exit

Auto Added by WPeMatico

Auto Added by WPeMatico

Fivetran, the data connectivity startup, had a big day today. For starters it announced a $565 million investment on a $5.6 billion valuation, but it didn’t stop there. It also announced its second acquisition this year, snagging HVR, a data integration competitor that had raised more than $50 million, for $700 million in cash and stock.

The company last raised a $100 million Series C on a $1.2 billion valuation, increasing the valuation by over 5x. As with that Series C, Andreessen Horowitz was back leading the round, with participation from other double dippers General Catalyst, CEAS Investments, Matrix Partners and other unnamed firms or individuals. New investors ICONIQ Capital, D1 Capital Partners and YC Continuity also came along for the ride. The company reports it has now raised $730 million.

The HVR acquisition represents a hefty investment for the startup, grabbing a company for a price that is almost equal to all the money it has raised to date, but it provides a way to expand its market quickly by buying a competitor. Earlier this year Fivetran acquired Teleport Data as it continues to add functionality and customers via acquisition.

“The acquisition — a cash and stock deal valued at $700 million — strengthens Fivetran’s market position as one of the data integration leaders for all industries and all customer types,” the company said in a statement.

While that may smack of corporate marketing-speak, there is some truth to it, as pulling data from multiple sources, sometimes in siloed legacy systems, is a huge challenge for companies, and both Fivetran and HVR have developed tools to provide the pipes to connect various data sources and put it to work across a business.

Data is central to a number of modern enterprise practices, including customer experience management, which takes advantage of customer data to deliver customized experiences based on what you know about them, and data is the main fuel for machine learning models, which use it to understand and learn how a process works. Fivetran and HVR provide the nuts and bolts infrastructure to move the data around to where it’s needed, connecting to various applications like Salesforce, Box or Airtable, databases like Postgres SQL or data repositories like Snowflake or Databricks.

Whether bigger is better remains to be seen, but Fivetran is betting that it will be in this case as it makes its way along the startup journey. The transaction has been approved by both companies’ boards. The deal is still subject to standard regulatory approval, but Fivetran is expecting it to close in October.

Powered by WPeMatico

Gingko Bioworks, a synthetic biology company now valued at around $15 billion, begins trading on the New York Stock Exchange today.

Gingko’s market debut is one of the largest in biotech history. It’s expected to raise about $1.6 billion for the company. It’s also one of the biggest SPAC deals done to date — Gingko is going public through a merger with Soaring Eagle Acquisition Corp., which was announced in May.

Shares opened at $11.15 each this morning under the ticker DNA — biotech dieharders will recognize it as the former ticker used by Genentech.

The exterior of the NYSE is decked out in Gingko décor. The imagery is clearly sporting Jurassic Park themes, as MIT Tech Review’s Antonio Regalado pointed out. It’s probably intentional: Jason Kelly, the CEO of Ginkgo Bioworks, has been re-reading “Jurassic Park” this week, he tells TechCrunch.

The décor also sports a company motto: “Grow everything.”

Ginkgo was founded in 2009, and now bills itself as a synthetic biology platform. That’s essentially premised on the idea that one day, we’ll use cells to “grow everything,” and Gingko’s plan is to be that platform used to do that growing.

Kelly, who often uses language borrowed from computing to describe his company, likens DNA to code. Gingko, he says, aims to “program cells like you can program computers.” Ultimately, those cells can be used to make stuff: like fragrances, flavors, materials, drugs or food products.

The biggest lingering question over Gingko, ever since the SPAC deal was announced, has centered on its massively high valuation. When Moderna, now a household name thanks to its COVID-19 vaccines, went public in 2018, the company was valued at $7.5 billion. Gingko’s valuation is double that number.

“I think that surprises people to be honest,” Kelly says.

Ginkgo’s massive valuation seems even starker when you look at its existing revenues. SEC documents show that the company pulled in $77 million in revenue in 2020, which increased to about $88 million in the first six months of 2021 (per an August investor call). The company has also reported losses: including $126.6 million in December 2020 and $119.3 million in 2019.

Gingko is aiming to increase revenue a significant amount in 2021. SEC documents initially noted that the company aimed to draw about $150 million in revenue in 2021, but the August earning call updated that total for the year to over $175 million.

Gingko aims to make money in two ways: first it contracts with manufacturers during the research and development phase (i.e. while the company works out how to manufacture a cell that spits out a certain fragrance, bio-based nylon or meatless burger). That process happens in Gingko’s “foundry,” a massive factory for bioengineering projects.

This source of money is already starting to flow. Gingko reported $59 million in foundry revenue for 2020, and anticipates $100 million in 2021, per the August investor call.

This revenue, though, isn’t covering the full costs of Gingko’s operations, according to the information shared by the company in SEC documents. It is covering an increasing share, though, and as Gingko scales up its platform, costs will come down. Based on fees alone, Kelly projects Gingko will break even by 2024 or 2025.

The second type of revenue comes from royalties, milestone payments or, in some cases, equity stakes in the companies that go on to sell products, like fragrances or meatless burgers, made using Gingko’s facilities or know-how. It’s this source of income that will make up the vast majority of the company’s future worth, according to its expectations.

Once the product is made and marketed by another company, it requires little to no more work on Gingko’s part — all the company does is collect cash.

The company is often hesitant to incorporate these earnings into projections, because they rely on other companies bringing products to market. That means it’s hard to know for sure when these downstream payments will emerge. “In our models, we are very sensitive that, at the end of the day, they’re not our products. I cannot predict when Roche might bring a drug to market and give me my milestones,” says Kelly.

Kelly says there’s evidence this model will start to work in the near-term.

Gingko earned a “bolus” milestone payment of 1.5 million shares of The Cronos Group, a cannabis company, for developing a commercially viable, lab-grown rare cannabinoid called CBG for commercial use (there are seven more in strains development, says Kelly). These milestone payments (in cash or shares) are earned when a company achieves some predetermined goal using Gingko’s platform.

Gingko has also worked with Aldevron to manufacture an enzyme critical to the production of mRNA vaccines, and plans to collect royalty payments from that relationship — though no foundry fees were collected from this project.

Finally, Gingko has negotiated an equity stake in Motif Foodworks, a spinout company based on its technology. That company has so far raised about $226 million, and will aim to launch a lab-grown beef product developed at Gingko’s foundry, paying Gingko the aforementioned foundry fees already for this contribution.

This rich source of cash will depend a lot on the outside contractor’s ability to manufacture and sell products made using Gingko’s platform. This opens the company up to some risk that’s beyond its control. Maybe, for instance, it turns people don’t want bio-manufactured meat as much as many anticipated — that means some types of downstream payments may not materialize.

Kelly says he’s not particularly worried about this. Even if one particular program fails, he’s planning on having so many programs running that one or two are bound to succeed.

“I’m just sorta like: some will work, some won’t work. Some will take a year, some will take three years. It doesn’t really matter, as long as everybody is working with us,” he says. “Apple doesn’t stress about what apps are going to be the next big app in the app store,” he continues.

One key metric to watch for Gingko going forward will be how many new cell programs they’re managing to close. So far, Gingko has added 30 programs this year, says Kelly. Last year, there were 50 programs.

Remember: Some of the projects are Gingko spinouts, like Motif Foodworks, not customers that come to the platform on their own. And historically, the number of companies Gingko has partnered with has been a point of criticism. Per SEC documents, the majority of revenue came from two large partners in 2020 — though Kelly told Business Insider that this was a pandemic-related downturn.

The more programs Gingko has, the more it becomes insulated from the success or failure of any one product. Plus it’s a sign that people are at least using the “app store” for biology.

“The biggest value driver of Gingko is how quickly we add programs,” Kelly says.

Powered by WPeMatico

At first blush, the $12 billion Intuit-Mailchimp deal might not make a heck of a lot of sense. But people tend to pigeonhole companies, and in this case they might see Intuit as purely a financial software company and Mailchimp as an email marketing firm and nothing more. If that’s as far as your perspective goes, the deal is confusing. From a wider lens, however, there’s more to both companies than you might think.

Let’s start with Intuit. If you go to the company website and scan the product set, it’s clearly all about managing finances for consumer and small businesses alike. The latter category appears to be what the company wants to exploit and expand upon with this deal.

Prior to yesterday’s news, Intuit’s biggest acquisition had been on the consumer side buying Credit Karma for $7.1 billion last year. That deal gave the company’s customers a way to access their credit scores outside of the big three reporting companies: Experian, Equifax and TransUnion. Apparently not content with only that transaction, it set its sights on Mailchimp to throw some money at the business side of the house.

Powered by WPeMatico

Quizlet, a flashcard tool turned artificial intelligence-powered tutoring platform, is planning an initial public offering nearly a year after it was valued at $1 billion. According to people familiar with the matter, Quizlet is considerably far along in the process to go public. A recent job filing shows that it is hiring for senior roles to “help build the financial systems and processes as we move towards an IPO.”

In an email to TechCrunch, the San Francisco-based edtech startup declined to comment. Quizlet hasn’t said much about its revenue specifics or if it’s profitable. Last year, the still-private startup claimed it was growing revenue 100% annually. On its website, Quizlet says that it has 60 million monthly learners, up 10 million learners compared to its 2018 totals.

Quizlet has built a large-scale business around simple to share and simple to use products. Its free flashcard maker helps students spin up study guides on topics to prepare for exams. Those insights fuel Quizlet Plus, the startup’s subscription product that charges $47.88 a year for access to more features, including tutoring services.

Quizlet’s tutoring arm, also known as Quizlet Learn, is the company’s most popular offering, per CEO Matthew Glotzbach. As a student goes through the system, Quizlet Learn consistently assesses students to see where they are making mistakes — and where they are making progress.

“It obviously doesn’t yet replace and can’t come anywhere close to replacing a human, but it can provide that guidance and point you in the right direction and help you spend your time in the right places,” he said. “Just even helping you set goals is such a critical step in learning.”

Most recently, Quizlet announced the launch of explanations, a feature that offers a step-by-step solution guide for problem sets from popular textbooks. The feature is “written and verified by experts” and is aimed to help “students better understand the reasoning and thought process behind study questions so they can practice and apply their learnings on their own,” it said in a statement. It also reclaimed the Q from its less fortunate predecessor, amid an entire rebrand.

Quizlet’s quiet march toward the public markets has been slow yet steady. The startup was founded in 2005 by a 15-year-old, Andrew Sutherland. It was fully bootstrapped until 2015. Glotzbach, who was previously an executive at YouTube, then joined in 2016. The startup still doesn’t appear to have a CFO, which is rare for companies that are going public.

Quizlet has raised a majority of its $62 million in venture capital under Glotzbach. Now, investors in the company include General Atlantic, Owl Ventures, Union Square Ventures, Costanoa Ventures and Altos Ventures.

Quizlet’s pursuit of the public markets comes as other edtech companies are proving the market’s reception to the sector. Duolingo, for example, is another consumer-focused education company, albeit one that focuses on one vertical versus Quizlet’s choice to stay broad. Duolingo went public in July, and is currently trading above its open price at $169.75 per share.

Powered by WPeMatico

Houseparty, the social video chat app acquired by Fortnite maker Epic Games for a reported $35 million back in 2019, is shutting down. The company says Houseparty will be discontinued in October when the app will stop functioning for its existing users; it will be pulled from the app stores today, however. Related to this move, Epic Games’ “Fortnite Mode” feature, which leveraged Houseparty to bring video chat to Fortnite gamers, will also be discontinued.

Founded in 2015, Houseparty offered a way for users to participate in group video chats with friends and even play games, like Uno, trivia, Heads Up and others. Last year, Epic Games integrated Houseparty with Fortnite, initially to allow gamers to see live feeds from friends while gaming, then later adding support to livestream gameplay directly into Houseparty. At the time, these integrations appeared to be the end goal that explained why Epic Games had bought the social startup in the first place.

Now, just over two years after the acquisition was announced, and less than half a year since support for livestreaming was added to the app, Houseparty is shutting down.

The company didn’t offer any solid insight into what, at first glance, feels like an admission of failure to capitalize on its acquisition. But the reality is that Epic Games may have something larger in store beyond just video chat. That said, all Epic Games would say today is that the Houseparty team could no longer give the app the attention it required — a statement that indicates an executive decision to shift the team’s focus to other matters.

While none of the Houseparty team members are being let go as a result of this move, we’re told, they will be joining other teams where they will work on new ways to allow for “social interactions” across the Epic Games family of products. The company’s announcement hinted that those social features would be designed and built at the “metaverse scale.”

The “metaverse” is an increasingly used buzzword that references a shared virtual environment, like those provided by large-scale online gaming platforms such as Fortnite, Roblox and others. Facebook, too, claims the metaverse is the next big gambit for social networking, with CEO Mark Zuckerberg having described it as an “embodied internet that you’re inside of rather than just looking at.”

To some extent, Fortnite has begun to embrace the metaverse by offering non-gaming experiences like online concerts you attend as your avatar, and other live events. Ahead of its shutdown, Houseparty also toyed with live events that users would co-watch and participate in alongside their friends.

An Epic Games spokesperson tells TechCrunch the Houseparty team has worked on (and continues to work on) a number of other projects that focus on social. But some of the “multiple, larger projects” Epic Games has in the works remain undisclosed, we’re told.

In terms of social products, Houseparty’s technology now underpins all of Fortnite voice chat and the features they built are widely available for free to developers through Epic Games Services. They also worked on building out new social experiences, which have ranged from the social RSVP functions for Fortnite’s global events, like the recent Ariana Grande concert, to the upcoming “Operation: Sky Fire” event for collaborating quests and other game mechanics. More social functionality and new experiences are also being built into Fortnite’s user-generated content platform, Create Mode.

While it may seem odd to close an app that only last year experienced a boost in usage due to the pandemic, it appears the COVID bump didn’t have staying power.

At the height of lockdowns, Houseparty had reported it had gained 50 million new sign-ups in a month’s time as users looked to video apps to connect with family and friends while the world was shut down. But as the pandemic wore on, other video chat experiences gained more ground. Zoom, which had established itself as an essential tool for remote work, became a tool for hanging out with friends after-hours, as well. Facebook also started to eat Houseparty’s lunch with its debut of drop-in video chat “Rooms” last year, which offered a similar group video experience. And bored users shifted to audio-based social networking on apps like Clubhouse or Twitter Spaces.

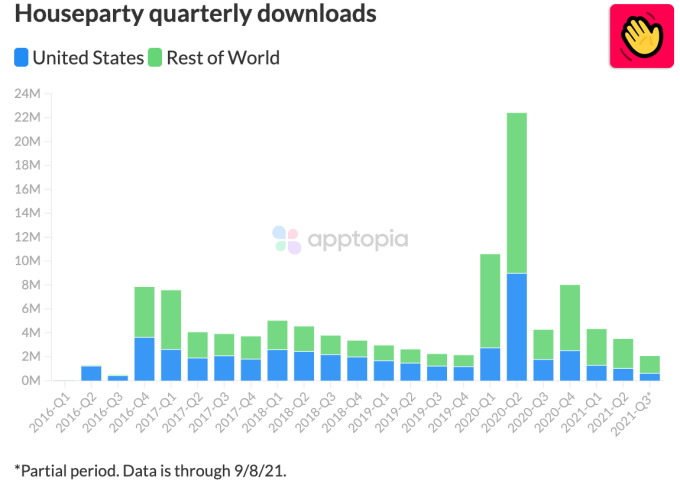

Image Credits: Apptopia

According to data from Apptopia, Houseparty has been continually declining since the pandemic bump. To date, its app has seen a total of 111 million downloads across iOS and Android, with the majority (63 million) on iOS. The U.S. was Houseparty’s largest market, accounting for 43.4% of downloads, followed by the U.K. (9.8%), then Germany (5.6%).

Epic Games, meanwhile, said the app served “tens of millions” of users worldwide. It insists the closure wasn’t decided lightly, nor was the decision to shutter “Fortnite Mode” made due to lack of adoption.

Houseparty will alert users to the shutdown via in-app notifications ahead of its final closure in October. At that point, Fortnite Mode will also no longer be available.

Powered by WPeMatico

PayPal Holdings, the U.S. fintech company, announced an acquisition of Paidy, a Japanese buy now, pay later (BNPL) service platform, for approximately $2.7 billion (300 billion yen), mostly in cash, to enhance its business in Japan.

The transaction completion, including the regulatory approval, is expected in the fourth quarter of 2021.

After the acquisition, the Japan-based company will continue to operate its existing business and maintain the brand while the leaders, Paidy’s president and CEO Riku Sugie and founder and executive chairman Russell Cummer, keep their positions.

Japan is the third largest e-commerce market in the world, and so this is a significant move by PayPal to gain more market share both in the country and the region, specifically in the area of providing deferred payment services as an alternative to credit cards.

PayPal has long played nice with payment cards — users can upload details of their cards to PayPal and use it as a kind of digital wallet to manage how they pay for things online through it — but it got its start actually as a payment platform in itself, where people could pay into and out of PayPal accounts. Paidy is, in that sense, a strengthening of PayPal’s first-party rails, providing a way to “own” that flow of money on its own infrastructure, not involving the card networks.

Paidy is basically a two-sided payments service, acting as a middleman between consumers and merchants in Japan. Using machine learning it determines the creditworthiness of a consumer related to a particular purchase, and then it underwrites those transactions in seconds, guaranteeing payments to merchants. Consumers then make deferred payment to Paidy for those goods.

Paidy’s platform, which offers a monthly payment installment service branded “3-Pay”, enables shoppers to make purchases online and then pay for them each month in a consolidated bill at a convenience store or via bank transfer.

“Paidy pioneered buy now, pay later solutions tailored to the Japanese market and quickly grew to become the leading service, developing a sizable two-sided platform of consumers and merchants,” said Peter Kenevan, vice president, head of Japan at PayPal.

Paidy has more than 6 million registered users, and the plan is to integrate PayPal and other digital and QR wallets with Paidy Link to connect further online and offline merchants.

In April 2021, the Japan-based company launched Paidy Link, allowing users to link digital wallets with their Paidy account. PayPal was the first digital wallet partner to integrate with Paidy Link.

“PayPal was a founding partner for Paidy Link and we look forward to looking together to create even more value,” Sugie said in a statement.

“Japan has been a vibrant environment for our growth to date and we’re honored to have our team’s hard work and potential recognized by a global leader. Together with PayPal, we will be able to further achieve our mission of taking the hassle out of shopping,” Cummer said.

Powered by WPeMatico

Rivian, the electric vehicle startup backed by a host of institutional and strategic investors, including Ford and Amazon, has confidentially filed paperwork with the U.S. Securities and Exchange Commission to go public.

The size and price range for the proposed offering have yet to be determined. The initial public offering is expected to take place after the SEC completes its review process, subject to market and other conditions, the brief statement said.

The confidential filing comes less than two months since Rivian announced it had closed a $2.5 billion private funding round led by Amazon’s Climate Pledge Fund, D1 Capital Partners, Ford Motor and funds and accounts advised by T. Rowe Price Associates Inc. Third Point, Fidelity Management and Research Company, Dragoneer Investment Group and Coatue also participated in that round.

The company did not share a post-money valuation at the time of the July 2021 announcement.

The electric automaker, which now employs 7,000 people, is preparing to deliver its R1T pickup truck in September. The road to produce the R1T and an accompanying SUV requires capital, which Rivian has had little trouble raising.

Rivian has raised roughly $10.5 billion to date. In January, the company brought in $2.65 billion from existing investors T. Rowe Price Associates Inc., Fidelity Management and Research Company, Amazon’s Climate Pledge Fund, Coatue and D1 Capital Partners. New investors also participated in that round, which pushed Rivian’s valuation to $27.6 billion, a source familiar with the investment round told TechCrunch at the time.

Developing….

Powered by WPeMatico

ForgeRock filed its form S-1 with the Securities and Exchange Commission (SEC) this morning as the identity management provider takes the next step toward its IPO.

The company did not provide initial pricing for its shares, which will trade on the New York Stock Exchange under the symbol FORG. The IPO is being led by Morgan Stanley and J.P. Morgan Chase & Co., with the company being valued as high as $4 billion, according to Bloomberg, which is a significant uplift over the $730 million post-money value that PitchBook had for the company after its last round in 2020.

With the ever-increasing volume of cybersecurity attacks against organizations of all sizes, the need to secure and manage user identities is of growing importance. Based in San Francisco, ForgeRock has raised $233 million in funding across multiple rounds. The company’s last round was a $93.5 million Series E announced in April 2020, which was led by Riverwood Capital alongside Accenture Ventures. At that time, CEO Fran Rosch told TechCrunch that the round would be the last before an IPO, which was also what former CEO Mike Ellis told us after the startup’s $88 million Series D in September 2017.

While the timing of its IPO might have been unclear over the last few years, the company has been on a positive trajectory for growth. In its S-1, ForgeRock reported that as of June 30, its annual recurring revenue (ARR) was $155 million, representing 30% year-over-year growth.

While revenue is growing, losses are narrowing as the company reported a $20 million net loss down from $36 million a year ago. There certainly is a whole lot of room to grow, as the company estimates that the total global addressable market for identity services to be worth $71 billion.

Among the many competitors that ForgeRock faces is Okta, which went public in 2017 and has been growing in the years since. In March, Okta acquired cloud identity startup Auth0 for $6.5 billion in a deal that raised a few eyebrows. Another competitor is Ping Identity, which went public in 2019 and is also growing, reporting on August 4 that its ARR hit $279.6 million in its quarter ended June 30, for a 19% year-over-year gain. There have also been a few big exits in the space over the years, including Duo Security, which was acquired by Cisco for $2.35 billion in 2018.

“ForgeRock has a good access management tool and they continue to be a strong player in customer identity and access management (CIAM),” commented Michael Kelley, senior research director at Gartner.

Kelley noted that in 2020, ForgeRock converted most of its core access management services to a SaaS delivery model, which helped the company catch up with the rest of the market that already offered access management as SaaS. Also last year the company expanded into identity governance, introducing a brand new identity, governance and administration (IGA) product.

“I think one of the more interesting products that ForgeRock offers is ForgeRock Trees, which is a no-code/low-code orchestration tool for building complex authentication and authorization journeys for customers, which is particularly helpful in the CIAM market,” Kelly added.

ForgeRock was founded in 2010, but its roots go back even further to an open-source single sign-on project known as OpenSSO that was created by Sun Microsystems in 2005. When Oracle acquired Sun Microsystems in early 2010, a number of its open-source efforts were left to languish, which is what led a number of former Sun employees to start ForgeRock.

Over the last decade, ForgeRock has expanded significantly beyond just providing a single sign-on to providing an identity platform that can handle consumer, enterprise and IoT use-cases. The company’s platform today handles identity and access management as well as identity governance.

The ability to scale is a key selling point that ForgeRock makes in the S-1, noting that its platform can handle over 60,000 user-based access transactions per second per customer.

“As of June 30, 2021, we had four customers with 100 million or more licensed identities, the company stated in the S-1. “Our ability to serve mission-critical needs in complex environments for large customers enables us to grow our base of large customers and expand within each of them. “

Powered by WPeMatico

Less than a year after raising its $6 million seed funding round, Tel Aviv and Sunnyvale-based startup build.security is being acquired by Elastic. Financial terms of the deal are not being publicly disclosed at this time. The deal is expected to close in Elastic’s Q2 FY22, ending October 31, 2021.

In an email to TechCrunch, Ash Kulkarni, chief product officer at Elastic, said that once the acquisition closes, the build.security technical team will continue as a unit in the Elastic Security organization. Kulkarni added that the acquisition will also become the foundation for a growing Elastic presence in Israel, with Amit Kanfer, co-founder and CEO of build.security, set to become the site lead for the region.

Build.security is focused on security policy management for applications. A core element of the company’s technology approach is the Open Policy Agent (OPA) open-source project, which is part of the Cloud Native Computing Foundation (CNCF), which is also home to Kubernetes. OPA was originally started by startup Styra, which itself has raised $40 million in funding to help build out policy management and authorization technology. Part of OPA is the Rego query language, which is used to structure security and authorization configuration policies.

“We see policy as a fundamental cornerstone of security,” Kulkarni said. “OPA and Rego provide an open, standards-based way to define, manage and enforce policies everywhere.”

Kulkarni noted that security policy technology is complementary to Elastic’s efforts in security and observability. He added that Elastic sees potential for using OPA and the technology that build.security has built on top of OPA to power deployment time, and in the future, build-time security for cloud-native environments.

YL Venture partner John Brennan, who helped to lead the seed round of build.security, sees the acquisition as being a good fit for both companies, as they are both creating solutions for developers that are based on open-source technologies.

“This move by a market leader like Elastic validates the need for transformation in the authorization space,” Brennan said. “This partnership will accelerate build.security’s shift-left vision of efficiently embedding access protection from the start, rather than trying to bolt it on after the fact or, worse, ignoring it completely.”

Elastic is known for its Elastic Stack, which provides Elasticsearch search capability, Logstash log monitoring and Kibana data visualization. In recent years the company has expanded into the security space, acquiring Endgame Security in 2019 for $234 million. On August 3, Elastic announced its Limitless XDR capabilities, which brings together endpoint security with security information and event management (SIEM).

With its new acquisition, Kulkarni said the goal is to go even deeper into security moving toward cloud security enforcement. He explained that after the acquisition closes and as the technology is integrated, users will be able to leverage the Elastic Stack to visualize and manage compliance policies and policy decisions at scale. An initial use-case for the build.security technology will be developing a Kubernetes security and compliance product based on OPA.

Powered by WPeMatico

Cisco announced on Friday that it’s acquiring Israeli applications-monitoring startup Epsagon at a price pegged at $500 million. The purchase gives Cisco a more modern microservices-focused component for its growing applications-monitoring portfolio.

The Israeli business publication Globes reported it had gotten confirmation from Cisco that the deal was for $500 million, but Cisco would not confirm that price with TechCrunch.

The acquisition comes on top of a couple of other high-profile app-monitoring deals, including AppDynamics, which the company bought in 2018 for $3.7 billion, and ThousandEyes, which it nabbed last year for $1 billion.

With Epsagon, the company is getting a way to monitor more modern applications built with containers and Kubernetes. Epsagon’s value proposition is a solution built from the ground up to monitor these kinds of workloads, giving users tracing and metrics, something that’s not always easy to do given the ephemeral nature of containers.

As Cisco’s Liz Centoni wrote in a blog post announcing the deal, Epsagon adds to the company’s concept of a full-stack offering in their applications-monitoring portfolio. Instead of having a bunch of different applications monitoring tools for different tasks, the company envisions one that works together.

“Cisco’s approach to full-stack observability gives our customers the ability to move beyond just monitoring to a paradigm that delivers shared context across teams and enables our customers to deliver exceptional digital experiences, optimize for cost, security and performance and maximize digital business revenue,” Centoni wrote.

That experience point is particularly important because when an application isn’t working, it isn’t happening in a vacuum. It has a cascading impact across the company, possibly affecting the core business itself and certainly causing customer distress, which could put pressure on customer service to field complaints, and the site reliability team to fix it. In the worst case, it could result in customer loss and an injured reputation.

If the application-monitoring system can act as an early warning system, it could help prevent the site or application from going down in the first place, and when it does go down, help track the root cause to get it up and running more quickly.

The challenge here for Cisco is incorporating Epsagon into the existing components of the application-monitoring portfolio and delivering that unified monitoring experience without making it feel like a Frankenstein’s monster of a solution globbed together from the various pieces.

Epsagon launched in 2018 and has raised $30 million. According to a report in the Israeli publication, Calcalist, the company was on the verge of a big Series B round with a valuation in the range of $200 million when it accepted this offer. It certainly seems to have given its early investors a good return. The deal is expected to close later this year.

Powered by WPeMatico