Europe

Auto Added by WPeMatico

Auto Added by WPeMatico

Many have tried to do away with it, but email refuses to die … although in the process it might be (figuratively speaking) killing some of us with the workload it brings on to triage and use it. A startup called Sedna has built a system to help with that — specifically for enterprise and other business customers — by “reading” the text of emails and chats, and automatically actioning items within them so that you don’t have to. Today, it’s announcing funding of $34 million to expand its work.

The funding, a Series B, is being led by Insight Partners, with Stride.VC, Chalfen Ventures and the SAP.iO fund (part of SAP) also participating. The funding will be used to continue building out more data science around Sedna’s core functionality, with the aim of moving into a wider set of verticals over time. Currently its main business is in the area of supply chain players, with Glencore, Norden and Bunge among its customers. Other customers in areas like finance include the neobank Starling. London-based Sedna is not disclosing valuation.

Bill Dobie, Sedna’s CEO and founder originally from Vancouver but now in London, said the idea for the company was hatched out of his own experience.

“I spent years building software to help users be more productive, but no matter what we built we never really reduced people’s workload,” he said. The reason: The millstone that is called email, with its endless, unsolicited, inbound messages, some of which (just enough not to ignore) might be important. “What really struck me was how long it spent to move items out of and into email,” he said of the “to-do’s” that arose out of there.

Out of that, Sedna was built to “read” emails and give them more context and direction. Its system removes duplicates of action items and essentially increases the strike rate when it comes people’s inboxes: What’s in there is more likely to be what you really need to see. And it does so at a very quick speed.

“Our main value is the sheer scale at which we operate,” Dobie said. “We read millions or even billions of messages in subsecond response times.” Indeed, while many of us are not getting “millions” of emails, there is a world of messaging out there that needs reading beyond that. Think, for example, of the volume of data that will be coming down the pike from IoT-based diagnostics.

“Smart” inboxes have definitely become a thing for consumers — although arguably none work as well as you wish they did. What’s notable about Sedna has been how it’s tuned its particular algorithms to specific verticals, letting them get smarter around the kind of content and work practices in particular organizations.

Right now the work is driven by an API framework, with elements of “low code” formatting to let people shape their own Sedna experiences. The aim will be to make that even easier over time. An API-driven framework right now, some low code we’re heading into, but mostly its SAP or shipping or a trading system that understands the transaction underway, then Sedna uses a decision tree to categorize.

Another area where Sedna might grow is in how it handles the information that it ingests. Currently, the company’s tech can be interconnected by a customer to then hand off certain work to RPA systems, as well as to specific humans. There is an obvious route to developing some of the second stage of software there — or alternatively, it’s a sign of how something like Sedna might get snapped up or copied by one of the big RPA players.

“Bill started reimagining email where it was most broken and therefore hardest to fix — large teams managing huge volumes and complicated processes,” said Rebecca Liu-Doyle, principal at Insight Partners, in a statement. “Today, Sedna’s power is in its ability to introduce immense speed, simplicity and delight to any inbox experience, regardless of scale or complexity. We are excited to partner with the Sedna team as they continue to make digital communication more intelligent for teams in global supply chain and beyond.” Liu-Doyle is joining the board with this round.

SAP is a strategic investor in this round, as Sedna potentially helps its customers be more productive while using SAP systems. “SAP continues to partner with SEDNA to deliver value to SAP customers. The ability to turn complex information into simpler intelligent collaboration has been a growing priority for many SAP customers,” said Stefan Sauer, global transport solutions lead at SAP, in a statement.

Powered by WPeMatico

Online abuse, disinformation, fraud and other malicious content is growing and getting more complex to track. Today, a startup called ActiveFence is coming out of the shadows to announce significant funding on the back of a surge of large organizations using its services. ActiveFence has quietly built a tech platform to suss out threats as they are being formed and planned to make it easier for trust and safety teams to combat them on platforms.

The startup, co-headquartered in New York and Tel Aviv, has raised $100 million, funding that it will use to continue developing its tools and to continue expanding its customer base. To date, ActiveFence says that its customers include companies in social media, audio and video streaming, file sharing, gaming, marketplaces and other technologies — it has yet to disclose any specific names but says that its tools collectively cover “billions” of users. Governments and brands are two other categories that it is targeting as it continues to expand. It has been around since 2018 and is growing at around 100% annually.

The $100 million being announced today actually covers two rounds: Its most recent Series B led by CRV and Highland Europe, as well as a Series A it never announced led by Grove Ventures and Norwest Venture Partners. Vintage Investment Partners, Resolute Ventures and other unnamed backers also participated. It’s not disclosing valuation but I understand it’s over $500 million.

“We are very honored to be ActiveFence partners from the very earliest days of the company, and to be part of this important journey to make the internet a safer place and see their unprecedented success with the world’s leading internet platforms,” said Lotan Levkowitz, general partner at Grove Ventures, in a statement.

The increased presence of social media and online chatter on other platforms has put a strong spotlight on how those forums are used by bad actors to spread malicious content. ActiveFence’s particular approach is a set of algorithms that tap into innovations in AI (natural language processing) and to map relationships between conversations. It crawls all of the obvious, and less obvious and harder-to-reach parts of the internet to pick up on chatter that is typically where a lot of the malicious content and campaigns are born — some 3 million sources in all — before they become higher-profile issues. It’s built both on the concept of big data analytics as well as understanding that the long tail of content online has a value if it can be tapped effectively.

“We take a fundamentally different approach to trust, safety and content moderation,” Noam Schwartz, the co-founder and CEO, said in an interview. “We are proactively searching the darkest corners of the web and looking for bad actors in order to understand the sources of malicious content. Our customers then know what’s coming. They don’t need to wait for the damage, or for internal research teams to identify the next scam or disinformation campaign. We work with some of the most important companies in the world, but even tiny, super niche platforms have risks.”

The insights that ActiveFence gathers are then packaged up in an API that its customers can then feed into whatever other systems they use to track or mitigate traffic on their own platforms.

ActiveFence is not the only company building technology to help platform operators, governments and brands have a better picture of what is going on in the wider online world. Factmata has built algorithms to better understand and track sentiments online; Primer (which also recently raised a big round) also uses NLP to help its customers track online information, with its customers including government organizations that used its technology to track misinformation during election campaigns; Bolster (formerly called RedMarlin) is another.

Some of the bigger platforms have also gotten more proactive in bringing tracking technology and talent in-house: Facebook acquired Bloomsbury AI several years ago for this purpose; Twitter has acquired Fabula (and is working on a bigger efforts like Birdwatch to build better tools), and earlier this year Discord picked up Sentropy, another online abuse tracker. In some cases, companies that more regularly compete against each other for eyeballs and dollars are even teaming up to collaborate on efforts.

Indeed, it may well be that ultimately there will exist multiple efforts and multiple companies doing good work in this area, not unlike other corners of the world of security, which might need more than one hammer thrown at problems to crack them. In this particular case, the growth of the startup to date, and its effectiveness in identifying early warning signs, is one reason investors have been interested in ActiveFence.

“We are pleased to support ActiveFence in this important mission,” commented Izhar Armony, a general partner at CRV, in a statement. “We believe they are ready for the next phase of growth and that they can maintain leadership in the dynamic and fast-growing trust and safety market.”

“ActiveFence has emerged as a clear leader in the developing online trust and safety category. This round will help the company to accelerate the growth momentum we witnessed in the past few years,” said Dror Nahumi, general partner at Norwest Venture Partners, in a statement.

Powered by WPeMatico

Meet Sproutl, a marketplace for gardeners living in the U.K. The startup founded by former Farfetch executives has raised a $9 million seed round. It wants to make gardening more accessible by providing a curated list of items, relevant advice as well as inspiration.

Index Ventures is leading the round in the startup with Ada Ventures and several business angels also participating. The funding round originally closed in April of this year.

“A few years ago, we bought a flat in London with a tiny little garden. We were both working full time in quite intense jobs with young kids. I went online assuming that I would be able to sort out this garden space. And I didn’t know a lot about gardening. And I just didn’t find anything that spoke to me as a new gardener. It felt like what was available was more for more knowledgeable people,” co-founder and CEO Anni Noel-Johnson told me.

If you’ve ever tried to search for gardening videos on YouTube, you may have ended up on long-winded videos with instructions that don’t make any sense to you. Similarly, there are not a lot of e-commerce websites focused on gardening specifically.

And yet, the market opportunity is quite big. There are millions of gardeners in the U.K. There are also quite a few independent garden centers, nurseries and shops with a turnover of several millions of pounds per year. More importantly, they generate the vast majority of their sales in store. Some of them have never sold anything online.

Sproutl is teaming up with those businesses so that they can find new customers across the U.K. Those third-party sellers list their items on Sproutl while the startup takes care of logistics, packaging sourcing and delivery.

On the marketplace, customers can buy indoor and outdoor plants, pots, gardening essentials and outdoor living products. Partners currently include Rosebourne, Polhill, Millbrook, Middleton, Bellr, Fertile Fibre and Horticus.

Anni Noel-Johnson, the CEO of the company, was the VP of Trading and Strategy at Farfetch. Sproutl CTO Andy Done also worked at Farfetch at some point as director of Data Engineering.

Hollie Newton is also going to be a key team member at Sproutl. She previously wrote a best-selling gardening book called “How to Grow.” She’s now the chief creative officer at Sproutl.

This is key to understanding Sproutl’s growth strategy. The company plans to provide a ton of content on all things related to your garden — the startup has already released a jargon buster. You might end up on Sproutl the next time you’re looking for gardening advice on Google.

And it’s also going to differentiate the platform from all-encompassing e-commerce platforms, such as Amazon. Other e-commerce companies focused on one vertical in particular, such as ManoMano, have been quite successful. With the right focus, Sproutl could quickly build a loyal customer base as well.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We were a smaller team this week, with Natasha and Alex together with Chris to sort through yet another summer frenzy of a week.

This time around we actually recorded live on Twitter Spaces, which was a first for the podcast. If you missed it, it’s probably because we didn’t promote the taping since it was just an experiment. Good news, though, is that it went well, and we’re going to do some more live tapings of the show with the entire crew on the mics. Make sure to follow the show on the Big Tweet to ensure that you can come hang with us next week. We’ll also do some Q&A at the end, if we’re in good moods.

Until then, let’s live in the present. Here’s what we got into in today’s show:

Powered by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

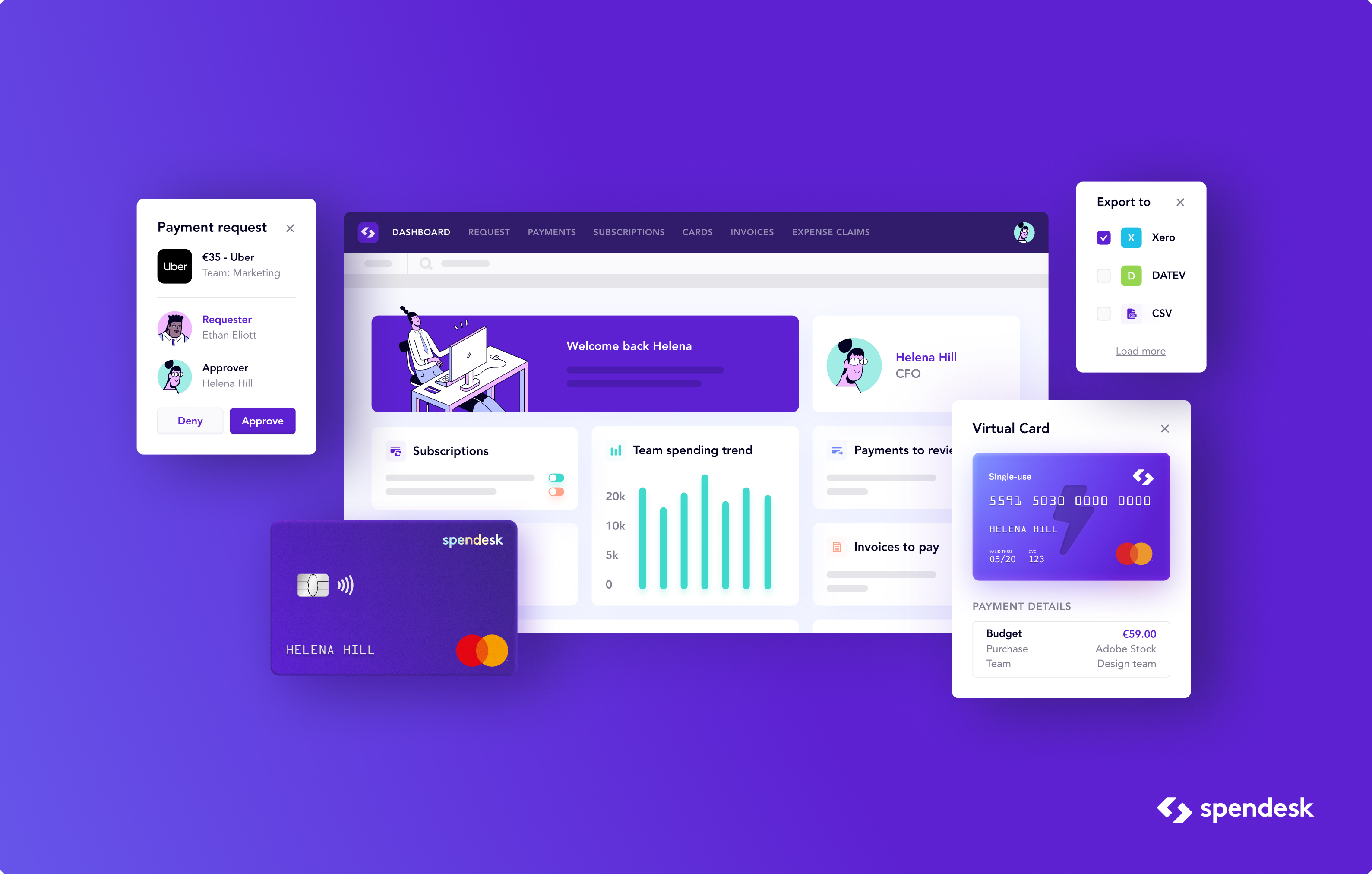

French startup Spendesk has announced earlier today that it has raised a $118 million funding round (€100 million) led by General Atlantic. Overall, the company has raised $189 million (€160 million) since its inception.

Existing investors Index Ventures and Eight Road Ventures participated once again in today’s funding round.

Spendesk, as the name suggests, focuses on all things related to spend management. Originally founded in startup studio eFounders, the startup first offered virtual and physical company cards for employees. While corporate cards are quite popular in the U.S., many small and medium companies in France can’t give a card to every single employee.

That’s why spending your company’s money can be a cumbersome process. You can borrow your boss’ card but they’ll have to trust you with it. You can pay with your own personal card but you want to be reimbursed as quickly as possible.

By combining a SaaS platform with corporate cards, it opens up a ton of possibilities. For instance, you can create an approval workflow for expensive purchases. You can set different budgets for different teams.

Over time, Spendesk has expanded beyond cards to manage expenses and invoice processing. It tries to automate some repetitive accounting tasks as well. Employees are automatically reminded that they have to attach a receipt for each transaction. You can export everything to Xero, Datev, Sage, Cegid or Netsuite.

If that pitch sounds familiar, it’s because there are a handful of European startups that are all doing well in this field. Soldo recently raised $180 million while Pleo snatched $150 million at a $1.7 billion valuation.

And yet, Spendesk doubled its revenue over the past year. Its team grew from 150 to 300 employees and it plans to double its headcount again over the next couple of years.

It means two things — the market opportunity is important and many customers are switching from old school workflows to modern SaaS products. That’s why three startups can grow at the same time.

“Traditionally, finance teams haven’t been equipped with the tools that can support this transformation,” Spendesk co-founder and CEO Rodolphe Ardant said in a statement. “In the past few years we have built the reference spend management solution for finance teams in Europe, which frees businesses and their people from administrative constraints of spending and managing money at work. While our solution is about empowering finance teams, we are actually delivering value to the entire business through the finance team.”

Spendesk currently has 3,000 clients, including Algolia, Soundcloud, Curve, Doctolib, Gousto, Raisin, Sezane and Wefox.

Image Credits: Spendesk

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Life insurance — financial protection you buy against your death — may not read like the liveliest of industries on paper. But a life insurance startup that believes it can turn that stigma around, by infusing the concept with gamification and a push toward wellness and health — and change the life insurance industry in the process — is today announcing significant funding, a sign of the traction it’s getting for its big ideas.

YuLife, a London startup that has built a new kind of life insurance concept — it incentivizes and rewards users to focus on their physical and mental health through a gamified interface — has raised $70 million in what is, to date, one of the largest Series Bs raised by an insurtech startup in Europe.

Led by Target Global, the round also included Eurazeo, Latitude and previous backers Creandum, Notion Capital, Anthemis, MMC Ventures, and OurCrowd. Sammy Rubin, YuLife’s CEO and founder, confirmed that the round values YuLife at $346 million (£250 million).

The company will be using the funding to continue expanding its business, build more products on its platform, and importantly continue to invest in the technology that it uses to run its service and determine how its policies should run.

“Our insurance is about helping people live healthier and longer lives,” Rubin said in an interview. “If we can help to reduce claims while incentivizing people to do that, it’s a win-win.” But it’s about more than that, he added. “We are building a new type of risk model where we are able to create new actuarial tables, which have not been updated in 200 years. Actually, I think smoker rates and how they’ve changed was the last update. So, most will just look at your age and whether you are a smoker and that’s it.”

YuLife is currently active only in the U.K. and is only sold directly to organizations, who in turn provide it to their employees. That business currently — which also includes income protection and critical illness cover — provides $15 billion of coverage and has seen 10x growth in the last year — a bumper one for life insurance policies, possibly for the worst reasons (hello, pandemic; goodbye, predicting what the future might look like). Customers include Capital One, Co-op, Curve, Havas Media, Severn Trent and Sodexo.

That $15 billion is just a drop in the bucket in an industry that is currently estimated to be worth some $2.2 trillion.

The company got its start on the back of a persistent problem that Rubin experienced at his previous insurance startup PruProtect (which is now called Vitality Life).

“Usually insurance benefits just sit on a shelf and never get used,” he said. YuLife set out to change that by making the policy “all about engagement.”

The app — built by veterans of the gaming industry — is designed around the concept of different environments, currently covering forest, ocean, desert and mountains, which YuLife collectively terms its “Yuniverse.” (This incidentally also became a template for the company’s HQ design in London.)

Within each of these environments, users are encouraged to walk, cycle, meditate and do other activities to get around their environments in a healthy way, while at the same time being able to compare their progress against other co-workers. There is a degree of personalization in everyone’s experience, in that one person leaning into one activity over another seems to produce different subsequent scenarios.

Along with this, users are offered discounts on third-party products to further engage with the game within YuLife, which could include a subscription to meditation app Calm, FitBit and Garmin devices, and more.

As users make their way through their worlds, they get rewards, in the form of something called YuCoins. The YuCoins can in turn be used to redeem vouchers from the likes of Amazon and Asos to buy things … consumerism being another way to improve happiness for some of us.

All of this sums up as more than just a policy aimed at giving people peace of mind for their families should they depart this world.

“Long term, it’s not just about health, it’s about lifestyle,” Rubin said.

It’s also about YuLife’s business: The various products that it offers are built around an affiliate model, so there is a business interest for the company around offering and seeing items purchased and redeemed. However, this is not essential to using the app as a policy holder.

The win-win theme runs strong, but so too does the fact that YuLife is taking a different approach altogether, in an industry where most of the “disruption” has up to now been more about how to buy life insurance, rather than reassessing what life insurance actually is. For others in the space doing just that, see DeadHappy, BIMA, and the Jay-Z-backed Ethos. That being said, it’s also not the only one tackling “lifestyle” as part of life insurance: Sproutt is another rethinking that area as well.

“YuLife is redefining life insurance, using the most innovative technologies to transform a largely traditional industry,” said Ben Kaminski, partner, Target Global, in a statement. “With health and well-being increasingly thrust into the limelight in the wake of COVID-19, YuLife is fundamentally changing insurance by incentivizing people to lead healthier lifestyles. YuLife is ideally positioned to build on its tenfold growth during the pandemic and lead the way in helping its clients respond to the challenges posed by an ever-changing working environment. We are very proud to partner with YuLife on its journey of becoming a global leader in life insurance.”

Powered by WPeMatico

Financial services as a service — where entities like neobanks, retailers and others can create and sell their own financial products by way of a few lines of code and APIs — has been one of the bigger trends in the world of fintech in recent years, with embedded finance on its way to being a $7.2 trillion market by 2030, according to a forecast from Bain Capital. Now, one of the companies building and providing those APIs is announcing some growth funding to expand.

Railsbank, which builds APIs for banking, payment cards and credit products for use by fintechs but also a wide range of other kinds of businesses, has raised $70 million in new equity funding, money that the London startup plans to use to continue growing internationally and to add more features to its product set.

“Our mission is to reinvent, unbundle and democratise access to the complex, opaque and byzantine 70-year-old credit card market, which is worth $4 trillion in the U.S. alone,” Nigel Verdon, CEO and co-founder of Railsbank, told TechCrunch in an interview last year. Verdon is a repeat entrepreneur, with one of his previous companies being Currency Cloud.

Railsbank not disclosing its valuation, but Verdon hints that it is in the high hundreds of millions and close to $1 billion.

“As a policy, we rarely talk about valuation as we prefer to talk about customers,” he told TechCrunch today. “Valuation is a very inward-facing and self-centered metric. Saying that, near-unicorn would best describe us today.”

As a point of comparison data from PitchBook noted that the company was valued at just under $200 million in its last round at the end of last year (we reported on it here).

This latest round is being led by Anthos Capital, a previous backer of the company, with Central Capital, Cohen and Company, and Chris Adelsbach’s fund Outrun Ventures, as well as other unnamed previous backers also participating. Central Capital is a strategic investor: It’s the VC arm of the largest privately held bank in Indonesia, while Cohen and Company is the founder of Bancorp. Those backers speak to where Railsbank is targeting its services and who is interested in potentially working with it.

Banking as a service, and other financial products as a service, has become one of the most significant building blocks not just in the world of fintech, but in financial services overall. As with Twilio or Sinch in communications, or Stripe in payments, the idea here is that financial specialists have built out the complicated infrastructure and partnerships that underpin a product like a credit card, or a banking account.

This is then packaged up in a service that can be integrated into another one by way of an API, and the small amount of code needed to add it to another platform. In turn, that API can be used not just by another financial services company that is consumer- or business-facing, but by any kind of company that sees offering a financial product as part of a bigger customer service and loyalty play. That could mean a retailer offering its own-brand credit card, but also a “neobank” that is building a slick front end with great customer service and personalization, without needing to build the now-commoditized banking infrastructure underneath it to run it.

Railsbank is far from being the only company that has identified and built around this concept. Other big players include Rapyd, which raised a big round at a $2.5 billion valuation earlier this year; Unit, which also has been picking up funding and growing; FintechOS, which really does what its name says; and the startup 10x was even built for incumbent players to also have access to lighter fintech as a service.

Railsbank believes its distinct from many of its would-be competitors in part because it has built a lot of its own infrastructure from the ground up (hence the “rails” in its name), “bypassing” legacy players, in contrast to others that are built as software that still ultimately runs on top of stacks (and inefficiencies) of those older providers. This also means that it is regulated as a financial institution.

Railsbank is also in the business of making some acquisitions in order to grow its business, for example acquiring the U.K. business of German fintech Wirecard when it was crashing due to financial malpractices. And it doesn’t build everything from scratch: Earlier this year it also partnered with Plaid to embed some of its services within Railsbank’s.

Railsbank does not disclose a full list of customer names but has case studies on a number of smaller clients that speak to just how widely proliferated financial services are today. They include GoSolo, Kyshi and SimpledCard.

“The market has evolved so rapidly since we founded the world’s first BaaS business, the Bancorp,” noted Betsy Cohen, chairman of Fintech Masala and founder of Bancorp, in a statement. “As we move into the $7 trillion embedded finance market, it has been great watching Railsbank’s growth story. With this investment, it’s a privilege to continue to be part of the journey with a global leader like Railsbank.”

Powered by WPeMatico

AttackIQ, a cybersecurity startup that provides organizations with breach and attack simulation solutions, has raised $44 million in Series C funding as it looks to ramp up its international expansion.

The funding round was led by Atlantic Bridge, Saudi Aramco Energy Ventures (SAEV) and Gaingels, with existing vendors — including Index Ventures, Khosla Ventures, Salesforce Ventures and Telstra Ventures — also participating. The round brings the company’s total funding raised to date to $79 million.

AttackIQ was founded in 2013 and is based out of San Diego, California. It provides an automated validation platform that runs scenarios to detect any gaps in a company’s defenses, enabling organizations to test and measure the effectiveness of their security posture and receive guidance on how to fix what’s broken. Broadly, AttackIQ’s platform helps an organization’s security teams anticipate, prepare and hunt for threats that may impact their business, before hackers get there first.

Its Security Optimization Platform platform, which supports Windows, Linux and macOS across public, private and on-premises cloud environments, is based on the MITRE ATT&CK framework, a curated knowledge base of known adversary threats, tactics and techniques. This is used by a number of cybersecurity companies also building continuous validation services, including FireEye, Palo Alto Networks and Cymulate.

AttackIQ says this latest round of funding, which comes more than two years after its last, arrives at a “dynamic time” for the company. Not only has cybersecurity become more of a priority for organizations as a result of a major uptick in both ransomware and supply-chain attacks, the company also recently accelerated its international expansion efforts through a partnership with technology distributor Westcon.

The startup says it’s planning to use these new funds to further expand internationally through its newfound partnership with Atlantic Bridge, which will also see Kevin Dillon, the company’s co-founder and managing director, join the AttackIQ board of directors.

“AttackIQ has established itself as a category leader with a formidable enterprise customer base that includes four of the Fortune 20,” said Dillon. “We believe deeply in the company’s vision and potential to become the next billion-dollar cybersecurity software company and look forward to helping the company turn early traction in Europe and the Middle East into robust, long-term expansion.”

Brett Galloway, CEO of AttackIQ, said the round “reaffirms the strength” of its platform.

As well as enabling organizations to review the robustness of their security defenses, the startup also runs the AttackIQ Academy, which provides free entry-level and advanced cybersecurity training. It has accumulated 17,200 registered students to date across 176 countries.

Powered by WPeMatico