fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

PayPal Holdings, the U.S. fintech company, announced an acquisition of Paidy, a Japanese buy now, pay later (BNPL) service platform, for approximately $2.7 billion (300 billion yen), mostly in cash, to enhance its business in Japan.

The transaction completion, including the regulatory approval, is expected in the fourth quarter of 2021.

After the acquisition, the Japan-based company will continue to operate its existing business and maintain the brand while the leaders, Paidy’s president and CEO Riku Sugie and founder and executive chairman Russell Cummer, keep their positions.

Japan is the third largest e-commerce market in the world, and so this is a significant move by PayPal to gain more market share both in the country and the region, specifically in the area of providing deferred payment services as an alternative to credit cards.

PayPal has long played nice with payment cards — users can upload details of their cards to PayPal and use it as a kind of digital wallet to manage how they pay for things online through it — but it got its start actually as a payment platform in itself, where people could pay into and out of PayPal accounts. Paidy is, in that sense, a strengthening of PayPal’s first-party rails, providing a way to “own” that flow of money on its own infrastructure, not involving the card networks.

Paidy is basically a two-sided payments service, acting as a middleman between consumers and merchants in Japan. Using machine learning it determines the creditworthiness of a consumer related to a particular purchase, and then it underwrites those transactions in seconds, guaranteeing payments to merchants. Consumers then make deferred payment to Paidy for those goods.

Paidy’s platform, which offers a monthly payment installment service branded “3-Pay”, enables shoppers to make purchases online and then pay for them each month in a consolidated bill at a convenience store or via bank transfer.

“Paidy pioneered buy now, pay later solutions tailored to the Japanese market and quickly grew to become the leading service, developing a sizable two-sided platform of consumers and merchants,” said Peter Kenevan, vice president, head of Japan at PayPal.

Paidy has more than 6 million registered users, and the plan is to integrate PayPal and other digital and QR wallets with Paidy Link to connect further online and offline merchants.

In April 2021, the Japan-based company launched Paidy Link, allowing users to link digital wallets with their Paidy account. PayPal was the first digital wallet partner to integrate with Paidy Link.

“PayPal was a founding partner for Paidy Link and we look forward to looking together to create even more value,” Sugie said in a statement.

“Japan has been a vibrant environment for our growth to date and we’re honored to have our team’s hard work and potential recognized by a global leader. Together with PayPal, we will be able to further achieve our mission of taking the hassle out of shopping,” Cummer said.

Powered by WPeMatico

Y Combinator kicked off its fourth-ever virtual Demo Day today, revealing the first half of its nearly 400-company batch. The presentation, YC’s biggest yet, offers a snapshot into where innovation is heading, from not-so-simple seaweed to a Clearco for creators.

The TechCrunch team stuck to its tradition of covering every single company live (but, you know, from home) so you’ll find all of the Day One companies here. For those who want a sampling of standouts, however, we’re also bringing you a host of our favorites from today’s one-minute pitch-off extravaganza.

As reporters, we’re constantly inundated with hundreds of pitches on a daily basis. The startups below caught our picky attention for a whole host of reasons, but that doesn’t mean other startups weren’t compelling or potential unicorns as well. Instead, consider the below to be a data point on which startups made us do a double take, be it due to the size of the market opportunity, the ambition exhibited by the founding team or an idea that was just too clever to pass up.

Genei is, dare I say, a refreshing mashup between robots and writers. The startup has a simple goal: Automatically summarize background reading so content creators can grab the top facts, attribute and move onto the next graf. Writing is innately an art, so I find Genei’s positioning as a tool for writers instead of a replacement out to take their jobs as smart. Better yet, it’s launching by targeting some of the hardest workers in our industry: freelance writers. These folks often have to balance consistent pitches, diverse assignments and tight deadlines for their livelihood, so I’d presume a sidekick can’t hurt. Down the road, I could totally see this startup playing the same role as a Grammarly: a helpful extension of workflows that optimizes the way people who write for a living, write. — Natasha

Powered by WPeMatico

Amsterdam-based challenger bank Bunq is updating its service with a handful of new features. In addition to Dutch, German and French bank account numbers, existing and new users in Spain can now get a Spanish IBAN.

European IBANs are supposed to work across Europe. Your employer or internet provider can’t force you to get a local IBAN. And yet, that’s rarely the case. When you move to another European country, chances are the first thing you do is that you open a local bank account.

While European fintech companies have teamed up to create a lobbying effort called “Accept my IBAN”, some challenger banks, such as Bunq, are adding the ability to get local bank account numbers as an intermediary fix. Bunq users can also choose to associate IBANs from multiple European countries with their account. You have to pay a one-time fee of €9.99 every time you add a new local IBAN.

Bunq is also drawing inspiration from Revolut, Wise, Vivid Money and others as you’ll soon be able to receive, convert and hold other currencies. For instance, if you’re going to a non-Euro country for an internship, you will be able to receive your salary on your Bunq account. Bunq is starting with USD accounts with plans to add more currencies down the road.

Other new features include the ability to receive reminders the day before a direct debit occurs, a subscription view that lets you view current subscriptions and when they’re set to expire, an improved search feature and the ability to automatically accept direct debits and payment requests from your friends — make sure you set up a limit before enabling that feature.

Bunq recently announced plans to raise $228 million (€193 million) at a $1.9 billion valuation (€1.6 billion). The investment round hasn’t been approved by the Netherlands’ banking regulator just yet. Bunq is currently operating in 29 European markets.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Natasha and Alex and Grace and Chris were joined by none other than TechCrunch’s own Mary Ann Azevedo, in her first-ever appearance on the show. She’s pretty much the best person and we’re stoked to have her on the pod.

And it was good that Mary Ann was on the show this week as she wrote about half the dang site. Which meant that we got to include all sorts of her work in the rundown. Here’s the agenda:

Powered by WPeMatico

Pry Financials wants to make startup finances approachable for its entire team, not just the people in charge of its accounting spreadsheets. The Y Combinator alum announced today it has raised $4.2 million from Global Founders Capital, Pioneer Fund, NOMO VC, Liquid2 and Hyphen Capital.

Launched in March, Pry now has more than 200 customers and claims it has grown 35% month-over-month since YC’s Demo Day. It was founded by Alex Sailer, Tiffany Wong, Hayden Jensen and Andy Su.

Before starting Pry, Su was co-founder of InDinero, another YC alum that started as a “Mint for small businesses” before pivoting to a full-service accounting company. InDinero launched while he was still a student at UC Berkeley, and Su eventually became responsible for its financial planning.

Pry Financials’ team. Image Credits: Pry Financials

He told TechCrunch that most startups can’t afford accounting software like Workday Adaptive Planning. Instead, they sometimes work with outsourced CFO services, but mostly rely on spreadsheets for everything: three-way forecasts, predicting runway, hiring and contractor budgets and investor updates.

“I was the chief technical officer and over the years, I also took on the finance function, so it was kind of a dual CTO/CFO role. This was 2010 through 2020 and as technology grew, the engineering and product teams got all sorts of new tools every six months or so, whereas the finance team was just stuck in Excel,” he said.

Started as a side project while Su was still at InDinero, Pry starts at just $50 a month and replaces those spreadsheets with easy-to-understand dashboards for accounting, financial planning and scenario modeling. The dashboards connect to QuickBooks, Xero or bank accounts, so numbers are continuously updated.

Pry’s clients typically start using it after they raise seed funding, because “for most first-time founders, that’s the most amount of money you have ever received, so you need to spend more time managing it and reviewing it every month. And you’re spending a lot of time on payroll each month,” Su said. Second-time founders, meanwhile, sign up for Pry because they are sick of Excel spreadsheets.

“Reviewing a spreadsheet is mind-numbingly hard,” said Su. “If you see a number that’s off, you get this weird formula if you didn’t do it yourself. Then you basically have to write a long email to the financial analyst who wrote it and hope that they get back to you before closing time.” For founders who need to update lenders or investors every month, this means a lot of work.

Pry makes the process more efficient by turning three-way reports — combinations of balance sheets, profit and loss statements and cashflow — into Financial Report dashboards, and then adding features like hiring plans, financial modeling and scenario planning.

The scenario planning feature serves as a sandbox, giving startup teams and their investors a way to predict how different situations will impact finances: for example, how much runway they have if they raise a certain amount of funding or adjust product pricing.

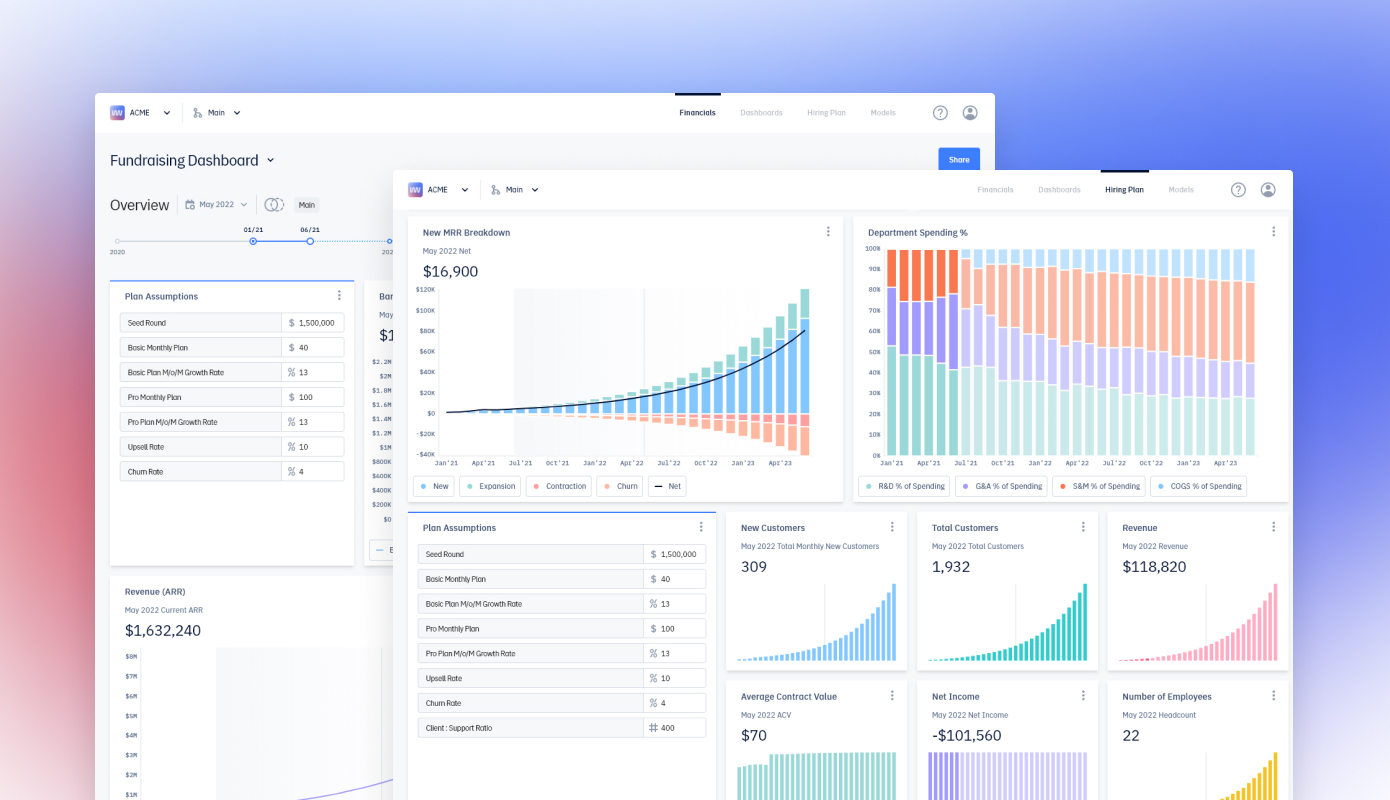

Fundraising dashboards created with Pry Financials. Image credits: Pry Financials

“We’re improving upon and trying to make decisions about the company in a collaborative way. The analogy we have is Git branching, where you have your main plan, and want to try something like a new revenue model or acquiring a business, but don’t want to mess with your current strategy,” said Su. “What you can do is create a completely new branch with, say, a new pricing strategy. You can make all the changes you want and then switch back to your old branch without worrying about overriding or conflicting with it.”

Those speculative branches are also continuously updated with the company’s most recent bank account and payroll information, so founders don’t need to recreate them from scratch if they want to revisit a potential scenario later.

Pry plans to build more complex predictive tools and also integrate industry standards, like statistic and benchmarks, into templates to help founders understand what targets they should set.

Because Pry is easier to manage than a set of Excel spreadsheets, Su said it’s helped startups spot important things. For example, one founder was able to find a way to save $15,000 by catching a tax issue. Pry also helps everyone at a startup understand its finances’ even if they haven’t worked with accounting spreadsheets before. The platform will add roles and permissions soon, so founders can give or restrict access to different people, like leaders of specific departments.

Su said Pry does not compete with the accounting services many startups rely on until they can hire a head of finance, but makes it easier for startups to collaborate with them since they can share their dashboards.

“Usually early on, you can outsource to a CFO firm. That’s the norm in the business and it works pretty well for most companies. You get a part-time CFO to work really hard for a month and get your fundraising structure done,” said Su, adding “we fit into that ecosystem well.”

Powered by WPeMatico

The dollars keep flowing into Latin America.

Today, Argentine personal finance management app Ualá announced it has raised $350 million in a Series D round at a post-money valuation of $2.45 billion.

SoftBank Latin America Fund and affiliates of China-based Tencent co-led the round, which included participation from a slew of existing backers, including funds managed by Soros Fund Management LLC, funds managed by affiliates of Goldman Sachs Asset Management, Ribbit Capital, Greyhound Capital, Monashees and Endeavor Catalyst. New funds, such as D1 Capital Partners and 166 2nd, also put money in the round in addition to angel investors such as Jacqueline Reses and Isaac Lee.

The round is believed to be the largest private raise ever by an Argentinian company and brings Ualá’s total raised to $544 million since its 2017 inception.

Founder and CEO Pierpaolo Barbieri, a Buenos Aires native and Harvard University graduate, has said his ambition was to create a platform that would bring all financial services into one app linked to one card.

Today, Ualá says it has developed “a complete financial ecosystem,” including universal accounts, a global Mastercard card, bill payment options, investment products, personal loans, installments (BNPL) and insurance. It has also launched merchant acquiring, Ualá Bis, a solution for entrepreneurs and merchants that allows selling through a payment link or mobile point-of-sales (mPOS).

The startup has issued more than 3.5 million cards in its home country and in Mexico, where it launched operations last year. The company claims that more than 22% of 18 to 25-year-olds in Argentina have a Ualá card. At the time of its Series C raise in November 2019, it had issued 1.3 million cards.

Image Credits: Ualá

Over 1 million users invest in the mutual fund available on the Ualá app, which the company claims is the second largest mutual fund in Argentina in number of participants. The company, which has aimed to provide more financial transparency and inclusion in the region, says that 65% of its users had no credit history prior to downloading the app.

Ualá plans to use its new capital to continue expanding within Latin America, develop new business verticals and do some hiring, with the plan of having 1,500 employees by year’s end. It currently has more than 1,000 employees.

“We are most impressed by Ualá’s ambition and execution. Our investment will propel the next stage of their vision, furthering a regional ecosystem that can make financial services more accessible and transparent across LatAm,” said Marcelo Claure, CEO of SoftBank Group International and COO of SoftBank Group, in a written statement.

Powered by WPeMatico

The Chinese government’s crackdown on its domestic technology industry continues, with Tencent under fresh pressure despite the company’s efforts to follow changing regulatory expectations.

News broke over the weekend that Beijing filed a civil suit against Tencent “over claims its messaging-app WeChat’s Youth Mode does not comply with laws protecting minors,” per the BBC. And NetEase, a major Chinese technology company, will delay the IPO of its music arm in Hong Kong. Why? Uncertain regulations, per Reuters.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The latest spate of bad news for China’s technology industry follows a raft of regulatory changes and actions by the nation’s government that have deleted an enormous quantity of equity value. After a period of relatively light-touch regulatory oversight, domestic Chinese technology companies have found themselves on defense after the Chinese Communist Party (CCP) came after their market power in antitrust terms — and some of their business operations from other perspectives. Sectors hit the hardest include fintech and edtech.

Gaming is also in the CCP crosshairs.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

NetEase stock traded around $110 per share in late July. It’s now worth around $90 per share after expectations shifted in light of the gaming news, indicating that investors are concerned about its future performance. Tencent’s Hong Kong-listed stock has also fallen, from HK$775.50 to HK$461.60 this morning.

Tencent tried to head off regulatory pressure, announcing changes to how it controls access to its games after the government’s shot across the bow. The effort doesn’t appear to have worked. That Tencent is being sued by the government despite its publicly announced changes implies that its proposed curbs to youth gaming were either insufficient or perhaps moot from the beginning.

Powered by WPeMatico

Canopy Servicing announced this morning it recently closed a $15 million Series A. The startup sells software to fintechs and others, allowing customers to create loan programs and service the resulting products.

The company raised a $3.5 million seed round in 2020. Canaan led its Series A, with participation from Homebrew, Foundation and BoxGroup, among others. Per Canopy, its valuation grew by 5x from its seed round to its Series A.

The company has raised $18.5 million to date.

So far this reads much like any other post announcing a new startup funding round, kicking off with an array of information concerning the round and who chipped into the transaction. Next, we’d probably note the competitors, growth and what investors in the company in question have to say about their recent purchase. This morning, however, I want to riff a bit on the future of fintech and how the financial tech stack of the future may be built.

TechCrunch chatted with Canopy CEO Matt Bivons last week. He has an interesting take on where fintech is headed. Let’s discuss it and work through what Canopy does.

As with many startups, Canopy was built to scratch an itch. Bivons had run into issues regarding loan servicing in prior jobs. He went on to found a startup that aimed to build a student credit card. But after working on that project, Bivons and co-founder Will Hanson pivoted the company to a B2B-focused concern building loan servicing technology.

Behind the decision was market research undertaken by the Canopy crew that uncovered that a great number of fintech startups wanted to get into the credit market. That makes sense; credit products can provide far more attractive economics to fintech startups than, say, checking and savings accounts. Knowing that loan servicing was a bear and a half to manage, Canopy decided to focus on it.

Bivons framed Canopy as a modern API for loan servicing that can be used to create and manage loans at any point in their lifecycle. He noted that what the startup is doing is akin to what several successful fintech companies have done, namely taking a piece of the fintech world and making it better for developers.

This is where Bivons’ view of the future of fintech products comes into play. According to the CEO, in the future, companies will not buy a monolithic financial technology stack. Instead, he thinks, they will buy the best API for each slice of the fintech world that they need to implement. This matters because we could argue that Canopy is targeting too small a product space. Not that its market isn’t large — debt and its servicing are massive problem spaces — but seeing a company find a niche to focus on makes more sense when its leaders expect focused fintech products to win out over large bundles of services.

Bivons added that much of the fintech focus of the last five years has been on debit, citing Chime, Step and Greenlight as examples. The next decade, he said, is going to focus on credit products. That would be good news for Canopy.

Canopy co-founders via the company. CTO Will Hanson (left) and CEO Matt Bivons (right).

Critically, and for the finance nerds out there, Bivons told TechCrunch that its loan servicing technology does not require the company to take on any credit risk, and that it has gross margins of around 90%. I never trust a too-round number, but the figure indicates that what Canopy has built could grow into an attractive business.

Today, Canopy is a traditional SaaS, though Bivons said that it wants to move toward usage-based pricing in time. Its service costs around 50 cents per account per month, or around $6 per year in its current form. Today, around 40% of Canopy’s customers are seed and Series A-scale startups, though Bivons noted that it is moving up the customer size chart over time.

The resulting growth is impressive. Canopy’s customer count grew 4.5x from February to May of 2021. Of course, Canopy is a young company, so its overall customer base could not have been massive at the start of the year. Still, that’s the sort of growth that makes investors sit up and pay attention, making the Canopy Series A somewhat unsurprising.

Fintech growth doesn’t seem to be slackening much, meaning that the market for what Canopy is selling should expand. Provided that its view that best-of-breed, more particular fintech products will beat larger stacks in the market, it could have an interesting trajectory ahead of it. And now that it has raised its Series A, we can start to annoy it with more concrete questions about its growth from here on out.

Powered by WPeMatico

Reserve Trust, a Denver-based financial services provider, has raised $30.5 million in a Series A round led by QED Investors.

FinTech Collective, Ardent Venture Partners, Flywire CEO Mike Massaro and Quovo founder and CEO Lowell Putnam also participated in the financing, which included $17.9 million in secondary shares. It brings the startup’s total raised since its 2016 inception to $35.5 million.

Reserve Trust describes itself as “the first fintech trust company with a Federal Reserve master account.” What does that mean exactly? Basically, a federal reserve master account allows Reserve Trust to move dollars on behalf of its customers directly, via wire and ACH payment rails, without an intermediate or partner bank.

Historically, only banks were able to access these payment rails directly, which left both domestic and international fintechs “with limited partner options, poor technology and slow implementations when it came to embedding high-value B2B payments,” says COO Dave Cahill. Reserve Trust touts that its technology and services give companies all over the world the ability to “seamlessly move money via the first cloud-based payment system connected directly to the Federal Reserve” since it is not limited by legacy banking systems.

Image Credits: CEO Dave Wright and COO Dave Cahill / Reserve Trust

In conjunction with the fundraise, Reserve Trust is also announcing that Dave Wright has been named CEO and Cahill joined as COO. The pair worked together previously at SolidFire, a flash storage startup that Wright founded and sold to NetApp for $870 million in 2016.

Reserve Trust works with businesses that seek to embed domestic and cross-border B2B payment by offering them the ability to store funds in custody accounts that are backed by its Federal Reserve master account.

The history of the company relates back to the global financial crisis. After the crisis, banks in the U.S. went through a process called derisking, which meant they shed businesses that on a risk return basis weren’t as strong as other businesses. One of those included the handling of U.S. dollar payments, particularly in emerging countries.

“One of the consequences of this is that it became significantly more difficult and expensive for businesses and smaller economies to trade and move U.S. dollars around the world,” Wright told TechCrunch. “And the founders of Reserve Trust saw this opportunity to build a new type of financial institution that was focused on helping to provide U.S. dollar payment services, especially to emerging fintechs in markets around the world, and helping to reconnect those economies to global trade.”

But rather than start a bank, the founders (Dennis Gingold, Justin Guilder) navigated a previously unexplored part of regulatory waters to create a state-chartered trust company with a Federal Reserve master account.

“That’s something that had never really been done before,” Wright added. “Pretty much every other trust company has to work through banks for all their payment services. Reserve Trust is the first that has actually managed to get a Federal Reserve master account and can process payments directly with the Federal Reserve.”

The complex process took about three years, and in 2018, the company got a Federal Reserve master account and started providing U.S. dollar custody and payment services for fintechs all over the world. Reserve Trust began to see strong demand from payment and fintech companies that were struggling to develop strong partner bank relationships, even though fundamentally there wasn’t any reason the banks couldn’t work with them.

“They found working with banks to be a slow process, one that didn’t involve a lot of technology expertise on the side of the banks, and it was really inhibiting their ability to develop their technology,” Wright said. And that was even here in the U.S. Today, more than half of its business is from domestic fintechs, although Reserve Trust still has a strong international presence as well.

The new funds will mainly go toward helping the company scale to handle what Wright describes as “a fairly overwhelming amount of demand” and toward building out the team, the technology and the services it needs to address the payment needs of larger, faster growing fintechs around the world.

“Most of our customers today are small and midsize fintechs, but now we’re seeing demand for much larger fintechs that have much higher payment volumes and are involved in embedded banking and B2B payments,” Wright said. “They are looking for a stronger banking partner than what they’ve been able to find among the role of traditional banks.” Customers include Unlimint and VertoFX, among others.

QED Investors partner Amias Gerety and FinTech Collective principal Matt Levinson are bullish both on Reserve Trust’s history and its potential.

The pair point to payments giant Stripe as an example of how far Reserve Trust can go.

“Stripe has significant market share doing merchant acquiring and processing e-commerce payments for the consumer,” Levinson said. “B2B payments is significantly bigger in terms of volume, so we’re talking about well over $20 trillion of addressable payment flow. But there’s no real technology company that’s brought the modern payments platform to market without being beholden to legacy banks. And that’s why we’re so excited about this business.”

Reserve Trust, he added, is giving businesses a way to facilitate B2B payments that “are smarter, faster and cheaper.”

Gerety agrees.

“Despite all the excitement around digital payments and infrastructure, there is still no fintech that can offer direct integration with the U.S. payment system,” he said. “With Reserve Trust, we are creating foundational infrastructure to hold and move payments globally and at scale.”

Powered by WPeMatico