Europe

Auto Added by WPeMatico

Auto Added by WPeMatico

Meet Tinybird, a new startup that helps developers build data products at scale without having to worry about infrastructure, query time and all those annoying issues that come up once you deal with huge data sets. The company ingests data at scale, lets you transform it using SQL and then exposes that data through API endpoints.

Over the past few years, analytics and business intelligence products have really changed the way we interact with data. Now, many big companies store data in a data warehouse or a data lake. They try to get insights from those data sets.

And yet, extracting and manipulating data can be costly and slow. It works great if you want to make a PowerPoint presentation for your quarterly results. But it doesn’t let you build modern web products and data products in general.

“What we do at Tinybird is we help developers build data products at any scale. And we’re really focused on the realtime aspect,” co-founder and CEO Jorge Gómez Sancha told me.

The team of co-founders originally met at Carto. They were already working on complex data issues. “Every year people would come with an order of magnitude more data,” Gómez Sancha said. That’s how they came up with the idea behind Tinybird.

Image Credits: Tinybird

The product can be divided into three parts. First, you connect your Tinybird account with your data sources. The company will then ingest data constantly from those data sources.

Second, you can transform that data through SQL queries. In addition to the command-line interface, you can also enter your SQL queries in a web interface, divide then into multiple steps and document everything. Every time you write a query, you can see your data filtered and sorted according to your query.

Third, you can create API endpoints based on those queries. After that, it works like a standard JSON-based API. You can use it to fetch data in your own application.

What makes Tinybird special is that it’s so fast that it feels like you’re querying your data in realtime. “Several of our customers are reading over 1.5 trillion rows on average per day via Tinybird and ingesting around 5 billion rows per day, others are making an average of 250 requests per second to our APIs querying several billion row datasets,” Gómez Sancha wrote in an email.

Behind the scene, the startup uses ClickHouse. But you don’t have to worry about that as Tinybird manages all the infrastructure for you.

Right now, Tinybird has identified three promising use cases. Customers can use it to provide in-product analytics. For instance, if you operate a web hosting service and wants to give some analytics to your customers or if you manage online stores and want to surface purchasing data to your customers, Tinybird works well for that.

Some customers also use the product for operational intelligence, such as realtime dashboards that you can share internally within a company. Your teams can react more quickly and always know if everything is running fine.

You can also use Tinybird as the basis for some automation or complex event processing. For instance, you can leverage Tinybird to build a web application firewall that scans your traffic and reacts in realtime.

Tinybird has raised a $3 million seed round led by Crane.vc with several business angels also participating, such as Nat Friedman (GitHub CEO), Nicholas Dessaigne (Algolia co-founder), Guillermo Rauch (Vercel CEO), Jason Warner (GitHub CTO), Adam Gross (former Heroku CEO), Stijn Christiaens (co-founder and CTO of Collibra), Matias Woloski (co-founder and CTO of Auth0) and Carsten Thoma (Hybris co-founder).

Powered by WPeMatico

Last week was a good one for edtech in Europe.

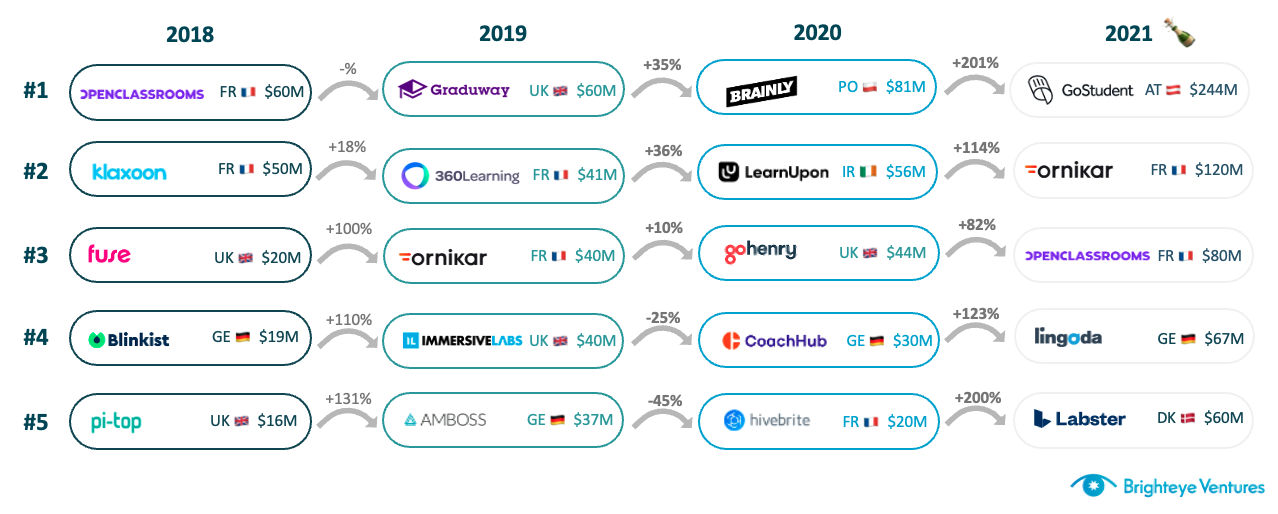

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

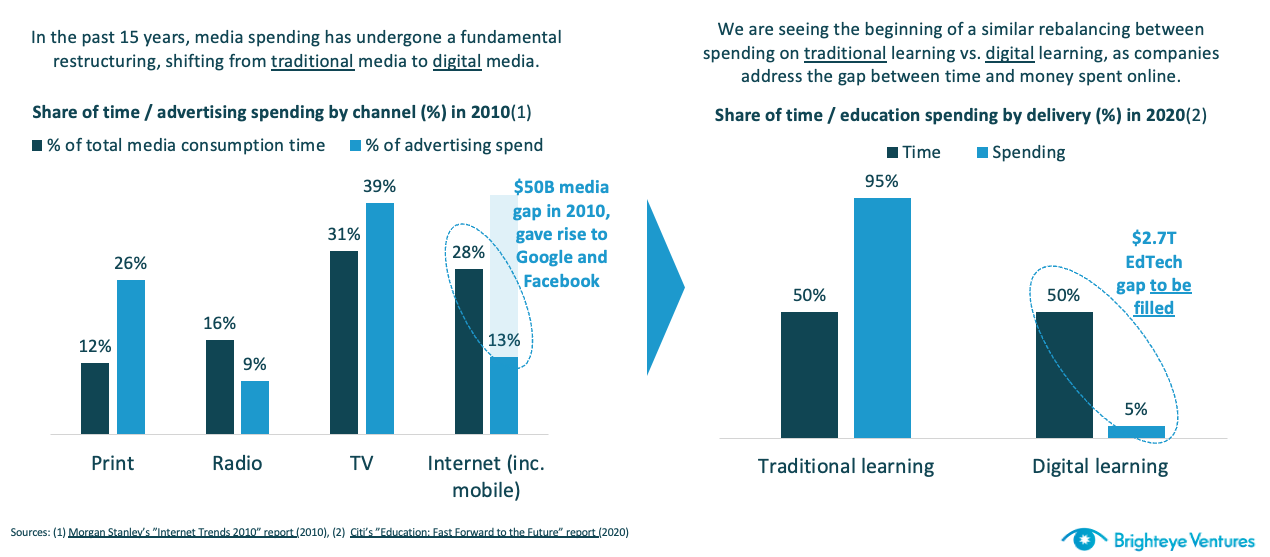

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Istanbul in Turkey continues to prove itself as very fertile ground for casual gaming startups, which appear to be growing from small seedlings into sizable trees. In the latest development, Dream Games — a developer of mobile puzzle games — has raised $155 million in funding, a Series B that values the startup at $1 billion.

This is a massive leap for the company, which raised $50 million (the largest Series A in Turkey’s startup history) only 3.5 months ago. This latest round is being co-led by Index Ventures and Makers Fund, with Balderton Capital, IVP and Kora also participating. It also comes in the wake of a bigger set of deals in the world of gaming and developers in Turkey, the most prominent of which saw Zynga acquire Peak Games for $1.8 billion, amid other acquisitions. Dream is one of several startups in the region founded by alums from Peak.

The focus of the funding, and currently of Dream Games itself, is Royal Match, a puzzle game (iOS, Android) that launched globally in March.

The game has been a huge hit for Dream, with 6 million monthly active users and $20 million/month in revenues from in-game purchases (not ads), according to figures from AppAnnie. (A source close to the company confirmed the figures are accurate, but Dream did not disclose its revenue numbers or revenues directly.) This has catapulted it into the top-20 grossing games categories in the U.S., U.K., and Germany, the same echelon as much older and bigger titles like Candy Crush and Homescapes.

“The funding will be used for heavy user acquisition in every channel and every geography,” Soner Aydemir, co-founder and CEO, Dream Games, told me in an interview. He said Asia would be a focus in that, specifically Japan, South Korea and China. “Our main target is to scale the game so that it becomes one of the biggest games in the global market.”

The world of mobile gaming has in many respects been a very cyclical and fickle one: today’s hot title becomes tomorrow’s has-been, while for developers, they can go through dozens of development processes and launches (and related costs) before they find a hit, if they find a hit. The role of app-install ads and other marketing tools to juice numbers has also been a problematic lever for growth: take away the costs of running those and often the house of cards falls apart.

Aydemir agrees, and while the company will be investing in those aforementioned in-game ads to encourage more downloads of Royal Match, he also said that this strategy can work, but only if the fundamentals of the game are solid, as is the case here.

“If you don’t have good enough metrics, even with all the money in the world it’s impossible to scale,” he said. “But our LTV [lifetime value] is high, and so we think it can be scaled in a sustainable way because of the quality of the game. It always depends on the product.”

In addition to its huge growth, Dream has taken a very focused approach with Royal Match, working on it for years before finally releasing it.

“We spent so much time on tiny details, so many tests over several years to create the dynamics of the game,” he said. “But we also have a feel for it,” he added, referring to the team’s previous lives at Peak Games. “Our users really appreciate this approach.”

For now, too, the focus will just one the one game, he said. Why not two, I asked?

“We believe in Pixar’s approach,” Aydemir said. “When Pixar started, it was very low frequency, a movie every 2-3 years but eventually the rate increased. And it will be similar for us. This year we need to focus on Royal Match but if we can find a way to create other games, we will.”

He added that the challenge — one that many startups know all too well — is that building a new product, in this case a new game, can take the focus away when you are a small team and also working on sustaining and maintaining a current game. “That is the most difficult and challenging part. If we can manage it we will be successful; otherwise we will fail because our business model is basically creating new IP.” He added that it’s likely that another game will be released out into the world at the beginning of next year.

The focus, in any case, was one of the selling points for its investors. “The Dream Games team’s deep genre insight, laser-focus on detail and team chemistry has helped create the early success of Royal Match,” said Michael Cheung, General Partner at Makers Fund, in a statement. “We’re excited to be on the journey with them as they grow Royal Match globally.”

In terms of monetization, Dream Games is pretty firmly in the camp of “no ads, just in-app purchases,” he said. “It’s really bad for user experience and we only care about user experience, so if you put ads in, it conflicts with that.”

Some of the struggles of building new while improving old product will of course get solved with this cash, and the subsequent hiring that Dream Games can do (and it’s doing a lot of that, judging by the careers section of its website). As more startups emerge out of the country — not just in gaming but also areas like e-commerce, where startups like Getir are for example making big waves in instant grocery delivery — it will be interesting to see how that bigger talent pool evolves.

“Since its launch in early March, Royal Match has become one of the top casual puzzle titles globally, driven by once in a decade retention metrics. It speaks to the sheer quality of the title that the Dream Games team has built and the flawless polish and execution across the board,” commented Stephane Kurgan, venture partner at Index Ventures and former COO of King. Index is also the backer of Roblox, Discord, King and Supercell, in a statement.

Powered by WPeMatico

Capping off our dig into the early-stage venture capital market, we’re taking a quick look at Europe this morning. Previously, The Exchange tucked into the United States’ early-stage market for startup capital, uncovering startups using abundant seed capital to get more done before raising a Series A, while others were using pedigree, team and market size to accelerate their first lettered raise.

For both cohorts, it appeared that a rapid-fire Series B could be in the offing, with VCs looking to get capital into winners early.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Latin American venture capital market for early-stage startups had a number of similar hallmarks. That shouldn’t have been surprising. According to Seth Pierrepont, a partner at London-based Accel, “fundraising dynamics are now no longer U.S.- or European-specific — they’re global.” Fundraising over videoconferencing services like Zoom has done more than make geographical distances less impactful inside of countries — it’s even made national borders and even oceans less meaningful.

Is the European startup market similar to what we’ve seen in Latin America and the United States — a cognate for the North American venture capital scene, given its outsized global weight by round count and amount invested?

Largely, yes, a trend that appears to be shaking up prices and the talent wars. This morning, we’re taking a final look at the early-stage venture capital market, this time through a European lens, with an assist from a few investors from the continent.

Broadly, early-stage venture capital rounds in Europe are happening “earlier and are larger in size,” according to Draper Esprit’s Vinoth Jayakumar, an investor based in London. The correlate of larger rounds being raised while startups are younger is valuation expansion, according to Jayakumar, who said that prices are going up “because larger rounds are very dilutive to founders if done at normal — or in this case too low — valuations.”

Powered by WPeMatico

Accel announced Tuesday the close of three new funds totaling $3.05 billion, money that it will be using to back early-stage startups, as well as growth rounds for more mature companies. Notably, the 38-year-old Silicon Valley-based venture firm is doubling down on global investing.

The announcement underscores both the robust confidence investors continue to have for backing startups in the tech sector and the amount of money available to startups these days.

Specifically, today Accel is announcing its 15th early-stage U.S. fund at $650 million; its seventh early-stage European and Israeli fund also at $650 million and its sixth global growth stage fund at $1.75 billion. The latter fund is in addition, and designed to complement, a previously unannounced $2.3 billion global “Leaders” fund that is focused on later-stage investing that Accel closed in December.

Accel expects to invest in about 20 to 30 companies per fund on average, according to Partner Rich Wong. Its average investment in its growth fund will be in the $50 million to $75 million range, and $75 million and $100 million out of its global Leaders fund.

But the firm is also still eager and “excited” to incubate companies, Wong said.

“We’ll still write $500,000 to $1 million seed checks,” he told TechCrunch. “It’s important to us to work with companies from the very beginning and support them through their entire journey.”

Indeed, as TechCrunch recently reported, Accel has a history of backing companies that were previously bootstrapped (and often profitable) -– the latest example being Lower, a Columbus, Ohio-based fintech, which just raised a $100 million Series A.

Interestingly, Accel is often referred to some of these companies by existing portfolio companies (also in the case of Lower, whose CEO was referred to Accel by Galileo Clay Wilkes). More often than not, companies that Accel backs out of its early-stage and growth funds are bootstrapped and located outside of Silicon Valley.

The venture firm has long looked outside of Silicon Valley for opportunities, and has had offices not only in the Bay Area, but in London and Bangalore for years. Part of its investment thesis is to “invest early and locally,” according to Wong. Examples of this philosophy include investments in companies based all over the world — from Mexico to Stockholm to Tel Aviv to Munich.

Since the time of its last fund closure in 2019, the firm has seen 10 portfolio companies go public, including Slack, Austin-based Bumble, Bucharest-based UiPath, CrowdStrike, PagerDuty, Deliveroo and Squarespace, among others.

It also had 40 companies experience an M&A, including Utah-based Qualtrics’s $8 billion acquisition by SAP and Segment’s $3.2 billion acquisition by Twilio. Also, just last week, Rockwell Automation announced it was buying Michigan-based Plex Systems for $2.22 billion in cash. Accel first invested in Plex, which has developed a subscription-based smart manufacturing platform, in 2012.

Recent investments include a number of fintech companies such as LatAm’s Flink, Berlin-based Trade Republic, Unit and Robinhood rival Public. Accel has also backed as existing portfolio companies such as Webflow, a software company that helps businesses build no-code websites and events startup Hopin.

Wong says Accel is “open-minded but thematic” in its investment approach.

Accel Partner Sonali de Rycker, who is based out of London, agrees.

“For example, we’ll look at automation companies, consumer businesses and security companies, but at a global scale. Our goal is to find the best entrepreneurs regardless of where they are,” she said.

That has only been intensified by the recent rise of the smartphone and cloud, Wong said.

“Before, companies were mostly selling to the consumer in their own country,” he added. “But now the size of the market is so dramatically bigger, allowing them to become even larger, which is one of the reasons why I believe we’re seeing investment pace at this speed.”

To support this, it’s notable that Accel’s global Leaders fund is “dramatically” larger than the $500 million Leaders fund the firm closed in 2019.

Also, de Rycker points out, companies are staying private longer so the opportunity to invest in them until they sell or go public is greater.

Accel is also patient. In some cases, the firm’s investors will develop “years-long” relationships with companies they are courting.

“1Password is an example of this approach,” Wong said. “Arun [Mathew] had that relationship for at least six years before that investment was made. Finally, 1Password called and said ‘We’re ready, and we want you to do it.’ ”

And so Accel led the Canadian company’s first external round of funding in its 14-year history — a $200 million Series A — in 2019.

While the firm is open-minded, there are still some industries it has not yet embraced as much as others. For example, Wong said, “We’re not announcing a $2.2 billion crypto fund, but we have done crypto investments, and see some very interesting trends there. We’ll look at where crypto takes us.”

Powered by WPeMatico

The U.K. is gaining in popularity as a great place to start a tech firm. The country is quickly catching up to China on the tech investment front, with VC investments reaching a record of $15 billion in 2020, according to TechNation. A global health crisis notwithstanding, London remained a favorite for investors. U.K. cities made up a fifth of the top 20 European cities, with names such as Oxford, Dublin, Edinburgh and Cambridge rising to the fore in 2020.

Bristol proved especially popular among tech investors last year — local businesses raked in an impressive $414 million in 2020, making it the third-largest U.K. city for tech investment. The city also has the most fintech startups per head in the U.K. outside London, according to Whitecap’s 2019-2020 Ecosystem Report.

Efforts by the city’s private and public sectors to modernize the city have helped it rank among the top smart cities in the U.K., attracting a bevy of tech entrepreneurs. Its proximity to London has meant that it is a good alternative for founders looking for a more affordable stay while letting them tap the capital’s financial resources. The University of Bristol also has the largest robotics department in Europe.

Use discount code HARBOURSIDE to save 25% off an annual or two-year Extra Crunch membership.

This offer is only available to readers in the U.K. and Europe, and expires on August 31, 2021.

Bristol is also home to an important startup accelerator, SETsquared. A collaborative effort by the five universities of Bath, Bristol, Exeter, Southampton and Surrey, the accelerator has supported over 4,000 entrepreneurs and helped their startups raise a total of £1.8 billion. Other startup support players include the new Science Creates VC fund, set up by entrepreneur Harry Destecroix, and TechSPARK Engine Shed.

Key emerging startups from Bristol include Graphcore, Open Bionics, Ultraleap, Immersive Labs and Five AI.

To get a better idea of the state of the tech ecosystem and the investor outlook for this city, we surveyed founders, leaders and executives involved in nurturing Bristol’s startup ecosystem.

The survey revealed that the city has a robust renewable, zero-carbon and fintech startup landscape. Robotics, VR, bio, quantum, digital and deep tech are also areas showing promise. As for the investing scene, although Bristol has a healthy angel network, the city lacks institutional VC, but with London only a drive or train ride away, this has not proved a significant problem.

We surveyed:

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in renewable and zero-carbon innovation, fintech and robotics. It’s weak in industry 4.0.

Which are the most interesting startups in Bristol?

Graphcore, LettUs Grow, Open Bionics, Ultraleap and YellowDog.

What are the tech investors like in Bristol? What’s their focus?

A lot of focus on fintech, I think.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Bristol is a great middle ground between a large dynamic city (plus it’s not far from London) and access to nice countryside area. With remote working we can expect it will attract new residents in the next few years.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Aimee Skinner, Abigail Frear and Stuart Harrison.

Where do you think the city’s tech scene will be in five years?

Second major city in U.K. innovation.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in media/animation, edtech, social impact, health and science. I’m most excited by edtech and the possibility to reach and positively impact millions of students via online learning. It’s weaker in hardware and fintech.

Which are the most interesting startups in Bristol?

Kaedim, Persona Education and One Big Circle.

What are the tech investors like in Bristol? What’s their focus?

There are several very active tech investment networks coming from several angles, e.g., university-led, groups of private angels and tech incubators. The great thing is they all collaborate and share resources, ideas and expertise in initiatives such as The Engine Shed and Silicon Gorge.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

More people are moving in, as Bristol has a great urban lifestyle with easy access to the countryside and Southwest/Wales holiday spots, and an international airport 20 minutes from the center.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Jerry Barnes at Bristol PE Club; Abby Frear at TechSPARK; Briony Phillips at Rocketmakers; Jack Jordan-Connelly at SETsquared.

Where do you think the city’s tech scene will be in five years?

It’s developing rapidly with lots of support, so it will be bigger, attracting more investment and definitely more on the international scene five years from now.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Our tech ecosystem is strong in the aerospace and defense sector. We are excited by the scope and scale of digital transformation opportunities with AI available in this sector. The main weakness in this sector is the slow pace of transformation, especially now due to the pandemic.

Which are the most interesting startups in Bristol?

Graphcore and YellowDog.

What are the tech investors like in Bristol? What’s their focus?

Compared to the U.K. tech sector average, Bristol has a very low proportion of established companies (4% versus 8%), a higher proportion of seed stage companies (42% versus 37%), and a higher death rate (21% versus 17%). It’s a particularly young ecosystem.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

It is possible that people moving out of London will come into Bristol due to the transport links, strong ecosystem and beautiful nature of the city.

Where do you think the city’s tech scene will be in five years?

I wouldn’t be surprised if Bristol turns out to be San Francisco of Europe!

Which sectors is Bristol’s tech ecosystem strong in? What does it lack?

Bristol is strong in the medtech, veterinary, industrial sectors.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Others have moved in.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

SETsquared.

Where do you think the city’s tech scene will be in five years?

We will see massive growth in five years.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Our sector is weak in entrepreneurial ambition among researchers, and so suffers from low rates of deep tech spinout activity from leading universities. We are most excited by the step change in activity we have seen in the past two years and culture shift towards innovation.

Which are the most interesting startups in Bristol?

Rosa Biotech, Albotherm and CytoSeek.

What are the tech investors like in Bristol? What’s their focus?

Medium strength in shallow tech; currently weak in deep tech.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

People are moving in.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Spin Up Science, Science Creates and Science Angel Syndicate.

Where do you think the city’s tech scene will be in five years?

Very strong in deep tech with an invested local community of entrepreneurs, incubators and investors.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in wireless (5G, 60 GHz, etc.), semiconductors (especially processors, AI/ML and parallel architectures), robotics and other hard tech/deep tech.

Which are the most interesting startups in Bristol?

Graphcore, Ultraleap, Blu Wireless and Five AI.

What are the tech investors like in Bristol? What’s their focus?

It’s limited. There are some angels, but few locally focused funds.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Much the same: People choose to live in Bristol/Bath for quality of life. Much of the work is already external — commuting to London.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Nigel Toon, Simon Knowles, Stan Boland, David May and Nick Sturge.

Where do you think the city’s tech scene will be in five years?

Much stronger, with more processor and hardware activity.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol has a strong robotics, aerospace and renewables scene. I’m most excited to see how the legacy in aerospace in Bristol will translate to future industry-defining companies. The ecosystem is weak on the investor side, though London VCs are less than a two-hour train journey away.

Which are the most interesting startups in Bristol?

Graphcore, Ultraleap and Open Bionics.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

I believe Bristol will become more attractive.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Tom Carter at Ultraleap, and Joel Gibbard at Open Bionics.

Where do you think the city’s tech scene will be in five years?

Getting closer to London and Cambridge.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol has a strong biotech, quantum, digital, science-based/deep tech ecosystem. I’m excited by this eclectic city with exciting people that think differently.

Which are the most interesting startups in Bristol?

Any QTEC, SETsquared, or UnitDX members and alumni.

What are the tech investors like in Bristol? What’s their focus?

Very early/nascent, mostly angels.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Probably move in! Beautiful green spaces around, lots of interesting, independent shops. And (just about) commutable from London.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

The incubators — QTEC, QTIC, SETsquared and UnitDX; Bristol Private Equity Club; Harry Destecroix.

Where do you think the city’s tech scene will be in five years?

Buzzing. More great startups and VCs moving in.

Powered by WPeMatico

Snowflake changed the conversation for many companies when it comes to the potentials of data warehousing. Now one of the startups that’s hoping to disrupt the disruptor is announcing a big round of funding to expand its own business.

Firebolt, which has built a new kind of cloud data warehouse that promises much more efficient, and cheaper, analytics around whatever is stored within it, is announcing a major Series B of $127 million on the heels of huge demand for its services.

The company, which only came out of stealth mode in December, is not disclosing its valuation with this round, which brings the total raised by the Israeli company to $164 million. New backers Dawn Capital and K5 Global are in this round, alongside previous backers Zeev Ventures, TLV Partners, Bessemer Venture Partners and Angular Ventures.

Nor is it disclosing many details about its customers at the moment. CEO and co-founder Eldad Farkash told me in an interview that most of them are U.S.-based, and that the numbers have grown from the dozen or so that were using Firebolt when it was still in stealth mode (it worked quietly for a couple of years building its product and onboarding customers before finally launching six months ago). They are all migrating from existing data warehousing solutions like Snowflake or BigQuery. In other words, its customers are already cloud-native, Big Data companies: it’s not trying to proselytize on the basic concept but work with those who are already in a specific place as a business.

“If you’re not using Snowflake or BigQuery already, we prefer you come back to us later,” he said. Judging by the size and quick succession of the round, that focus is paying off.

The challenge that Firebolt set out to tackle is that while data warehousing has become a key way for enterprises to analyze, update and manage their big data stores — after all, your data is only as good as the tools you have to parse it and keep it secure — typically data warehousing solutions are not efficient, and they can cost a lot of money to maintain.

The challenge was seen firsthand by the three founders of Firebolt, Farkash (CEO), Saar Bitner (COO) and Ariel Yaroshevich (CTO) when they were at a previous company, the business intelligence powerhouse Sisense, where respectively they were one of its co-founders and two members of its founding team. At Sisense, the company continually came up against an issue: When you are dealing in terabytes of data, cloud data warehouses were straining to deliver good performance to power their analytics and other tools, and the only way to potentially continue to mitigate that was by piling on more cloud capacity. And that started to become very expensive.

Firebolt set out to fix that by taking a different approach, rearchitecting the concept. As Farkash sees it, while data warehousing has indeed been a big breakthrough in Big Data, it has started to feel like a dated solution as data troves have grown.

“Data warehouses are solving yesterday’s problem, which was, ‘How do I migrate to the cloud and deal with scale?’” he told me back in December. Google’s BigQuery, Amazon’s RedShift and Snowflake are fitting answers for that issue, he believes, but “we see Firebolt as the new entrant in that space, with a new take on design on technology. We change the discussion from one of scale to one of speed and efficiency.”

The startup claims that its performance is up to 182 times faster than that of other data warehouses with a SQL-based system that works on academic research that had yet to be applied anywhere, around how to handle data in a lighter way, using new techniques in compression and how data is parsed. Data lakes in turn can be connected with a wider data ecosystem, and what it translates to is a much smaller requirement for cloud capacity. And lower costs.

Fast forward to today, and the company says the concept is gaining a lot of traction with engineers and developers in industries like business intelligence, customer-facing services that need to parse a lot of information to serve information to users in real time and back-end data applications. That is proving out what investors suspected would be a shift before the startup even launched, stealthily or otherwise.

“I’ve been an investor at Firebolt since their Series A round and before they had any paying customers,” said Oren Zeev of Zeev Ventures. “What had me invest in Firebolt is mostly the team. A group of highly experienced executives mostly from the big data space who understand the market very well, and the pain organizations are experiencing. In addition, after speaking to a few of my portfolio companies and Firebolt’s initial design partners, it was clear that Firebolt is solving a major pain, so all in all, it was a fairly easy decision. The market in which Firebolt operates is huge if you consider the valuations of Snowflake and Databricks. Even more importantly, it is growing rapidly as the migration from on-premise data warehouse platforms to the cloud is gaining momentum, and as more and more companies rely on data for their operations and are building data applications.”

Powered by WPeMatico

Aircall has raised a $120 million Series D round led by Goldman Sachs Asset Management. Following today’s funding round, the company has reached unicorn status, which means it has a valuation above $1 billion — this is the 16th French unicorn.

The startup has been building a cloud-based phone system for call centers, support lines and sales teams. It integrates with Salesforce, HubSpot, Zendesk, Slack, Intercom and other popular CRM, support and communication systems.

Aircall customers can create local numbers and set up an interactive voice response directory. The service manages the call queue for you and your agents can start answering inbound calls. Agents can transfer calls and put customers on hold. Admins can see analytics, monitor calls and see how everyone is doing.

In addition to Goldman Sachs Asset Management, existing investors DTCP, eFounders, Draper Esprit, Adam Street Partners, NextWorldCap and Gaia are also participating once again in today’s funding round.

As a cloud-based software product, Aircall works well with remote or hybrid teams. For the past year, many companies have been looking for a new phone system with various lockdowns taking place around the world. And Aircall has capitalized on this influx of customers.

When it comes to metrics, it means that signups increased by 65% in 2020. New customers include Caudalie, OpenClassrooms and Too Good To Go. Overall, Aircall has 8,500 customers. 15% of them are based in France, 35% in the U.S. and 50% in other countries.

With the new funding round, the company plans to iterate on its product with new integrations with third-party tools, and in particular industry-specific integrations. There will be new offices in London and Berlin as well as new hires in the company’s existing offices based in New York, Paris, Sydney and Madrid.

The company also plans to control a bigger chunk of its tech stack. It means that it’ll collaborate with big telecommunications companies to leverage their networks. You can also expect more product features with better transcription and better sentiment analysis.

Powered by WPeMatico

Time is your most valuable asset — as the saying goes — and today a startup called Memory.ai, which is building AI-based productivity tools to help you with your own time management, is announcing some funding to double down on its ambitions: It wants not only to help manage your time, but to, essentially, provide ways to use it better in the future.

The startup, based out of Oslo, Norway, initially made its name with an app called Timely, a tool for people to track time spent doing different tasks. Aimed not just at people who are quantified self geeks, but those who need to track time for practical reasons, such as consultants or others who work on the concept of billable hours. Timely has racked up 500,000 users since 2014, including more than 5,000 paying businesses in 160 countries.

Now, Memory.ai has raised $14 million as it gears up to launch its next apps, Dewo (pronounced “De-Voh”), an app that is meant to help people do more “deep work” by learning about what they are working on and filtering out distractions to focus better; and Glue, described as a knowledge hub to help in the creative process. Both are due to be released later in the year.

The funding is being led by local investors Melesio and Sanden, with participation from Investinor, Concentric and SNÖ Ventures, who backed Memory.ai previously.

“Productivity apps” has always been something of a nebulous category in the world of connected work. They can variously cover any kind of collaboration management software ranging from Asana and Jira through to Slack and Notion; or software that makes doing an existing work task more efficient than you did it before (e.g. Microsoft has described all of what goes into Microsoft 365 — Excel, Word, PowerPoint, etc. — as “productivity apps”); or, yes, apps like those from Memory.ai that aim to improve your concentration or time management.

These days, however, it feels like the worlds of AI and advances in mobile computing are increasingly coming together to evolve that concept once again.

If the first wave of smartphone communications and the apps that are run on smartphone devices — social, gaming, productivity, media, information, etc. — have led to us getting pinged by a huge amount of data from lots of different places, all of the time, then could it be that the second wave is quite possibly going to usher in a newer wave of tools to handle all that better, built on the premise that not everything is of equal importance? No-mo FOMO? We’ll see.

In any case, some bigger platform players also helping to push the agenda of what productivity means in this day and age.

For example, in Apple’s recent preview of iOS 15 (due to come out later this year) the company gave a supercharge to its existing “do not disturb” feature on its phones, where it showed off a new Focus mode, letting users customize how and when they want to receive notifications from which apps, and even which apps they want to have displayed, all organized by different times of day (e.g. work time), place, calendar items and so on.

“Today, iPhone plays so many roles in our lives. It’s where we get information, how people reach us, and where we get things done. This is great, but it means our attention is being pulled in so many different directions and finding that balance between work and life can be tricky,” said Apple’s Craig Federighi in the WWDC keynote earlier this month. “We want to free up space to focus and help you be in the moment.” How well that gets used, and how much other platforms like Google follow suit, will be interesting to see play out. It feels, in any case, like it could be the start of something.

And, serendipitously — or maybe because this is some kind of zeitgeist — this is also playing into what Memory.ai has built and is building.

Mathias Mikkelsen, the Oslo-based founder of Memory.ai, first came up with his idea for Timely (which had also been the original name of the whole startup) when he was working as a designer in the ad industry, one of those jobs that needed to track what he was working on, and for how long, in order to get paid.

He said he knew the whole system as it existed was inefficient: “I just thought it was insane how cumbersome and old it was. But at the same time how important it was for the task,” he said.

The guy had an entrepreneurial itch that he was keen to scratch, and this idea would become the salve to help him. Mikkelsen was so taken with building a startup around time management, that he sold his apartment in Oslo and moved himself to San Francisco to be where he believed was the epicenter of startup innovation. He tells me he lived off the proceeds of his flat for two years “in a closet” in a hacker house, bootstrapping Timely, until eventually getting into an accelerator (500 Startups) and subsequently starting to raise money. He eventually moved back to Oslo after two years to continue growing the business, as well as to live somewhere a little more spacious.

The startup’s big technical breakthrough with Timely was to figure out an efficient way of tracking time for different tasks, not just time worked on anything, without people having to go through a lot of data entry.

The solution: to integrate with a person’s computer, plus a basic to-do schedule for a day or week, and then match up which files are open when to determine how long one works for one client or another. Phone or messaging conversations, for the moment, are not included, and neither are the contents of documents — just the titles of them. Nor is data coming from wearable devices, although you could see how that, too, might prove useful.

The basic premise is to be personalised, so managers and others cannot use Timely to track exactly what people are doing, although they can track and bill for those billable hours. All this is important, as it also will feed into how Dewo and Glue will work.

The startup’s big conceptual breakthrough came around the same time: Getting time tracking or any productivity right “has never been a UI problem,” Mikkelsen said. “It’s a human nature problem.” This is where the AI comes in, to nudge people towards something they identify as important, and nudge them away from work that might not contribute to that. Tackling bigger issues beyond time are essential to improving productivity overall, which is why Memory.ai now wants to extend to apps for carving out time for deep thinking and creative thinking.

While it might seem to be a threat that a company like Apple has identified the same time management predicament that Memory.ai has, and is looking to solve that itself, Mikkelsen is not fazed. He said he thinks of Focus as not unlike Apple’s work on Health: there will be ways of feeding information into Apple’s tool to make it work better for the user, and so that will be Memory.ai’s opportunity to hopefully grow, not cannibalize, its own audience with Timely and its two new apps. It is, in a sense, a timely disruption.

“Memory’s proven software is already redefining how businesses around the world track, plan and manage their time. We look forward to working with the team to help new markets profit from the efficiencies, insights and transparency of a Memory-enabled workforce,” said Arild Engh, a partner at Melesio, in a statement.

Kjartan Rist, a partner at Concentric, added: “We continue to be impressed with Memory’s vision to build and launch best-in-class products for the global marketplace. The company is well on its way to becoming a world leader in workplace productivity and collaboration, particularly in light of the remote and hybrid working revolution of the last 12 months. We look forward to supporting Mathias and the team in this exciting new chapter.”

Powered by WPeMatico

As enterprise startups continue to target interesting gaps in the market, we’re seeing increasingly sophisticated tools getting built for small and medium businesses — traditionally a tricky segment to sell to, too small for large enterprise tools, and too advanced in their needs for consumer products. In the latest development of that trend, an Israeli startup called DataRails has raised $25 million to continue building out a platform that lets SMBs use Excel to run financial planning and analytics like their larger counterparts.

The funding closes out the company’s Series A at $43.5 million, after the company initially raised $18.5 million in April (some at the time reported this as its Series A, but it seems the round had yet to be completed). The full round includes Zeev Ventures, Vertex Ventures Israel and Innovation Endeavors, with Vintage Investment Partners added in this most recent tranche. DataRails is not disclosing its valuation, except to note that it has doubled in the last four months, with hundreds of customers and on target to cross 1,000 this year, with a focus on the North American market. It has raised $55 million in total.

The challenge that DataRails has identified is that on one hand, SMBs have started to adopt a lot more apps, including software delivered as a service, to help them manage their businesses — a trend that has been accelerated in the last year with the pandemic and the knock-on effect that has had for remote working and bringing more virtual elements to replace face-to-face interactions. Those apps can include Salesforce, NetSuite, Sage, SAP, QuickBooks, Zuora, Xero, ADP and more.

But on the other hand, those in the business who manage finances and financial reporting are lacking the tools to look at the data from these different apps in a holistic way. While Excel is a default application for many of them, they are simply reading lots of individual spreadsheets rather than integrated data analytics based on the numbers.

DataRails has built a platform that can read the reported information, which typically already lives in Excel spreadsheets, and automatically translate it into a bigger picture view of the company.

For SMEs, Excel is such a central piece of software, yet such a pain point for its lack of extensibility and function, that this predicament was actually the germination of starting DataRails in the first place,

Didi Gurfinkel, the CEO who co-founded the company with Eyal Cohen (the CPO) said that DataRails initially set out to create a more general-purpose product that could help analyze and visualize anything from Excel.

Image: DataRails

“We started the company with a vision to save the world from Excel spreadsheets,” he said, by taking them and helping to connect the data contained within them to a structured database. “The core of our technology knows how to take unstructured data and map that to a central database.” Before 2020, DataRails (which was founded in 2015) applied this to a variety of areas with a focus on banks, insurance companies, compliance and data integrity.

Over time, it could see a very specific application emerging, specifically for SMEs: providing a platform for FP&A (financial planning and analytics), which didn’t really have a solution to address it at the time. “So we enabled that to beat the market.”

“They’re already investing so much time and money in their software, but they still don’t have analytics and insight,” said Gurfinkel.

That turned out to be fortunate timing, since “digital transformation” and getting more out of one’s data was really starting to get traction in the world of business, specifically in the world of SMEs, and CFOs and other people who oversaw finances were already looking for something like this.

The typical DataRails customer might be as small as a business of 50 people, or as big as 1,000 employees, a size of business that is too small for enterprise solutions, “which can cost tens of thousands of dollars to implement and use,” added Cohen, among other challenges. But as with so many of the apps that are being built today to address those using Excel, the idea with DataRails is low-code or even more specifically no-code, which means “no IT in the loop,” he said.

“That’s why we are so successful,” he said. “We are crossing the barrier and making our solution easy to use.”

The company doesn’t have a huge number of competitors today, either, although companies like Cube (which also recently raised some money) are among them. And others like Stripe, while currently not focusing on FP&A, have most definitely been expanding the tools that it is providing to businesses as part of their bigger play to manage payments and subsequently other processes related to financial activity, so perhaps it, or others like it, might at some point become competitors in this space as well.

In the meantime, Gurfinkel said that other areas that DataRails is likely to expand to cover alongside FP&A include HR, inventory and “planning for anything,” any process that you have running in Excel. Another interesting turn would be how and if DataRails decides to look beyond Excel at other spreadsheets, or bypass spreadsheets altogether.

The scope of the opportunity — in the U.S. alone there are more than 30 million small businesses — is what’s attracting the investment here.

“We’re thrilled to reinvest in DataRails and continue working with the team to help them navigate their recent explosive and rapid growth,” said Yanai Oron, general partner at Vertex Ventures, in a statement. “With innovative yet accessible technology and a tremendous untapped market opportunity, DataRails is primed to scale and become the leading FP&A solution for SMEs everywhere.”

“Businesses are constantly about to start, in the midst of, or have just finished a round of financial reporting — it’s a never-ending cycle,” added Oren Zeev, founding partner at Zeev Ventures. “But with DataRails, FP&A can be simple, streamlined, and effective, and that’s a vision we’ll back again and again.”

Powered by WPeMatico