financial technology

Auto Added by WPeMatico

Auto Added by WPeMatico

With $90 million in deposits and $18.25 million in new financing, HMBradley is making moves as the Los Angeles-based entrant into the challenger bank competition.

LA is home to a growing community of financial services startups, and HMBradley is quickly taking its place among the leaders with a novel twist on the banking business.

Unlike most banking startups that woo customers with easy credit and savvy online user interfaces, HMBradley is pitching a better savings account.

The company offers up to 3% interest on its savings accounts, much higher than most banks these days, and it’s that pitch that has won over consumers and investors alike, according to the company’s co-founder and chief executive, Zach Bruhnke.

With climbing numbers on the back of limited marketing, Bruhnke said raising the company’s latest round of financing was a breeze.

“They knew after the first call that they wanted to do it,” Brunke said of the negotiations with the venture capital firm Acrew, a venture firm whose previous exposure to fintech companies included backing the challenger bank phenomenon which is Chime . “It was a very different kind of fundraise for us. Our seed round was a terrible, treacherous 16-month fundraise,” Brunke said.

For Acrew’s part, the company actually had to call Chime’s founder to ensure that the company was okay with the venture firm backing another entrant into the banking business. Once the approval was granted, Brunke said the deal was smooth sailing.

Acrew, Chime and HMBradley’s founders see enough daylight between the two business models that investing in one wouldn’t be a conflict of interest with the other. And there’s plenty of space for new entrants in the banking business, Bruhnke said. “It’s a very, very large industry as a whole,” he said.

As the company grows its deposits, Bruhnke said there will be several ways it can leverage its capital. That includes commercial lending on the back end of HMBradley’s deposits and other financial services offerings to grow its base.

For now, it’s been wooing consumers with one-click credit applications and the high interest rates it offers to its various tiers of savers.

“When customers hit that 3% tier they get really excited,” Bruhnke said. “If you’re saving money and you’re not saving to HMBradley then you’re losing money.”

The money that HMBradley raised will be used to continue rolling out its new credit product and hiring staff. It already poached the former director of engineering at Capital One, Ben Coffman, and fintech thought leader Saira Rahman, the company said.

In October, the company said, deposits doubled month-over-month and transaction volume has grown to over $110 million since it launched in April.

Since launching the company’s cash back credit card in July, HMBradley has been able to pitch customers on 3% cash back for its highest tier of savers — giving them the option to earn 3.5% on their deposits.

The deposit and lending capabilities the company offers are possible because of its partnership with the California-based Hatch Bank, the company said.

Powered by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

One of my favorite series of Monty Python sketches is built around the concept of surprise:

Chapman: I didn’t expect a kind of Spanish Inquisition.

[JARRING CHORD]

[Three cardinals burst in]

Cardinal Ximénez: NOBODY expects the Spanish Inquisition!

I was reminded of this today when I needed to reschedule a few stories so we could cover DoorDash’s S-1 filing from multiple angles. First, Managing Editor Danny Crichton looked at how well the company’s co-founders and many investors stand to make out. Alex Wilhelm covered the IPO announcement in depth on TechCrunch before writing an Extra Crunch column that studied the role the COVID-19 pandemic played in the home-delivery platform’s recent growth.

Our all-hands-on-deck coverage of DoorDash’s S-1 is a good illustration of Extra Crunch’s mission: timely analysis of current and future technology trends that serves founders and investors. We have a talented team, and as today’s coverage shows, they’re just as good as they are fast.

The stories that follow are an overview of Extra Crunch from the last five days. The full articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thanks very much for reading Extra Crunch this week. I hope you have a great weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Klaus Vedfelt / Getty Images

We frequently run posts by guest contributors, but two stories we published this week were written in the first person, which is a bit of a departure.

In Why I left edtech and got into gaming, Darshan Somashekar brought us inside his decision to pivot away from a sector that’s been growing hotter in 2020.

His post is a unique take on two oft-discussed categories, but it also examines one founder/investor’s thought process when it comes to evaluating new opportunities.

Andy Areitio, a partner at early-stage fund TheVentureCity, wrote What I wish I’d known about venture capital when I was a founder, a reflection on the “classic mistakes” founders tend to make when it’s time to fundraise.

“Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time,” he says. “They can also put all their eggs in one basket too early. I made that mistake.”

You can find business writing that explores best practices anywhere, which is why we hunt down stories that are firmly rooted in data or personal experience (which includes success and failure).

Image Credits: DoorDash

The coronavirus pandemic looms large in DoorDash’s S-1 filing.

According to the food-delivery platform, “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” and “the COVID-19 pandemic has further accelerated these trends.”

As in other sectors, the pandemic didn’t wave a magic wand — instead, it hastened trends that were already in play: consumers love convenience, which means DoorDash’s gross order volume and revenue were tracking well before the virus started to shape our lives.

“It’s your call on how to balance the factors and decide whether or not to buy into the IPO, but this one is going to be big,” writes Alex Wilhelm in a supplemental edition of today’s The Exchange.

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

None of us knew DoorDash would release its S-1 filing today, but Danny Crichton jumped on the story “so we can see who is raking in the returns on the country’s delivery startup champion.”

After estimating the value of the respective ownership stakes held by DoorDash’s four co-founders, he turned to the investors who participated in rounds seed through Series H.

Some growth funds are about to look very good after this IPO, and each founder is looking at hundreds of millions, he found.

But even so, their diminished haul of about $1.3 billion is “a sign of just how much dilution the co-founders took given the sheer amount of capital the company fundraised over its life.”

Image Credits: Nigel Sussman (opens in a new window)

Investors sent stacks of cash to late-stage fintech companies in Q3 2020, but these sizable rounds may also point to shrinking opportunities for early-stage firms, reports Alex Wilhelm in this morning’s edition of The Exchange.

2020 could be a record year for fintech VC in Europe and North America, but are these “huge late-stage dollars” actually “a dampener for new fintech startups trying to get off the ground?”

Devin Coldewey interviewed the leaders of three startup accelerators to learn more about the adaptations they’ve made in recent months:

Due to travel bans, shelter-in-place orders and other unknowns, they’ve all shifted to virtual. But accelerators are intensive programs designed to indoctrinate founders and elicit brutally honest feedback in real time.

Despite the sudden shift, that boot-camp mindset is still in effect, Devin reports.

“Cutting out the commute time in a busy city leaves founders with more time for workshops, mentor matchmaking, pitch practice and other important sessions,” said Fernandez. “Everybody just has more flexibility and tranquility.”

Said Ebersweiler: “People are for some reason more participative and have more feedback than physically — it’s pretty strange.”

Image Credits: Greylock

In a recent interview with Greylock partner Asheem Chandna, Managing Editor Danny Crichton asked him about the buzz around no-code platforms and what’s happening in early-stage enterprise startups before segueing into a discussion about “shift left” security:

“Every organization today wants to bring software to market faster, but they also want to make software more secure,” said Chandna.

“There is a genuine interest today in making the software more secure, so there’s this concept of shift left — bake security into the software.”

Image Credits: Nigel Sussman (opens in a new window)

If you missed Wednesday’s The Exchange, Alex scoured earnings reports from PayPal and Square to see what the near future might hold for several fintech startups currently waiting in the wings.

Using Square and PayPal’s recent numbers for stock purchases, card usage and consumer payment activity as a proxy, he attempts to “see what we can learn, and to which unicorns it might apply.”

Image Credits: jayk7 (opens in a new window)/ Getty Images

In California, non-competition agreements can’t be enforced and a court has ruled that customer contact lists aren’t trade secrets.

That doesn’t mean salespeople who switch jobs can start soliciting their former customers on their first day at the new gig, however.

Before you jump ship — or hire a salesperson who already has — read this overview of California’s trade secret laws.

“Even without litigation, a former employer can significantly hamper a departing salesperson’s career,” says Nick Saenz, a partner at Lewis & Llewellyn LLP, who focuses on employment and trade secret issues.

Image: Bryce Durbin / TechCrunch

News of a highly effective COVID-19 vaccine appeared to drive down prices of the three best-known publicly traded edtech companies: 2U, Chegg and Kahoot saw declines of about 20%, 10% and 9%, respectively after the report.

Are COVID-19 tailwinds dissipating, or did the market make a correction because “edtech has been categorically overhyped in recent months?”

Image Credits: Sophie Alcorn

What does President-elect Biden’s victory mean for U.S. immigration and immigration reform?

I’m in tech in SF and have a lot of friends who are immigrant founders, along with many international teammates at my tech company. What can we look forward to?

— Anticipation in Albany

Powered by WPeMatico

Subscription services are on the rise. During the pandemic, Americans have been spending more time at home and more money on the digital products that make navigating our new normal easier.

More than ever, Americans’ lives are aided by companies like Netflix, Instacart and, of course, Amazon, which reported record-setting earnings from its 2020 Prime Day savings event.

A recent survey even found that spending on subscription services had more than tripled since March, with one in three respondents saying they’d purchased a new online subscription while quarantining.

Now, a new concern lingers: Is the market getting oversaturated? The question doesn’t just apply to streaming services and food delivery companies — it’s an issue financial technology businesses can’t afford to ignore.

As subscriptions become an increasingly alluring business model, fintechs will be forced to consider whether this proven strategy is worth the risk.

In the CompareCards survey, two-thirds of respondents said they purchased a new streaming service mainly for entertainment. Still, that doesn’t mean there isn’t room for fintechs to carve out their own space.

Bradley Leimer, co-founder of the financial consulting firm Unconventional Ventures, said he’s certainly seen more fintechs exploring subscription models. As Leimer explained, the financial services industry may have not fully embraced the idea, but it’s “starting to take notice.” Leimer, who has more than 25 years of experience in the industry, believes fintechs can learn a lot from subscription services — provided they’re willing to look in the right place.

One major lesson? Transparency. Subscription services give companies an opportunity to be upfront about their fees, as well as their benefits.

“When we talk about subscriptions, the more clear and more transparent we are, the better,” Leimer said.

Acorns is an easy case study. The microinvesting app offers three subscription levels — lite, personal and family — each with a clearly explained list of features. For what it’s worth, the company added more than 2 million users between March 2019 and March 2020, according to Forbes.

Leimer said fintechs should also take note of the way subscription services collaborate. For example, he pointed out how Amazon users can add an HBO subscription to their Prime Video account, essentially “bundling” two subscriptions into one. Fintechs, Leimer said, could stand to take a page out of that playbook.

“There are a lot of ways to sort of skin that cat — for a fintech company to generate income and for a customer to get value on top of that,” Leimer said.

Powered by WPeMatico

Year-in, year-out, the gender gap in venture capital investment continues to be a problem women founders face. While the gender gap in other areas (such as the number of women entering tech in general) may be on the right path, this disparity in funding seems to be stagnant. There has been little movement in the amount of VC dollars going to women-founded companies since 2012.

In fintech, the problem is especially prominent: Women-founded fintechs have raised a meager 1% of total fintech investment in the last 10 years. This should come as no surprise, given that fintech combines two sectors traditionally dominated by men: finance and technology. Though by no means does this mean that women aren’t doing incredible work in the field and it’s only right that women founders receive their fair share of VC investment.

In the short term, women founders can take action to boost their chances at VC success in the current investment climate, including leveraging their community and support network and building the necessary self-belief to thrive. In the long term, there needs to be foundational change to level the playing field for women entrepreneurs. VC funds must look at ways they can bring in more women decision-makers, all the way up to the top.

Let’s dive into the state of gender bias in VC investing as it stands, and what founders, stakeholders and funds themselves can do to close the gap.

In 2019, less than 3% of all VC investment went to women-led companies, and only one-fifth of U.S. VC went to startups with at least one woman on the founder team. The average deal size for female-founded or female co-founded companies is less than half that of only male-founded startups. This is especially concerning when you consider that women make up a much bigger portion of the founder community than proportionately receive investment (around 28% of founders are women). Add in the intersection of race and ethnicity, and the figures become bleaker: Black women founders received 0.6% of the funding raised since 2009, while Latinx female founders saw only 0.4% of total investment dollars.

The statistics paint a stark picture, but it’s a disparity that I’ve faced on a personal level too. I have been faced with VC investors who ask my co-founder — in front of me — why I was doing the talking instead of him. On another occasion, a potential investor asked my co-founder who he was getting into business with, because “he needed to know who he’d be going to the bar with when the day was up.”

This demonstrates a clear expectation on the part of VC investors to have a male counterpart within the founding team of their portfolio companies, and that they often — whether subconsciously or consciously — value men’s input over that of the women on the leadership team.

So, if you’re a female founder faced with the prospect of pitching to VCs — what steps can you take to set yourself up for success?

Women founders looking to receive VC investment can take a number of steps to increase their chances in this seemingly hostile environment. My first piece of advice is to leverage your own community and support network, especially any mentors and role models you may have, to introduce you to potential investors. Contacts that know and trust your business may be willing to help — any potential VC is much more likely to pay you attention if you come as a personal recommendation.

If you feel like you’re lacking in a strong support network, you can seek out female-founder and startup groups and start to build your community. For example, The Next Women is a global network of women leaders from progress-driven companies, while Women Tech Founders is a grassroots organization on a mission to connect and support women in technology.

Confidence is key when it comes to fundraising. It’s essential to make sure your sales, pitch and negotiation skills are on point. If you feel like you need some extra training in this area, seek out workshops or mentorship opportunities to make sure you have these skills down before you pitch for funding.

When talking with top male VCs and executives, there may be moments where you feel like they’re responding to you differently because of your gender. In these moments, channeling your self-belief and inner strength is vital: The only way that they’re going to see you as a promising, credible founder is if you believe you are one too.

At the end of the day, women founders must also realize that we are the first generation of our gender playing the VC game — and there’s something exciting about that, no matter how challenging it may be. Even when faced with unconscious bias, it’s vital to remember that the process is a learning curve, and those that come after us won’t succeed if we simply hand the task over to our male co-founder(s).

While there are actions that women can take on an individual level, barriers cannot be overcome without change within the VC firms themselves. One of the biggest reasons why women receive less VC investment than men is that so few of them make up decision-makers in VC funds.

A study by Harvard Business Review concluded that investors often make investment decisions based on gender and ask women founders different questions than their male counterparts. There are countless stories of women not being taken seriously by male investors, and subsequently not being seen as a worthwhile investment opportunity. As a result of this disparity in VC leadership teams, women-focused funds are emerging as a way to bridge the funding gender gap. It’s also worth noting that women VCs are not only more likely to invest in women-founded companies, but also those founded by Black entrepreneurs. In addition to embracing women and minority-focused investors, the VC community as a whole should ensure they’re bringing in more women leaders into top positions.

From day one, the Prometeo team has made concerted efforts to have both men and women in decision-maker roles. Having women in the founding team and in leadership positions has been crucial in not only helping to fight the unconscious bias that might take place, but also in creating a more dynamic work environment, where diversity of thought powers better business decisions.

Striving for gender equality, both within the walls of VC funds and in the founder community, is also better for businesses’ bottom line. In fact, a study by Boston Consulting Group found that women-founded startups generate 78% for every dollar invested, compared to 31% from men-founded companies.

Here in Latin America, women founders receive a higher proportion of VC investment than anywhere else in the world, so it’s no surprise that women are leading the region’s fintech revolution. Having more women in leadership positions is ultimately a better bet for business.

Closing the gender gap in VC funding is no simple task, but it’s one that must be undertaken. With the help of internal VC reform and external initiatives like community building, training opportunities and women-focused support networks, we can work toward finally making the VC game more equitable for all.

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

I’ve worked at TechCrunch for a little over a year, but this was one of the hardest weeks on the job so far.

Like many people, I’ve been distracted in recent days. As I write this, I have one eye on my keyboard and another on a TV that sporadically broadcasts election results from battleground states. Despite the background noise, I’m completely impressed with the TechCrunch staff; it takes a great deal of focus and energy to set aside the world’s top news story and concentrate on the work at hand.

Monday feels like a distant memory, so here’s an overview of top Extra Crunch stories from the last five days. These articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Marketplaces created for B2B activity are surging in popularity. According to one report, transactions in these venues generated around $680 billion in 2018, but that figure is predicted to reach $3.6 trillion by 2024.

The COVID-19 pandemic is helping startups that innovate in areas like payments, financing, insurance and compliance.

Even so, according to Merritt Hummer, a partner at Bain Capital Ventures, “B2B marketplaces cannot simply remain stagnant, serving as simple transactional platforms.”

The startups that are first to market with innovative “adjacent services will emerge as winners in the next few years,” she advises.

For this morning’s edition of The Exchange, Alex Wilhelm interviewed three executives at cloud and SaaS companies to find out how well Q3 2020 has been treating them:

As one Twitter commenter noted, Alex doesn’t just talk to the best-known tech execs; he reaches out to a wide range of people, and it shows in the quality of his reporting.

New Regulation Crowdfunding guidelines the SEC released this week allow companies to directly raise up to $5 million each year from individual investors, an increase from the previous limit of $1.07 million.

“Life has gotten easier in other ways as well for founders pursuing this fundraising type and the platforms that seek to simplify it,” reports Lucas Matney, who interviewed Wefunder CEO Nicholas Tommarello.

Funding for seed-stage startups slumped 32% last quarter compared to 2019, so “the tide could be turning” for founders who were reluctant to raise from a giant pool of small dollars, Lucas found.

Reaching scale is paramount for software companies, so growth is a top priority.

In a guest post for Extra Crunch, Drift CEO David Cancel explains that too many SaaS and cloud companies waste time trying out a number of solutions before finding the right recipe.

“I can tell you that there absolutely is a repeatable process to building a successful SaaS business,” he says, “one that can reliably guide you to product-market fit and then help you quickly scale.”

Companies that hope to eliminate longstanding inequities in the workplace can’t just rely on doing what they think is right. Without a data-driven approach, subjective judgments and implicit bias tend to negate good intentions.

Many startups don’t hire full-time HR managers until they’ve reached scale, but this comprehensive post lays out several critical factors for creating — and maintaining — a fair pay model.

News broke this week that Airbnb plans to to raise approximately $3 billion in a public filing that would allow it to reach a valuation in the $30 billion range.

Our expert unicorn wrangler Alex Wilhelm says curious investors should ask themselves the following:

“People at the end of their career write memoirs,” Starling Bank founder Anne Boden told TechCrunch’s Steve O’Hear. “I’m at the beginning.”

In Boden’s new book, “Banking On It,” she shares the story of how (and why) she decided to found a challenger bank, eventually parting with colleagues who launched competitor Monzo.

“This is really putting down on paper where we are at the moment,” she said. “It’s been written over several years, and I’m hoping to use this to inspire a generation of entrepreneurs.”

Natasha Mascarenhas and Alex Wilhelm collaborated on Monday’s edition of The Exchange to report on how investors became less likely to fund female founders since the beginning of the COVID-19 pandemic.

Drawing on data from multiple sources, Alex and Natasha found that startups led by women and mixed-gender founding teams received 48% less VC funding in Q3 2020 than in Q2, even though overall funding bounced back.

“From fear in late Q1, to a middling Q2, to a boom in Q3,” they wrote. “It was an impressive comeback. For some.”

Natasha Mascarenhas has owned TechCrunch’s edtech beat since she came aboard at the start of 2020, just a few months before the pandemic led to widespread school closures.

She’s reported on countless funding rounds and interviewed founders and investors who are active in the space, but she recently spotted a new trend: “M&A activity is buzzier than usual.”

Alex Wilhelm shrugged off his Election Day distractions long enough to write a column that comprehensively examined fintech investment activity over the last quarter.

In Q3 2020, “60% of all capital raised by financial technology startups came from just 25 rounds worth $100 million or more,” he reports.

Are these mega-rounds funding “the next crop of unicorns?” It’s too early to say, but it’s clear that pandemic-fueled uncertainty is driving consumers into the arms of companies like Robinhood, Chime, Lemonade and Root.

In 1,316 words, Alex captures the state of play in insurtech, banking, wealth management and payments investing: “Now, we just want to see some ******* IPOs.”

Five years ago, Terri Burns was a product manager at Twitter. Today, she’s the first Black woman — and the youngest person — to be promoted to partner at Google Ventures.

In a Q&A with Natasha Mascarenhas, Burns talked about her plans for the new role, as well as her investment thesis.

“I don’t know what it actually means to build a sustainable business and venture is a really great way to sort of learn that,” said Burns.

Are founders and investors really leaving Silicon Valley for greener pastures? Now that investors are limited to virtual interactions, are they being more hands-on with their portfolio companies?

In an Extra Crunch Live chat hosted by Darrell Etherington, GV General Partner MG Siegler talked about how the pandemic is — and is not — shaping the way he does business.

“I do feel like things are operating in a pretty streamlined manner, or as much as they can be at this point,” he said.

“But, you know, there’s always going to be some more wildcards — like we’re a week away, today, from the U.S. election.”

Thank you very much for reading Extra Crunch; I hope you have a great weekend.

Powered by WPeMatico

According to industry reports, venture capital deal-making has notably rebounded since dropping off briefly in March as shelter-in-place orders gripped much of the country.

As seed-stage fintech investors, this has certainly been our experience: “Hot” deals are getting funded faster than ever, and we increasingly see the large multistage global funds competing for the earliest access to companies. However, in our experience and anecdotal conversations with other early-stage investors, that excitement has not been translating to the Series A stage.

We’ve increasingly wondered if the Series A market in fintech is really as hot as it seems. As pre-seed and seed-stage investors, we know that the health of the Series A market is of critical importance.

In early October 2020, the Financial Venture Studio put together a brief survey of the Series A market in fintech and shared it with more than 100 investors with whom we work closely. Despite the high-level numbers indicating a healthy market, our research indicates a market that remains in flux, with significant ramifications for early-stage founders.

Although the seed and pre-seed fintech market continues to attract substantial entrepreneurial and investor interest, it is also in some ways one of the easiest parts of the market to fund. The check size is smaller, the velocity of new deals is highest, and while the potential returns are also the highest, this is also the part of the market where information is most scarce. Perhaps counterintuitively, the fact that there is so little information on a business — aside from a plan, a team and maybe some early anecdotal evidence to support the vision — actually makes it easier to “pull the trigger” on deals where those data points align. There just often isn’t a lot more to dig into.

Similarly, by the time a company is raising Series B capital, they typically have some objective evidence that the idea is working. Companies are typically generating revenue, small teams have grown and become more sophisticated in how they operate, and importantly, the governance functions of a company have (hopefully) begun to take shape. The simple existence of a board member with invested capital at stake means that some of the more existential risks of the earliest stage have been mitigated.

In contrast, one of the big milestones for any startup has been to raise a Series A from an institutional investor. Besides an infusion of capital (which is often 2-3x the aggregate capital a company may have raised since its inception), this “stamp of approval” lends credibility to a small company that is trying to hire talent, sell to customers, and, in most cases, raise substantial subsequent capital.

Thus, it’s critical that Series A investors remain active; if not, many of these upstart companies may fail due to a lack of investment, even if they are able to demonstrate early market traction. The Series A funding market is one of — if not the most — critical funding stage in the innovation economy because it acts as a bridge between scrappy early innovation and commercialization at scale.

It stands to reason, then, that dollar amounts invested may not be the best barometer of the ecosystem’s health. What really matters is the volume of companies being funded and the variety of product approaches being pursued.

Once the initial shock of the pandemic wore off, the VC community had to get back to business, which admittedly is harder to do for funds that write $10 million+ checks and like getting to know founders in person. Still, Series A investors made it a point to let entrepreneurs know they were, and continue to be, “open for business.”

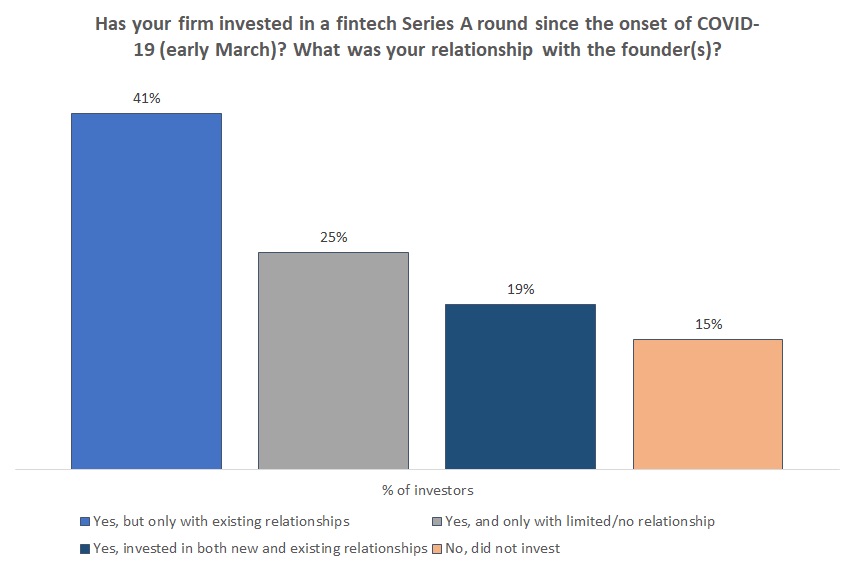

As investors have gotten more comfortable with the new normal, they have been more open to a virtual diligence process. Of the firms we surveyed, only 15% stated they have not completed a Series A investment during COVID-19 work restrictions. Of the firms who completed a Series A investment during COVID-19 (~85%), about half invested in a company whose founder(s) they had a limited or no relationship with prior to the onset of shelter-in-place orders.

Image Credits: Financial Venture Studio (opens in a new window)

The shift to a virtual environment means that process is more important than ever. Numerous investors have cited their renewed focus on following a structured approach to sourcing and diligence. The interpersonal aspect remains important to close a deal, but customer references, referrals from trusted seed-stage investors and a heightened scrutiny of metrics are all at the forefront of investors’ evaluations.

Powered by WPeMatico

Figma for filmmakers, TikTok for English learners and a cryptocurrency twist that actually makes sense?

After 197 pitches, Y Combinator’s Demo Day for its Summer 2020 cohort has concluded. While the fanfare, run-ins and fortune cookies were missing in this virtual session, it was still exciting to see and hear founders from 26 countries pitch their passions. Of course, some opted for a more quiet route, raising millions before the two-day pitch session even kicked off.

Members of the Summer 2020 class drew attention from nearly 2,400 investors across the world. For those who didn’t tune in, no worries: here’s our write-up of the companies that presented yesterday.

Participating startups spanned a number of sectors: we saw companies in the future of work, sustainability, no-code, consumer, edtech and delivery solutions. Several entrepreneurs aimed big at e-mail, small at socks and straight at Shopify’s recent success.

While TechCrunch reporters aren’t in the business of cutting checks or predicting success, read on to learn about the 12 startups that stuck out to us for a variety of reasons (apart from their Zoom backgrounds).

CarbonChain may be the company that times the carbon market correctly. Now that the European Union and other regions are taking a serious look at penalizing businesses that fail to reduce carbon emissions, a service that provides accurate accounting for a company’s carbon footprint will be increasingly valuable.

And if the company can add marketplace and offsetting services on the back of its assessments, then its proposition becomes even more valuable. But what really makes CarbonChain stand out is the rigor with which it approaches its measurements.

The company uses independent software tools to make a digital twin of the carbon-emitting assets in a company’s business and claims that it can determine the emissions footprint of operations down to a cup of coffee (it also has models for the carbon footprint of heavy industrial equipment in the world’s most polluting industries).

For the world to address its carbon emissions, companies must understand their contribution to the problem. CarbonChain could be an invaluable tool in that effort.

Powered by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico