financial technology

Auto Added by WPeMatico

Auto Added by WPeMatico

Funding for Black entrepreneurs in the U.S. hit nearly $1.8 billion in the first half of 2021 — a fourfold increase from the previous year. But most venture-backed startups are “still overwhelmingly white, male, Ivy-League-educated and based in Silicon Valley,” according to a study conducted by RateMyInvestor and Diversity VC.

With venture investors committing to funding Black and minority founders, alongside the growing availability of government-backed proposals, such as New Jersey allocating $10 million to a seed fund for Black and Latinx startups, can we expect to see fundamental change? Or will we have to repeat the same conversations about representation failings within VC funds?

Crunchbase examined the access to capital in the venture-backed startup ecosystem and proved that many industry leaders still worry that nothing will drastically shift. As a Black fintech founder, I believe that venture investors are making safe bets and investing in late-stage founders instead of early or even pre-seed stages.

But what about those minority founders who don’t have family, friends or connections to lean on for the first $250,000? Venture funding does remain elusive, but here are some tricks for startup founders to hack the system.

Getting your foot in the door with new venture capitalist partners is challenging, and it is often easy for minority founders to be naive at first. I thought that reading TechCrunch and analyzing other VC deals I saw in the news would help me land multiple responses and speak the language of those who managed to score million-dollar deals for their startups. However, I didn’t receive a single response while other founders received VC investment for basic ideas.

This is something I had to learn the hard way: What you hear in the media or read on a company blog post often simplifies the process, and sometimes fails to cover the trajectory that minority founders, in particular, must follow to secure funding.

I experienced hundreds of rejections before raising $2 million to start a mobile payment platform, Bleu, using beacon technology to drive simple and secure payments. It is a huge mountain to climb and a full-time job to continuously pitch your vision and yourself to reach the first meeting with a VC fund — and that’s still miles away from a funding discussion.

These discussions then bring further biases to the surface. If you sat in the conference rooms or on those Zoom calls and heard the types of deals proposed to minority founders, you’d see how offensive they can be. Often, these founders are offered all the money they have requested — but don’t be fooled. It is usually not given all at once due to what I consider to be a lack of trust. Essentially, interval funding equates to being babysat.

Therefore, as a minority founder, you have to realize that it will be a long ride, and you will face rejections because you are at a disadvantage before even opening your mouth to pitch your idea. It is all possible, but patience is key.

Once I figured out how complicated the funding process was, my coping mechanism was to figure out how to capitalize on the business ideas I already had in place in case I never received any VC funding.

Think: How could you make money without an institutional investor, friends, family or internal networks? You’ll be surprised by your entrepreneurial thirst for success when you’ve experienced 100 rejections. This is why minority businesses caught in these testing situations can quickly gain the upper hand, whether through ancillary and side businesses or crowdfunding over GoFundMe and Kickstarter.

Although generally considered non-essential, ancillary companies do provide a regular flow of income and services to assist your core business idea. Most importantly, a recurring revenue stream outside your core business demonstrates to investors that you can create valuable products and acquire loyal customers.

Make sure to find a niche market and carry out surveys with potential clients to find out what specific needs they have. Then, build a product with their feedback in mind and launch it to beta clients. When you publicly release the product, find resellers to keep internal headcount low and generate recurring revenue.

Don’t take ancillaries lightly, though; they are not just a side business. There can be payment issues if you get hooked on them for revenue, distractions from clients or partners wanting custom requests, and supply chain problems.

In my case, I built a point-of-sale (POS) software platform to sell to merchants, which gave me a different revenue stream that could integrate with Bleu’s payment technology. These ancillary businesses can help fund your core business until you manage to plan how to launch fully or source further funding.

In 2019, The New York Times published an article headlined “More Start-Ups Have an Unfamiliar Message for Venture Capitalists: Get Lost.” It highlights how more and more entrepreneurs shunned by the VC funding route are turning to alternatives and forming counter-movements. There are always alternatives to look at if the fundraising process is proving to be too arduous.

Accelerators allow ventures to define their products or services, quickly build networks and, most importantly, sit at tables they wouldn’t be able to on their own. Applying to accelerators as a minority founder was the real turning point for me because I met a crucial investor who allowed us to build credibility and open up to new networks, investors and clients.

I would suggest looking out for accelerators explicitly searching for minority founders by using platforms such as F6S. They match you with accelerators and early growth programs committed to innovation in various global industries, like financial technology. That’s how I found the VC FinTech Accelerator in 2016, where one-third of founders were from minority backgrounds.

Then, Bleu earned a spot in the 2020 class of the IBM Hyper Protect Accelerator dedicated to supporting innovative startups in fintech and health tech industries. These types of accelerators offer startups workshops, technical and business mentorship, and access to a network of partners, customers and stakeholders.

You can impress accelerators by creating a pitch deck and a company video less than two minutes long that shows your founder and the product, and engaging with the fintech community to spread the news.

The other alternative to accelerators is government funds, but they have had little success investing in startups for myriad reasons. It tends to be a more hands-off approach as government funds are not under significant pressure from limited partners (LPs, either institutional or individual investors) to perform.

What you need as a minority founder is an investor who is an active partner but, with government-backed funds, there is less demand to return the capital. We have to ask ourselves whether governments are really searching for the best minority-owned startups to help them get sufficient returns.

There are many unconscious social stigmas, stereotypes and unseen biases that exist in the U.S. And you’ll find those cultural dynamics are radically different in other countries that don’t have the same history of discrimination, especially when looking at a team or assessing founders.

I also noticed that, as well as reduced bias, investors out of Southeast Asia, Nordic countries and Australia seemed far more likely to take risks on new contactless payment technology as cash use decreased across their regions. Take Klarna and Afterpay as examples of fintech success stories.

First, I engaged in market research and pored over annual reports to decide whether I should look abroad for funding, instead of applying to funds closer to home. I looked at Nielsen reports, payment publications, PaymentSource and numerous government documents or white papers to figure out the cash usage globally.

My investigations revealed that fintech in Australia was far ahead of the curve, with four-fifths of the population using contactless payments. The financial services sector is also the largest contributor to the national economy, contributing around $140 billion to GDP a year. Therefore, I spoke to the Australian Department of Foreign Affairs and Trade in the U.S., and they recommended some regulatory payment groups.

I immediately flew to Australia to meet with the banking community, and I was able to find an Australian investor by word of mouth who was surrounded by the demand for mobile payment solutions.

In contrast, an investor in the U.S. still using cash and card had no interest in what I had to say. This highlights the importance of market research and seeking out investors rather than waiting for them to come to you. There is no science to it; leverage your network and reach out to people over LinkedIn, too.

VC funding needs to become more inclusive for women and minority groups by tackling the pipeline problem and addressing the level of diversity within VC funds. All of the networks that VCs reach out to first tend to come from university programs at Stanford, MIT and Harvard. These more privileged and wealthy students are able to easily leverage the traditional and outdated networks built to benefit them.

The number of venture dollars flowing to Black and Latinx founders is dismally low partly due to this knowledge gap; many female and minority founders don’t even know that VC funding is an option for them. Therefore, if you do receive seed funding, spread the news about it within your networks to help others.

Inclusion starts at the educational level but, when the percentage of Black and minority students at these elite colleges are still low, you can see why minority representation is needed in the VC ranks. Even if representation rises by a percent, that would be a significant change.

There are increasing numbers of VC funds announcing initiatives and interest in investing in minority businesses, and I would recommend looking at these in-depth. But what about the demographics of the VC firms? How many ethnicities are present in the executive ranks?

To change the venture-backed startup ecosystem, we need to start at the top and diversify those signing the checks. Looking toward the future, it is Black-led funds, like Sequoia, or others that focus on diversity, like Women’s Venture Fund, BackStage Capital and Elevate Capital Inclusive Fund, that are lighting the way to solutions that will reflect the diversity of the U.S.

It’s up to the investor community at large to be intentional about building relationships with, and ultimately providing funding to, more women and minority-led startups.

Despite the barriers and hurdles minority founders face when searching for VC funding, more and more avenues for acquiring funding are appearing as the disparities are brought to the media’s attention.

As the outdated system adjusts, the key is to continue preparing yourself for rejections and searching for appropriate accelerators to build vital networks. Then, if you aren’t having any luck, consider what you could do with your business idea without the VC funding or turn to foreign markets, which may have a different setup and varied opportunities.

Powered by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

Oh, how the tables have turned.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

But lately, fintech upstarts are the ones doing the acquiring. Over just the last year or so, we’ve seen:

So what’s going on here? Why are fintechs now acquiring legacy financial services businesses, instead of the other way around?

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

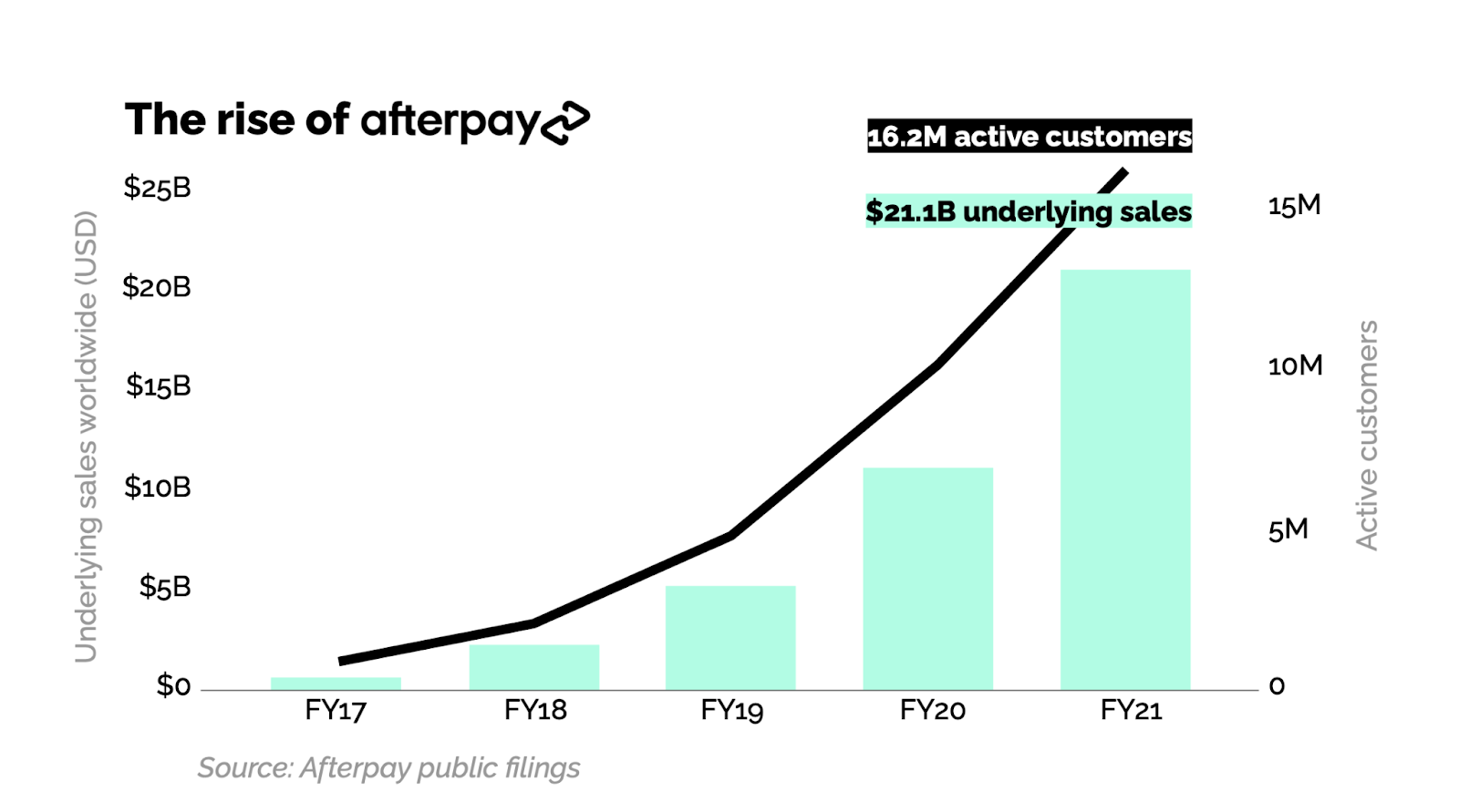

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

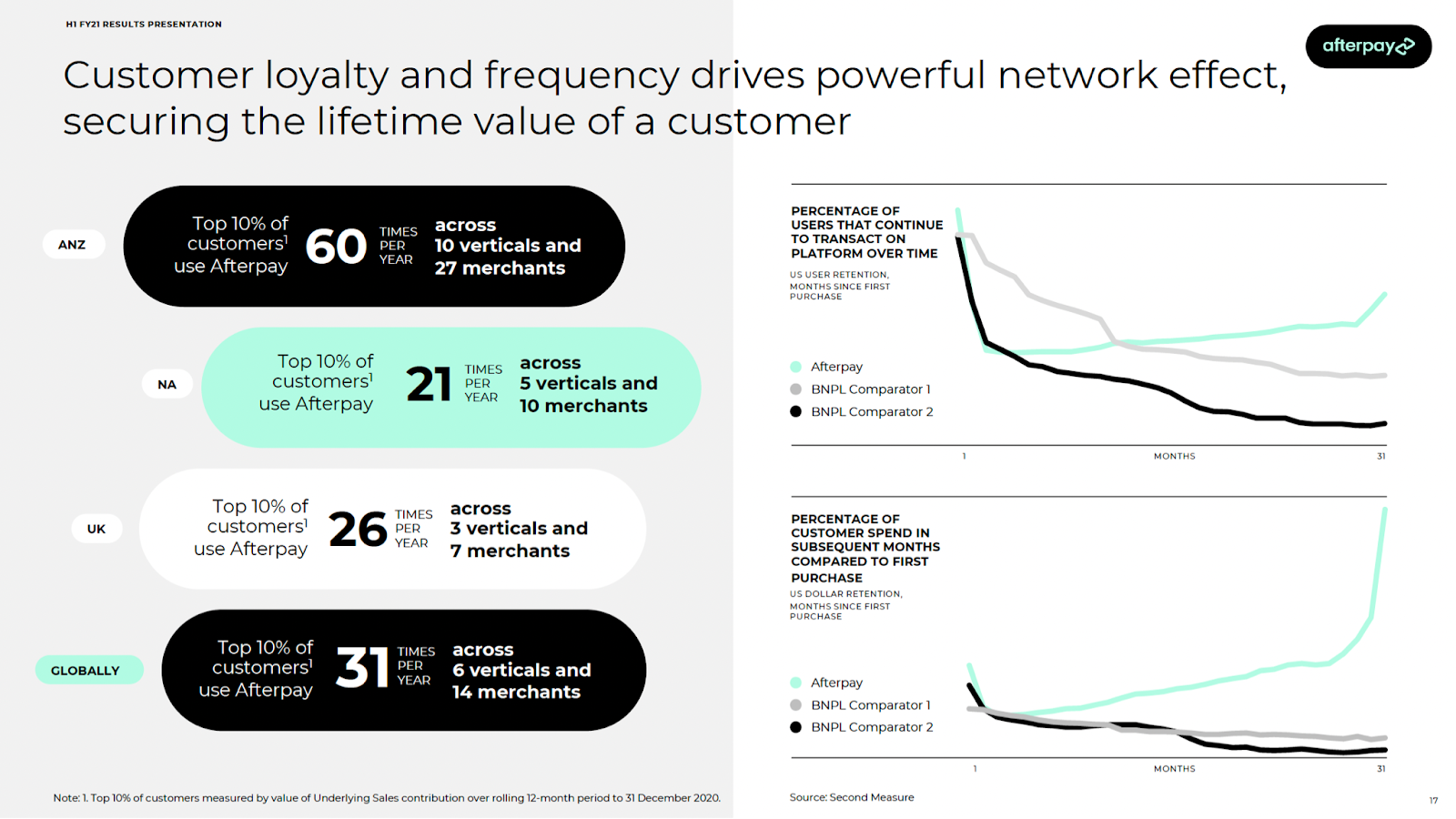

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Sila announced Monday it raised $13 million in Series A funding for its banking and payment platform that gives software teams tools to build the next generation of financial products and services.

Revolution Ventures led the round and was joined by existing investors Madrona Venture Group, Oregon Venture Fund and Mucker Capital, as well as Wise co-founder Taavet Hinrikus. The funding brings the total investment to date for Portland, Oregon-based Sila to $20 million.

The company was founded in 2018 by Shamir Karkal, Angela Angelovska, Isaac Hines and Alex Lipton to simplify digital payments and storage in a regulatory compliant way and build on blockchain technology. CEO Karkal has a long history in the fintech space, co-founding Simple, an app unifying various accounts into one accessible bank card, in 2009. It was acquired by BBVA in 2014 for $117 million and shuttered earlier this year.

Karkal told TechCrunch that the idea for Sila was born out of frustration while starting another bank. He saw a need for financial application development, but was hindered by a banking system “still stuck in the 20th century.” He thought consumers expected a different level of service, which is why many flock to fintechs.

However, whenever a business tried to connect existing banking systems, fintechs and cryptocurrency innovators, as it built and scale, would always run into technology and compliance issues, Karkal said.

“The problem with working with banks, is that you have to figure out how to integrate with their mainframe,” he added. “In the process, you end up having to also be compliance experts just to be able to do it.”

Whereas it took Karkal three years to get bank processes set up for other companies, it took Sila 18 months. Its banking APIs enable developers to create their own digital wallets, replacing the need to integrate with legacy financial institutions. Sila also has partnerships with fintech platforms, including Plaid, Alloy, Lithic and Arcus to move money, and is backed by Evolve Bank and Trust.

Sila can now get customers up-and-running in six to eight weeks. And unlike competitors that focus almost exclusively on e-commerce, most of Sila’s customers are doing regulated payments within the fintech, insurtech, commercial real estate and cryptocurrency spaces that tend to be more complex from a compliance basis, Karkal said.

Since the company launched its platform, business was building steadily, and took off in the second half of 2020. The company raised a $7.7 million seed round earlier in the year. In the last 12 months, Sila grew its revenue 10 times and customers’ end users grew over 500% in the last seven months.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network.

“There is a massive wave of fintechs emerging in the U.S., and we have barely scratched the surface,” Karkal said. “Places like India, Africa and Latin America could accelerate at the same time because they are mainly starting from zero. We are here to ‘arm the rebels’ and help those innovators build applications to give all end users a much better financial experience.”

As part of the investment, Clara Sieg, partner at Revolution Ventures, is joining the company’s board. She told TechCrunch she met the company’s co-founders through the Portland ecosystem.

Revolution tends to look at fintech startups from a consumer angle. Recognizing that the problem with building infrastructure meant dealing with banks, the firm set out how to find a company building the pipes to solve it, she said.

In the landscape of fintech, she considers Dwolla to be a competitor to Sila. Last week, the company raised $21 million to continue developing its API that allows companies to build and facilitate fast payments, specifically with a focus on ACH. However, it comes down to actually signing up customers, and that competitive landscape is pretty thin, Sieg added.

“Sila is building an easy way for people to program money and taking a regulatory eye to things,” Sieg said. “When Shamir was building Simple, he could see how challenging it was for incumbents to provide the tools developers need to embed financial services, and this is why we have confidence in his ability to win.”

Powered by WPeMatico

Not every startup wants to raise venture capital. And then there are those that do want to raise VC money but don’t want to use it for specific things.

In recent years, a number of firms have emerged looking to meet the credit needs of such venture-backed and growth startups: i80 Group is one of those firms.

Former Goldman Sachs investment banker Marc Helwani founded i80 in 2016 after investing in early-stage New York-based fintechs in 2014-2015 via his VC fund, Avenue A Ventures.

“It became very clear to me that fintech was going to explode,” he recalls. “At that time, it was still relatively new. And every time I spoke to a company, they would tell me, ‘We know how to raise VC, but what about the credit?’ I just saw this white space.”

For example, proptechs that buy homes on behalf of buyers don’t want to use venture money. Fintechs that want to make loans to consumers don’t want to use equity to do it. Instead, in those cases, credit might be more desirable.

Enter i80. The firm offers credit exclusively, and over the years has quietly committed more than $1 billion to over 15 companies –including real estate marketplace Properly, finance app MoneyLion and SaaS financing company Capchase — that have all raised a significant amount of venture capital but are looking for credit “to help them scale very efficiently and in a non-dilutive manner so they can retain more ownership of their companies,” Helwani said.

Its $1 billion milestone follows fund commitments nearing $500 million from an unnamed “leading global asset manager” as well as other institutional and retail investors.

Image Credits: Founder and Chief Investment Officer Marc Helwani / i80 Group

I80 — which derives its name from the highway that connects New York and San Francisco — is mainly focused on the fintech and proptech sectors.

“They are the two centers for the venture ecosystem,” Helwani said. “And we’re trying to be a bridge between those two cities.” I80 has offices in both locations and will soon be opening one in Montreal.

The firm works in conjunction with VC firms such as a16z (more formally known as Andreessen Horowitz); Affirm and PayPal co-founder Max Levchin’s SciFi; Khosla Ventures; Union Square Ventures; and QED.

“In a perfect world, venture capital would be called venture equity,” Helwani said. “VCs’ capital is critical for companies to hire and get office space. But when it comes time to do what the actual business is, such as provide loans or buy homes, capital like ours is very accretive without VCs and management losing ownership in the business. In these cases, using both credit and equity makes a lot of sense.”

Helwani is reluctant to call what i80 offers venture “debt.” He says that has a very specific connotation and is what Silicon Valley Bank and others like it do in providing debt as a percentage of a previous equity round. Instead, according to Helwani, i80’s approach is to minimize fees. The vast majority of its deals are “interest-rate related.”

“With mortgages, for example, we never think about the fees upfront, and focus more on the interest rate,” Helwan said. “We believe the more transparent we are, the more companies will want to work with us.”

I80 conducts quarterly calls with VCs and for now, that’s how it typically sources most of its deal flow. It also gets referrals. Helwani believes that i80 stands out from other firms also offering credit in that it’s “not trying to be credit investors in VC clothing.”

He also thinks that the fact that the i80 team is made of operators, as well as investors, is a contributing factor.

The firm is set to close another half a dozen deals in the next 60 to 90 days, and then plans to set its sights on raising more capital.

“We want to fill this void, and help companies raise money in their subsequent rounds at higher valuations,” Helwani said.

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Even as NFT sales dip below their most speculative highs, startups aiming to tap into their potential are still scoring big funding rounds from investors who believe there’s much more to crypto collectibles than the past few months of hype.

Mythical Games, an NFT games startup based out of Los Angeles, has banked a $75 million raise from new and existing investors betting on the startup’s aim to expand the ambitions of their first title and locate a substantial platform opportunity amid helping developers build blockchain-based gaming experiences.

The round was led by WestCap. Existing investors were joined by 01 Advisors and Gary Vaynerchuk’s VaynerFund in the Series B funding. The startup has raised a whopping $120 million to date.

The company has been building a title called Blankos Block Party that seems to be Fall Guys meets Roblox meets Funko Pop. The PC game capitalizes on a number of big social gaming trends around user-created content, while adding in a marketplace where users can buy avatar figures and accessories crafted by a variety of artists and designers that Mythical has partnered with. Users can buy or sell the limited run or open edition items through their marketplace. Unlike some other NFT platforms, the goods live on a private blockchain so they can’t be re-sold on public marketplace platforms like OpenSea.

Mythical Games is part of a growing movement to bring blockchain-based game mechanics mainstream while leaving behind elements of crypto platforms that are seen as less ready for primetime. Users can purchase avatars on the platform with cryptocurrency through BitPay but they can also pay with a credit card. Users don’t need to walk through the mechanics of setting up a wallet or writing down a seed phrase either.

While the company has big hopes for Blankos as it onboards more users, the bigger investor opportunity is likely in the game engine that the team is building. The startup’s “Mythical Economic Engine” is being designed to help budding game builders create NFT-based marketplaces that won’t get them in any regulatory trouble, marrying compliance across geographies and tools that help creators comply with anti-money laundering laws and know-your-customer frameworks.

“With any new market like [NFTs], it goes through all these different cycles,” Mythical Games CEO John Linden tells TechCrunch. “We think this will actually change gaming for the long haul. The more we talk to game studios, we’re finding more and more potential use cases.”

Powered by WPeMatico