exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Everyone loves a tale of a bootstrapped startup founder’s journey to an eight-figure exit.

The team at Toronto-based Cluep have a good one.

The founders of the adtech startup raised less than $500,000 from angel investors before selling their company to Impact Group for $40 million ($53 million CAD) this week.

Founded in 2012, Karan Walia, Sobi Walia and Anton Mamonov were just 21, 17 and 16 years old, respectively, when they started the digital advertising platform, which uses artificial intelligence to help brands connect and engage with people based on what they are sharing, how they are feeling and the places they’ve been.

They, being so young, struggled initially to get the company off the ground. At one point, the trio hacked into computers at a university in Toronto to train the neural networks on large amounts of data sets because they didn’t have enough money to buy their own tech. On a shoe-string budget, they would split meals at Popeyes to get by.

“No one wanted to give us money at that time so we had to live off of my student loans,” Walia told TechCrunch. “We did pretty much everything, whether it was programming and building the product, or going out and selling. I was our first sales rep and I was pretty bad early on but I learned.”

Ultimately, Cluep was able to raise enough from angels to pay themselves a salary, hire a few engineers and sales representatives and move into an actual office. From that point, their revenue began growing significantly YoY.

They fielded offers from VCs toward the end of 2015 and considered raising a proper Series A round of capital, but ultimately decided staying independent would lead to the best exit.

“This way allowed us to basically maintain control and exit on our terms,” Walia said.

Impact Group, a Boise, Idaho-based grocery sales and marketing agency, will operate Cluep independently.

Powered by WPeMatico

MariaDB, the company behind the eponymous MySQL drop-in replacement database, today announced that it has acquired Clustrix, which itself is a MySQL drop-in replacement database, but with a focus on scalability. MariaDB will integrate Clustrix’s technology into its own database, which will allow it to offer its users a more scalable database service in the long run.

That by itself would be an interesting development for the popular open source database company. But there’s another angle to this story, too. In addition to the acquisition, MariaDB also today announced that cloud computing company ServiceNow is investing in MariaDB, an investment that helped it get to today’s acquisition. ServiceNow doesn’t typically make investments, though it has made a few acquisitions. It is a very large MariaDB user, though, and it’s exactly the kind of customer that will benefit from the Clustrix acquisition.

MariaDB CEO Michael Howard tells me that ServiceNow current supports about 80,000 instances of MariaDB. With this investment (which is actually an add-on to MariaDB’s 2017 Series C round), ServiceNow’s SVP of Development and Operations Pat Casey will join MariaDB’s board.

Why would MariaDB acquire a company like Clustrix, though? When I asked Howard about the motivation, he noted that he’s now seeing more companies like ServiceNow that are looking at a more scalable way to run MariaDB. Howard noted that it would take years to build a new database engine from the ground up.

“You can hire a lot of smart people individually, but not necessarily have that experience built into their profile,” he said. “So that was important and then to have a jumpstart in relation to this market opportunity — this mandate from our market. It typically takes about nine years, to get a brand new, thorough database technology off the ground. It’s not like a SaaS application where you can get a front-end going in about a year or so.

Howard also stressed that the fact that the teams at Clustrix and MariaDB share the same vocabulary, given that they both work on similar problems and aim to be compatible with MySQL, made this a good fit.

While integrating the Clustrix database technology into MariaDB won’t be trivial, Howard stressed that the database was always built to accommodate external database storage engines. MariaDB will have to make some changes to its APIs to be ready for the clustering features of Clustrix. “It’s not going to be a 1-2-3 effort,” he said. “It’s going to be a heavy-duty effort for us to do this right. But everyone on the team wants to do it because it’s good for the company and our customers.

MariaDB did not disclose the price of the acquisition. Since it was founded in 2006, though, the Y Combinator-incubated Clustrix had raised just under $72 million, though. MariaDB has raised just under $100 million so far, so it’s probably a fair guess that Clustrix didn’t necessarily sell for a large multiple of that.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

After a long run of having guests climb aboard each week, we took a pause on that front, bringing together three of our regular hosts instead: Connie Loizos, Danny Chrichton, and myself.

Despite the fact that there were just three of us instead of the usual four, we got through a mountain of stuff. Which was good as it was a surprisingly busy week, and we didn’t want to leave too much behind.

Up top we dug into the latest in the land of crypto, which Danny had politely summarized for us in an article. The gist of his argument is that the analogies relating crypto as an industry to the Internet may work, but most people have their timelines wrong: Crypto isn’t like the Internet in the 90s, perhaps. More like the 80s.

On the same topic, crypto companies formed a team lobbying effort, and a high-flying crypto fund is struggling to once again post strong profit figures.

Moving along, Juul is back in the news. Not, however, for raising more money or posting quick growth. Well, sort of the latter, as the government is after it. The Food and Drug Administration has put Juul on a countdown to get its act together regarding teens and smoking. That the financially impressive unicorn is in as much trouble as it is, is nearly surprising.

Finally, we ran through the three most recent Chinese IPOs that hit our radar. Here they are:

And that was the end of things. Thanks for sticking with us, as always. Speaking of which, our 100th episode is coming up. Who should we bring onto the show to celebrate?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Microsoft today announced that is has acquired Lobe, a startup that lets you build machine learning models with the help of a simple drag-and-drop interface. Microsoft plans to use Lobe, which only launched into beta earlier this year, to build upon its own efforts to make building AI models easier, though, for the time being, Lobe will operate as before.

“As part of Microsoft, Lobe will be able to leverage world-class AI research, global infrastructure, and decades of experience building developer tools,” the team writes. “We plan to continue developing Lobe as a standalone service, supporting open source standards and multiple platforms.”

Lobe was co-founded by Mike Matas, who previously worked on the iPhone and iPad, as well as Facebook’s Paper and Instant Articles products. The other co-founders are Adam Menges and Markus Beissinger.

In addition to Lobe, Microsoft also recently bought Bonsai.ai, a deep reinforcement learning platform, and Semantic Machines, a conversational AI platform. Last year, it acquired Disrupt Battlefield participant Maluuba. It’s no secret that machine learning talent is hard to come by, so it’s no surprise that all of the major tech firms are acquiring as much talent and technology as they can.

“In many ways though, we’re only just beginning to tap into the full potential AI can provide,” Microsoft’s EVP and CTO Kevin Scott writes in today’s announcement. “This in large part is because AI development and building deep learning models are slow and complex processes even for experienced data scientists and developers. To date, many people have been at a disadvantage when it comes to accessing AI, and we’re committed to changing that.”

It’s worth noting that Lobe’s approach complements Microsoft’s existing Azure ML Studio platform, which also offers a drag-and-drop interface for building machine learning models, though with a more utilitarian design than the slick interface that the Lobe team built. Both Lobe and Azure ML Studio aim to make machine learning easy to use for anybody, without having to know the ins and outs of TensorFlow, Keras or PyTorch. Those approaches always come with some limitations, but just like low-code tools, they do serve a purpose and work well enough for many use cases.

Powered by WPeMatico

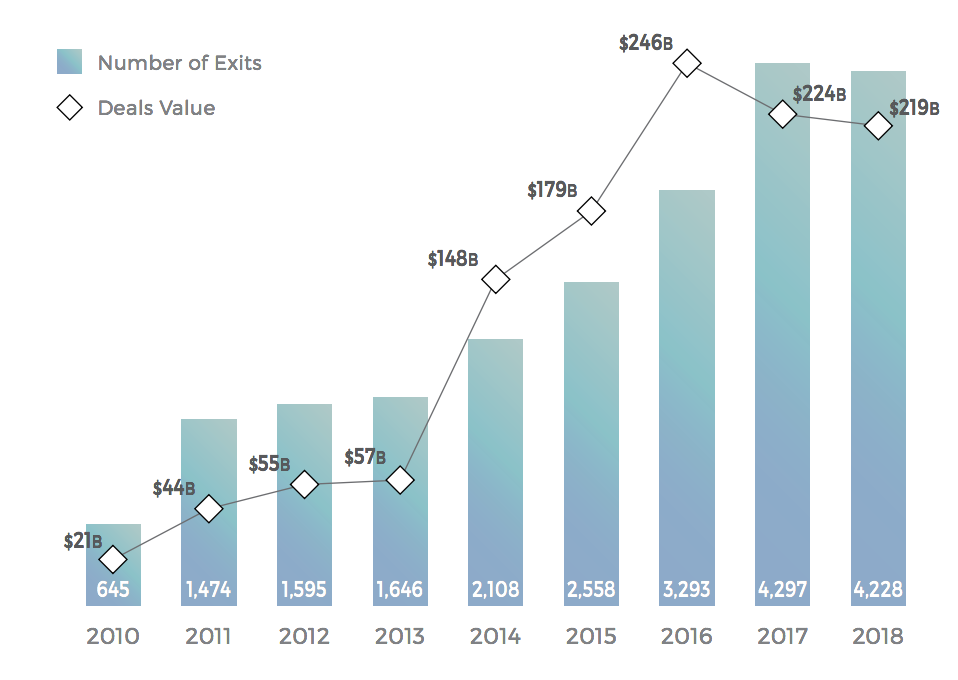

U.S. tech companies continue to be the most active acquirers in the world, says a new report from Crunchbase and Mind the Bridge.

The pair crunched data on 22,000 startup exits since 2010, recording about 4,200 so far this year. U.S. companies, though less active this year than last, have acquired approximately 2x more startups than their European counterparts.

Overall, 2018 is a flat year for M&A activity, despite a record-setting 2017.

Here are a few key takeaways from the report, which you can read in full here.

Powered by WPeMatico

Opendoor, a four year-old, San Francisco-based company, has from the outset intended to make it possible to buy and sell residential real estate with a few key strokes. It seemingly gets closer to that audacious vision by the day. The company closed on $325 million in new funding in June in a round that brought its total equity funding to $645 million to date — and its valuation to more than $2 billion. The company has also raised $1.75 billion in debt, and two sources tell us more funding from SoftBank is imminent.

Opendoor’s cofounder and CEO, Eric Wu, who previously cofounded two other companies, won’t answer questions about SoftBank when asked. But there’s no question the company is one of the most capital-intensive startups on the scene currently. Opendoor bids on homes sight unseen, agrees to buy them, then — contingent on an inspection to verify the quality of the home (“sometimes customers aren’t aware of things like foundation issues,” explains Wu) — it sells them, charging a fee of “about 6 percent,” he says. (Recent reports claim this number can reach as high as 13 percent.)

To date, the company has largely been working with people who need to sell their homes quickly because of a new job or other life event. By using Opendoor, goes the pitch, they don’t get stuck paying for two mortgages when they can’t afford it. Yet Opendoor increasingly wants to help them buy that next house, too. Toward that end, the company has just acquired Open Listings, a four-year-old, L.A.-based startup that has aimed to make it easier and cheaper for buyers to purchase homes by automating much of what an agent would do, thus reducing the fee an agent would traditionally take.

Opendoor isn’t saying what it’s paying for Open Listings, which had raised $7.6 million from investors over the years, including Y Combinator, Matrix Partners, Arena Ventures, and Initialized Capital. But all of Open Listings’ 45 employees will join the 900 employees of Opendoor, and the move gets Opendoor into a handful of new cities in which it wasn’t already operating, including San Francisco, Seattle, Austin, L.A., and Chicago.

The deal was also a very natural fit, suggests Wu. He says he met Open Listings cofounder and CEO Judd Schoenholtz in 2015, when Schoenholtz — through YC’s alumni network — approached Wu, whose last company had passed through YC’s program. Schoenholtz “reached out and wanted to share what they were trying to solve in real estate, so we met up and talked about problems we saw and our respective approaches . . . Judd was starting with the buyer side, and we were starting with the sales side, and we continued to share notes on how we were solving both.”

The acquisition is the very first for Opendoor, though one senses it’s just the beginning of similar tie-ups. In a call yesterday, Wu referred to other initiatives that Opendoors is exploring, including a kind of financing business, which Wu has been talking about for years but that sounds closer now to fruition. “We’re doing some things around mortgages that will integrated into the shopping experience,” says Wu, without wanting to elaborate further. Home improvement loans may also be on the horizon. (Wu says Opendoor “also wants to enable home buyers to personalize their experience.”)

Opendoor is also working more closely with developers, forming partnerships with “19 of the 25 largest home builders in the country over the last 18 months,” says Wu. The idea is for Opendoor’s customers to put down a deposit on a new home, with Opendoor operating quietly in the background to both help choose a closing date, as well as to sell those customers’ previous homes.

The big question, as always, is what Opendoor does in a sustained market downturn. The company is reportedly on pace to spend more than $2.5 billion on home purchases over the next year. Yet buying homes is a complicated affair. For starters, after Opendoor acquires each home, it has to ensure the home is up to code in order to resell it. Indeed, though the company is willing to buy homes built after 1960, Wu says a growing amount of its inventory was built no earlier than 1990.

Hanging on to its inventory, which Opendoor does for 90 days on average, would seem to pose an equally big risk, particularly given that the housing market is highly sensitive to interest rates and other macroeconomic factors that could prompt a market cool-off. We may even be seeing early signs of one right now.

Wu doesn’t seem concerned, focused as he is on creating a kind of virtuous cycle of home buying. Asked about housing market slowdowns, he shrugs off the question. Maybe he needs to operate that way, given the ambitious vision of Opendoor.

Says Wu when talk turns to rising mortgage rates and growing new home inventory, “We have a world-class pricing team to track data on a national and subdivision level that informs [what we do].” As for the condition of the housing market, “we aren’t commenting,” he says.

Pictured above, left to right: Eric Wu and Judd Schoenholtz.

Powered by WPeMatico

Now valued at $5.6 billion, zero-fee stock trading app and cryptocurrency exchange Robinhood is starting preparations to go public. Just a year and a half ago, it was still largely under the radar. But then it raised a $110 million Series C at a $1.3 billion valuation in April 2017 and then just a year later scored a $363 million Series D, both led by Russian firm DST Global. Combined with the growth of its premium subscription for trading on margin called Robinhood Gold, the startup now has the firepower and revenue to make a viable Wall Street debut.

Today during Robinhood CEO Baiju Bhatt’s talk at TechCrunch Disrupt SF, he revealed that his company is on the path to an IPO and has begun its search for a chief financial officer. It’s also undergoing constant audits from the SEC, FINRA and its security team to make sure everything is kosher and locked up tight.

The CFO hire could help the five-year-old Silicon Valley startup pitch itself as the cheaper youthful alternative to E*Trade and traditional stock brokers. They’d also have to convince potential investors that even though cryptocurrency prices are in a downturn, allowing people to trade them for cheaper than competitors like Coinbase is a powerful user acquisition funnel.

Robinhood now has 5 million customers tracking, buying and selling stocks, options, ETFs, American depositary slips receipts of international companies and cryptos like Bitcoin and Ethereum. That’s twice as many customers as its incumbent competitor E*Trade despite it having 4,000 employees compared to Robinhood’s 250.

The startup has raised a total of $539 million to date from prestigious investors like Andreessen Horowitz, Kleiner Perkins, Sequoia and Google’s Capital G, allowing it to rapidly roll out products before its rivals can react. This rapid rise in valuation can go to some founders’ heads, or crush them under the pressure, but Bhatt cited “friendship” with his co-CEO Vlad Tenev as what keeps him sane.

The startup has three main monetization streams. First, it earns interest on money users keep in their Robinhood account. Second, it sells order flow to stock exchanges that want more liquidity for their traders. And it sells Robinhood Gold subscriptions which range from $10 per month for $2,000 in extra buying power to $200 per month for $50,000 in margin trading, with a 5 percent APR charged for borrowing over that. Gold was growing its subscriber count at 17 percent per month earlier this year, showing the potential of giving trades away for free and then charging for extra services.

But Robinhood is also encountering renewed competition as both startups and incumbents wise up. European banking app Revolut is building a commission-free stock trading, and Y Combinator startup Titan just launched its app that lets you buy into a managed portfolio of top stocks. Finance giant JP Morgan now gives customers 100 free trades in hopes of not being undercut by Robinhood.

Over on the crypto side, Coinbase continues to grow in popularity despite its 1.4 percent to 4 percent fees on trades. It’s rapidly expanding its product offering and the two fintech startups are destined to keep clashing. Robinhood may also be suffering from the crypto downturn, which is likely dissuading the mainstream public from dumping cash into tokens after seeing people lose fortunes as Bitcoin and Ethereum’s prices tumbled this year.

There’s also the persistent risk of a security breach that could tank Robinhood’s brand. Meanwhile, the startup uses both human and third-party software-based systems to moderate its crypto chat rooms to make sure pump and dump schemes aren’t running rampant. Bhatt says he’s proud of making cryptocurrency more accessible, though he didn’t say he felt responsible for prices plummeting, which could mean many of Robinhood Crypto’s users have lost money.

Fundamentally, Robinhood is using software to make the common but expensive behavior of stock trading much cheaper and more accessible to a wider audience. Traditional banks and brokers have big costs for offices and branches, trading execs and TV commercials. Robinhood has managed to replace much of that with a lean engineering team and viral app that grows itself. Once it finds its CFO, that could give it an efficiency and growth rate that has Wall Street seeing green.

Powered by WPeMatico

Berlin based Internet of Things (IoT) startup relayr, whose middleware platform is geared towards helping industrial companies unlock data insights from their existing machinery and production line kit by linking Internet connected sensors and edge devices to platform controls, has been acquired by insurance group Munich Re in a deal which values the company at $300 million.

relayr was founded back in 2013 with the initial aim of helping software developers hack around with hardware, at a time when developer interest in IoT was just taking off.

The startup went on to pass through startupbootcamp and crowdfunded a cute looking chocolate-bar shaped hardware starter kit before expanding into building a hardware agnostic cloud services platform to act as a central hub for data flows. relayr then further honed its focus to the needs of industrial IoT, and its platform — which is now used by around 130 businesses — offers end-to-end middleware combined with device management and IoT analytics, and can operate in the cloud, on-premise or a hybrid of both depending on customers needs.

We first covered the Berlin-based startup back in 2014 when it closed a $2.3M seed round. It’s raised $66.8M in total, according to Crunchbase, which includes a $30M Series C round in February led by Deutsche Telekom Capital Partners.

relayr did not disclose the investors in its 2014 seed at the time, saying only that they were unnamed U.S. and Switzerland-based investors. But Kleiner Perkins and Munich Re (via its HSB subsidiary which is acquiring relayr now) were named as investors in later rounds, along with Deutsche Telekom .

Insurance giants and telcos have a clear strategic interest in IoT — with the technology promising to drive network usage and utility on the telco side, and offering transformative potential for the insurance industry as data streams can be used to monitor equipment performance and predict (and even steer off) costly failures.

Munich Re said today that its HSB subsidiary is acquiring 100% of relayr in a deal that values the business at $300M. (It’s not clear if it’s all cash or a mix of cash and stock — we’ve asked. Update: A spokeswomen for Munich Re confirmed the transaction will be financed with “internal cash funds” from the group).

It says the deal will help it “shape opportunities in the fast-growing IoT market”, and is envisaging a joint business model with the combined pair developing not just tech solutions for clients but risk management, data analysis and financial instruments.

“IoT is already significantly changing our world and has the potential to disrupt the traditional insurance and reinsurance industry through new business models, services and competitors,” said Torsten Jeworrek, member of Munich Re’s board of management in a statement. “I am truly happy to announce this acquisition, as it supports our strategy to combine our knowledge of risk, data analysis skills and financial strength with the technological expertise of relayr. This is our basis to develop new ideas for tomorrow’s commercial and industrial worlds.”

“We are delighted to strengthen our relationship with Munich Re/HSB to push digitalization in commercial and industrial markets and strive for our mission to help commercial and industrial businesses stay relevant,” added relayr CEO, Josef Brunner. “The unique combination of the companies demonstrates the importance to deliver business outcomes to customers and the need to combine first-class technology and its delivery with powerful financial and insurance offerings. This transaction is a great opportunity to build a global category leader.”

The pair have been partnered since 2016, when the insurance firm invested in relayr’s Series B, but say they see the acquisition strengthening Munich Re’s financial and insurance offerings while also offering a route to expand relayr’s middleware business via leveraging the insurance group’s large client base.

“Back in 2016, HSB invested in relayr in an effort to harness the strategically significant business potential offered by IoT. relayr’s end-to-end IoT solutions for the industrial and commercial sectors are an ideal addition to our Group’s capabilities,” said Greg Barats, president and CEO of HSB, and the person responsible for Munich Re’s IoT strategy, in another supporting statement. “HSB has always focused on insurance and technology… relayr will help us to rapidly implement our global strategy to develop new IoT solutions for our clients. Digital transformation in the industrial and commercial sectors offers opportunities for new services and financial applications.”

relayr says it already offers industrial companies which are seeking to digitalise their businesses a “comprehensive range of services” — such as being able to extract and analyse data from machines and equipment to determine when a machine is likely to fail (and it touts cutting costs, increased energy efficiency and product quality improvement as among the benefits its platform offers) — but says the acquisition will allow it to develop its “innovative value stack”, by enabling new revenue models, cost reduction, and “increased effectiveness across industries”.

It also sees benefit in sitting under the established Munich Re umbrella — as a way to convince customers it will be a long-term business partner. It adds that it will continue to maintain its current focus on IoT for the industrial sector.

Powered by WPeMatico

Reaching event organizers to help them sell tickets isn’t cheap. Eventbrite — the 12-year-old, San Francisco-based ticketing company that announced plans last week to go public and sell $200 million worth of shares on the NYSE — has been losing money since 2016, posting losses of $40.4 million in 2016, $38.5 million for 2017 and $15.6 million so far this year.

Now the company is trying to make up for some of those losses by announcing a new pricing scheme. Today, it sent customers a note explaining that for those using its “Essentials” package (unlike its “Professional” package, whose bells and whistles include customer support, customer questions for attendees and more), reduced prices are coming for many of its customers. Specifically, payment processing fees are dropping from 3 percent to 2.5 percent. Fees for ticket are falling from .99 cents to .70 cents.

The moves don’t really mean that Eventbrite is charging less. In fact, instead of charging one percent of every ticket price as a service fee, Eventbrite will now take a 2 percent cut, which should add up for organizers that use the service for bigger events. It’s also removing a service fee cap of $19.99 that it used to institute no matter how much an event organizer was charging.

Asked about the pricing changes, a spokesperson sent us a fairly bland statement: “At Eventbrite we have always been committed to enabling event creators to deliver a diverse range of live experiences by offering a superior product at a fair price. The changes we announced today will mean lower ticket fees for the vast majority of our creators, and the millions of people that attend the events they plan, promote and produce each year. We succeed when our creators succeed and this change is indicative of a focus on ensuring we make the best decisions for the majority of our customers.”

It isn’t surprising that Eventbrite is looking for ways to fight rising acquisition costs owing to the competition it faces from all corners. In addition to platforms for smaller get-togethers like Paperless Post and competition for bigger events like Ticketmaster (which owns Live Nation), Eventbrite acknowledged in its S-1 filing that it could face competition from large internet companies like Facebook, Google and Twitter, too.

Eventbrite had reportedly filed confidentially for an IPO back in July. As noted on TechCrunch’s “Equity” podcast last week by Susan Mac Cormac, a partner at the global law firm Morrison Foerster, companies often file confidentially first if they are exploring other options, including, most notably, M&A.

“These unicorns,” says Mac Cormac, “it’s difficult for them to go public because they have such a huge valuation to begin with that M&A is often a better option. You don’t want to go out and have your stock fall 30, 40, 50 percent as sometimes happens.”

Partly through acquisitions, Eventbrite saw its revenue rise from $133 million in 2016 to $201 million last year. Last year, for example, Eventbrite acquired Ticketfly, a ticketing company that focused largely on the live entertainment industry and which had sold to the streaming music company Pandora in 2015 for a reported $335 million but Eventbrite was able to nab last year at the discounted price of $200 million.

Eventbrite has also made a broader international push in recent years, acquiring Ticketea, one of Spain’s leading ticketing providers, back in April, and acquiring Amsterdam-based Ticketscript back in January of last year. And those deals followed roughly half a dozen others.

Over the years, the company has raised roughly $330 million from investors, according to Crunchbase. Its biggest shareholders, shows its S-1, are Tiger Global Management, Sequoia Capital and T. Rowe Price. Collectively, the three entities own roughly half of Eventbrite’s pre-IPO shares.

Powered by WPeMatico

VMware is hosting its VMworld customer conference in Las Vegas this week, and to get things going it announced that it’s acquiring Boston-based CloudHealth Technologies. They did not disclose the terms of the deal, but Reuters is reporting the price is $500 million.

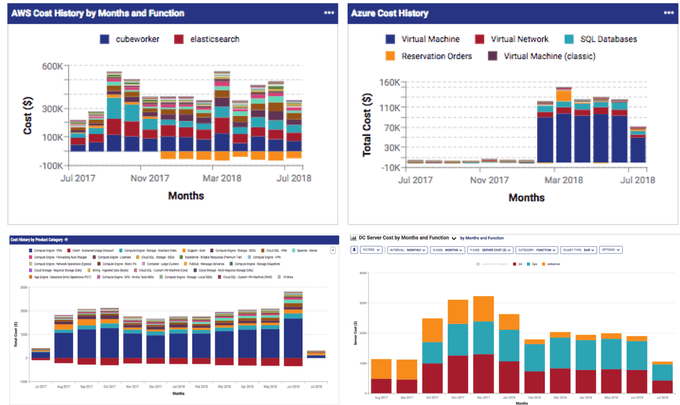

CloudHealth provides VMware with a crucial multi-cloud management platform that works across AWS, Microsoft Azure and Google Cloud Platform, giving customers a way to manage cloud cost, usage, security and performance from a single interface.

Although AWS leads the cloud market by a large margin, it is a vast and growing market and most companies are not putting their eggs in a single vendor basket. Instead, they are looking at best of breed options for different cloud services.

This multi-cloud approach is great for customers in that they are not tied down to any single provider, but it does create a management headache as a consequence. CloudHealth gives multi-cloud users a way to manage their environment from a single tool.

CloudHealth multi-cloud management. Photo: CloudHealth Technologies

VMware’s chief operating officer for products and cloud services, Raghu Raghuram, says CloudHealth solves the multi-cloud operational dilemma. “With the addition of CloudHealth Technologies we are delivering a consistent and actionable view into cost and resource management, security and performance for applications across multiple clouds,” Raghuram said in a statement.

CloudHealth began offering support for Google Cloud Platform just last month. CTO Joe Kinsella told TechCrunch why they had decided to expand their platform to include GCP support: “I think a lot of the initiatives that have been driven since Diane Greene joined Google [at the end of 2015] and began really driving towards the enterprise are bearing fruit. And as a result, we’re starting to see a really substantial uptick in interest.”

It also gave them a complete solution for managing across the three of the biggest cloud vendors. That last piece very likely made them an even more attractive target for a company like VMware, who apparently was looking for a solution to buy that would help customers manage across a hybrid and multi-cloud environment.

The company had been planning future expansion to manage not just the public cloud, but also private clouds and data centers from one place, a strategy that should fit well with what VMware has been trying to do in recent years to help companies manage a hybrid environment, regardless of where their virtual machines live.

With CloudHealth, VMware not only gets the multi-cloud management solution, it gains its 3000 customers which include Yelp, Dow Jones, Zendesk and Pinterest.

CloudHealth was founded in 2012 and has raised over $87 million. Its most recent round was a $46 million Series D in June 2017 led by Kleiner Perkins. Other lead investors across earlier rounds have included Sapphire Ventures, Scale Venture Partners and .406 Ventures.

Powered by WPeMatico