Goldman Sachs

Auto Added by WPeMatico

Auto Added by WPeMatico

When you think of old, giant mainframes that sit in the basement of a giant corporation, still doing the same work they did 30 years ago, chances are you’re thinking about a financial institution. It’s the financial enterprises, though, that are often leading the charge in bringing new technologies and software development practices to their employees and customers. That’s in part because they are in a period of disruption that forces them to become more nimble. Often, this means leaving behind legacy technology and embracing the cloud.

At TC Sessions: Enterprise, which is happening on September 5 in San Francisco, Capital One executive VP in charge of its technology operations, George Brady, will talk about the company’s journey from legacy hardware and software to embracing the cloud and open source, all while working in a highly regulated industry. Indeed, Capital One was among the first companies to embrace the Facebook-led Open Compute project and it’s a member of the Cloud Native Computing Foundation. It’s this transformation at Capital One that Brady is leading.

At our event, Brady will join a number of other distinguished panelists to specifically talk about his company’s journey to the cloud. There, Capital One is using serverless compute, for example, to power its Credit Offers API using AWS’s Lambda service, as well as a number of other cloud technologies.

Before joining Capital One as its CTO in 2014, Brady ran Fidelity Investment’s global enterprise infrastructure team from 2009 to 2014 and served as Goldman Sachs’ head of global business applications infrastructure before that.

Currently, he leads cloud application and platform productization for Capital One. Part of that portfolio is Critical Stack, a secure container orchestration platform for the enterprise. Capital One’s goal with this work is to help companies across industries become more compliant, secure and cost-effective operating in the public cloud.

Early-bird tickets are still on sale for $249; grab yours today before we sell out.

Student tickets are just $75 — grab them here.

Powered by WPeMatico

In the early 2000s, journalists popularized the term “PayPal mafia” to describe the PayPal founders and employees who left to start their own wildly successful tech companies, including Peter Thiel, Reid Hoffman, and Elon Musk. Drawing from that idea, this article seeks to cover the formation and flow of talent within the crypto landscape today.

I’m fascinated by the concept of tech mafias, popularized by Paypal in the early 00s.

Early signs of crypto mafias:

Coinbase

@0xProject @dydxprotocol

Ethereum/ConsenSys

MIT

IC3Others?

— Ash Egan (@AshAEgan) April 3, 2019

The crypto world is in a constant state of flux, with new startups entrants joining the industry every single day. These new startups have the potential either to be superstars within a portfolio company or to start the next Coinbase. Additionally, there are already impressive spin-outs from some of the more established crypto companies.

For ease of framing, I’ve separated these early-forming mafias into four categories: Crypto, Tech, Wall Street, and Academia. Since 2009, there have been 186 spinout companies originating from those four categories (33% from Academia, 28% from Crypto, 24% from Tech, and 15% from Wall Street).

Obvious but important disclaimer: this article does not intend to promote organized crime within crypto.

Powered by WPeMatico

Slack, the popular workplace messaging company, is expected to list on the New York Stock Exchange on Thursday in the second major direct listing in the U.S. after Spotify introduced the concept to investors in April of last year.

At this point, plenty of industry observers think it makes sound sense for Slack to embrace the direct listing approach, wherein a company places its stock on a public exchange without raising any money or using underwriters. Though the company warned last week that its operating losses are widening as it chases new customers, it has $800 million on its balance sheet, meaning it doesn’t need to raise more right now.

Slack also doesn’t need underwriters who typically discount a company’s shares in order to ensure that they appreciate in value when they begin trading. It’s a known brand in the tech world, and that universe is broadening by the day. Put another way, Slack doesn’t need to be “sold” for investors to want to snap up its shares.

Still, we wondered about some of the thinking that has gone into preparing Slack for its move into the world of publicly traded companies, so we talked with a couple of people who are familiar with what’s happening behind the scenes to find out more. They asked not to be named, but here’s what we learned:

1) Unlike with the popular streaming music platform Spotify, which has more than 100 million premium subscribers and roughly twice as many active monthly users, Slack wasn’t as well-known to Wall Street as Silicon Valley might imagine. In fact, we’re told the bankers that were selected to advise Slack on its offering — Morgan Stanley, Goldman Sachs and Allen & Co., which are the same three that advised Spotify — had to provide more education to analysts and institutional investors this time around.

2) There will (hopefully) be enough shares to go around, while also not a glut of them. The big concern in a direct offering — which does not feature a lock-up period — is that too many people will dump their shares on the market, crushing the company’s share price, or else that too few will part with their holdings, turning the buying and selling of the company’s shares into a financial game of chicken. We’ll see what happens here, but we’re told the banks have spent the last six months trying to ensure that many — but not all — of the company’s institutional shareholders will be selling some of their stakes at the offering, Also worth noting is that unlike with Spotify, some Slack employees have restricted stock units that will vest upon its public listing and so be part of the supply of shares on its first day.

3) In establishing guidance around how Spotify’s shares should be valued, the banks advising the company looked almost entirely to its private market trades, of which there were many. There has been less secondary activity with Slack’s shares, so the banks are likely to rely on these sales but also to use other inputs. We’ll learn soon enough what they settle on, but based on the latest prices at which its shares have traded in the private market, Slack’s presumed valued right now is at $16.7 billion, or 36 times trailing 12-month sales.

4) You might imagine that banks hate direct listings because of the rich underwriting fees they aren’t collecting, and they probably do. Still, even with a direct listing, they get paid pretty well, thanks to both advisory fees and also because investors often trade through the banks named as advisers in the prospectus. There are also fewer mouths to feed on a deal with a direct listing. In Slack’s case — as happened with Spotify — Morgan Stanley, Goldman Sachs and Allen & Co. will reportedly reap almost all of the spoils — or a reported 90% of the $22 million in fees earmarked for all the advisers involved in the deal. In a traditional IPO, a longer number of banks that promise research coverage are given shares to sell, which eats into lead underwriters’ allotment.

5) One risk that Slack shouldn’t necessarily run into but that may have adversely impacted Uber’s IPO is its investor base. According to Slack’s S-1, its biggest outside shareholders include Accel (it owns 24% sailing into the offering), Andreessen Horowitz (13.3%), Social Capital (10.2%) and SoftBank (7.3 %). Why it matters: Slack doesn’t have to worry about less traditional private company backers like mutual funds not wanting to buy up its shares because they’re too busy trying to offload some.

6) Direct listings may well become a more popular product for consumer companies because companies can avoid further dilution, and there’s no lock-up on their shares, creating a shorter path to liquidity for the company and its employees and its investors. Still, Slack is probably anomalous as an enterprise company with a high enough profile to pull one off. The listings are really for companies that don’t need money any time soon and whose shares are already of interest to investors, who don’t need inducements to pay attention.

7) This is the second direct listing of a highly valued privately held company and, for the second time, it’s happening on the NYSE, with the same market maker, Citadel Securities, charged with ensuring orderly trading; the same bank, Morgan Stanley, selected to advise Citadel; and even the same law firms that worked on Spotify’s direct listing pulled back into service.

It’s nice if you’re part of this particular club, and no one can blame Slack for not wanting to reinvent the wheel. But one wonders how nervous it makes Nasdaq, as well as other banks and law firms, to be shut out of this process a second time.

Powered by WPeMatico

William Hockey, co-founder, chief technology officer and president of the fast-growing fintech business Plaid, will step down next week, TechCrunch has learned.

The former Bain associate (pictured above left) co-founded the startup in 2012 alongside chief executive officer Zach Perret. Today, the San Francisco-based company employs 300 with additional offices in Salt Lake City and New York.

Plaid has confirmed the news, stating that Hockey will remain on the company’s board of directors.

“This conclusion was neither a rash nor a recent decision,” Hockey writes in a blog post shared with TechCrunch. “Over the past couple of years, I have known that there would come a point at which I would choose to move to a purely strategic and advisorial role.”

Most companies should be constantly running running at least one exec search. Post-product/market fit, the limiting factor to scale generally derives from some version of not having enough great leaders.

— Zachary Perret (@zachperret) June 18, 2019

Plaid builds infrastructure that allows consumers to interact with their bank account on the web, powering a number of third-party applications, like Venmo, Robinhood, Coinbase, Acorns and LendingClub. It rose to prominence recently, closing a $250 million Series C investment at a $2.65 billion valuation late last year. The deal was led by famed venture capitalist and author of the Internet Trends report Mary Meeker, who’s joined the startup’s board of directors.

In total, Plaid has secured $310 million in venture capital funding from Andreessen Horowitz, Index Ventures, Norwest Venture Partners, Coatue Management, Goldman Sachs, NEA, Spark Capital and others.

Plaid has integrated with 15,000 banks in the U.S. and Canada and says 25% of people living in those countries with bank accounts have linked with Plaid through at least one of the hundreds of apps that leverage Plaid’s application program interfaces (APIs) — an increase from 13% last year. Last month, the company launched its fintech platform in the U.K.

“As we’ve done in the U.S., Plaid will become the foundation for that growth by providing access to a financial network that allows developers to deliver the experience users expect from their financial apps,” the company wrote in a blog post.

TechCrunch participated in a panel discussion with Hockey and Brex CEO Henrique Dubugras last month, in which Hockey gave no indication of impending plans to leave the business. In fact, taking off just as Plaid amps up its global expansion efforts and accelerates growth is strange timing for a founder to depart.

Oftentimes, when a startup co-founder steps down from the C-suite, it’s to make room for a more experienced executive to lead the company through periods of fast growth. Recently, for example, Lime announced its co-founder Toby Sun would transition out of the CEO role to focus on company culture and R&D. Brad Bao, a Lime co-founder and longtime Tencent executive, assumed chief responsibilities.

Other times, it comes amid turmoil. Mike Cagney’s departure from SoFi, of course, is an example of this. One month after reports of a sexual harassment and wrongful termination lawsuit against the online lending business surfaced, SoFi announced Cagney would step down.

In Hockey’s case, the move was planned and calculated, he said. Plaid chief operating officer Eric Sager, who joined earlier this year, Perret and other executives will take over engineering and product reports, among Hockey’s other responsibilities.

“In tech, it has historically been taboo to talk about founders or executives transitioning to different roles inside companies,” Hockey writes. “Leadership transitions need to become a bedrock of any company that desires to endure across decades.”

Powered by WPeMatico

Optimizely, a platform that offers tools for A/B testing and personalization on the web and in mobile apps, today announced that it has raised a total of $105 million. This includes a $50 million Series D round led by Goldman Sachs Private Capital, with the participation of Accenture Ventures, as well as a $55 million line of credit from Bridge Bank.

Goldman Sachs’s Michael Kondoleon will join Optimizely’s board of directors as a board member.

“We’re excited to reach this milestone because these investments cement our leadership position in the market,” Optimizely CEO Jay Larson told me. “We can invest more in products to put an even bigger gap between Optimizely and our competition. We can expand geographically. And we will continue to grow our team of world-class digital optimization experts. This is a big day for Optimizely and a big day for the experimentation and personalization industry.”

The company notes that about a quarter of the Fortune 100 currently use its services. The company says it now handles more than 6 billion events a day and that its customers have tripled their investments in digital experience optimization in the last two years. Current customers include the likes of Gap, Visa, IBM, StubHub, Metromile, Lending Club and Sonos.

The company notes that about a quarter of the Fortune 100 currently use its services. The company says it now handles more than 6 billion events a day and that its customers have tripled their investments in digital experience optimization in the last two years. Current customers include the likes of Gap, Visa, IBM, StubHub, Metromile, Lending Club and Sonos.

In total, Optimizely has now raised more than $200 million, excluding the line of credit. The additional $55 million from Bridge Bank is a bit unusual, but not completely out of the ordinary for companies at this stage. “Bridge Bank is proud to continue working with Optimizely, a global leader at the forefront of the digital experience optimization market,” said Mike Lederman, senior vice president and western region director of Bridge Bank’s technology banking group. “Optimizely is on a path of substantial growth and the additional capital will help them continue to build market-leading products that are used by an increasing number of top global brands.”

As is pretty much standard for companies at this stage, Optimizely will use the new funding to drive growth.

Powered by WPeMatico

Carta, a seven-year-old, San Francisco-based startup, is the newest unicorn in tech. The company, which largely helps private company investors, founders, and employees manage their equity and ownership, tells TechCrunch it has raised $300 million in a Series E round at a $1.7 billion valuation, led by Andreessen Horowitz. Firm co-founder Marc Andreessen is also joining the board.

The round has been a poorly kept secret. The outlet The Information reported more than a month ago the details that Carta is sharing today. In fact, that leak has given people in the industry who understand Carta’s business time to quietly ask of its valuation whether it isn’t high for a company that does what it does.

Unsurprisingly, Carta argues that it is not, that it has evolved considerably from the outset — which is true. Though it launched as a way for venture-backed companies to mange equity, issue securities, and track their cap tables, by 2014, Carta, formerly known as eShares, had moved beyond replacing paper records and into selling as a monthly service appraisals of the fair market value of private companies’ common stock in order to determine their strike price. It calls this “409A-as-a-service.”

Carta has continued tacking on more services. Among the most notable was the launch last year of a fund administration product designed to help venture capital firms not only manage their portfolio stakes more easily but to more seamlessly work with their own investors or limited partners. Toward this end, Carta now provides portfolio analytics, including deal IRRs and cash management, it helps VCs distribute their quarterly investor reports and it integrates with third-party tax and payroll providers.

Carta has so many pieces in place that in a call on Friday, founder and CEO Henry Ward told us Carta is taking what may be its biggest step yet and becoming the first real “private stock market for companies.” Its massive new funding round is “about act three,” he said. “Now that you have this network of companies and investors all on one platform and the ability to transfer securities, you can build liquidity on top of it.” It’s this vision that enticed Andreessen to jump aboard, he suggested.

There’s unquestionably a need for a kind of private stock market. Private funding has been outpacing IPO funding for years, and it shows no sign of stopping. It’s largely why the SEC is trying to better enable people who are not accredited investors to access private company shares. Most of the U.S. has missed out on the wealth creation happening before companies go public or sell to other companies.

It’s also true that Carta has its hooks into a meaningful number of startups and venture firms at this point. The company says more than 700,000 shareholders are on its platform, that it works with more than 11,000 companies and that its fund administration product now serves 143 venture firms.

Still, some longtime industry observers wonder if Carta isn’t mashing together a lot of disparate, moderately lucrative businesses and positioning it as the next-big platform company, and the view resonates. For one thing, Carta likes to talk about assets managed, though it’s really talking about how much in assets the startups and VCs that use its platform control, which is $575 billion altogether. Carta — which now employs nearly 600 employees across seven offices — says its own annual revenue run rate is currently $55 million.

Relatedly, while Ward says Carta’s primary revenue right now is its software subscription business — another revenue stream is the money it’s paid by the venture firms that use it as a fund administrator — people who question Carta’s fundraising note the people-intensive nature of the kind of work that Carta has been systemizing. Yes, there’s a sophisticated software component, but Carta is more Accenture than Salesforce, and services businesses are valued very differently.

There’s also the question of growth. Ward points to the roughly 450 startups that are garnering venture funding each month right now — all potential customers for Carta. But plenty of companies are also quietly going out of business all the time, a process that will accelerate whenever this very long funding boom finally slows.

This newest business conveys the impression that big things are coming, though it doesn’t sound exactly like a private stock market as Ward describes it, either. Primarily, it won’t provide the relative transparency that stock markets do. We don’t think that’s the case, anyway. Ward was somewhat dismissive of questions we asked about how Carta’s newest business will be fundamentally different than that of secondary players in the market that are already making it possible for shareholders to value and transact shares.

Indeed, though Carta says it’s changing how assets are acquired, valued and transacted, Ward also did not respond to several simple follow-up queries sent to him on Friday about the mechanics of this new business, dubbed CartaX. Instead, he thanked us for our efforts to understand and articulate Carta’s business. Meanwhile, his press team told us it was limited in what it can say about how CartaX operates for now.

Carta has savvy investors. In addition to Andreessen Horowitz, this newest round includes Lightspeed Venture Partners, Goldman Sachs Principal Strategic Investments, Tiger Global, Thrive Capital and earlier backers Tribe Capital, Menlo Ventures and Meritech Capital.

No doubt that in valuing the company, they took into account that Solium — a Canada-based software-as-a-service for stock administration, financial reporting and compliance that was publicly traded — sold for $900 million in cash earlier this year to Morgan Stanley. That’s roughly double Carta’s total funding so far of $447 million.

More likely, they were viewing the company based on its potential as a kind of more liquid market, ambitious as that might seem today. Consider that the parent company to both the NYSE and the Chicago Stock Exchange currently has a market cap of roughly $45 billion. Then again, that company operates 12 exchanges and marketplaces altogether, and it enjoyed more than $6 billion in revenue last year by transacting more than a $100 billion dollars in volume on the NYSE alone on a daily basis.

Perhaps most important to them, Carta is now as well-positioned as anyone to capture and cater to the growing number of privately held companies looking to provide more of their employees liquidity and to cash out early investors. Add to the mix a mega-round and a star board member, and the company may well get to where Ward and his investors want it to go.

We’ll be watching to see.

[Correction: We’d originally misstated the market cap of Intercontinental Exchange, owner of the NYSE and Chicago Stock Exchange, among other marketplaces; we cited its annual revenue instead.]

Powered by WPeMatico

The RealReal, an online retailer for authenticated luxury consignment, has authorized the sale of up to $70 million in new shares, per a Delaware stock authorization filing discovered by the Prime Unicorn Index. If the company raises the entire amount, it would reach a valuation of $1.06 billion, cementing its status as the newest e-commerce unicorn.

The filing doesn’t guarantee The RealReal will sell the full amount of authorized shares. The company declined to comment on its fundraising plans.

The RealReal is led by founder and chief executive officer Julie Wainwright (pictured), the former CEO of Pets.com, a company now synonymous with the dot-com bust. It has raised quite a bit of capital to date — a total of $288 million from venture capital and private equity backers, including Great Hill Partners, Sandbridge Capital, PWP Growth Equity, Industry Ventures, Greycroft Partners and Canaan Partners. Most recently, The RealReal closed a Series G financing of $115 million in July 2018 that valued the business at $745 million, per PitchBook.

The RealReal has recently expanded its brick-and-mortar footprint and added additional e-commerce fulfillment centers as demand increased for its supply of second-hand luxury items. Founded in 2011, the company operates eight luxury consignment offices, where customers can receive free valuations of their luxury items. The RealReal is headquartered in San Francisco.

In a conversation with TechCrunch in 2017, Wainwright confirmed the company’s intent to go public at some point. With this upcoming round, The RealReal would be well placed for a 2020 initial public offering.

“That’s the goal,” Wainwright said during the interview. “We really aren’t in the mood to sell the business, we’re in the mood to go public at some point in the future.”

The RealReal competes with fellow second-hand e-tailers ThredUp and Poshmark . The latter is gearing up for a fall IPO, according to The Wall Street Journal. The online marketplace has tapped Morgan Stanley and Goldman Sachs to lead its offering after closing in on $150 million in revenue in 2018. ThredUp, another major player in the fashion retail market, hasn’t raised capital since 2015, but did begin opening physical stores in 2017 as part of its greater effort to compete with fellow venture-backed second-hand e-tailers.

The RealReal would also be the latest in a series of high-profile female-founded companies to gain unicorn status. Glossier tripled its valuation to $1.2 billion with a $100 million round earlier this year, followed by Rent the Runway, which attracted a $125 million investment at a $1 billion valuation, to name a few.

Powered by WPeMatico

Zoom, the only profitable unicorn in line to go public, priced its initial public offering at between $28 and $32 per share Monday morning. The video conferencing business plans to trade on the Nasdaq under the ticker symbol “ZM.”

Zoom, valued at $1 billion in 2017, initially filed to go public in March. According to its amended IPO filing, the company will raise up to $348.1 million by selling 10.9 million Class A shares. The offering will grant Zoom a fully diluted market value of $8.7 billion, a more than 8x increase to its latest private market valuation.

Although the company has garnered praise for its stellar financials — Zoom posted $330 million in revenue in the year ending January 31, 2019, a remarkable 2x increase year-over-year, with a gross profit of $269.5 million — the road to IPO hasn’t been without hiccups.

The company’s founder and chief executive officer Eric Yuan last night published an open letter concerning the conduct of Zoom’s chief financial officer Kelly Steckelberg. According to the letter, Zoom was recently informed by an anonymous source that Steckelberg had an “undisclosed, consensual relationship” during her tenure at a previous employer.

Steckelberg was most recently the CEO of the online dating site Zoosk; before that, she was a senior director in consumer finance at Cisco . The letter does not specify where the relationship took place, when or with whom.

Losing a CFO mere days before an IPO would have been a major loss for Zoom. CFOs often become the face of the IPO, handling the grueling tasks associated with crafting an IPO prospectus, leading the roadshow and more, while also maintaining day-to-day financial operations.

Yuan writes that the Zoom’s board of directors conducted a full investigation into the matter and determined that Steckelberg would stay on as Zoom’s CFO: “Kelly expressed regret for what transpired at her former employer, took ownership for the situation, and made clear to us that she had learned valuable lessons from the experience,” he wrote.

“We appreciated Kelly’s openness and candor during this process,” he continued. “It is clear that this matter related only to circumstances at her former employer. During Kelly’s tenure at Zoom, she has been an incredible contributor, as well as a model steward of our culture, values, and high standards since joining the Company.”

We reached out to Zoosk for comment. Zoom declined to comment further.

Zoom, expected to make the final call on its IPO price next Wednesday, will likely price at the top of the range and see a clean pop on its first day on the markets given its clean track record and positive financials. The business was founded in 2011 by Eric Yuan, an early engineer at WebEx, which sold to Cisco for $3.2 billion in 2007. Before launching Zoom, he spent four years at Cisco as its vice president of engineering.

Zoom has raised $145 million to date from investors, including Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent pre-IPO stake); Digital Mobile Venture (8.5 percent), a fund affiliated with former Zoom board member Samuel Chen; and Bucantini Enterprises Limited (5.9 percent), a fund owned by Li Ka-shing, a Chinese billionaire and among the richest people in the world.

Morgan Stanley, JP Morgan and Goldman Sachs are leading its offering.

Powered by WPeMatico

Less than a decade ago IPOs, acquisitions and global expansion by African startups were more possibility than reality. March saw all three from the continent’s tech scene.

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange, per SEC documents and confirmation from chief executive Sacha Poignonnec.

In an updated filing, (since the March 12 original) Jumia indicated it will offer 13,500,000 ADR shares, for an offering price of $13 to $16 per share to trade under the ticker symbol “JMIA.” The IPO could raise up to $216 million for Jumia.

Since our first story (and reflected in the latest SEC docs), Mastercard Europe agreed upfront to buy $50 million in Jumia ordinary shares.

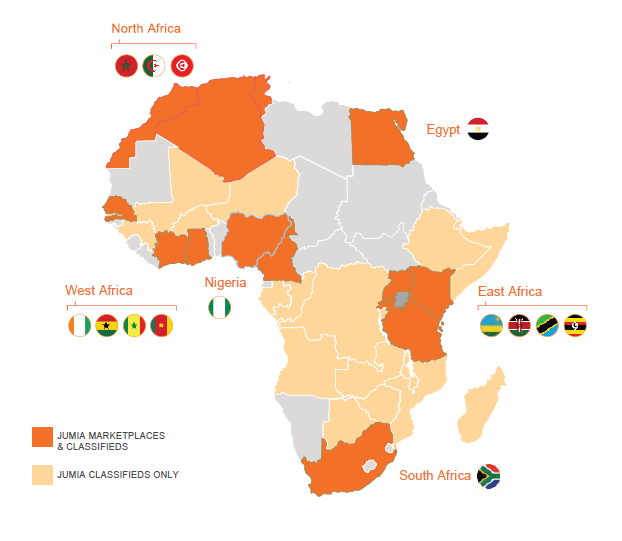

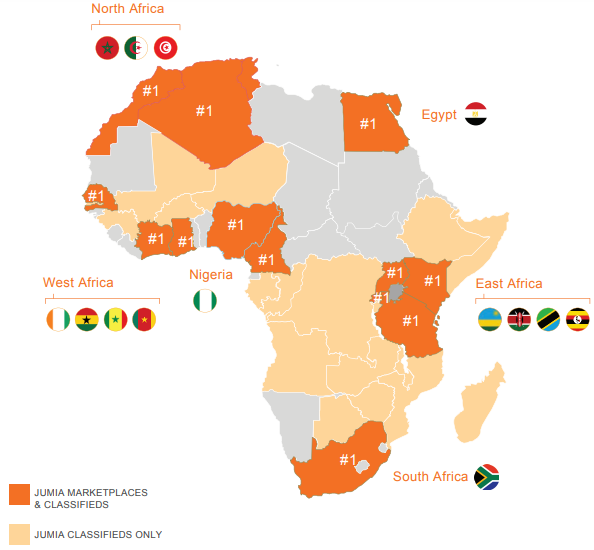

With a smooth filing process, Jumia will become the first African startup to list on a major global exchange. The company is incorporated in Germany, but maintains its headquarters in Nigeria, and operates exclusively in Africa, with 4,000 employees on the continent.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data. The company has started to generate annual revenues over $100 million, but like many burn-rate startups, has done so while racking up big losses.

There’ll be a lot more to cover, analyze and debate pre and post Jumia’s NYSE bell toll — which could happen in coming weeks or months. For example, can Jumia generate a profit; is it really an African startup; will Jumia become an acquisition target for a big outside name or an acquirer of smaller startups in African e-commerce? Stay tuned for continuing TechCrunch coverage.

On the acquisition front, Lagos-based online lending startup OneFi bought Nigerian payment solutions company Amplify for an undisclosed amount.

OneFi is taking over Amplify’s IP, team and client network of more than 1,000 merchants to which Amplify provides payment processing services, OneFi CEO Chijioke Dozie told TechCrunch.

The purchase of Amplify caps off a busy period for OneFi. Over the last seven months the Nigerian venture secured a $5 million lending facility from Lendable, announced a payment partnership with Visa and became one of the first (known) African startups to receive a global credit rating. OneFi is also dropping the name of its signature product, Paylater, and will simply go by OneFi (for now).

Collectively, these moves represent a pivot for OneFi away from operating primarily as a digital lender, toward becoming an online consumer finance platform.

“We’re not a bank but we’re offering more banking services…Customers are now coming to us not just for loans but for cheaper funds transfer, more convenient bill payment, and to know their credit scores,” said Dozie.

OneFi will add payment options for clients on social media apps, including WhatsApp, this quarter — something in which Amplify already holds a specialization and client base. Through its Visa partnership, OneFi will also offer clients virtual Visa wallets on mobile phones and start providing QR code payment options at supermarkets, on public transit and across other POS points in Nigeria.

On the back of the acquisition, OneFi is in the process of raising a round and will look to expand internationally, considering Senegal, Côte d’Ivoire, DRC, Ghana and Egypt and Europe for Diaspora markets.

On African startups expanding globally, FlexClub — a South African venture that matches investors and drivers to cars for ride-hailing services — announced it will expand in Mexico in a partnership with Uber after closing a $1.2 million seed round led by CRE Venture Capital.

The move comes as Africa’s tech-transit space continues to produce unique mobility solutions shaped around local needs.

FlexClub touts itself as a “gig economy investment platform” that is creating new asset classes in emerging markets, according to chief executive and co-founder Tinashe Ruzane.

That asset class, for now, is ride-hail vehicles. FlexClub allows investors to go on the site and purchase a car (ultimately managed and serviced by FlexClub). The startup then connects that car to an Uber driver who uses earnings to pay a weekly rental charge.

Those fees generate monthly fixed-rate interest income for the investor. The driver has the option of buying the car after 12 months, with a descending purchase price over time.

FlexClub’s platform manages the investment, rental income and disbursement of funds across all parties. The startup also handles insurance, maintenance and upkeep of the cars.

Ruzane envisions this as a model to finance multiple asset classes in emerging markets — where lending options are fewer for individuals who may not have credit histories.

“Our goal is to make this completely passive… where investors can invest in different kinds of assets on our platform, login to a dash, and see this is how my five cars in South Africa are doing, my vans in Mexico, my motorbikes in Indonesia — with a diversified portfolio around the world,” he explained.

FlexClub will begin work matching investors to cars and Uber drivers in Mexico in April. The startup sees opportunities to move into other mobility classes, such as Africa’s ride-hail motorcycle taxi and three-wheel tuk-tuk market, CEO Tinashe Ruzane told TechCrunch in this feature.

And finally, francophone Africa will see a boost in funds and support for startups. The Dakar Network Angels group launched last month, making its first investment to cleantech venture Coliba — an Ivorian startup that uses a mobile app to coordinate waste recycling

The deal is part of Dakar Network Angels’ mission of convening experts and capital to bridge the resource gap for startups in French-speaking Africa — or 24 of the continent’s 54 countries.

The organization — which goes by DNA for short — will offer seed fund investments of between $25,000 to $100,000 to early-stage ventures with high growth potential. These rounds will come with the entrepreneurial guidance of DNA’s angel network.

Launched in Senegal, the organization’s founder Marieme Diop — a VC investor at Orange Digital Ventures — named the goal of bridging VC disparities between francophone and non-francophone Africa as the primary driver for DNA. She pointed to funding data by Partech, indicating that 76 percent of investment to African startups goes to three English-speaking countries — Nigeria, Kenya and South Africa.

To gain consideration for DNA investment, startups must gain referral by a member. DNA will take a minority stake (less than 10 percent) in ventures that receive seed funds and provide program mentorship until exits, Diop told TechCrunch.

To become an angel, members must commit to investing a minimum of $10,000 a year (for those coming on as individuals), $20,000 (for corporates) and be on hand to support the portfolio startups, according to DNA’s Corporate Membership Charter.

More Africa Related Stories @TechCrunch

African Tech Around The Net

Powered by WPeMatico

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico