fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

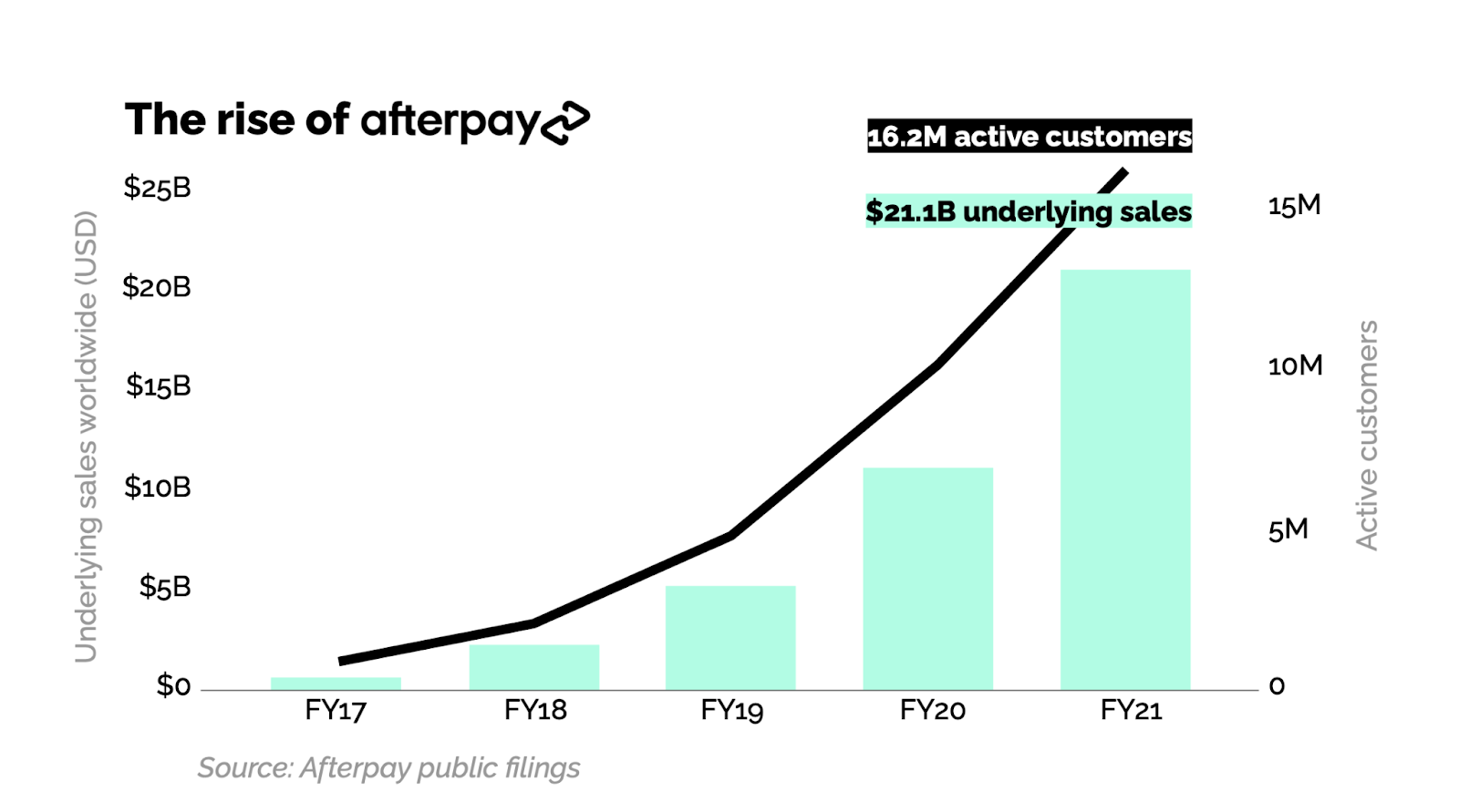

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

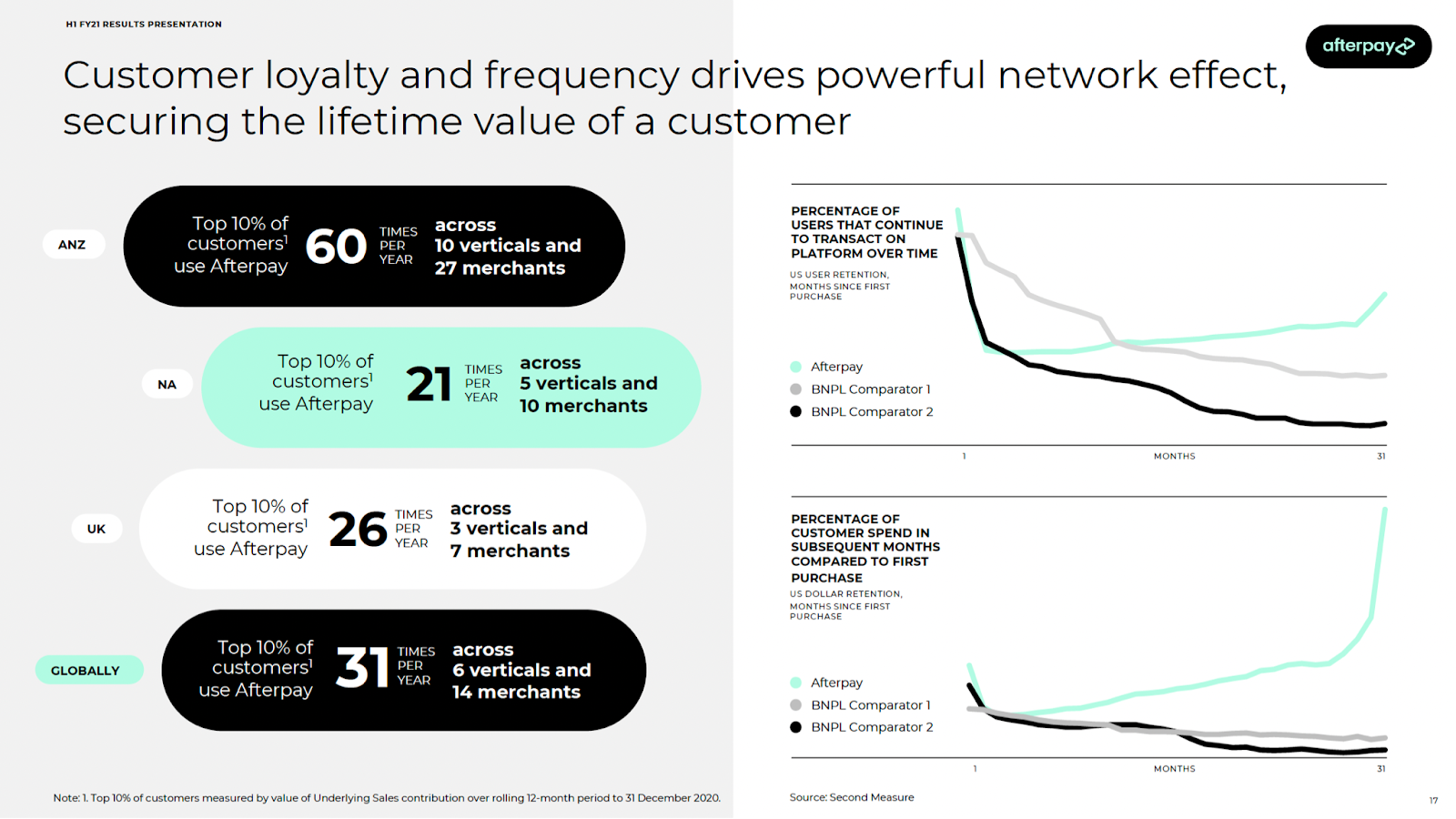

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Chilean startup Xepelin, which has created a financial services platform for SMEs in Latin America, has secured $30 million in equity and $200 million in credit facilities.

LatAm venture fund Kaszek Ventures led the equity portion of the financing, which also included participation from partners of DST Global and a slew of other firms and founders/angel investors. LatAm- and U.S.-based asset managers and hedge funds — including Chilean pension funds — provided the credit facilities. In total over its lifetime, Xepelin has raised over $36 million in equity and $250 million in asset-backed facilities.

Also participating in the round were Picus Capital; Kayak Ventures; Cathay Innovation; MSA Capital; Amarena; FJ Labs; Gilgamesh Ventures. A group of angels also participated in the financing, including Kavak founder and CEO Carlos Garcia; Jackie Reses, executive chairman of Square Financial Services; Justo founder and CEO Ricardo Weder; Tiger Global Management Partner John Curtius; GGV’s Hans Tung; and Gerry Giacoman, founder and CEO of Clara, among others.

Nicolás de Camino and Sebastian Kreis founded Xepelin in mid-2019 with the mission of changing the fact that “only 5% of companies in all LatAm countries have access to recurring financial services.”

“We want all SMEs in LatAm to have access to financial services and capital in a fair and efficient way,” the pair said.

Xepelin is built on a SaaS model designed to give SMEs a way to organize their financial information in real time. Embedded in its software is a way for companies to apply for short-term working capital loans “with just three clicks, and receive the capital in a matter of hours,” the company claimed.

It has developed an AI-driven underwriting engine, which the execs said gives it the ability to make real-time loan approval decisions.

“Any company in LatAm can onboard in just a few minutes and immediately access a free software that helps them organize their information in real time, including cash flow, revenue, sales, tax, bureau info — sort of a free CFO SaaS,” de Camino said. “The circle is virtuous: SMEs use Xepelin to improve their financial habits, obtain more efficient financing, pay their obligations, and collaborate effectively with clients and suppliers, generating relevant impacts in their industries.”

The fintech currently has over 4,000 clients in Chile and Mexico, which currently has a growth rate “four times faster” than when Xepelin started in Chile. Over the past 22 months, it has loaned more than $400 million to SMBs in the two countries. It currently has a portfolio of active loans for $120 million and an asset-backed facility for more than $250 million.

Overall, the company has been seeing a growth rate of 30% per month, the founders said. It has 110 employees, up from 20 a year ago.

“When we talk about creating the largest digital bank for SMEs in LatAm, we are not saying that our goal is to create a bank; perhaps we will never ask for the license to have one, and to be honest, everything we do, we do it differently from the banks, something like a non-bank, a concept used today to exemplify focus,” the founders said.

Both de Camino and Kreis said they share a passion for making financial services more accessible to SMEs all across Latin America and have backgrounds rooted deep in different areas of finance.

“Our goal is to scale a platform that can solve the true pains of all SMEs in LatAm, all in one place that also connects them with their entire ecosystem, and above all, democratized in such a way that everyone can access it,” Kreis said, “regardless of whether you are a company that sells billions of dollars or just a thousand dollars, getting the same service and conditions.”

For now, the company is nearly exclusively focused on the B2B space, but in the future, it believes several of its services “will be very useful for all SMEs and companies in LatAm.”

“Xepelin has developed technology and data science engines to deliver financing to SMBs in Latin America in a seamless way,” Nicolas Szekasy, co-founder and managing partner at Kaszek Ventures, said in a statement. “The team has deep experience in the sector and has proven a perfect fit of their user-friendly product with the needs of the market.”

Chile was home to another large funding earlier this week. NotCo, a food technology company making plant-based milk and meat replacements, closed on a $235 million Series D round that gives it a $1.5 billion valuation.

Powered by WPeMatico

When co-founders Songe LaRon and Dave Salvant first began barbershop tech platform Squire in 2016, they leaned in: The duo bought a barbershop in New York City’s Chelsea neighborhood to see firsthand how the business worked. For one year, the co-founders religiously worked at the shop, now owned by a larger barbershop chain, handling every bit of the business (except cutting hair).

Five years later, the co-founders view that experience as a key moment in the history of Squire, now a 175-person company with a tech platform used by over 2,000 shops across three continents. After last raising a Series C in December and tripling its valuation, Squire announced today that it has raised a $60 million round led by Tiger Global.

And, it tripled its valuation, again. Off of 300% year-over-year revenue growth, the New York startup is now valued at $750 million. It’s a massive uptick: A little over a year ago, Squire was valued at $75 million.

Like many startups these days, Squire wasn’t searching for capital when Tiger Global, which participated in its Series B and C rounds, offered to lead its next financing. The startup has only spent 10% of its previous round, a $45 million equity round, and now has tens of millions more in the bank. Ultimately, its decision to bring on more capital is so it can expand in the U.K. and Canada more aggressively — even in the wake of early-stage competitors like Boulevard. Squire’s dry powder also puts the co-founders in a position to acquire companies, a strategy that Salvant is into and plans to be “aggressive about.”

Squire also announced today the official launch of a product that has been in the roadmap since inception: Squire Capital, a money management platform with tools tailored to the needs of barbershop operations, such as instant payments. Squire’s core business has been more around appointments, loyalty programs and the installment of contactless payment. Now, a fintech layer aims to offer a more niche service than current financial services heavyweights like Square or Paypal.

Fintech is a “natural next frontier” for Squire, Salvant said, because the startup already has deep insights into how its businesses operate and how they process sales; now, it wants to add another service so it can offer a more holistic experience to them.

Squire Capital was built with Bond, a venture-backed fintech infrastructure startup that aims to help enterprise operations launch their own banking products. After experimenting with a $15 million debt financing arm around the time of its Series C, Squire isn’t offering loans at this time, hoping to find a better way to scale offerings in the future.

Squire is en route to becoming a historical and unfortunately still rare Black-led unicorn. Salvant talked about the significance of that feat, noting that this was “the optimal outcome” when founding the company. He hopes that VCs and investors will start to invest more in Black founders with Squire as a data point of a success story.

“Let’s face it, we’re not typical founders, we don’t look the same and we don’t act the same,” Salvant said. “I just want to serve as a lighthouse and this is validation for myself, my co-founder, but more importantly, what’s coming after us.”

Powered by WPeMatico

Monarch, a subscription-based platform that aims to help consumers “plan and manage” their financial lives, has raised $4.8 million in seed funding.

Accel led the round, which also included participation from SignalFire, and brings the Mountain View-based yet fully distributed startup’s total funding since its 2019 inception to $5.5 million.

Co-founder and CEO Val Agostino was the first product manager on the original team that built Mint.com. There, he said, he saw firsthand that Americans with a greater understanding of financial matters “needed software solutions that went beyond just tracking and budgeting.”

“They needed help planning their financial future and understanding the tradeoffs between competing financial priorities,” he said.

Monarch aims to help people address those needs with software it says “makes it easy” for people to outline their financial goals and then create a detailed, forward-looking plan toward achieving them.

“We then help customers track their progress against their plan and automatically course correct as their financial situation changes, which it always does,” Agostino said.

Monarch came out of private beta in early 2021 with apps for web, iOS and Android, and is priced at $9.99 per month or $89.99 per year. The startup intentionally opted to not be ad-supported or sell customers’ financial data.

These approaches are “misaligned with users’ financial interests,” Agostino said.

“We felt that a subscription business model would best support that ethos and align our users’ interests with our own,” he added. Since launching publicly, Monarch has been growing its paid subscriber base by about 9% per week.

Image Credits: Monarch

Monarch launched during the pandemic, the uncertainty of which carried over into people’s financial lives, believes Agostino.

“As a result, we saw a lot of people make use of Monarch’s forecasting features to compare different ‘what if ‘scenarios such as switching jobs or moving to a different city or state,” he said.

Earlier this month, TechCrunch reported on a company with a similar mission, BodesWell, teaming up with American Express on a financial planning tool for its cardholders. Agostino said that Monarch is similar to BodesWell in that both startups help customers map a financial plan and future.

“The difference is that Monarch also has a full suite of PFM tools, such as budgeting, reporting and investment analysis,” he said. “The benefit to the consumer is that because Monarch is connected to your entire financial picture, we can help you actually stay on track with your financial plan and/or update the plan in real time if needed.”

Accel’s Daniel Levine said that until he came across Monarch, he was “somehow still a Mint customer despite its obsolescence.”

Over the past decade, the landscape for financial products has expanded dramatically, with more people having brokerage and crypto accounts, for example, Levine said.

In his view, Monarch stands out for a couple of reasons. For one, it’s a subscription product.

“One thing I always hated about Mint was when it would suggest the objectively wrong credit card for me,” Levine said. “It has all of my transaction data, it should tell me the card with the best rewards for me. Monarch is set up to never compromise what’s best for the user in favor of advertising.”

Secondly, Monarch’s aim is to serve as the infrastructure for its customers. To do that, it needs to monitor all of someone’s finances.

“They need to track checking, credit cards, brokerage, real estate and crypto,” he said. “Monarch is committed to doing that. It’s an incredibly painful problem and even though Monarch is a new entrant in the space, I think they’ve clearly separated themselves on that dimension.”

Powered by WPeMatico

It’s pretty easy for individuals to send money back and forth, and there are lots of cash apps from which to choose. On the commercial side, however, one business trying to send $100,000 the same way is not as easy.

Paystand wants to change that. The Scotts Valley, California-based company is using cloud technology and the Ethereum blockchain as the engine for its Paystand Bank Network that enables business-to-business payments with zero fees.

The company raised $50 million Series C funding led by NewView Capital, with participation from SoftBank’s SB Opportunity Fund and King River Capital. This brings the company’s total funding to $85 million, Paystand co-founder and CEO Jeremy Almond told TechCrunch.

During the 2008 economic downturn, Almond’s family lost their home. He decided to go back to graduate school and did his thesis on how commercial banking could be better and how digital transformation would be the answer. Gleaning his company vision from the enterprise side, Almond said what Venmo does for consumers, Paystand does for commercial transactions between mid-market and enterprise customers.

“Revenue is the lifeblood of a business, and money has become software, yet everything is in the cloud except for revenue,” he added.

He estimates that almost half of enterprise payments still involve a paper check, while fintech bets heavily on cards that come with 2% to 3% transaction fees, which Almond said is untenable when a business is routinely sending $100,000 invoices. Paystand is charging a flat monthly rate rather than a fee per transaction.

Paystand’s platform. Image Credits: Paystand

On the consumer side, companies like Square and Stripe were among the first wave of companies predominantly focused on accounts payable and then building business process software on top of an existing infrastructure.

Paystand’s view of the world is that the accounts receivables side is harder and why there aren’t many competitors. This is why Paystand is surfing the next wave of fintech, driven by blockchain and decentralized finance, to transform the $125 trillion B2B payment industry by offering an autonomous, cashless and feeless payment network that will be an alternative to cards, Almond said.

Customers using Paystand over a three-year period are able to yield average benefits like 50% savings on the cost of receivables and $850,000 savings on transaction fees. The company is seeing a 200% increase in monthly network payment value and customers grew two-fold in the past year.

The company said it will use the new funding to continue to grow the business by investing in open infrastructure. Specifically, Almond would like to reboot digital finance, starting with B2B payments, and reimagine the entire CFO stack.

“I’ve wanted something like this to exist for 20 years,” Almond said. “Sometimes it is the unsexy areas that can have the biggest impacts.”

As part of the investment, Jazmin Medina, principal at NewView Capital, will join Paystand’s board. She told TechCrunch that while the venture firm is a generalist, it is rooted in fintech and fintech infrastructure.

She also agrees with Almond that the B2B payments space is lagging in terms of innovation and has “strong conviction” in what Almond is doing to help mid-market companies proactively manage their cash needs.

“There is a wide blue ocean of the payment industry, and all of these companies have to be entirely digital to stay competitive,” Medina added. “There is a glaring hole if your revenue is holding you back because you are not digital. That is why the time is now.”

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Mortgages may not be considered sexy, but they are a big business.

If you’ve refinanced or purchased a home digitally lately, you may not have noticed the company powering the software behind it — but there’s a good chance that company is Blend.

Founded in 2012, the startup has steadily grown to be a leader in the mortgage tech industry. Blend’s white label technology powers mortgage applications on the site of banks including Wells Fargo and U.S. Bank, for example, with the goal of making the process faster, simpler and more transparent.

The San Francisco-based startup’s SaaS (software-as-a-service) platform currently processes over $5 billion in mortgages and consumer loans per day, up from nearly $3 billion last July.

Today, Blend made its debut as a publicly traded company on the New York Stock Exchange, trading under the symbol “BLND.” As of early afternoon, Eastern Time, the stock was trading up over 13% at $20.36.

On Thursday night, the company had said it would offer 20 million shares at a price of $18 per share, indicating the company was targeting a valuation of $3.6 billion.

That compares to a $3.3 billion valuation at the time of its last raise in January — a $300 million Series G funding round that included participation from Coatue and Tiger Global Management. Also, let’s not forget that Blend only became a unicorn last August when it raised a $75 million Series F. Over its lifetime, Blend had raised $665 million before Friday’s public market debut.

In filing its S-1 on June 21, Blend revealed that its revenue had climbed to $96 million in 2020 from $50.7 million in 2019. Meanwhile, its net loss narrowed from $81.5 million in 2019 to $74.6 million in 2020.

In 2020, the San Francisco-based startup significantly expanded its digital consumer lending platform. With that expansion, Blend began offering its lender customers new configuration capabilities so that they could launch any consumer banking product “in days rather than months.”

Looking ahead, the company had said it expects its revenue growth rate “to decline in future periods.” It also doesn’t envision achieving profitability anytime soon as it continues to focus on growth. Blend also revealed that in 2020, its top five customers accounted for 34% of its revenue.

Today, TechCrunch spoke with co-founder and CEO Nima Ghamsari about the company’s decision to go with a traditional IPO versus the ubiquitous SPAC or even a direct listing.

For one, Blend said he wanted to show its customers that it is an “around for a long time company” by making sure there’s enough on its balance sheet to continue to grow.

“We had to talk and convince some of the biggest investors in the world to invest in us, and that speaks to how long we’ll be around to serve these customers,” he said. “So it was a combination of our capital need and wanting to cement ourselves as a really credible software provider to one of the most regulated industries.”

Ghamsari emphasized that Blend is a software company that powers the mortgage process and is not the one offering the mortgages. As such, it works with the flock of fintechs that are working to provide mortgages.

“A lot of them are using Blend under the hood, as the infrastructure layer,” he said.

Overall, Ghamsari believes this is just the beginning for Blend.

“One of the things about financial services is that it’s still mostly powered by paper. So a lot of Blend’s growth is just going deeper into this process that we got started in years ago,” he said. As mentioned above, the company started out with its mortgage product but just keeps adding to it. Today, it also powers other loans such as auto, personal and home equity.

“A lot of our growth is actually powered by our other lines of business,” Ghamsari told TechCrunch. “There’s a lot to build because the larger digitization trends are just getting started in financial services. It’s a relatively large industry that has lots of change.”

In May, digital mortgage lender Better.com announced it would combine with a SPAC, taking itself public in the second half of 2021.

Powered by WPeMatico

American Express is branching out into financial planning, with a little help from a seven-person startup called BodesWell.

This week, the credit card giant launched a pilot of its first self-service digital financial planning tool, dubbed “My Financial Plan (MFP).” The six-month pilot kicked off on July 11 with about 25,000 select Amex cardmembers.

American Express quietly invested in BodesWell in late 2020 via its venture arm, Amex Ventures. Since then, the financial services behemoth teamed up with the tiny startup to develop the financial planning tool for its users. The new product is designed to give users a complete picture of their financial health and help them make and achieve major life goals, such as buying a house or retirement.

TechCrunch talked with Amex Ventures’ Julia Huang, who led the investment and strategy around the new product, and BodesWell co-founder and CEO Matthew Bellows to learn more details.

The pair actually met while serving on a panel together in 2019.

“I was drawn to the fact that it was not a round-up savings tool, but rather a holistic tool to understand your full financial picture that could be used to plan for the financial impact of your life decisions,” Huang told TechCrunch.

Before deciding to invest in BodesWell, Huang says Amex Ventures — which over time has backed more than 70 startups — had “evaluated the space quite extensively.”

Huang introduced Bellows and his staff to Amex’s Digital Labs team and they embarked on jointly developing a specialized offering for Amex customers. (While Bellow is based in Boston, he says the startup is “globally distributed.”)

“Our goal is to democratize financial planning with our cardmembers by providing detailed insights and forecasts to help them with their holistic planning,” she told TechCrunch.

Image Credits: Amex Ventures

Bellows started BodesWell in early 2019 with the goal of empowering clients and customers to build their own financial plan.

“So much of financial planning software is aimed at financial advisors, and requires them to run it,” he said. “So, most people can’t get the benefits of financial planning…Our hope is to expand benefits to a lot more people.”

BodesWell will guide users in setting up a financial plan and will work even better if they sync with their other financial information via Plaid so it can “update in real time,” Huang said.

The tool “takes into account income, assets, expenses and liabilities — what cash flow looks like holistically so that users can drag & drop to plan life events,” Bellow said.

An estimated 85 million American households don’t have a financial, planner for a variety of reasons — including mistrust of a planner’s intentions or just feeling overwhelmed by the process.

The product is free during the pilot phase and American Express hasn’t yet determined if it will charge for it afterwards.

“We’re gauging first for engagement and the power of the product for our customers,” Huang told TechCrunch. “We want to make sure the product resonates and that we iterate on the product to make sure it’s good for the broader population. Our primary goal is that our customers use it and find it valuable.”

Amex Ventures has formed “some level of partnership” with more than two-thirds of its portfolio companies, she added.

“We try to engage with our portfolio in that way, to provide value with our startup ecosystem,” Huang said.

For its part, BodesWell had previously raised about $1.5 million from investors such as Cleo Capital, Ex Ventures, Riot.vc, GritCapital and Argon Capital and angels like HubSpot CEO Brian Halligan and Kintent CEO Sravish Sridhar.

Powered by WPeMatico

The gamification of payments is not a new concept.

A number of companies are attempting to combine gamification and payments in creative ways. And today, one such company, Play2Pay, has raised $13 million in a Series A round of funding.

The Miami-based startup has a straightforward mission. It wants to give consumers a way to reduce their bills — it claims by an average of 30%! — by playing games, watching videos and completing daily challenges, offers and surveys.

Play2Pay was bootstrapped for the first five years of its life, raising its first external capital in June of 2020 — a $7.5 million seed round from individual angel investors. Telesoft Partners led its Series A round, which included participation from Harbor Spring Capital and individual investors including former AT&T vice chairman Ralph de la Vega, former Reuters CEO Tom Glocer, Madison Dearborn Partners co-founder and senior advisor Jim Perry and Virtusa founder and former CEO, Kris Canekeratne.

The alternative payment platform says it brokers a “value exchange” between brands and consumers, converting attention and engagement into a currency, which can be redeemed for bill payment. Meanwhile, brands get a new way to promote their products and services.

Play2Pay founder and CEO Brian Boroff started the company in 2015 based on a vision that prepaid mobile phone users should have an alternative way to pay for their mobile phone service and that wireless carriers would adopt an ad-funded commercial model.

Today, the company claims to be positioned to be the world’s first “ad supported payment rail” directly integrated into payments platforms of major service providers and financial institutions. It also claims to be the only company that converts user engagement directly into bill payment.

Image Credits: Play2Pay

The “opt-in” offering is currently available to more than 100 million mobile subscribers across the United States, United Kingdom, Mexico, Brazil and Indonesia through partnerships with telecom companies such as AT&T Mexico, Cricket in the U.S., TIM in Brazil, lndosat Ooredoo in Indonesia and U.K.-based Lycamobile.

The rewarding approach seems to be resonating with users. From June 2020 to June 2021, the startup saw its ARR (annual recurring revenue) spike by nearly 300%, according to Boroff, a telecom veteran.

Among the users engaged on the platform, about 25% generated revenue daily, he said. And service providers realized up to 17% revenue expansion as a result of subscriber engagement on the Play2Pay platform, according to Boroff.

“Our distribution model is B2B2C, with Tier-1 service providers worldwide directly integrating our bill payment capability. We’re growing our audience through promotion of the service to their customer base,” he told TechCrunch.

End users, he added, can share their targeting preferences in exchange for value, giving mobile app developers and brands more information when promoting their own products and services to Play2Pay’s audience.

The platform is free for service providers and merchants, meaning the payment does not have costs or fees from interchange, acquirers, chargebacks or gateways.

Instead, Play2Pay generates revenue from mobile app developers and brands. Those developers and brands pay to access Play2Pay’s mobile audience in order to promote their products and services. For example, a mobile gaming company might pay Play2Pay $100 for every user that downloads their app from the Play2Pay app and plays the game for a period of time (such as two hours). Through its technology and partner network, Play2Pay has attribution tracking to ensure that the end user and mobile gaming company both know how much progress has been made toward completing that goal. Other formats include watching videos, completing surveys and more conventional native advertising in some areas.

Powered by WPeMatico

Financial services as a service — where entities like neobanks, retailers and others can create and sell their own financial products by way of a few lines of code and APIs — has been one of the bigger trends in the world of fintech in recent years, with embedded finance on its way to being a $7.2 trillion market by 2030, according to a forecast from Bain Capital. Now, one of the companies building and providing those APIs is announcing some growth funding to expand.

Railsbank, which builds APIs for banking, payment cards and credit products for use by fintechs but also a wide range of other kinds of businesses, has raised $70 million in new equity funding, money that the London startup plans to use to continue growing internationally and to add more features to its product set.

“Our mission is to reinvent, unbundle and democratise access to the complex, opaque and byzantine 70-year-old credit card market, which is worth $4 trillion in the U.S. alone,” Nigel Verdon, CEO and co-founder of Railsbank, told TechCrunch in an interview last year. Verdon is a repeat entrepreneur, with one of his previous companies being Currency Cloud.

Railsbank not disclosing its valuation, but Verdon hints that it is in the high hundreds of millions and close to $1 billion.

“As a policy, we rarely talk about valuation as we prefer to talk about customers,” he told TechCrunch today. “Valuation is a very inward-facing and self-centered metric. Saying that, near-unicorn would best describe us today.”

As a point of comparison data from PitchBook noted that the company was valued at just under $200 million in its last round at the end of last year (we reported on it here).

This latest round is being led by Anthos Capital, a previous backer of the company, with Central Capital, Cohen and Company, and Chris Adelsbach’s fund Outrun Ventures, as well as other unnamed previous backers also participating. Central Capital is a strategic investor: It’s the VC arm of the largest privately held bank in Indonesia, while Cohen and Company is the founder of Bancorp. Those backers speak to where Railsbank is targeting its services and who is interested in potentially working with it.

Banking as a service, and other financial products as a service, has become one of the most significant building blocks not just in the world of fintech, but in financial services overall. As with Twilio or Sinch in communications, or Stripe in payments, the idea here is that financial specialists have built out the complicated infrastructure and partnerships that underpin a product like a credit card, or a banking account.

This is then packaged up in a service that can be integrated into another one by way of an API, and the small amount of code needed to add it to another platform. In turn, that API can be used not just by another financial services company that is consumer- or business-facing, but by any kind of company that sees offering a financial product as part of a bigger customer service and loyalty play. That could mean a retailer offering its own-brand credit card, but also a “neobank” that is building a slick front end with great customer service and personalization, without needing to build the now-commoditized banking infrastructure underneath it to run it.

Railsbank is far from being the only company that has identified and built around this concept. Other big players include Rapyd, which raised a big round at a $2.5 billion valuation earlier this year; Unit, which also has been picking up funding and growing; FintechOS, which really does what its name says; and the startup 10x was even built for incumbent players to also have access to lighter fintech as a service.

Railsbank believes its distinct from many of its would-be competitors in part because it has built a lot of its own infrastructure from the ground up (hence the “rails” in its name), “bypassing” legacy players, in contrast to others that are built as software that still ultimately runs on top of stacks (and inefficiencies) of those older providers. This also means that it is regulated as a financial institution.

Railsbank is also in the business of making some acquisitions in order to grow its business, for example acquiring the U.K. business of German fintech Wirecard when it was crashing due to financial malpractices. And it doesn’t build everything from scratch: Earlier this year it also partnered with Plaid to embed some of its services within Railsbank’s.

Railsbank does not disclose a full list of customer names but has case studies on a number of smaller clients that speak to just how widely proliferated financial services are today. They include GoSolo, Kyshi and SimpledCard.

“The market has evolved so rapidly since we founded the world’s first BaaS business, the Bancorp,” noted Betsy Cohen, chairman of Fintech Masala and founder of Bancorp, in a statement. “As we move into the $7 trillion embedded finance market, it has been great watching Railsbank’s growth story. With this investment, it’s a privilege to continue to be part of the journey with a global leader like Railsbank.”

Powered by WPeMatico