Auto Added by WPeMatico

Arrikto raises $10M for its MLOps platform

Arrikto, a startup that wants to speed up the machine learning development lifecycle by allowing engineers and data scientists to treat data like code, is coming out of stealth today and announcing a $10 million Series A round. The round was led by Unusual Ventures, with Unusual’s John Vrionis joining the board.

“Our technology at Arrikto helps companies overcome the complexities of implementing and managing machine learning applications,” Arrikto CEO and co-founder Constantinos Venetsanopoulos explained. “We make it super easy to set up end-to-end machine learning pipelines. More specifically, we make it easy to build, train, deploy ML models into production using Kubernetes and intelligent intelligently manage all the data around it.”

Like so many developer-centric platforms today, Arrikto is all about “shift left.” Currently, the team argues, machine learning teams and developer teams don’t speak the same language and use different tools to build models and to put them into production.

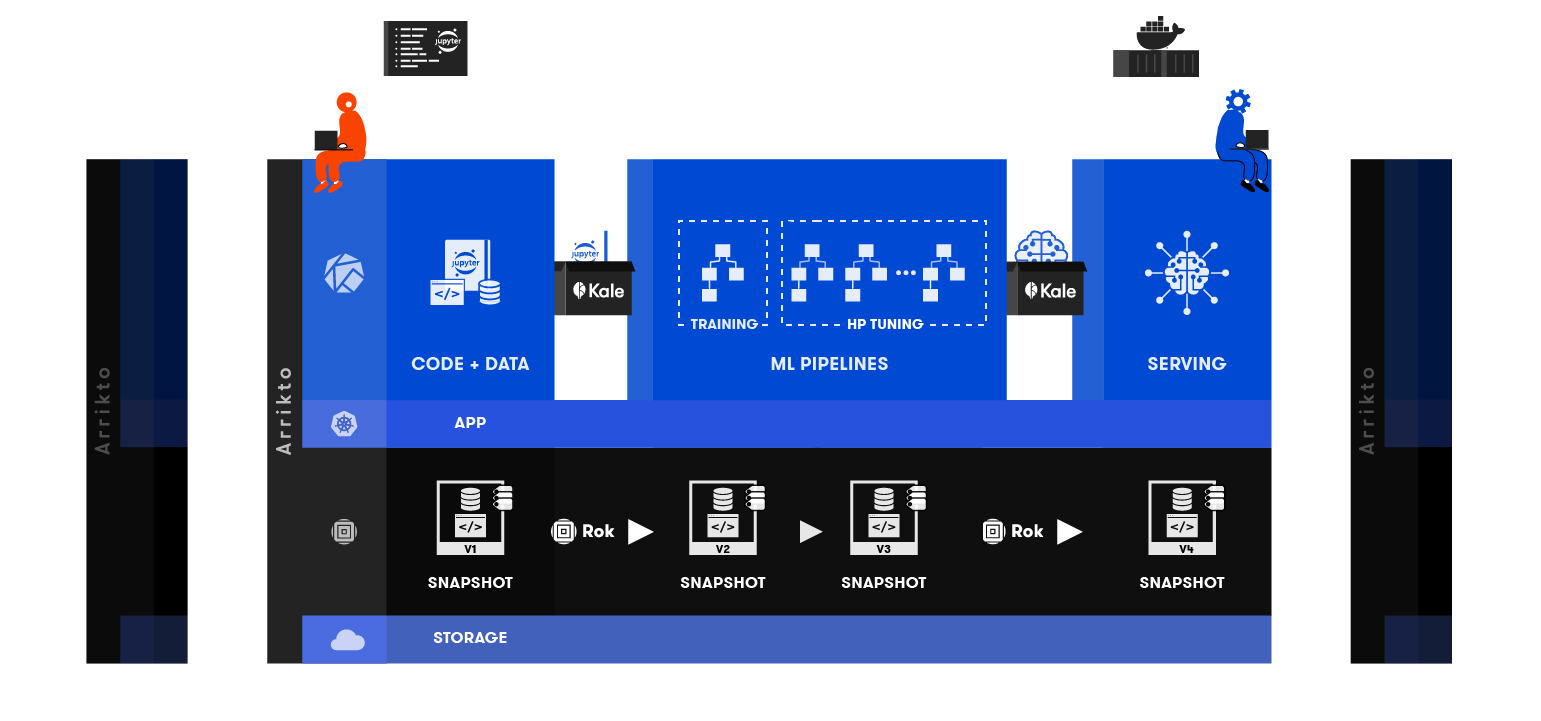

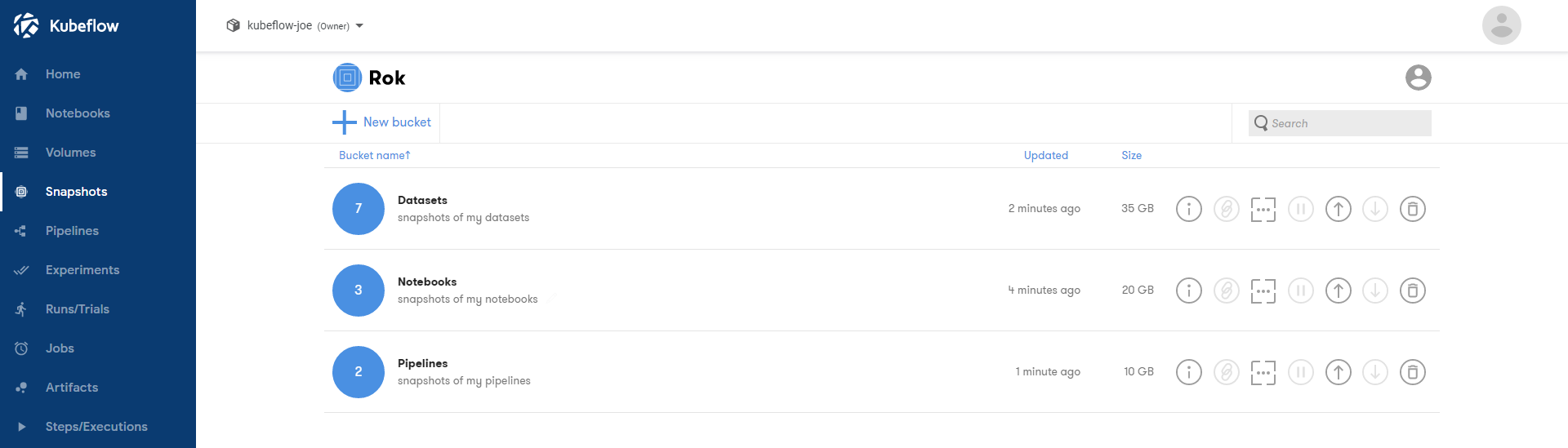

Image Credits: Arrikto

“Much like DevOps shifted deployment left, to developers in the software development life cycle, Arrikto shifts deployment left to data scientists in the machine learning life cycle,” Venetsanopoulos explained.

Arrikto also aims to reduce the technical barriers that still make implementing machine learning so difficult for most enterprises. Venetsanopoulos noted that just like Kubernetes showed businesses what a simple and scalable infrastructure could look like, Arrikto can show them what a simpler ML production pipeline can look like — and do so in a Kubernetes-native way.

Arrikto CEO Constantinos Venetsanopoulos. Image Credits: Arrikto

At the core of Arrikto is Kubeflow, the Google -incubated open-source machine learning toolkit for Kubernetes — and in many ways, you can think of Arrikto as offering an enterprise-ready version of Kubeflow. Among other projects, the team also built MiniKF to run Kubeflow on a laptop and uses Kale, which lets engineers build Kubeflow pipelines from their JupyterLab notebooks.

As Venetsanopoulos noted, Arrikto’s technology does three things: it simplifies deploying and managing Kubeflow, allows data scientists to manage it using the tools they already know, and it creates a portable environment for data science that enables data versioning and data sharing across teams and clouds.

While Arrikto has stayed off the radar since it launched out of Athens, Greece in 2015, the founding team of Venetsanopoulos and CTO Vangelis Koukis already managed to get a number of large enterprises to adopt its platform. Arrikto currently has more than 100 customers and, while the company isn’t allowed to name any of them just yet, Venetsanopoulos said they include one of the largest oil and gas companies, for example.

And while you may not think of Athens as a startup hub, Venetsanopoulos argues that this is changing and there is a lot of talent there (though the company is also using the funding to build out its sales and marketing team in Silicon Valley). “There’s top-notch talent from top-notch universities that’s still untapped. It’s like we have an unfair advantage,” he said.

“We see a strong market opportunity as enterprises seek to leverage cloud-native solutions to unlock the benefits of machine learning,” Unusual’s Vrionis said. “Arrikto has taken an innovative and holistic approach to MLOps across the entire data, model and code lifecycle. Data scientists will be empowered to accelerate time to market through increased automation and collaboration without requiring engineering teams.”

Image Credits: Arrikto

Powered by WPeMatico

Huawei reportedly set to sell Honor budget phone division for $15B

Following weeks of rumors surrounding a potential sale, Huawei has reportedly struck a deal to divest itself of its Honor brand. A new report out today from Reuters notes that the embattled hardware maker will sell the budget unit to a consortium of buyers that includes the government of the city of Shenzhen and Digital China, a phone distributor.

The report, which cites “people familiar with the matter,” puts the price tag for the Honor unit at $15.2 billion. Honor’s new owners will reportedly keep much of the brand’s 7,000 employees (management included) in tact, with plans to take the company public in around three years. The Honor brand has largely focused on low-cost devices, with sales in China, Europe and the U.S. This deal would likely find Huawei focusing more exclusively on high-end products under its own brand.

While the deal has been rumored for some time now, its seeming conclusion comes in the wake of Joe Biden’s presidential election win. It seems clear from Huawei’s decision to press on with the all-cash deal that the company doesn’t believe its international fortunes will change immediately under a new U.S. president.

The news comes in the wake of ongoing difficulties tied to U.S. sanctions. Huawei’s inability to access technologies from companies like Google have proven to be a major hit for the world’s second largest phone maker. While the company has managed to maintain solid sales in its native China, even those have taken a hit amid its struggles.

Powered by WPeMatico

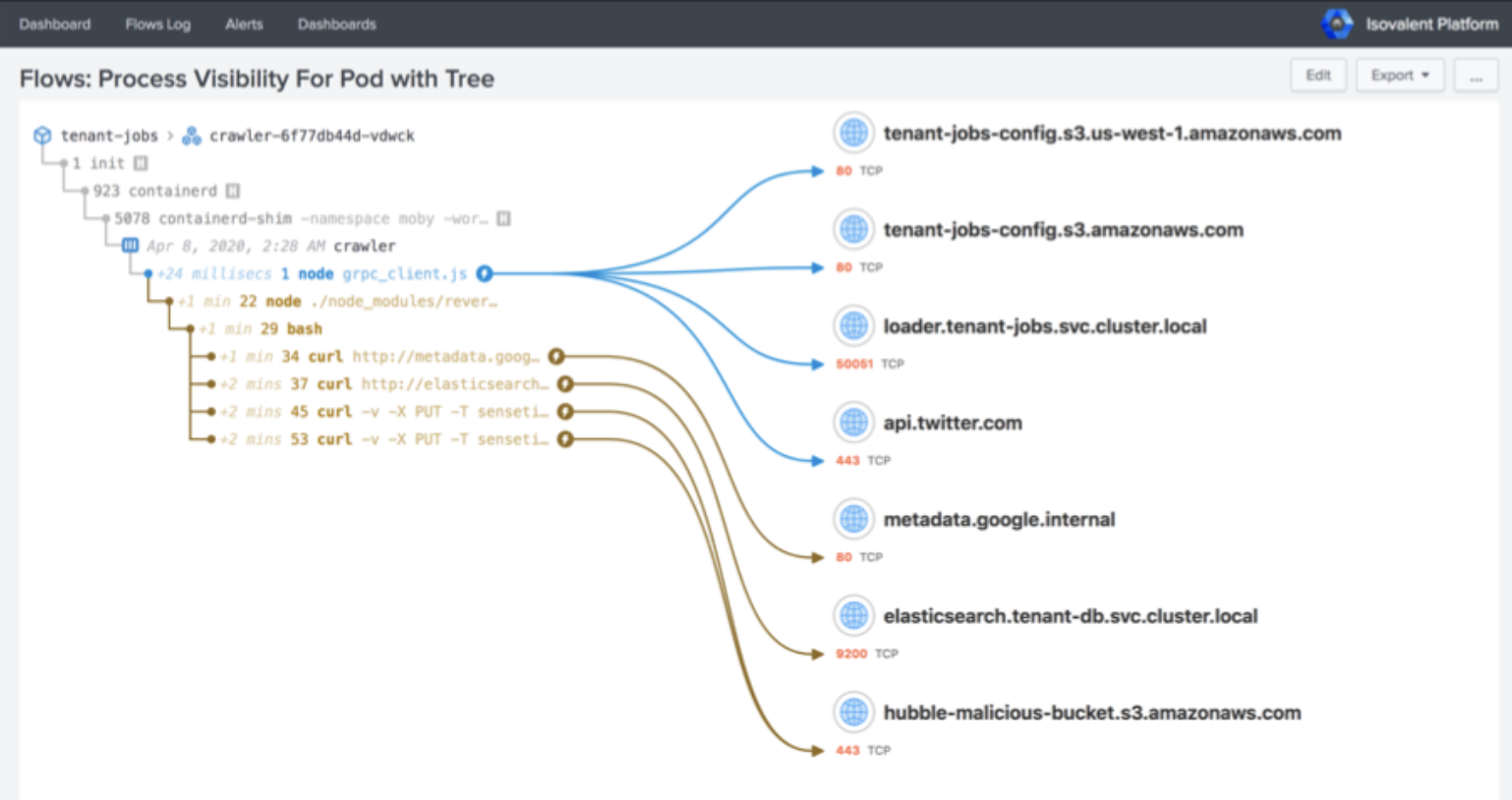

With $29M in funding, Isovalent launches its cloud-native networking and security platform

Isovalent, a startup that aims to bring networking into the cloud-native era, today announced that it has raised a $29 million Series A round led by Andreessen Horowitz and Google. In addition, the company today officially launched its Cilium Enterprise platform (which was in stealth until now) to help enterprises connect, observe and secure their applications.

The open-source Cilium project is already seeing growing adoption, with Google choosing it for its new GKE data plane, for example. Other users include Adobe, Capital One, Datadog and GitLab. Isovalent is following what is now the standard model for commercializing open-source projects by launching an enterprise version.

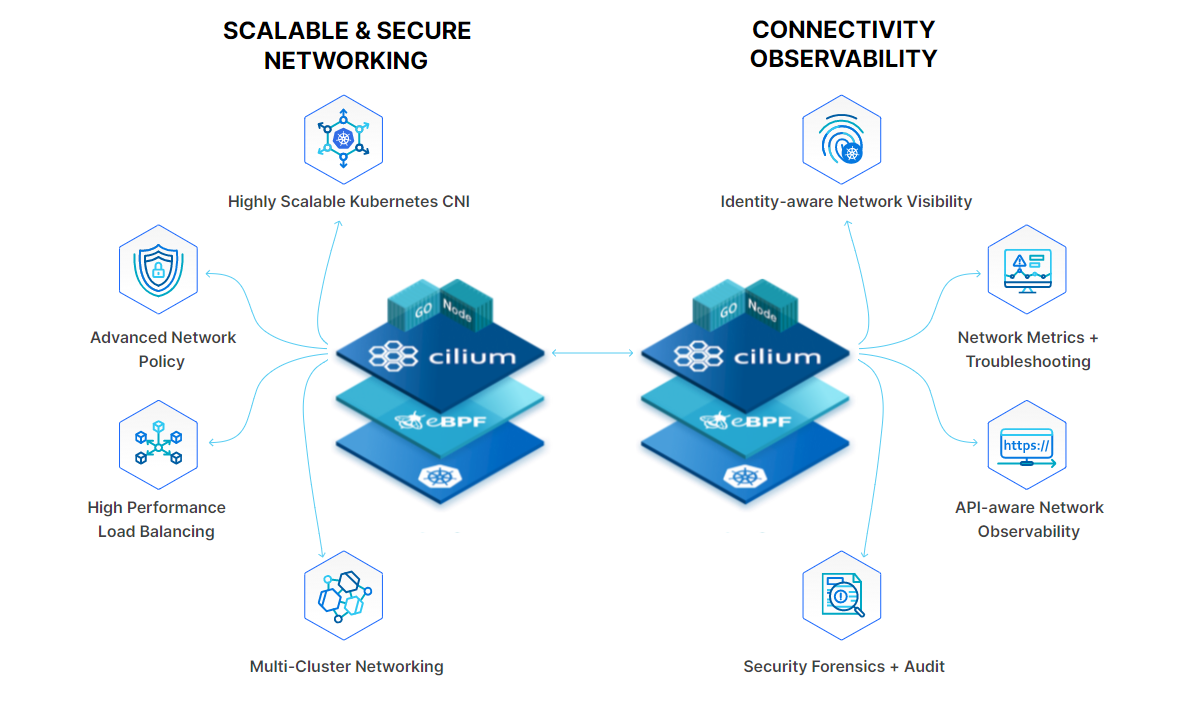

Image Credits: Cilium

The founding team of CEO Dan Wendlandt and CTO Thomas Graf has deep experience in working on the Linux kernel and building networking products. Graf spent 15 years working on the Linux kernel and created the Cilium open-source project, while Wendlandt worked on Open vSwitch at Nicira (and then VMware).

Image Credits: Isovalent

“We saw that first wave of network intelligence be moved into software, but I think we both shared the view that the first wave was about replicating the traditional network devices in software,” Wendlandt told me. “You had IPs, you still had ports, you created virtual routers, and this and that. We both had that shared vision that the next step was to go beyond what the hardware did in software — and now, in software, you can do so much more. Thomas, with his deep insight in the Linux kernel, really saw this eBPF technology as something that was just obviously going to be groundbreaking technology, in terms of where we could take Linux networking and security.”

As Graf told me, when Docker, Kubernetes and containers, in general, become popular, what he saw was that networking companies at first were simply trying to reapply what they had already done for virtualization. “Let’s just treat containers as many as miniature VMs. That was incredibly wrong,” he said. “So we looked around, and we saw eBPF and said: this is just out there and it is perfect, how can we shape it forward?”

And while Isovalent’s focus is on cloud-native networking, the added benefit of how it uses the eBPF Linux kernel technology is that it also gains deep insights into how data flows between services and hence allows it to add advanced security features as well.

As the team noted, though, users definitely don’t need to understand or program eBPF, which is essentially the next generation of Linux kernel modules, themselves.

Image Credits: Isovalent

“I have spent my entire career in this space, and the North Star has always been to go beyond IPs + ports and build networking visibility and security at a layer that is aligned with how developers, operations and security think about their applications and data,” said Martin Casado, partner at Andreesen Horowitz (and the founder of Nicira). “Until just recently, the technology did not exist. All of that changed with Kubernetes and eBPF. Dan and Thomas have put together the best team in the industry and given the traction around Cilium, they are well on their way to upending the world of networking yet again.”

As more companies adopt Kubernetes, they are now reaching a stage where they have the basics down but are now facing the next set of problems that come with this transition. Those, almost by default, include figuring out how to isolate workloads and get visibility into their networks — all areas where Isovalent/Cilium can help.

The team tells me its focus, now that the product is out of stealth, is about building out its go-to-market efforts and, of course, continuing to build out its platform.

Powered by WPeMatico

Why I left edtech and got into gaming

Darshan Somashekar co-founded drop.io (acquired by Facebook), Imagine Easy Solutions (acquired by Chegg) and is currently co-founder of gaming platform Solitaired and a venture partner at TMV.

Now that COVID-19 has accelerated the adoption of digital education tools, edtech has become one of the hottest areas of investment.

As someone who has been in edtech for nearly 20 years, this sounds like the precise moment to capitalize on all the newfound interest. Which is why what I’m about to say might be surprising: I’m leaving edtech for the world of gaming with my new company, Solitaired.

I first got into edtech in high school, when a friend and I founded EasyBib, a website that helped students cite sources for their papers. At the time, we were just students who felt there had to be a better way than formatting tedious citations for research papers by hand. But as we dove into the business further, we realized there was a lot to like about bibliographies and education technology in general.

For one, the education market is large. There are more than 56 million K-16 students in the U.S., and over 1.3 billion globally. Federal, state and local governments spend an aggregate of 5% of GDP on education, and that doesn’t even include what students and parents spend on content and technology.

Secondly, it’s structured. Students generally all go through the same curriculum together. That means most students have the same problem in the same way; if you solve a problem for one group of users, you’ve probably solved it for most users.

The citation problem was just like that. When we sold our company to Chegg, we were already reaching four out of five students that needed bibliographies, or over 30 million students in the U.S. Edtech companies that help students with math, chemistry, homework help, tutoring and other curricular needs can build massive audiences quickly.

Edtech that’s part of the curriculum also has high engagement. EasyBib users stayed on our site for nearly ten minutes per session, creating one citation after another for their bibliographies. For direct-to-consumer edtech companies that are ad and subscription driven, this behavior creates many monetization opportunities.

While we grew fast, our endemic market opportunity was limited. Why? The strengths of edtech can also be its downsides, especially for a startup. On the user growth front, we focused on school relationships, marketing and SEO. But once we reached four out of every five students in the U.S., there wasn’t much more room to grow.

To increase engagement even further, we tried a number of things: encouraging more citation creation, adding research and note-taking features and building a Chrome extension to be more ever-present in the user’s research journey. Those efforts fell short too. Ultimately, the school calendar dictated how often students needed to use us, and we were constrained by the number of research papers teachers assigned.

These challenges can certainly be overcome. But as a startup, we had to decide if we wanted to pursue adjacencies and expansions ourselves. Ultimately, this realization was one of the reasons we decided to sell our company to Chegg, which had a wider user base and product synergies that we couldn’t achieve on our own. As anyone who follows Chegg might know, they’ve been very successful in accelerating the edtech digital transformation.

When we began thinking about our second business, we had these lessons in the back of our mind. That’s when we discovered gaming.

Powered by WPeMatico

Alibaba passes IBM in cloud infrastructure market with over $2B in revenue

When Alibaba entered the cloud infrastructure market in earnest in 2015 it had ambitious goals, and it has been growing steadily. Today, the Chinese e-commerce giant announced quarterly cloud revenue of $2.194 billion. With that number, it has passed IBM’s $1.65 billion revenue result (according to Synergy Research market share numbers), a significant milestone.

But while $2 billion is a large figure, it’s one worth keeping in perspective. For example, Amazon announced $11.6 billion in cloud infrastructure revenue for its most recent quarter, while Microsoft’s Azure came in second place with $5.9 billion.

Google Cloud has held onto third place, as it has for as long as we’ve been covering the cloud infrastructure market. In its most recent numbers, Synergy pegged Google at 9% market share, or approximately $2.9 billion in revenue.

While Alibaba is still a fair bit behind Google, today’s numbers puts the company firmly in fourth place now, well ahead of IBM . It’s doubtful it could catch Google anytime soon, especially as the company has become more focused under CEO Thomas Kurian, but it is still fairly remarkable that it managed to pass IBM, a stalwart of enterprise computing for decades, as a relative newcomer to the space.

The 60% growth represented a slight increase from the previous quarter’s 59%, but basically means it held steady, something that’s not easy to do as a company reaches a certain revenue plateau. In its earnings call today, Daniel Zhang, chairman and CEO at Alibaba Group, said that in China, which remains the company’s primary market, digital transformation driven by the pandemic was a primary factor in keeping growth steady.

“Cloud is a fast-growing business. If you look at our revenue breakdown, obviously, cloud is enjoying a very, very fast growth. And what we see is that all the industries are in the process of digital transformation. And moving to the cloud is a very important step for the industries,” Zhang said in the call.

He believes eventually that most business will be done in the cloud, and the growth could continue for the medium term, as there are still many companies that haven’t made the switch yet, but will do so over time.

John Dinsdale, an analyst at Synergy Research, says that while China remains its primary market, the company does have a presence outside the country too, and can afford to play the long game in terms of the current geopolitical situation with trade tensions between the U.S. and China.

“Alibaba has already made some strides outside of China and Hong Kong. While the scale is rather small compared with its Chinese operations, Alibaba has established a data center and cloud presence in a range of countries, including six more APAC countries, U.S., U.K. and UAE. Among these, it is the market leader in both Indonesia and Malaysia,” Dinsdale told TechCrunch.

In its most recent data released a couple of weeks ago, prior to today’s numbers, Synergy broke down the market this way: “Amazon 33%, Microsoft 18%, Google 9%, Alibaba 5%, IBM 5%, Salesforce 3%, Tencent 2%, Oracle 2%, NTT 1%, SAP 1% – to the nearest percentage point.”

Powered by WPeMatico

Booming edtech M&A activity brings consolidation to a fragmented sector

As the COVID-19 pandemic continues to force teachers, students and parents to adopt new technologies, edtech’s total addressable market has massively grown in the last several months. The shift has urged venture capitalists to pour money into the sector accordingly, ushering a number of startups into the unicorn club.

But maturation doesn’t just mean bigger checks and high-flying unicorns — it also brings exits.

Edtech M&A activity is buzzier than usual: In the last week, Course Hero, a startup that sells Netflix-like subscriptions to students looking for learning and teaching content, bought Symbolab, an artificial intelligence-powered calculator. Saga Education, a tutoring nonprofit backed by Comcast, the Bill & Melinda Gates Foundation and others, acquired math software platform Woot Math. We also saw PowerSchool, which sells a suite of software services to manage schools, scoop up Hoonuit, a data management and analytics tool for educators. Finally, K-12 curriculum company Discovery Education bought K-5 science and stem curriculum upstart Mystery Science.

It’s a lot of news in a short period of time. Luckily, these consolidations offer some directional guidance regarding where some edtech businesses think the future of their industry is headed.

Smart content as a competitive advantage

Content, to an extent, is commoditized. If you can find a free tutorial on Youtube or Khan Academy, buy a subscription to an edtech platform that offers the same solution? The commodification of education is good for end-users and is often why startups have a freemium model as a customer acquisition strategy. To convert free users into paying subscribers, edtech startups need to offer differentiated and targeted content.

The Course Hero and Mystery Science deals show us that edtech businesses are hungry for personalized, targeted content. Course Hero’s acquisition of Symbolab was essentially a deal for more than a decade’s worth of data that captured which math questions students found hardest.

Symbolab is a math calculator that is set to answer over 1 billion questions this year. With each answer, Symbolab adds information to its algorithm regarding students’ most common pain points and confusion. Course Hero, in contrast, is a broader service that focuses on Q&A from a variety of subjects. CEO Andrew Grauer says Symbolab’s algorithm isn’t something that Course Hero, which has been operating since 2006, can drum up overnight. That’s precisely why he “decided to buy, instead of build.”

“It made a lot of sense to move fast enough so it wouldn’t take up multiple years to get this technology,” Grauer said. The deal was made as big companies get in the Q&A game too, he noted. Google acquired homework helper app Socratic in 2019 and Microsoft built Microsoft Solver in the same year.

Discovery Education, a curriculum provider for K-12 classrooms, acquired San Francisco-based K-5 STEM curriculum provider, Mystery Science. Discovery Education has launched a series of other products focused on science education, including Discovery Education Experience, the Science Techbook series and STEM Connect. However, Mystery Science is largely focused on offering a creative digital solution to science education. The programming, a mix of videos, prompts and projects, cover a range of questions such as, “Where do rivers flow?” and “Could a volcano pop up where you live?” for young students.

Mystery Science CEO and founder Keith Schact explained how his product focuses on kids and educators, while Discovery Education focuses on educators and districts, making the deal feel like a “natural marriage.” Even as edtech goes directly to consumers, Schact remains bullish on the role that institutions play in true adoption of technology.

“You can go straight to teachers and get a certain market share,” he said. “But the institutions still do have a big role.” The founder likened the dynamic to the state of media: With the rise of blogs, you can publish directly and reach an engaged audience, but writers who want a bigger positioning tend to join larger platforms to grow their overall reach. Edtech is the same, in that some startups need an official sign-off from schools before they can reach venture-scale returns.

According to a source familiar with the transaction, Mystery Science was sold for $175 million after only raising $4 million in venture financing.

Using data management and analytics to improve student outcomes

Powered by WPeMatico

Q3 earnings find Apple and Google looking to the future for hardware rebounds

“5G is a once-in-a-decade kind of opportunity,” Tim Cook told the media during the Q&A portion of Apple’s Q3 earnings call. “And we could not be more excited to hit the market exactly when we did.”

The truth of the matter is its timing was a mixed bag. Apple was, by some accounts, late to 5G. By the time the company finally announced that it was adding the technology across its lineup of iPhone 12 variants, much of its competition had already beat the company to the punch. Of course, that’s not a huge surprise. Apple’s strategy is rarely a rush to be first.

5G networks are only really starting to come into their own now. Even today, there are still wide swaths of users who will have to default to an LTE connection the majority of the time they use their handsets. The arrival of 5G on the iPhone was really as much about future-proofing this year’s models as anything. Consumers are holding onto phones longer, and in the three or four years before it’s time for another upgrade, the 5G maps will look very different.

Clearly, the new iPhone didn’t hit the market exactly when Apple had hoped; the pandemic saw to that. Manufacturing bottlenecks in Asia delayed the iPhone 12’s launch by a month. That’s going to have an impact on the bottom line of your quarterly earnings. The company saw a 20% drop for the quarter, year-over-year. That’s hugely significant, causing the company’s stock to drop more than 4% in extended trading.

Apple’s diverse portfolio helped curb some of those revenue slides. While the pandemic has generally had a profound impact on consumer spending on “non-essentials,” changing where and how we work has helped bolster Mac and iPad sales, which were up 28% and 46%, respectively, year-over-year. It wasn’t enough to completely stop the iPhone stumble, but it certainly brings the importance of a diverse hardware portfolio into sharp relief.

China was a big issue for the company this time around — and the lack of a new, 5G-enabled iPhone was a big contributor. In greater China (including Taiwan and Hong Kong), the company saw a 28% drop in sales. There are a number of reasons to be hopeful about iPhone sales in Q4, however.

As I noted this morning, smartphone shipments were down almost across the board in China for Q3, per new figures from Canalys. Much of that can be chalked up to Huawei’s ongoing issues with the U.S. government. Long the dominant manufacturer in mainland China, the company has been hamstrung by, among other things, a ban on access to Android and other U.S.-made technologies. Apple’s numbers remained relatively steady compared to the competition and Huawei’s issues could present a big hole in the market. With 5G on its side, this next quarter could prove a banner year for the company.

Powered by WPeMatico

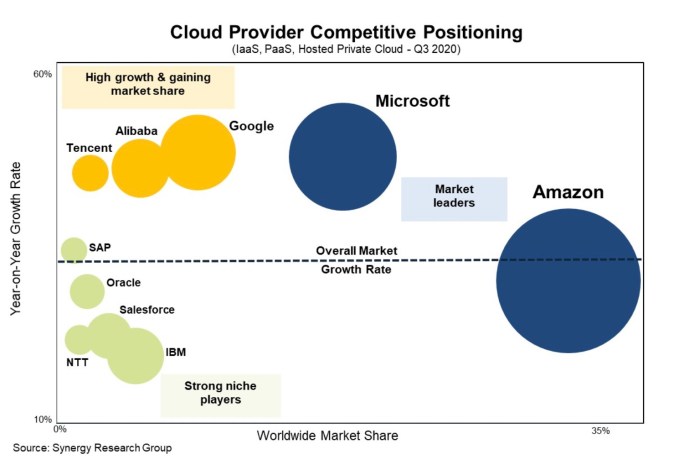

Cloud infrastructure revenue grows 33% this quarter to almost $33B

The cloud infrastructure market kept growing at a brisk pace last quarter, as the pandemic continued to push more companies to the cloud with offices shut down in much of the world. This week the big three — Amazon, Microsoft and Google — all reported their numbers and, as expected, the news was good, with Synergy Research reporting revenue growth of 33% year over year, up to almost $33 billion for the quarter.

Still, John Dinsdale, chief analyst at Synergy, was a bit taken aback that the market continued to grow as much as it did. “While we were fully expecting continued strong growth in the market, the scale of the growth in Q3 was a little surprising,” he said in a statement.

He added, “Total revenues were up by $2.5 billion from the previous quarter causing the year-on-year growth rate to nudge upwards, which is unusual for such a large market. It is quite clear that COVID-19 has provided an added boost to a market that was already developing rapidly.”

Per usual Amazon led the way with $11.6 billion in revenue, up from $10.8 billion last quarter. That’s up 29% year over year. Amazon continues to exhibit slowing growth in the cloud market, but because of its market share lead of 33%, a rate that has held fairly steady for some time, the growth is less important than the eye-popping revenue it continues to generate, almost double its closest rival Microsoft .

Speaking of Microsoft, Azure revenue was up 48% year over year, also slowing some, but good enough for a strong second place with 18% market share. Using Synergy’s total quarterly number of $33 billion, Microsoft came in at $5.9 billion in revenue for the quarter, up from $5.2 billion last quarter.

Finally, Google announced cloud revenue of $3.4 billion, but that number includes all of its cloud revenue including G Suite and other software. Synergy reported that this was good for 9%, or $2.98 billion, up from $2.7 billion last quarter, good for third place.

Alibaba and IBM were tied for fourth with 5%, or around $1.65 billion each.

Image Credits: Synergy Research

It’s worth noting that Canalys had similar numbers to Synergy, with growth of 33% to $36.5 billion. They had the same market order with slightly different numbers, with Amazon at 32%, Microsoft at 19% and Google at 7%, and Alibaba in 4th place at 6%.

Canalys sees continued growth ahead, especially as hybrid cloud begins to merge with newer technologies like 5G and edge computing. “All three [providers] are collaborating with mobile operators to deploy their cloud stacks at the edge in the operators’ data centers. These are part of holistic initiatives to profit from 5G services among business customers, as well as transform the mobile operators’ IT infrastructure,” Canalys analyst Blake Murray said in a statement.

While the pure growth continues to move steadily downward over time, this is expected in a market that’s maturing like cloud infrastructure, but as companies continue to shift workloads more rapidly to the cloud during the pandemic, and find new use cases like 5G and edge computing, the market could continue to generate substantial revenue well into the future.

Powered by WPeMatico

Microsoft now lets you bring your own data types to Excel

Over the course of the last few years, Microsoft started adding the concept of “data types” to Excel; that is, the ability to pull in geography and real-time stock data from the cloud, for example. Thanks to its partnership with Wolfram, Excel now features more than 100 of these data types that can flow into a spreadsheet. But you won’t be limited to only these pre-built data types for long. Soon, Excel will also let you bring in your own data types.

That means you can have a “customer” data type, for example, that can bring in rich customer data from a third-party service into Excel. The conduit for this is either Power BI, which now allows Excel to pull in any data you previously published there, or Microsoft’s Power Query feature in Excel that lets you connect to a wide variety of data sources, including common databases like SQL Server, MySQL and PostreSQL, as well as third-party services like Teradata and Facebook.

Image Credits: Microsoft

“Up to this point, the Excel grid has been flat… it’s two dimensional,” Microsoft’s head of product for Excel, Brian Jones, writes in today’s announcement. “You can lay out numbers, text, and formulas across the flexible grid, and people have built amazing things with those capabilities. Not all data is flat though and forcing data into that 2D structure has its limits. With Data Types we’ve added a 3rd dimension to what you can build with Excel. Any cell can now contain a rich set of structured data… in just a single cell.”

The promise here is that this will make Excel more flexible, and I’m sure a lot of enterprises will adapt these capabilities. These companies aren’t likely to move to Airtable or similar Excel-like tools anytime soon, but have data analysis needs that are only increasing now that every company gathers more data than it knows what to do with. This is also a feature that none of Excel’s competitors currently offer, including Google Sheets.

Image Credits: Microsoft

Powered by WPeMatico

Mophie introduces a modular wireless charging module

Here’s a clever addition for Mophie, one of the longstanding battery case makers, which is now a part of the same smartphone accessory conglomerate as Zagg, Braven, iFrogz and InvisibleShield. The Juice Pack Connect is a modular take on the category, with a battery pack that slides on and off.

For $80 you get a 5,400mAh battery (that should get you plenty of additional charge time) and a ring stand that props the phone up. Mophie may offer additional models at some point, but right now, the biggest selling point is less about add-ons and more the fact that you can slip the battery off the device when not needed and still use the case.

Image Credits: Mophie

It’s not entirely dissimilar from the modular uniVERSE case OtterBox introduced a bunch of years ago, but the big advantage here is that the charging works via Qi, so you don’t have to plug it into the phone’s port.

It’s not cheap (Mophie isn’t, generally). And, no, it’s not a MagSafe accessory. Instead, the add-on attaches to your case (needs to be one thin enough to support the charging, mind) using adhesive. The upside is that it works with a much larger number of phones, including multiple generations of iPhones and wireless-capable handsets like Samsung Galaxies and Google Pixels.

Powered by WPeMatico