Extra Crunch

Auto Added by WPeMatico

Auto Added by WPeMatico

Matt Ocko, co-founder of venture firm Data Collective (DCVC), was among a small group of VCs viewed as alarmists when they began tweeting about the coronavirus’s imminent appearance in the U.S. back in January.

In retrospect, those individuals were prescient, so we spoke with Ocko last week about why he was so certain the U.S. was about to get walloped by COVID-19, and asked how some of the startups in DCVC’s portfolio — which has long had a strong biotech focus — are trying to get us back to a state of normalcy.

This conversation has been edited for length.

TechCrunch: You were tweeting about COVID-19 back in January; I almost canceled a flight out of San Francisco because of your [expressed concern about a flight bound for SFO from Wuhan, China]. What did you see that the rest of us missed?

Matt Ocko: My family has been working with the Chinese government at a reasonably high level since the late 1970s, starting with my dad, and I kind of grew up in that environment. And at a relatively young age, as a professional [in the 1990s], I started pro bono helping my dad, who’s a Chinese legal expert, on things like constructing the laws around China’s Nasdaq equivalent, its stock markets, the joint dollar-renminbi investment legislation, advice on technology development and venture capital development.

I’m not an anti-China hawk by any means. But I do have an understanding of some of the idiosyncrasies of Chinese culture reflected in its government, the same way every country has its idiosyncrasies.

[In China’s case], it’s a focus on face and reputation and extreme sensitivity to negative perception or shame or humiliation at every level of government and culture. And so there’s [an] unfortunate trend — and not a universal one — for people to manage upwards, especially in the government, and tell their higher-ups what they want to hear to avoid shame, to avoid the loss of reputation and to kick the can down the road or hope that circumstances on the ground change favorably in the face of denial or equivocation.

Powered by WPeMatico

As a small business owner, I was excited to learn about the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act that offers low-interest loans to firms impacted by the COVID-19 pandemic. However, as I read through the details and began to apply, it became clear that this legislation — while well-intentioned — may not be enough to help many SMBs and startups.

Here’s a quick recap of my experience.

First and foremost: You need to act swiftly. Emergency Economic Injury Grant and Economic Injury Disaster Loan programs included in the CARES Act function on a first-come, first-served basis, and are funded from a limited pool of resources.

I began my company’s application process by submitting our EIDL and EEIG applications through the SBA website. This was easy, if tedious. It took about two hours to complete the necessary online forms and about two seconds to click the EEIG checkbox. Submission was seamless, but I haven’t received any further communication from the SBA since completing my application, which is a bit confusing — EEIG funds are supposed to be dispersed within 3-5 days of the submission date.

However, I know there’s been a huge volume of submissions recently and this must be exceptionally difficult to handle. I look forward to any email correspondence or updates from the SBA that might give me — and other applicants — an updated estimate of the expected dispersal timeline.

Powered by WPeMatico

Prompted by Jeff Bezos’s plans to test all Amazon employees for the virus that causes COVID-19, we wondered whether employers can mandate employee testing, regardless of symptoms. The issue pits public safety against personal privacy, but limited testing availability has rendered the question somewhat moot.

But as the World Health Organization and U.S. Centers for Disease Control and Prevention have noted, asymptomatic COVID-19 carriers can spread the virus without realizing they’re infected. To learn more about workers’ rights in this arena, we spoke to Tricia Bozyk Sherno, counsel at Debevoise & Plimpton, who focuses on employment and general commercial litigation.

The answer, for now, is not entirely straightforward, though updates from the U.S. Equal Employment Opportunity Commission could make the situation clearer going forward as more tests are made available and state governments begin pushing to reopen businesses.

Sherno offered a fair amount of insight into the EEOC’s updated guidance and made some predictions about how things may look for both employers and workers going forward.

TechCrunch: Prior to the COVID-19 pandemic, what sorts of laws governed an employer’s ability to test employees for infectious diseases?

Tricia Bozyk Sherno: Covered employers (employers with 15 or more employees) must comply with the requirements of the Americans with Disabilities Act (ADA), which limits an employer’s ability to make disability-related inquiries or require medical examinations. (Note that certain states may also have similar statutes in place.) Generally, disability-related inquiries and medical examinations are prohibited by the ADA except in limited circumstances. A “medical examination” is a procedure or test that seeks information about an individual’s physical or mental impairments or health — so infectious disease testing would fall into this category.

Powered by WPeMatico

For the vast majority of startup founders who were planning their capital raise in Q1 2020, the COVID-19 blow was so dramatic and sweeping, we cannot see all its effects at once.

One big question on the minds of most founders: How should we plan our next raise in terms of timing, valuation and amounts?

Sarah Guo, partner at Greylock Partners, says the fundraising environment has slowed down significantly, but founders who have built ties with VCs via informal coffee updates and check-ins are at a clear advantage. “Early-stage bets require relationship-building,” says Guo, who has been investing in seed through Series B rounds.

Ram Shanmugam, founder and CEO of AutonomIQ*, a seed-stage code and process automation company, has been strengthening his relationships. For a company that has low operating expenses and a community of 600,000 developers, he says he is not fazed. “Our automation code brings efficiencies and in fact, we have nine inbound leads in Q2. Having said that, we are being realistic at the pace at which we can close these contracts.”

Similarly, Fred Blumer, who exited Hughes Telematics at an enviable $750 million, says he is taking a more pragmatic approach to the Series A raise for his new company, Mile Auto. “We expect to have a 5x growth in our business in 2020, even after adjusting for COVID,” he said. “Our pay-per-mile insurance is a great fit for people who are driving less.” Because so many drivers are sheltering in place, legacy insurance companies are refunding hundreds of millions of dollars to customers, which offers an advantage (and an opportunity) to a startup like his.

“But we need to be patient and mindful. While our families, health and safety are top priority, we are staying focused on our customers,” Blumer said. “Insurtech is a resilient arena, and in my past company we raised $100 million, so working with investors has never been a challenge. Keeping up with growth and perfecting the customer experience are what keep us up at night.” He said he plans to get out in the market after investor confidence returns.

Which may be a good idea, considering Jason Lemkin’s Twitter survey, where only 32% of respondents said they plan to deploy the same amount of capital as in the past. But another 30% are on the opposite end of the spectrum, deploying 40% to 60% less capital.

Powered by WPeMatico

Earlier this week, we kicked off our Extra Crunch Live series with an interesting chat with Cowboy’s Aileen Lee and Ted Wang. Today, we will be back at 3 p.m. PST/6 p.m. EST/10 p.m. GMT with a new guest: Charles Hudson, the general partner of Precursor Ventures.

Extra Crunch members will find an AddEvent link below to drop the details directly into their calendar and folks who want to participate directly can hit up the Zoom link (also below). We’ll ask as many audience questions as we can, so please make them sharp — no pitches, please.

Charles Hudson founded Precursor Ventures to invest in pre-seed and seed-stage companies. Earlier this year, the firm filed paperwork to put together a $40 million third fund after previously raising two main funds and one $10 million “opportunity” fund.

As we await hard and accurate numbers on how COVID-19 is impacting fundraising, we’ll ask Hudson to walk us through the changes he has seen and will cover some basics: The best way to pitch him, what his to-do list looks like these days and if the pandemic has made Precursor newly bullish or bearish on certain sectors.

Then, we’ll get much nerdier: Will we see the number of party rounds fall further now that it’s harder to gather investors in real life? Do you think we’ll see pre-seed raises ask for more ownership terms? And what is the latest with the wacky world of early-stage valuations?

There’s a lot to talk about. And we haven’t even mentioned YC’s pro rata change yet.

After Hudson, we have a stacked lineup of Extra Crunch live guests, including Mitch and Freada Kapor, Mark Cuban, Roelof Botha and Kirsten Green, with more to be announced soon.

You can find information below with details for joining today’s discussion, as well as an AddEvent link to put the details directly onto your calendar.

Sign up for Extra Crunch to get access to all these episodes where you can view the talks live, participate in the Q&A with industry leaders and watch later on-demand if you can’t make the live timing. You can also see the chat via YouTube below. Talk soon!

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

While some U.S. investors might have taken comfort from China’s rebound, we still find ourselves in the early innings of this period of uncertainty.

Some epidemiologists have estimated that COVID-19 cases will peak in April, but PitchBook reports that dealmaking was down -26% in March, compared to February’s weekly average. The decline is likely to continue in coming weeks — many of the deals that closed last month were initiated before the pandemic, and there is a lag between when deals are made and when they are announced.

However, there’s still hope. A recent report concluded that because valuations are lower and there’s less competition for deals, “the best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery.” There are countless examples from the 2008 recession, including many highly valued VC-backed businesses such as WhatsApp, Venmo, Groupon, Uber, Slack and Square. Other early-stage VCs seem to have arrived at a similar conclusion.

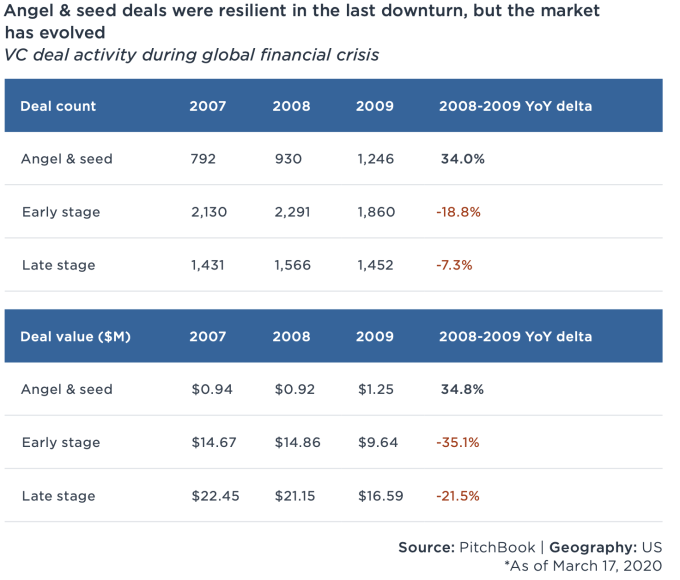

Also, early-stage investing seems more resilient. During the last recession, angel and seed activity increased 34% as interest in the stage boomed during a period of prolonged growth.

Image Credits: PitchBook (opens in a new window)

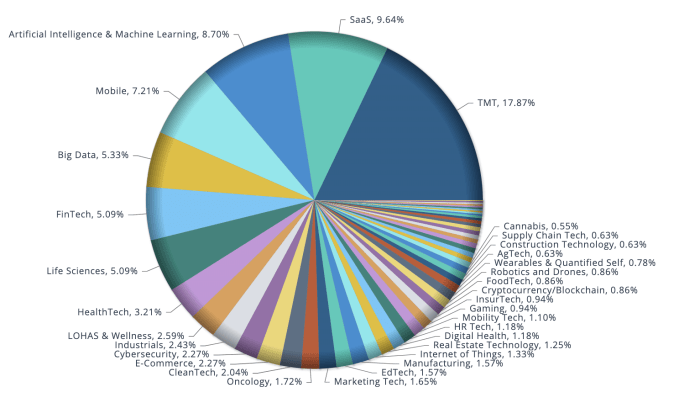

Furthermore, there is still capital to be deployed in categories that interested investors before the pandemic, which may set the new order in a post-COVID-19 world. According to data provider Preqin Ltd., VC dry powder rose for a seventh consecutive year to roughly $276 billion in 2019, and another $21 billion were raised last quarter. And looking at the deals on the early-stage side that were made year to date, especially in March, the vertical categories that garnered the most funding were enterprise SaaS, fintech, life sciences, healthcare IT, edtech and cybersecurity.

Image Credits: PitchBook

That said, if VCs have the capital to deploy and are able to overcome the obstacle of “having never met in person,” here are six investment trends that could emerge when the pandemic is over.

Powered by WPeMatico

Since first uploading a YouTube teaser video of its tech five years ago, Magic Leap’s presence in the augmented reality industry has been controversial.

Some have lauded the team’s ambitions, while others I’ve talked to say the company’s posturing has dissuaded investors from taking chances on other AR hardware startups, which has hampered the industry’s advance.

Regardless of its impact, Magic Leap carries outsized weight, leading one to question what would happen to other AR companies if the company’s situation worsened.

The company announced layoffs today, with reports indicating that it is dismissing around 1,000 employees — about half of the company. Magic Leap’s added news of a major pivot to enterprise makes it seem like that wasn’t its primary strategy over the past year. From my perspective, the company looks like it is on a path to a fire sale and will be dependent on executing a dramatic turnaround, which grows tougher under current economic conditions.

Magic Leap has few users, so a theoretical shutdown would likely have a lesser impact than other unicorn flare-outs; still, losing a company on the forefront of a technology lauded by many as the next ubiquitous platform will certainly impact others that are striving to bring this tech to market.

The impact for startups moving forward would be nuanced. Without a substantial software suite of its own, Magic Leap relied heavily on developer partnerships, though in recent months many of those seemed to promote enterprise use cases. AR/VR startups are already in a rough position, and one less developer platform could force more companies to de-prioritize headset-based platforms and shift their focus to mobile.

Powered by WPeMatico

The tech industry (and the world at large) is not experiencing temporary anxiety — the uncertainty we’re all coping with is the new normal.

Sudden shifts in behavior have made some startups targeting slow-moving, old-school industries more relevant than they could have imagined, such as those in telehealth, distance learning and remote work. Most, however are seeing massive decreases in revenue, forcing them to cut costs and even lay off teams to slash burn rates. Other startups simply won’t be here in three to six months.

Cowboy Ventures founder and managing partner Aileen Lee, who coined the term “unicorn,” says tech companies going through scenario planning need to begin thinking long-term.

“We’ve spent the last month scenario planning with our portfolio companies, and in most cases, we’ll have conversations about what these scenarios can include,” said Lee. “And when we look at the planning around those scenarios, they often don’t feel conservative enough. Most entrepreneurs are optimists, and we are, too! But it seems safer to have more conservative plans [and start expecting] that this is going to impact us for longer and be worse than we expected.”

Lee and Cowboy Ventures partner Ted Wang joined TechCrunch on Tuesday for our first episode of Extra Crunch Live, a virtual speaker series for Extra Crunch members. In a live Q&A that included questions from myself and the Extra Crunch audience, Wang and Lee covered a wide range of topics, including PPP loans, advice for business leaders around layoffs, the right time to seek funding and the right firms from which to seek that funding, how to pitch during a downturn and which sectors in particular Cowboy is interested in financing right now.

You can check out the best insights from the call, or catch up on the full conversation via the YouTube embed below.

We have several outstanding guests, including Charles Hudson, Mitch and Freada Kapor, Mark Cuban, Roelof Botha, Hunter Walk and Kirsten Green, joining us on Extra Crunch Live over the next few weeks. Sign up for Extra Crunch to get access to all of them.

Powered by WPeMatico

Two months ago, seemingly out of nowhere, CrowdStrike’s co-founder Dmitri Alperovitch decided it was time to depart.

Alperovitch, who served as the cybersecurity giant’s chief technology office since its 2011 debut, said he was leaving to launch a non-profit policy accelerator. CrowdStrike named Michael Sentonas, who managed the firm’s tech strategy for three years, as his replacement.

The news came at a critical time for the maker and seller of subscription-based endpoint security software that protects against breaches and cyberattacks. The company’s stock was in recovery after it fell below its IPO price, just months after popping 90% on its first day on the public market. It was one of the biggest offerings of the year, reaching more than $11 billion in value by the end, a far cry from a decade earlier when the security giant started out as a few notes scribbled on a napkin in a hotel lobby.

And then the pandemic happened.

By the time of his appointment, Sentonas was preparing to move to the U.S. from his native Australia, but “that hasn’t been the easiest thing to work through,” he told TechCrunch in a recent call. Despite having to balance the time difference and often swapping days with nights, the newly-appointed chief technology officer says it’s largely been “business as usual” for CrowdStrike.

Here’s why.

This interview was edited for clarity and length.

TechCrunch: Two months ago, you were appointed chief technology officer at CrowdStrike. Prior to that you were vice president of tech strategy. How have things been since the promotion?

Michael Sentonas: In some respects, things have been business as usual. A lot of the work I was doing around tech strategy and longer-term vision about [what] we should be working on hasn’t changed for me. Obviously, when one of the co-founders moves on, they have big shoes to fill. So, I’ve inherited a larger team. It’s working with the team around what can I assist them with to help us continue to focus. Probably the biggest change is just being stuck here because of what’s going on around the world and just adjusting to largely covering a U.S. timezone from Australia, which isn’t easy.

That can’t be easy?

We’re a globally-spread and globally-diverse organization. The last statistic that I looked at a few weeks ago was that 70% of our staff logins are remote. I’m dealing with Europe and the U.S., that’s just the way we’re spread. It’s all around the world.

Powered by WPeMatico