path to an IPO and has begun its search for a chief financial officer. It’s also undergoing constant audits from the SEC, FINRA and its security team to make sure everything is kosher and locked up tight.

The CFO hire could help the five-year-old Silicon Valley startup pitch itself as the cheaper youthful alternative to E*Trade and traditional stock brokers. They’d also have to convince potential investors that even though cryptocurrency prices are in a downturn, allowing people to trade them for cheaper than competitors like Coinbase is a powerful user acquisition funnel.

Robinhood now has 5 million customers tracking, buying and selling stocks, options, ETFs, American depositary slips receipts of international companies and cryptos like Bitcoin and Ethereum. That’s twice as many customers as its incumbent competitor E*Trade despite it having 4,000 employees compared to Robinhood’s 250.

The startup has raised a total of $539 million to date from prestigious investors like Andreessen Horowitz, Kleiner Perkins, Sequoia and Google’s Capital G, allowing it to rapidly roll out products before its rivals can react. This rapid rise in valuation can go to some founders’ heads, or crush them under the pressure, but Bhatt cited “friendship” with his co-CEO Vlad Tenev as what keeps him sane.

The startup has three main monetization streams. First, it earns interest on money users keep in their Robinhood account. Second, it sells order flow to stock exchanges that want more liquidity for their traders. And it sells Robinhood Gold subscriptions which range from $10 per month for $2,000 in extra buying power to $200 per month for $50,000 in margin trading, with a 5 percent APR charged for borrowing over that. Gold was growing its subscriber count at 17 percent per month earlier this year, showing the potential of giving trades away for free and then charging for extra services.

But Robinhood is also encountering renewed competition as both startups and incumbents wise up. European banking app Revolut is building a commission-free stock trading, and Y Combinator startup Titan just launched its app that lets you buy into a managed portfolio of top stocks. Finance giant JP Morgan now gives customers 100 free trades in hopes of not being undercut by Robinhood.

Over on the crypto side, Coinbase continues to grow in popularity despite its 1.4 percent to 4 percent fees on trades. It’s rapidly expanding its product offering and the two fintech startups are destined to keep clashing. Robinhood may also be suffering from the crypto downturn, which is likely dissuading the mainstream public from dumping cash into tokens after seeing people lose fortunes as Bitcoin and Ethereum’s prices tumbled this year.

There’s also the persistent risk of a security breach that could tank Robinhood’s brand. Meanwhile, the startup uses both human and third-party software-based systems to moderate its crypto chat rooms to make sure pump and dump schemes aren’t running rampant. Bhatt says he’s proud of making cryptocurrency more accessible, though he didn’t say he felt responsible for prices plummeting, which could mean many of Robinhood Crypto’s users have lost money.

Fundamentally, Robinhood is using software to make the common but expensive behavior of stock trading much cheaper and more accessible to a wider audience. Traditional banks and brokers have big costs for offices and branches, trading execs and TV commercials. Robinhood has managed to replace much of that with a lean engineering team and viral app that grows itself. Once it finds its CFO, that could give it an efficiency and growth rate that has Wall Street seeing green.

Powered by WPeMatico

Elastic, the provider of subscription-based data search software used by Dell, Netflix, The New York Times and others, has unveiled its IPO filing after confidentially submitting paperwork to the SEC in June. The company will be the latest in a line of enterprise SaaS businesses to hit the public markets in 2018.

Headquartered in Mountain View, Elastic plans to raise $100 million in its NYSE listing, though that’s likely a placeholder amount. The timing of the filing suggests the company will transition to the public markets this fall; we’ve reached out to the company for more details.

Elastic will trade under the symbol ESTC.

The business is known for its core product, an open-source search tool called ElasticSearch. It also offers a range of analytics and visualization tools meant to help businesses organize large data sets, competing directly with companies like Splunk and even Amazon — a name it mentions 14 times in the filing.

“Amazon offers some of our open source features as part of its Amazon Web Services offering. As such, Amazon competes with us for potential customers, and while Amazon cannot provide our proprietary software, the pricing of Amazon’s offerings may limit our ability to adjust,” the company wrote in the filing, which also lists Endeca, FAST, Autonomy and several others as key competitors.

This is our first look at Elastic’s financials. The company brought in $159.9 million in revenue in the 12 months ended July 30, 2018, up roughly 100 percent from $88.1 million the year prior. Losses are growing at about the same rate. Elastic reported a net loss of $18.5 million in the second quarter of 2018. That’s an increase from $9.9 million in the same period in 2017.

Founded in 2012, the company has raised about $100 million in venture capital funding, garnering a $700 million valuation the last time it raised VC, which was all the way back in 2014. Its investors include Benchmark, NEA and Future Fund, which each retain a 17.8 percent, 10.2 percent and 8.2 percent pre-IPO stake, respectively.

A flurry of business software companies have opted to go public this year. Domo, a business analytics company based in Utah, went public in June raising $193 million in the process. On top of that, subscription biller Zuora had a positive debut in April in what was a “clear sign post on the road to SaaS maturation,” according to TechCrunch’s Ron Miller. DocuSign and Smartsheet are also recent examples of both high-profile and successful SaaS IPOs.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

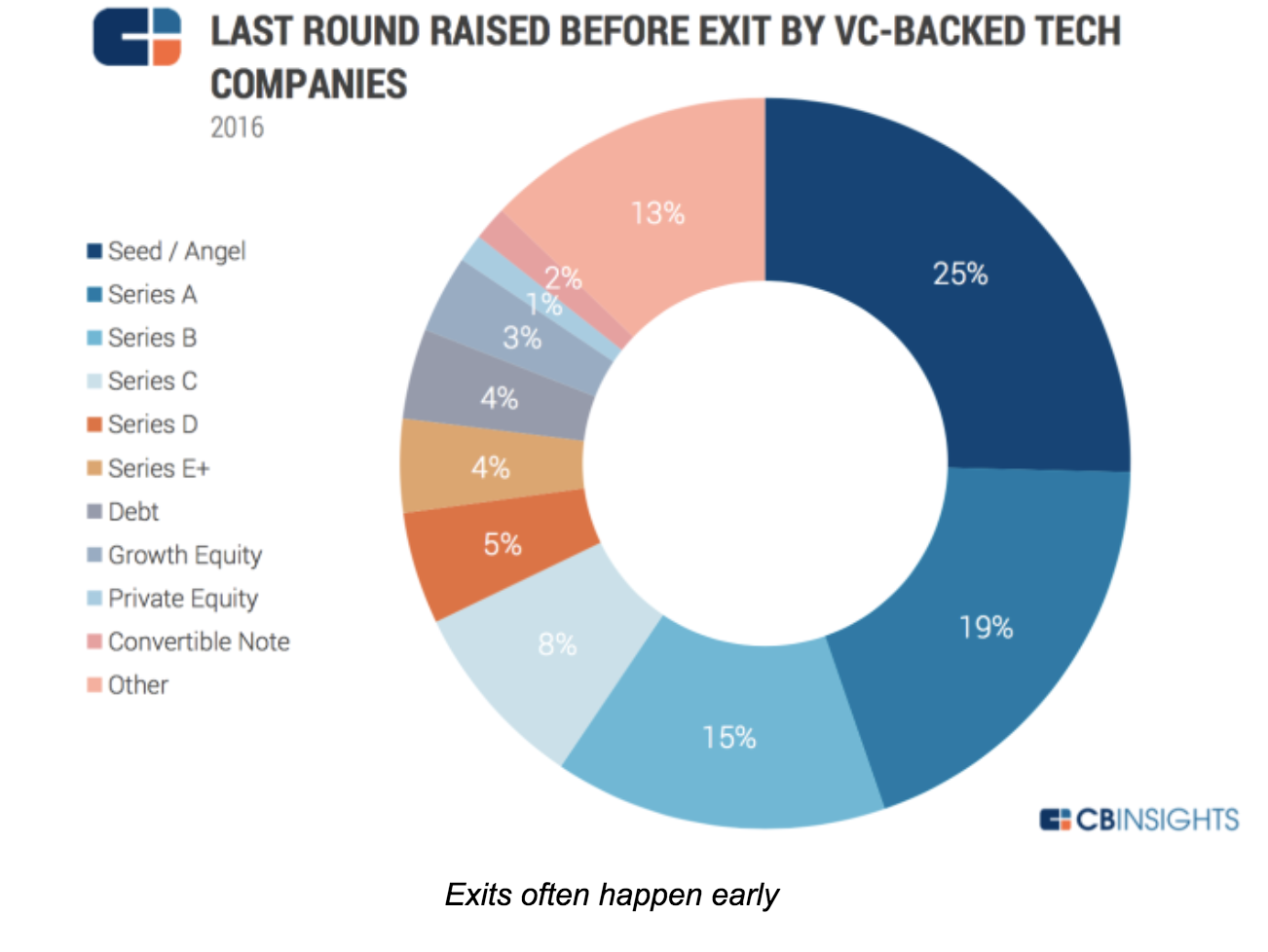

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

Tilray, a five-year-old, British Columbia-based medical cannabis company that sells its products to patients, researchers, pharmacies and even governments, saw its shares get high (sorry) on the Nasdaq today, after the company priced 9 million shares at $17 apiece and watched them soar, closing at $22.39, a jump of slightly more than 32 percent.

The company raised $153 million in the offering, capital it will reportedly use in part to fuel its marijuana growing and processing facilities in Ontario.

It was a huge win for the cannabis industry, which has been growing like a weed (sorry again). Related startups attracted $593 million in funding last year, twice what they raised in 2016 and a meaningful jump from the $121 million invested in related startups in 2014, according to CB Insights. Among the different types of companies to garner investor dollars, shows CB Insights’ research, are: startups focused on research or distribution of medical marijuana products (as with Tilray); tools for ensuring compliance with state and federal marijuana laws; startups focused on payments for marijuana companies; startups collecting data and producing marketing insights about the industry; and companies creating novel strains and types of marijuana using new farming techniques.

Tilray’s performance today is also a very positive signal for Seattle-based Privateer Holdings, a private equity firm that owned 100 percent of the startup as it headed into its offering. In fact, Privateer’s CEO, Brendan Kennedy, is also the CEO of Tilray. (Cannabis companies are weird.)

Privateer has itself raised more than $200 million since its founding in 2010, including from Founders Fund and Subversive Capital, and it has used that capital to fund, acquire and incubate companies. While it incubated Tilray, for example, it also owns Leafly, a large cannabis information resource that it acquired in 2011. Another of its portfolio companies is Marley Natural, a Bob Marley-branded cannabis line that it launched in partnership with the Marley’s estate and that sells a line of cannabis strains, smoking accessories and even body care products.

It isn’t exactly clear how much Privateer had sunk into Tilray (we have a press request into the company). Tilray had announced C$60 million in Series A funding back in February, composed of a “group of leading global institutional investors.” But according to its S-1, it was solely owned until today by Privateer.

What we do know: Tilray remains unprofitable, reporting a net loss of $7.8 million last year. The company also cannot sell its products in the U.S. market, given that marijuana remains illegal under federal law, despite that 30 states and Washington, D.C. have legalized it in some form. The reason: The U.S. government classifies marijuana as a schedule 1 drug, meaning it’s considered to have no medical value and a high potential for abuse.

That could change, but as this Vox explainer makes clear, a review process for the current schedule would need to be initiated by either the secretary of health and human services or the attorney general, and current Attorney General Jeff Sessions despises marijuana, saying once that “Good people don’t smoke marijuana.”

He seems to be among a dwindling minority. According to a Gallup Poll published last October, 64 percent of Americans favor legalization.

Powered by WPeMatico

Norway-based company Opera Ltd. has filed for an initial public offering in the U.S. According to its F-1 document, the company plans to raise up to $115 million.

In 2017, Opera generated $128.9 million in operating revenue, which led to a net income of $6.1 million.

While many people are already familiar with the web browser Opera, the company itself has had a tumultuous history. Opera shareholders separated the company into two different entities — the browser maker and the adtech operations.

The advertising company is now called Otello. And a consortium of Chinese companies acquired the web browser, the consumer products and the Opera brand. That second part is the one that is going public in the U.S.

Opera currently manages a web browser for desktop computers and a handful of web browsers for mobile phones. On Android, you can download Opera, Opera Mini and Opera Touch. On iOS, you’ll only find Opera Mini. More recently, the company launched a standalone Opera News app.

Overall, Opera currently has around 182 million monthly active users across its mobile products, 57.4 million monthly active users for its desktop browser and 90.2 million users for Opera News in its browsers and standalone app. There’s some overlap across those user bases.

More interestingly, Opera only makes money through three revenue sources. The main one is a deal with two search engines. Yandex is the default search engine in Russia, and Google is the default search engine in the rest of the world. As the company’s user base grows, partners pay more money to remain the default search engine.

“A small number of business partners contribute a significant portion of our revenues,” the company writes in its F-1 document. “In 2017, our top two largest business partners in aggregate contributed approximately 56.1% of our operating revenue, with Google and Yandex accounting for 43.2% and 12.9% of our operating revenue, respectively.”

The rest is ads and licensing deals. You may have noticed that Opera’s speed dial is pre-populated with websites by default, such as Booking.com or eBay. Those are advertising partners. Some phone manufacturers and telecom companies also pre-install Opera browsers on their devices. The company is getting some revenue from that too.

The browser market is highly competitive and Opera is facing tech giants such as Google, Apple and Microsoft. At the same time, people spend so much time in their browser that there is probably enough room for a small browser company like Opera. The company will be listed on NASDAQ under the symbol OPRA.

Powered by WPeMatico

M17 Entertainment, a Taipei-based live streaming and dating app group, priced its IPO this morning on the NYSE and was expected to open trading today according to their final press release. But with just a little more than two hours to go before market closing, it’s still not trading, and no one seems to know why.

An interview I had scheduled with the CEO earlier this afternoon was canceled at the last minute, with the company’s representative saying that M17 couldn’t comment since its shares were not yet actively trading, and thus the company remains under an SEC-mandated quiet period.

M17 has had a rocky non-debut so far. Originally targeting a fundraise of $115 million of American Depository Receipts (shares of foreign companies listed domestically on the NYSE), the company concluded its roadshow raising less than half of its target, for a final investment of $60.1 million. The company priced its ADR shares at $8 each, with each ADR representing 8 shares of the stock’s Class A security.

My colleague Jon Russell has covered the company’s rapid growth over the past three years. It was formed from the merger of dating app company Paktor and live-streaming business 17 Media. Joseph Phua, who was CEO of Paktor, became CEO of the joint M17 company following the merger. Together, the two halves have raised tens of millions in venture capital.

M17 provides live-streaming and dating apps throughout “Developed Asia”

The company’s main product is a live-streaming product where creators can build their fan bases and brands. Fans can purchase virtual gifts to send to their favorite artists, and those points are proving to be extraordinarily lucrative for the company. The company, according to its amended F-1 statement, has seen tremendous revenue growth, netting $37.9 million of revenue in the first three months of this year. The company has also been able to attract more live-streaming talent, increasing its contracted artists from 999 at the end of December 2016 to 7,719 at the end of March this year.

That’s where the good news ends for the company. Despite that revenue growth, operating losses are torrential, with the company losing $24.8 million in the first three months of this year. The company in its statement says that it has $31.4 million in cash and cash equivalents, giving it limited runway to continue operations without a strong IPO debut.

User growth has been mostly stagnant. Active monthly users has increased from 1.5 million to 1.7 million between March 31 of 2017 and 2018. What the company has succeeded in doing is monetizing those users much better. The percentage of users paying on the platform has more than doubled over the same time period, and the value of those users has increased more than 40 percent to $355 per user per month.

The big challenge for M17 is revenue quality. Live streaming represents 91.4 percent of the company’s revenues, but those revenues are concentrated on a handful of “whales” who buy a freakishly high number of virtual gifts. The company’s top 10 users represent 11.8 percent of all revenues (that’s $447,220 per user in the first three months this year!), and its top 500 users accounted for almost a majority of total revenues. That concentration on the demand side is just as heavy on the supply side. M17’s top 100 artists accounted for more than a third of the company’s revenue.

That concentration has improved over the past few months, according to the company’s filing. But Wall Street investors have learned after Zynga and other whale-based revenue models that the sustainability of these businesses can be tough.

Finally, one complication for many investors wary of the increasing use of dual-class stock issues is the governance of the company. Phua, the CEO, will have 56.3 percent of the voting rights of the company, and M17 will be a controlled company under NYSE rules according to the company’s amended filing. Class B shares vote at a 20:1 ratio with Class A share voting rights.

All of this is to say that while the company has had some dizzying growth in its revenue numbers over the past 24 months, that success is moderated by some significant challenges in revenue concentration that will have to be a top priority for M17 going forward. Why the company priced and hasn’t traded remains a mystery, and we have reached out for more comments.

Powered by WPeMatico

After their long post-financial-crisis slump, European tech IPOs are starting to rebound. Tech companies raised more money on European public markets between 2015-17 (€5.3 billion) than in the previous seven years combined. With venture capital having boomed in that time, that trend is set to continue: There is a generation of well-funded, fast-growing technology companies now eyeing the public markets as the platform for continued rapid growth. The pipeline is healthy. But what needs to be done to get ready for an IPO and, crucially, what comes next?

Money raised and market opportunity alone do not make for a public-company-in-waiting. You do not transform from a scrappy growth business into a tightly governed, transparent public company overnight. It has to be a gradual evolution, one which requires the right people, structures and mindset to be in place. Companies need to ask themselves not just if they want to pursue an IPO, but how exactly they plan to go about it, and how they will prepare for the realities of life as a public company.

Having advised three companies on their journey to an IPO, across three different geographies, I think there should be at least two years of careful planning between deciding to seek a listing and hearing the bell ring on your market open.

You have to start with bringing in the right people. A business can grow a long way on the back of an inspirational founding team, but as an aspiring public company, you need an experienced and high-performing management team as well. Do you have a CFO who has credibility with public market investors? Does the board have enough members with independent authority; will it meet the requirements of those institutional investors who now require a minimum quota of female directors?

Ultimately it comes down to one question: Can you start operating like a public company before you become one?

Your board will have to grow, not least to fulfill necessary governance functions, from audit to compensation and nomination committees. These are important and often complex hires, which can take anything from six months to a year to put in place. It also takes a while for new board members to start working well together and gain a detailed understanding of the company.

The composition of the board is just one area where a private company has to start asking itself new questions as it prepares for a listing. Another is the financial profile of the business and the trade-off between growth and profitability. Will investors give us credit for growing, say, 80 percent year over year? Should we front-load investments and associated losses, or incur them over time when required? The CEO also must think about how she is going to communicate with the market, and whether she needs others around her to give investors the full package. A very visionary and product-focused CEO, for example, will need to be complemented by a brilliant CFO who can handle detailed questions about the company’s finances.

A company thinking about going public also needs to evolve its mindset. After an IPO, you will no longer be a tight-knit group of founders, early hires and investors who know the business intimately. The relationship you have known with your private backers is going to bear no relation to the one you will experience with public market investors. As a public company, you are no longer being supportively cheered on, but independently scrutinized by investors who understand the business in less detail and are liable to react strongly to indicators whose significance they can easily misinterpret. In this environment, if you set an ambitious target, you can’t achieve only 95 percent of it and expect to be consoled and encouraged. Institutional investors are going to want to know why you didn’t exceed that target, let alone failed to meet it.

Ultimately it comes down to one question: Can you start operating like a public company before you become one? The companies that succeed post-IPO are those that have laid the foundation to make the transition from private to public as seamless as possible. There are rich rewards to be enjoyed on the public markets, but only for those who do the hard work in advance to ease into life as a public company. Europe’s fast-growing tech companies should consider not just whether an IPO is the right option for them, but if they are willing to put in the work that is necessary to make it a success.

Powered by WPeMatico

Airbnb brings in billions of dollars of revenue annually and is profitable on an EBITDA basis, so many wonder if and when the home-sharing company will go public. At the Code Conference today, Airbnb CEO Brian Chesky said the company will “be ready to IPO next year, but I don’t know if we will.”

He added that he wants to make sure it’s a major benefit to the company when Airbnb does go public. Following some more probing, Chesky said he has “no issues with [going public] at all. It could happen.”

Meanwhile, Airbnb has been struggling from a regulatory standpoint since at least 2010. Specifically, San Francisco and New York are two of the most difficult cities from a regulatory standpoint, Chesky said.

In New York, for example, there has been a standstill since 2010. At this point, Chesky said he expects it to take a few more years to overcome the challenge in New York.

“It doesn’t seem like the end is in sight with that challenge,” Chesky said. That challenge, Chesky said, involves the hotel industry and unions that “have galvanized people in these perpetual battles.”

Another general critique of Airbnb is its effect on rising rent costs and displacement. Chesky added that if it was simply a business decision, “it probably wouldn’t be worth it to stay there” in New York. But Chesky said there are hosts who have come to rely on Airbnb to earn income.

At Code, Chesky also touted Airbnb’s experiences product and how it’s growing 10x faster than its homes product. Airbnb Experiences sees 1.5 million bookings a year, Chesky said. Experiences, which Airbnb started testing in 2014 and officially launched in 2016, is Airbnb’s product that helps travelers find things to do in cities throughout the world.

When it first launched, Airbnb didn’t verify the experiences, but after some bad experiences, Airbnb has started verifying them.

“They’re doing incredibly well,” Chesky said. He added that the “experience economy” is growing and “there will probably be a massive economy around experiences.”

Powered by WPeMatico