harvard

Auto Added by WPeMatico

Auto Added by WPeMatico

Labster, a virtual science lab edtech company, today announced that it is partnering with California’s community college network to bring its software to 2.1 million students.

California Community Colleges claims to be the largest system of higher education in the country. The Labster partnership will provide 115 schools with 130 virtual laboratory simulations in biology, chemistry, physics and general sciences.

As COVID-19 has forced schools to shutter, edtech companies have largely responded by offering their software for free or through extended free trials. What’s new and notable about Labster’s partnership today is that it shows the first few signs of how that momentum can lead to a business deal.

Based in Copenhagen, Labster sells virtual STEM labs to institutions. The startup has raised $34.7 million in known venture capital to date, according to Crunchbase data. Labster customers include California State University, Harvard, Gwinnett Technical College, MIT, Trinity College and Stanford.

Lab equipment is expensive, and budget constraints mean that schools struggle to afford the latest technology. So Labster’s value proposition is that it is a cheaper alternative (plus, if students spill a testing vial in a virtual lab, there’s less clean up).

That pitch has slightly changed since COVID-19 forced schools across the world to shut down to limit the spread of the pandemic. Now, it’s pitching itself as the only currently viable alternative to science labs.

For many edtech companies, the surge of remote learning has been a large experiment. Often, edtech companies are giving away their product and technology for free to help as schools scramble to move operations completely digital.

For example, last week self-serve learning platforms Codecademy, Duolingo, Quizlet, Skillshare and Brainly launched a Learn From Home Club for students and teachers. Before that, Wize made its exam content and homework services available for free. And Zoom offered its video-conferencing software for free to K through 12 schools, which had mixed results.

Labster itself gave $5 million in free Labster credits to schools across the country. The list continues.

Labster’s new deal shows edtech companies can secure new customers right now — without breaking the bank.

Labster CEO and co-founder Michael Bodekaer declined to give specifics on what the deal is worth. He did share that Labster works with schools one by one to understand how much they can, or want to, invest in teacher training and webinar support. He also confirmed that Labster does profit from the deal.

“We want to make sure that we set ourselves up for supporting our partners but still also make sure that Labster as a financial institution can pay our salaries,” Bodekaer said. “But again, heavy discounts that help us cover our costs.”

The long game for Labster, like many edtech companies, is that schools like the platform so much that these short-term stints have a better chance to lead to long-term relationships.

“We’ll be keeping these discounts as long as we possibly can sustain as a company,” he said. “It looks like initially the discount was until August and now we’re extending it until the end of the year. If that continues, we may extend it even further.”

Pricing aside, the real struggle toward implementation for Labster, and honestly any other edtech company focused on remote learning, is the digital divide. Some students do not have access to a computer for video conferencing or even internet connection for assignments.

The COVID-19 pandemic has highlighted how many households across America lack access to the technology needed for remote learning. In California, Google donated free Chromebooks and 100,000 mobile hotspots to students in need.

Bodekaer said that Labster is currently working on providing its software on mobile, and has worked with Google to make sure its product works on low-end computers like Chromebooks.

“We really want to be hardware agnostic and support any system or any platform that the students already have,” he said. “So that hardware does not become a barrier.”

While today’s partnership brings 2.1 million students access to Labster’s technology, it does not directly account for the percentage of that same group that might not have access to a computer in the first place. The true test, and perhaps success, of edtech will rely on a true hybrid of hardware and software, not one or the other.

Powered by WPeMatico

Climate risk, including extreme events and the related pressures our environment, are fundamentally affecting the way businesses and governments operate — both tactically and strategically. Increasing climate volatility is causing food supply disruptions and increasing pressure on Enterprises (including financial institutions, insurers and producers) to disclose what’s going on.

The trouble is, while there is a lot of data about all this, its complexity, incompleteness and sheer volume is too vast for humans to process with the tools available today. So just as the climate changes, we are faced with “data chaos.” Equally, other parts of the world suffer from data scarcity, making it much harder to provide useful and timely analysis.

So the challenge is to address these issues simultaneously. So a new startup, Cervest, has created an AI-driven platform designed to inform the decision-making capabilities of businesses, governments and growers in the face of increasing climate volatility.

Cervest, has now closed a £3.7 million investment round to fund the launch of its real-time, climate forecasting platform.

The round was led by deep-tech investor Future Positive Capital, with co-investor Astanor Ventures . The seed-stage funding round brings the company’s total funding to more than £4.5 million.

Built on three years of research and development by a team of scientists, mathematicians, developers and engineers, Cervest says its Earth Science AI platform can analyze billions of data points to forecast how changes in the climate will impact the future of entire countries, right down to individual landscapes.

It does this by combining research and modeling techniques taken from proven Earth sciences — including atmospheric science, meteorology, hydrology and agronomy — with artificial intelligence, imaging, machine learning and Bayesian statistics.

Using large collections of satellite imagery and probability theory, the platform can identify signals, or early-warning signs, of extreme events such as floods, fires and strong winds. It also can spot changes in soil health and identify water risk.

Cervest says the platform could do such things as reveal the optimum location to build a new factory; warn a wheat grower that their crop yield isn’t expected to meet its targets; or be used by insurers to help them set premiums for the next 12 months.

The team comes from a network of more than 30 universities, including Imperial College, The Alan Turing Institute, Cambridge, UCL, Harvard and Oxford, and has published more than 60 peer-reviewed scientific papers.

A beta version of the platform is due to launch in Q1 2020.

Iggy Bassi, founder & CEO, Cervest said: “Our goal is to empower everyone to make informed decisions that improve the long-term resilience of our planet. Today decision-makers are struggling with climate uncertainty and extreme events and how they are affecting their business operations, assets, investments, or policy choices.”

Sofia Hmich, founder, Future Positive Capital said: “With reports suggesting we have fewer than 60 years of farming left unless drastic action is taken, the need for science-backed decisions could not be greater. Businesses and policymakers hold the key to change and with access to Cervest’s proprietary AI technology they can start to make that change a reality at low cost — before it’s too late.”

Bassi previously ran the impact-led agribusiness GADCO, which was supported by Acumen Fund, Soros, Gates Foundation, World Bank and Syngenta . Its impact was featured in UNDP, World Economic Forum, FT, The Guardian and Huff Post. He previously built a software company focused on data analytics.

Cervest was inspired by Bassi’s experience building a farm-to-market agribusiness whilst confronting first-hand the impacts of climate and natural resource volatilities.

The Cervest team includes eight scientists and four PhDs. Between them, they have published more than 60 peer-reviewed scientific papers with more than 3,000 citations in high-profile titles, including Nature, Proceedings of the National Academy of Sciences and The Royal Statistical Society.

Powered by WPeMatico

As biotechnology becomes more central to new innovations in healthcare, material science and manufacturing, one of the nation’s research hubs is getting a new accelerator called Petri to launch companies focused on the commercialization of new technologies.

Backed by the Boston-based venture capital firm Pillar, Petri has a three-year $15 million commitment to back companies developing new biotech applications in food, healthcare, industrial chemicals and new materials — along with the enabling technologies to bring these products to market.

“We’re at the inflection point where these technologies will impact and continue to impact health but will also impact food, agriculture, chemicals and materials,” says Petri co-founder, Tony Kulesa. “Everything we touch has some element of biology.”

Pillar has already invested in a couple of companies that show the potential promise of new biotech research coming from Boston-based universities, like Boston University, Harvard and the Massachusetts Institute of Technology.

Asimov,io, a company that has set an ultimate goal of designing new genomes for industrial applications, was co-founded by graduates from Boston University and MIT, and is a part of the Pillar portfolio. PathAi, a company working on enabling technologies for computational biology, also counts an MIT grad as a co-founder. Meanwhile, Harvard’s George Church has been instrumental in the development of a number of biotech companies working at the frontier of genetic applications for healthcare and manufacturing.

As an instructor at MIT, Kulesa spent seven years at MIT watching, in his words, how engineering has transformed biology. “It became clear to me that these technologies need to get out in the world,” he said.

Joining Kulesa as a managing director is Brian Baynes, a serial entrepreneur who founded Midori Health, an animal nutrition startup; Kaleido Biosciences, a microbiome control focused company; Celexion, a protein engineering and synthetic biology company; and Codon Devices, a synthetic biology toolkit company which was sold to Ginkgo Bioworks .

Over time, Kulesa and Baynes expect to have 10 to 20 companies in each cohort as the program expands. In addition to checks of at least $250,000 the Petri accelerator has lab and office space available for each company.

The companies also could benefit from potential partnerships with companies like Ginkgo Bioworks, which happens to share office space in the same building, and with the accelerator’s clutch of big-name advisors and “co-founders” recruited from across the life sciences industry.

These co-founders, who collectively hold a double-digit equity stake in Petri’s accelerator, include Reshma Shetty, from Ginkgo Bioworks; Emily Leproust of Twist Bioscience; Stan Lapidus, who was at Exact Sciences and Cytyc; Daphne Koller, the co-founder and chief executive of Insitro; Alec Nielsen, the founder Asimov; and researchers Chris Voigt of MIT and Pam Silver and George Church from Harvard’s Wyss Institute.

Genetically engineered organisms are finding their way into everything from food to fuel to chemistry. Companies like Impossible Foods, which uses genetically modified soy product, has raised hundreds of millions for its protein replacement, while Solugen, a manufacturer of chemicals using genetically modified organisms, has raised tens of millions to commercialize its technology. And Ginkgo Bioworks has raised nearly half a billion dollars to pursue applications for industrial biology.

Powered by WPeMatico

Much of Silicon Valley mythology is centered on the founder-as-hero narrative. But historically, scientific founders leading the charge for bio companies have been far less common.

Developing new drugs is slow, risky and expensive. Big clinical failures are all too common. As such, bio requires incredibly specialized knowledge and experience. But at the same time, the potential for value creation is enormous today more than ever with breakthrough new medicines like engineered cell, gene and digital therapies.

What these breakthroughs are bringing along with them are entirely new models — of founders, of company creation, of the businesses themselves — that will require scientists, entrepreneurs and investors to reimagine and reinvent how they create bio companies.

In the past, biotech VC firms handled this combination of specialized knowledge + binary risk + outsized opportunity with a unique “company creation” model. In this model, there are scientific founders, yes; but the VC firm essentially founded and built the company itself — all the way from matching a scientific advance with an unmet medical need, to licensing IP, to having partners take on key roles such as CEO in the early stages, to then recruiting a seasoned management team to execute on the vision.

Image: PASIEKA/SCIENCE PHOTO LIBRARY/Getty Images

You could call this the startup equivalent of being born and bred in captivity — where great care and feeding early in life helps ensure that the company is able to thrive. Here the scientific founders tend to play more of an advisory role (usually keeping day jobs in academia to create new knowledge and frontiers), while experienced “drug hunters” operate the machinery of bringing new discoveries to the patient’s bedside. This model’s core purpose is to bring the right expertise to the table to de-risk these incredibly challenging enterprises — nobody is born knowing how to make a medicine.

But the ecosystem this model evolved from is evolving itself. Emerging fields like computational biology and biological engineering have created a new breed of founder, native to biology, engineering and computer science, that are already, by definition, the leading experts in their fledgling fields. Their advances are helping change the industry, shifting drug discovery away from a highly bespoke process — where little knowledge carries over from the success or failure of one drug to the next — to a more iterative, building-block approach like engineering.

Take gene therapy: once we learn how to deliver a gene to a specific cell in a given disease, it is significantly more likely we will be able to deliver a different gene to a different cell for another disease. Which means there’s an opportunity not only for novel therapies but also the potential for new business models. Imagine a company that provides gene delivery capability to an entire industry — GaaS: gene-delivery as a service!

Once a founder has an idea, the costs of testing it out have changed too. The days of having to set up an entire lab before you could run your first experiments are gone. In the same way that AWS made starting a tech company vastly faster and easier, innovations like shared lab spaces and wetlab accelerators have dramatically reduced the cost and speed required to get a bio startup off the ground. Today it costs thousands, not millions, for a “killer experiment” that will give a founding team (and investors) early conviction.

What all this amounts to is scientific founders now have the option of launching bio companies without relying on VCs to create them on their behalf. And many are. The new generation of bio companies being launched by these founders are more akin to being born in the wild. It isn’t easy; in fact, it’s a jungle out there, so you need to make mistakes, learn quickly, hone your instincts, and be well-equipped for survival. On the other hand, given the transformative potential of engineering-based bio platforms, the cubs that do survive can grow into lions.

Image via Getty Images / KTSDESIGN/SCIENCE PHOTO LIBRARY

So, which is better for a bio startup today: to be born in the wild — with all the risk and reward that entails — or to be raised in captivity

The “bred in captivity” model promises sureness, safety, security. A VC-created bio company has cache and credibility right off the bat. Launch capital is essentially guaranteed. It attracts all-star scientists, executives and advisors — drawn by the balance of an innovative, agile environment and a well-funded, well-connected support network. I was fortunate enough to be an early executive in one of these companies, giving me the opportunity to work alongside industry luminaries and benefit from their well-versed knowledge of how to build a world-class bio company with all its complex component parts: basic, translational, clinical research, from scratch. But this all comes at a price.

Because it’s a heavy lift for the VCs, scientific founders are usually left with a relatively small slug of equity — even founding CEOs can end up with ~5% ownership. While these companies often launch with headline-grabbing funding rounds of $50m or above, the capital is tranched — meaning money is doled out as planned milestones are achieved. But the problem is, things rarely go according to plan. Tranched capital can be a safety net, but you can get tangled in that net if you miss a milestone.

Being born in the wild, on the other hand, trades safety for freedom. No one is building the company on your behalf; you’re in charge, and you bear the risk. As a recent graduate, I co-founded a company with Harvard geneticist George Church. The company was bootstrapped — a funding strategy that was more famine than feast — but we were at liberty to try new things and run (un)controlled experiments like sequencing heavy metal wildman Ozzy Osbourne.

ozzypic.jpg for post 106294")

It was the early, Wild West days of the genomics revolution and many of the earliest biotech companies mirrored that experience — they weren’t incepted by VCs; they were created by scrappy entrepreneurs and scientists-turned-CEO. Take Joshua Boger, organic chemist and founder of Vertex Pharmaceuticals: starting in 1989 his efforts to will into existence a new way to develop drugs, thrillingly captured in Barry Werth’s The Billion-Dollar Molecule and its sequel The Antidote in all its warts and nail-biting glory, ultimately transformed how we treat HIV, hepatitis C and cystic fibrosis.

Today we’re in a back-to-the-future moment and the industry is being increasingly pushed forward by this new breed of scientist-entrepreneur. Students-turned-founder like Diego Rey of in vitro diagnostics company GeneWEAVE and Ramji Srinivasan of clinical laboratory Counsyl helped transform how we diagnose disease and each led their companies to successful acquisitions by larger rivals.

Popular accelerators like Y Combinator and IndieBio are filled with bio companies driven by this founder phenotype. Ginkgo Bioworks, the first bio company in Y Combinator and today a unicorn, was founded by Jason Kelly and three of his MIT biological engineering classmates, along with former MIT professor and synthetic biology legend Tom Knight. The company is not only innovating new ways to program biology in order to disrupt a broad range of industries, but it’s also pioneering an innovative conglomerate business model it has dubbed the “Berkshire for biotech.”

Like the Ginkgo founders, Alec Nielsen and Raja Srinivas launched their startup Asimov, an ambitious effort to program cells using genetic circuits, shortly after receiving their PhDs in biological engineering from MIT. And, like Boger, renowned machine learning Stanford professor Daphne Koller is working to once again transform drug discovery as the founder and CEO of Instiro.

Just like making a medicine, no one is born knowing how to build a company. But in this new world, these technical founders with deep domain expertise may even be more capable of traversing the idea maze than seasoned operators. Engineering-based platforms have the potential to create entirely new applications with unprecedented productivity, creating opportunities for new breakthroughs, novel business models, and new ways to build bio companies. The well-worn playbooks may be out of date.

Founders that choose to create their own companies still need investors to scrub in and contribute to the arduous labor of company-building — but via support, guidance, and with access to networks instead. And like this new generation of founders, bio investors today need to rethink (and re-value) the promise of the new, and still appreciate the hard-earned wisdom of the old. In other words, bio investors also need to be multidisciplinary. And they need to be comfortable with a different kind of risk: backing an unproven founder in a new, emerging space. As a founder, if you’re willing to take your chances in the wild, you should have an investor that understands you, believes in you, can support you and, importantly, is willing to dream big with you.

Powered by WPeMatico

One of the most-discussed plot twists in recent advertising has been the pivot of Direct-to-Consumer (DTC) brands to linear TV. These data-driven, digital-first players are expanding well beyond Facebook and Instagram—and becoming serious players on the largest traditional medium in advertising.

A January 2019 Video Advertising Bureau study found that in 2018, 120 DTC brands collectively spent over $2 billion in TV ads—up from $1.1 B in 2016. 70 of those 2018 advertisers ran TV ads for the first time.

But while we know that they’re advertising on TV, what may be less discussed is whether they’re succeeding on television—and what strategies they use to achieve their success.

At EDO, we have a unique and differentiated ability to measure how DTC advertisers perform on TV by tracking incremental online searches above baseline in the minutes immediately following individual TV ad airings as viewers translate their interest in advertised brands and products directly into online engagement with them.

By measuring incremental search activity across 60 million national TV ad airings since 2015, we are able to effectively isolate the effects of TV ad placement and creative decisions that are most likely to cause online engagement.

We ran the numbers on DTCs as well as advertisers in various other categories to better understand how DTCs specifically are succeeding in TV ads—and what DTCs who are considering TV advertising can do to achieve success on TV.

The DTC revolution is a quintessential David and Goliath story. In vertical after vertical, small, digital-native upstarts are changing the game and overtaking major brands. Does that story play out on TV as well—or is TV advertising one area where DTC marketers have finally met their match?

To answer that question, EDO looked at how effectively TV ads elicited viewer activity since September 2018 across eight major industry categories including DTC. Guided by historical ad performance across billions of ads, we rated ad performance based on how closely the DTC ads came to meeting the benchmark volume of brand-related online activity in the minutes following each TV ad airing.

We index each industry accordingly—giving an index value of 100 to an ad that meets benchmark standards, and below-par ads getting a score under 100 while higher-scoring ads receive a score over 100. We chose to set our index baseline of 100 to the average Consumer Packaged Good (CPG) ad since it is such a large and broad ad category. Our results are as follows:

Powered by WPeMatico

Tech ethics can mean a lot of different things, but surely one of the most critical, unavoidable, and yet somehow still controversial propositions in the emerging field of ethics in technology is that tech should promote gender equality. But does it? And to the extent it does not, what (and who) needs to change?

In this second of a two-part interview “On The Internet of Women,” Harvard fellow and Logic magazine founder and editor Moira Weigel and I discuss the future of capitalism and its relationship to sex and tech; the place of ambivalence in feminist ethics; and Moira’s personal experiences with #MeToo.

Greg E.: There’s a relationship between technology and feminism, and technology and sexism for that matter. Then there’s a relationship between all of those things and capitalism. One of the underlying themes in your essay “The Internet of Women,” that I thought made it such a kind of, I’d call it a seminal essay, but that would be a silly term to use in this case…

Moira W.: I’ll take it.

Greg E.: One of the reasons I thought your essay should be required reading basic reading in tech ethics is that you argue we need to examine the degree to which sexism is a part of capitalism.

Moira W.: Yes.

Greg E.: Talk about that.

Moira W.: This is a big topic! Where to begin?

Capitalism, the social and economic system that emerged in Europe around the sixteenth century and that we still live under, has a profound relationship to histories of sexism and racism. It’s really important to recognize that sexism and racism themselves are historical phenomena.

They don’t exist in the same way in all places. They take on different forms at different times. I find that very hopeful to recognize, because it means they can change.

It’s really important not to get too pulled into the view that men have always hated women there will always be this war of the sexes that, best case scenario, gets temporarily resolved in the depressing truce of conventional heterosexuality. The conditions we live under are not the only possible conditions—they are not inevitable.

A fundamental Marxist insight is that capitalism necessarily involves exploitation. In order to grow, a company needs to pay people less for their work than that work is worth. Race and gender help make this process of exploitation seem natural.

Image via Getty Images / gremlin

Certain people are naturally inclined to do certain kinds of lower status and lower waged work, and why should anyone be paid much to do what comes naturally? And it just so happens that the kinds of work we value less are seen as more naturally “female.” This isn’t just about caring professions that have been coded female—nursing and teaching and so on, although it does include those.

In fact, the history of computer programming provides one of the best examples. In the early decades, when writing software was seen as rote work and lower status, it was mostly done by women. As Mar Hicks and other historians have shown, as the profession became more prestigious and more lucrative, women were very actively pushed out.

You even see this with specific coding languages. As more women learn, say, Javascript, it becomes seen as feminized—seen as less impressive or valuable than Python, a “softer” skill. This perception, that women have certain natural capacities that should be free or cheap, has a long history that overlaps with the history of capitalism. At some level, it is a byproduct of the rise of wage labor.

To a medieval farmer it would have made no sense to say that when his wife had their children who worked their farm, gave birth to them in labor, killed the chickens and cooked them, or did work around the house, that that wasn’t “work,” [but when he] took the chickens to the market to sell them, that was. Right?

A long line of feminist thinkers has drawn attention to this in different ways. One slogan from the 70s was, ‘whose work produces the worker?’ Women, but neither companies nor the state, who profit from this process, expect to pay for it.

Why am I saying all this? My point is: race and gender have been very useful historically for getting capitalism things for free—and for justifying that process. Of course, they’re also very useful for dividing exploited people against one another. So that a white male worker hates his black coworker, or his leeching wife, rather than his boss.

Greg E.: I want to ask more about this topic and technology; you are a publisher of Logic magazine which is one of the most interesting publications about technology that has come on the scene in the last few years.

Powered by WPeMatico

Aditya and Aarti Kochhar Kaji didn’t set out to start the snack food business Taali Foods when they were studying for their business degrees at Harvard.

The couple both hail from Mumbai and met at the University of Pennsylvania . They were married before starting at Harvard’s Business School and initially were interested in other areas — Aarti was exploring a career in venture capital and Aditya was looking at the food and beverage industry broadly in his classes at Harvard.

Addicted to snack foods like chips and popcorn to fuel her Harvard study sessions, Aarti started making popped water lily seeds as a snack — a food both she and her husband had grown up eating in India, she said.

The seeds, which are high in anti-oxidants and low in fat, have been a staple of Ayurvedic medicine — thanks to their purported anti-inflammatory properties, and are a staple of Indian snacking traditions. Now, with American consumers on the hunt for healthier snacks, they’re becoming a big business in the U.S. as well.

Y Combinator is very on-trend, with its decision to invest and accelerate Taali as part of its most recent cohort of startups. But in this instance you may call the accelerator a fast follower rather than a progenitor of this trend.

No less auspicious a food tastemaker than Whole Foods named water lily seeds as one of the top 10 new food trends of 2019. With that attention, competitors to Taali abound.

Bohana and AshaPops are just two new snack food companies floating on the popped water lily seed movement. Bohana even managed to nab the attention of PepsiCo’s Nutrition Greenhouse competitive accelerator.

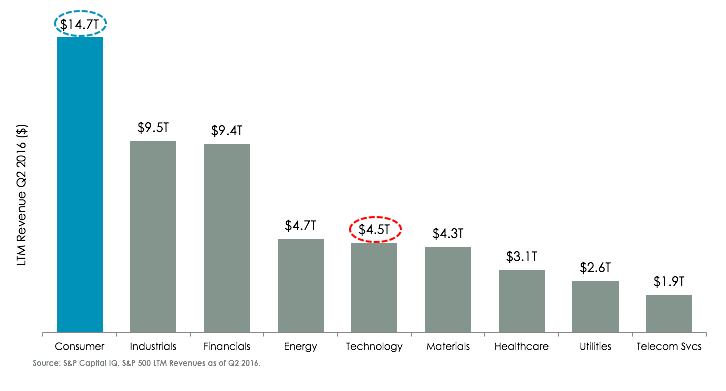

It’s no secret that technology investors are investing more heavily in consumer businesses — everything from snack foods to period products and baby formula — and startups need only point to the success of Amazon as the everything store to show that there’s always money to be made in the category.

Indeed, at $1.47 trillion, the consumer packaged goods industry dwarfs technology as a share of the nation’s economy.

As Ryan Caldbeck, the head of the consumer-focused investment firm CircleUp noted last year:

The uptick in tech VC dollars going to the CPG market is partly because tech investing is brutally competitive and saturated, and largely because these VCs are awakening to the strong historical returns in CPG, especially with the trend leaning towards small brands stealing market share.

Consumer is a massive market – about 3x the size of tech, as seen below.

Despite the size of the market, the early-stage has historically been underserved by investors due to market inefficiencies like the geographic dispersion of brands and a lack of structured information sources (i.e. there is no Silicon Valley for consumer, and certainly no Crunchbase equivalents – yet).

Strong exits are already possible for consumer brands — and not necessarily from the big-ticket, headline grabbing acquisitions like Dollar Shave Club. Last week This is L. — the condom and period product retailer — sold for roughly $100 million after raising seed funding from investors, including 500 Startups and Y Combinator.

Taali was similarly bootstrapped before it was accepted into Y Combinator. The company is already selling its snacks through Amazon and in retail locations like Fairway in New York and Central Market in Texas. The founders expect to be in stores in California in the next few months.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

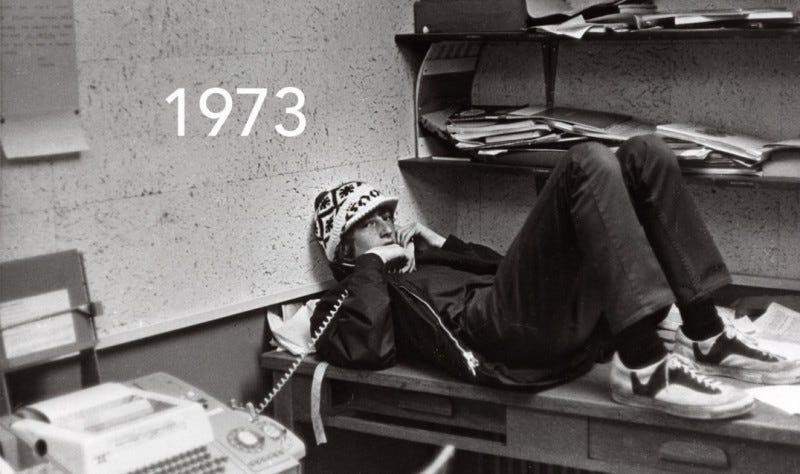

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

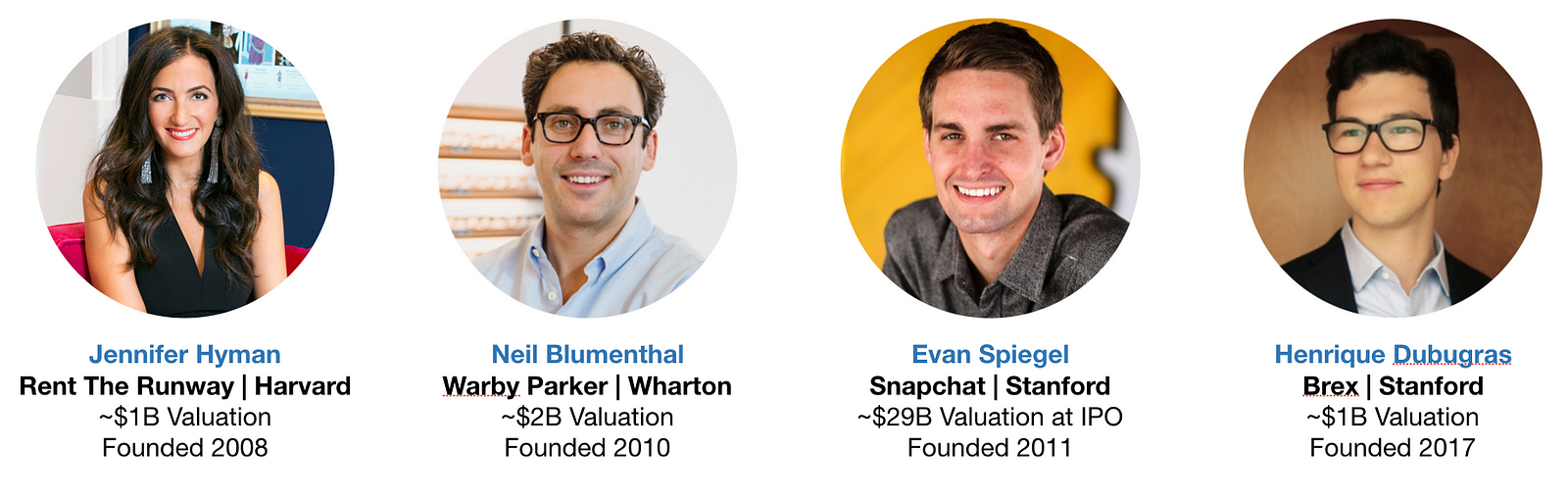

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

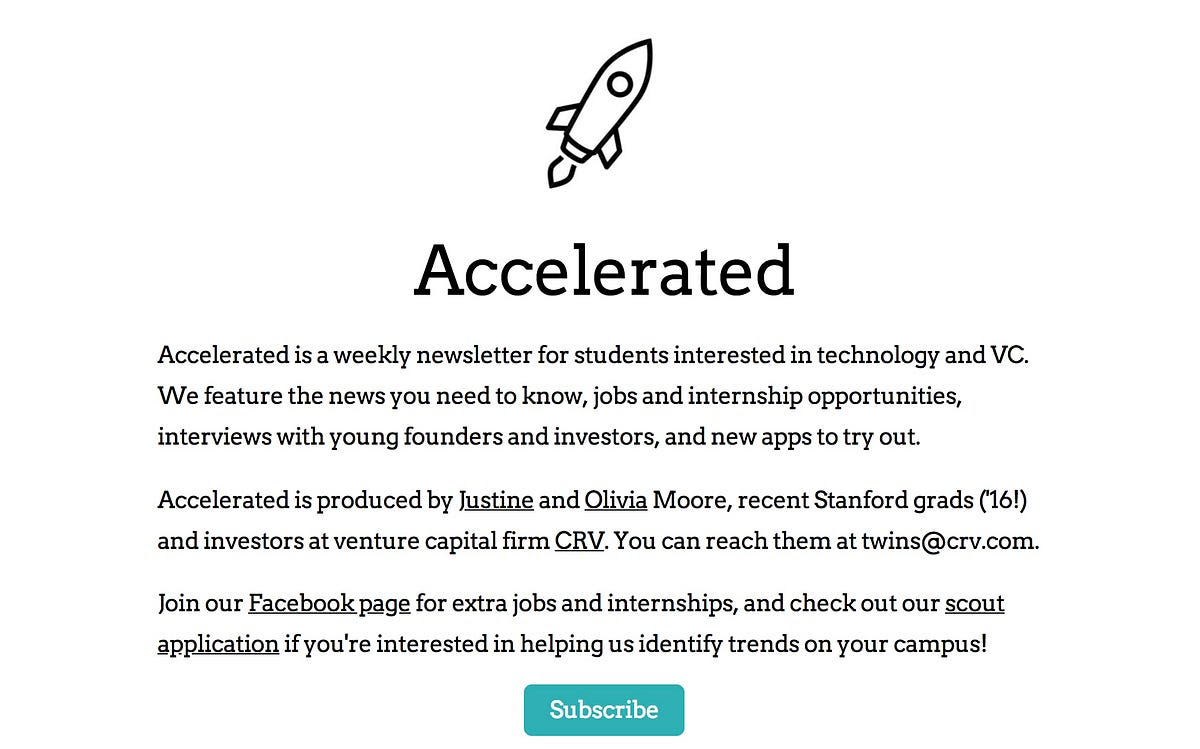

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

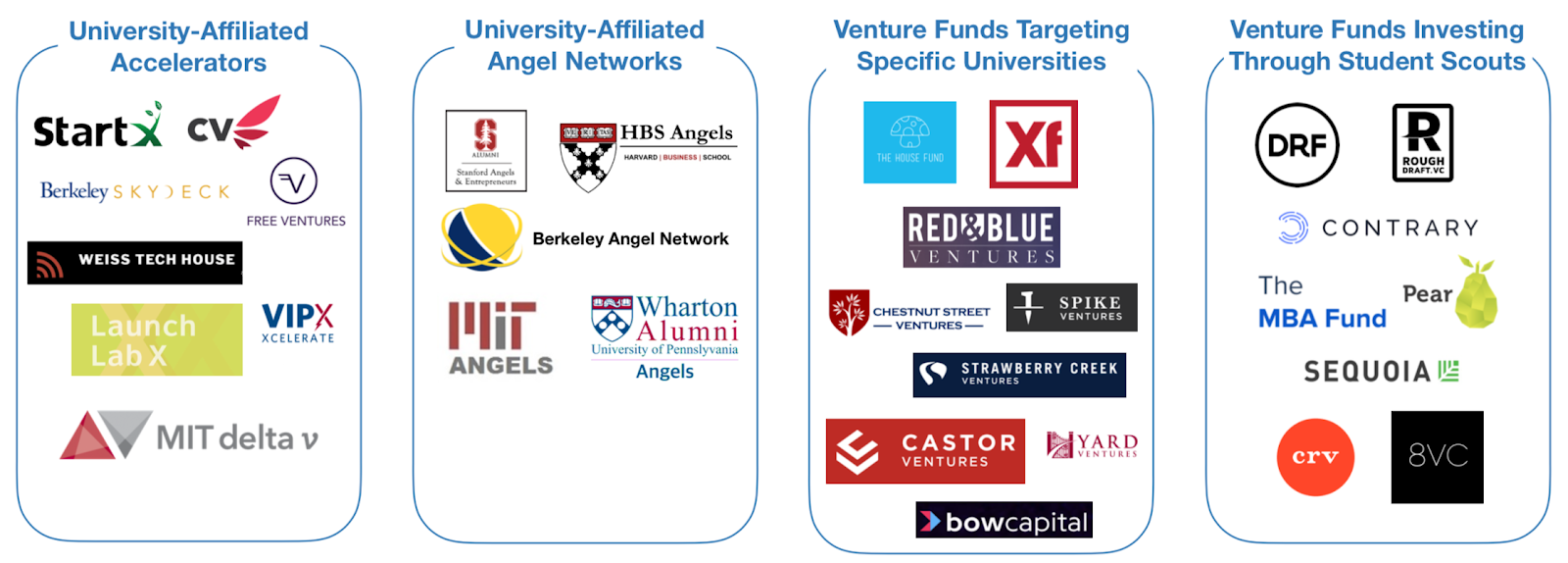

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

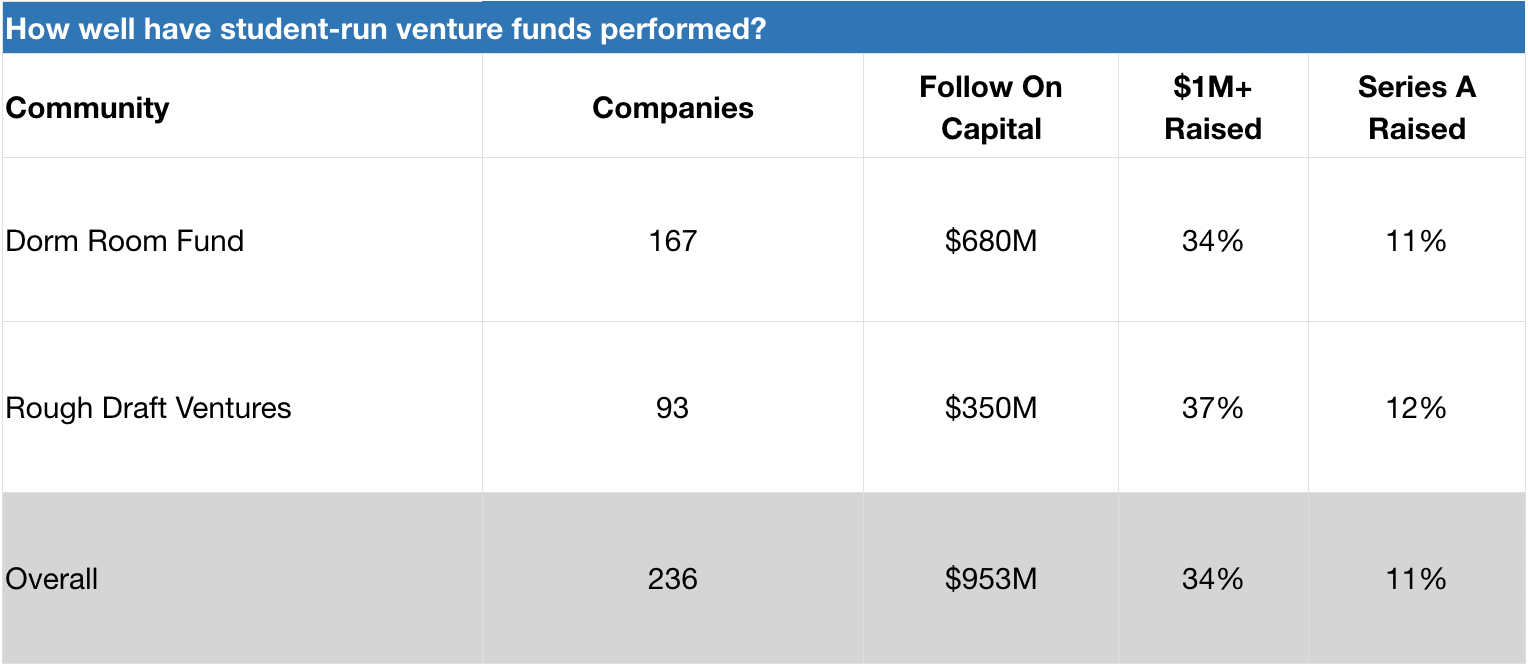

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

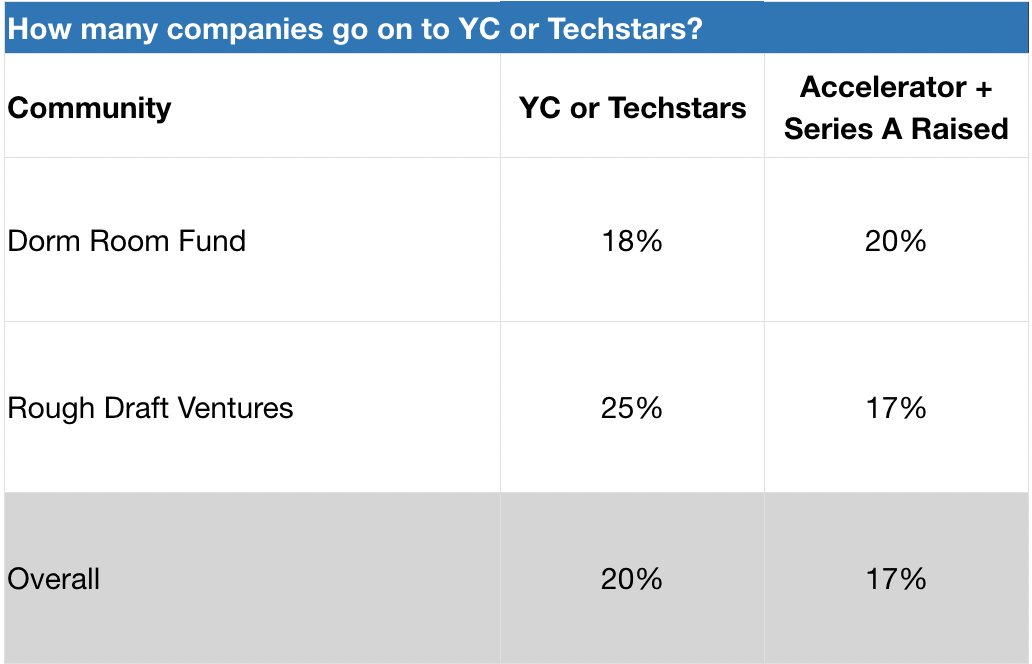

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

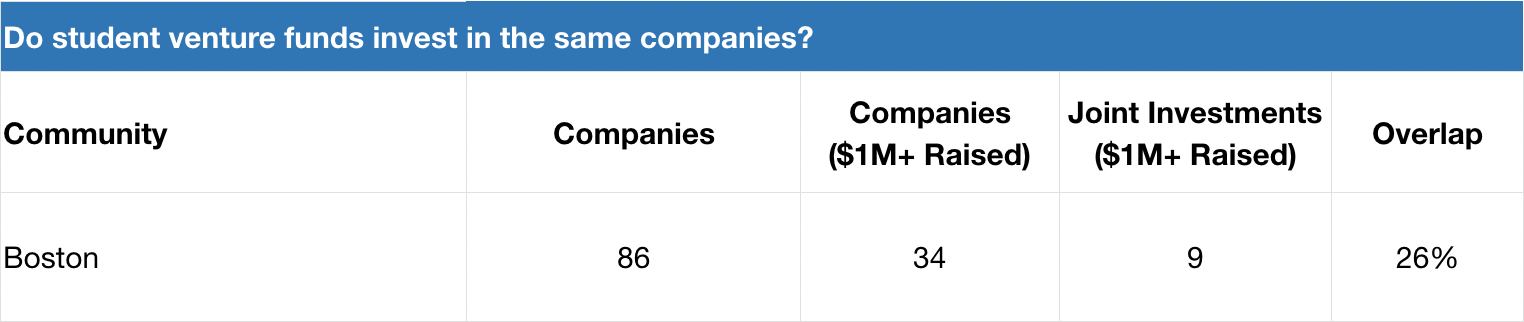

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

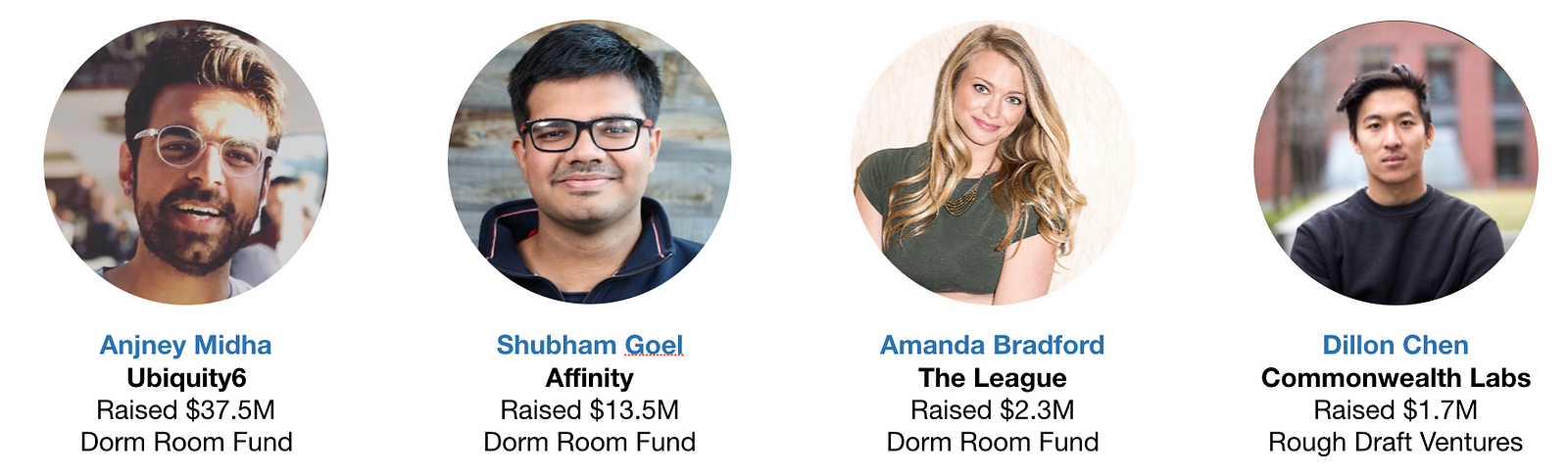

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

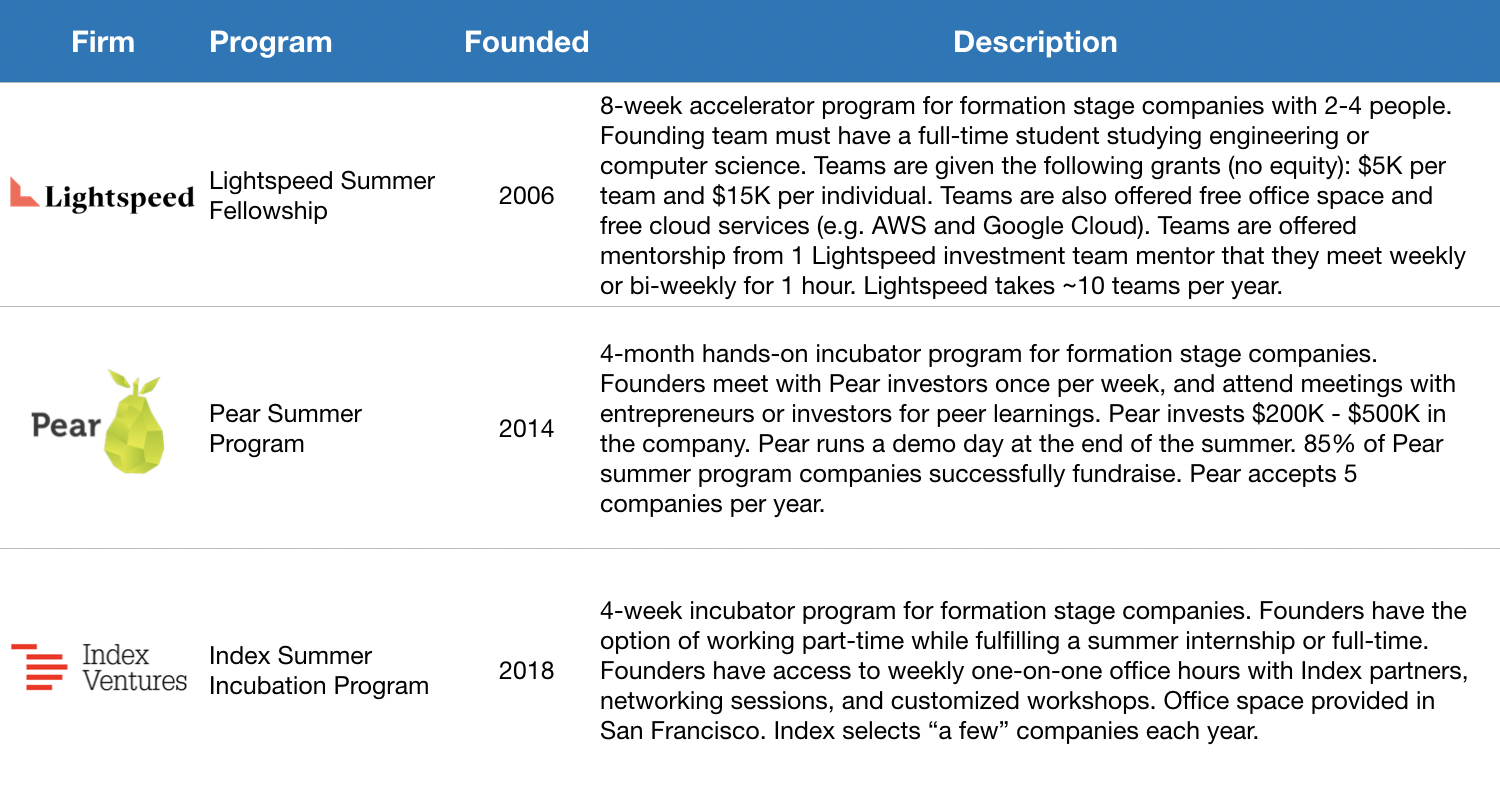

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

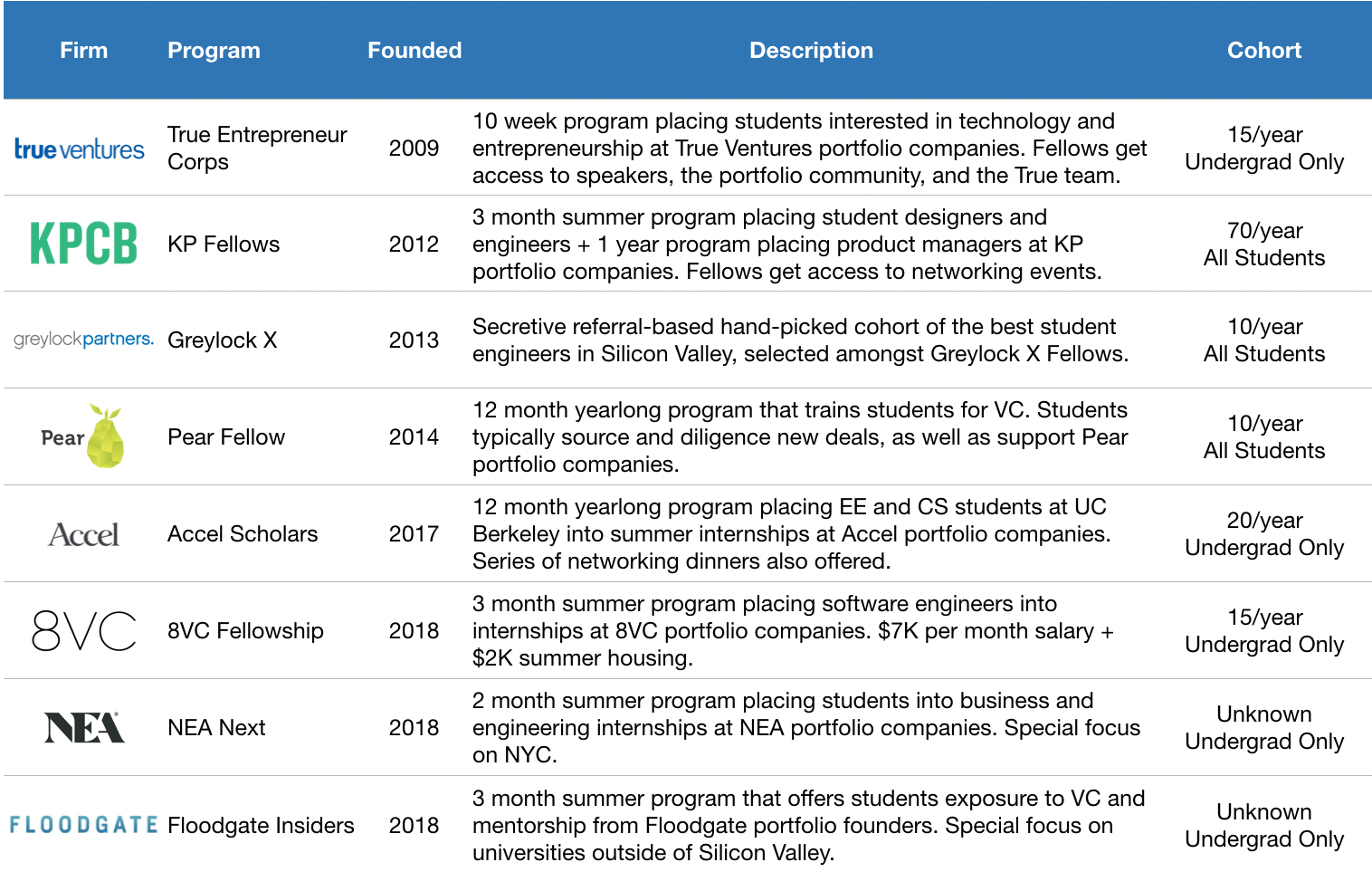

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Taiwanese technology giant Foxconn International is backing Carbon Relay, a Boston-based startup emerging from stealth today that’s harnessing the algorithms used by companies like Facebook and Google for artificial intelligence to curb greenhouse gas emissions in the technology industry’s own backyard — the data center.

Already, the computing demands of the technology industry are responsible for 3 percent of total energy consumption — and the addition of new technologies like Bitcoin to the mix could add another half a percent to that figure within the next few years, according to Carbon Relay’s chief executive, Matt Provo.

That’s $25 billion in spending on energy per year across the industry, Provo says.

A former Apple employee, Provo went to Harvard Business School because he knew he wanted to be an entrepreneur and start his own business — and he wanted that business to solve a meaningful problem, he said.

Variability and dynamic nature of the data center relating to thermodynamics and the makeup of a facility or building is interesting for AI because humans can’t keep up.

“We knew what we wanted to focus on,” said Provo of himself and his two co-founders. “All three of us have an environmental sciences background as well… We were fired up about building something that was true AI that has positive value… the risk associated [with climate change] is going to hit in our lifetime, we were very inspired to build a company whose technology would have an impact on that.”

Carbon Relay’s mission and founding team, including Thibaut Perol and John Platt (two Harvard graduates with doctorates in applied mathematics) was able to attract some big backers.

The company has raised $6 million from industry giants like Foxconn and Boston-based angel investors, including Dr. James Cash — a director on the boards of Walmart, Microsoft, GE and State Street; Black Duck Software founder, Douglas Levin; Karim Lakhani, a director on the Mozilla Corporation board; and Paul Deninger, a director on the board of the building operations management company, Resideo (formerly Honeywell).

Provo and his team didn’t just raise the money to tackle data centers — and Foxconn’s involvement hints at the company’s broader goals. “My vision is that commercial HVAC systems or any machinery that operates in a business would not ship without our intelligence inside of it,” says Provo.

What’s more compelling is that the company’s technology works without exposing the underlying business to significant security risks, Provo says.

“In the end all we’re doing are sending these floats… these values. These values are mathematical directions for the actions that need to be taken,” he says.

Carbon Relay is already profitable, generating $4 million in revenue last year and on track for another year of steady growth, according to Provo.

Carbon Relay offers two products: Optimize and Predict, that gather information from existing HVAC devices and then control those systems continuously and automatically with continuous decision making.

“Each data center is unique and enormously complex, requiring its own approach to managing energy use over time,” said Cash, who’s serving as the company’s chairman. “The Carbon Relay team is comprised of people who are passionate about creating a solution that will adapt to the needs of every large data center, creating a tangible and rapid impact on the way these organizations do business.”

Powered by WPeMatico

Alumni Ventures Group’s (AVG) limited partners aren’t endowment or pension funds. Its typical LP is a heart surgeon in Des Moines, Iowa.

The firm has both an unorthodox model of fundraising and dealmaking. Across 25 micro funds, AVG is raising and investing upwards of $200 million per year for and in tech startups.

Tucked away in Boston, far from the limelight of Silicon Valley, few seem to be paying attention to AVG. There are a few reasons why, and those seem to be working to the firm’s advantage.

Today, AVG is announcing a close of roughly $30 million for three additional funds: Green D Ventures, Chestnut Street Ventures and Purple Arch Ventures, which represent capital committed by Dartmouth, the University of Pennsylvania and Northwestern alums, respectively.

AVG walks and talks like a venture fund, but a peek under the hood reveals its unconventional fundraising mechanisms.

Rather than collecting $5 million minimum investments from institutional LPs, AVG takes $50,000 directly from individual alums of prestigious universities. The firm pools the capital and creates university-specific venture funds for graduates of Duke, Stanford, Harvard, MIT and several other colleges.

“People don’t really know what to make of us because we’re so different,” said Michael Collins, AVG’s founder and chief executive officer.

Collins started AVG to make venture capital more accessible to individual people. He’s been a VC since 1986, formerly of TA Associates, and had grown tired of the hubris that runs rampant in the industry. In 2014, he started a $1.5 million fund for alums of his alma mater, Dartmouth. Since then, AVG has grown into 25 funds, each of which fundraise annually and are seeing substantial growth over their previous raises.

“What we observed is VC is a really good asset class but it’s really designed for institutional investors,” Collins (pictured below) said. “It’s really hard for individual people to put together a smart, simple portfolio unless they do it themselves. That’s why we created AVG.”

AVG and its team of 40 investment professionals make 150 to 200 investments per year of roughly $1 million each in U.S. startups across industries. In the second quarter of 2018, PitchBook listed the firm as the second most active global investor, ranked below only Plug and Play Tech Center and above the likes of Kleiner Perkins, NEA and Accel.

Unlike the Kleiners, NEAs and Accels of the world, AVG never leads investments. Collins says they just “tuck themselves into” a deal with a great lead investor. They don’t take board seats; Collins says he doesn’t see any value in more than one VC on a company board. And they don’t try to negotiate deal terms.

Though unusual, all of this works to their advantage. Founders appreciate the easy capital and access to AVG’s network, and other VC firms don’t view AVG as a threat, making it easier for the firm to get in on great deals.

“We are low friction, we are small and we have a hell of a Rolodex,” Collins said.

Despite a deal flow that’s unmatched by many VC firms, AVG manages to fly under the radar — and the firm is totally OK with that.

“A lot of VC is a bit of a star business where people try to build their own individual brand,” Collins said. “They get out there; they like publicity; they blog; they speak at conferences; they want to be known as the person to bring great deals to. We don’t lead. We work in the background. We just don’t feel the need to put the energy into PR.”

“Most VC returns are really achieved through investing in great companies as opposed to changing the trajectory of a company because you’re on the board,” he added. “If you’re a seed investor in Airbnb or Google, you were really great to be an early investor in that company, not because you sat on the board and you’re brilliance created Google’s success.”

AVG has completed 115 investments in the last 12 months. It’s investing out of 10-year funds, so at just four years in, it has some more waiting to do before it’ll see the full outcomes of its investments. Still, Collins says 65 of their portfolio companies have had liquidity events so far, including Jump, which sold to Uber in April, and Whistle, acquired by Mars Petcare a few years back.

“I hope that we can be a catalyst to bring more people into this asset class,” he concluded.

“I am a big believer that it’s really important that America continues to lead in entrepreneurship and I think the more people that own this asset class the better.”

Powered by WPeMatico