Extra Crunch

Auto Added by WPeMatico

Auto Added by WPeMatico

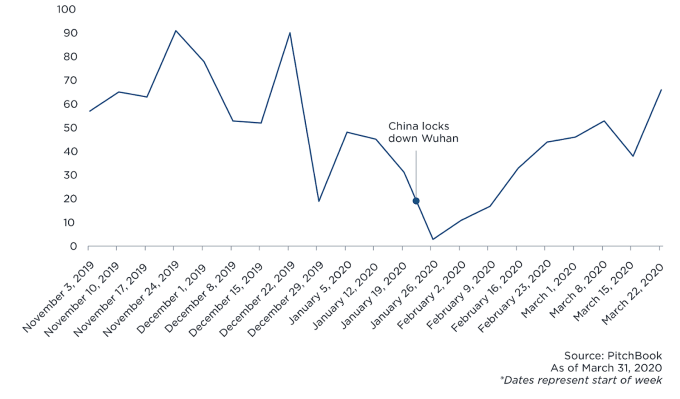

For the past month, VC investment pace seems to have slacked off in the U.S., but deal activities in China are picking up following a slowdown prompted by the COVID-19 outbreak.

According to PitchBook, “Chinese firms recorded 66 venture capital deals for the week ended March 28, the most of any week in 2020 and just below figures from the same time last year,” (although 2019 was a slow year). There is a natural lag between when deals are made and when they are announced, but still, there are some interesting trends that I couldn’t help noticing.

While many U.S.-based VCs haven’t had a chance to focus on new deals, recent investment trends coming out of China may indicate which shifts might persist after the crisis and what it could mean for the U.S. investor community.

Image Credits: PitchBook

Powered by WPeMatico

It would be easy to assume that Verizon’s purchase last week of video-conferencing tool BlueJeans was an opportunistic move to capitalize on the sudden shift to remote work, but the ball began rolling last June and has implications far beyond current work-from-home requirements.

The video-chat darling of the moment is Zoom, but BlueJeans is considered by many to be the enterprise tool of choice. The problem, it seems, is that it had grown as far as it could on its own and went looking for a larger partner to help it reach the next level.

BlueJeans started working with Verizon (which owns this publication) as an authorized reseller before the talks turned toward a deeper relationship that culminated in the acquisition. Assuming the deal passes regulatory scrutiny, Verizon will use its emerging 5G technology to produce much more advanced video-conferencing scenarios.

We spoke to the principals involved in this deal and several industry experts to get a sense of where this could lead. As with any large company buying a startup, outcomes are uncertain; sometimes the acquired company gets lost in the larger corporate bureaucracy, and sometimes additional resources will help grow the company much faster than it could have on its own.

Powered by WPeMatico

Welcome to a look back at the past week in security and what it means for you. Each week we’ll look at the big news of the week and why it matters.

What will the world look like after the coronavirus pandemic subsides?

Some of us are now in our fifth week of sheltering in place, but there’s no fixed end-date in sight. We’ve gone from a period of confusion and concern to testing and mitigation. Now we’re starting to look ahead at the world post-coronavirus. Things still have to get done. But how do we regain a semblance of normality in the middle of a pandemic?

Tech can be the answer but it’s not a panacea; Apple and Google have explained more about their contact tracing efforts to help better understand the spread of the virus seems promising. But privacy concerns and worries that the system could be abused have raised justified concerns. On the other hand, with a U.S. presidential election slated for later this year, many experts want tech out of the picture in favor of a secure solution that uses paper ballots.

Will tech save the day, or will it kick us while we’re down? Let’s dive in.

This year’s U.S. presidential election will still go ahead — it’s in the constitution as an immutable fact — but a pandemic throws a wrench in the works.

But security experts say electronic voting isn’t secure or resilient enough to protect from foreign interference. Even the more established mobile voting offerings have been shown to be deeply flawed.

Powered by WPeMatico

Welcome back to This Week in Apps, the Extra Crunch series that recaps the latest OS news, the applications they support and the money that flows through it all.

The app industry is as hot as ever, with a record 204 billion downloads in 2019 and $120 billion in consumer spending in 2019, according to App Annie’s “State of Mobile” annual report. People are now spending 3 hours and 40 minutes per day using apps, rivaling TV. Apps aren’t just a way to pass idle hours — they’re a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus.

In this Extra Crunch series, we help you keep up with the latest news from the world of apps, delivered on a weekly basis.

This week we’re continuing to look at how the coronavirus outbreak is impacting the world of mobile applications, including a dig into Houseparty’s big surge, layoffs at VSCO, Google’s launch of a “Teacher Reviewed” tag, Bumble’s virtual dating, plus changes to Instagram in support of small business and live streaming, among other things. Also this week, Google changed its Play Store guidelines, TikTok launched parental controls, a report suggested Apple may be expanding its Search Ads and more.

Powered by WPeMatico

Before the COVID-19 pandemic shook up the world and reshaped the economy, Boston was quietly setting records.

According to new venture data compiled by TechCrunch, the region set what was at least a local maximum in venture capital raised in the space of a single quarter in Q1 2020.

But while Boston’s startup market announced a number of huge rounds that bolstered its total venture dollars raised in the first quarter, there were signs of weakness: Deal volume was its best since Q2 2019, according to a set of data compiled and released by PwC and CB Insights, but was still a little under the pace set in 2018.

So Boston’s startups raised lots of money, but couldn’t match prior highs when it came to the number of checks written. And those results were largely recorded before COVID-19 shuttered the city. Since then, we’ve seen a number of area startups lay off staff, something we explored last week.

Now, with fresh data in hand, we can take a closer look at the city’s first quarter of 2020. To better understand what we’re unpacking, we asked a number of local venture capitalists to weigh in. Let’s look back at Boston’s Q1 as we stride into Q2 with the help of Venture Lane, .406 Ventures, Volition Capital and Flybridge Capital Partners.

Starting with a programming note is counter-flow, but bear with us. TechCrunch is starting a regular, monthly series on Boston and its startup market. This is a second prelude of sorts. Normally we’d hold news and interviews for a later date so that we’d have plenty of material for a column. In the face of relentless change, however, we didn’t want to hold off on reporting and synthesizing new information. When things are more normal, our pace will follow.

Per PwC and CB Insights, here’s the last few quarters of data, along with a few yearly totals to draw you the picture we can now see:

Powered by WPeMatico

As silently and swiftly as it has devastated families and communities around the world, COVID-19 has also left many startups gasping for air. Emerging companies with strong 2020 revenue forecasts have seen their high-confidence plans reduced by 60%-80% in a matter of days. Even in the best of times, startups must reach value-unlocking milestones to successfully raise new capital. But today, a globally synchronized halt to business activity has made irrelevant normal benchmarks for financing rounds.

Obtaining payroll support from the recently enacted special government programs for small businesses will not resolve the cascading problems startups are grappling with, regardless of whether or not they are VC-backed.

Product development roadmaps in many innovation-driven industries are changing in ways that may permanently alter a company’s future strategic direction. Merger and acquisition discussions are being shelved. Normal financing rounds, in process and contemplated, are contracting or being abandoned altogether. Many venture funds, including corporate venture programs, have unilaterally “taken a pause” to reevaluate the radically changing landscape for their early-stage company portfolios.

I last experienced this phenomenon in the aftermath of the Great Technology Bubble: 2002-2003. And all signs show that we are at the beginning of a new round of punitive “incentives” for venture investors to keep their companies alive.

Several of my current portfolio companies have recently proposed “emergency bridge” convertible note financings of between $5 million and $15 million, each featuring a painful feature for non-participants: multiple liquidation preferences benefiting only the new money above 3x, with discounts greater than 20% on conversion in a new equity financing. Of course, these financings are open to both existing and new investors. But the likelihood of another round is actually diminished by this type of structure.

Powered by WPeMatico

Marty Pichinson gets called a lot of things: Silicon Valley’s undertaker, its terminator, a grave digger. These aren’t meant as slights; Pichinson is the founder of Sherwood Partners, a restructuring firm that Bay Area venture firms frequently turn to when they need someone to help sell off the assets of startups they have funded. The idea is to return at least some money to the company’s creditors and, if anything is left, to the VCs, too.

We last checked in with Pichinson almost exactly three years ago when the startup world was humming along. Even then, because of the sheer number of companies that get funded — and thus the number of startups that invariably don’t make it — Sherwood Partners was helping to wind down two to four companies a week.

Now, as he told us in conversation last week, it’s winding down two to three companies every day.

So who is shutting down, how does it all work and what can VCs expect to get in terms of a return in the age of the coronavirus?

Right now, Pichinson says the shutdowns are across verticals and across stages. “We’re in companies that raised $10 million to $25 million, to companies that raised up to $1.5 billion. It doesn’t matter what size they are; when they come to us, they’re all broke. If we’re closing it down to clean up and monetize what we can, they are basically in the same position, whether they raised $20 million or they were once a billion-dollar business.”

Powered by WPeMatico

Adobe was scheduled to hold its annual conference in Las Vegas two weeks ago, but the coronavirus pandemic forced the company to make alternate plans. In less than a month, its events team shifted venues for the massive conference, not once, but twice as the severity of the situation became clear.

This year didn’t just involve Adobe Summit itself. To make things more interesting, it was also hosting Magento Imagine as a separate conference within a conference at the same time. (Adobe bought Magento in 2018 for $1.6 billion.)

Originally, Adobe had more than 500 sessions planned across four venues on the Las Vegas Strip, with more than 23,000 attendees expected. Combining all of the sponsors, partners and Adobe personnel, it involved more than 40,000 hotel rooms.

Once it became clear that such a large event couldn’t happen, the company reimagined the conference as a fully digital experience.

VP of Experience Marketing Alex Amado is in charge of planning Adobe Summit, a tall task under normal circumstances.

“Planning Summit is a year-round endeavor,” he said. “Literally within weeks of finishing one of those Las Vegas events we are starting on the next one, and some of the work actually is on an 18 or 24-month cycle because we have those long-term hotel contracts and all of that stuff.

“For the last 12 months, basically, we had people who were working on what we now call Plan A — and we didn’t know that we needed a Plan B and Plan C — and the original event was going to be our biggest yet.”

2019 Adobe Summit stage in Las Vegas. Photo: Ron Miller/TechCrunch

After the team began to wonder in January if the virus would force them to change how they deliver the conference, they started building contingency plans in earnest, Amado said. “As we got into February, things started looking a little scarier, and it very quickly escalated to the point where we were talking really seriously about Plan B.”

Powered by WPeMatico

There are early signs that media will be one of many industries to take a huge blow from the COVID-19 pandemic, with sharp declines in ad revenue and significant layoffs. Podcasting is unlikely to be an exception; Podtrac recently reported that downloads have fallen 10% since the beginning of March, while unique listeners fell by 20%.

A different picture emerged when I spoke to Ross Adams, CEO of podcast advertising company Acast, which works with both bedroom podcasters and large publishers like the BBC and PBS NewsHour.

Adams said listenership isn’t down — it’s just that audiences have changed when they’re listening and what they’re listening to, with Acast seeing its largest weekends ever in recent weeks. And plenty of people want to start new podcasts; signups for the Acast Open platform increased 49% month-over-month in March.

“What we’re seeing now is an opportunity for people to discover podcasting as a medium,” he said. “And once you discover it, you stick with it.”

Advertising may be a separate issue, with Adams admitting that the downturn is likely to affect “every business that has the majority of their revenue from ads.” But even then, he sees opportunity as marketing dollars move from traditional industries like radio and out-of-home advertising.

We also discussed Acast’s financials, the podcast discovery process and tips for new podcasters. Read a transcript of our conversation, edited for length and clarity, below.

TechCrunch: Let’s start with the good news. One of the prompts for this conversation is the fact that you guys announced some financial numbers — you doubled the revenue last year to $38 million. So first of all, congratulations.

Ross Adams: Thank you.

And secondly, there’s a lot of different factors at play and different conversations about podcasting breaking through in 2019. But when you look back, what do you see as the biggest factors that contributed to your growth?

Powered by WPeMatico

Consumption of all types of kids-focused digital media has soared with a large portion of the world’s children home from school right now. At all times of day, children are playing games, watching shows and using edtech tools — often in a social context with friends online.

This only accelerates the normalization of virtual spaces as social hubs, and it makes protection of children’s data a more pressing concern for entertainment and communications platforms (like Zoom) that haven’t built a product specific to this demographic.

During last week’s TechCrunch Live session on the state of kids’ media, I had an engaging discussion with three industry leaders about how COVID-19 is impacting companies in the space and what long-term changes could result from it:

Below is the recording of our conversation as well as the full transcript (with minor edits for clarity):

TechCrunch: The COVID-19 crisis has put families all at home together and changed a lot for your businesses. I want to set context first by looking at the couple years leading up to this. What have been the two biggest changes in the kids’ media space from your perspectives?

Craig Donato: One huge shift that we’ve seen over the last five years is the evolution of games into social places — experiences where kids hang out with their friends, do things with them versus these narrow competitive environments. We really see Roblox as a medium of shared experience. That’s a pretty significant shift, and it’s really benefited platforms like Roblox, but also Minecraft and Fortnite.

Powered by WPeMatico