initial public offering

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We are back, as promised. Kate Clark and Alex Wilhelm re-convened today to discuss the latest from the Uber IPO. Namely that it opened down, and then kept falling.

A few questions spring to mind. Why did Uber lose ground? Was it the company’s fault? Was it simply the macro market? Was it something else altogether? What we do know is that Uber’s pricing wasn’t what we were expecting and its first day was not smooth.

There are a whole bunch of reasons why Uber went out the way it did. Firstly, the stock market has had a rough week. That, coupled with rising U.S.-China tensions made this week one of the worst of the year for Uber’s monstrous IPO.

But, to make all that clear, we ran back through some history, recalled some key Lyft stats, and more.

We don’t know what’s next but we will be keeping a close watch, specifically on the next cohort of unicorn companies ready to IPO (Postmates, hi!).

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

With news that the We Company (formerly known as WeWork) has officially filed to go public confidentially with the SEC today, there’s a big question on everyone’s mind: Is this the next massive startup win or a house of cards waiting to be toppled by the glare of the public markets?

No company I follow has as much polarized opinion as the We Company. And while the company will have to reveal at least some of its hand in its official S-1, my guess is that the polarization around the company will not be alleviated until well after it goes public, if ever.

The challenge with understanding its business is how much the details of each of its leases, real estate markets and tenants matter to its bottom line. We already know the top line numbers: the company had revenue of $1.8 billion in 2018, and a net loss of $1.9 billion that year. That led to the received opinion that the company has an extraordinarily weak business. As Crunchbase News editor Alex Wilhelm put it:

Powered by WPeMatico

WeWork, the co-working giant now known as The We Company, has submitted confidential documents to the U.S. Securities and Exchange Commission for an initial public offering, the company confirmed in a press release Monday.

According to The New York Times, the business initially filed IPO paperwork in December.

WeWork, valued at $47 billion in January, has raised $8.4 billion in a combination of debt and equity funding since it was founded by Adam Neumann and Miguel McKelvey in 2010. WeWork is among several tech unicorns with hundreds of millions, billions actually, in backing from the SoftBank Vision Fund. Recently, the Japanese telecom giant eyed a majority stake in the company worth $16 billion, but cooled their jets at the last minute.

WeWork doubled its revenue from $886 million in 2017 to roughly $1.8 billion in 2018, with net losses hitting a staggering $1.9 billion. These aren’t attractive metrics for a pre-IPO business; then again, Uber’s currently completing a closely watched IPO roadshow despite shrinking growth. Here’s more from Crunchbase News on WeWork’s top line financials:

On the bright side, per Axios, WeWork established a 90 percent occupancy rate in 2018, with total membership rising 116 percent to 401,000.

WeWork is often referenced as the perfect example of Silicon Valley’s tendency to inflate valuations. WeWork, a real estate business, burns through cash rapidly and will undoubtedly have to work hard to convince public markets investors of its longevity, as well as its status as a tech company.

WeWork is backed by SoftBank, Benchmark, T. Rowe Price, Fidelity, Goldman Sachs and several others.

Powered by WPeMatico

Fastly, the content delivery network that’s raised $219 million in financing from investors (according to Crunchbase), is ready for its close up in the public markets.

The eight-year-old company is one of several businesses that improve the download time and delivery of different websites to internet browsers and it has just filed for an IPO.

Media companies like The New York Times use Fastly to cache their homepages, media and articles on Fastly’s servers so that when somebody wants to browse the Times online, Fastly’s servers can send it directly to the browser. In some cases, Fastly serves up to 90 percent of browser requests.

E-commerce companies like Stripe and Ticketmaster are also big users of the service. They appreciate Fastly because its network of servers enable faster load times — sometimes as quickly as 20 or 30 milliseconds, according to the company.

The company raised its last round of financing roughly nine months ago, a $40 million investment that Fastly said would be the last before a public offering.

True to its word, the company is hoping public markets have the appetite to feast on yet another “unicorn” business.

While Fastly lacks the sizzle of companies like Zoom, Pinterest or Lyft, its technology enables a huge portion of the activities in which consumers engage online, and it could be a bellwether for competitors like Cloudflare, which recently raised $150 million and was also exploring a public listing.

The company’s public filing has a placeholder amount of $100 million, but given the amount of funding the company has received, it’s far more likely to seek closer to $1 billion when it finally prices its shares.

Fastly reported revenue of roughly $145 million in 2018, compared to $105 million in 2017, and its losses declined year on year to $29 million, down from $31 million in the year-ago period. So its losses are shrinking, its revenue is growing (albeit slowly) and its cost of revenues are rising from $46 million to around $65 million over the same period.

That’s not a great number for the company, but it’s offset by the amount of money that the company’s getting from its customers. Fastly breaks out that number in its dollar-based net expansion rate figure, which grew 132 percent in 2018.

It’s an encouraging number, but as the company notes in its prospectus, it’s got an increasing number of challenges from new and legacy vendors in the content delivery network space.

The market for cloud computing platforms, particularly enterprise-grade products, “is highly fragmented, competitive and constantly evolving,” the company said in its prospectus. “With the introduction of new technologies and market entrants, we expect that the competitive environment in which we compete will remain intense going forward. Legacy CDNs, such as Akamai, Limelight, EdgeCast (part of Verizon Digital Media), Level3, and Imperva, and small business-focused CDNs, such as Cloudflare, InStart, StackPath, and Section.io, offer products that compete with ours. We also compete with cloud providers who are starting to offer compute functionality at the edge like Amazon’s CloudFront, AWS Lambda, and Google Cloud Platform.”

Powered by WPeMatico

Zoom, a relatively under-the-radar tech unicorn, has defied expectations with its initial public offering. The video conferencing business priced its IPO above its planned range on Wednesday, confirming plans to sell shares of its Nasdaq stock, titled “ZM,” at $36 apiece, CNBC reports.

The company initially planned to price its shares at between $28 and $32 per share, but following big demand for a piece of a profitable tech business, Zoom increased expectations, announcing plans to sell shares at between $33 and $35 apiece.

The offering gives Zoom an initial market cap of roughly $9 billion, or nine times that of its most recent private market valuation.

Zoom plans to sell 9,911,434 shares of Class A common stock in the listing, to bring in about $350 million in new capital.

If you haven’t had the chance to dive into Zoom’s IPO prospectus, here’s a quick run-down of its financials:

Zoom is backed by Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent); Digital Mobile Venture, a fund affiliated with former Zoom board member Samuel Chen (8.5 percent); and Bucantini Enterprises Limited (5.9 percent), a fund owned by Chinese billionaire Li Ka-shing.

Zoom will debut on the Nasdaq the same day Pinterest will go public on the NYSE. Pinterest, for its part, has priced its shares above its planned range, per The Wall Street Journal.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

It’s time for another Equity Shot, a quick-take episode centered around a breaking news event. This time, as you already guessed, Kate Clark and I sat down to dig into the Uber S-1. It’s a huge, complex document, but we did our best to summarize what’s inside.

First, we talked through yearly results, looking back a half-decade into Uber’s revenue growth. In the filing, Uber reported 2018 revenues of $11.27 billion, net income of $997 million and adjusted EBITDA losses of $1.85 million. We highlighted those numbers, talked about operating losses and the company’s gyrating net results that included the positive impacts of various divestitures.

Yes, this S-1 required a bit more unpacking than most. We apologize for the frantic scrolling, we were pouring through the document live and we were a bit excited. This is an IPO that’s been talked about for years and will be easily one of the largest floats of all time.

Anyway, an S-1 brings insights to more than just a company’s financials, so we spent time highlighting key stakeholders, or, in other words, the people are are going to get really really really rich off Uber’s IPO. That includes Uber co-founder and chief executive officer Travis Kalanick, famous venture capital firms like the SoftBank Vision Fund and Benchmark, and more.

The IPO, remember, is expected to sell $10 billion in stock (primary and secondary) and value the company at $100 billion or more.

If 30 minutes digging through the S-1 wasn’t enough for you, don’t fret, we’ll be following the Uber IPO for weeks — probably months — to come.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Zoom, the only profitable unicorn in line to go public, priced its initial public offering at between $28 and $32 per share Monday morning. The video conferencing business plans to trade on the Nasdaq under the ticker symbol “ZM.”

Zoom, valued at $1 billion in 2017, initially filed to go public in March. According to its amended IPO filing, the company will raise up to $348.1 million by selling 10.9 million Class A shares. The offering will grant Zoom a fully diluted market value of $8.7 billion, a more than 8x increase to its latest private market valuation.

Although the company has garnered praise for its stellar financials — Zoom posted $330 million in revenue in the year ending January 31, 2019, a remarkable 2x increase year-over-year, with a gross profit of $269.5 million — the road to IPO hasn’t been without hiccups.

The company’s founder and chief executive officer Eric Yuan last night published an open letter concerning the conduct of Zoom’s chief financial officer Kelly Steckelberg. According to the letter, Zoom was recently informed by an anonymous source that Steckelberg had an “undisclosed, consensual relationship” during her tenure at a previous employer.

Steckelberg was most recently the CEO of the online dating site Zoosk; before that, she was a senior director in consumer finance at Cisco . The letter does not specify where the relationship took place, when or with whom.

Losing a CFO mere days before an IPO would have been a major loss for Zoom. CFOs often become the face of the IPO, handling the grueling tasks associated with crafting an IPO prospectus, leading the roadshow and more, while also maintaining day-to-day financial operations.

Yuan writes that the Zoom’s board of directors conducted a full investigation into the matter and determined that Steckelberg would stay on as Zoom’s CFO: “Kelly expressed regret for what transpired at her former employer, took ownership for the situation, and made clear to us that she had learned valuable lessons from the experience,” he wrote.

“We appreciated Kelly’s openness and candor during this process,” he continued. “It is clear that this matter related only to circumstances at her former employer. During Kelly’s tenure at Zoom, she has been an incredible contributor, as well as a model steward of our culture, values, and high standards since joining the Company.”

We reached out to Zoosk for comment. Zoom declined to comment further.

Zoom, expected to make the final call on its IPO price next Wednesday, will likely price at the top of the range and see a clean pop on its first day on the markets given its clean track record and positive financials. The business was founded in 2011 by Eric Yuan, an early engineer at WebEx, which sold to Cisco for $3.2 billion in 2007. Before launching Zoom, he spent four years at Cisco as its vice president of engineering.

Zoom has raised $145 million to date from investors, including Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent pre-IPO stake); Digital Mobile Venture (8.5 percent), a fund affiliated with former Zoom board member Samuel Chen; and Bucantini Enterprises Limited (5.9 percent), a fund owned by Li Ka-shing, a Chinese billionaire and among the richest people in the world.

Morgan Stanley, JP Morgan and Goldman Sachs are leading its offering.

Powered by WPeMatico

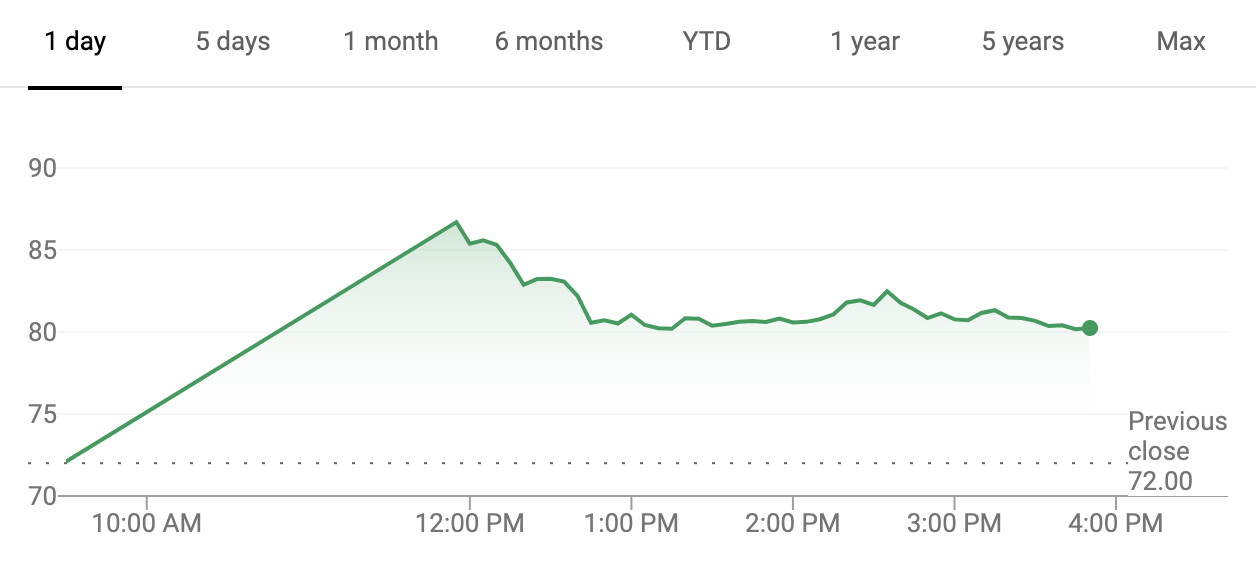

Pink confetti fell from the ceiling Friday as Lyft co-founders Logan Green and John Zimmer celebrated their company’s IPO. The stock offering was a bona fide success, with shares selling for $87.24 apiece Friday morning — 21 percent higher than Lyft’s initial $72 share price — and closing at $78.29 per share.

Lyft raised roughly $2.3 billion Thursday evening, hours before ringing the opening bell of the Nasdaq on Friday around noon Pacific. The IPO gave Lyft an initial market cap of about $24 billion, representing an 11x revenue multiple and a 1.6x step-up from its most recent private valuation of $15.1 billion.

On Bloomberg TV, Lyft’s co-founders discussed the company’s long-term prospects, including international growth, autonomous vehicle plans, the future of car ownership and insurance.

“We are confident that the business will be very profitable,” Green told Emily Chang. “We are making tremendous progress going after this once-in-a-generation shift where this entire industry, a $1.2 trillion market, could flip from an ownership model to a service model and we are leading the way there.”

The pair opted to host their IPO in Los Angeles, Lyft’s largest market.

“We want to make a point that you can both invest in communities and build a great business,” Zimmer said. “It was fun to ring the bell with several members of our driver community and have many of them participate in our IPO because we gave them a bonus to do so.”

Powered by WPeMatico

Lyft raised more than $2 billion Thursday afternoon after pricing its shares at $72 apiece, the top of the expected range of $70 to $72 per share. This gives Lyft a fully diluted market value of $24 billion.

The company will debut on the Nasdaq stock exchange Friday morning, trading under the ticker symbol “LYFT.”

The initial public offering is the first-ever for a ride-hailing business and represents a landmark liquidity event for private market investors, which had invested billions of dollars in the San Francisco-based company. In total, Lyft had raised $5.1 billion in debt and equity funding, reaching a valuation of $15.1 billion last year.

Lyft’s blockbuster IPO is unique for a number of reasons, in addition to being amongst transportation-as-a-service companies to transition from private to public. Lyft has the largest net losses of any pre-IPO business, posting losses of $911 million on revenues of $2.2 billion in 2018. However, the company is also raking in the largest revenues, behind only Google and Facebook, for a pre-IPO company. The latter has made it popular on Wall Street, garnering buy ratings from analysts prior to pricing.

Uber is the next tech unicorn, or company valued north of $1 billion, expected out of the IPO gate. It will trade on the New York Stock Exchange in what is one of the most anticipated IPOs in history. The company, which reported $3 billion in Q4 2018 revenues with net losses of $865 million, is reportedly planning to unveil its IPO prospectus next month.

Next in the pipeline is Pinterest, which dropped its S-1 last week and revealed a path to profitability that is sure to garner support from Wall Street investors. The visual search engine will trade on the NYSE under the symbol “PINS.” It posted revenue of $755.9 million last year, up from $472.8 million in 2017. The company’s net loss, meanwhile, shrank to $62.9 million last year from $130 million in 2017.

Other notable companies planning 2019 stock offerings include Slack, Zoom — a rare, profitable pre-IPO unicorn — and, potentially, Airbnb.

Updating.

Powered by WPeMatico

Direct-to-consumer mattress business Casper has secured a $100 million Series D investment from existing investors Target, NEA, IVP and Norwest Venture Partners.

The fresh infusion of capital values Casper at $1.1 billion, Bloomberg first reported and Casper confirmed.

“We are in the very early chapters of our growth story as demand for Casper products continues to expand across the globe,” Casper chief executive officer and co-founder Philip Krim said in a statement. “Today’s financing accelerates Casper’s vision to become the world’s largest end-to-end sleep company. Our growth will continue to be catalyzed by state-of-the-art sleep products, best-in-class customer experiences, and world-class leadership.”

Casper posted $373 million in net revenue in 2018, according to leaked financials published by The Information this week. In a press release issued today, however, Casper said 2018 revenue topped $400 million. The company, of course, isn’t profitable, with losses reaching $64 million last year, again per The Information. According to Casper’s projections, it will become profitable on an EBITDA basis in 2019 and is expecting revenues of $556 million this year.

Casper has previously raised $240 million in equity funding from celebrity investors Leonardo DiCaprio and 50 Cent, as well as institutional investors, including Lerer Hippeau .

Founded in 2014, the New York business will use the latest investment to expand overseas and open additional brick-and-mortar stores. Competing with other well-funded startups in the business of sleep, like the publicly traded Purple and the VC-backed Leesa Sleep, Casper has taken to physical retail to augment its following. The company opened its first store in New York City in 2018 and has detailed additional plans to open another 200 stores.

An initial public offering is likely the next step for the sleep products retailer, which sells pillows and an $89 sleep-friendly light, in addition to mattresses. Per a recent Reuters report, Casper is in the process of hiring underwriters for its IPO.

Powered by WPeMatico