Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Business, now more than ever before, is going digital, and today a startup that’s building a vertically integrated solution to meet business banking needs is announcing a big round of funding to tap into the opportunity. Airwallex — which provides business banking services directly to businesses themselves as well as via a set of APIs that power other companies’ fintech products — has raised $200 million, a Series E round of funding that values the Australian startup at $4 billion.

Lone Pine Capital is leading the round, with new backers G Squared and Vetamer Capital Management, and previous backers 1835i Ventures (formerly ANZi), DST Global, Salesforce Ventures and Sequoia Capital China also participating.

The funding brings the total raised by Airwallex — which has head offices in Hong Kong and Melbourne, Australia — to $700 million, including a $100 million injection that closed out its Series D just six months ago.

Airwallex will be using the funding both to continue investing in its product and technology as well as to continue its geographical expansion and to focus on some larger business targets. The company has started to make some headway into Europe and the U.K. and that will be one big focus, along with the U.S.

The quick succession of funding and rising valuation underscore Airwallex’s traction to date around what CEO and co-founder Jack Zhang describes as a vertically integrated strategy.

That involves two parts. First, Airwallex has built all the infrastructure for the business banking services that it provides directly to businesses with a focus on small and medium enterprise customers. Second, it has packaged up that infrastructure into a set of APIs that a variety of other companies use to provide financial services directly to their customers without needing to build those services themselves — the so-called “embedded finance” approach.

“We want to own the whole ecosystem,” Zhang said to me. “We want to be like the Apple of business finance.”

That seems to be working out so far for Airwallex. Revenues were up almost 150% for the first half of 2021 compared to a year before, with the company processing more than US$20 billion for a global client portfolio that has quadrupled in size. In addition to tens of thousands of SMEs, it also, via APIs, powers financial services for other companies like GOAT, Papaya Global and Stake.

Airwallex got its start like many of the strongest startups do: It was built to solve a problem that the founders encountered themselves. In the case of Airwallex, Zhang tells me he had actually been working on a previous startup idea. He wanted to build the “Blue Bottle Coffee” of Asia Pacific out of Australia, and it involved buying and importing a lot of different materials, packaging and, of course, coffee from all around the world.

“We found that making payments as a small business was slow and expensive,” he said, since it involved banks in different countries and different banking systems, manual efforts to transfer money between them and many days to clear the payments. “But that was also my background — payments and trading — and so I decided that it was a much more fascinating problem for me to work on and resolve.”

Eventually one of his co-founders in the coffee effort came along, with the four co-founders of Airwallex ultimately including Zhang, along with Xijing Dai, Lucy Liu and Max Li.

It was 2014, and Airwallex got attention from VCs early on in part for being in the right place at the right time. A wave of startups building financial services for SMBs were definitely gaining ground in North America and Europe, filling a long-neglected hole in the technology universe, but there was almost nothing of the sort in the Asia Pacific region, and in those earlier days solutions were highly regionalized.

From there it was a no-brainer that starting with cross-border payments, the first thing Airwallex tackled, would soon grow into a wider suite of banking services involving payments and other cross-border banking services.

“In the last six years, we’ve built more than 50 bank integrations and now offer payments across 95 countries, payments through a partner network,” he added, with 43 of those offering real-time transactions. From that, it moved on to bank accounts and “other primitive stuff” with card issuance and more, he said, eventually building an end-to-end payment stack.

Airwallex has tens of thousands of customers using its financial services directly, and they make up about 40% of its revenues today. The rest is the interesting turn the company decided to take to expand its business.

Airwallex had built all of its technology from the ground up itself, and it found that — given the wave of new companies looking for more ways to engage customers and become their one-stop shop — there was an opportunity to package that tech up in a set of APIs and sell that on to a different set of customers, those who also provided services for small businesses. That part of the business now accounts for 60% of Airwallex’s business, Zhang said, and is growing faster in terms of revenues. (The SMB business is growing faster in terms of customers, he said.)

A lot of embedded finance startups that base their business around building tech to power other businesses tend to stay at arm’s length from offering financial services directly to consumers. The explanation I have heard is that they do not wish to compete against their customers. Zhang said that Airwallex takes a different approach, by being selective about the customers they partner with, so that the financial services they offer would not be in direct competition with those of its customers. The GOAT marketplace for sneakers, or Papaya Global’s HR platform are classic examples of this.

However, as Airwallex continues to grow, you can’t help but wonder whether one of those partners might like to gobble up all of Airwallex and take on some of that service provision role itself. In that context, it’s very interesting to see Salesforce Ventures returning to invest even more in the company in this round, given how widely the company has expanded from its early roots in software for salespeople into a massive platform providing a huge range of cloud services to help people run their businesses.

For now, it’s been the combination of its unique roots in Asia Pacific, plus its vertical approach of building its tech from the ground up, plus its retail acumen that has impressed investors and may well see Airwallex stay independent and grow for some time to come.

“Airwallex has a clear competitive advantage in the digital payments market,” said David Craver, MD at Lone Pine Capital, in a statement. “Its unique Asia-Pacific roots, coupled with its innovative infrastructure, products and services, speak volumes about the business’ global growth opportunities and its impressive expansion in the competitive payment providers space. We are excited to invest in Airwallex at this dynamic time, and look forward to helping drive the company’s expansion and success worldwide.”

Updated to note that the coffee business was in Australia, not Hong Kong.

Powered by WPeMatico

Major gains in online advertising have boosted valuations for adtech startups since the pandemic began, but one insider says investors are missing the party.

“Adtech is having a moment,” writes industry veteran Casey Saran.

“And while much of the oxygen has been soaked up by large legacy companies hitting the public market, there have been smaller deals that indicate a hunger for better creative adtech.”

Saran shares five reasons “why VCs should consider ratcheting up their investment into adtech startups building the next generation of creative tools.”

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

On Wednesday, September 22 at 9:05 a.m PT, I’m moderating “The Path for Underrepresented Entrepreneurs,” a panel discussion at Disrupt 2021.

Our conversation will examine some of the unique challenges facing founders from historically marginalized groups, the strategies they used along the way, and the disruptive changes we need to consider if we want to see fundamental change.

I’ll be speaking with:

I hope you’ll attend; we’ll take audience questions after our discussion concludes. Thanks very much for reading Extra Crunch this week, and have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: AndrewLilley (opens in a new window) / Getty Images

Congratulations on shipping your product, but how much do you know about your target customers?

Companies that haven’t created an ideal customer profile and performed a SWOT analysis are making big bets on guesswork and intuition. Sometimes that works out, but more frequently, it leads to tears.

In a guest post that walks readers through the fundamentals of creating customer personas that map to your company’s goals, Grammarly product marketing lead Bryan Dsouza shares five basic requirements for customer acquisition.

“Understanding and executing on these things can guarantee you that first customer win, provided you do them well and with sincerity,” he says.

“Your investors will also see the fruits of your labor and be comforted knowing their dollars are at good work.”

Image Credits: joshblake (opens in a new window) / Getty Images

In school, it’s highly unethical to copy someone else’s work and pass it off as your own. In business, however, it is expected.

Xiaoyun TU, global director of demand generation at Brightpearl, wrote a comprehensive guide for how to use the key metric of return on advertising spend (ROAS) to triple your company’s lead generation.

“A ‘good’ ROAS score is different for each company and campaign,” she says. “If your figure isn’t where you’d like it to be, you can leverage ROAS data to create targeted campaigns and personalized experiences.”

Image Credits: porcorex (opens in a new window) / Getty Images

Most of us prefer to trust our instincts instead of letting automated tools help us make decisions, particularly when it comes to hiring. But that’s not smart.

If your startup relies on an ad hoc hiring process, you’re probably not tracking candidates properly, there’s likely little consistency regarding how they’re treated, and bias can play a major role in who gets hired.

It’s fine to be skeptical of automated hiring tools — but not ignorant.

Image Credits: Nigel Sussman (opens in a new window)

In yesterday’s edition of The Exchange, Anna Heim and Alex Wilhelm speculated about the conditions that could combine to cool off a hot startup market currently fueled by low interest rates and a sweeping digital transformation.

“From where we stand, the factors underpinning the startup fundraising boom appear solid and unlikely to unwind overnight. Still, no golden period shines forever, and even today’s luster will eventually tarnish.”

Image Credits: Smith Collection/Gado / Getty Images

Before news broke this week that Intuit was acquiring Mailchimp for $12 billion, the ’80s-born fintech giant’s biggest buy was spending $7.1 billion last year for Credit Karma.

In the last few years, Mailchimp “has been expanding upon its core email marketing functionality” with offerings like web design and CRM, writes enterprise reporter Ron Miller.

The industry watchers he interviewed said the move signals Intuit’s interest in acquiring and serving more SMB customers with a variety of tools:

Image Credits: Nigel Sussman (opens in a new window)

“One of my favorite long-term issues with the late-stage startup market is that it is far better at creating value than it is at finding an exit point for that accreted value,” Alex Wilhelm writes for The Exchange. “More simply, the startup market is excellent at creating unicorns but somewhat poor at taking them public.”

That’s good news for Forge Global, a technology startup that operates a market for secondary transactions in private companies, with Alex dubbing its plans to go public via a SPAC combination “perfectly reasonable.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

At Burning Man a few years ago, I was arrested and charged with a misdemeanor for smoking marijuana in public (in my car) and driving under the influence.

I currently have a green card and want to apply for U.S. citizenship next year.

Can I? If so, how should I handle my criminal record?

— Remorseful About the Reefer

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm and Anna Heim continued their tour of U.S. cities after hitting up Chicago and Boston in recent weeks.

This time, they dug into Atlanta’s booming startup scene, which is seeing record capital inflows.

“The picture that forms is one of a city enjoying a rising tide of venture activity, boosted by some local dynamics that may have helped some of its earlier-stage companies scale for cheaper than they might have in other markets,” they write.

Powered by WPeMatico

Cross-border commerce company Zonos raised $69 million in a Series A, led by Silversmith Capital Partners, to continue building its APIs that auto classify goods and calculate an accurate total landed cost on international transactions.

St. George, Utah-based Zonos is classifying the round as a minority investment that also included individual investors Eric Rea, CEO of Podium, and Aaron Skonnard, co-founder and CEO of Pluralsight. The Series A is the first outside capital Zonos has raised since it was founded in 2009, Clint Reid, founder and CEO, told TechCrunch.

As Reid explained it, “total landed cost” refers to the duties, taxes, import and shipping fees someone from another country might pay when purchasing items from the U.S. However, it is often difficult for businesses to figure out the exact cost of those fees.

Global cross-border e-commerce was estimated to be over $400 billion in 2018, but is growing at twice the rate of domestic e-commerce. This is where Zonos comes in: The company’s APIs, apps and plugins simplify cross-border sales by providing an accurate final price a consumer pays for an item on an international purchase. Businesses can choose which one or multiple shipping carriers they want to work with and even enable customers to choose at the time of purchase.

“Businesses can’t know all of a country’s laws,” Reid added. “Our mission is to create trust in global trade. If you are transparent, you bring trust. This was traditionally thought to be a shipping problem, but it is really a technology problem.”

As part of the investment Todd MacLean, managing partner at Silversmith Capital Partners, joined the Zonos board of directors. One of the things that attracted MacLean to the company was that Reid was building a company outside of Silicon Valley and disrupting global trade far from any port.

He says while looking into international commerce, he found people wound up being charged additional fees after they have already purchased the item, leading to bad customer experiences, especially when a merchant is trying to build brand loyalty.

Even if someone chooses not to purchase the item due to the fees being too high, MacLean believes the purchasing experience will be different because the pricing and shipping information was provided up front.

“Our diligence said Zonos is the only player to take the data that exists out there and make sense of it,” MacLean said. “Customers love it — we got the most impressive customer references because this demand is already out there, and they are seeing more revenue and their customers have more loyalty because it just works.”

In fact, it is common for companies to see 25% to 30% year over year increase in sales, Reid added. He went on to say that due to fees associated with shipping, it doesn’t always mean an increase in revenue for companies. There may be a small decrease, but a longer lifetime value with customers.

Going after venture capital at this time was important to Reid, who saw global trade becoming more complex as countries added new tax laws and stopped using other trade regulations. However, it was not just about getting the funding, but finding the right partner that recognizes that this problem won’t be solved in the next five years, but will need to be in it for the long haul, which Reid said he saw in Silversmith.

The new investment provides fuel for Zonos to grow in product development and go-to-market while also expanding its worldwide team into Europe and Asia Pacific. Eighteen months ago, the company had 30 employees, and now there are over 100. It also has more than 1,500 customers around the world and provides them with millions of landed cost quotes every day.

“Right now, we are the leader for APIs in cross-border e-commerce, but we need to also be the technology leader regardless of the industry,” Reid added. “We can’t just accept that we are good enough, we need to be better at doing this. We are looking at expanding into additional markets because it is more than just servicing U.S. companies, but need to be where our customers are.”

Powered by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

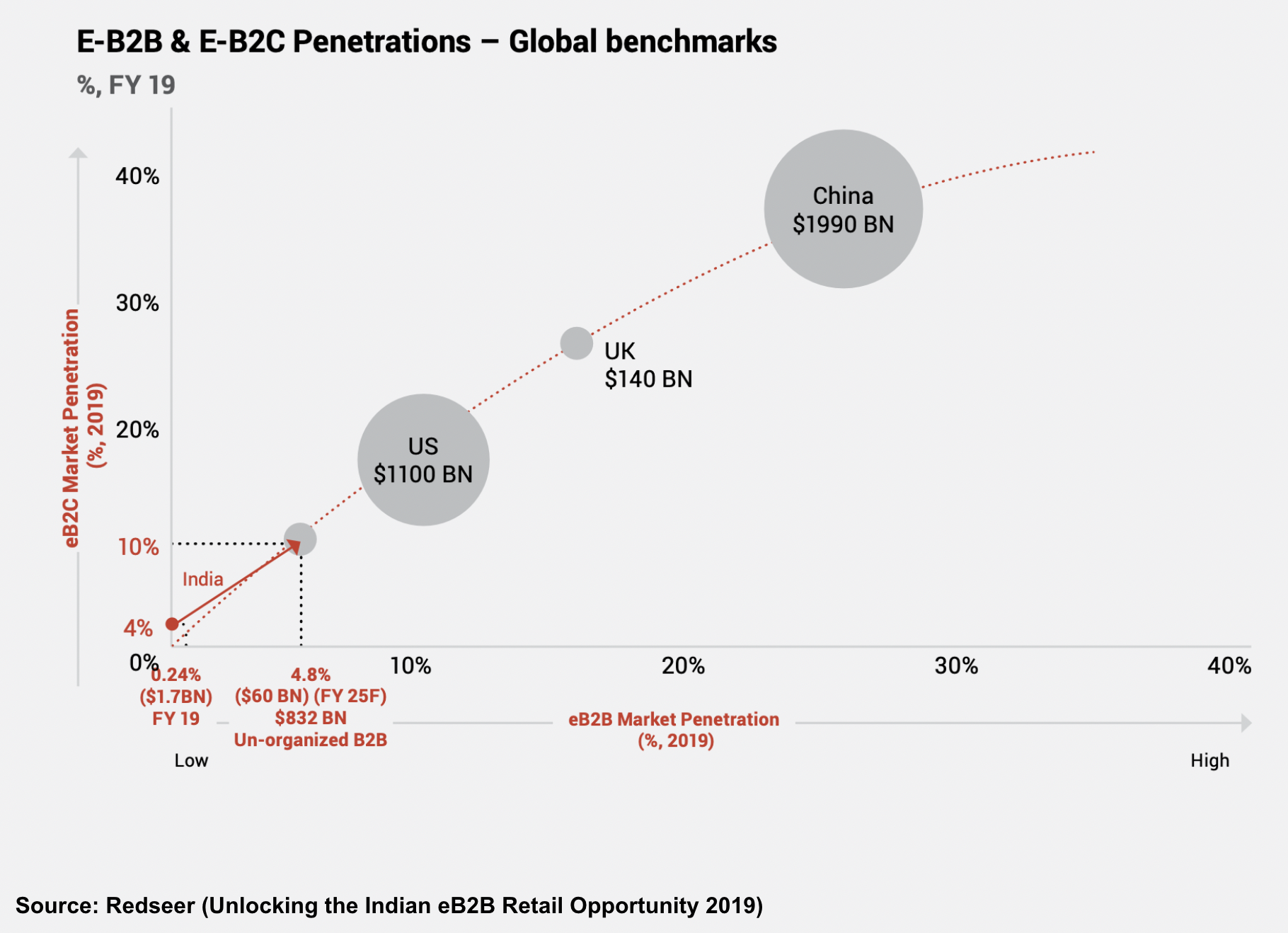

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

China’s first data privacy laws go into effect on November 1, 2021. Will your company be in compliance?

Modeled after the EU’s GDPR, the new regulations “[introduce] perhaps the most stringent set of requirements and protections for data privacy in the world,” writes Scott W. Pink, special counsel in O’Melveny’s Data Security & Privacy practice.

In a comprehensive overview, he explains its key requirements and compliance steps for U.S.-based firms that service Chinese consumers.

“American firms doing business in China or with companies inside China will need to immediately start assessing how this new law will impact their activities,” he advises.

Now that the world has embraced remote work, are visas as critical for startup founders who want to succeed in the United States?

On Tuesday, September 14, at 2 p.m PT/5 p.m. ET, Managing Editor Danny Crichton and immigration law attorney Sophie Alcorn will discuss the matter on Twitter Spaces.

Join @DannyCrichton on Tuesday, September, 14 at 2 p.m. PT/5 p.m. ET as he discusses if remote work will make H-1B visas redundant with @Sophie_Alcorn https://t.co/SCMUiqUj8J

— TechCrunch (@TechCrunch) September 10, 2021

They’ll take questions from the audience, so mark your calendar and follow @techcrunch on Twitter to get a reminder before the chat.

Thanks very much for reading Extra Crunch; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: hauged (opens in a new window) / Getty Images

Whether or not he actually said it, “buy land, they ain’t making any more of it,” is one of Mark Twain’s best quotes on capitalism.

Past recessions and the ongoing pandemic have created real uncertainty about the future of commercial and residential real estate, but farmland is “historically stable,” says Artem Milinchuk, founder and CEO of FarmTogether.

Image Credits: mikroman6 (opens in a new window) / Getty Images

Online mortgage company Better.com isn’t waiting to complete its SPAC merger before making big moves: Ryan Lawler reported that it purchased Property Partners, a U.K.-based startup that offers fractional property ownership.

It’s the second company Better bought in recent months: In July, it snapped up digital mortgage brokerage Trussle.

“We aren’t so easily categorized,” said Better CEO Vishal Garg, who told Ryan that the company plans to soon expand into traditional financial services like auto loans and insurance.

Said CFO Kevin Ryan, “a lot of people have their niches in the way they’re attacking this, but we feel like we’re on a path to being full stack where everything’s embedded in the same flow.”

Image Credits: JoKMedia (opens in a new window) / Getty Images

If you don’t have a good story to share, it doesn’t matter how big your marketing budget is.

“Paid marketing can be a useful tool in your toolkit to accelerate an already humming flywheel. Just don’t let it be the only one,” suggests Brian Rothenberg, a two-time founder who’s now a partner at Defy.

Drawing from his time as VP of growth for Eventbrite, he shares five critical factors for kick-starting, maintaining and measuring growth over the long term.

Image Credits: Peter Dazeley (opens in a new window) / Getty Images

Many potential founders are well-versed in startup economics — and many are completely green.

When it comes to raising funds, understanding the relative benefits (and limitations) of debt and equity financing is required knowledge, however.

Founders who are less willing to dilute their control may be willing to use debt financing to fund their capital expenditures, “but it doesn’t make sense for everyone,” says six-time entrepreneur David Friend.

Image Credits: Getty Images

Last year, startups based in Southeast Asia raised more than $8.2 billion, a 4x increase from 2015.

In the first half of 2021, regional M&A has increased 83% to a record $124.8 billion.

It’s not just venture capitalists and Big Tech who are beefing up their presence in the region.

“Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion,” writes Amit Anand, a founding partner of Jungle Ventures.

Image Credits: Bryce Durbin / TechCrunch

Natasha Mascarenhas examined the parallels between edtech and the creator economy, both of which boomed amid the pandemic — and blurred amid the rise of cohort-based classes.

“Edtech and the creator economy certainly differ in the problems they try to solve: Finding a VR solution to make online STEM classes more realistic is a different nut to crack than streamlining all of a creator’s different monetization strategies into one platform. Still, the two sectors have found common ground in the past year.”

Image Credits: Liyao Xie (opens in a new window) / Getty Images

Were the shoes, jacket and makeup that looked so good on Instagram (and in your shopping cart) disappointing when you put them on for the first time?

Due to buyer’s remorse, it’s not uncommon for apparel or beauty products to languish in the back of a drawer or end up as gifts, but there are also serious consequences.

“The beauty industry produces over 120 billion units of packaging every year, little of which is recycled. Globally, an estimated 92 million tons of textile waste ends up in landfills,” Sindhya Valloppillil, founder and CEO of Skin Dossier, notes in a guest column.

The answer to bringing sustainability to the industry, she says, is using tech to personalize the retail experience:

Image Credits: Bryce Durbin / TechCrunch

Twenty million people live in Lagos, Nigeria, and each day, 14 million of them use the city’s transit system.

Travelers rely on overcrowded public buses that navigate congested routes: What should be a 30-minute trip is often a three-hour journey, but Treepz CEO and co-founder Onyeka Akumah “has big plans to ameliorate the public transport infrastructure in Africa and beyond,” writes Rebecca Bellan.

“We wanted to give people a better way to commute with predictability, where they can know when the bus will get here, the certainty that they will have a seat in a vehicle, that it’s a decent vehicle and a safe one where you can bring your laptop,” said Akumah.

“Those are the things we said we wanted to change.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

My husband just accepted a job in Silicon Valley. His new employer will be sponsoring him for an E-3 visa.

I would like to continue working after we move to the United States. I understand I can get a work permit with the E-3 visa for spouses.

How soon can I apply for my U.S. work permit?

— Adaptive Aussie

Powered by WPeMatico

Vouch, a provider of business insurance to startups and high-growth companies, announced today it has raised $90 million in new funding.

The $90 million figure was raised across two rounds: a $60 million Series C co-led by SVB Capital (a subsidiary of Silicon Valley Bank) and Ribbit Capital that values the company at $550 million, and a previously unannounced $30 million Series B1 led by Redpoint Ventures.

With the latest financing, San Francisco-based Vouch has now raised a total of $160 million since its 2018 inception. Other investors include Allegis Group, Sound Ventures and SiriusPoint.

While there are many insurance technology companies out there that serve consumers, there are far fewer that offer it to companies, much less startups. Vouch describes itself as “a new kind of insurance platform” for startups that offers fully digital, “tailored coverage that takes minutes to activate.”

Over the past year, Vouch has seen impressive growth. The company declined to reveal hard revenue figures, but said it saw “7x” increase in its customer base year over year and currently protects over $5.7 billion in risk across thousands of policies. Today, Vouch has more than 1,600 clients, including Pipe, Middesk, Neighbor and Routable. It is also the “preferred” business insurance provider to the customers of Silicon Valley Bank, Brex, Carta and WeWork. Y Combinator too also refers Vouch to its portfolio companies.

To Vouch co-founder and CEO Sam Hodges, the ability to attract some of the highest-profile businesses in the startup world speaks to the company’s understanding of the startup ecosystem.

“It’s our responsibility to meet startup founders where they are, and give startups flexibility as they navigate changing laws, regulations and the virtual and physical locations of their businesses,” he said.

Like many other companies, Vouch had to shift its model during the pandemic to adapt to the different types of emerging risks businesses have faced. For example, last year, Vouch saw a change in where its startup clients’ teams were distributed. Before the pandemic, nearly 30% of the teams were remote. During the pandemic, that figure has shifted to over 53%. As a result, Vouch developed a broader range of insurance coverages to adapt to the “new normal.”

Included in its new line of proprietary products and services aimed at startups are: work from anywhere coverage, broader cyber coverages and embedded insurance. It also expanded its underwriting capabilities to serve early-stage to growth-market startups.

In particular, the work from anywhere coverage is in direct response to the pandemic-related shift in remote work and can insure up to $500,000 per occurrence and can include a specified property owned by a startup regardless of the location of that property.

One major differentiator for Vouch, said Hodges, is that it is now the only business insurance provider for startups that has its own insurance carrier, which means the company backs its own policies.

“This capability means we have a lot of control over how we build and underwrite our policies — which translates into superior coverage and a better experience for our clients,” he said.

Hodges co-founded Vouch with Travis Hedge three years ago after seeing how challenging it could be for a company to get the business insurance it needs to start and then scale.

The goal is to make it as easy as possible to onboard new customers and personalize the coverage as much as possible based on each company’s needs based on what they do, their customer base, stage of growth and the founder’s threshold for risk.

“A typical client can get a quote and bind their coverage online in under 10 minutes, without any phone calls or paperwork,” he told TechCrunch. “Vouch also has many coverage features that are uniquely geared for startups. For example, our directors and officers coverage includes a cap table coverage feature meant specifically to protect startups.”

Vouch looks at startups that need business insurance on a case by case basis, Hodges added.

For example, it asks questions like, “Does an e-commerce company handle a very limited amount of client-sensitive information?” If so, it could make sense that it has a lower cyber insurance coverage limit and pay less for its policy.

Conversely, if a startup is trying to raise money, it might need to invest more in Vouch’s directors and officers insurance to make sure it is covered should disputes arise in the future.

Looking ahead, Hodges said the new capital would go toward continued investment in technical capabilities, an expansion of its product offerings, more hiring and building embedded insurance for its partners.

With regard to the embedded capabilities, within the next 12 months, all of the company’s partners’ customers will be able to purchase Vouch insurance directly from those partners’ websites. Vouch’s headcount has more than doubled, from 55 employees in September 2020 to 125 full-time employees presently, and Hodges expects that will continue to grow.

Greg Becker, president and CEO of SVB Financial Group, said that Vouch’s mission aligns with SVB’s in that they both aim to “empower the innovation economy.”

“That’s what Vouch is doing today, helping startups and tech innovators mitigate their risks as they grow,” he wrote via email. “We are proud to co-lead Vouch’s latest funding round to give startups access to the insurance they need as they add headcount, increase their customer base, or raise funding rounds of their own.”

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

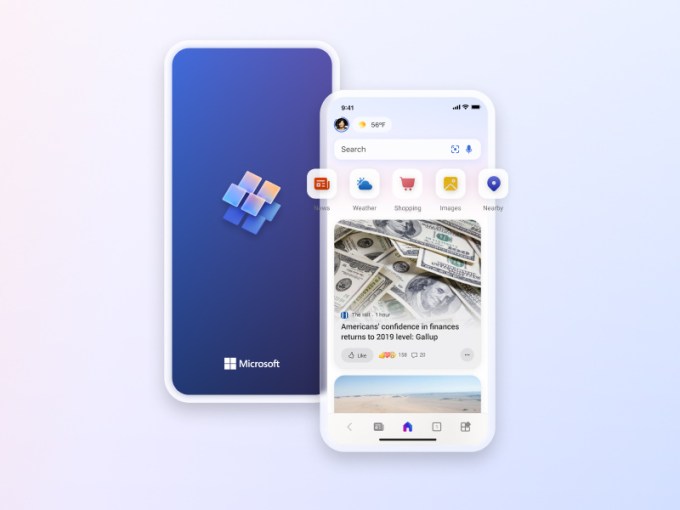

Microsoft today is introducing its own personalized news reading experience called Microsoft Start, available as both a website and mobile app, in addition to being integrated with other Microsoft products, including Windows 10 and 11 and its Microsoft Edge web browser. The feed will combine content from news publishers, but in a way that’s tailored to users’ individual interests, the company says — a customization system that could help Microsoft better compete with the news reading experiences offered by rivals like Apple or Google, as well as popular third-party apps like Flipboard or SmartNews.

Microsoft says the product builds on the company’s legacy with online and mobile consumer services like MSN and Microsoft News. However, it won’t replace MSN. That service will remain available, despite the launch of this new, in-house competitor.

To use Microsoft Start, consumers can visit the standalone website MicrosoftStart.com, which works on both Google Chrome and Microsoft Edge (but not Safari), or they can download the Microsoft Start mobile app for iOS or Android.

The service will also power the News and Interests experience on the Windows 10 taskbar and the Widgets experience on Windows 11. In Microsoft Edge, it will be available from the New Tab page, too.

Image Credits: Microsoft

At first glance, the Microsoft Start website is very much like any other online portal offering a collection of news from a variety of publishers, alongside widgets for things like weather, stocks, sports scores and traffic. When you click to read an article, you’re taken to a syndicated version hosted on Microsoft’s domain, which includes the Microsoft Start top navigation bar at the top and emoji reaction buttons below the headline.

Users can also react to stories with emojis while browsing the home page itself.

This emoji set is similar to the one being offered today by Facebook, except that Microsoft has replaced Facebook’s controversial laughing face emoji with a thinking face. (It’s worth noting that the Facebook laughing face has been increasingly criticized for being used to openly ridicule posts and mock people — even on stories depicting tragic events, like COVID deaths, for instance.)

Microsoft has made another change with its emoji, as well: After you react to a story with an emoji, you only see your emoji instead of the top three and total reaction count.

Image Credits: Microsoft

But while online web portals tend to be static aggregators of news content, Microsoft Start’s feed will adjust to users’ interests in several different ways.

Users can click a “Personalize” button to be taken to a page where they can manually add and remove interests from across a number of high-level categories like news, entertainment, sports, technology, money, finance, travel, health, shopping and more. Or they can search for categories and interests that could be more specific or more niche. (Instead of “parenting,” for instance, “parenting teenagers.”) This recalls the recent update Flipboard made to its own main page, the For You feed, which lets users make similar choices.

As users then begin to browse their Microsoft Start feed, they can also click a button to thumbs up or thumbs down an article to better adjust the feed to their preferences. Over time, the more the user engages with the content, the better refined the feed becomes, says Microsoft. This customization will leverage AI and machine learning, as well as human moderation, the company notes.

The feed, like other online portals, is supported by advertising. As you scroll down, you’ll notice every few rows will feature one ad unit, where the URL is flagged with a green “Ad” badge. Initially, these mostly appear to be product ads, making them distinct from the news content. Since Microsoft isn’t shutting down MSN and is integrating this news service into a number of other products, it’s expanding the available advertising real estate it can offer with this launch.

According to the iOS app’s privacy label, the data being used to track users across websites and apps owned by other companies includes the User ID. By comparison, Google News does not include a tracking section. Both Microsoft Start and Google News collect a host of “data linked to you,” like location, identifiers, search history, usage data, contact info, and more. The website itself, however, only links to Microsoft’s general privacy policy.

The website, app, and integrations are rolling out starting today. (If you aren’t able to find the new app yet — it replaces Microsoft News — you can try scanning the QR code from your mobile device. We currently found the app had rolled out on iOS but the link pointed us to Microsoft News on Android. Your mileage may vary.)

Powered by WPeMatico

In the United States, a 401(k) plan is an employer-sponsored defined-contribution pension account. However, with legacy institutional investing, most of these have at least some level of fossil fuel involvement, and, let’s face it, very few of us really know. Now a startup plans to change that.

California-based startup Sphere wants to get employees to ask their employers for investment options that are not invested in fossil fuels. To do that it’s offering financial products that make it easier — it says — for employers to offer fossil-free investment options in their 401(k) plans. This could be quite a big movement. Sphere says there are more than $35 trillion in assets in retirement savings in the U.S. as of Q1 2021.

It’s now raised a $2 million funding round led by climate tech-focused VC Pale Blue Dot. Also participating were climate-focused investors including Sundeep Ahuja of Climate Capital. Sphere is also a registered “Public Benefit Corporation,” allowing it to campaign in public about climate change.

Alex Wright-Gladstein, CEO and founder of Sphere said: “We are proud to be partnering with Pale Blue Dot on our mission to reverse climate change by making our money talk. Heidi, Hampus, and Joel have the experience and drive to help us make big changes on the short seven-year time scale that we have to limit warming to 1.5°C.” Wright-Gladstein has also teamed up with sustainable investing veteran Jason Britton of Reflection Asset Management and BITA custom indexes.

Wright-Gladstein said she learned the difficulty of offering fossil-free options in 401(k) plans when running her previous startup, Ayar Labs. She tried to offer a fossil-free option for employees, but found out it took would take three years to get a single fossil-free option in the plan.

Heidi Lindvall, general partner at Pale Blue Dot, said: “We are big believers in Sphere’s unique approach of raising awareness through a social movement while offering a range of low-cost products that address the structural issues in fossil-free 401(k) investing.”

Powered by WPeMatico

Even as hundreds of millions of people in India have a bank account, only a tiny fraction of this population invests in any financial instrument.

Fewer than 30 million people invest in mutual funds or stocks, for instance. In recent years, a handful of startups have made it easier for users — especially the millennials — to invest, but the figure has largely remained stagnant.

Now, an Indian startup believes that it has found the solution to tackle this challenge — and is already seeing good early traction.

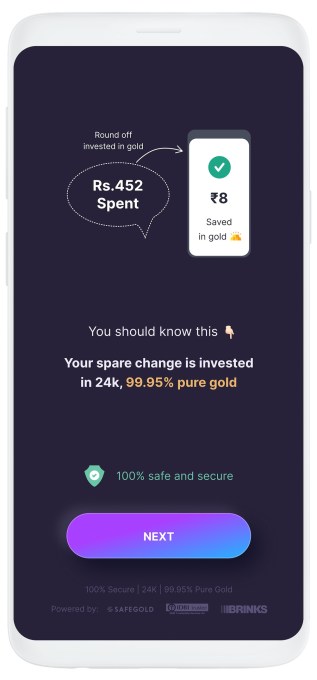

Nishchay AG, former director of mobility startup Bounce, and Misbah Ashraf, co-founder of Marsplay (sold to Foxy), founded Jar earlier this year.

The startup’s eponymous six-month-old Android app enables users to start their savings journey for as little as 1 Indian rupee.

Users on Jar can invest in multiple ways and get started within seconds. The app works with Paytm (PhonePe support is in the works) to set up a recurring payment. (The startup is the first to use UPI 2.0’s recurring payment support.) They can set up any amount between 1 Indian rupee to 500 for daily investments.

The Jar app can also glean users’ text messages and save a tiny amount based on each monetary transaction they do. So, for instance, if a user has spent 31 rupees in a transaction, the Jar app rounds that up to the nearest tenth figure (40, in this case) and saves nine rupees. Users can also manually open the app and spend any amount they wish to invest.

Once users have saved some money in Jar, the app then invests that into digital gold.

The startup is using gold investment because people in the South Asian market already have an immense trust in this asset class.

India has a unique fascination for gold. From rural farmers to urban working class, nearly everyone stashes the yellow metal and flaunts jewelry at weddings.

Indian households are estimated to have a stash of over 25,000 tons of the precious metal whose value today is about half of the country’s nominal GDP. Such is the demand for gold in India that the South Asian nation is also one of the world’s largest importers of this precious metal.

Jar’s Android app (Image Credits: Jar)

“When you’re thinking about bringing the next 500 million people to institutional savings and investments, the onus is on us to educate them on the efficacies of the other instruments that are in the market,” said Nishchay.

“We want to give them the instrument they trust the most, which is gold,” he said. The startup plans to eventually offer several more investment opportunities, he said.

The founders met several years ago when they were exploring if MarsPlay and Bounce could have any synergies. They stayed in touch and, last year during one of their many conversations, realized that neither of them knew much about investments.

“That’s when the dots started to connect,” said Misbah, drawing stories from his childhood. “I come from a small town in Bihar called Bihar Sharif. During my childhood days, I saw my family deeply troubled with debt because of poor financial decisions and no savings,” he said.

“We both understand what a typical middle class family goes through. Someone who comes from this background never had any means in the past but their aspirations are never-ending. So when you start earning, you immediately start to spend it all,” said Nishchay.

“The market needs products that will help them get started,” he said.

That idea, which is similar to Acorn and Stash’s play in the U.S. market, is beginning to make inroads. The app has already amassed about half a million downloads, the founders said. Investors have taken notice, too.

On Wednesday, Jar announced it has raised $4.5 million from a clutch of high-profile investors, including Arkam Ventures, Tribe Capital, WEH Ventures, and angels including Kunal Shah (founder of CRED), Shaan Puri (formerly with Twitch), Ali Moiz (founder of Stonks), Howard Lindzon (founder of Social Leverage), Vivekananda Hallekere (co-founder of Bounce), Alvin Tse (of Xiaomi) and Kunal Khattar (managing partner at AdvantEdge).

“Over 400 million Indians are about to embrace digital financial services for the first time in their lives. Jar has built an app that is poised to help them — with several intuitive ways including gamification — start their investment journey. We love the speed at which the team has been executing and how fast they are growing each week,” said Arjun Sethi, co-founder of Tribe Capital, in a statement.

Transactions and AUM on the Jar app are surging 350% each month, said Nishchay. The startup plans to broaden its product offerings in the coming days, he said.

Powered by WPeMatico