financial technology

Auto Added by WPeMatico

Auto Added by WPeMatico

One of the biggest trends in the world of financial technology has been an ongoing push towards consolidation, where larger fish are snapping up smaller fish (including a proliferation of interesting startups) to get improved economies of scale in a business model where every transaction brings incremental returns. But today, a startup that has built the concept of consolidation into its basic DNA has raised another round of funding to continue doubling down on its business.

Rapyd — a London-based startup that has built an API that lets customers tap into a range of financial services spanning payments, checkout, funds collection, fund disbursements, compliance as a service, foreign exchange, card issuing and soon logistics across a wide range of geographies — has picked up an additional $20 million. Rapyd’s valuation with the funding is now at $1.2 billion (up from just under $1 billion in October).

The $20 million comes from new investment firm Durable Capital Partners.

Notably, it was only in October that Rapyd announced a $100 million raise. CEO and co-founder and Arik Shtilman said that Rapyd has now raised $180 million in total, with previous investors in the startup including Oak HC/FT Tiger Global, Coatue, General Catalyst, Target Global, Stripe and Entrée Capital. (Stripe, itself a fast-growing fintech upstart, remains only a financial investor in the company, Shtilman confirmed.)

Durable is the firm founded by Henry Ellenbogen, formerly a star investor at T. Rowe Price, in what Rapyd said was the firm’s first investment. (Note: Durable was also announced earlier as an investor in Convoy’s $400 million round, some clear signs that it’s open for business now.)

With Rapyd only recently raising a round, Shtilman said that the reason for the — err — rapid follow up was because the company is gearing up to make some acquisitions, as it too moves in on the consolidation trend by adding in more tools into its “Swiss Army Knife” of services.

“We’ve started to look at two acquisitions that were bigger than what we originally planned, with prices more in the range of $100 million,” he said. Up to now, Rapyd has largely built its technology from the ground up, but this will be about “getting at new business very quickly,” he added. Both deals are in progress now and are likely to close in February / March. One is of a card issuing platform (a la Marqeta), and the other is of a company based in Asia Pacific that is a significant player in payments in the region.

The focus on Asia Pacific both for testing out new services and acquisitions is in part because this, along with Latin America, have shaped up to be important geographies for the company. In the last three months, Rapyd has signed on 20 additional large-scale companies, Shtilman said, with several of them based out of, or serving, customers out of the two regions.

In fact, Rapyd doesn’t talk much about actual customers, but they include e-commerce merchants, gig-economy platforms — including Uber — financial institutions, and technology providers. The basic pitch is that financial services are complex, and providing one like payments often means having to offer others. Building these from scratch if this is not your core competency can be time-consuming and costly, and so that is where a company like Rapyd steps in with its API.

This is what attracted its newest investor, too. “Durable Capital Partners LP has a vision to identify and invest in promising early stage growth companies and invest in teams that have bold ideas but can also execute at a world-class level and build much larger companies,” said Ellenbogen in a statement. “I believe the Fintech-as-a-Service category has tremendous potential as companies seek to embed financial services as an integral part of the next generation technology stack. I believe Rapyd is very well positioned to drive this trend and I believe Arik’s track record in scaling cloud-based businesses will deliver success in this sector.”

When we last talked with Rapyd in October, we asked Shtilman about whether the company would ever move into logistics as part of its range of tools. After all, when you think about the complexities of procuring, storing and moving goods, it’s clear that logistics is one of the cornerstones you need to get right in an online business.

He said that this was on the company’s roadmap, and now Rapyd is in a pilot in Indonesia — an interesting test bed, considering that the country’s is spread across thousands of islands — where it has integrated a logistics service and given access to a single merchant as stage one of its closed beta. It’s also in discussions with other companies about how it can incorporate their services into the Rapyd platform to provide further “logistics as a service” to customers. He also confirmed the Durable has been a help here, by making an introduction to Convoy as part of that wider strategy.

Powered by WPeMatico

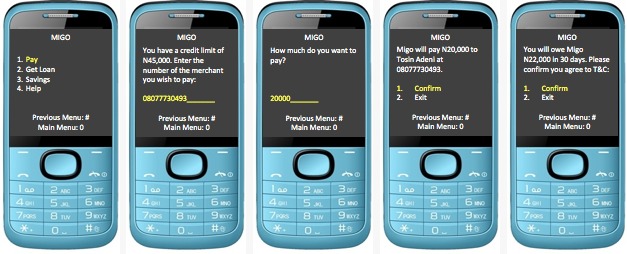

After growing its lending business in West Africa, emerging markets credit startup Migo is expanding to Brazil on a $20 million Series B funding round led by Valor Capital Group.

The San Franicso-based company — previously branded Mines.io — provides AI-driven products to large firms so those companies can extend credit to underbanked consumers in viable ways.

That generally means making lending services to low-income populations in emerging markets profitable for big corporates, where they previously were not.

Founded in 2013, Migo launched in Nigeria, where the startup now counts fintech unicorn Interswitch and Africa’s largest telecom, MTN, among its clients.

Offering its branded products through partner channels, Migo has originated more than 3 million loans to over 1 million customers in Nigeria since 2017, according to company stats.

“The global social inequality challenge is driven by a lack of access to credit. If you look at the middle class in developed countries, it is largely built on access to credit,” Migo founder and CEO Ekechi Nwokah told TechCrunch.

“What we are trying to do is to make prosperity available to all by reinventing the way people access and use credit,” he explained.

Migo does this through its cloud-based, data-driven platform to help banks, companies and telcos make credit decisions around populations they previously may have bypassed.

These entities integrate Migo’s API into their apps to offer these overlooked market segments digital accounts and lines of credit, Nwokah explained.

“Many people are trying to do this with small micro-loans. That’s the first place you understand risk, but we’re developing into point of sale solutions,” he said.

Migo’s client consumers can access their credit lines and make payments by entering a merchant phone number on their phone (via USSD) and then clicking on “Pay with Migo.” Migo can also be set up for use with QR codes, according to Nwokah.

He believes structural factors in frontier and emerging markets make it difficult for large institutions to serve people without traditional credit profiles.

“What makes it hard for the banks is its just too expensive,” he said of establishing the infrastructure, technology and staff to serve these market segments.

Nwokah sees similarities in unbanked and underbanked populations across the world, including Brazil and African countries such as Nigeria.

“Statistically, the number of people without credit in Nigeria is about 90 million people and its about 100 million adults that don’t have access to credit in Brazil. The countries are roughly the same size and the problem is roughly the same,” he said.

On clients in Brazil, Migo has a number of deals in the pipeline — according to Nwokah — and has signed a deal with a big-name partner in the South American country of 210 million, but could not yet disclose which one.

Migo generates revenue through interest and fees on its products. With lead investor Valor Capital Group, Velocity Capital and The Rise Fund joined the startup’s $20 million Series B.

Increasingly, Africa — with its large share of the world’s unbanked — and Nigeria — home to the continent’s largest economy and population — have become proving grounds for startups looking to create scalable emerging market finance solutions.

Migo could become a pioneer of sorts by shaping a fintech credit product in Africa with application in frontier, emerging and developed markets.

“We could actually take this to the U.S. We’ve had discussions with several partners about bringing the technology to the U.S. and Europe,” said founder Ekechi Nwokah. In the near-term, though, Migo is more likely to expand to Asia, he said.

Powered by WPeMatico

November 2019 could mark when Nigeria (arguably) became Africa’s unofficial capital for fintech investment and digital finance startups.

The month saw $360 million invested in Nigerian-focused payment ventures. That is equivalent to roughly one-third of all the startup VC raised for the entire continent in 2018, according to Partech stats.

A notable trend-within-the-trend is that more than half — or $170 million — of the funding to Nigerian fintech ventures in November came from Chinese investors. This marks a pivot (to tech) in China’s engagement with Africa. We’ll get to that.

Before the big Chinese-backed rounds, one of Nigeria’s earliest fintech companies, Interswitch, confirmed its $1 billion valuation after Visa took a minority stake in the company. Interswitch would not disclose the amount to TechCrunch, but Sky News reporting pegged it at $200 million for 20%.

Founded in 2002 by Mitchell Elegbe, Interswitch pioneered the infrastructure to digitize Nigeria’s then predominantly paper-ledger and cash-based economy.

The company now provides much of the tech-wiring for Nigeria’s online banking system that serves Africa’s largest economy and population. Interswitch offers a number of personal and business finance products, including its Verve payment cards and Quickteller payment app.

The financial services firm has expanded its physical presence to Uganda, Gambia and Kenya . The Nigerian company also sells its products in 23 African countries and launched a partnership in August for Verve cardholders to make payments on Discover’s global network.

Visa and Interswitch touted the equity investment as a strategic collaboration between the two companies, without a lot of detail on what that will mean.

One point TechCrunch did lock down is Interswitch’s (long-awaited) and imminent IPO. A source close to the matter said the company will list on a major exchange by mid-2020.

For the near to medium-term, Interswitch could stand as Africa’s sole tech-unicorn, as e-commerce venture Jumia’s volatile share-price and declining market-cap — since an April IPO — have dropped the company’s valuation below $1 billion.

Circling back to China, November was the month that signaled Chinese actors are all in on African tech.

In two separate rounds, Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent.

PalmPay, a consumer-oriented payments product, went live last month with a $40 million seed round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phone seller — China’s Transsion.

The startup was upfront about its ambitions, stating in a company release its goals to become “Africa’s largest financial services platform.”

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

![]()

OPay’s $120 million Series B was announced several days after the PalmPay news and came only months after the mobile-based fintech venture raised $50 million.

Founded by Chinese-owned consumer internet company Opera — and backed by nine Chinese investors — OPay is the payment utility for a suite of Opera -developed internet-based commercial products in Nigeria. These include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa and Ghana.

Though it wasn’t fintech, Chinese investors also backed a (reported) $30 million Series B for East African trucking logistics company Lori Systems in November.

With OPay, PalmPay and Lori Systems, startups in Africa have raised a combined $240 million from 15 Chinese investors in a span of months.

There are a number of things to note and watch out for here, as TechCrunch reporting has illuminated (and will continue to do in follow-on coverage).

These moves mark a next chapter in China’s engagement in Africa and could raise some new issues. Hereto, the country’s interaction with Africa’s tech ecosystem has been relatively light compared to China’s deal-making on infrastructure and commodities.

There continues to be plenty of debate (and critique) of China’s role in Africa. This new digital phase will certainly add a fresh component to all that. One thing to track will be data-privacy and national-security concerns that may emerge around Chinese actors investing heavily in African mobile consumer platforms.

We’ve seen lines (allegedly) blur on these matters between Chinese state and private-sector actors with companies such as Huawei.

As OPay and PalmPay expand, they may need to do some reassuring of African regulators as countries (such as Kenya) establish more formal consumer protection protocols for digital platforms.

One more thing to follow on OPay’s funding and planned expansion is the extent to which it puts Opera (and its entire suite of consumer internet products) in competition with multiple actors in Africa’s startup ecosystem. Opera’s Africa ventures could go head to head with Uber, Jumia and M-Pesa — the mobile money-product that put Kenya out front on digital finance in Africa before Nigeria.

Shifting back to American engagement in African tech, Twitter and Square CEO Jack Dorsey was on the continent in November. No sooner than he’d finished his first trip, Dorsey announced plans to move to Africa in 2020, for three to six months, saying on Twitter, “Africa will define the future (especially the bitcoin one!).”

We still don’t know much about what this last trip — or his future foray — mean in terms of concrete partnerships, investment or market moves in Africa from Dorsey and his companies.

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

I know pretty well most of the organizations and people Dorsey talked to and nothing has shaken out yet in terms of partnership or investment news from his recent trip.

On what could come out of Dorsey’s 2020 move to Africa, per his tweet and news highlighted in this roundup, a good bet would be it will have something to do with fintech and Square.

More Africa-related stories @TechCrunch

African tech around the ‘net

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Airbnb’s issues. Before that, I noted Uber’s new “money” team.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you’re new, you can subscribe to Startups Weekly here.

Three African fintech startups; OPay, PalmPay and East African trucking logistics company Lori Systems, closed large fundraises this year. On their own, the deals aren’t particularly notable, but together, they expose a new trend within the African startup ecosystem.

This year, those three companies brought in a total of $240 million in venture capital funding from 15 different Chinese investors, who’ve become increasingly active in Africa’s tech scene. TechCrunch reporter Jake Bright, who covers African tech, writes that 2019 marks “the year Chinese investors went all in on the continent’s startup scene” — particularly its fintech projects. Why?

“The continent’s 1.2 billion people represent the largest share of the world’s unbanked and underbanked population — which makes fintech Africa’s most promising digital sector,” Bright notes. “In previous years, the country’s interactions with African startups were relatively light compared to deal-making on infrastructure and commodities. Chinese actors investing heavily in African mobile consumer platforms lends to looking at new data-privacy and security issues for the continent.”

Active Chinese investors in Africa include Hillhouse Capital, Meituan-Dianping, GaoRong, Source Code Capital, SoftBank Ventures Asia, BAI, Redpoint, IDG Capital, Sequoia China, Crystal Stream Capital, GSR Ventures, Chinese mobile-phone maker Transsion and NetEase .

Here’s more of TechCrunch’s recent coverage of Africa startup activity:

It was a short week (Happy Thanksgiving, by the way). But here’s a quick look at the top deals of the last few days.

Last week, Facebook announced it was buying Beat Games, the game studio behind Beat Saber, a rhythm game that’s equal parts Fruit Ninja and Guitar Hero. Heard of the company? Maybe if you’re a gamer, but if you’re readying this newsletter because of your interest in VC, this company may not have come across your radar.

Why? It’s one of virtual reality’s biggest successes today, but it’s just an eight-person team with no funding.

“I’m really proud that we were able to build the company with this mindset of making decisions based on what is good for the game and not what is the most profitable thing,” Beat Games CEO told TechCrunch earlier this year. Read about Facebook’s acquisition here and an in-depth profile of the small team here.

If you like this newsletter, you will definitely enjoy Equity, which brings the content of this newsletter to life — in podcast form! Join myself and Equity co-host Alex Wilhelm every Friday for a quick breakdown of the week’s biggest news in venture capital and startups.

This week, we discussed Weekend Fund’s new vehicle, Cocoon’s new friend-tracking app and the unfortunate demise of a startup called Omni. You can listen here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about how SoftBank is screwing up. Before that, I noted All Raise’s expansion, Uber the TV show and the unicorn from down under.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Uber Head of Payments Peter Hazlehurst addresses the audience during an Uber products launch event in San Francisco, California, on September 26, 2019. (Photo by Philip Pacheco / AFP) (Photo credit should read PHILIP PACHECO/AFP/Getty Images)

The sheer number of startup players moving into banking services is staggering,” writes my Crunchbase News friends in a piece titled “Why Is Every Startup A Bank These Days.”

I’ve been asking myself the same question this year, as financial services business like Brex, Chime, Robinhood, Wealthfront, Betterment and more raise big rounds to build upstart digital banks. North of $13 billion venture capital dollars have been invested in U.S. fintech companies so far in 2019, up from $12 billion invested in 2018.

This week, one of the largest companies to ever emerge from the Silicon Valley tech ecosystem, Uber, introduced its team focused on developing new financial products and technologies. In a vacuum, a multibillion-dollar public company with more than 22,000 employees launching one new team is not big news. Considering investment and innovation in fintech this year, Uber’s now well-documented struggles to reach profitability and the company’s hiring efforts in New York, a hotbed for financial aficionados, the “Uber Money” team could indicate much larger fintech ambitions for the ride-hailing giant.

As it stands, the Uber Money team will be focused on developing real-time earnings for drivers accessed through the Uber debit account and debit card, which will itself see new features, like 3% or more cash back on gas. Uber Wallet, a digital wallet where drivers can more easily track their earnings, will launch in the coming weeks too, writes Peter Hazlehurst, the head of Uber Money.

This is hardly Uber’s first major foray into financial services. The company’s greatest feature has always been its frictionless payments capabilities that encourage riders and eaters to make purchases without thinking. Uber’s even launched its own consumer credit card to get riders cash back on rides. It’s no secret the company has larger goals in the fintech sphere, and with 100 million “monthly active platform consumers” via Uber, Uber Eats and more, a dedicated path toward new and better financial products may not only lead to happier, more loyal drivers but a company that’s actually, one day, able to post a profit.

The TechCrunch team is heading to Berlin again this year for our annual event, TechCrunch Disrupt Berlin, which brings together entrepreneurs and investors from across the globe. We announced the agenda this week, with leading founders including Away’s Jen Rubio and UiPath’s Daniel Dines. Take a look at the full agenda.

I will be there to interview a bunch of venture capitalists, who will give tips on how to raise your first euros. Buy tickets to the event here.

This week on Equity, I was in studio while Alex was remote. We talked about a number of companies and deals, including a new startup taking on Slack, Wag’s woes and a small upstart disrupting the $8 billion nail services industry. Listen to the episode here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on iTunes, Overcast and all the casts.

Powered by WPeMatico

Why raise venture capital when you can raise debt and keep your equity?

That’s the question a whole slew of new financial technology companies are hoping entrepreneurs will ask themselves as they begin to think about collecting outside capital for their businesses. Clearbanc made waves with its “20-Minute Term Sheet” campaign, with a goal of backing 2,000 businesses with $1 billion in non-dilutive capital by the end of 2019. Now, Capital is launching to educate founders about the possibility of debt funding.

Founded by former Draper Fisher Jurvetson (now known as Threshold Ventures) investor Blair Silverberg, Csaba Konkoly and Chris Olivares, Capital is launching today with $5 million from Future Ventures, Greycroft, Wavemaker and others. Additionally, it’s raised from “prominent institutional pools of capital” to invest between $5 million and $50 million in promising companies, determined using “The Capital Machine.”

Capital co-founder Blair Silverberg.

Capital’s underwriting technology, dubbed The Capital Machine, determines if businesses have the growth potential necessary for an infusion of debt (by analyzing revenue and other financial considerations), then delivers term sheets within 24 hours. The expedited process cuts out the time-consuming elements of pitching venture capitalists, the company says, allowing businesses to go from zero to $5 million — or more — in a matter of hours.

For companies that are’t ready for a debt round, or that don’t meet Capital’s qualification, the company is offering access to a free calculator that determines the cost of a company’s capital based on their fundraising and valuation data.

“We are trying to create a business that is the place that all founders go to start their fundraising process,” Silverberg tells TechCrunch. “We just want entrepreneurs to understand that step one in building a balance sheet is to understand your cost of capital. Step two is you can now use that to compare your financing options. We hope we can make this process simpler and more transparent.”

Capital charges a 5% to 15% flat fee on its capital, investing a maximum of $50 million over time. The company has ambitions of becoming a holistic investment bank of sorts, says Silverberg, ready and willing to advise companies on fundraising possibilities and connect them with VCs for future deals.

Historically, Silverberg explains, venture capital dollars went to risky upstarts poised to disrupt a category. Today, loads of equity funding is funneled into predictable business models that could be funded entirely with non-dilutive capital: “I saw what the venture process was like,” Silverberg said, referencing his stint at DFJ. “Tech companies do not utilize debt … this is extremely expensive for founders.”

There’s a culture surrounding venture capital fundraising in Silicon Valley and beyond. One in which startups seek to become “unicorns,” hoping for stories on this very site to laud their accomplishments — including the loads of venture capital dollars they’ve pulled in. In reality, much of that capital is plowed into things like Facebook and Google to fuel digital ad campaigns, which is not how VC is intended to be used and can result in founders taking a company public with just a few percentage points of ownership.

Solutions like Capital, Clearbanc, Lighter Capital and others should remind entrepreneurs that venture capital isn’t the only route to getting a company off the ground and can be raised in addition to venture debt.

“There’s no excuse for not knowing your cost of capital,” Silverberg adds.

Powered by WPeMatico

Project A, the Berlin-based VC, just raised a new $200 million fund (€180 million) to continue backing European startups at Seed and Series A stage.

In addition, the firm — whose investments include WorldRemit, Catawiki, Voi and Uberall — announced it will now have a presence in London and Stockholm in order to put people on the ground in what it says are “two of its favorite ecosystems.”

What better time, therefore, to catch up with the team at Project A, where we talked investment thesis, why Stockholm and London, and the increasing interest in Europe from U.S. LPs and VCs. Other subjects we touched on include diversity in venture, and, of course, Brexit!

TechCrunch: You last raised a fund in 2016, totaling €140 million, what changes have you noticed since then with regards to the types of companies you are seeing and the European ecosystem as a whole?

Uwe Horstmann: Entrepreneurs definitely matured a lot over the last few years. We see more and more of serial founders who combine drive with experience delivering great results. We also noticed an increase in more tech / product-centric and in B2B models.

This doesn’t come as a surprise as the market for consumer-oriented models started developing much earlier and is now reaching its limits after a few years. Many entrepreneurs gained experience in the Old Economy or have been consulting companies for a few years, learned about the struggle with products and processes first-hand and developed solutions specifically tailored to the industry’s needs.

We also notice a rise in professionalism in company setups and a higher ambition level in founding teams. This is probably also due to a more professional angel and micro fund scene that has developed in Europe.

TC: I note that you have U.S. LPs in the new fund, which I think is a first for Project A, and more broadly we are seeing a lot more interest from U.S. VCs in Europe these days. Why do you think that is, and how does this change the competitive landscape for deal-flow and the ambition of European founders?

Thies Sander: Having our first U.S. LPs on board makes us proud. LPs have noticed that European VC returns have really picked up during recent fund cohorts.

Powered by WPeMatico

For a seemingly tough pitch, Light has had little trouble getting noticed. The company has run two successful crowdfunding campaigns for a pair of minimalist phones designed to augment or replace the smartphone. Today the startup announced that it will be shipping the second version of the handset, which introduces a handful of features back into the product, like texting.

Ahead of the launch, we spoke to Light’s founders, Kaiwei Tang and Joe Hollier, about funding, feature glut and the future of the handset.

Brian Heater: The project essentially started as an in-house at Google, is that correct?

Kaiwei Tang: We met in 2014 in Google’s incubator called 30 Weeks. That’s where we met and started talking about Light Phone eventually.

Joe Hollier: 30 Weeks program was an experiment that came out of the Google creative lab, and their hypothesis was that if given the right resources, guidance, designers might be able to create new creative startups, and that designers should be on the founding table of companies.

So their hypothesis was that we as designers would be able to imagine a new startup in the software application space, and then through designing the end product, which is how the Google creative lab works, we’d be able to inspire the engineers and investors that we would need to make the product a reality.

Brian: What did you see in the market that wasn’t being fulfilled by countless different smartphone companies?

Joe: People were feeling overwhelmed by their smartphone and craving some escape, and we didn’t really see an escape.

Powered by WPeMatico

Financial service companies like banks have seen some of their business cannibalised over the years with the rise of digital-based alternatives — often in the form of apps — that provide lower fees, faster responsiveness and more flexibility to consumers. Today, Toronto-based startup Flybits is announcing $35 million in funding for a platform that it believes can offer these banks a way of continuing to capture their users’ attention and help them pivot into the next generation of services, financial or otherwise.

Today, a typical end product for a customer of Flybits’ services will use insights to upsell a customer by offering financial services; for example, a bank providing an offer of a specific kind of loan or credit card that you are more likely to take; or to offer a loyalty program or rewards for usage. But the longer-term goal, said CEO and co-founder Hossein Rahnama, is to help its customers take on a bigger role as repositories that can be used for more than just money, and used beyond the walls of the bank.

“We don’t think banks will go away, as some do, but we think that they could have a role not just as money vaults, but as data vaults: a place where you can deposit data, which you trust,” he said in an interview. Indeed, some of the funding will be used to put into action some of the AI and machine learning patents the startup has amassed, with the building of a “data” marketplace for banks, fintechs and other data providers to partner and build more services together.

The Series C comes from an interesting group of investors that includes both strategic backers using Flybits’ services, as well as backers of the more non-strategic, financial kind. Led by Point72 Ventures (hedge fund supremo Steve Cohen’s VC fund), the list also includes Mastercard, Citi Ventures and Reinventure (the fund backed by Australia’s Westpac Banking Corporation), Portag3 Ventures, TD Bank and Information Venture Partners. Valuation is not being disclosed, and prior to this the company had raised around $15 million.

Much like another marketing tech company, Near — which today announced $100 million in funding — the premise that underpins Flybits’ technology is that there is a lot of disparate data out there that, if it’s treated correctly, can uncover a lot more insights about consumer behavior, and that by and large many companies are missing this opportunity because they haven’t found the right way of merging the data to unlock insights.

While Near is applying this to location-based data and a range of different verticals, Flybits’ primary target has been banks and the data that they and other financial services providers already possess.

Many smaller startups in the world of financial services have stolen a march on bigger incumbents by building personalization into their products from the ground up. (Indeed, some like Step, aimed at teens, are so personalised that they will actually change their service mix as their customer base grows up and needs new products.) This is something that incumbents might have been more readily able to do in the old days, when people knew their bank managers and tellers and made daily trips into branches to transact. In the digital age they have fallen behind and are now catching up.

Flybits’ investors have spotted that and this in part is why they are banking on technologies like this to help bigger companies catch up, not just in financial services (although with banking alone estimated to be a €6.9 trillion industry, this is clearly a good start).

“Personalization is mission-critical for all D2C businesses in the digital age. Flybits’ integrated platform allows financial services firms to offer contextualized experiences, driving product awareness and adding significant value to the lives of their customers,” said Ramneek Gupta, managing director and co-head of Venture Investing at Citi Ventures, in a statement. “We look forward to partnering with Flybits in its next phase of growth as it continues to set the bar for hyper-personalized customer experiences.”

Indeed, it’s not just banks that are working on upselling, or that have large repositories of data that are not used as well as they could be.

“Mastercard and Flybits share a vision on using data driven insights to enrich consumers’ experiences,” said Francis Hondal, president, Loyalty & Engagement at Mastercard, in a statement. “Our ultimate goal is to develop products and services that engage consumers in a highly contextual manner. Through this collaboration with Flybits, we’ll be able to offer rich, personalized experiences for them throughout their journeys.”

Powered by WPeMatico

In the years following the financial crisis, de novo bank activity in the US slowed to a trickle. But as memories fade, the economy expands and the potential of tech-powered financial services marches forward, entrepreneurs have once again been asking the question, “Should I start a bank?”

And by bank, I’m not referring to a neobank, which sits on top of a bank, or a fintech startup that offers an interesting banking-like service of one kind or another. I mean a bank bank.

One of those entrepreneurs is Judith Erwin, a well-known business banking executive who was part of the founding team at Square 1 Bank, which was bought in 2015. Fast forward a few years and Erwin is back, this time as CEO of the cleverly named Grasshopper Bank in New York.

With over $130 million in capital raised from investors including Patriot Financial and T. Rowe Price Associates, Grasshopper has a notable amount of heft for a banking newbie. But as Erwin and her team seek to build share in the innovation banking market, she knows that she’ll need the capital as she navigates a hotly contested niche that has benefited from a robust start-up and venture capital environment.

Gregg Schoenberg: Good to see you, Judith. To jump right in, in my opinion, you were a key part of one of the most successful de novo banks in quite some time. You were responsible for VC relationships there, right?

…My background is one where people give me broken things, I fix them and give them back.

Judith Erwin: The VC relationships and the products and services managing the balance sheet around deposits. Those were my two primary roles, but my background is one where people give me broken things, I fix them and give them back.

Schoenberg: Square 1 was purchased for about 22 times earnings and 260% of tangible book, correct?

Erwin: Sounds accurate.

Schoenberg: Plus, the bank had a phenomenal earnings trajectory. Meanwhile, PacWest, which acquired you, was a “perfectly nice bank.” Would that be a fair characterization?

Erwin: Yes.

Schoenberg: Is part of the motivation to start Grasshopper to continue on a journey that maybe ended a little bit prematurely last time?

Erwin: That’s a great insight, and I did feel like we had sold too soon. It was a great deal for the investors — which included me — and so I understood it. But absolutely, a lot of what we’re working to do here are things I had hoped to do at Square 1.

Image via Getty Images / Classen Rafael / EyeEm

Schoenberg: You’re obviously aware of the 800-pound gorilla in the room in the form of Silicon Valley Bank . You’ve also got the megabanks that play in the segment, as well as Signature Bank, First Republic, Bridge Bank and others.

Powered by WPeMatico