Goldman Sachs

Auto Added by WPeMatico

Auto Added by WPeMatico

Amount, a new service that helps traditional banks compete in a digital world, has raised $81 million from none other than Goldman Sachs as it looks to help legacy fintech players compete with their more nimble digital counterparts.

The company, which spun out from the startup lending company Avant in January of this year, has already inked deals with Banco Popular, HSBC, Regions Bank and TD Bank to power their digital banking services and offer products like point-of-sale lending to compete with challenger banks like Chime and lenders like Affirm or Klarna.

“Most banks are looking for resources and infrastructure to accelerate their digital strategy and meet the demands of today’s consumer,” said Jade Mandel, a vice president in Goldman Sachs’ growth equity platform, GS Growth, who will be joining the board of directors at Amount, in a statement. “Amount enables banks to navigate digital transformation through its modular and mobile-first platform for financial products. We’re excited to partner with the team as they take on this compelling market opportunity.”

Complementing those customer-facing services is a deep expertise in fraud prevention on the back-end to help banks provide more loans with less risk than competitors, according to chief executive Adam Hughes.

It’s the combination of these three services that led Goldman to take point on a new $81 million investment in the company, with participation from previous investors August Capital, Invus Opportunities and Hanaco Ventures — giving Amount a post-money valuation of $681 million and bringing the company’s total capital raised in 2020 to a whopping $140 million.

Think of Amount as a white-labeled digital banking service provider for Luddite banks that hadn’t upgraded their services to keep pace with demands of a new generation of customers or the COVID-19 era of digital-first services for everything.

Banks pay a pretty penny for access to Amount’s services. On top of a percentage for any loans that a bank processes through Amount’s services, there’s an up-front implementation fee that typically averages at $1 million.

The hefty price tag is a sign of how concerned banks are about their digital challengers. Hughes said that they’ve seen a big uptick in adoption since the launch of their buy-now-pay-later product designed to compete with the fast growing startups like Affirm and Klarna .

Indeed, by offering banks these services, Amount gives Klarna and Affirm something to worry about. That’s because banks conceivably have a lower cost of capital than the startups and can offer better rates to borrowers. They also have the balance sheet capacity to approve more loans than either of the two upstart lenders.

“Amount has the wind at its back and the industry is taking notice,” said Nigel Morris, the co-founder of Capital One and an investor in Amount through the firm QED Investors. “The latest round brings Amount’s total capital raised in 2020 to nearly $140 million, which will provide for additional investments in platform research and development while accelerating the company’s go-to-market strategy. QED is thrilled to be a part of Amount’s story and we look forward to the company’s future success as it plays a vital role in the digitization of financial services.”

FT Partners served as advisor to Amount on this transaction.

Powered by WPeMatico

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

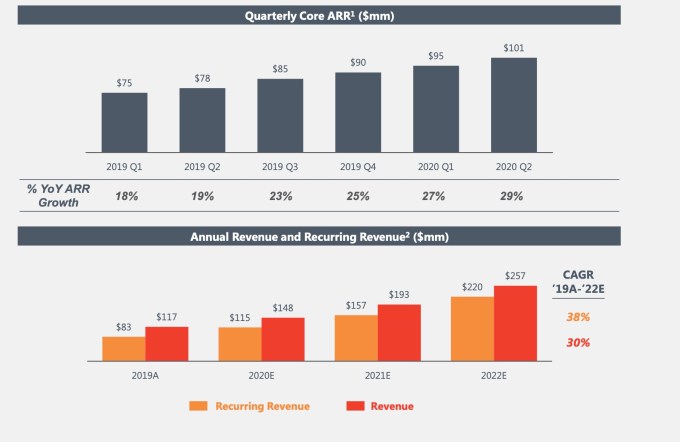

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico

Coupa Software, a publicly traded company that helps large corporations manage spending, announced that it was buying Llamasoft, an 18-year-old Michigan company that helps large companies manage their supply chain. The deal was pegged at $1.5 billion.

This year Llamasoft released its latest tool, an AI-driven platform for managing supply chains intelligently. This capability in particular seemed to attract Coupa’s attention, as it was looking for a supply chain application to complement its spend management capabilities.

Coupa CEO and chairman Rob Bernshteyn says when you combine that supply chain data with Coupa’s spending data, it can produce a powerful combination.

“Llamasoft’s deep supply chain expertise and sophisticated data science and modeling capabilities, combined with the roughly $2 trillion of cumulative transactional spend data we have in Coupa, will empower businesses with the intelligence needed to pivot on a dime,” Bernshteyn said in a statement.

The purchase comes at a time when companies are focusing more and more on digitizing processes across enterprise, and when supply chains can be uncertain, depending on the location of COVID hotspots at any particular time.

“With demand uncertainty on one hand, and supply volatility on the other, companies are in need of supply chain technology that can help them assess alternatives and balance trade-offs to achieve desired business results. LLamasoft provides these capabilities with an AI-powered cloud platform that empowers companies to make smarter supply chain decisions, faster,” the company wrote in a statement.

Llamasoft was founded in 2002 in Ann Arbor, Michigan and has raised more than $56 million, according to Crunchbase data. Its largest raise was a $50 million Series B in 2015 led by Goldman Sachs .

The company generated more than $100 million in revenue and has 650 big customers, including Boeing, DHL, Kimberly-Clark and GM, according to company data.

Coupa has been extremely acquisitive over the years, buying 17 companies, according to Crunchbase data. This deal represents the fourth acquisition this year for the company. So far the stock market is not enamored with the acquisition; the company’s stock price is down 5.20% at publication.

Powered by WPeMatico

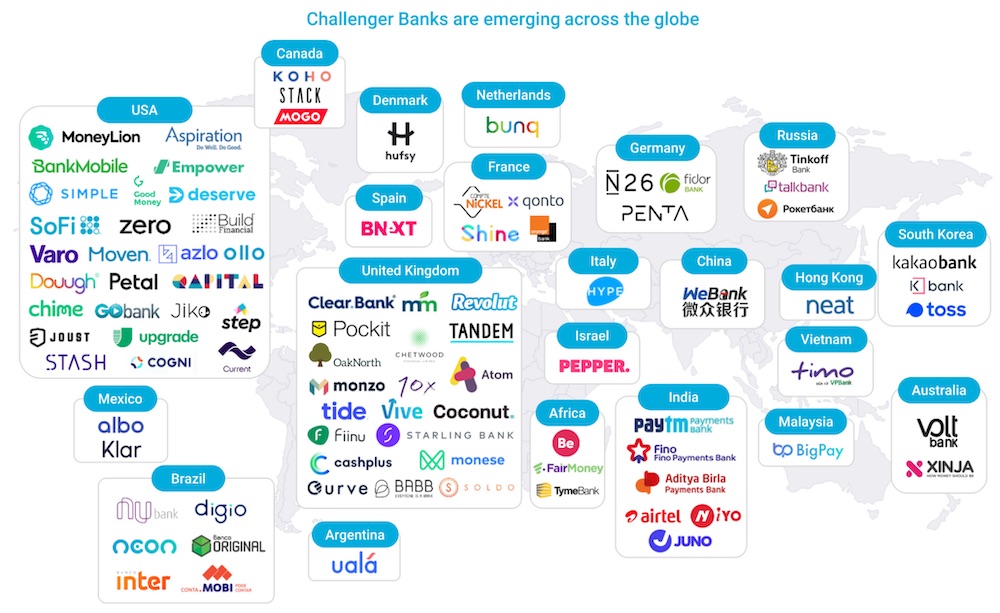

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Paige, the startup that spun out of the Memorial Sloan Kettering Cancer Center and launched in 2018 to help advance cancer research and care by applying AI to better understand cancer pathology, is today announcing a milestone in its growth story: it has raised a further $20 million from Goldman Sachs and Healthcare Venture Partners, closing out its Series B at $70 million.

Leo Grady, Paige’s CEO, says the funding will go toward several areas.

It will be used for hiring; to continue expanding its partnerships with biopharmaceutical companies (deals that have not yet been made public); and to continue investing in clinical work, based around algorithms it has built and trained using more than 25 million pathology slides in MSK’s archive, plus IP related to the AI-based computational pathology that underpins Paige’s work. It will also be used to help it expand to the U.K. and Europe. Paige has a CE mark to be used clinically in both regions and the startup already has beta sites in the U.K. and EU, but it hasn’t had a fully commercial launch in either region, Grady said.

Paige — which has now raised more than $95 million with other investors, including Breyer Capital, MSK and Kenan Turnacioglu — is keeping quiet about its valuation. But for some context, we noted that it was around $208 million when the first tranche of the round was announced — $45 million in December 2019, with a further $5 million in April. It attracted this latest $20 million in part because business has been strong, Grady noted. As a result, despite it being a generally tough climate for raising money right now, Paige didn’t face those challenges.

“The climate in which Goldman made its initial investment” — the $5 million round in April — “was when COVID-19 had hit hard and they were realising the magnitude,” Grady said. “They wanted to see how things played out for Paige in the economy. But the way it has been going has been encouraging.”

Indeed, a lot of attention these days is focused around the current public health crisis making its way around the world in the form of COVID-19, and the knock-on effects that it is having across the economy and socially. Paige’s growth in that context has been interesting.

We’re still in the early stages of understanding COVID-19 and how it interacts with other conditions (such as cancer) — and it’s not an area that Paige is directly exploring in its work. But in the meantime, its platform — based around digitised slides — has come into its own for clinicians and others who can no longer regularly physically visit laboratories.

Paige’s enterprise imaging system — the company was co-founded by Dr Thomas Fuchs, known as the “father of computational pathology” and is the director of Computational Pathology in The Warren Alpert Center for Digital and Computational Pathology at Memorial Sloan Kettering, as well as a professor of machine learning at the Weill Cornell Graduate School of Medical Sciences; and Dr David Klimstra, chairman of the department of pathology at MSK — allows users to view digital slides remotely, and while all hardware manufacturers today have digital viewers, these are proprietary, tied to those scanners and “not built for high performance,” Grady noted.

Paige’s platform allows its users not only to share research and primary data without physically sending slides around, but to use high performance software built to “read” the data in a more comprehensive way than clinicians and researchers would otherwise be able to do. That initially has been applied to work in prostrate and breast cancers but is now also being explored around other cancers as well, Grady said. “We’re adding in information to the workflow, boosting the confidence and quality of data. The first piece [the platform and the slides] enables the second piece.”

The Goldman Sachs investment is coming from the financial services giant’s merchant banking division, and as part of it, David Castelblanco, MD at Goldman Sachs, has joined Paige’s board of directors.

“We have been very impressed with the company and its pace of development,” he said in a statement. “We are excited to increase our commitment to support Leo, Thomas and the Paige team’s transformative work with artificial intelligence and machine learning in the cancer field.”

“We initially invested in Paige recognizing the potential of their products to add significant value to the industry and impact the future of cancer care,” added Jeffrey C. Lightcap, senior managing director of Healthcare Venture Partners. “After seeing Paige make tremendous progress in such a short period, we added to our investment to further accelerate their growth.”

Powered by WPeMatico

I recently sat on a panel for gaming website Pocket Gamer that was focused on esports and the Olympics. We were debating whether esports were filling the gap in sporting events, including the Olympic games, which have been paused due to the COVID-19 pandemic.

It was an interesting conversation that started out like most esports panels. The only difference here is that instead of the typical question, “When will esports catch up to traditional sports?” it was, “Will esports become mainstream enough to make it into the Olympics?” A slightly different question, but the same sentiment: The international games are one of televised sports’ marquee events, and esports companies hope to earn a seat at the grown-up’s table.

In truth, the Olympics have been dropping in ratings relatively steadily in the U.S. for a long time. The only Olympic games that scored in the top five ratings going back to 1992 were the Salt Lake City Winter Olympics, presumably because they were held in the United States. Overall, viewership has been declining in recent years and the games don’t hold the prestige they once did.

Additionally, audiences are slowly becoming worth less and less to advertisers because the age of the average viewer is rising rapidly, a trend we are seeing in almost all traditional sports.

I doubt it would surprise anyone to learn that the average age of almost all traditional sports viewership skews older than esports’ audience. Even then, I think the actual data will be quite surprising. Only one professional sport (women’s tennis) actually saw its average viewers age come down in the last decade or so. Even in that context, the average age of a Women’s Tennis Association home spectator is 55 years old.

The average age of esports viewership looks to be around 26 years old. Think about that from a marketer’s perspective. Traditional sports are just missing young people, by a wide margin.

But there are more factors at play than just a lack of interest from millennials and Gen Z driving this trend: There’s also a question of access.

The IOC made the decision in recent years to stream the Olympics (the way most younger people consume content), but it capped the ability to watch online to 30 minutes if viewers didn’t sign in with their cable company (a relationship many millennials don’t have) to continue watching.

Additionally, the IOC made the laughable decision to “ban” GIFs with the press covering the event, which qualifies as one of the more stupid things a governing body has ever tried to do. First, it won’t work. Secondly, and more to the point, it demonstrates how out of touch the IOC is with the ways in which media has evolved in the last 20 years.

However, unlike the Olympics, where no corporation owns the rights to volleyball or the pole vault, all esports companies own the IP associated with the game itself. That means, by default, the IOC would not have carte blanche when making decisions about how to represent the games, programming, licensing rights and other factors it has enjoyed for a long time.

Finally, it’s worth noting that the IOC doesn’t like the idea of “violent” games being added to the Olympic roster. It would prefer to see current sports transformed into virtual competitions. But anyone who knows anything about esports understands that this isn’t how esports works. Before a game ascends to esports royalty, it needs to be a good game. If nobody plays it, it’s unlikely anyone will want to watch it.

Secondly, it has be digestible as a viewing experience. World of Warcraft Arena is a game that draws a lot of players, but it’s almost impossible to know what is going on unless you’re an expert at the game or you have a godly shoutcaster who can translate the on-screen action. You can’t make track and field an esport and hope audiences will want to watch.

The IOC has taken steps to try and stave off declining youth viewership trends by adopting sports considered “young” in the past few years. Five sports recently added to the Olympic games include:

The baseball/softball addition notwithstanding, I think you would have to live under a rock if you thought that competitive sport climbing held a candle to Fortnite or League of Legends in terms of generating youth interest. Frankly, this seems like an idea that came from an old person trying to find a way to “get the kids back.”

To the IOC’s credit, it has begun to hold panels and conferences with esports experts and game publishers, but the deals that will come from these will look REALLY different than what they are used to. It seems to me that we have a long way to go here.

For my part of the panel, I argued that the Olympics need esports much more than esports need the Olympics. Media companies are only going to overpay for broadcasting rights for traditional sports for so long. At some point, someone is going to notice that the “inside the demo” group isn’t there and move on.

The thing that esports CAN get from the Olympics is understanding a better way to monetize its audience, something that the Olympics do well and esports doesn’t do well right now. A report from Goldman Sachs shows the audience size and monetization based on that audience, showing that esports dramatically underindex on monetization relative to their more established sports league equivalents. It is clear that esports is immature from a monetization perspective and, while the Olympics aren’t on this chart, I would assume that it punches WAY above its weight, much like MLB does, trading on its reputation more than on actual results these days.

The IOC should act fast, though. It won’t be long until esports figures this whole thing out and once they do, the Olympic games won’t have anything to offer this emerging media powerhouse.

Powered by WPeMatico

Some of Latin America’s leading venture capital investors are now backing hotel chains.

In fact, Ayenda, the largest hotel chain in Colombia, has raised $8.7 million in a new round of funding, according to the company.

Led by Kaszek Ventures, the round will support the continued expansion of Ayenda’s chain of hotels in Colombia and beyond. The hotel operator already has 150 hotels operating under its flag in Colombia and has recently expanded to Peru, according to a statement.

Financing came from Kaszek Ventures and strategic investors like Irelandia Aviation, Kairos, Altabix and BWG Ventures.

The company, which was founded in 2018, now has more than 4,500 rooms under its brand in Colombia and has become the biggest hotel chain in the country.

Investments in brick and mortar chains by venture firms are far more common in emerging markets than they are in North America. The investment in Ayenda mirrors big bets that SoftBank Group has made in the Indian hotel chain Oyo and an investment made by Tencent, Sequoia China, Baidu Capital and Goldman Sachs, in LvYue Group late last year, amounting to “several hundred million dollars”, according to a company statement.

“We’re seeking to invest in companies that are redefining the big industries and we found Ayenda, a team that is changing the hotel’s industry in an unprecedented way for the region”, said Nicolas Berman, Kaszek Ventures partner.

Ayenda works with independent hotels through a franchise system to help them increase their occupancy and services. The hotels have to apply to be part of the chain and go through an up to 30-day inspection process before they’re approved to open for business.

“With a broad supply of hotels with the best cost-benefit relationship, guests can travel more frequently, accelerating the economy,” says Declan Ryan, managing partner at Irelandia Aviation.

The company hopes to have more than 1 million guests in 2020 in their hotels. Rooms list at $20 per-night, including amenities and an around the clock customer support team.

Oyo’s story may be a cautionary tale for companies looking at expanding via venture investment for hotel chains. The once high-flying company has been the subject of some scathing criticism. As we wrote:

The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Powered by WPeMatico

Early Stage SF is around the corner, on April 28 in San Francisco, and we are more than excited for this brand new event. The intimate gathering of founders, VCs, operators and tech industry experts is all about giving founders the tools they need to find success, no matter the challenge ahead of them.

Struggling to understand the legal aspects of running a company, like negotiating cap tables or hiring international talent? We’ve got breakout sessions for that. Wondering how to go about fundraising, from getting your first yes to identifying the right investors to planning the timeline for your fundraise sprint? We’ve got breakout sessions for that. Growth marketing? PR/Media? Building a tech stack? Recruiting?

We. Got. You.

Today, we’re very proud to announce one of our few Main Stage sessions that will be open to all attendees. Reid Hoffman and Sarah Guo will join us for a conversation around “How To Raise Your Series A.”

Reid Hoffman is a legendary entrepreneur and investor in Silicon Valley. He was an Executive VP and founding board member at PayPal before going on to co-found LinkedIn in 2003. He led the company to profitability as CEO before joining Greylock in 2009. He serves on the boards of Airbnb, Apollo Fusion, Aurora, Coda, Convoy, Entrepreneur First, Microsoft, Nauto and Xapo, among others. He’s also an accomplished author, with books like “Blitzscaling,” “The Startup of You” and “The Alliance.”

Sarah Guo has a wealth of experience in the tech world. She started her career in high school at a tech firm founded by her parents, called Casa Systems. She then joined Goldman Sachs, where she invested in growth-stage tech startups such as Zynga and Dropbox, and advised both pre-IPO companies (Workday) and publicly traded firms (Zynga, Netflix and Nvidia). She joined Greylock Partners in 2013 and led the firm’s investment in Cleo, Demisto, Sqreen and Utmost. She has a particular focus on B2B applications, as well as infrastructure, cybersecurity, collaboration tools, AI and healthcare.

The format for Hoffman and Guo’s Main Stage chat will be familiar to folks who have followed the investors. It will be an updated, in-person combination of Hoffman’s famously annotated LinkedIn Series B pitch deck that led to Greylock’s investment, and Sarah Guo’s in-depth breakdown of what she looks for in a pitch.

They’ll lay out a number of universally applicable lessons that folks seeking Series A funding can learn from, tackling each from their own unique perspectives. Hoffman has years of experience in consumer-focused companies, with a special expertise in network effects. Guo is one of the top minds when it comes to investment in enterprise software.

We’re absolutely thrilled about this conversation, and to be honest, the entire Early Stage agenda.

Here’s how it all works:

There will be about 50+ breakout sessions at the event, and attendees will have an opportunity to attend at least seven. The sessions will cover all the core topics confronting early-stage founders — up through Series A — as they build a company, from raising capital to building a team to growth. Each breakout session will be led by notables in the startup world.

Don’t worry about missing a breakout session, because transcripts from each will be available to show attendees. And most of the folks leading the breakout sessions have agreed to hang at the show for at least half the day and participate in CrunchMatch, TechCrunch’s app to connect founders and investors based on shared interests.

Here’s the fine print. Each of the 50+ breakout sessions is limited to around 100 attendees. We expect a lot more attendees, of course, so signups for each session are on a first-come, first-serve basis. Buy your ticket today and you can sign up for the breakouts that we’ve announced. Pass holders will also receive 24-hour advance notice before we announce the next batch. (And yes, you can “drop” a breakout session in favor of a new one, in the event there is a schedule conflict.)

Grab yourself a ticket and start registering for sessions right here. Interested sponsors can hit up the team here.

Powered by WPeMatico

Venture capital investment exploded across a number of geographies in 2019 despite the constant threat of an economic downturn.

San Francisco, of course, remains the startup epicenter of the world, shutting out all other geographies when it comes to capital invested. Still, other regions continue to grow, raking in more capital this year than ever.

In Utah, a new hotbed for startups, companies like Weave, Divvy and MX Technology raised a collective $370 million from private market investors. In the Northeast, New York City experienced record-breaking deal volume with median deal sizes climbing steadily. Boston is closing out the decade with at least 10 deals larger than $100 million announced this year alone. And in the lovely Pacific Northwest, home to tech heavyweights Amazon and Microsoft, Seattle is experiencing an uptick in VC interest in what could be a sign the town is finally reaching its full potential.

Seattle startups raised a total of $3.5 billion in VC funding across roughly 375 deals this year, according to data collected by PitchBook. That’s up from $3 billion in 2018 across 346 deals and a meager $1.7 billion in 2017 across 348 deals. Much of Seattle’s recent growth can be attributed to a few fast-growing businesses.

Convoy, the digital freight network that connects truckers with shippers, closed a $400 million round last month bringing its valuation to $2.75 billion. The deal was remarkable for a number of reasons. Firstly, it was the largest venture round for a Seattle-based company in a decade, PitchBook claims. And it pushed Convoy to the top of the list of the most valuable companies in the city, surpassing OfferUp, which raised a sizable Series D in 2018 at a $1.4 billion valuation.

Convoy has managed to attract a slew of high-profile investors, including Amazon’s Jeff Bezos, Salesforce CEO Marc Benioff and even U2’s Bono and the Edge. Since it was founded in 2015, the business has raised a total of more than $668 million.

Remitly, another Seattle-headquartered business, has helped bolster Seattle’s startup ecosystem. The fintech company focused on international money transfer raised a $135 million Series E led by Generation Investment Management, and $85 million in debt from Barclays, Bridge Bank, Goldman Sachs and Silicon Valley Bank earlier this year. Owl Rock Capital, Princeville Global, Prudential Financial, Schroder & Co Bank AG and Top Tier Capital Partners, and previous investors DN Capital, Naspers’ PayU and Stripes Group also participated in the equity round, which valued Remitly at nearly $1 billion.

Up-and-coming startups, including co-working space provider The Riveter, real estate business Modus and same-day delivery service Dolly, have recently attracted investment too.

A number of other factors have contributed to Seattle’s long-awaited rise in venture activity. Top-performing companies like Stripe, Airbnb and Dropbox have established engineering offices in Seattle, as has Uber, Twitter, Facebook, Disney and many others. This, of course, has attracted copious engineers, a key ingredient to building a successful tech hub. Plus, the pipeline of engineers provided by the nearby University of Washington (shout-out to my alma mater) means there’s no shortage of brainiacs.

There’s long been plenty of smart people in Seattle, mostly working at Microsoft and Amazon, however. The issue has been a shortage of entrepreneurs, or those willing to exit a well-paying gig in favor of a risky venture. Fortunately for Seattle venture capitalists, new efforts have been made to entice corporate workers to the startup universe. Pioneer Square Labs, which I profiled earlier this year, is a prime example of this movement. On a mission to champion Seattle’s unique entrepreneurial DNA, Pioneer Square Labs cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest.

Boundless CEO Xiao Wang at TechCrunch Disrupt 2017

Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. Seattle is home to two of the most valuable businesses in the world, but it has not created as many founders as anticipated. PSL hopes that by removing some of the risk, it can encourage prospective founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon, to build.

“The studio model lends itself really well to people who are 99% there, thinking ‘damn, I want to start a company,’ ” PSL co-founder Ben Gilbert said in March. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Boundless is one of several successful PSL spin-outs. The business, which helps families navigate the convoluted green card process, raised a $7.8 million Series A led by Foundry Group earlier this year, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

Years-old institutional funds like Seattle’s Madrona Venture Group have done their part to bolster the Seattle startup community too. Madrona raised a $100 million Acceleration Fund earlier this year, and although it plans to look beyond its backyard for its newest deals, the firm continues to be one of the largest supporters of Pacific Northwest upstarts. Founded in 1995, Madrona’s portfolio includes Amazon, Mighty AI, UiPath, Branch and more.

Voyager Capital, another Seattle-based VC, also raised another $100 million this year to invest in the PNW. Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, closed on another $180 million to invest in early-stage consumer startups in May. And new efforts like Flying Fish Partners have been busy deploying capital to promising local companies.

There’s a lot more to say about all this. Like the growing role of deep-pocketed angel investors in Seattle have in expanding the startup ecosystem, or the non-local investors, like Silicon Valley’s best, who’ve funneled cash into Seattle’s talent. In short, Seattle deal activity is finally climbing thanks to top talent, new accelerator models and several refueled venture funds. Now we wait to see how the Seattle startup community leverages this growth period and what startups emerge on top.

Powered by WPeMatico

Bespoke Financial wants to provide cannabis businesses with the same kind of financial services that other businesses get, but that dispensaries and growers can’t yet access.

The regulations around cannabis operations are so stringent at the local level — and so nebulous at the federal level — that national banks won’t give businesses in the cannabis industry the same basic services (like short-term loans).

That’s why one former Goldman Sachs banker has partnered with two entrepreneurs from the traditional agriculture industry to create Bespoke Financial. And it’s why the company has raised $7 million in financing led by Casa Verde Capital — the investment firm launched by legendary cannabis aficionado, Calvin Broadus (AKA Snoop Dogg).

In some ways, George Mancheril is the new face of the cannabis business. The former banker hails from Goldman Sachs and Guggenheim Partners and worked on the desks that dealt with alternative lending.

A transplant to Los Angeles roughly six years ago, Mancheril says he saw the migration of legally sanctioned cannabis begin for recreational use and knew there would be opportunities for new lending businesses.

“Cannabis will become a broad, mature industry just like any other, and if that is going to happen, there needs to be a debt structure that can support that,” Mancheril says.

The biggest impediment to the industry’s growth is the one that Bespoke Financial wants to tackle first — and that’s access to debt.

To build the company’s first product, Mancheril looked to his co-founder’s Pablo Borquez-Schwarzbeck and Benjamin Dusastre. Borquez-Schwarzbeck and Dusastre previously launched ProducePay, a fintech platform focused on produce farmers that has financed roughly $2 billion in perishable commodities throughout 13 countries. It’s backed by around $200 million in venture capital and debt financing.

What Mancheril and his co-founders have done is take ProducePay’s underwriting model and apply it to the cannabis industry. The financial instrument that they’re starting with is known “in the business” as factoring.

It’s basically advancing money to businesses for a contract that’s signed in exchange for a cut of the money once a company gets paid for the goods or services they’ve rendered.

“While the US legal cannabis market is forecasted to grow over 20% annually, reaching $23B by 2022, the industry’s true growth potential is limited by long cash flow cycles throughout the supply chain and a lack of scalable and efficient capital sources,” says Bespoke Financial co-founder and chief executive, George Mancheril, in a statement. “Our approach will dramatically improve cash flow cycles across the supply chain and provide scalable working capital to fuel our clients’ growth.”

“In general, in the cannabis industry overall, it’s difficult to access any part of the financial system,” says Karan Wadhera, a managing director at Casa Verde. “Now that we’re moving into a place where equity financing is getting expensive, a company like Bespoke plays an important and valuable role in the ecosystem to help young brands and mature brands get access to working capital when they need it the most.”

Powered by WPeMatico