exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Earth Class Mail, a company that digitizes your physical mail so you don’t have to go to the mailbox every day, today announced that it has acquired receipt scanning and expense tracking service Shoeboxed.

The reason Earth Class Mail would be interested in Shoeboxed is pretty obvious, given that both companies focus on taking the pain out of dealing with paper. Both services will continue to operate as usual, though we’ll likely see some deep integrations between the two over time.

Shoeboxed, which launched 11 years ago, currently digitizes over five million documents per year for its more than 1 million customers in 90 countries. Its main market is small businesses in the U.S., which make up 500,000 of its users.

“When we started in 2008 and put the first iPhone app in the app store to scan receipts, there was one other powerhouse around helping small business go digital — Earth Class Mail,” the company’s CEO and co-founder Tobias Walter tells us. “The combined power of our two companies will be a massive shift for small businesses to finally become paperless and say goodbye to old workflows that cost them hours of their productivity. I could not be happier with the new home we found for the company, the team and our customers!”

What sets Earth Class Mail apart from the United States Postal Service’s Informed Delivery service is that it not only scans the outside of the envelopes that you are about to receive but that you can also give the company permission to scan all the documents inside, too (and the price you pay for the service depends mostly on how many of these full scans you want per month). While Oregon-based Earth Class Mail had to file for bankruptcy protection in 2015, its new leadership team turned the company around. The company says that its annual run rate is now $10 million, up 20 percent since Jess Garza become its new CEO last December.

Walter also notes that users would occasionally send unopened envelopes, too, but the company wasn’t allowed to open them. These customers can now easily become Earth Class Mail users.

Over the course of its existence, Shoeboxed only raised a moderate amount of funding, with a $580,000 Series A round led by Novak Biddle Venture Partners in 2008 (when Series A rounds were still much smaller than today) and a $1.4 million Series B round in 2011. The financial details of today’s acquisition were not disclosed.

Powered by WPeMatico

Coinbase wants to be Facebook Connect for crypto. The blockchain giant plans to develop “Login with Coinbase” or a similar identity platform for decentralized app developers to make it much easier for users to sign up and connect their crypto wallets. To fuel that platform, today Coinbase announced it has acquired Distributed Systems, a startup founded in 2015 that was building an identity standard for dApps called the Clear Protocol.

The five-person Distributed Systems team and its technology will join Coinbase. Three of the team members will work with Coinbase’s Toshi decentralized mobile browser team, while CEO Nikhil Srinivasan and his co-founder Alex Kern are forming the new decentralized identity team that will work on the Login with Coinbase product. They’ll be building it atop the “know your customer” anti-money laundering data Coinbase has on its 20 million customers. Srinivasan tells me the goal is to figure out “How can we allow that really rich identity data to enable a new class of applications?”

Distributed Systems had raised a $1.7 million seed round last year led by Floodgate and was considering raising a $4 million to $8 million round this summer. But Srinivasan says, “No one really understood what we’re building,” and it wanted a partner with KYC data. It began talking to Coinbase Ventures about an investment, but after they saw Distributed Systems’ progress and vision, “they quickly tried to move to find a way to acquire us.”

Distributed Systems began to hold acquisition talks with multiple major players in the blockchain space, and the CEO tells me it was deciding between going to “Facebook, or Robinhood, or Binance, or Coinbase,” having been in formal talks with at least one of the first three. Of Coinbase the CEO said, they “were able to convince us they were making big bets, weaving identity across their products.” The financial terms of the deal weren’t disclosed.

Coinbase’s plan to roll out the Login with Coinbase-style platform is an SDK that others apps could integrate, though that won’t necessarily be the feature’s name. That mimics the way Facebook colonized the web with its SDK and login buttons that splashed its brand in front of tons of new and existing users. This turned Facebook into a fundamental identity utility beyond its social network.

Developers eager to improve conversions on their signup flow could turn to Coinbase instead of requiring users to set up whole new accounts and deal with crypto-specific headaches of complicated keys and procedures for connecting their wallet to make payments. One prominent dApp developer told me yesterday that forcing users to set up the MetaMask browser extension for identity was the part of their signup flow where they’re losing the most people.

This morning Coinbase CEO Brian Armstrong confirmed these plans to work on an identity SDK. When Coinbase investor Garry Tan of Initialized Capital wrote that “The main issue preventing dApp adoption is lack of native SDK so you can just download a mobile app and a clean fiat to crypto in one clean UX. Still have to download a browser plugin and transfer Eth to Metamask for now Too much friction,” Armstrong replied “On it :)”

On it 🙂

— Brian Armstrong (@brian_armstrong) August 15, 2018

In effect, Coinbase and Distributed Systems could build a safer version of identity than we get offline. As soon as you give your Social Security number to someone or it gets stolen, it can be used anywhere without your consent, and that leads to identity theft. Coinbase wants to build a vision of identity where you can connect to decentralized apps while retaining control. “Decentralized identity will let you prove that you own an identity, or that you have a relationship with the Social Security Administration, without making a copy of that identity,” writes Coinbase’s PM for identity B. Byrne, who’ll oversee Srinivasan’s new decentralized identity team. “If you stretch your imagination a little further, you can imagine this applying to your photos, social media posts, and maybe one day your passport too.”

Considering Distributed Systems and Coinbase are following the Facebook playbook, they may soon have competition from the social network. It’s spun up its own blockchain team and an identity and single sign-on platform for dApps is one of the products I think Facebook is most likely to build. But given Coinbase’s strong reputation in the blockchain industry and its massive head start in terms of registered crypto users, today’s acquisition well position it to be how we connect our offline identity with the rising decentralized economy.

Powered by WPeMatico

Zombie-like passive consumption of static video is both unhealthy for viewers and undifferentiated for the tech giants that power it. That’s set Facebook on a mission to make video interactive, full of conversation with broadcasters and fellow viewers. It’s racing against Twitch, YouTube, Twitter and Snapchat to become where people watch together and don’t feel like asocial slugs afterward.

That’s why Facebook today told TechCrunch that it’s acqui-hired Vidpresso, buying its seven-person team and its technology but not the company itself. The six-year-old Utah startup works with TV broadcasters and content publishers to make their online videos more interactive with on-screen social media polling and comments, graphics and live broadcasting integrated with Facebook, YouTube, Periscope and more. The goal appears to be to equip independent social media creators with the same tools these traditional outlets use so they can make authentic but polished video for the Facebook platform.

Financial terms of the deal weren’t disclosed, but it wouldn’t have taken a huge price for the deal to be a success for the startup. Vidpresso had only raised a $120,00 in seed capital from Y Combinator in 2014, plus some angel funding. By 2016, it was telling hiring prospects that it was profitable, but also that, “We will not be selling the company unless some insane whatsapp like thing happened. We’re building a forever biz, not a flip.” So either Vidpresso lowered its bar for an exit or Facebook made coming aboard worth its while.

For now, Vidpresso clients and partners like KTXL, Univision, BuzzFeed, Turner Sports, Nasdaq, TED, NBC and others will continue to be able to use its services. A Facebook spokesperson confirmed that customers will work with the Vidpresso team at Facebook, who are joining its offices in Menlo Park, London and LA. That means Facebook is at least temporarily becoming a provider of enterprise video services. But Facebook confirms it won’t charge Vidpresso clients, so they’ll be getting its services for free from now on. Whether Facebook eventually turns away old clients or stops integrating with competing video platforms like Twitch and YouTube remains to be seen. For now, it’s giving Vidpresso a much more dignified end than the sudden shutdowns some tech giants impose on their acquisitions.

“We’ve had a lot of false starts along the way . . . We finally landed on helping create high quality broadcasts back on social media, but we still haven’t realized the full vision yet. That’s why we’re joining Facebook,” the Vidpresso team writes. “This gives us the best opportunity to accelerate our vision and offer a simple way for creators, publishers, and broadcasters to use social media in live video at a high quality level . . . By joining Facebook, we’ll be able to offer our tools to a much broader audience than just our A-list publishing partners. Eventually, it’ll allow us to put these tools in the hands of creators, so they can focus on their content, and have it look great, without spending lots of time or money to do so.”

Facebook Live has seen 3.5 billion broadcasts to date, and they get six times as many interactions as traditional videos. But beyond public figures, game streamers, and the odd moment of citizen journalism, it’s become clear that most users don’t have compelling enough content to stream. Interactivity could take some pressure off the broadcaster by letting the audience chip in.

Facebook already has some interactive video experiments out in the wild. For users, it recently rolled out its Watch Party tool for letting Groups view and chat about videos together. It’s also trying new games like Lip Sync Live and a Talent Show feature where users submit videos of them singing. For creators, Facebook now let streamers earn tips with its new Stars virtual currency, and lets fans subscribe to donating money to their favorite video makers like on Patreon. And on the publisher side, Facebook Live has also built tools to help publishers pull in social media content. It’s even got an interactive video API that it’s developing to allow developers to launch their own HQ Trivia-game shows.

But the last line of Vidpresso’s announcement above explains Facebook’s intentions here, and also why it didn’t just try to build the tools itself. It doesn’t just want established news publishers and TV studios making video for its platform. It wants semi-pro creators to be able to broadcast snazzy videos with graphics, comments and polls that can aesthetically compete with “big video” but that feel more natural. This focus on creators over news outlets aligns with reports of Facebooks head of journalist relations Campbell Brown allegedly saying that Mark Zuckerberg doesn’t care about publishers and that “We are not interested in talking to you about your traffic and referrals any more. That is the old world and there is no going back.” Facebook has contested these reports.

Every internet platform is wising up to the fact that web-native creators who grew up on their sites often create the most compelling content and the most fervent fan bases. Whichever video hub offers the best audience growth, creative expression tools and monetization options will become the preferred destination for creators’ work, and their audiences will follow. Vidpresso could help these creators look more like TV anchors than selfie monologuers, but also help them earn money by integrating brand graphics and tie-ins. Facebook couldn’t risk another tech giant buying up Vidpresso and gaining an edge, or wasting time trying to build interactive video technology and expertise from scratch.

Powered by WPeMatico

Google has acquired GraphicsFuzz, a company that builds a framework for testing the security and reliability of Android graphics drivers. The news, which was first spotted by XDA Developers, comes on the same day Google announced the release of Android 9 Pie.

A Google spokesperson confirmed the news to us but declined to provide any further information. The companies also declined to provide any details about the price of the acquisition.

The GraphicsFuzz team, which consists of co-founders Alastair Donaldson, Hugues Evrard and Paul Thomson, will join the Android graphics team to bring its driver-testing technology to the wider Android ecosystem.

“GraphicsFuzz has pioneered the combination of fuzzing and metamorphic testing to yield a highly automatic method for testing graphics drivers that quickly finds and fixes bugs that could undermine reliability and security before they affect end users,” the team explains in today’s announcement. The company’s founders started their work at the Department of Computing at Imperial College London and received funding support from the U.K. Engineering and Physical Sciences Research Council and the TETRACOM EU project.

While this is obviously not the splashiest of acquisitions, it is nevertheless an important one. In the fractured Android ecosystem, graphics drivers are one of the many pieces that make a phone or tablet work — and when they don’t, it’s often immediately obvious to the user. But broken drivers also expose a phone to security exploits. GraphicsFuzz uses the same kind of fuzzing technique, which essentially throws lots of random data at a program, that’s also becoming increasingly popular in other areas of software development.

Powered by WPeMatico

Facebook had a rough day yesterday when its stock plunged after a poor earnings report. What better way to pick yourself up and dust yourself off than to buy a little something for yourself. Today the company announced it has acquired Redkix, a startup that provides tools to communicate more effectively by combining email with a more formal collaboration tool. The companies did not reveal the acquisition price.

Redkix burst out of the gate two years ago with a $17 million seed round, a hefty seed amount by any measure. What prompted this kind of investment was a tool that combined a collaboration tool like Slack or Workplace by Facebook with email. People could collaborate in Redkix itself, or if you weren’t a registered user, you could still participate by email, providing a more seamless way to work together.

Alan Lepofsky, who covers enterprise collaboration at Constellation Research, sees this tool as providing a key missing link. “Redkix is a great solution for bridging the worlds between traditional email messaging and more modern conversational messaging. Not all enterprises are ready to simply switch from one to the other, and Redkix allows for users to work in whichever method they want, seamlessly communicating with the other,” Lepofsky told TechCrunch.

As is often the case with these kinds of acquisitions, the company bought the technology itself along with the team that created it. This means that the Redkix team including the CEO and CTO will join Facebook and they will very likely be shutting down the application after the acquisition is finalized.

Lepofsky thinks that enterprises that are adopting Facebook’s enterprise tool will be able to more seamlessly transition between the two modes of communication, the Workplace by Facebook tool and email, as they prefer.

Although a deal like this has probably been in the works for some time, after yesterday’s earning’s debacle, Facebook could be looking for ways to enhance its revenue in areas beyond the core Facebook platform. The enterprise collaboration tool does offer a possible way to do that in the future, and if they can find a way to incorporate email into it, it could make it a more attractive and broader offering.

Facebook is competing with Slack, the darling of this space and others like Microsoft, Cisco and Google around communications and collaboration. When it launched in 2015, it was trying to take that core Facebook product and put it in a business context, something Slack had been doing since the beginning.

To succeed in business, Facebook had to think differently than as a consumer tool, driven by advertising revenue and had to convince large organizations that they understood their requirements. Today, Facebook claims 30,000 organizations are using the tool and over time they have built in integrations to other key enterprise products, and keep enhancing it.

Perhaps with today’s acquisition, they can offer a more flexible way to interact with the platform and could increase those numbers over time.

Powered by WPeMatico

Grubhub announced this morning that it’s agreed to acquire LevelUp for $390 million cash.

Founder and CEO Matt Maloney told me that while previous Grubhub acquisitions like Eat24 were designed to give the company’s delivery business more scale, “This is kind of a different acquisition. It’s a product and strategic positioning acquisition.”

LevelUp is based in Boston, offering a platform to manage digital ordering, payments and loyalty, with customers like KFC, Taco Bell Pret a Manger, Potbelly and Bareburger. Maloney said that buying the company allows Grubhub to deepen its integration with restaurants’ point-of-sale systems. That, in turn, will allow them to handle more deliveries.

At the same time, Maloney said LevelUp can help Grubhub build a restaurant platform that goes beyond delivery, for example by managing their customer interactions across mobile and the web.

“We want to help restaurants actively engage with their diners,” Maloney said. “This is a huge step in that direction.”

Once the regulatory waiting period is over, the entire LevelUp team will be joining Grubhub, with founder and CEO Seth Priebatsch reporting to Maloney — who said that in the short term, he plans to change very little, aside from the POS integrations. Even in the long term, he suggested that LevelUp could continue to operate as its own brand within the larger Grubhub platform.

“They’re doing something really well and we don’t want to screw that up,” he said. “We want to make as little change as possible, until we all understand how we’re better working together.”

The LevelUp platform was launched in 2011, and the company has raised around $108 million in total funding, according to Crunchbase. Investors include Highland Capital, GV, Balderton Capital, Deutsche Telecom Strategic Investments, Continental Advisors, Transmedia Capital and U.S. Boston Capital.

“For the last seven years, we have worked to provide restaurant clients with a complete solution to engage customers, and this agreement is the biggest and most exciting step in achieving that mission,” Priebatsch said in a statement provided by Grubhub. “After close, the entire team will remain in Boston and our office will become Grubhub’s newest center of technology excellence.”

The announcement came as part of Grubhub’s second quarter earnings release, which saw the company grow active diners by 70 percent year-over-year, to 15.6 million, while revenue increased 51 percent, to $240 million.

Powered by WPeMatico

Doughbies should have been a bakery, not a venture-backed startup. Founded in the frothy days of 2013 and funded with $670,000 by investors, including 500 Startups, Doughbies built a same-day cookie delivery service. But it was never destined to be capable of delivering the returns required by the VC model that depends on massive successes to cover the majority of bets that fail. The startup became the butt of jokes about how anything could get funding.

This weekend, Doughbies announced it was shutting down immediately. Surprisingly, it didn’t run out of money. Doughbies was profitable, with 36 percent gross margins and 12 percent net profit, co-founder and CEO Daniel Conway told TechCrunch. “The reason we were able to succeed, at this level and thus far, is because we focused on unit economics and customer feedback (NPS scoring). That’s it.”

Many other startups in the on-demand space missed that memo and vaporized. Shyp mailed stuff for you and Washio dry cleaned your clothes, until they both died sudden deaths. Food delivery has become a particularly crowded cemetery, with Sprig, Maple, Juicero and more biting the dust. Asked his advice for others in the space, Conway said to “Make sure your business makes sense — that you’re making money, and make sure your customers are happy.”

Doughbies certainly did that latter. They made one of the most consistently delicious chocolate chip cookies in the Bay Area. I had them cater our engagement party. At roughly $3 per cookie plus $5 for delivery, it was pricey compared to baking at home, but not outrageous given SF restaurant rates. From its launch at 500 Startups Demo Day with an “Oprah” moment where investors looked beneath their seats to find Doughbies waiting for them, it cared a lot about the experience.

But did it make sense for a bakery to have an app and deliver on-demand? Probably not. There was just no way to maintain a healthy Doughbies habit. You were either gunning for the graveyard yourself by ordering every week, or like most people you just bought a few for special occasions. Startups like Uber succeed by getting people to routinely drop $30 per day, not twice a year. And with the push for nutritious and efficient offices, it was surely hard for enterprise customers to justify keeping cookies stocked.

Flanked by Instacart and Uber Eats, there weren’t many ripe adjacent markets for Doughbies to conquer. It was stuck delivering baked goods to customers who were deterred from growing their cart size by a sense of gluttony.

Without stellar growth or massive sales volumes, there aren’t a lot of exciting challenges to face for people like Conway and his co-founder Mariam Khan. “Ultimately we shut down because our team is ready to move on to something new,” Conway says.

The startup just emailed customers explaining that “We’re currently working on finding a new home for Doughbies, but we can’t make any promises at this time.” Perhaps a grocery store or broader food company will want its logistics technology or customer base. But delivery is a brutal market to break into, dominated by those like Uber who’ve built economies of scale through massive fleets of drivers to maximize routing efficiency.

In the end, Doughbies was a lifestyle business. That’s not a dirty word. A few co-founders with a dream can earn a respectable living doing what they care about. But they have to do it lean, without the advantage of deep-pocketed investors.

As soon as a company takes venture funding, it’s under pressure to deliver adequate returns. Not 2X or 5X, but 10X, 100X, even 1,000X what they raise. That can lead to investors breathing down their neck, encouraging big risks that could tank the business just for a shot at those outcomes. Two years ago we saw a correction hit the ecosystem, writing down the value of many startups, and we continue to see the ripple effect as companies funded before hit the end of their runway.

Desperate for cash, founders can accept dirty funding terms that screw over not just themselves, but their early employees and investors. FanDuel raised more than $416 million at a peak valuation of $1.3 billion. But when it sold for $465 million, the founders and employees received zero as the returns all flowed to the late-stage investors who’d secured non-standard liquidation preferences. After nearly 10 years of hard work, the original team got nothing.

Not every business is a startup. Not every startup is a rocket ship. It takes more than just building a great product to succeed. It can require suddenly cutting costs to become profitable before you run out of funding. Or cutting ambitions and taking less cash at a lower valuation so you can realistically hit milestones. Or accepting a low-ball acquisition offer because it’s better than nothing. Or not raising in the first place, and building up revenues the old-fashioned way so even modest growth is an accomplishment.

Investors are often rightfully blamed for inflating the bubble, pushing up raises and valuations to lure startups to take their money instead of someone else’s. But when it comes to deciding what could be a fast-growing business, sometimes its the founders who need the adjustment.

Powered by WPeMatico

For people who make investment decisions based on revenues and projected earnings, biotech IPOs are kind of a non-starter. Not only are new market entrants universally unprofitable, most have zero revenue. Going public is mostly a means to raise money for clinical trials, with red ink expected for years to come.

That pattern may be one reason the venture capital press, Crunchbase News included, tends to devote a disproportionately small portion of coverage to biotech IPOs. It’s more exciting to watch a big-name internet company pop in first-day trading or poke fun at an underperforming dud.

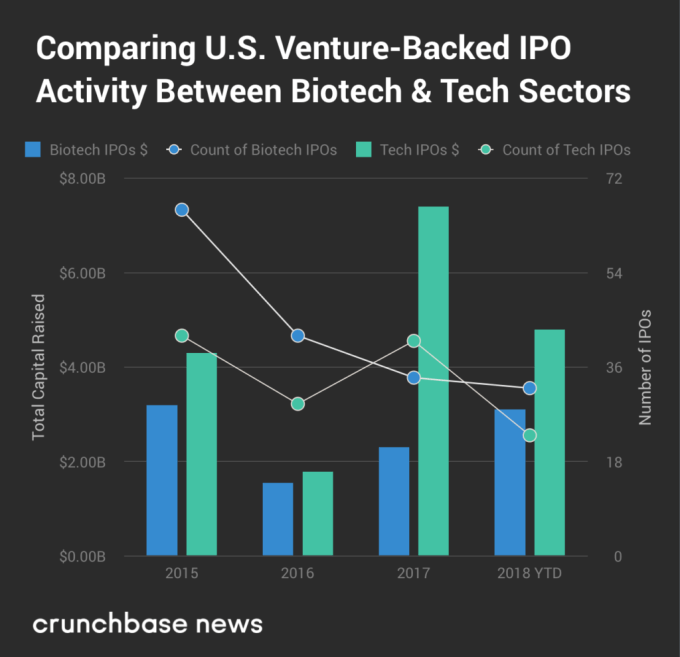

But with our fixation on all things tech, we’re missing out on the big picture. There are actually a lot more biotech and healthcare startup IPOs than tech offerings. In the second quarter of this year, for instance, at least 16 U.S. venture-backed biotech and healthcare companies went public, compared to just 11 tech startups. In three of the past four years, bio offerings outnumbered tech IPOs, according to Crunchbase data.

In the following analysis, we attempt to get up to speed on the pace of biotech offerings, assess where we are in the cycle and spotlight some of the rising stars.

As mentioned above, U.S. bio IPOs outnumber tech offerings in most years. However, the bio cohort raises less total capital, partly because the largest technology IPOs tend to be much bigger than the largest bio IPOs. In the chart below, we compare the two sectors over the past four years.

Globally, the numbers are much higher. Using Crunchbase data, we’ve put together a chart looking at global VC-backed biotech and healthcare IPOs over the past four years. While we’re just over halfway through 2018, biotech and health IPOs have already raised more money than in any of the prior three full calendar years.

It’s pretty clear we’re in an upcycle for all things startup-related. VCs are flush with cash, late-stage rounds are ballooning in size and IPO and M&A action is picking up, too.

So what does that mean for bio IPOs? Is the uptick in the pace and size of offerings mostly a result of bullish market conditions? Or is the current slate of pre-IPO candidates more compelling than in the past?

We turned to Bob Nelsen, co-founder of ARCH Venture Partners, one of the top-performing biotech investors, for his take, which is that it’s a “fundamentals driven, cycle amplified” IPO boomlet.

More companies are launching well-received IPOs because the pace of startup innovation is faster than in the past. Nelson calls it “the result of the previous 30 years of investment and innovation in biotech that has finally led to essentially data-driven innovation.” That’s leading to more curative treatments, disease-modifying therapies and preventative technologies.

Yet we’re also in a bullish segment of the market cycle for biotech. That’s prompting companies that might have stayed private under other conditions to give going public a shot. It’s also providing bigger outcomes for emerging companies that were already on the IPO track.

The latest example of a big outcome IPO is Rubius Therapeutics, which develops drugs based on genetically engineered red blood cells. This week, the five-year-old company raised $241 million at an initial valuation of over $2 billion, making it the largest bio offering of 2018. The Cambridge, Mass. company, which previously raised nearly a quarter-billion-dollars in venture funding, is still in the pre-clinical trial phase.

This year has delivered several other good-sized offerings as well, including drug developers Eidos Therapeutics and Homology Medicines, recently valued around $800 million each, along with Tricida, valued around $1.2 billion. (See the full list of 2018 global bio and health offerings here.)

As for aftermarket performance, that’s been up and down, but includes some big ups. Last year, biotech led the pack for best-performing IPOs on U.S. exchanges. The sector accounted for four of the six top spots, according to Renaissance Capital, led by drug developers AnaptysBio, Argenx and UroGen, along with Calyxt, an agbio startup.

While things are already up, bio VCs, generally an optimistic bunch, see several reasons why bio IPOs could go higher.

Nelson points to what he sees as the lagging pace of in-house innovation at big pharma and biotech players. Increasingly, they need to acquire startups and recently public companies to stay competitive and build out new product pipelines.

There is also tons of fresh capital earmarked for healthcare startups. In the U.S. in 2017, healthcare-focused venture capitalists raised $9.1 billion. That figure was up 26 percent from 2016, per Silicon Valley Bank.

More dollars also are flowing from venture firms that invest in a mix of tech and life sciences through a single fund. That list includes well-established VCs with dry powder to invest, including Polaris Partners, Founders Fund, Kleiner Perkins and Sequoia Capital.

Still, Nelson observes, deep into an IPO bull market, the average quality of offerings does tend to decline. That said, he’s been through similar inflection points in previous cycles and “for the same point in the cycle, the quality is markedly higher.”

Powered by WPeMatico

Tilray, a five-year-old, British Columbia-based medical cannabis company that sells its products to patients, researchers, pharmacies and even governments, saw its shares get high (sorry) on the Nasdaq today, after the company priced 9 million shares at $17 apiece and watched them soar, closing at $22.39, a jump of slightly more than 32 percent.

The company raised $153 million in the offering, capital it will reportedly use in part to fuel its marijuana growing and processing facilities in Ontario.

It was a huge win for the cannabis industry, which has been growing like a weed (sorry again). Related startups attracted $593 million in funding last year, twice what they raised in 2016 and a meaningful jump from the $121 million invested in related startups in 2014, according to CB Insights. Among the different types of companies to garner investor dollars, shows CB Insights’ research, are: startups focused on research or distribution of medical marijuana products (as with Tilray); tools for ensuring compliance with state and federal marijuana laws; startups focused on payments for marijuana companies; startups collecting data and producing marketing insights about the industry; and companies creating novel strains and types of marijuana using new farming techniques.

Tilray’s performance today is also a very positive signal for Seattle-based Privateer Holdings, a private equity firm that owned 100 percent of the startup as it headed into its offering. In fact, Privateer’s CEO, Brendan Kennedy, is also the CEO of Tilray. (Cannabis companies are weird.)

Privateer has itself raised more than $200 million since its founding in 2010, including from Founders Fund and Subversive Capital, and it has used that capital to fund, acquire and incubate companies. While it incubated Tilray, for example, it also owns Leafly, a large cannabis information resource that it acquired in 2011. Another of its portfolio companies is Marley Natural, a Bob Marley-branded cannabis line that it launched in partnership with the Marley’s estate and that sells a line of cannabis strains, smoking accessories and even body care products.

It isn’t exactly clear how much Privateer had sunk into Tilray (we have a press request into the company). Tilray had announced C$60 million in Series A funding back in February, composed of a “group of leading global institutional investors.” But according to its S-1, it was solely owned until today by Privateer.

What we do know: Tilray remains unprofitable, reporting a net loss of $7.8 million last year. The company also cannot sell its products in the U.S. market, given that marijuana remains illegal under federal law, despite that 30 states and Washington, D.C. have legalized it in some form. The reason: The U.S. government classifies marijuana as a schedule 1 drug, meaning it’s considered to have no medical value and a high potential for abuse.

That could change, but as this Vox explainer makes clear, a review process for the current schedule would need to be initiated by either the secretary of health and human services or the attorney general, and current Attorney General Jeff Sessions despises marijuana, saying once that “Good people don’t smoke marijuana.”

He seems to be among a dwindling minority. According to a Gallup Poll published last October, 64 percent of Americans favor legalization.

Powered by WPeMatico

Okta, the cloud identity management company, announced today it has purchased a startup called ScaleFT to bring the Zero Trust concept to the Okta platform. Terms of the deal were not disclosed.

While Zero Trust isn’t exactly new to a cloud identity management company like Okta, acquiring ScaleFT gives them a solid cloud-based Zero Trust foundation on which to continue to develop the concept internally.

“To help our customers increase security while also meeting the demands of the modern workforce, we’re acquiring ScaleFT to further our contextual access management vision — and ensure the right people get access to the right resources for the shortest amount of time,” Okta co-founder and COO Frederic Kerrest said in a statement.

Zero Trust is a security framework that acknowledges work no longer happens behind the friendly confines of a firewall. In the old days before mobile and cloud, you could be pretty certain that anyone on your corporate network had the authority to be there, but as we have moved into a mobile world, it’s no longer a simple matter to defend a perimeter when there is effectively no such thing. Zero Trust means what it says: you can’t trust anyone on your systems and have to provide an appropriate security posture.

The idea was pioneered by Google’s “BeyondCorp” principals and the founders of ScaleFT are adherents to this idea. According to Okta, “ScaleFT developed a cloud-native Zero Trust access management solution that makes it easier to secure access to company resources without the need for a traditional VPN.”

Okta wants to incorporate the ScaleFT team and, well, scale their solution for large enterprise customers interested in developing this concept, according to a company blog post by Kerrest.

“Together, we’ll work to bring Zero Trust to the enterprise by providing organizations with a framework to protect sensitive data, without compromising on experience. Okta and ScaleFT will deliver next-generation continuous authentication capabilities to secure server access — from cloud to ground,” Kerrest wrote in the blog post.

ScaleFT CEO and co-founder Jason Luce will manage the transition between the two companies, while CTO and co-founder Paul Querna will lead strategy and execution of Okta’s Zero Trust architecture. CSO Marc Rogers will take on the role of Okta’s Executive Director, Cybersecurity Strategy.

The acquisition allows the Okta to move beyond purely managing identity into broader cyber security, at least conceptually. Certainly Roger’s new role suggests the company could have other ideas to expand further into general cyber security beyond Zero Trust.

ScaleFT was founded in 2015 and has raised $2.8 million over two seed rounds, according to Crunchbase data.

Powered by WPeMatico