Auto Added by WPeMatico

For the love of the loot: Blockchain, the metaverse and gaming’s blind spot

The speed at which gaming has proliferated is matched only by the pace of new buzzwords inundating the ecosystem. Marketers and decision-makers, already suffering from FOMO about opportunities within gaming, have latched onto buzzy trends like the applications of blockchain in gaming and the “metaverse” in an effort to get ahead of the trend rather than constantly play catch-up.

The allure is obvious, as the relationship between the blockchain, metaverse and gaming makes sense. Gaming has always been on the forefront of digital ownership (one can credit gaming platform Steam for normalizing the concept for games, and arguably other media such as movies), and most agreed upon visions of the metaverse rely upon virtual environments common in games with decentralized digital ownership.

Whatever your opinion of either, I believe they both have an interrelated future in gaming. However, the success or relevance of either of these buzzy topics is dependent upon a crucial step that is being skipped at this point.

Let’s start with the example of blockchain and, more specifically, NFTs. Collecting items of varying rarities and often random distribution form some of the core “loops” in many games (e.g., kill monster, get better weapon, kill tougher monster, get even better weapon, etc.), and collecting “skins” (i.e., different outfits/permutation of game character) is one of the most embraced paradigms of microtransactions in games.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track.

Now, NFTs are positioned to be a natural fit with various rare items having permanent, trackable and open value. Recent releases such as “Loot (for Adventurers)” have introduced a novel approach wherein the NFTs are simply descriptions of fantasy-inspired gear and offered in a way that other creators can use them as tools to build worlds around. It’s not hard to imagine a game built around NFT items, à la Loot.

But that’s been done before … kind of. Developers of games with a “loot loop” like the one described above have long had a problem with “farmers,” who acquire game currencies and items to sell to players for real money, against the terms of service of the game. The solution was to implement in-game “auction houses” where players could instead use real money to purchase items from one another.

Unfortunately, this had an unwanted side effect. As noted by renowned game psychologist Jamie Madigan, our brains are evolved to pay special attention to rewards that are both unexpected and beneficial. When much of the joy in some games comes from an unexpected or randomized reward, being able to easily acquire a known reward with real money robbed the game of what made it fun.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track. The most extreme examples of this phenomena commit the biggest cardinal sin in gaming — a game that is “pay to win,” where a player with a big bankroll can acquire a material advantage in a competitive game.

Blockchain games such as Axie Infinity have rapidly increased enthusiasm around the concept of “play to earn,” where players can potentially earn money by selling tokenized resources or characters earned within a blockchain game environment. If this sounds like a scenario that can come dangerously close to “pay to win,” that’s because it is.

What is less clear is whether it matters in this context. Does anyone care enough about the core game itself rather than the potential market value of NFTs or earning potential through playing? More fundamentally, if real-world earnings are the point, is it truly a game or just a gamified micro-economy, where “farming” as described above is not an illicit activity, but rather the core game mechanic?

The technology culture around blockchain has elevated solving for very hard problems that very few people care about. The solution (like many problems in tech) involves reevaluation from a more humanist approach. In the case of gaming, there are some fundamental gameplay and game psychology issues to be tackled before these technologies can gain mainstream traction.

We can turn to the metaverse for a related example. Even if you aren’t particularly interested in gaming, you’ve almost certainly heard of the concept after Mark Zuckerberg staked the future of Facebook upon it. For all the excitement, the fundamental issue is that it simply doesn’t exist, and the closest analogs are massive digital game spaces (such as Fortnite) or sandboxes (such as Roblox). Yet, many brands and marketers who haven’t really done the work to understand gaming are trying to fast-track to an opportunity that isn’t likely to materialize for a long time.

Gaming can be seen as the training wheels for the metaverse — the ways we communicate within, navigate and think about virtual spaces are all based upon mechanics and systems with foundations in gaming. I’d go so far as to predict the first adopters of any “metaverse” will indeed be gamers who have honed these skills and find themselves comfortable within virtual environments.

By now, you might be seeing a pattern: We’re far more interested in the “future” applications of gaming without having much of a perspective on the “now” of gaming. Game scholarship has proliferated since the early aughts due to a recognition of how games were influencing thought in fields ranging from sociology to medicine, and yet the business world hasn’t paid it much attention until recently.

The result is that marketers and decision-makers are doing what they do best (chasing the next big thing) without the usual history of why said thing should be big, or what to do with it when they get there. The growth of gaming has yielded an immense opportunity, but the sophistication of the conversations around these possibilities remains stunted, due in part to our misdirected attention.

There is no “pay to win” fast track out of this blind spot. We have to put in the work to win.

Powered by WPeMatico

In growth marketing, signal determines success

Unlike a weak phone signal solely causing a grainy sound, in growth marketing, it can mean the difference between a successful program or a massive cash bleed. As we move toward an increasingly privacy-centric world, it is even more necessary for companies to nail down signal early on.

So what exactly is “signal” in growth marketing? It can carry many different meanings, but holistically speaking, it’s the event data in our arsenal to help guide decisions. When it comes to paid acquisition, it’s vital to optimize and pass back the correct event data to paid channels. This is so that targeting and bidding algorithms have the most enriched data to utilize.

I’ve seen startups spend thousands of dollars inefficiently as a result of not having optimal signal in their paid acquisition campaigns. I’ve also spent millions at companies such as Postmates refining our signal to the best possible state. I’d like every startup to avoid the painful mistake of not having this set up correctly, instead making the most of every important ad dollar.

The selection

When starting out, it may seem obvious to optimize toward a north-star metric such as a purchase. If spend is very minimal, that could mean that the conversion volume will be low across campaigns. On the flip side, if the optimization event is set at a top-of-funnel event such as a landing page view, the signal strength may be very weak. The reason that the strength may be weak is due to passing back a low-intent event as successful to the paid channels. By marking a landing page view as successful, paid channels such as Facebook will continue to find users that are similar to these lower-propensity users that are converting.

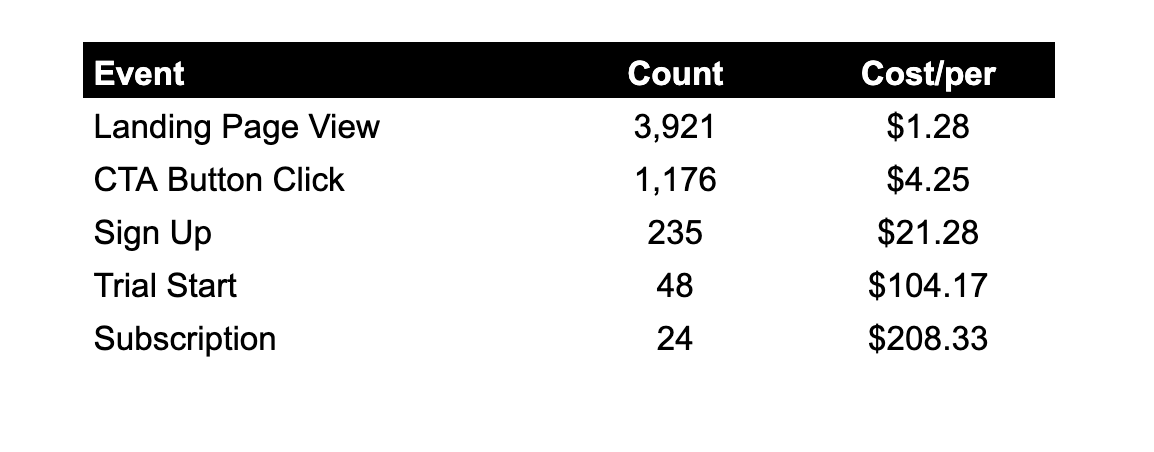

Let’s take an example of a health-and-wellness app with a goal of driving memberships to their coaching program. They’re just starting out with exploring paid acquisition and spending $5,000 per week on Facebook. Below is a look at their events in the funnel, weekly volume and cost per event:

Example of a health-and-wellness app and their weekly conversion volume at $5,000 spend. Image Credits: Jonathan Martinez

In the above example, we can see that there’s significant volume for landing page views. As we go down the simplified flow, there is less volume as users drop off the funnel. Almost everyone’s instinct would be to optimize for either the landing page view, because there’s so much data, or the subscription event, because it’s the strongest. I would argue (after extensive testing across multiple ad accounts) that neither of these events would be the correct pick. With landing page views as an optimization event, the users have an egregiously low propensity since the landing page view to subscription conversion rate is 0.61%.

The correct event to optimize for here would either be sign up or trial start because they have sufficient enough volume and are strong signals of a user converting to the north-star metric (subscription). Looking at the conversion rate between sign up and subscription, it’s a much healthier 10.21%, versus the 0.61% from landing page view.

I’m always a huge proponent of testing all events, as there can definitely be big surprises in what may work best for you. When testing events, make sure that there’s a stat-sig baseline that’s being followed to make decisions. Additionally, I think it’s a great practice to test events regularly early on because conversion rates can change as other channel variables are adjusted.

Flow adjustments

In certain cases, the current events that are set up aren’t optimal for paid acquisition campaigns. I’ve seen this happen frequently with startups that have long windows of time between conversion events. Take a startup such as Thumbtack, which provides a marketplace of providers who can help with home repairs. After someone signs up to their app, the user may place a request but not hire someone until a few weeks later. In this case, making flow adjustments could potentially improve the signal and data that you collect from users.

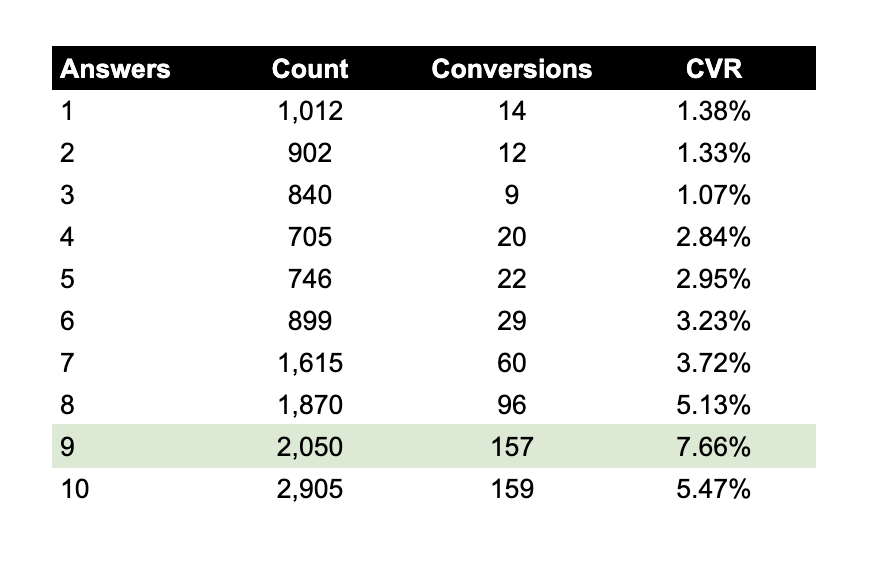

A solution that Thumbtack could implement to gather a stronger signal would be to add another step between the request being placed and hiring someone. This could potentially be a survey with propensity check questions that could ask how soon the user needs help or how important their project is from a 1–10.

Example of in-app survey responses to “How important is your project?” Image Credits: Jonathan Martinez.

After accumulating the data, if there’s a high correlation between survey answers and someone starting their project, we can start to explore optimizing for that event.

In the above example, we see that users who responded with “9” have a 7.66% likelihood to convert. Therefore, this should be the event we optimize for. Artificially adding steps that qualify users in a longer flow can help steer optimization targeting in the right direction.

Enhancing signal

Let’s imagine that you have the most ideal flow that captures large volumes of event signal without much of a delay to your optimization event. That’s still far from perfect. There are myriad solutions that can be implemented to further enhance the signal.

For Facebook specifically, there are connections such as CAPI that can be integrated to pass back data in a more accurate way. CAPI is a method of passing back web events server-to-server rather than relying on cookies and the Facebook pixel. This helps mitigate browsers that block cookies or users who may delete their web history. This is just one example. I won’t run through all the channels, but each has its own solution to help enhance event signal being passed back to it.

iOS 14 signal

This wouldn’t be a column written in 2021 without mention of iOS 14 and the strategies that can be leveraged for this growing user segment. I’ve written another piece about iOS-14-specific tactics, but I’ll cover it here on a broad level. If the north-star metric (i.e., purchase) event can be triggered within 24 hours of the initial app launch, then that’s golden.

This would bring large volumes of high-intent data that would not be at the mercy of the SKAD 24-hour event timer. For most companies, this may sound like a lofty goal, so the target should be to have an event fire within 24 hours that is a high-likelihood indicator of someone completing your north-star metric. Think of which events happen in the flow that lead to someone eventually purchasing. Maybe someone adding a payment method happens within 24 hours and historically has a 90% conversion rate to someone purchasing. An “add payment info” event would be a great conversion event to use in this case. The landscape of iOS 14 is constantly changing but this should apply for the immediate future.

Incrementality and staying ahead

As a rule of thumb, incrementality checks should constantly be performed in growth marketing. It gives an important read on whether advertising dollars are bringing in users that wouldn’t have converted had they not seen an ad.

When comparing optimization events, this rule still applies. Make sure that costs per action aren’t the only metric that’s being used as a measure of success, but instead, use the incremental lift on each conversion event as the ultimate key performance indicator. In this piece, I detail how to run lean incrementality tests without swarms of data scientists.

So how do you stay ahead and continue moving the needle on your growth marketing campaigns? First and foremost, constantly question the events you’re optimizing for. And second, leave no stone unturned.

If you’re using the same optimization event forever, it will be a disservice to your campaign performance potential. By experimenting with flow changes and running tests on new events, you’ll be way ahead of the curve. When iterating on the flow, think about user behavior and events from the user’s perspective. Which flow events, if added, would correlate to a high propensity conversion segment?

Powered by WPeMatico

LinkedIn launches a $25M fund for creators, will test Clubhouse-style audio feature in coming weeks

When LinkedIn first launched Stories format, and later expanded its tools for creators earlier this year, one noticeable detail was that the Microsoft-owned network for professionals hadn’t built any kind of obvious monetization into the program — noticeable, given that creators earn a living on other platforms like Instagram, YouTube and TikTok, and those apps had lured creators, their content and their audiences in part by paying out.

“As we continue to listen to feedback from our members as we consider future opportunities, we’ll also continue to evolve how we create more value for our creators,” is how LinkedIn explained its holding pattern on payouts to me at the time. But that strategy may have backfired for the company — or at least may have played a role in what came next: last month, LinkedIn announced it would be scrapping its Stories format and going back to the proverbial drawing board to work on other short-form video content for the platform.

Now comes the latest iteration in that effort. To bring more creators to the platform, the company today announced that it would be launching a new $25 million creator fund, which initially will be focused around a new Creator Accelerator Program.

It’s coming on the heels of LinkedIn also continuing to work on one of its other new-content experiments: a Clubhouse-style live conversation platform. As we previously reported, LinkedIn began working on this back in March of this year. Now, we are hearing that the feature will make an appearance as part of a broader events strategy for the company very soon.

“We’ll be starting to test audio with a small pilot group in the coming weeks,” said Chris Szeto, senior director of product at LinkedIn, who heads up its audio efforts. “Given the trends in virtual, hybrid events we are also working on making audio part of our overall event strategy rather than a standalone offering, so that we can give people more choice about how they want to run and engage with their audiences.”

Notably, in a blog post announcing the creator fund, LinkedIn also listed a number of creator events coming up. Will the Clubhouse-style feature pop up there? Watch this space. Or maybe… listen up.

In any case, the creator accelerator that LinkedIn is announcing today is part of a bigger effort it’s been making to build out a platform for creating content. That has included building new tools and acquiring companies like Jumprope (a platform devised to make “how-to” videos) earlier this year. Together with the accelerator, the idea that LinkedIn wants to encourage more dynamic and lively set of voices to get more people talking and spending time on LinkedIn.

Andrei Santalo, global head of community at LinkedIn, noted in the blog post that the accelerator/incubator will be focused on the many ways that one can engage on LinkedIn.

“Creating content on LinkedIn is about creating opportunity, for yourselves and others,” he writes. “How can your words, videos and conversations make 774+ million professionals better at what they do or help them see the world in new ways?”

The incubator will last for 10 weeks and will take on 100 creators in the U.S. to coach them on building content for LinkedIn. It will also give them chances to network with like-minded individuals (naturally… it is LinkedIn), as well as a $15,000 grant to do their work. The deadline for applying (which you do here) is October 12.

The idea of starting a fund to incentivize creators to build video for a particular platform is definitely not new — and that is one reason why it was overdue for LinkedIn to think about its own approach.

Leading social media platforms like TikTok, Snapchat, Instagram and Facebook and YouTube all have announced hundreds of millions of dollars in payouts in the form of creator funds to bring more original content to their platforms.

You could argue that for mass-market social media sites, it’s important to pay creators because competition is so fierce among them for consumer attention.

But on the other hand, those platforms have appeal for creators because of the potential audience size. At 774 million users, LinkedIn isn’t exactly small, but the kind of content that tends to live on there is so different, and maybe drier — it’s focused on professional development, work and “serious” topics — that perhaps it might need the most financial incentive of all to get creators to bite.

LinkedIn’s bread and butter up to now has been around professional development: people use it to look for work, to get better jobs, to hire people, and to connect with people who might help them get ahead in their professional lives.

But it’s done so in a very prescribed set of formats that do not leave much room for exploring “authenticity” — not in the modern sense of “authentic self”, and not in the more old-school sense of just letting down your guard and being yourself. (Even relatively newer initiatives like its education focus directly play into this bigger framework.)

With authenticity becoming an increasing priority for people — and maybe more so as we have started to blur the lines between work and home because of COVID-19 and the changes that it has forced on us — I can’t help but wonder whether LinkedIn will use this opportunity to rethink, or at least expand the concept of, what it means to spend time on its platform.

Powered by WPeMatico

Investors are doubling down on Southeast Asia’s digital economy

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Big tech

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

Venture capitalists

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

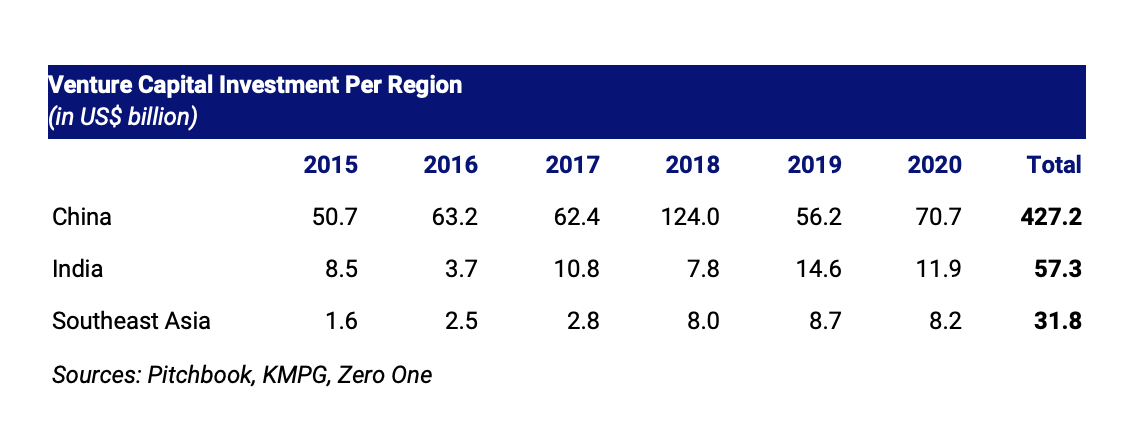

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

Epic Games to shut down Houseparty in October, including the video chat ‘Fortnite Mode’ feature

Houseparty, the social video chat app acquired by Fortnite maker Epic Games for a reported $35 million back in 2019, is shutting down. The company says Houseparty will be discontinued in October when the app will stop functioning for its existing users; it will be pulled from the app stores today, however. Related to this move, Epic Games’ “Fortnite Mode” feature, which leveraged Houseparty to bring video chat to Fortnite gamers, will also be discontinued.

Founded in 2015, Houseparty offered a way for users to participate in group video chats with friends and even play games, like Uno, trivia, Heads Up and others. Last year, Epic Games integrated Houseparty with Fortnite, initially to allow gamers to see live feeds from friends while gaming, then later adding support to livestream gameplay directly into Houseparty. At the time, these integrations appeared to be the end goal that explained why Epic Games had bought the social startup in the first place.

Now, just over two years after the acquisition was announced, and less than half a year since support for livestreaming was added to the app, Houseparty is shutting down.

The company didn’t offer any solid insight into what, at first glance, feels like an admission of failure to capitalize on its acquisition. But the reality is that Epic Games may have something larger in store beyond just video chat. That said, all Epic Games would say today is that the Houseparty team could no longer give the app the attention it required — a statement that indicates an executive decision to shift the team’s focus to other matters.

While none of the Houseparty team members are being let go as a result of this move, we’re told, they will be joining other teams where they will work on new ways to allow for “social interactions” across the Epic Games family of products. The company’s announcement hinted that those social features would be designed and built at the “metaverse scale.”

The “metaverse” is an increasingly used buzzword that references a shared virtual environment, like those provided by large-scale online gaming platforms such as Fortnite, Roblox and others. Facebook, too, claims the metaverse is the next big gambit for social networking, with CEO Mark Zuckerberg having described it as an “embodied internet that you’re inside of rather than just looking at.”

To some extent, Fortnite has begun to embrace the metaverse by offering non-gaming experiences like online concerts you attend as your avatar, and other live events. Ahead of its shutdown, Houseparty also toyed with live events that users would co-watch and participate in alongside their friends.

An Epic Games spokesperson tells TechCrunch the Houseparty team has worked on (and continues to work on) a number of other projects that focus on social. But some of the “multiple, larger projects” Epic Games has in the works remain undisclosed, we’re told.

In terms of social products, Houseparty’s technology now underpins all of Fortnite voice chat and the features they built are widely available for free to developers through Epic Games Services. They also worked on building out new social experiences, which have ranged from the social RSVP functions for Fortnite’s global events, like the recent Ariana Grande concert, to the upcoming “Operation: Sky Fire” event for collaborating quests and other game mechanics. More social functionality and new experiences are also being built into Fortnite’s user-generated content platform, Create Mode.

While it may seem odd to close an app that only last year experienced a boost in usage due to the pandemic, it appears the COVID bump didn’t have staying power.

At the height of lockdowns, Houseparty had reported it had gained 50 million new sign-ups in a month’s time as users looked to video apps to connect with family and friends while the world was shut down. But as the pandemic wore on, other video chat experiences gained more ground. Zoom, which had established itself as an essential tool for remote work, became a tool for hanging out with friends after-hours, as well. Facebook also started to eat Houseparty’s lunch with its debut of drop-in video chat “Rooms” last year, which offered a similar group video experience. And bored users shifted to audio-based social networking on apps like Clubhouse or Twitter Spaces.

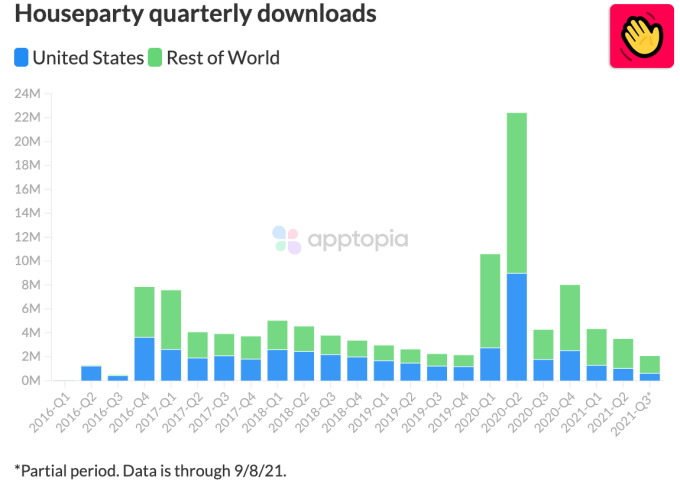

Image Credits: Apptopia

According to data from Apptopia, Houseparty has been continually declining since the pandemic bump. To date, its app has seen a total of 111 million downloads across iOS and Android, with the majority (63 million) on iOS. The U.S. was Houseparty’s largest market, accounting for 43.4% of downloads, followed by the U.K. (9.8%), then Germany (5.6%).

Epic Games, meanwhile, said the app served “tens of millions” of users worldwide. It insists the closure wasn’t decided lightly, nor was the decision to shutter “Fortnite Mode” made due to lack of adoption.

Houseparty will alert users to the shutdown via in-app notifications ahead of its final closure in October. At that point, Fortnite Mode will also no longer be available.

Powered by WPeMatico

Performance marketing agency MuteSix bets on content and data to boost DTC e-commerce

Warby Parker filing to IPO last week was one more sign that direct-to-consumer (DTC) is an extremely powerful e-commerce trend. But LA-based performance marketing agency MuteSix didn’t wait that long to build its business around scaling DTC brands.

Created in 2014 and acquired by Dentsu in 2019, MuteSix was recommended to TechCrunch by Rhoda Ullmann, VP Consumer at Sense, a Boston-based startup building a home energy monitor. “They demonstrate best-in-class expertise with Facebook and Google paid ad platforms. They also have a very smart and efficient approach to creative development that was critical to helping us scale,” she wrote. (If you have growth marketing agencies or freelancers to recommend, please fill out our survey!)

Besides Sense, MuteSix’s former and current clients include companies such as Adidas, Petco, Ring and Theragun, to whom it provides a full range of marketing services, including top-notch direct response videos. But regardless of whether you can afford this, we think you’ll learn interesting lessons from our conversation with their CRO, Greg Gillman. The key takeaway? In today’s highly competitive ad environment, both content and data are kings.

Editor’s note: The interview below has been edited for length and clarity.

What can you tell us about MuteSix as an agency?

Image Credits: MuteSix

Greg Gillman: We’ve been around for about nine years. We started out as a Facebook ad agency — as opposed to a lot of agencies that start out by saying they do everything, we decided to focus on what we were really good at. At the time, it was doing Facebook media buying for e-commerce companies. Primarily here in LA, which is kind of the hub of these companies, but also all over. And then bit by bit, we grew the organization.

At this point, we’re a little over 400 people, and we manage upward of $500 million in spend on Facebook and Google, including Instagram and YouTube. What we’ve grown into is a one-stop shop for DTC e-commerce companies: We manage all the channels that a DTC brand needs. And we’re a performance agency; everything we do is based on results. People come to us to drive revenue into their e-commerce businesses.

Why do you think that performance marketing is the right fit for DTC?

DTC entrepreneurs are more focused on immediate impact, because if they’re not selling product, there’s no large brand propping them up. So I think that doing DTC marketing requires you to be more performance focused. For agencies that work with large brands, usually it’s more about impression buying versus performance buying. They can say: I did a reach campaign today to hit 10 million eyeballs, and whatever happens happens, because at the end of the day, you just told us to do 10 million impressions. It’s different than working with a group like us that’s trying to optimize every small piece of the funnel, and being accountable for the entire funnel to drive as much sales or revenue.

What type of clients do you work with?

The majority of the companies we work with are digitally native DTC companies. We’ve mostly stayed in that lane, because we’re really good at it. That being said, we work with companies of all sizes — startups, companies that are already established, and very large companies that need to rework both their creative and their media buying strategy.

I oversee sales, marketing and partnerships, and my role is really trying to figure out which brands make most sense to partner with MuteSix. We’re looking for high-growth brands that we can scale, and we’ve learned through the years that what works well are demonstrable products that have cool user value props.

We’ve worked with lots of startups at different points in the funnel, starting from the ground up and working with them through various rounds of funding, all the way through acquisitions, including two by unicorns. But these days, ground up is tougher. I like them to have some proof of concept — putting through $10,000-$15,000 per month on Facebook or $5,000-10,000 on Google usually shows me that there’s some life to it. But I don’t want to limit us if it’s a cool idea. I talk to a lot of people who come back once they’ve proven it out a little bit.

Have you worked with a talented individual or agency who helped you find and keep more users?

Respond to our survey and help other startups find top growth marketers they can work with!

What kind of clients are definitely not a good fit?

It won’t be a fit if there’s no real unique value prop for the product. If it’s just another run-of-the-mill company, a consultant can charge them a lower amount of money and set up Facebook ads, but what we are looking for are high-growth businesses.

The compensation for our campaign managers is actually tied to the performance of the campaigns, so if I bring a bunch of campaigns that we can’t scale, we’re gonna have a lot of unhappy media buyers who ask: “Greg, why would we take on this brand?” It’s a business model that has helped us attract top talent, but we need to make sure that we’re bringing brands that we think we can scale.

And it’s easier than ever to start a company, but it’s tougher now to scale it and take it past the $2 million-$3 million run rate. So I always revert back to asking founders: What are five reasons why people want to buy your product? What are the five reasons that they don’t? If the entrepreneur has trouble answering this, it’s not going to work. If they can’t tell somebody why their business is good, then we’re not going to be good at selling it.

How is MuteSix different from other agencies?

I’d say the main difference is that we have a 70-person in-house video creative team; and what we’re really good at doing is shooting and coming up with performance content. Not just content that looks and feels great, but video that is reverse-engineered to sell product.

Another key component is that we have a whole data science team that is also integrated with our media buying team, and that helps companies navigate things like attribution and signal loss due to the iOS 14 update. Right now, that means focusing on looking at the whole picture rather than by channel and working on mix-modeling attribution.

What are some of the things your data team focuses on?

One of the biggest things that brands struggle with is figuring out attribution, and how you continue to spend money even though you may have lost some signal into the platform. If Facebook skews too heavily, and Google is on last click, then sometimes it looks like things are never working. To help companies make informed business decisions, we are building statistical models that show information at higher-than-the-platform level.

We are also building better segments of customer profiles that help the clients understand who their core audience is, but also helps us build predictive audiences for finding new people.

Another big thing we’re trying to solve is incrementality. We work with large brands that have a strong organic following on social media; and their question is: “Hey, Greg, why should I spend more money if I would have acquired those users anyway?” So we’ve done incrementality testing with brands that spend a lot in other channels than Facebook and Google. We helped them build out different ways to look at the data so that we continue to spend in those channels and they actually know the incremental lift that they’re getting.

There’s one other piece that I think is super important and usually overlooked: first-party data. We work with brands to try and acquire as much of that first-party data as possible, segment it and use it, because that’s what they’d be left with if Facebook shut off tomorrow.

How do you prepare and adapt for changes in the marketing ecosystem?

Because we work with so many brands, we have a lot of senior leadership on each channel level. We routinely meet across departments and share insights. The data science team also builds pretty robust reporting. We try to stay ahead of our brands and to be forward-thinking about anything that is ultimately going to impact the agency. We’re constantly trying to hack our way through things like the types of content that work and things that we know will help us scale.

That’s how we have always approached it. Every major shift in our business was done to answer the needs of the brands that we were working with. For instance, there’s a data side to our business because it’s more important than ever to use that. Facebook used to be a platform where you could throw anything at the wall, and you would get a 4x or 5x return. No one’s asking about data when you’re literally printing money out of Facebook, right? It only happens when the margins get tight. But then Facebook became a more crowded platform, and the same happened with Google: more advertisers, higher CPM and a more competitive environment. We needed to be smarter about what we were doing, so we built out our data team.

Now there’s two levers that we can pull: the data side and the creative side of the business. Again, we are a performance marketing agency, focusing on all the levers. Because platforms like Facebook are only going to be more competitive, they’re only going to get more expensive, and we are only going to lose more traffic. So the more agile agencies have to think much farther outside of what we are doing on these platforms; because we’re going to make up the incremental revenue on things like SMS, influencer marketing and organic content, to continue to drive money into the top of the funnel.

Why is your content arm so important as a lever?

We have an integrated solution where our media buyers are paired directly with our video editors and producers to allow us to be agile and quick; because as everyone knows, content is king. What we try to do is optimize around things like what we call the thumbs-up rate on Facebook — three-second video views. If I held someone for that long in their newsfeed, I can potentially get them into our flow. We do the same on YouTube, and we do things like this on programmatic, because the name of the game is to get people into the funnel and work them through it. And we’re using both our data science team and our creative team to build out and optimize on the front end around these quick metrics to get things moving.

In my opinion, there’s no close second to an SMB agency that has a content arm like we do. Leveraging our content team to build performance content is one of the biggest levers that we have. Three and a half years ago, Facebook was telling us: “If you don’t build video content, and if you don’t prioritize video in the newsfeed, it’s not going to work.” At the time, we leaned in very hard — and the pain of growing a creative team of 70 people is real, especially in LA. But it’s allowed us to scale our agency.

Powered by WPeMatico

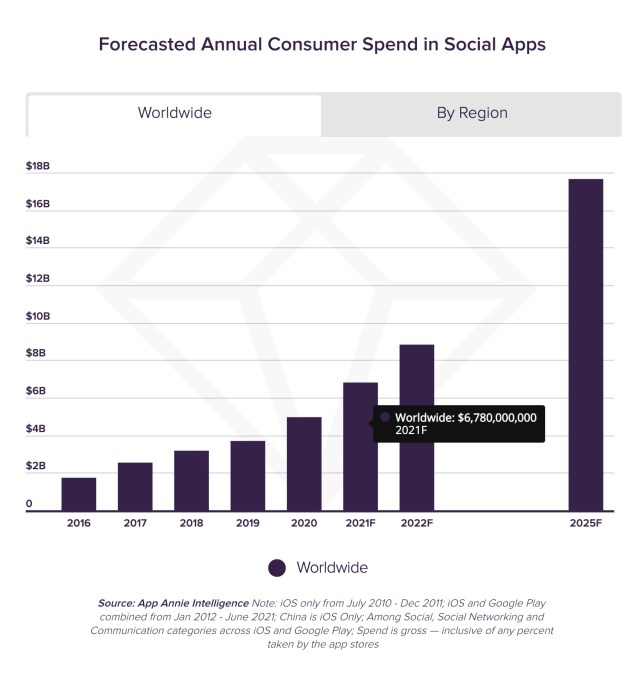

Driven by livestreams, consumer spending in social apps to hit $17.2B in 2025

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

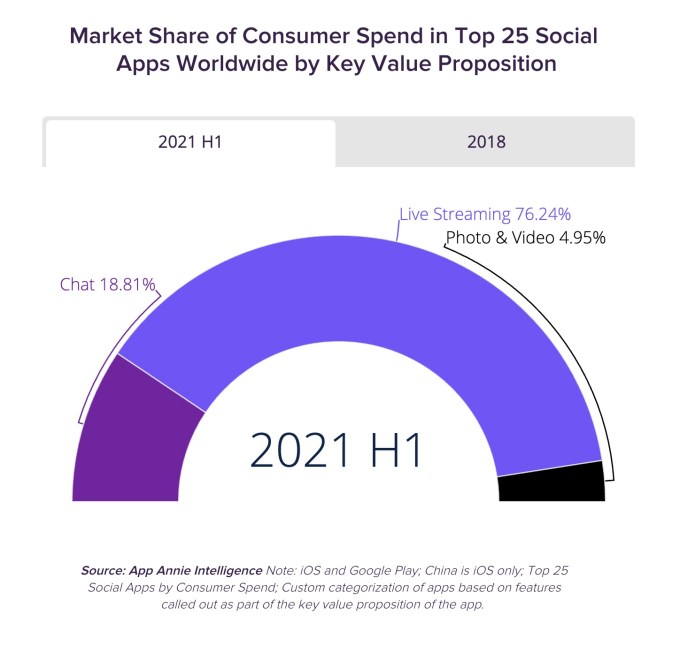

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

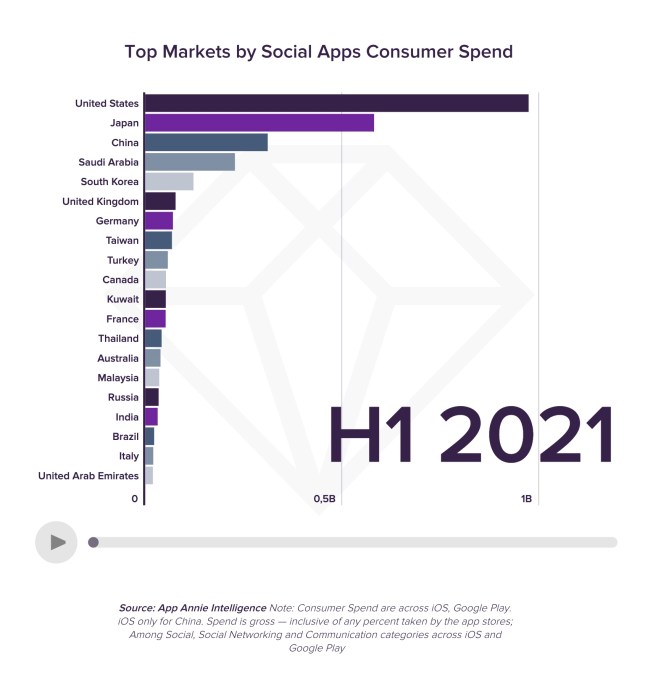

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

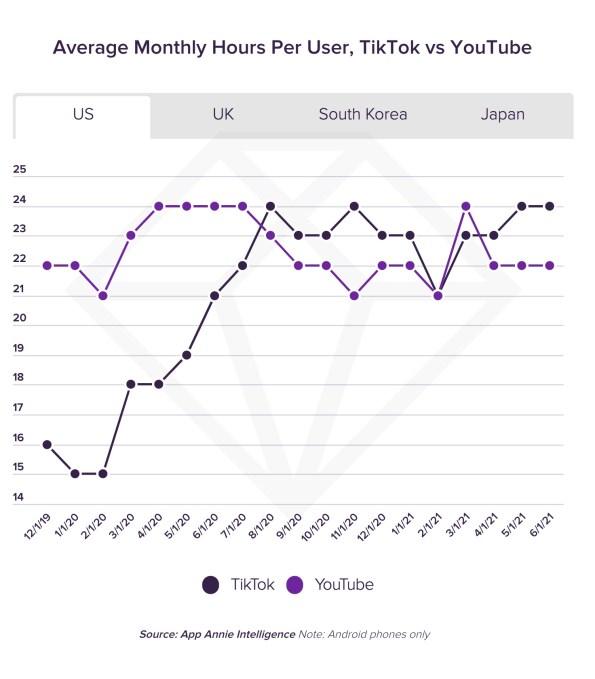

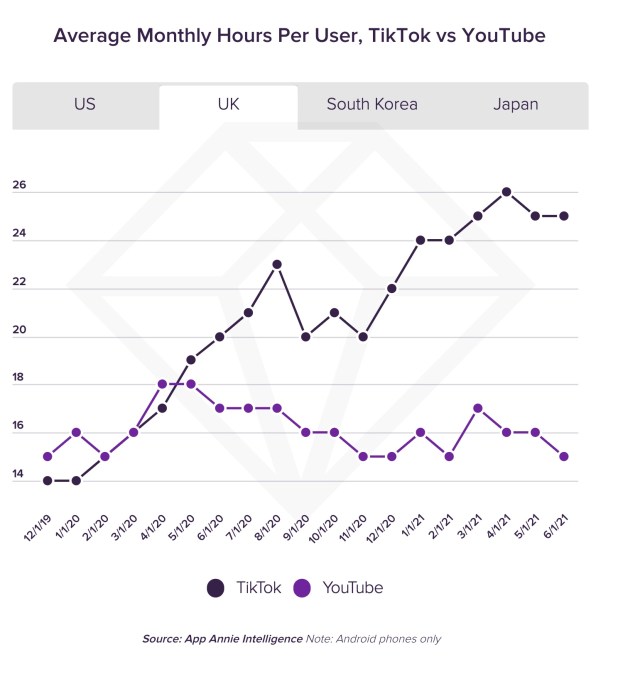

One top app that’s significantly gaining here is TikTok.

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

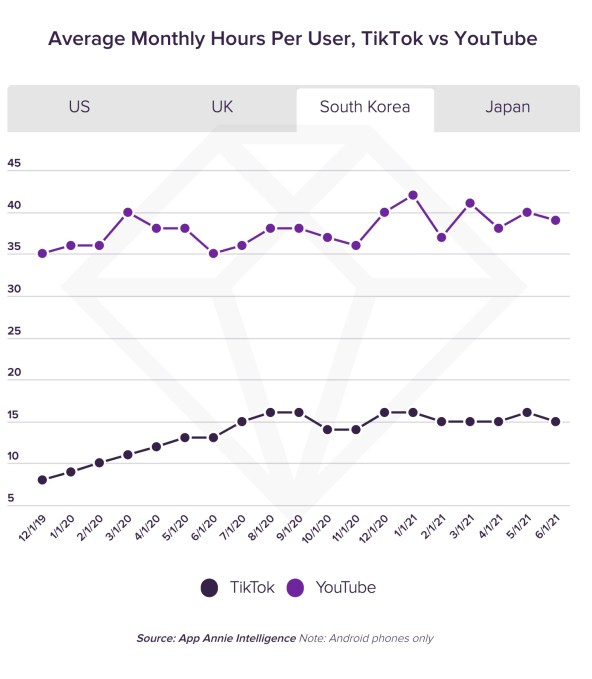

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

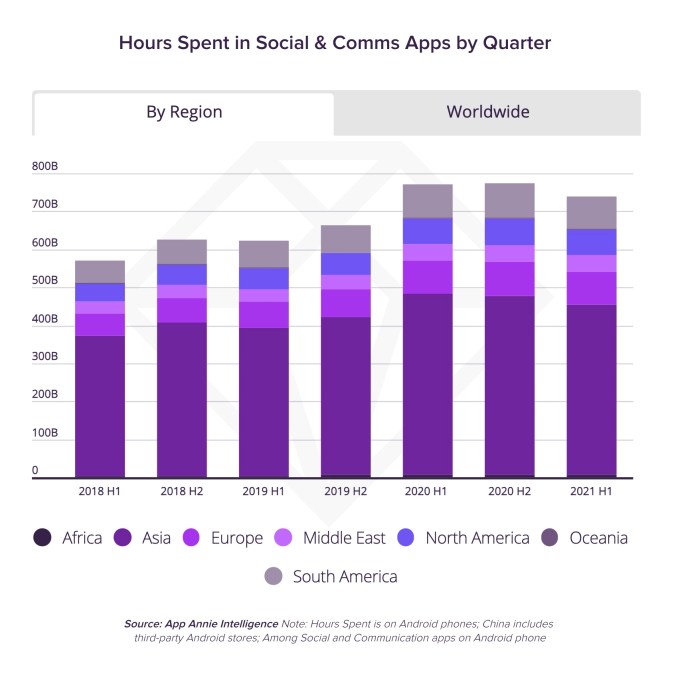

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

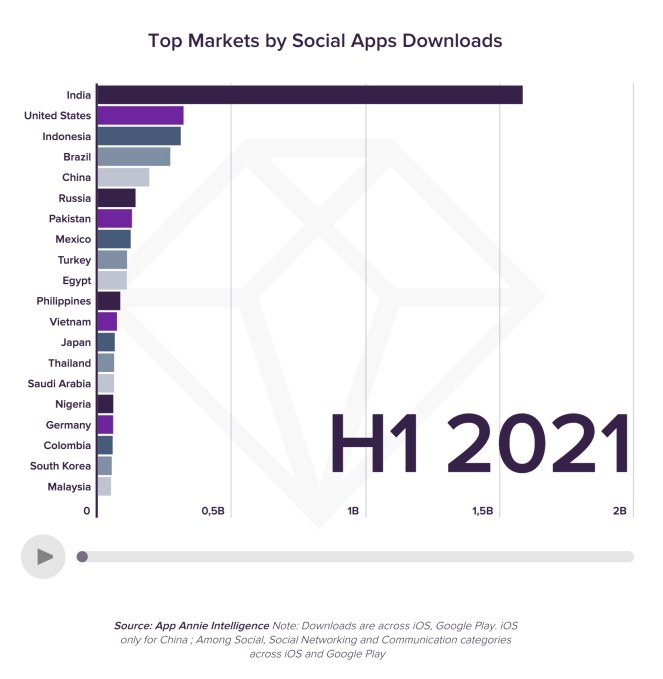

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

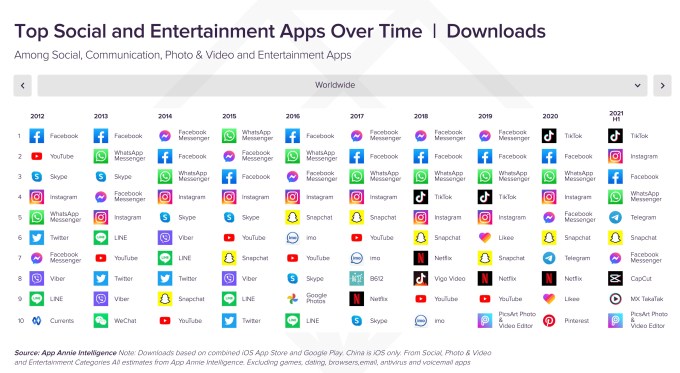

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

Facebook enters the fantasy gaming market

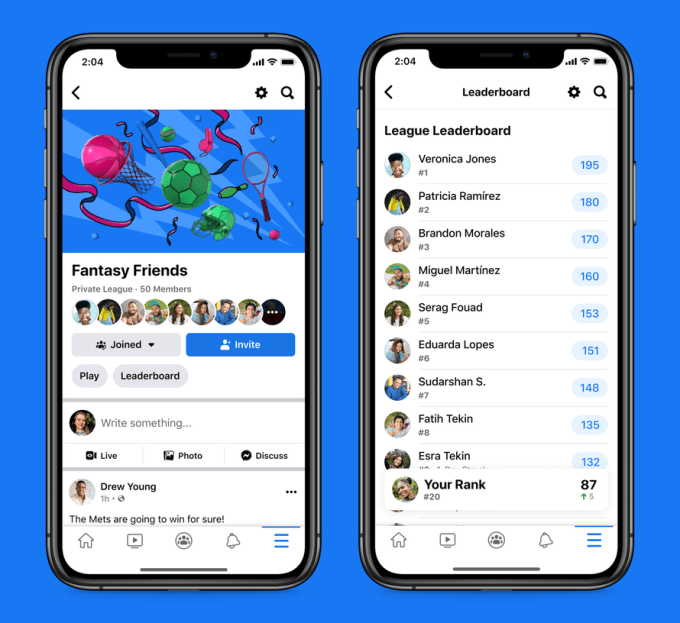

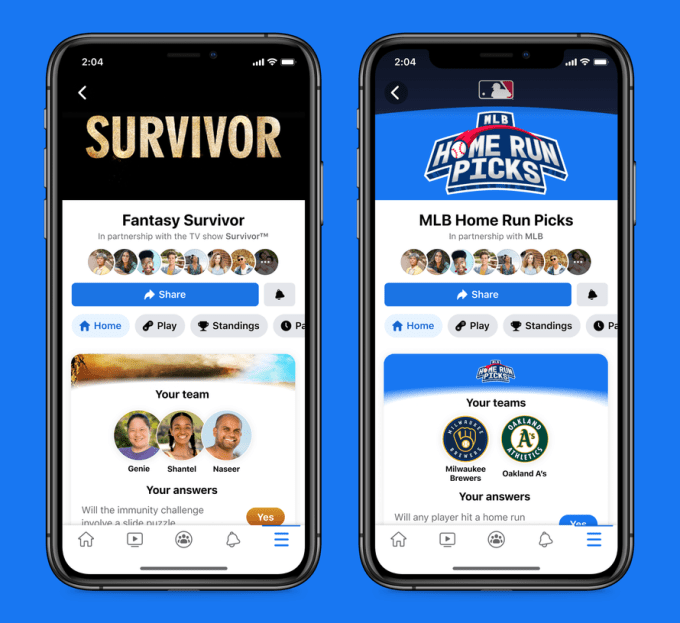

Facebook is getting into fantasy sports and other types of fantasy games. The company this morning announced the launch of Facebook Fantasy Games in the U.S. and Canada on the Facebook app for iOS and Android. Some games are described as “simpler” versions of the traditional fantasy sports games already on the market, while others allow users to make predictions associated with popular TV series, like “Survivor” or “The Bachelorette.”

The first game to launch is Pick & Play Sports, in partnership with Whistle Sports, where fans get points for correctly predicting the winner of a big game, the points scored by a top player or other events that unfold during the match. Players can also earn bonus points for building a streak of correct predictions over several days. This game is arriving today.

Image Credits: Facebook

In the months ahead, it will be followed by other games in sports, TV and pop culture, including Fantasy Survivor, where players choose a set of castaways from the popular CBS TV show to join their fantasy team and Fantasy “The Bachelorette,” where fans will pick a group of men from the suitors vying for the Bachelorette’s heart and get points based on their actions and events that take place during the show. Other upcoming sports-focused games include MLB Home Run Picks, where players pick the team that they think will hit the most home runs, and LaLiga Winning Streak, where fans predict the team that will win that day.

In addition to top players being featured on leaderboards, games have a social component for those who want to play with friends.

Image Credits: Facebook

Players can create their own fantasy league with friends to compete with one another or against other fans, either publicly or privately. League members can compare scores with each other and will have a place where they can share picks, reactions and comments. This league area resembles a private group on Facebook, as it offers its own compose box for posting only to members, and its own dedicated feed. However, the page is designed to support groups with specific buttons to “play” or view the “leaderboard,” among others.

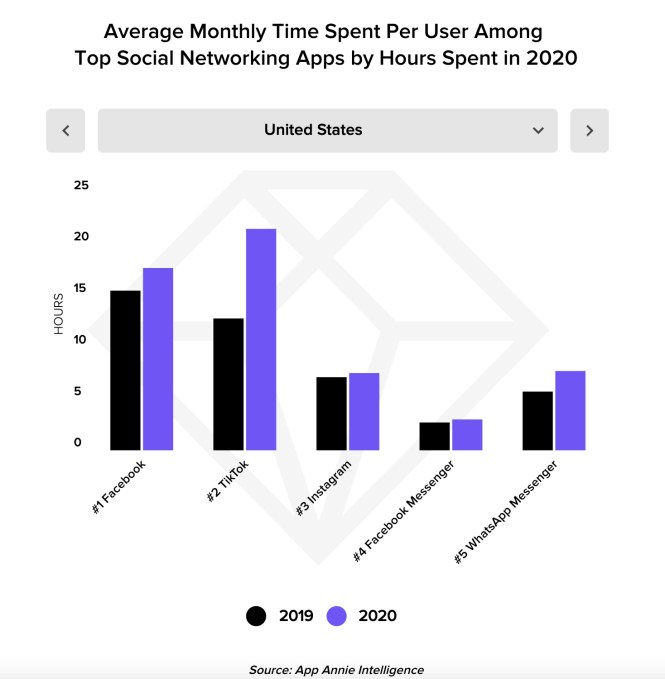

The addition of fantasy games could help Facebook increase the time users spent on its app at a time when the company is facing significant competition in social, namely from TikTok. According to App Annie, the average monthly time spent per user in TikTok grew faster than other top social apps in 2020, including by 70% in the U.S., surpassing Facebook.

Facebook had dabbled with the idea of becoming a second screen companion for live events in the past, but in a different way than fantasy sports and games. Instead, its R&D division tested Venue, which worked as a way for fans to comment on live events which were hosted in the app by well-known personalities.

The company has several other gaming investments, as well, including through its cloud gaming service on the desktop web and Android, its Games tab for streamers, and its VR company, Oculus.

The new league games will be available from the bookmark menu on the mobile app and in News Feed through notifications.

Powered by WPeMatico

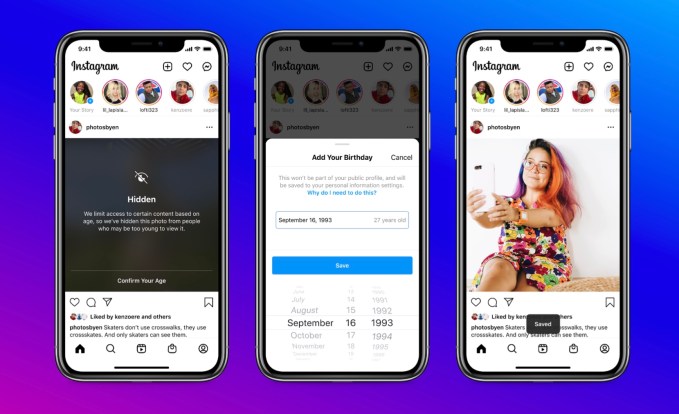

Instagram will require users to provide their birthday

Instagram will begin prodding users to share their birthday with the service, if they haven’t already done so. The company today announced it will now start popping up a notification that asks you to add your birthday to “personalize your experience.” But the prompt can only be dismissed a handful of times before becoming a requirement. The move is a part of Instagram’s larger goal to create new safety features aimed at younger users, the company explains. This includes the teen privacy protections introduced earlier this year, as well as Instagram’s longer-term plan to launch a version of its service aimed at users under the age of 13.

This March, Instagram rolled out new features that made it more difficult for adults to contact teens through its app. Then in July, the company announced a larger series of changes to the default settings for new users under the age of 16. It will now default these users’ accounts to “private” and limit their accounts from being suggested elsewhere in the app. It also now restricts adults whose accounts are flagged as “potentially suspicious” from being able to reach out to other minors or interact with their posts.

Starting this week, Instagram says users who have not yet shared their birthday will begin to see pop-up notifications when they open the Instagram app.

These notifications will appear a handful of times, but at some point, users will no longer be able to dismiss the message by tapping “Not Now.” Instead, everyone will ultimately be required to share their birthday to continue to use Instagram.

The company will also now request you to share your birthday information when you come across a post with a warning screen. These screens, which hide content that’s flagged as sensitive or graphic, are not new. But Instagram has never before asked for a user’s birthday before displaying the hidden content.

Image Credits: Instagram

The birthday entry form itself is not complex. You simply scroll to choose the month, day and year of your birthday.

Of course, kids are commonly known to lie on these entry forms in order to bypass restrictions when signing up for apps. On this front, Instagram has developed AI technology to help it identify accounts were kids may have lied. For instance, it may be able to infer someone’s birthday based on comments left on “Happy Birthday” posts, where the user’s age may be referenced. The company also hints at further plans in this area, noting how it will later require users to verify their age when Facebook’s technology determines a mismatch between the age the user submitted and what appears to be their real age, based on other signals.

That technology is still in the “early stages,” says Instagram, but will involve a menu of options that will allow someone to verify their age.

The need to have users’ birthdays on hand isn’t only meant to power the recently launched teen protection features. Instagram is also working to bring its app to younger users — a decision that’s been met with a hostile response from legislators and consumer advocacy groups alike. In addition, age remains an important data point for ad targeting. Even as Instagram pulled back on the ability for marketers to target teens using interest data or their activity on other apps, it will continue to allow ad targeting based on age, gender and location across age groups.

The company is now one of several to have rolled out added protections for younger teen users, ahead of regulations that would force them to do so. Over the course of this year, TikTok, YouTube and Google have also announced changes to how younger teens can use their services and how they can be targeted by ads, in anticipation of a regulatory crackdown. While each has crafted its own set of teen safety features independently, the changes have largely addressed making the default settings for new teenage users more restrictive.

Instagram says the new birthday pop-up notifications will begin to appear this week on the mobile app and will continue to roll out over the weeks ahead to reach more users.

Powered by WPeMatico

Today’s real story: The Facebook monopoly

Facebook is a monopoly. Right?

Mark Zuckerberg appeared on national TV today to make a “special announcement.” The timing could not be more curious: Today is the day Lina Khan’s FTC refiled its case to dismantle Facebook’s monopoly.

To the average person, Facebook’s monopoly seems obvious. “After all,” as James E. Boasberg of the U.S. District Court for the District of Columbia put it in his recent decision, “No one who hears the title of the 2010 film ‘The Social Network’ wonders which company it is about.” But obviousness is not an antitrust standard. Monopoly has a clear legal meaning, and thus far Lina Khan’s FTC has failed to meet it. Today’s refiling is much more substantive than the FTC’s first foray. But it’s still lacking some critical arguments. Here are some ideas from the front lines.

To the average person, Facebook’s monopoly seems obvious. But obviousness is not an antitrust standard.

First, the FTC must define the market correctly: personal social networking, which includes messaging. Second, the FTC must establish that Facebook controls over 60% of the market — the correct metric to establish this is revenue.

Though consumer harm is a well-known test of monopoly determination, our courts do not require the FTC to prove that Facebook harms consumers to win the case. As an alternative pleading, though, the government can present a compelling case that Facebook harms consumers by suppressing wages in the creator economy. If the creator economy is real, then the value of ads on Facebook’s services is generated through the fruits of creators’ labor; no one would watch the ads before videos or in between posts if the user-generated content was not there. Facebook has harmed consumers by suppressing creator wages.

A note: This is the first of a series on the Facebook monopoly. I am inspired by Cloudflare’s recent post explaining the impact of Amazon’s monopoly in their industry. Perhaps it was a competitive tactic, but I genuinely believe it more a patriotic duty: guideposts for legislators and regulators on a complex issue. My generation has watched with a combination of sadness and trepidation as legislators who barely use email question the leading technologists of our time about products that have long pervaded our lives in ways we don’t yet understand. I, personally, and my company both stand to gain little from this — but as a participant in the latest generation of social media upstarts, and as an American concerned for the future of our democracy, I feel a duty to try.

The problem

According to the court, the FTC must meet a two-part test: First, the FTC must define the market in which Facebook has monopoly power, established by the D.C. Circuit in Neumann v. Reinforced Earth Co. (1986). This is the market for personal social networking services, which includes messaging.

Second, the FTC must establish that Facebook controls a dominant share of that market, which courts have defined as 60% or above, established by the 3rd U.S. Circuit Court of Appeals in FTC v. AbbVie (2020). The right metric for this market share analysis is unequivocally revenue — daily active users (DAU) x average revenue per user (ARPU). And Facebook controls over 90%.

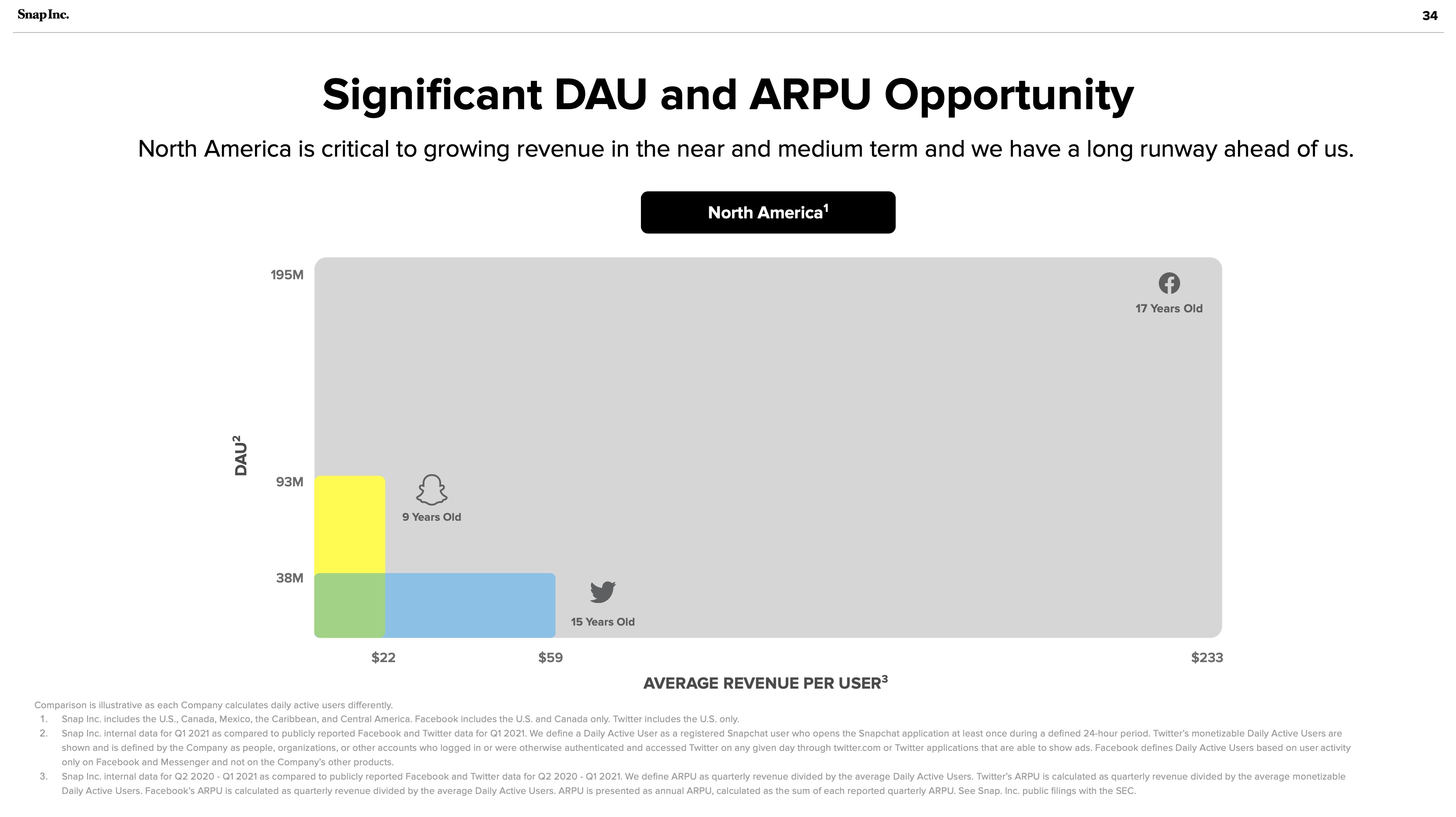

The answer to the FTC’s problem is hiding in plain sight: Snapchat’s investor presentations:

Snapchat July 2021 investor presentation: Significant DAU and ARPU Opportunity. Image Credits: Snapchat

This is a chart of Facebook’s monopoly — 91% of the personal social networking market. The gray blob looks awfully like a vast oil deposit, successfully drilled by Facebook’s Standard Oil operations. Snapchat and Twitter are the small wildcatters, nearly irrelevant compared to Facebook’s scale. It should not be lost on any market observers that Facebook once tried to acquire both companies.

The market Includes messaging

The FTC initially claimed that Facebook has a monopoly of the “personal social networking services” market. The complaint excluded “mobile messaging” from Facebook’s market “because [messaging apps] (i) lack a ‘shared social space’ for interaction and (ii) do not employ a social graph to facilitate users’ finding and ‘friending’ other users they may know.”

This is incorrect because messaging is inextricable from Facebook’s power. Facebook demonstrated this with its WhatsApp acquisition, promotion of Messenger and prior attempts to buy Snapchat and Twitter. Any personal social networking service can expand its features — and Facebook’s moat is contingent on its control of messaging.

The more time in an ecosystem the more valuable it becomes. Value in social networks is calculated, depending on whom you ask, algorithmically (Metcalfe’s law) or logarithmically (Zipf’s law). Either way, in social networks, 1+1 is much more than 2.

Social networks become valuable based on the ever-increasing number of nodes, upon which companies can build more features. Zuckerberg coined the “social graph” to describe this relationship. The monopolies of Line, Kakao and WeChat in Japan, Korea and China prove this clearly. They began with messaging and expanded outward to become dominant personal social networking behemoths.

In today’s refiling, the FTC explains that Facebook, Instagram and Snapchat are all personal social networking services built on three key features:

- “First, personal social networking services are built on a social graph that maps the connections between users and their friends, family, and other personal connections.”

- “Second, personal social networking services include features that many users regularly employ to interact with personal connections and share their personal experiences in a shared social space, including in a one-to-many ‘broadcast’ format.”

- “Third, personal social networking services include features that allow users to find and connect with other users, to make it easier for each user to build and expand their set of personal connections.”

Unfortunately, this is only partially right. In social media’s treacherous waters, as the FTC has struggled to articulate, feature sets are routinely copied and cross-promoted. How can we forget Instagram’s copying of Snapchat’s stories? Facebook has ruthlessly copied features from the most successful apps on the market from inception. Its launch of a Clubhouse competitor called Live Audio Rooms is only the most recent example. Twitter and Snapchat are absolutely competitors to Facebook.

Messaging must be included to demonstrate Facebook’s breadth and voracious appetite to copy and destroy. WhatsApp and Messenger have over 2 billion and 1.3 billion users respectively. Given the ease of feature copying, a messaging service of WhatsApp’s scale could become a full-scale social network in a matter of months. This is precisely why Facebook acquired the company. Facebook’s breadth in social media services is remarkable. But the FTC needs to understand that messaging is a part of the market. And this acknowledgement would not hurt their case.

The metric: Revenue shows Facebook’s monopoly

Boasberg believes revenue is not an apt metric to calculate personal networking: “The overall revenues earned by PSN services cannot be the right metric for measuring market share here, as those revenues are all earned in a separate market — viz., the market for advertising.” He is confusing business model with market. Not all advertising is cut from the same cloth. In today’s refiling, the FTC correctly identifies “social advertising” as distinct from the “display advertising.”

But it goes off the deep end trying to avoid naming revenue as the distinguishing market share metric. Instead the FTC cites “time spent, daily active users (DAU), and monthly active users (MAU).” In a world where Facebook Blue and Instagram compete only with Snapchat, these metrics might bring Facebook Blue and Instagram combined over the 60% monopoly hurdle. But the FTC does not make a sufficiently convincing market definition argument to justify the choice of these metrics. Facebook should be compared to other personal social networking services such as Discord and Twitter — and their correct inclusion in the market would undermine the FTC’s choice of time spent or DAU/MAU.

Ultimately, cash is king. Revenue is what counts and what the FTC should emphasize. As Snapchat shows above, revenue in the personal social media industry is calculated by ARPU x DAU. The personal social media market is a different market from the entertainment social media market (where Facebook competes with YouTube, TikTok and Pinterest, among others). And this too is a separate market from the display search advertising market (Google). Not all advertising-based consumer technology is built the same. Again, advertising is a business model, not a market.

In the media world, for example, Netflix’s subscription revenue clearly competes in the same market as CBS’ advertising model. News Corp.’s acquisition of Facebook’s early competitor MySpace spoke volumes on the internet’s potential to disrupt and destroy traditional media advertising markets. Snapchat has chosen to pursue advertising, but incipient competitors like Discord are successfully growing using subscriptions. But their market share remains a pittance compared to Facebook.

An alternative pleading: Facebook’s market power suppresses wages in the creator economy

The FTC has correctly argued for the smallest possible market for their monopoly definition. Personal social networking, of which Facebook controls at least 80%, should not (in their strongest argument) include entertainment. This is the narrowest argument to make with the highest chance of success.

But they could choose to make a broader argument in the alternative, one that takes a bigger swing. As Lina Khan famously noted about Amazon in her 2017 note that began the New Brandeis movement, the traditional economic consumer harm test does not adequately address the harms posed by Big Tech. The harms are too abstract. As White House advisor Tim Wu argues in “The Curse of Bigness,” and Judge Boasberg acknowledges in his opinion, antitrust law does not hinge solely upon price effects. Facebook can be broken up without proving the negative impact of price effects.

However, Facebook has hurt consumers. Consumers are the workers whose labor constitutes Facebook’s value, and they’ve been underpaid. If you define personal networking to include entertainment, then YouTube is an instructive example. On both YouTube and Facebook properties, influencers can capture value by charging brands directly. That’s not what we’re talking about here; what matters is the percent of advertising revenue that is paid out to creators.

YouTube’s traditional percentage is 55%. YouTube announced it has paid $30 billion to creators and rights holders over the last three years. Let’s conservatively say that half of the money goes to rights holders; that means creators on average have earned $15 billion, which would mean $5 billion annually, a meaningful slice of YouTube’s $46 billion in revenue over that time. So in other words, YouTube paid creators a third of its revenue (this admittedly ignores YouTube’s non-advertising revenue).

Facebook, by comparison, announced just weeks ago a paltry $1 billion program over a year and change. Sure, creators may make some money from interstitial ads, but Facebook does not announce the percentage of revenue they hand to creators because it would be insulting. Over the equivalent three-year period of YouTube’s declaration, Facebook has generated $210 billion in revenue. one-third of this revenue paid to creators would represent $70 billion, or $23 billion a year.

Why hasn’t Facebook paid creators before? Because it hasn’t needed to do so. Facebook’s social graph is so large that creators must post there anyway — the scale afforded by success on Facebook Blue and Instagram allows creators to monetize through directly selling to brands. Facebooks ads have value because of creators’ labor; if the users did not generate content, the social graph would not exist. Creators deserve more than the scraps they generate on their own. Facebook suppresses creators’ wages because it can. This is what monopolies do.

Facebook’s Standard Oil ethos

Facebook has long been the Standard Oil of social media, using its core monopoly to begin its march upstream and down. Zuckerberg announced in July and renewed his focus today on the metaverse, a market Roblox has pioneered. After achieving a monopoly in personal social media and competing ably in entertainment social media and virtual reality, Facebook’s drilling continues. Yes, Facebook may be free, but its monopoly harms Americans by stifling creator wages. The antitrust laws dictate that consumer harm is not a necessary condition for proving a monopoly under the Sherman Act; monopolies in and of themselves are illegal. By refiling the correct market definition and marketshare, the FTC stands more than a chance. It should win.

A prior version of this article originally appeared on Substack.

Powered by WPeMatico