exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Snowflake filed to go public today joining a bushel of companies making their S-1 documents public today. TechCrunch has a longer digest of all the IPO filings coming soon, but we could not wait to get into the Snowflake numbers, given the huge anticipation that the company has generated in recent quarters.

Why? Because the cloud data warehouse company has been on a fundraising tear in recent years, including a $450 million Series F in late 2018 and a $479 million Series G in February of this year. The latter round valued the mega-unicorn at around $12.5 billion. More on this later.

Snowflake is, then, one of the world’s most valuable former startups that is still private. Its public debut will make a splash. But what did its $1.4 billion in capital raised (Crunchbase data) build? Let’s take a peek at the numbers.

Even glancing at the Snowflake S-1 makes it clear what investors are excited about when it comes to the big-data storage service: Its growth. In its fiscal year ending January 31, 2019, for example, Snowflake had revenue of $96.7 million. A year later that number was $264.7 million, or growth of around 150% at scale.

More recently, the company’s growth has remained impressive. In the six months ending July 31, 2019, Snowflake’s revenue was $104.0 million. A year later, those two quarters generated revenues of $242.0 million. That’s growth of 132.7% on a year-over-year basis. Impressive, and just the sort of top line expansion that private investors want to staple their wallet to.

So, lots of growth. But how high-quality is the revenue?

Let’s take a look at the company’s gross margins over different time periods. The data will help us better understand the company’s value, and its gross margin improvement, or impairment over time. Given Snowflake’s soaring valuation over time, we are expecting to see improvements as time passes:

Et voilà ! Just like we expected, improving gross margins over time. Recall that the higher (stronger) a company’s gross margins are, the more of its revenue it gets to keep to cover its operating costs. Which is, notably, where the Snowflake story goes from super-exciting to slightly harrowing.

Let’s talk losses.

In no way does Snowflake’s operations pay for themselves. Indeed, the company is super unprofitable on both an operating and net basis.

In its fiscal year ending January 31, 2019, Snowflake lost $178.0 million on a net basis. A year later the figure swelled to $348.5 million. In the six months ending July 31, 2019, the company’s net loss was $177.2 million. In the same two quarters of this year, it was slightly lower at $171.3 million.

And that’s why the company is probably trying to go public. Now that it can point to falling net losses as its revenues grow and its gross margins improve, you can chart a path to break-even. And Snowflake’s operations are burning less cash over time. The pace was north of $50 million a quarter in the two three-month periods ending July 31, 2019, for example.

And even more, if we look inside the last two quarters, the most recent period (three months ending July 31, 2019) is larger than the one preceding it in revenue terms ($133.1 million versus $108.8 million), and its net loss is smaller ($77.6 million versus $93.6 million). This lowered the company’s net margin from -86% to -58%. Still bad! But far less bad in short order, which could cut worries about Snowflake’s enormous history of unprofitability at scale.

Since Snowflake first appeared in 2012, its ability to take the idea of a data warehouse, a concept that has existed on prem for years, and move into a cloud context had great appeal — and it attracted great investment. Imagine taking virtually all your data and having it in a single place in the cloud.

The money train started slowly at first, with $900,000 in seed money in February 2012, followed quickly by a $5 million Series A later that year. Within a few years investors would be handing the company bundles of cash and the train would be the high-speed variety, first with former Microsoft executive Bob Muglia leading the way, and more recently with former ServiceNow CEO Frank Slootman in charge.

By 2017 there were rapid-fire rounds for big money: $105 million in 2017, $263 million in January 2018, $450 million in October 2018 and finally $479 million this past February. With each chunk of money came gaudier valuations, with the most recent weighing in at an eye-popping $12.4 billion. That was triple the company’s $3.9 billion valuation in that October 2018 investment.

In February, Slootman did not shy away from the IPO question. Unlike so many startup CEOs, he actually embraced the idea of finally taking his company public, whenever the time was right, and apparently that would be now, pandemic or not.

He actually almost called the timing in a conversation with TechCrunch at the time of the $479 million round:

I think the earliest that we could actually pull that trigger is probably early- to mid-summer time frame. But whether we do that or not is a totally different question because we’re not in a hurry, and we’re not getting pressure from investors.

All money talk aside, at its core, what Snowflake offers is this ability to store vast amounts of data in the cloud without fear of locking yourself in to any particular cloud vendor. While all three cloud players have their own offerings in this space, Snowflake has the advantage of being a neutral vendor — and that has had great appeal to customers, who are concerned about vendor lock-in.

As Slootman told TechCrunch in February:

One of the key distinguishing architectural aspects of Snowflake is that once you’re on our platform, it’s extremely easy to exchange data with other Snowflake users. That’s one of the key architectural underpinnings. So content strategy induces network effect which in turn causes more people, more data to land on the platform, and that serves our business model.

When it rains it pours. Unity filed. JFrog filed. We still need to talk X-Peng. Corsair has filed as well. And there are still a host of companies that have filed privately, like Airbnb and DoorDash, that could drop a new filing at any moment. What an August!

Powered by WPeMatico

Luminar, the lidar startup that burst onto the autonomous vehicle scene in April 2017 after operating for years in secrecy, is merging with special purpose acquisition company Gores Metropoulos Inc., with a post-deal market valuation of $3.4 billion.

Gores Metropoulos, which is listed on the Nasdaq exchange, is a special purpose acquisition company, or SPAC, sponsored by an affiliate of The Gores Group, the global investment firm founded in the late 1980s by Alec Gores.

The SPAC merger comes just three months after Luminar hit a critical milestone and announced that Volvo would start producing vehicles in 2022 equipped with its lidar and a perception stack. The Luminar technology will be used to deploy an automated driving system for highways.

Luminar founder and CEO Austin Russell told TechCrunch that they wanted to go public at some point. But the momentum from the Volvo deal along with interest within public markets led the company to take the SPAC route, Russell said.

Luminar is the latest startup — and second lidar company — to turn to SPACs this summer in lieu of a traditional IPO process. In June, Velodyne Lidar struck a deal to merge with special purpose acquisition company Graf Industrial Corp., with a market value of $1.8 billion. Four electric vehicle startups have also skipped the traditional IPO path in recent months, opting instead to go public through a merger agreement with a SPAC, which are also known as blank check companies. Canoo, Fisker Inc., Lordstown Motors and Nikola Corp. have gone public via a SPAC merger this spring and summer.

Luminar said it was able to raise $170 million in private investment in public equity, or PIPE, by institutional investors, including Alec Gores, Van Tuyl Companies, Peter Thiel, Volvo Cars Tech Fund, Crescent Cove, Moore Strategic Ventures, GoPro founder Nick Woodman and VectoIQ, with the majority of the major existing investors participating. The transaction will also include a balance of about $400 million cash that has been held by Gores Metropoulos.

Once the transaction closes, Luminar will maintain its name and will be listed on Nasdaq under the ticker symbol LAZR. The deal is expected to close in the fourth quarter of 2020. Russell will continue to serve as CEO and Tom Fennimore will continue to serve as CFO. Alec Gores will join the Luminar board of directors upon closing of the transaction.

“This milestone is pivotal not just for us, but also for the larger automotive industry,” said Russell said in a statement. “Eight years ago, we took on a problem to which most thought there would be no technically or commercially viable solution. We worked relentlessly to build the tech from the ground up to solve it and partnered directly with the leading global automakers to show the world what’s possible. Today, we are making our next industry leap through our new long-term partnership with Gores Metropoulos, a team that has deep experience in technology and automotive and shares our vision of a safe autonomous future powered by Luminar.”

Luminar was founded by Russell in 2012, but it operated in secret for years until coming out of stealth in spring 2017 with backing from Thiel and others. Russell, who is now 25 years old, worked on the Luminar technology as a Thiel fellow, which gives young people $100,000 over two years to drop out of college and pursue their ideas.

Luminar raised $250 million prior to the SPAC announcement. The company now has 350 employees and operations in Silicon Valley as well as a factory in Orlando. Luminar said it plans to open an office in Detroit as well.

Lidar, light detection and ranging radar, measures distance using laser light to generate a highly accurate 3D map of the world around the car. The sensor is widely considered critical to the commercial deployment of autonomous vehicles. Automakers have also begun to view lidar as an important sensor to be used to beef up the capabilities and safety of its advanced driver assistance systems in the new cars trucks and SUVs available to consumers.

Volvo is one of those automakers. Luminar’s Iris lidar sensors — which TechCrunch has described as about the size of really thick sandwich and one-third smaller than its previous iterations — will be integrated in the roof of Volvo’s production vehicles, beginning in 2022.

Luminar also announced Monday that it has hired 16 people who worked on Samsung’s now dissolved DRVLINE team. Samsung once described the DRVLINE platform as an “open, modular, and scalable hardware and software-based platform” for the autonomous driving market. Earlier this year, TechCrunch reported that Samsung shuttered the DRVLINE/Smart Machines team.

Those hires are directly tied to Luminar’s strategy to capitalize on what Russell believes is the nearer term application of lidar in production vehicles, not robotaxis. Luminar is still working with companies seeking to commercialize robotaxis, but he believes it’s a longer-term play.

“I think that there are huge, long-term promises associated with robotaxis, but I really see that market taking off in the 2030s as opposed to the 2020s,” Russell said. Lidar used to support active driver safety system will be provides the kind of volume and economies of scale that are going to be driving this business, he added.

Powered by WPeMatico

In a turn of fortune, Airbnb today announced that it has filed to go public, albeit confidentially.

The move puts the home-sharing service on a path to a public offering sooner rather than later, and comes after reports that the company was prepping an IPO filing this month. Those same reports indicated that Airbnb could go public as soon as the end of the year.

A Q3 or Q4 Airbnb offering is therefore a distinct possibility.

Airbnb has mounted a comeback since COVID-19-related shutdowns slammed the travel market, tanking its revenues at the same time. Airbnb laid off nearly 2,000 workers, and took on expensive capital from external sources.

The company promised in 2019 that it would go public in 2020, but that pledge seemed far-off in the middle of the year. Since then, Airbnb has made noise about different parts of its business coming back to life, although changed by new travel and work and vacation patterns from its users.

If Airbnb has filed, we can presume that present results are good enough to get it life, else the firm would have not filed and would have simply gone public later. The question now becomes if its Q2 numbers were good enough to get it out the door, or if the company intends to update its S-1 filing with Q3 numbers, push the filing live and go public with more recovery time in its results.

Of course, such a course of action would put its public debut perilously close to the American election. And, Airbnb’s Q2 numbers are down not only from Q1 in revenue terms, but even more sharply from its year-ago results for the same calendar period. In short, Airbnb’s growth story may not be clear until Q3 numbers are tallied, a month and a half from now.

Airbnb joins other companies that have filed privately, like DoorDash, waiting in the wings for the right moment to go public, or the right set of results.

We’ll see, but the company’s public debut is back to being impending. Now the question becomes whether Airbnb intends to go public in an IPO, as the wording of its filing appears to suggest, or if a direct listing could still be in the cards. We think it’s more likely the former and not the latter, but, hey, in 2020 you never know.

Powered by WPeMatico

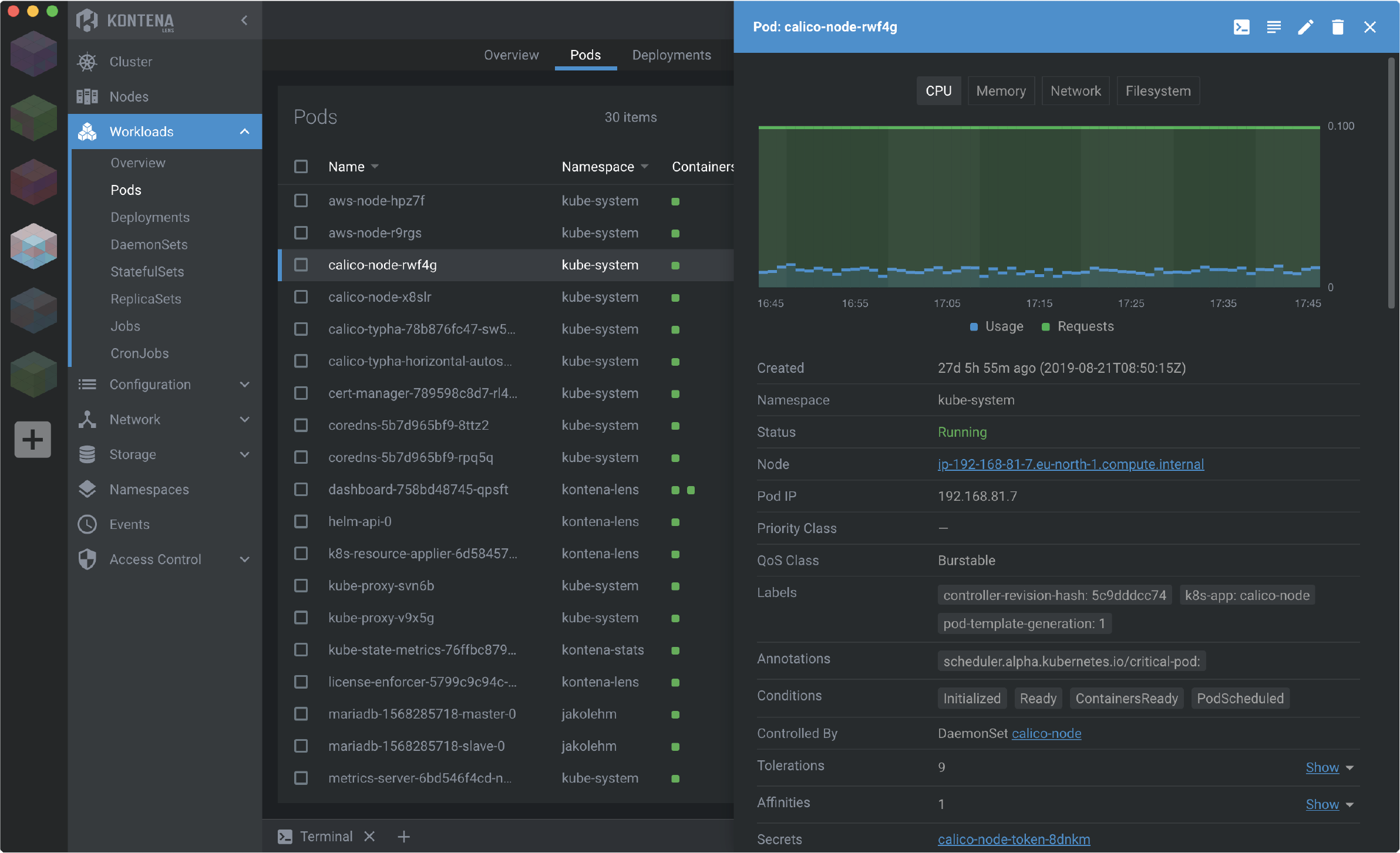

Mirantis, the company that recently bought Docker’s enterprise business, today announced that it has acquired Lens, a desktop application that the team describes as a Kubernetes-integrated development environment. Mirantis previously acquired the team behind the Finnish startup Kontena, the company that originally developed Lens.

Lens itself was most recently owned by Lakend Labs, though, which describes itself as “a collective of cloud native compute geeks and technologists” that is “committed to preserving and making available the open-source software and products of Kontena.” Lakend open-sourced Lens a few months ago.

Image Credits: Mirantis

“The mission of Mirantis is very simple: We want to be — for the enterprise — the fastest way to [build] modern apps at scale,” Mirantis CEO Adrian Ionel told me. “We believe that enterprises are constantly undergoing this cycle of modernizing the way they build applications from one wave to the next — and we want to provide products to the enterprise that help them make that happen.”

Right now, that means a focus on helping enterprises build cloud-native applications at scale and, almost by default, that means providing these companies with all kinds of container infrastructure services.

“But there is another piece of the story that’s always been going through our minds, which is, how do we become more developer-centric and developer-focused, because, as we’ve all seen in the past 10 years, developers have become more and more in charge off what services and infrastructure they’re actually using,” Ionel explained. And that’s where the Kontena and Lens acquisitions fit in. Managing Kubernetes clusters, after all, isn’t trivial — yet now developers are often tasked with managing and monitoring how their applications interact with their company’s infrastructure.

“Lens makes it dramatically easier for developers to work with Kubernetes, to build and deploy their applications on Kubernetes, and it’s just a huge obstacle-remover for people who are turned off by the complexity of Kubernetes to get more value,” he added.

“I’m very excited to see that we found a common vision with Adrian for how to incorporate Lens and how to make life for developers more enjoyable in this cloud-native technology landscape,” Miska Kaipiainen, the former CEO of Kontena and now Mirantis’ director of Engineering, told me.

He describes Lens as an IDE for Kubernetes. While you could obviously replicate Lens’ functionality with existing tools, Kaipiainen argues that it would take 20 different tools to do this. “One of them could be for monitoring, another could be for logs. A third one is for command-line configuration, and so forth and so forth,” he said. “What we have been trying to do with Lens is that we are bringing all these technologies [together] and provide one single, unified, easy to use interface for developers, so they can keep working on their workloads and on their clusters, without ever losing focus and the context of what they are working on.”

Among other things, Lens includes a context-aware terminal, multi-cluster management capabilities that work across clouds and support for the open-source Prometheus monitoring service.

For Mirantis, Lens is a very strategic investment and the company will continue to develop the service. Indeed, Ionel said the Lens team now basically has unlimited resources.

Looking ahead, Kaipiainen said the team is looking at adding extensions to Lens through an API within the next couple of months. “Through this extension API, we are actually able to collaborate and work more closely with other technology vendors within the cloud technology landscape so they can start plugging directly into the Lens UI and visualize the data coming from their components, so that will make it very powerful.”

Ionel also added that the company is working on adding more features for larger software teams to Lens, which is currently a single-user product. A lot of users are already using Lens in the context of very large development teams, after all.

While the core Lens tools will remain free and open source, Mirantis will likely charge for some new features that require a centralized service for managing them. What exactly that will look like remains to be seen, though.

If you want to give Lens a try, you can download the Windows, macOS and Linux binaries here.

Powered by WPeMatico

According to The Wall Street Journal, Airbnb could file confidentially to go public as early as this month. The same report states that Airbnb could follow that filing with an IPO before year’s end. Morgan Stanley and Goldman are helping the former startup with its IPO process, the Journal writes.

The news that Airbnb’s IPO could be back on caps a tumultuous year for the home-sharing unicorn, which promised in 2019 to go public in 2020. The company was widely tipped to be considering a direct listing before COVID-19 arrived, crashing the global travel market, and with it, Airbnb’s financial health.

Airbnb declined to comment on its IPO plans.

As travelers stayed home, the company was forced to sharply cut staff and take on billions in capital at prices that, compared to its late 2019-momentum, looked rather expensive.

But since those blows, Airbnb has begun to make noise about positive progress regarding its platform usage, and, implicitly, its financial performance.

In June, Airbnb said that between “May 17 to June 6, 2020, there were more nights booked for travel to Airbnb listings in the US than during the same time period in 2019,” and that “globally, over the most recent weekend (June 5-7), we saw year-over-year growth in gross booking value” for “the first time since February.”

And in July, the company said that its users had “booked more than 1 million nights’ worth of future stays at Airbnb listings” globally in a single day, the first time since March 3rd that that had happened.

Precisely how far Airbnb has financially clawed its way back is not clear. But the company’s cost basis in the wake of its layoffs could lower the revenue base it needs to recover to reach something akin to profitability, a traditional IPO benchmark, though one that has lost luster in recent years.

And with local travel taking off — slowly-improving airline occupancy rates are, therefore, not indicative of Airbnb’s performance or health — the company could have retooled its business in the wake of COVID to something that can still put up attractive revenues at strong margins.

Needless to say, I am hyped to read the Airbnb S-1, so the sooner it drops the happier I’ll be. Getting an in-depth look at what happened to the unicorn during COVID-19 is going to be fascinating.

Airbnb joins DoorDash, Coinbase, Palantir and others on our IPO shortlist. More as we have it.

Powered by WPeMatico

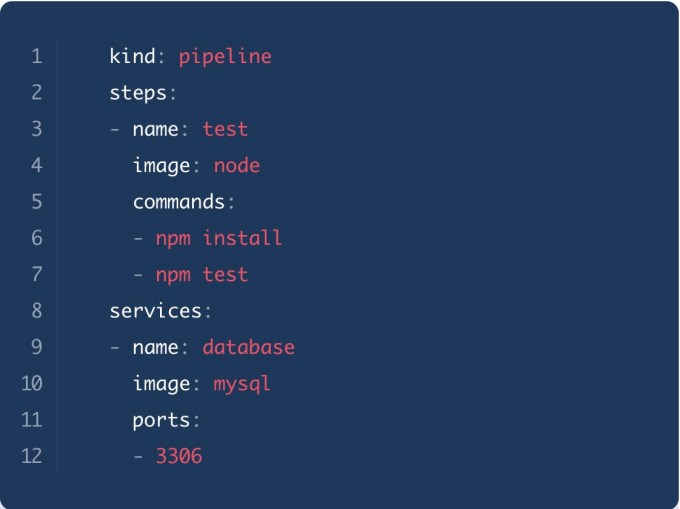

Harness has made a name for itself creating tools like continuous delivery (CD) for software engineers to give them the kind of power that has been traditionally reserved for companies with large engineering teams like Google, Facebook and Netflix. Today, the company announced it has acquired Drone.io, an open-source continuous integration (CI) company, marking the company’s first steps into open source, as well as its first acquisition.

The companies did not share the purchase price.

“Drone is a continuous integration software. It helps developers to continuously build, test and deploy their code. The project was started in 2012, and it was the first cloud-native, container-native continuous integration solution on the market, and we open sourced it,” company co-founder Brad Rydzewski told TechCrunch.

Drone delivers pipeline configuration information as code in a Docker container. Image: Drone.io

While Harness had previously lacked a CI tool to go with its continuous delivery tooling, founder and CEO Jyoti Bansal said this was less about filling in a hole than expanding the current platform.

“I would call it an expansion of our vision and where we were going. As you and I have talked in the past, the mission of Harness is to be a next-generation software delivery platform for everyone,” he said. He added that buying Drone had a lot of upside.”It’s all of those things — the size of the open-source community, the simplicity of the product — and it [made sense], for Harness and Drone to come together and bring this integrated CI/CD to the market.”

While this is Harness’ first foray into open source, Bansal says it’s just the starting point and they want to embrace open source as a company moving forward. “We are committed to getting more and more involved in open source and actually making even more parts of Harness, our original products, open source over time as well,” he said.

For Drone community members who might be concerned about the acquisition, Bansal said he was “100% committed” to continuing to support the open-source Drone product. In fact, Rydzewski said he wanted to team with Harness because he felt he could do so much more with them than he could have done continuing as a standalone company.

“Drone was a growing community, a growing project and a growing business. It really came down to I think the timing being right and wanting to partner with a company like Harness to build the future. Drone laid a lot of the groundwork, but it’s a matter of taking it to the next level,” he said.

Bansal says that Harness intends to also offer on the Harness platform a commercial version of Drone with some enterprise features, even while continuing to support the open source side of it.

Drone was founded in 2012. The only money it raised was $28,000 when it participated in the Alchemist Accelerator in 2013, according to Crunchbase data. The deal has closed and Rydzewski has joined the Harness team.

Powered by WPeMatico

As the Internet of Things proliferates, security cameras are getting smarter. Today, these devices have machine learning capability that helps the camera automatically identify what it’s looking at — for instance, an animal or a human intruder? Today, Cisco announced that it has acquired Swedish startup Modcam and is making it part of its Meraki smart camera portfolio with the goal of incorporating Modcam computer vision technology into its portfolio.

The companies did not reveal the purchase price, but Cisco tells us that the acquisition has closed.

In a blog post announcing the deal, Cisco Meraki’s Chris Stori says Modcam is going to up Meraki’s machine learning game, while giving it some key engineering talent, as well.

“In acquiring Modcam, Cisco is investing in a team of highly talented engineers who bring a wealth of expertise in machine learning, computer vision and cloud-managed cameras. Modcam has developed a solution that enables cameras to become even smarter,” he wrote.

What he means is that today, while Meraki has smart cameras that include motion detection and machine learning capabilities, this is limited to single camera operation. What Modcam brings is the added ability to gather information and apply machine learning across multiple cameras, greatly enhancing the camera’s capabilities.

“With Modcam’s technology, this micro-level information can be stitched together, enabling multiple cameras to provide a macro-level view of the real world,” Stori wrote. In practice, as an example, that could provide a more complete view of space availability for facilities management teams, an especially important scenario as businesses try to find safer ways to open during the pandemic. The other scenario Modcam was selling was giving a more complete picture of what was happening on the factory floor.

All of Modcams employees, which Cisco described only as “a small team,” have joined Cisco, and the Modcam technology will be folded into the Meraki product line, and will no longer be offered as a standalone product, a Cisco spokesperson told TechCrunch.

Modcam was founded in 2013 and has raised $7.6 million, according to Crunchbase data. Cisco acquired Meraki back in 2012 for $1.2 billion.

Powered by WPeMatico

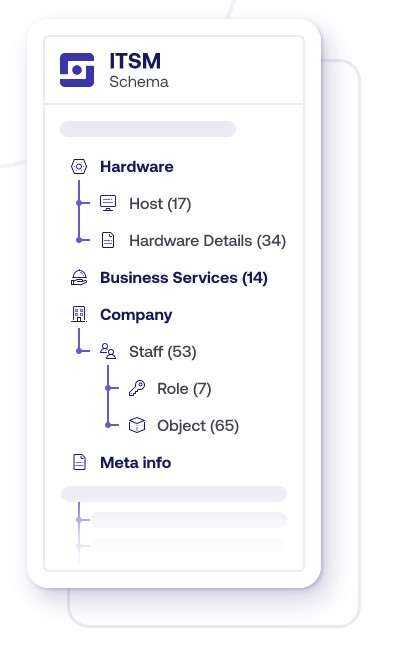

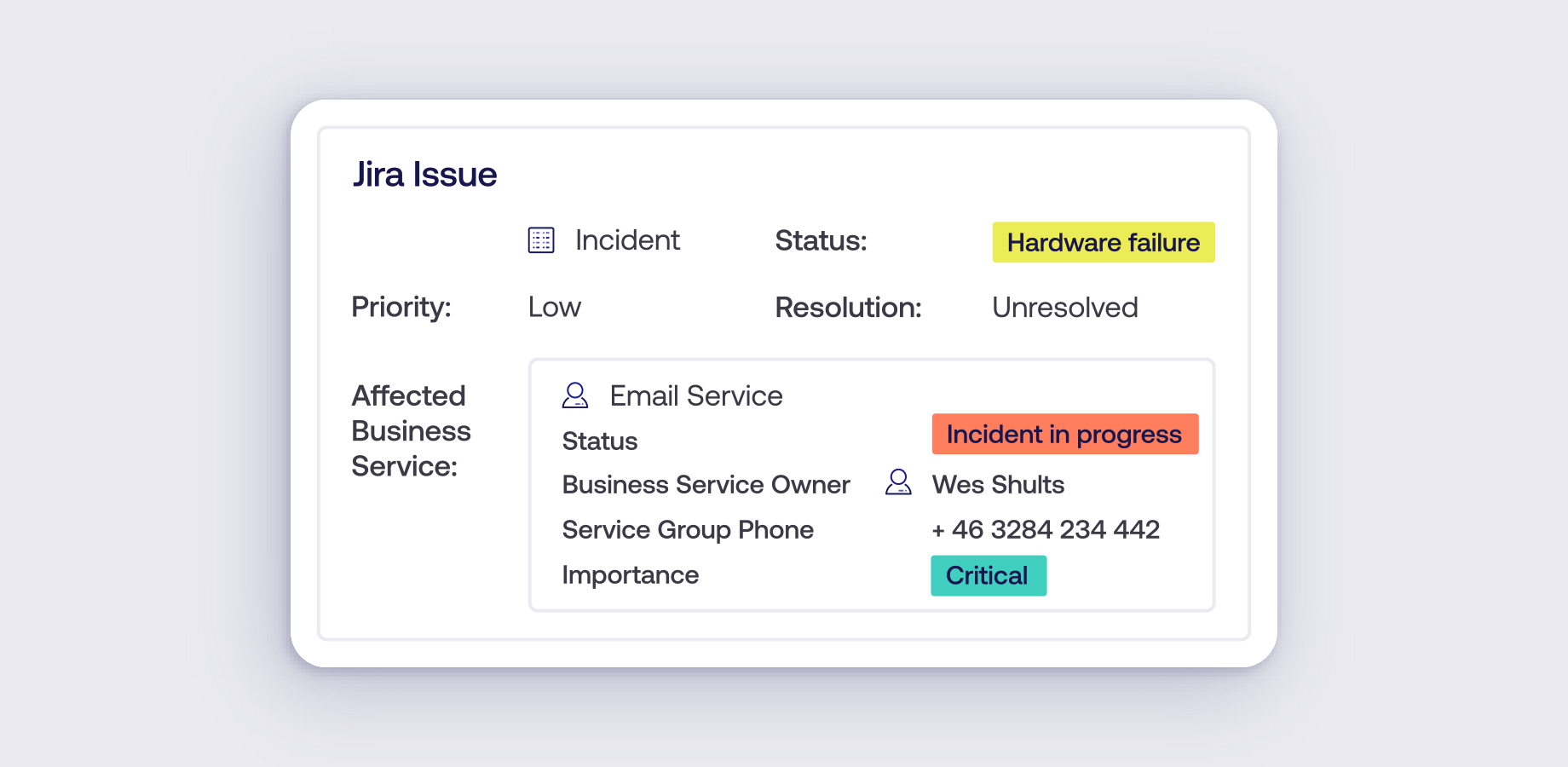

Atlassian today announced that it has acquired Mindville, a Jira-centric enterprise asset management firm based in Sweden. Mindville’s more than 1,700 customers include the likes of NASA, Spotify and Samsung.

Image Credits: Atlassian

With this acquisition, Atlassian is getting into a new market, too, by adding asset management tools to its lineup of services. The company’s flagship product is Mindville Insights, which helps IT, HR, sales, legal and facilities to track assets across a company. It’s completely agnostic as to which assets you are tracking, though, given Atlassian’s user base, most companies will likely use it to track IT assets like servers and laptops. But in addition to physical assets, you also can use the service to automatically import cloud-based servers from AWS, Azure and GCP, for example, and the team has built connectors to services like Service Now and Snow Software, too.

Image Credits: Mindville

“Mindville Insight provides enterprises with full visibility into their assets and services, critical to delivering great customer and employee service experiences. These capabilities are a cornerstone of IT Service Management (ITSM), a market where Atlassian continues to see strong momentum and growth,” Atlassian’s head of tech teams Noah Wasmer writes in today’s announcement.

Co-founded by Tommy Nordahl and Mathias Edblom, Mindville never raised any institutional funding, according to Crunchbase. The two companies also didn’t disclose the acquisition price.

Like some of Atlassian’s other recent acquisitions, including Code Barrel, the company was already an Atlassian partner and successfully selling its service in the Atlassian Marketplace.

“This acquisition builds on Atlassian’s investment in [IT Service Management], including recent acquisitions like Opsgenie for incident management, Automation for Jira for code-free automation, and Halp for conversational ticketing,” Atlassian’s Wasmer writes.

The Mindville team says it will continue to support existing customers and that Atlassian will continue to build on Insight’s tools while it works to integrate them with Jira Service Desk. That integration, Atlassian argues, will give its users more visibility into their assets and allow them to deliver better customer and employee service experiences.

Image Credits: Mindville

“We’ve watched the Insight product line be used heavily in many industries and for various disciplines, including some we never expected! One of the most popular areas is IT Service Management where Insight plays an important role connecting all relevant asset data to incidents, changes, problems, and requests,” write Mindville’s founders in today’s announcement. “Combining our solutions with the products from Atlassian enables tighter integration for more sophisticated service management, empowered by the underlying asset data.”

Powered by WPeMatico

After raising $15 million in financing from one of technology’s most successful global investment firms, the Los Angeles-based consumer goods rental company Joymode is selling itself to an early-stage retail investment firm out of New York, XRC Labs.

Joymode’s founder Joe Fernandez will continue on as an advisor to Joymode as the company moves to pivot its business to focus on retail partnerships.

The relationship with XRC Labs’ Pano Anthos began after a small pilot integration between Joymode and Walmart launched in late 2019. “[It] became obvious that we should go all in on retail partnerships,” according to Fernandez. And as the company cast about for partners to pursue the strategy, Anthos and his firm, XRC, kept being mentioned, Fernandez said.

The precise terms of the deal with XRC Labs were undisclosed, but Joymode will become a wholly owned business of XRC and could potentially return to market to raise additional funds from additional investors, according to Fernandez.

“We could never crack growth at the scale we needed,” said Fernandez of the company’s initial business. “From day one, my belief was Joymode was going to be huge or dead. We grew, but given the cost structure of our business it put a lot of pressure on the business to grow exponentially fast. Everyone loved the idea but the actual growth was slower than we needed it to be.”

Though Joymode wasn’t a success, Fernandez said he can’t fault his investors or his team. “We got to iterate through every possible idea we had. Literally every idea we had was exhausted… We failed and that’s a bummer, but we got a fair shot,” he said.

What remains of the company is an inventory management system on the back end and a service that will allow any retailer to get involved in the rental business going forward.

“Part of the thesis was that by making things available for rental, people would want to do more stuff,” said Fernandez, but what happened was that consumers needed additional reasons to use the company’s service, and there weren’t enough events to drive demand.

“I believe that the inventory management system we made was incredible and it will be a standard for retailers doing rentals going forward,” he said.

As the company turned to retailers, the rental option became a way to generate revenue through additional products. “All the accessories that made the event even better,” said Fernandez. “Add-ons, try before you buy, experiential things that are just much more complete in a retail environment.”

At Joymode, the problem was that the company was owning the inventory, which created a high fixed cost. “We never felt confident with the growth in LA to justify the expense of opening in another city,” Fernandez said. “If we had cracked user acquisition in LA we would have rolled it out in a bunch of places.”

Ultimately, Joymode members saved $50 million by using Joymode to rent products rather than buying them. In all, the company acquired 2,000 unique products — from beach and camping equipment to video games, virtual reality headsets to cooking appliances. On a given weekend, roughly 30,000 products would ship from the company’s warehouse to locations across Southern California.

At XRC Labs, a firm launched in 2015 to support the consumer goods and brand space, Joymode will complement an accelerator that raises between $6 million and $9 million every two years and manages a growth fund that could reach $50 million in assets under management.

For Anthos, the best corollary to Joymode’s business could be the rental business at Home Depot. “Home Depot’s rental business is over $1 billion per year,” Anthos said. “There’s going to be this enormous component of our society and for them renting will be not just a more sustainable but reasonable option. They’re going to want to rent because they don’t want to own it.”

Joymode was backed by TenOneTen, Wonder, Struck Ventures, Homebrew and Naspers (now Prosus).

Powered by WPeMatico

Now that I’ve offered an overview to help you think through where concentrated stock sits in your overall plan, let’s take a closer look at why selling can be challenging for some.

In the following section, I reveal the facts of the concentrated stock “get rich” myths that reside in the minds of many first-time concentrated stock owners, and I show why it is prudent to consider greater diversification.

Keep reading to learn more about the benefits of diversification, discover how much company stock is likely too much to hold, and the options you have when it comes to diversifying strategically.

There are several hard facts to keep in mind in contemplating maintaining a concentrated position:

The odds of any new IPO being among the top 4% is just slightly better than hitting your lucky number on the roulette wheel. But is your investment portfolio success and the odds of achieving your long-term financial goals something you want to spin the wheel on?

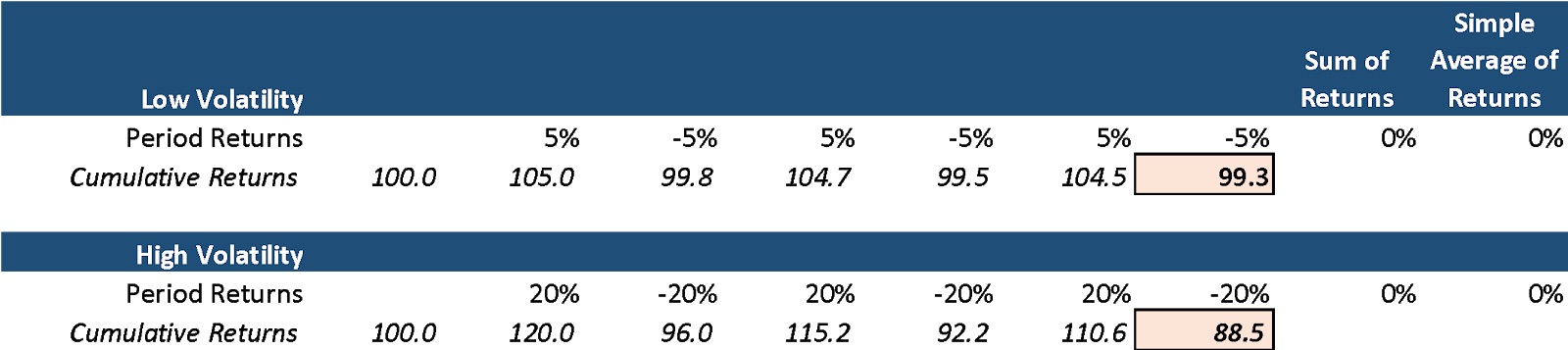

Excess volatility can harm returns. Note the example below that shows the comparison between a low-volatility diversified portfolio versus a high-volatility concentrated portfolio. Despite the same simple average return, the low-volatility portfolio below materially outperforms the high-volatility portfolio.

Image Credits: Peyton Carr

Beyond the math, unexpected spikes in volatility can cause significant price declines. Volatility increases the chances that an investor reacts emotionally and makes a poor investment decision. I’ll cover the behavioral finance aspect of this later. Lowering your portfolio volatility can be as simple as increasing your portfolio diversification.

The Russell 3000, an index representing the 3,000 largest U.S.-based publicly traded companies, has lower volatility when compared against 95%+ of all single stocks. So, how much return do you give up for having lower volatility?

According to Northern Trust Research, the 5.96% annualized average return of the Russell 3000 is 0.73% more than the 5.23% return of the median stock. Additionally, owning the Russell 3000, rather than a single stock, eliminates the likelihood of catastrophic loss scenarios — more than 20% of shares averaged a loss of more than 10% per year over a 20-year time frame.

If this establishes that the avoidance of overly concentrated portfolios is important, how much stock is too much? And at what price should you sell?

We consider any stock position or exposure greater than 10% of a portfolio to be a concentrated position. There is no hard number, but the appropriate level of concentration is dependent on several factors, such as your liquidity needs, overall portfolio value, the appetite for risk and the longer-term financial plan. However, above 10% and the returns and volatility of that single position can begin to dominate the portfolio, exposing you to high degrees of portfolio volatility.

The company “stock” in your portfolio often is only a fraction of your overall financial exposure to your company. Think about your other sources of possible exposure such as restricted stock, RSUs, options, employee stock purchase programs, 401k, other equity compensation plans, as well as your current and future salary stream tied to the company’s success. In most cases, the prudent path to achieving your financial goals involves a well-diversified portfolio.

Facts aside, maintaining a concentrated position in your company stock is far more tempting than taking a more measured approach. Token examples like Zuckerberg and Bezos tend to outshine the dull rationale of reality, and it’s hard to argue against the possibility of becoming fabulously wealthy by betting on yourself. In other words, your emotions can get the best of you.

But your goals — not your emotions — should be driving your investment strategy and decisions regarding your stock. Your investment portfolio and the company stock(s) within it should be used as tools to achieve those goals.

So first, we’ll take a deep dive into the behavioral psychology that influences our decision-making.

Despite all the evidence, sometimes that little voice remains.

“I want to hold the stock.”

Why is it so hard to shake? This is a natural human tendency. I get it. We have a strong impetus to rationalize our biases and not believe we are vulnerable to being influenced by them.

Becoming attached to your company is common, since after all, that stock has made you, or has the potential of making you wealthy. More often than not, selling and diversifying is the tough, but more rational decision.

Numerous studies have furnished insights into the correlation between investing and psychology. Many unrecognized psychological barriers and behavioral biases can influence you to hold concentrated stock even when the data shows that you should not.

Understanding these biases can be helpful when deciding what to do with your stock. These behavioral biases are hard to spot and even harder to overcome. However, awareness is the first step. Here are a few more common behavioral biases, see if any apply to you:

Familiarity bias: Familiarity is likely why so many founders are willing to hold concentrated positions in their own company’s stock. It is easy to confuse the familiarity with your own company with the safety in the stock. In the stock market, familiarity and safety are not always related. A great (safe) company sometimes can have a dangerously overvalued stock price, and terrible companies sometimes have terrifically undervalued stock prices. It’s not just about the quality of the company but the relationship between the quality of a company and its stock price that dictates whether a stock is likely to perform well in the future.

Another way this manifests is when a founder has less experience with stock market investing and has only owned their company stock. They may think the market has more risk than their company when in actuality, it is usually safer than holding just their individual position.

Overconfidence: Every investor is exhibiting overconfidence when they hold an overly concentrated position in an individual stock. Founders are likely to believe in their company; after all, it already achieved enough success to IPO. This confidence can be misplaced in the stock. Founders often are reluctant to sell their stock if it has been going up since they believe it will continue to go up. If the stock has sold off, the opposite is true, and they are convinced it will recover. Often, it is challenging for founders to be objective when they are so close to the company. They commonly believe that they have unique information and know the “true” value of the stock.

Anchoring: Some investors will anchor their beliefs to something they experienced in the past. If the price of the concentrated stock is down, investors may anchor their belief that the stock is worth its recent previous higher value and be unwilling to sell. This previous value of the stock is not an indicator of its real value. The real value is the current price where buyers and sellers exchange the stock while incorporating all presently available information.

Endowment effect: Many investors tend to place a higher value on an asset they currently own than if they did not own it at all. It makes it harder to sell. An excellent way to check for the endowment effect is to ask yourself: “If I did not own these shares, would I purchase them today at this price?” If you are not willing to purchase the shares at this price today, it likely means you are only holding onto the shares because of the endowment effect.

A fun spin on this is to look into the IKEA effect study, which demonstrates that people assign more value to something that they made than it is potentially worth.

When framed this way, investors can make more intentional decisions on whether to continue holding concentrated stock or selling. At times, these biases are hard to spot, which is why having a second person, a co-pilot, or an advisor, is helpful.

Congratulations to those of you with a concentrated stock position in your company; it is hard-earned and likely represents a material wealth. Understand, there is no “right” answer when it comes to managing concentrated stock. Each situation is unique, so it is essential to speak with a professional about options specific to your situation.

It starts with having a financial plan, complete with specific investment goals that you want to achieve. Once you have a clear picture of what you want to accomplish, you can look at the facts in a new light and gain a deeper appreciation for the dangers of holding a concentrated position in company stock versus the benefits of diversification, considering all of the implications and opportunities involved in rational decision-making and investment behavior.

Most individuals understand they can simply and directly sell their equity, but there are a variety of other strategies. Some of these opportunities may be far better at minimizing taxes or better at achieving the desired risk or return profile. Some might wonder what the best timing is to sell. I will cover these topics in the final article of the series.

Powered by WPeMatico