Flipkart

Auto Added by WPeMatico

Auto Added by WPeMatico

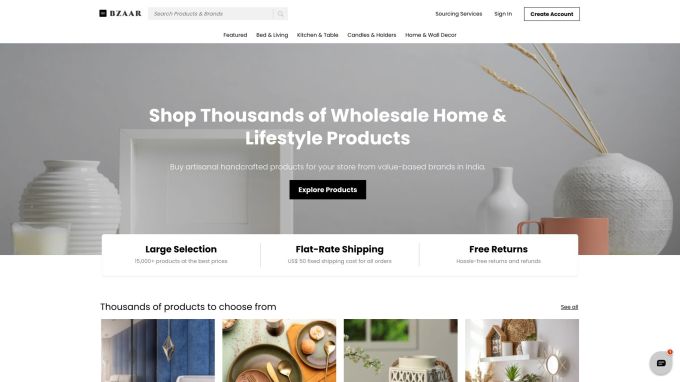

Small businesses in the U.S. now have a new way to source home and lifestyle goods from new manufacturers. Bzaar, a business-to-business cross-border marketplace, is connecting retailers with over 50 export-ready manufacturers in India.

The U.S.-based company announced Monday that it raised $4 million in seed funding, led by Canaan Partners, and including angel investors Flipkart co-founder Binny Bansal, PhonePe founders Sameer Nigam and Rahul Chari, Addition founder Lee Fixel and Helion Ventures co-founder Ashish Gupta.

Nishant Verman and Prasanth Nair co-founded Bzaar in 2020 and consider their company to be like a “fair without borders,” Verman put it. Prior to founding Bzaar, Verman was at Bangalore-based Flipkart until it was acquired by Walmart in 2018. He then was at Canaan Partners in the U.S.

“We think the next 10 years of global trade will be different from the last 100 years,” he added. “That’s why we think this business needs to exist.”

Traditionally, small U.S. buyers did not have feet on the ground in manufacturing hubs, like China, to manage shipments of goods in the same way that large retailers did. Then Alibaba came along in the late 1990s and began acting as a gatekeeper for cross-border purchases, Verman said. U.S. goods imports from China totaled $451.7 billion in 2019, while U.S. goods imports from India in 2019 were $87.4 billion.

Bzaar screenshot. Image Credits: Bzaar

Small buyers could buy home and lifestyle goods, but it was typically through the same sellers, and there was not often a unique selection, nor were goods available handmade or using organic materials, he added.

With Bzaar, small buyers can purchase over 10,000 wholesale goods on its marketplace from other countries like India and Southeast Asia. The company guarantees products arrive within two weeks and manage all of the packaging logistics and buyer protection.

Verman and Nair launched the marketplace in April and had thousands users in three continents purchasing from the platform within six months. Meanwhile, products on Bzaar are up to 50% cheaper than domestic U.S. platforms, while SKU selection is growing doubling every month, Verman said.

The new funding will enable the company to invest in marketing to get in front of buyers and invest on its technology to advance its cataloging feature so that goods pass through customs seamlessly. Wanting to provide new features for its small business customers, Verman also intends to create a credit feature to enable buyers to pay in installments or up to 90 days later.

“We feel this is a once-in-a-lifetime shift in how global trade works,” he added. “You need the right team in place to do this because the problem is quite complex to take products from a small town in Vietnam to Nashville. With our infrastructure in place, the good news is there are already shops and buyers, and we are stitching them together to give buyers a seamless experience.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here.

It’s WWDC week, so expect a deluge of Apple news to overtake your Twitter feed here and there over the next few days. But there’s a lot more going on, so let’s dig in:

And that’s your start to the week. More to come from your friends here on Wednesday, and Friday. Chat soon!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

After spending more than a decade disrupting the neighborhood stores in the U.S. and several other markets, Amazon and Walmart are employing an unusual strategy in India to face off this competitor: Friending them.

Walmart and Amazon, both of which face restrictions from New Delhi on what all they could do in India, have partnered with tens of thousands of neighborhood stores in the world’s second-largest internet market this year to leverage the vast presence of these mom and pop stores.

In June this year, at the height of the pandemic, Amazon announced “Smart Stores.” Through this India-specific program, for instance, Amazon is providing physical stores with software to maintain a digital log of the inventory they have in the shop and supplying them with a QR code.

When consumers walk to the store and scan this QR code with the Amazon app, they see everything the shop has to offer, in addition to any discounts and past reviews from customers. They can select the items and pay for it using Amazon Pay. Amazon Pay in India supports a range of payments services, including the popular UPI, and debit and credit cards.

The world’s largest e-commerce giant also maintains partnerships that allow it to turn tens of thousands of neighborhood stores as its delivery point for customers — and sometimes even rely on them for inventory.

India has over 60 million small businesses that dot the thousands of cities, towns and villages across the country. These mom and pop stores offer all kinds of items, are family run, and pay low wages and little to no rent.

This has enabled them to operate at an economics that is better than most — if not all — of their digital counterparts, and their scale allows them to offer unmatched fast delivery.

Krishna Shah, a New Delhi-based doctor, on paper is one of the perfect customers of e-commerce services. She lives in an urban city, uses digital payments apps and her earnings put her in the top 5% income level in the country. Yet, when she needed to buy food for her cats and needed it as soon as possible, she realized the major giants would take hours, if not longer. She ended up placing a call to a neighborhood store, which delivered the item within 10 minutes.

That neighborhood store, which employs fewer than half a dozen people, was competing with over a dozen giants and heavily funded startups including Grofers and BigBasket — and it won.

At stake is India’s retail market, which is estimated to be worth $1.3 trillion by 2025, from about $700 billion last year, according to Boston Consulting Group and the Retailers’ Association India. E-commerce, by several estimates, accounts for just 3% of the retail market in the country.

If that figure wasn’t small enough already, consider this: Some of the biggest customers of Flipkart and Amazon are these small retail stores. An executive with direct knowledge of the matter told TechCrunch that during some sales, as high as 40% of all smartphone units are bought by physical stores. The idea is, the executive said, to buy the devices at a discounted price, sit on them for a few days and when Amazon and Flipkart are done with their sales, sell the same phones at their standard prices.

Sujeet Kumar, co-founder of Udaan, a Bangalore-based startup that works with merchants, said that even as smartphones and the internet have reached all corners of India, e-commerce hasn’t been able to disrupt the retail market.

“The problem is that it is very difficult for e-commerce companies to build a supply chain and distribution network that is more efficient than those established by neighborhood stores. These mom and pop stores operate on an insanely different kind of cost economics. E-commerce companies are not able to match it,” he said.

Powered by WPeMatico

DealShare, a startup in India that has built an e-commerce platform for middle and lower-income groups of consumers, said on Tuesday it has raised $21 million in a new financing round as it looks to expand its footprint in the world’s second-largest internet market.

WestBridge Capital led the Series C round of the three-year-old startup, which is based in Bangalore. Alpha Wave Incubation, a venture fund managed by Falcon Edge Capital, Z3Partners and existing investors Matrix Partners India and Omidyar Network India also participated in the round, bringing DealShare’s to-date raise to $34 million.

DealShare kickstarted its journey the day Walmart acquired Flipkart, the startup’s founder and chief executive Vineet Rao said at a recent virtual conference. Rao said that even as Amazon and Flipkart had been able to create a market for themselves in the urban Indian cities, much of the nation was still underserved. There was an opportunity for someone to jump in, he said.

The startup began as an e-commerce platform on WhatsApp, where it offered hundreds of products to consumers. It didn’t take long before a major consumer spending pattern was visible, Rao said. People were only interested in buying items that were selling at discounted rates, said Rao.

Over time, that idea has become part of DealShare’s core offering. Today it incentivizes consumers — by offering them discounts and cashbacks — to share deals on products with their friends. The startup, which has since launched its own app and website, now operates in over two dozen cities in India.

Consumers wanted products that were relevant to them and they wanted to buy these items at a price that instilled the most value for their bucks, said Rao. “We focused on locally produced items instead of national brands. Even today, 80% to 90% of items we sell are locally produced,” he said.

“We started building a network of these suppliers. It was very tough because none of these guys fancied joining modern retail like e-commerce. Some of them had tried to work with e-commerce firms before but the experience left a lot to be desired,” he said.

Sandeep Singhal, co-founder and managing director of WestBridge, said in a statement, “Majority of Indian population is currently residing in the non-metros and there is a huge business opportunity in these regions. The buying pattern of low and middle-income group is different especially in smaller markets and DealShare seems to have understood the nuances very well. We are very impressed with how the team has scaled up in the last 2 years, while retaining a sharp focus on low cost, high impact model.”

The startup says it spent the last 18 months to improve its finances and is nearing profitability. Now it plans to invest in its technology stack and expand its platform to 100 cities and towns in five states of India in the next year. It did not disclose how many customers it serves today, but said it is working to reach 10 million customers and clock $339 million in annual GMV.

Powered by WPeMatico

Xpressbees, an Indian logistics firm that works with several e-commerce firms in the country, said on Monday it has raised $110 million in a new financing round as online shopping booms in the world’s second largest internet market.

The Pune-headquartered startup’s Series E financing round was led by private equity firms Investcorp, Norwest Venture Partners and Gaja Capital, the five-year-old startup said. Xpressbees, which concluded its Series D round three years ago, has raised $175.8 million to date, according to research firm Tracxn. The new round valued the startup at more than $350 million.

Xpressbees helps more than 1,000 customers — including financial and e-commerce services giant Paytm, social commerce startup Meesho, eyewear seller Lenskart, phone maker Xiaomi, online pharmacy NetMeds and online marketplace Snapdeal — deliver their products across the country. It has presence in over 2,000 cities and towns, and it processes more than 2.5 million orders a day — up from about 600,000 daily orders last year.

“We have been truly impressed by their strong customer centricity and capital efficiency which has resulted in exceptional feedback from top players in the e-commerce sector!” said Niren Shah, managing director and head of Norwest Venture Partners in India, in a statement.

Xpressbees started its journey within FirstCry, an e-commerce for baby products, in 2012. But in 2015, it became an independent company with Amitava Saha, co-founder and chief operating officer of FirstCry, moving out of FirstCry to become chief executive of Xpressbees. Supam Maheshwari, who co-founded FirstCry and serves as its chief executive, is the other co-founder of Xpressbees.

The startup said it plans to deploy the fresh capital to further automate its hubs and sorting centres, and expand its delivery footprint to cover the entire country. “I am delighted to see the impact we are making in the logistics ecosystem in the country,” said Saha in a statement.

At stake is India’s growing logistics industry, which NVP’s Shah estimated to be worth $200 billion. “We continue to believe that new age technology led logistics players such as Xpressbees will continue to play a pivotal role both in the growth of the e-commerce sector in India,” he added.

E-commerce sales, which account for less than 5% of all retail sales in India, skyrocketed during the pandemic after New Delhi enforced a two-month nationwide lockdown. During their festival sales last month, Amazon India and Walmart-owned Flipkart reported a record surge in their sales. The firms have created more than 150,000 seasonal jobs to accommodate the growing demand of orders. Xpressbees works with over 30,000 delivery staff.

Xpressbees competes with a handful of established firms and startups, including SoftBank-backed Delhivery, which became a unicorn last year, and Ecom Express, which has presence in about 2,400 Indian cities and towns.

Powered by WPeMatico

Despite e-commerce firms Amazon and Walmart and others pouring billions of dollars into India, offline retail still commands more than 95% of all sales in the world’s second largest internet market.

The giants have acknowledged the strong hold neighborhood stores (mom and pop shops) have in the country, and in recent quarters scrambled for ways to work with them. Mukesh Ambani, India’s richest man, has made the dynamics more interesting in the past year as he works to help these neighborhood stores sell online.

But the market opportunity is still too large, and there are many aspects of the old retail business that could use some tech. That’s the bet WareIQ, a Bangalore-headquartered, Y Combinator-backed startup is making. And it has just raised a $1.65 million seed financing round from YC, FundersClub, Pioneer Fund, Soma Capital, Emles Venture Advisors and founders of Flexport.

The one-year-old startup operates a platform to leverage the warehouses across the country. It has built a management system for these warehouses, most of which largely engage in offline business-to-business commerce and have had little to no prior e-commerce exposure.

“We connect these warehouses across India to our platform and utilize their infrastructure for e-commerce order processing,” said Harsh Vaidya, co-founder and chief executive of WareIQ, in an interview with TechCrunch. The company offers this as a service to retail businesses.

Who are these businesses? Third-party sellers (some of whom sell to Amazon and Flipkart and use WareIQ to speed up their delivery), e-commerce firms, social commerce platforms, as well as neighborhood stores and social media influencers.

Any online store, for instance, can send its products to WareIQ, which has integrations with several popular e-commerce platforms and marketplaces. It works with courier partners to move items from one warehouse to another to offer the fastest delivery, explained Vaidya.

The infrastructure stitched together by WareIQ also enables an online seller to set up their own store and engage with customers directly, thereby saving fees they would have paid to Amazon and other established e-commerce players.

“The sellers were not able do this on their own before because it required them to talk directly to warehousing companies that maintain their own rigid contracts, and high-security deposits, and they still needed to work with multiple technology providers to complete the tech-stack,” he said. WareIQ also offers these sellers last-mile delivery, cash collection and fraud detection among several other services.

“In a way, we are building an open-source Amazon fulfilment service, where any seller can send their goods to any of our warehouses and we fulfil their Amazon orders, Myntra orders, Flipkart orders or their own website orders. We also comply with the standard of these individual marketplaces, so our sellers get a Prime tag on Amazon,” he said.

WareIQ is free for anyone to sign up with any charge and it takes a cut by the volume of orders it processes. The startup today works with more than 40 fulfilment centres and plans to deploy the fresh capital to expand its network to tier 2 and tier 3 cities, he said. It’s also hiring for a number of tech roles.

Powered by WPeMatico

Sinch said on Monday it has agreed to buy Indian firm ACL Mobile for £56 million (roughly $70 million) in what is the fourth acquisition deal the Swedish mobile voice and messaging firm has entered into at the height of a global pandemic.

The Swedish firm said acquiring ACL Mobile will enable it to leverage the Indian firm’s connections with local mobile operators in the world’s second largest internet market, as well as in Malaysia and UAE, to expand its end-to-end connectivity without working with a third-party firm.

Twenty-year-old ACL Mobile, which has headquarters in Delhi, Dubai and Kuala Lumpur, enables businesses to interact with their customers through SMS, email, WhatsApp and other channels. In a press statement, the Indian firm said it serves more than 500 enterprise customers, including Flipkart, OLX, MakeMyTrip, HDFC Bank and ICICI Bank.

“With ACL we gain critical scale in the world’s second-largest mobile market. We gain customers, expertise and technology and we further strengthen our global messaging product for discerning businesses with global needs,” said Sinch chief executive Oscar Werner.

The Indian firm, which employs 288 people, reported gross profits of $14.2 million on sales of about $65 million in the financial year that ended in March. During the same period, ACL Mobile claims it delivered 47 billion messages on behalf of its enterprise customers.

“Although the long-term growth outlook is favorable, lower commercial activity in India due to the COVID-19 pandemic means that the near-term growth outlook is less predictable,” Sinch said of ACL Mobile’s future outlook.

ACL Mobile is the fourth acquisition Sinch has unveiled since March this year. Last month the company said it was buying SAP’s Digital Interconnect for $250 million. In March, it announced deals to buy Wavy and Chatlayer.

Sinch, founded in 2008, employs more than 700 people in over 40 locations worldwide and is increasingly expanding to more markets. Last month it said acquiring SAP’s Digital Interconnect will help it expand in the U.S. market. The company says it is profitable.

“Together with Sinch we are scaling up to become one of the leading global players in our industry. I’m excited about this next chapter and the many new opportunities that we can pursue together,” said Sanjay K Goyal, founder and chief executive of ACL Mobile.

Powered by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico

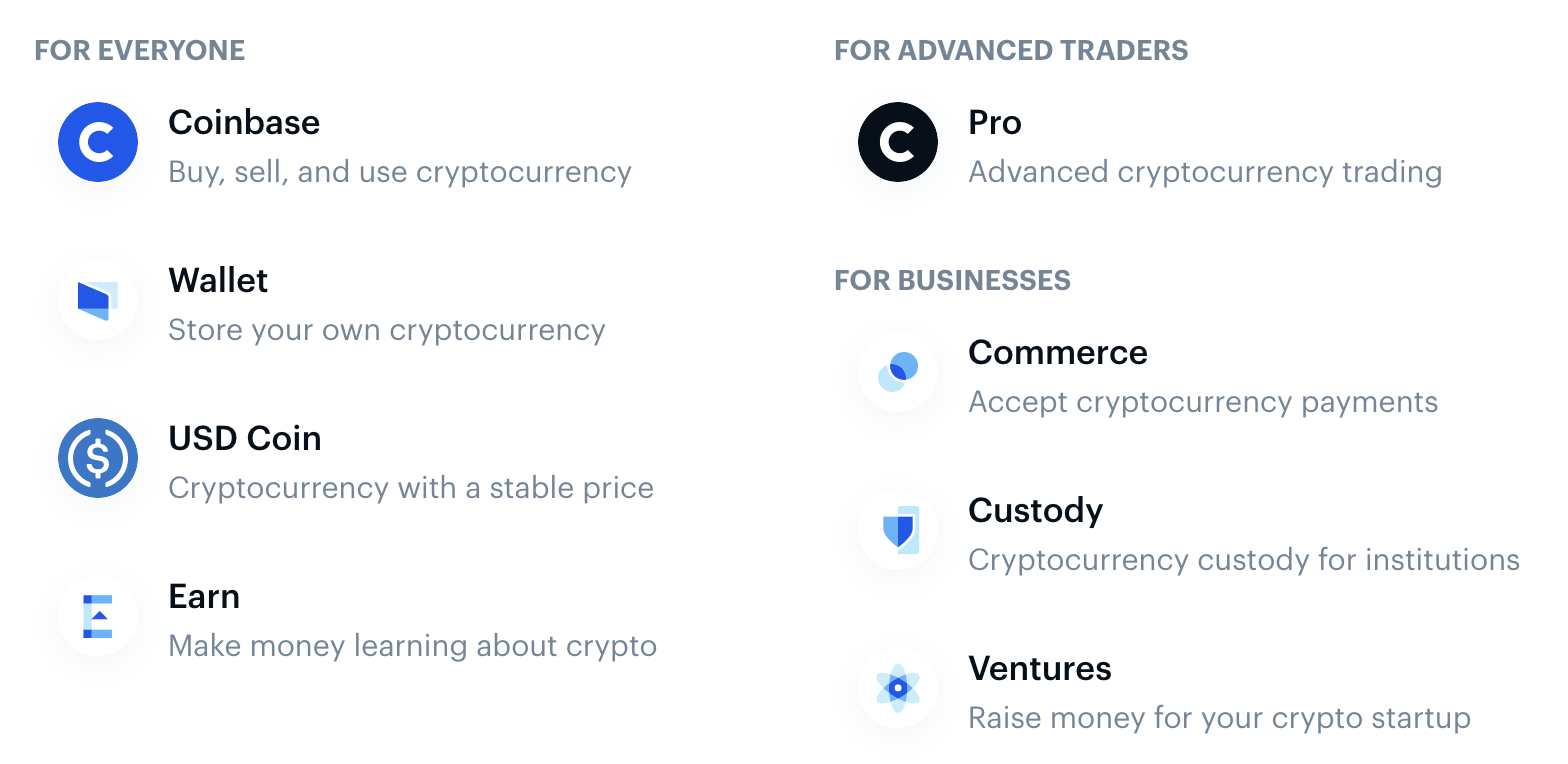

“We’re trying to shift cryptocurrency from this speculative asset class to driving real-world utility,” Coinbase CEO Brian Armstrong tells me. How? Through commerce and micropayments. But now Coinbase has the who to build it. Today the startup announced it has hired away former head of Product for Indian e-commerce giant Flipkart and Google Shopping VP of Product Surojit Chatterjee to become Coinbase’s chief product officer.

“I’ve always enjoyed being associated with technology that is on the brink of changing how we live” writes Chatterjee. “Google ads has helped democratize commerce, Flipkart and ecommerce has revolutionized life in India, and I believe Coinbase is going to turn conventional finance on its head.”

Chatterjee spent more than 11 years at Google over two stints, the first as a founding member of Google’s mobile search Ads product that’s grown to tens of billions in revenue per year. When he starts at Coinbase next week, Armstrong tells me he’ll help Coinbase organize its complex array of products, including its cryptocurrency exchange, wallet, stablecoin, incentivized crypto education platform Earn and Coinbase Commerce that lets businesses take payments in Bitcoin, Ethereum and more. Chatterjee replaces Jeremy Henrickson, the former Coinbase CPO who departed in December 2018.

“Surojit is a huge asset here because we’re a product-led company,” Armstrong says. “We have different leaders and they increasingly have responsibilities around P&L. Having one really experienced chief product officer that can mentor them and teach them to own revenues and budgets — really in the model of Google — that will professionalize Coinbase.”

One opportunity Armstrong hopes Chatterjee can help Coinbase seize on is building products for emerging markets where financial infrastructure is weak. “E-commerce is not equally distributed around the world. Micropayments don’t work that well … Him spending time living in India, a developing market, he deeply understands mobile money.” Given the explosion of phone-based payments, the demonetization and the prevalence of cash on delivery methods in India that Flipkart dealt with, “his background is kind of ideal from that worldly perspective,” Armstrong explains.

Chatterjee cites his upbringing as inspiration to deliver “economic freedom for everyone,” as Armstrong says is Coinbase’s mission. “Growing up in India in a poor middle-class household, I saw very closely what a lack of liquid cash does to a family’s lifestyle,” Chatterjee recalls.

“As a kid I would go with my mom to a local bank to withdraw money. And believe me when I tell you that the process was epic!” It included withdrawal slips, tokens and anxiously trying to match current signatures to versions decades old. When India demonetized and made everyone exchange their cash, “My dad, who was almost 80 at that time, stood in a queue for five hours to get 2000 Rs, which was the per-day limit for the first week. That’s less than $30!” Digital money could ensure people always have access to everything they own.

Surojit Chatterjee (far right) rides along for a Flipkart delivery to understand the consumer commerce experience

In developed countries, Armstrong sees a chance for Chatterjee to enable digital content creators to turn their passion into their profession. “There’s lots of people who lurk on Reddit or Stack Overflow and answer questions … If there was real money on these things, these could be their full time jobs — contributing content on user-generated social sites,” Armstrong predicts. “I think you’d see a lot more contributions, as well.”

Now might be the perfect time to hire Chatterjee since we’re in a lull period for cryptocurrency in the wake of the rush at the end of 2018. “Crypto is always challenging to navigate. In these periods when it’s relatively quiet, we tend to do really well,” Armstrong says. The company grew market share, volume and app installs versus competitors between 50% and 100%, according to the CEO. Referencing ancient war strategy, Armstrong concludes that, “There’s years where you just want to train the soldiers and stockpile resources and you’re basically just preparing. We’re building the company, not just responding to crazy hype.”

Powered by WPeMatico

Two co-founders of Google Pay in India are building a neo-banking platform in the country — and they have already secured backing from three top VC funds.

Sujith Narayanan, a veteran payments executive who co-founded Google Pay in India (formerly known as Google Tez), said on Monday that his startup, epiFi, has raised $13.2 million in its Seed financial round led by Sequoia India and Ribbit Capital. The round valued epiFi at about $50 million.

David Velez, the founder of Brazil-based neo-banking giant Nubank, Kunal Shah, who is building his second payments startup CRED in India, and VC fund Hillhouse Capital also participated in the round.

The eight-month-old startup is working on a neo-banking platform that will focus on serving millennials in India, said Narayanan, in an interview with TechCrunch.

“When we were building Google Tez, we realized that a consumer’s financial journey extends beyond digital payments. They want insurance, lending, investment opportunities and multiple products,” he explained.

The idea, in part, is to also help users better understand how they are spending money, and guide them to make better investments and increase their savings, he said.

At this moment, it is unclear what the convergence of all of these features would look like. But Narayanan said epiFi will release an app in a few months.

Working with Narayanan on epiFi is Sumit Gwalani, who serves as the startup’s co-founder and chief product and technology officer. Gwalani previously worked as a director of product management at Google India and helped conceptualize Google Tez. In a joint interview, Gwalani said the startup currently has about two-dozen employees, some of whom have joined from Netflix, Flipkart, and PayPal.

Shailesh Lakhani, Managing Director of Sequoia Capital India, said some of the fundamental consumer banking products such as savings accounts haven’t seen true innovation in many years. “Their vision to reimagine consumer banking, by providing a modern banking product with epiFi, has the potential to bring a step function change in experience for digitally savvy consumers,” he said.

Cash dominates transactions in India today. But New Delhi’s move to invalidate most paper bills in circulation in late 2016 pushed tens of millions of Indians to explore payments app for the first time.

In recent years, scores of startups and Silicon Valley firms have stepped to help Indians pay digitally and secure a range of financial services. And all signs suggest that a significant number of people are now comfortable with mobile payments: More than 100 million users together made over 1 billion digital payments transaction in October last year — a milestone the nation has sustained in the months since.

A handful of startups are also attempting to address some of the challenges that small and medium sized businesses face. Bangalore-based Open, NiYo, and RazorPay provide a range of features such as corporate credit cards, a single dashboard to manage transactions and the ability to automate recurring payouts that traditional banks don’t currently offer. These platforms are also known as neo-bank or challenger banks or alternative banks. Interestingly, most neo-banking platforms in South Asia today serve startups and businesses — not individuals.

Powered by WPeMatico