Flipkart

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

Accel, one of the world’s most influential venture capitalist firms, is getting more bullish on India.

The Silicon Valley-headquartered firm, which largely focuses on early-stage investments, said today it has closed $550 million for its sixth venture fund in India.

This is a significant amount of capital for Accel’s efforts in the country, where it began investing 15 years ago and has infused roughly $1 billion through all its previous funds.

Anand Daniel, a partner for Accel in India, told TechCrunch in an interview that the VC fund will continue to focus on identifying and investing in seed and early-stage startups.

But the fund realized it needed more money so it could actively participate in follow-on rounds (later-stage financing rounds) of its portfolio startups. The announcement today follows Accel’s similar recent push in Europe and Israel, where it closed a $575 million fund.

“We also selectively do growth investments for companies that are scaling well, such as Swiggy, UrbanClap, BlackStone and Bounce. We have continued to back them through Series B and Series C rounds,” he said.

At the risk of being accused of bias, I’ll say this: Accel India is a rare Indian fund that had credible exits and more promising exits in the pipeline. They’re also some of the nicest people to work with. https://t.co/aZGjDgSQKe

— JPK (@therealjpk) December 2, 2019

Like in many other markets, Accel’s track record in India is quite impressive. It participated in the seed financing round of e-commerce firm Flipkart, which was then valued at $4 million post-money. Walmart bought a majority stake in Flipkart last year for $16 billion. (This helped Accel net more than $1 billion in return from Flipkart.)

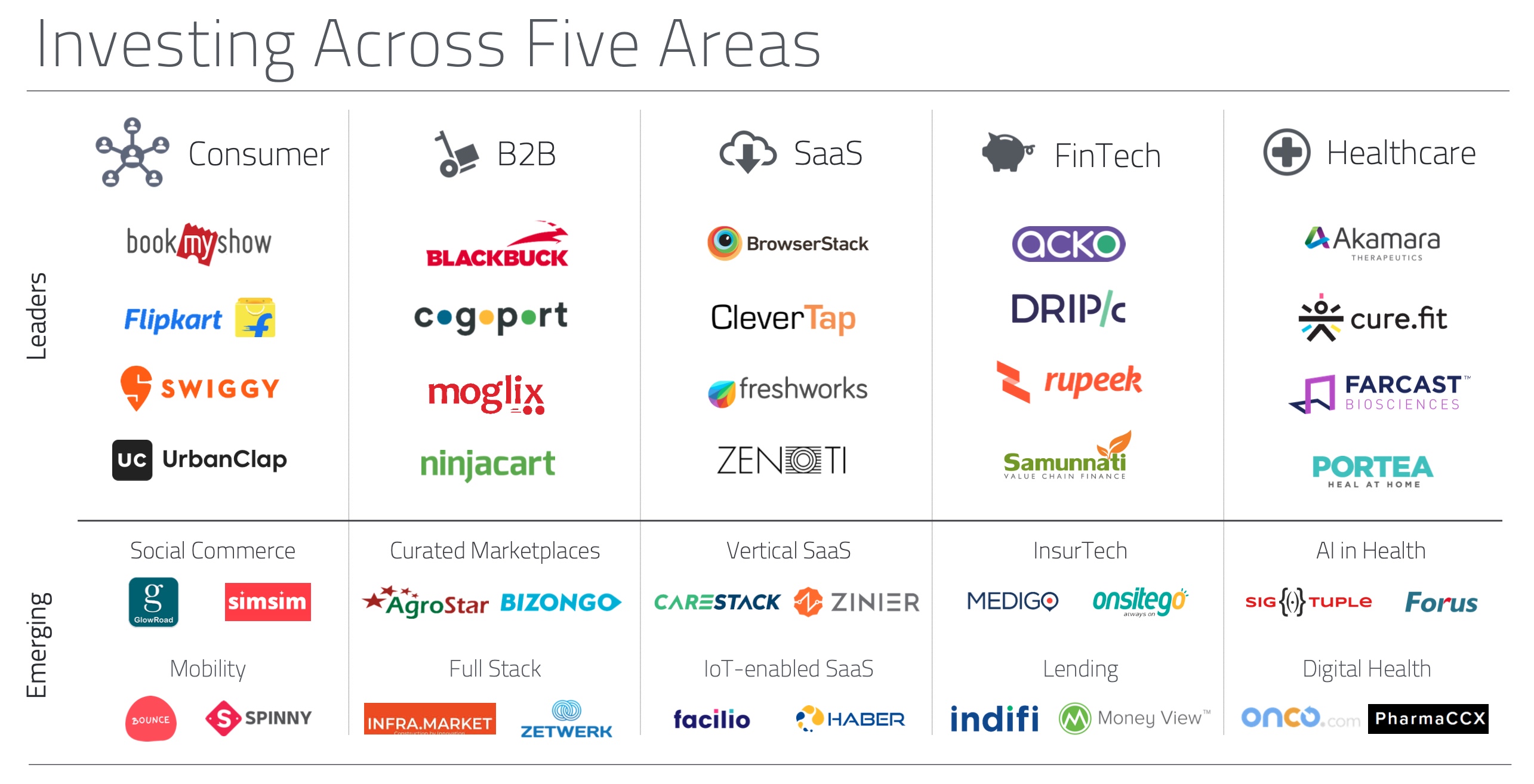

Accel, which has nine partners and more than 50 members in total in India, also invested in the seed round of SaaS giant Freshworks, which is now valued at more than $3 billion, food delivery startup Swiggy, also valued at north of $3 billion, and recently turned unicorn BlackBuck. Accel has been the first institutional investor for 85% of startups in its portfolio.

The VC firm says 44 of the 100-odd startups in its India portfolio today are valued at over $100 million each. In total, including Flipkart’s $21 billion market value, Accel’s portfolio firms have created $44 billion in market value.

Some of the investments Accel has made in India

“When we started our first fund in India in 2005, the world was a very different place. Just 1 in 50 Indians had access to the internet and mobile phone ownership was nascent. Yet we firmly believed that India was on the cusp of a big change,” the firm said in a statement.

“Today, the opportunity ahead is significantly bigger than when we started in 2005: India can now digitally identify 1.3 billion people, has 600 million internet users and 150 million online transacting customers with a national payments platform that processes $20 billion a month.”

Daniel said moving forward Accel will continue to focus on consumer, business-to-business, fintech, healthcare and global SaaS categories. “We have nine partners with their own areas of interest. They invest from their own conviction and finance seed rounds. If we see a particular sector evolving, then we do a deeper thesis work,” he said.

“We then develop deeper confidence for the space. For example, back in the day we invested in mobility startup TaxiForSure, long before Uber had arrived in India. That helped us understand mobility well. We have used those learnings to invest in several more mobility startups.”

Accel’s growing interest in India comes at a time when several other giants, including SoftBank and Prosus Ventures, have also become more active in the nation — though they tend to finance later-stage rounds.

For Indian startups that are already having their best year, this can only be good news.

Powered by WPeMatico

Of the 1.3 billion people who live in India, more than 100 million of whom are using digital payment apps each day, only about 20 million today invest in mutual funds and stocks. An Indian startup that is betting on changing that figure by courting millennials has just received a big backing.

Groww, a Bangalore-based startup, said today it has raised $21.4 million in a Series B financing round that was led by U.S.-based VC firm Ribbit Capital. Existing investors Sequoia India and Y Combinator also participated in the round, said the two-year-old startup that has raised about $29 million to date.

Groww allows users to invest in mutual funds, including systematic investment planning (SIP) and equity-linked savings. The app, which maintains a very simplified user interface to make it easier for its largely millennial customer base to comprehend the investment world, offers every fund that is currently available in India.

Lalit Keshre, co-founder and CEO of Groww, told TechCrunch in an interview earlier this week that the market of mutual funds is increasingly widening in India and the startup is hoping to accelerate its growth with the fresh capital. Other than that, he plans to double Groww’s headcount to 200 in the coming months.

Groww has amassed about 2.5 million registered users, two-thirds of whom are first-time investors, Keshre said. Groww is currently free to use and does not charge any commission on transactions. The startup eventually plans to offer a paid service as it looks to monetize its user base, but Keshre declined to share a timeline on how soon that would happen.

Groww will also soon begin to offer the ability to purchase stocks from its eponymous app, said Keshre, a former executive at Flipkart who co-founded Groww with three other Flipkart colleagues (Harsh Jain, Neeraj Singh and Ishan Bansal).

In a statement, Micky Malka, founder of Ribbit Capital, said, “We backed the Groww team because we believe in their mission. They have built the most trusted product in this space and are on the path to create a category-defining product.”

Ribbit Capital has made a number of investments in India in recent months. Last month, it invested in Cred, a startup that is trying to improve the financial behavior of credit card holders, and BharatPe, a payments solution for businesses.

In recent years, a number of startups such as INDWealth and Cube Wealth have emerged in India to offer wealth management platforms to the country’s growing internet population. Many established financial firms such as Paytm have also expanded their offerings to include investments in mutual funds.

Ashish Agarwal, a principal partner at Sequoia Capital India, said, “Investment products such as mutual funds and stocks were traditionally sold offline through financial advisors, who were mis-incentivized to sell high-commission products. Groww is taking a refreshing approach with a zero-commission mobile first model, enabling investors to make their own investment choices through a slick and easy user interface.”

Powered by WPeMatico

Flipkart, the largest e-commerce platform in India, said Tuesday it has concluded the roll-out of a range of features to its shopping app in what is its biggest update in recent years.

Chief among these new features is access to Flipkart in Hindi language. Prior to the revamp of the app, Flipkart was available only in English, a language spoken by 10% of India’s 1.3 billion population.

Flipkart says it is hoping that the new features, which includes a video streaming service, would help it reach the next 200 million users in India.

The major bet on Hindi, a language spoken by more than 500 million people in India, illustrates a growing push from local and international companies operating in the country as they adapt their services and business models to go beyond the urban cities.

And that’s where much of the opportunity, which countless startups and companies have trumpeted to investors to successfully raise hundreds of millions of dollars in debt and venture capital in recent years, lies in the nation.

Powered by WPeMatico

India’s e-commerce giant Flipkart said on Tuesday that it is revamping its shopping app to add support for Hindi language, a video streaming service and an audio-visual assistant, the latest in a series of recent efforts to expand its reach in the country.

The e-commerce firm, which sold a majority stake to Walmart for $16 billion last year and leads the local market, told TechCrunch that it has started to roll out the features on its shopping app and will push it to all its existing users within the next 20 days.

Only 10% of India’s 1.3 billion people speak English. Flipkart said it has been working to customize its entire platform for several months to add support for Hindi. More than 500 million people in India speak Hindi.

As part of the revamp, the company is also introducing an “audio visual guided navigation” feature, also built in Hindi, that is aimed at first-time internet users — and existing online users not comfortable with making transactions online — to make it easier for them to navigate the service and place orders.

Its rival Amazon India added support for Hindi last year, though the feature is limited to basic text translation.

As part of the accessibility push, Flipkart is also introducing an in-app video streaming feature dubbed “Flipkart Videos” that will syndicate movies, shows and other long-form and short-form content from a number of production houses and movie studios, the company said.

The inclusion of the video streaming feature comes as Indians’ appetite for consuming media content on the internet has ballooned in the recent years. Hotstar, a Disney-owned video streaming service, has amassed more than 300 million monthly active users in the country.

Flipkart said the video streaming feature will enable it to invite a new segment of users to its platform who are online but don’t currently shop on the internet. Even as more than 500 million users are connected to the web in India, only tens of millions of them currently shop there.

The streaming feature will be accessible to all users at no charge without any loyalty program, a company spokesperson said, refuting a recent media report that claimed otherwise.

“In the past 10 years our vision and ethos have been to solve for ‘Real India,’ create India specific tech solutions, here in India. What we are rolling out when it comes to addressing the needs of the next 200 million users in our country, is taking forward those founding principles of access and affordability,” said Kalyan Krishnamurthy, Group CEO of Flipkart, in a statement.

“We strongly believe that the next phase of our growth is rooted in loyalty, democratizing e-commerce and the country will continue seeing more innovations that stem from our deep understanding of Indian consumers, especially middle India.”

Flipkart said it is also attempting to make it easier for users to discover items on its app. So it is introducing a feed called “Flipkart Ideas” that will populate short-form videos, animated images, polls and quizzes.

For instance, a user may see a short-form video that shows a sportsperson wearing a pair of sneakers, a t-shirt, a pair of jeans and a cap. If they tap on the video, they will see the exact items the person in the video is wearing and other similar items. One more tap, and the user would be able to purchase any of those items.

The company said it is working with more than 400 influencers and 30 brands to create content that will appear on the feed.

All of these features, as well as a gaming section that Flipkart introduced last year, will now appear at the bottom of the screen for easier navigation, the company said. More than half a million users in India play mini-games on Flipkart everyday. The company said it will introduce more games to boost engagement levels and offer loyalty points as incentive to customers.

Powered by WPeMatico

Indifi, a Gurgaon-based startup that offers loans to small and medium-sized businesses and also operates an online lending marketplace, has raised 1,450 million Indian rupees ($20.4 million) in a new financing round to expand its business in the country.

The Series C round for the four-year-old startup was led by CDC Group, a U.K.-government-owned VC fund. Existing investors Accel, Elevar Equity, Omidyar Networks and Flourish Ventures also participated in the round, the startup announced on Tuesday (Indian Standard Time).

Indifi, which has raised about $34 million in venture capital to date, has also relied on debt to grow and finance loans on its platform. Currently, it’s in about $21 million in debt, Alok Mittal, co-founder and managing director of Indifi, told TechCrunch in an interview.

Indifi, which itself finances some loans, additionally also serves as a marketplace for banks and non-banking financial companies to participate in funding loans to small and medium-sized enterprises, said Mittal. Both the businesses are equally growing and contributing to its bottom line, he said.

A typical loan processed by Indifi is of about $7,000 in size. Overall, the startup offers between $1,400 to $70,000 in capital to businesses.

Unlike banks and many other online lenders, Indifi works with an ecosystem of companies to assess risk factors before granting a loan to a business, Mittal said. For instance, Indifi works with food-delivery startups Zomato and Swiggy and checks a restaurant’s history and feedback from their customers before issuing to a restaurant.

Similarly, if an enterprise from the travel industry were to look for a loan, Indifi checks the volatility of the market. Some of its other business partners include Oyo Rooms, MakeMyTrip, Flipkart, FirstData, Travel Booking and Riya Travel.

“We chose to invest in Indifi because of its advanced data-driven approach that enables it to reach [thousands] of underserved customers across India. By reducing the high cost of risk assessment and customer acquisition, Indifi helps formal and informal businesses to access growth finance that otherwise may not receive it,” Srini Nagarajan, managing director and head of CDC Group’s Asia business, said in a statement.

Despite its longer background check process, Mittal said Indifi has been able to finance nearly 50% of all the applications it gets, compared to about 10% deals that materialize with banks and other lenders.

Indifi, which spent the first year and a half of its existence building relationships with major companies and refining its products, has amassed more than 15,000 customers to date, Mittal said. Its client base has grown by 2.5 times in the past year, he said.

The startup will use the fresh capital to find new clients and lending partners to expand its marketplace business, Mittal said. It will also explore lending to businesses in more sectors, including logistics (so fleet-owners could also get loan).

Indifi competes with a handful of businesses, including Bangalore-based Zest Money, Five Star Finance, Capital Float and, in some capacity, Drip Capital, which recently raised $25 million.

Powered by WPeMatico

India ordered an investigation into Google’s alleged abuse of Android’s dominance in the country to hurt local rivals. A document made public by the local antitrust watchdog has now further revealed the nature of the allegations and identified the people who filed the complaint.

Umar Javeed and Sukarma Thapar, two associates at Competition Commission of India — and Aaqib Javeed, brother of Umar and who interned at the watchdog last year, filed the complaint, the document revealed. The revelation puts an end to months-long interest from industry executives, many of whom wondered if a major corporation was behind it.

The case, filed against Google’s global unit and Indian arm on April 16 this year, makes several allegations, including the possibility that Google used Android’s dominant position in India to hurt local companies. The accusation is that Google requires handset and tablet vendors to pre-install its own applications or services if they wish to get the full-blown version of Android . Google’s Android mobile operating system powered more than 98% of smartphones that shipped in the country last year, research firm Counterpoint said.

This accusation is partly true, if at all. To be sure, Google does offer a “bare Android” version, which a smartphone vendor could use and then they wouldn’t need to pre-install Google Mobile Services (GMS). Though by doing so, they will also lose access to Google Play Store, which is the largest app store in the Android ecosystem. Additionally, phone vendors do partner with other companies to pre-install their applications. In India itself, most Android phones sold by Amazon India and Flipkart include a suite of their apps preloaded on the them.

“OEMs can offer Android devices without preinstalling any Google apps. If OEMs choose to preinstall Google mobile apps, the MADA (Mobile Application Distribution Agreement) allows OEMs to preinstall a suite of Google mobile apps and services referred to as Google Mobile Services (GMS),” said Google in response.

The second allegation is that Google is bundling its apps and services in a way that they are able to talk to each other. “This conduct illegally prevented the development and market access of rival applications and services in violation of Section 4 read with Section 32 of the Act,” the trio wrote.

This also does not seem accurate. Very much every Android app is capable of talking to one another through APIs. Additionally, defunct software firm Cyanogen partnered with Microsoft to “deeply integrate” Cortana into its Android phones — replacing Google Assistant as the default virtual voice assistant. So it is unclear what advantage Google has here.

Google’s response: “This preinstallation obligation is limited in scope. It was pointed out that preinstalled Google app icons take up very little screen space. OEMs can and do use the remaining space to preinstall and promote both their own, and third-party apps. It was also submitted that the MADA preinstallation conditions are not exclusive. Nor are they exclusionary. The MADA leaves OEMs free to preinstall rival apps and offer them the same or even superior placement.”

The third accusation is that Google prevents smartphone and tablet manufacturers in India from developing and marketing modified and potentially competing versions of Android on other devices.

This is also arguably incorrect. Micromax, which once held tentpole position among smartphone vendors in India, partnered with Cyanogen in their heyday to launch and market Android smartphones running a customized operating system. Chinese smartphone vendor OnePlus followed the same path briefly.

Google’s response: “Android users have considerable freedom to customise their phones and to install apps that compete with Google’s. Consumers can quickly and easily move or disable preinstalled apps, including Google’s apps. Disabling an app makes it disappear from the device screen, prevents it from running, and frees up device memory – while still allowing the user to restore the app at a later time or to factory reset the device to its original state.”

Additionally, Google says it requires OEMs to “adhere to a minimum baseline compatibility standard” for Android called Compatibility Definition Document (COD) to ensure that apps written for Android run on their phones. Otherwise, this risks creating a “threat to the viability and quality of the platform.”

“If companies make changes to the Android source code that create incompatibilities, apps written for Android will not run on these incompatible variants. As a result, fewer developers will write apps for Android, threatening to make Android less attractive to users and, in turn, even fewer developers will support Android,” the company said.

The antitrust is ongoing, but based on an initial probe of the case, CCI has found that Google has “reduced the ability and incentive of device manufacturers to develop and sell devices” running Android forks, the watchdog said. Google’s condition to include “the entire GMS suite” to devices from OEMs that have opted for full-blown a version of Android, amounts to “imposition of unfair condition on the device manufacturers,” the watchdog added.

The document also reveals that Google has provided CCI with some additional responses that have been kept confidential. A Google spokesperson declined to comment.

Powered by WPeMatico

Away from the limelight of the press and the frenzy of fundraising, a tech startup in India has achieved a feat that few of its peers have managed: going public.

IndiaMART, the country’s largest online platform for selling products directly to businesses, raised nearly $70 million in a rare tech IPO for India this week.

The milestone for the 23-year-old firm is so uncommon for India’s otherwise burgeoning startup ecosystem that, beyond being over-subscribed 36 times, pent up demand for IndiaMART’s stock saw its share price pop 40% on its first day of trading on National Stock Exchange on Thursday — a momentum that it sustained on Friday.

The stock ended Friday at Rs 1326 ($19.3), compared to its issue price of Rs 973 ($14.2).

IndiaMART is the first business-to-business e-commerce firm to go public in India. Its IPO also marks the first listing for a firm following the May reelection of Narendra Modi as the nation’s Prime Minister and the months-long drought that led to it.

Accounting firm EY said it expects more companies from India to follow suit and file for IPO in the coming months.

“Now that national elections are over and favorable results secured, IPO activity is expected to gain momentum in H2 2019 (second half of the year). Companies that had filed their offer documents with the Indian stock markets regulator during H2 2018 and Q1 2019 may finally come to market in the months ahead,” it said in a statement (PDF).

The fireworks of the IPO are just as impressive as IndiaMART’s journey.

The startup was founded in 1996 and for the first 13 years, it focused on exports to customers abroad, but it has since modernized its business following the wave of the internet.

“The thesis was, in 1996, there were no computers or internet in India. The information about India’s market to the West was very limited,” Dinesh Agarwal, co-founder and CEO of IndiaMART, told TechCrunch in an interview.

Until 2008, IndiaMART was fully bootstrapped and profitable with $10 million in revenue, Agarwal said. But things started to dramatically change in that year.

“The Indian rupee became very strong against the dollar, which dwindled the exports business. This is also when the stock market was collapsing in the West, which further hurt the exports demand,” he explained.

Dinesh Agarwal, founder and CEO of IndiaMart.com, poses for a profile shot on July 29, 2015 in Noida, India.

By this time, millions of people in India were on the internet and, with tens of millions of people owning a feature phone, the conditions of the market had begun to shift towards digital.

“This is when we decided to pursue a completely different path. We started to focus on the domestic market,” Agarwal said.

Over the last 10 years, IndiaMART has become the largest e-commerce platform for businesses with about 60% market share, according to research firm KPMG. It handles 97,000 product categories — ranging from machine parts, medical equipment and textile products to cranes — and has amassed 83 million buyers and 5.5 million suppliers from thousands of towns and cities of India.

According to the most recent data published by the Indian government, there are about 50 to 60 million small and medium-sized businesses in India, but only around 10 million of them have any presence on the web. Some 97% of the top 50 companies listed on National Stock Exchange use IndiaMART’s services, Agarwal said.

That’s not to say that the transition to the current day was a straightforward process for the company. IndiaMART tried to capitalize on its early mover advantage with a stream of new services which ultimately didn’t reap the desired rewards.

In 2002, it launched a travel portal for businesses. A year later, it launched a business verification service. It also unveiled a payments platform called ABCPayments. None of these services worked and the firm quickly moved on.

Part of IndiaMART’s success story is its firm leadership and how cautiously it has raised and spent its money, Rajesh Sawhney, a serial angel investor who sits on IndiaMART’s board, told TechCrunch in an interview.

IndiaMART, which employs about 4,000 people, is operationally profitable as of the financial year that ended in March this year. It clocked some $82 million in revenue in the year. It has raised about $32 million to date from Intel Capital, Amadeus Capital Partners and Quona Capital. (Notably, Agarwal said that he rejected offers from VCs for a very long time.)

The firm makes most of its revenue from subscriptions it sells to sellers. A subscription gives a seller a range of benefits including getting featured on storefronts.

4/4. So many Indian small businesses have so much to thank @DineshAgarwal for. And after the iconic IPO, so many Indian entreprenuers will have so much to thank him for – forever unlocking the Indian public markets to current & future generation of Indian internet companies

— Kunal Bahl (@1kunalbahl) July 4, 2019

There are only a handful of internet companies in India that have gone public in the last decade. Online travel service MakeMyTrip went public in 2010. Software firm Intellect Design Arena and e-commerce store Koovs listed in 2014, then travel portal Yatra and e-commerce firm Infibeam followed two years later.

India has consistently attracted billions of dollars in funding in recent years and produced many unicorns. Those include Flipkart, which was acquired by Walmart last year for $16 billion, Paytm, which has raised more than $2 billion to date, Swiggy, which has bagged $1.5 billion to date, Zomato, which has raised $750 million, and relatively new entrant Byju’s — but few of them are nearing profitability and most likely do not see an IPO in their immediate future.

In that context, IndiaMART may set a benchmark for others to follow.

“The fact that we have a homegrown digital commerce business, serving both the urban and smaller cities, and having struggled and been around for so long building a very difficult business and finally going public in the local exchange is a phenomenal story,” Ganesh Rengaswamy, a partner at Quona Capital, told TechCrunch in an interview. “It keeps the story of India tech, to the Western world, going.”

Congratulations @DineshAgarwal for an iconic IPO! @IndiaMART has set an example and hope for all Indian Internet companies looking to go public. Cheers! https://t.co/yJumFjfitS

— Vani Kola (@VaniKola) July 4, 2019

Generally, it is agreed that there are too few IPOs in India and the industry can benefit from momentum and encouragement of high profile and successful public listings.

“There is a firm consensus that in India, markets will prefer only the IPOs of companies that are profitable. And investors in India might not value those companies. Both of these issues are being addressed by IndiaMART,” said Sawhney.

“We need 30 to 40 more IPOs. This will also mean that the stock market here has matured and understands the tech stocks and how it is different from other consumer stocks they usually handle. More tech companies going public would also pave the way for many to explore stock exchanges outside of India.

“Indian market is ready for more tech stocks. We just need to get more companies to go out there,” Sawhney added, although he did predict that it will take a few years before the vast majority of leading startups are ready for the public market.

The Indian government, for its part, this week announced a number of incentives to uplift the “entrepreneurial spirit” in the nation.

Finance minister Nirmala Sitharaman said the government would ease foreign direct investment rules for certain sectors — including e-commerce, food delivery, grocery — and improve the digital payments ecosystem. Sitharaman, who is the first woman to hold this position in India, said the government would also launch a TV program to help startups connect with venture capitalists.

IndiaMART has managed to build a sticky business that compels more than 55% of its customers to come back to the platform and make another transaction within 90 days, Agarwal — its CEO — said. With some 3,500 of its 4,000 employees classified as sales executives, the company is aggressive in its pursuit of new customers. Moving forward, that will remain one of its biggest focuses, according to Agarwal.

“Most of our time still goes into educating MSMEs on how to use the internet. That was a challenge 20 years ago and it remains a challenge today,” he told TechCrunch.

In recent years, IndiaMART has begun to expand its suite of offerings to its business customers in a bid to increase the value they get from its platform and thus increase their reliance on its service.

IndiaMART has built a customer relationship management (CRM) tool so that customers need not rely on spreadsheets or other third-party services.

“We will continue to explore more SaaS offerings and look into solving problems in accounting, invoice management and other areas,” said Agarwal.

The firm also recently started to offer payment facilitation between buyers and sellers through a PayPal -like escrow system.

“This will bridge the trust gap between the entities and improve an MSME’s ability to accept all kinds of payment options including the new age offerings.”

There’s an elephant in the room, however.

A bigger challenge that looms for IndiaMART is the growing interest of Amazon and Walmart in the business-to-business space. Several startups including Udaan — which has raised north of $280 million from DST Global and Lightspeed Venture Partners — have risen up in recent years and are increasingly expanding their operations. Agarwal did not seem much worried, however, telling TechCrunch that he believes that his prime competition is more focused on B2C and serving niche audiences. Besides he has $100 million in the bank himself.

Indeed, as Quona Capital’s Rengaswamy astutely noted, competition is not new for IndiaMART — the company has survived and thrived more than two decades of it.

“Alibaba came and gave up,” he noted.

An important — and unanswered question — that follows the successful IPO is how IndiaMART’s stock will fare over the coming months. A glance to the U.S. — where hyped companies like Uber, Lyft and others have seen prices taper off — shows clearly that early demand and sustained stock performance are not one and the same.

Nobody knows at this point, and the added complexity at play is that the concept of a tech IPO is so uncommon in India that there is no definitive answer to it… yet. But IndiaMART’s biggest achievement may be that it sets the pathway that many others will follow.

Powered by WPeMatico

Away from the limelight of urban cities, where an increasingly growing number of firms are fighting for a piece of India’s digital payments market, a South Korean startup’s app is quietly helping millions of Indians pay digitally and enjoy many financial services for the first time.

The app, called True Balance, began its life as a tool to help users easily find their mobile balance, or topping up pre-pay mobile credit. But in its four-year journey, its ambition has significantly grown beyond that. Today, it serves as a digital wallet app that helps users pay their mobile and electricity bills, and it also lets users pay later.

One thing that has not changed for the parent company of True Balance, BalanceHero, which employs less than 200 people, is its consumer focus. It is strictly catering to people in tier-two and tier-three markets — often dubbed as India 2 and India 3 — who have relatively limited access to the internet, and lower financial power. And it remains operational just in India.

Even as India is already the second largest internet market with more than 500 million users, more than half of its population remains offline. In recent years, the nation has become a battleground for Silicon Valley giants and Chinese firms that are increasingly trying to win existing users and bring the rest of the population online.

And like many other companies, BalanceHero’s bet on India is beginning to pay off. The startup told TechCrunch today that it has clocked $100 million in GMV sales and has amassed about 60 million registered users. Yongsung Yoo, a spokesperson for the startup, added that BalanceHero, which has raised $42 million to date, is also nearing profitability.

The South Korean firm’s playbook is different from many other players that are racing to claim a slice of India’s burgeoning digital payments market. True Balance competes with the likes of Paytm, MobiKwik, Google, Amazon and Walmart-owned Flipkart, though its competitors are still largely catering to the urban parts of India.

In the last two years, many firms have begun to explore smaller cities and towns, but their services are still too out-of-the-world for local residents. Raising awareness about digital services is a big challenge in such markets, Yoo said, so the startup is relying on existing users to help others make their first transactions and in paying bills.

Yoo said the startup rewards these “digital agents” with cash back and other benefits. For these digital agents, many of whom do not have a day job, True Balance has emerged as a side project to make extra money.

Later this year, Yoo said the startup, which recently also added support for UPI in its service, will open an e-commerce store on its app and also offer insurance to users. To accelerate its growth and expansion, True Balance is in the final stages of raising between $50 million to $70 million in a new round that it expects to close in July this year, Yoo said.

Powered by WPeMatico

Amazon and Walmart’s problems in India look set to continue after Narendra Modi, the biggest force to embrace the country’s politics in decades, led his Hindu nationalist Bharatiya Janata Party to a historic landslide re-election on Thursday, reaffirming his popularity in the eyes of the world’s largest democracy.

The re-election, which gives Modi’s government another five years in power, will in many ways chart the path of India’s burgeoning startup ecosystem, as well as the local play of Silicon Valley companies that have grown increasingly wary of recent policy changes.

At stake is also the future of India’s internet, the second largest in the world. With more than 550 million internet users, the nation has emerged as one of the last great growth markets for Silicon Valley companies. Google, Facebook, and Amazon count India as one of their largest and fastest growing markets. And until late 2016, they enjoyed great dynamics with the Indian government.

But in recent years, New Delhi has ordered more internet shutdowns than ever before and puzzled many over crackdowns on sometimes legitimate websites. To top that, the government recently proposed a law that would require any intermediary — telecom operators, messaging apps, and social media services among others — with more than 5 million users to introduce a number of changes to how they operate in the nation. More on this shortly.

Powered by WPeMatico