entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

Zocdoc founder Cyrus Massoumi and Indiegogo founder Slava Rubin have created a new $30 million fund called Humbition aimed at early stage, founder-led companies in New York.

“The fund is focused on connecting startups with investors and advisors experienced in building and growing successful businesses,” said Rubin.

“We are seeking to fill a void in NYC, where the vast majority of early stage investors have no significant experience building and scaling businesses,” he said. “The fund’s main areas of investment include marketplaces, consumer and health tech. But the primary criteria for investments is high quality founders. The fund is also seeking out mission-driven businesses because the companies that are socially responsible will be the most successful in the coming decades.”

The fund has brought on ClassPass founder Payal Kadakia, Warby Parker founder Neil Blumenthal, Charity: Water CEO and founder Scott Harrison, and Casper founder and CEO Philip Krim as advisors. They have already invested some of the $30 million raise in Burrow, a couch-on-demand service.

“New York City is home to a tremendous number of mission-driven startups that are simply not receiving the same level of support as their peers in the Bay Area. This void presents a unique opportunity for humbition to reach the incredible local talent who need the funding and guidance to build and grow their businesses in New York City,” said Rubin.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

Eventbrite is having one hell of a debut on the New York Stock Exchange this morning.

Shares of the ticketing startup, founded back in 2006, have shot up over 50 percent in trading on the NYSE. After pricing its shares at $23 in its initial offering, investors have bid up the stock to a whopping $37, putting the company’s valuation at nearly $3 billion.

$EB prices $23, opens $36 pic.twitter.com/cYgCuqbmh8

—

(@hunterwalk) September 20, 2018

That’s well above where the ticketing company had hoped to be when it initially set terms for the public offering earlier this month.

The company started trading priced above its share price and nearly doubled its valuation. And if Eventbrite can do it, really almost any later-stage startup should be thinking about the public markets right now.

Performance for the San Francisco ticketing company has been… somewhat lackluster. As we noted when wrote about the company’s offering:

Eventbrite is not profitable and has been losing money since 2016. According to the documents, it posted losses of $40.4 million in 2016 and $38.5 million in 2017. In the first six months of 2018, the company has posted a net loss of $15.6 million. The company is making changes to make up for some of those losses — at the end of August, it announced a new pricing scheme for its customers using the “Essentials” package.

Its revenue is rising though, increasing from $133 million in 2016 to $201 million last year.

Since the beginning of the year tech public offerings have been on a tear. As The Wall Street Journal noted in July, 120 companies had raised $35.2 billion on U.S. exchanges at that point — the best showing for public markets since 2014 and the fourth busiest year since 1995, according to the financial data and analysis service Dealogic.

We’ve noted before that it’s a bit mind-boggling that investors and their portfolio companies wouldn’t be taking more advantage of these heady times. Nothing lasts forever (not even cold November rain) and certainly not markets that have been this bullish for this long.

Some of the reasoning is likely thanks to a market that’s still awash in private equity, sovereign wealth and late-stage dollars. SoftBank has hundreds of billions to invest; private equity firms are beginning to look at growth-stage companies the way that I look at banana cream pies from Cassell’s; and venture firms are beefing up big time to keep up with the Joneses (or in this case, the Blackstoneses).

However, the fun is certainly going to come to an end, and likely sooner rather than later. Early-stage investors are beginning to dole out their advice on lowering cash burn (something that happens every time they see the beginning of the end of the beginning of the end).

Low burn rates have gone out of fashion, but I expect we’ll be reminded very quickly at the beginning of the next downturn why they’re so valuable for early-stage startups.

— Sam Altman (@sama) September 19, 2018

With that in mind, later-stage companies should be looking for the exit signs wherever they can find them. Right now, that’s an IPO window that seems to be wide open.

Powered by WPeMatico

Labor Day is a holiday that just doesn’t fit Silicon Valley. Its purported purpose is to celebrate working men and women and their — our — progress toward better working conditions and fairer workplaces. Yet, few regions in recent times have supposedly done more to “destroy” quality working conditions than the Valley, from the entire creation of the precarious 1099 economy to automation of labor itself.

My colleague John Chen offered the received wisdom on this discrepancy this weekend, arguing that Valley entrepreneurs should take the traditional message of Labor Day to heart, encouraging them to create more equitable, fair, and secure workplaces not just for their own employees, but also for all the workers that power the platforms we create and operate every day.

It’s a nice sentiment that I agree with, but I think he misses the mark.

What Silicon Valley needs — now more than ever before — is to double down on the kind of ambitious, hard-charging, change-the-world labor that created our modern knowledge economy in the first place. We can’t and shouldn’t slow down. We need more technological progress, not less. We need more automation of labor, not less. And we need as much of this innovation to happen in the United States as possible.

The tech industry may have become a dominant force by some metrics, but we are only just getting started. Entire industries like freight have little to no automation. Several billion people lack access to the internet, to say nothing of critical, basic infrastructure. Our drug pipeline is anemic, and costs for education, health care, construction, and government are continuing to skyrocket.

In short, we have barely scratched the surface of what we can achieve with software, with hardware, with better business models and better automation. These aren’t table scraps, but trillions dollar opportunities lying in wait for entrepreneurs to seize them.

And yet, we keep hearing persistent claims that overwork is a problem in the Valley. Discussions of work-life balance are practically de rigueur for startups these days, as are free meals and massages and unlimited vacation time. These demands are coming at a time when some of the most fertile opportunities for innovation in areas as diverse as robotics, space, biotech, cancer, and construction remain ripe for the taking.

It’s a hustlers world out there, and the message that those who want to shape that world should be hearing this Labor Day is simple: work harder. Hell, work today.

Certainly that’s the message ingrained in most places competing with the Valley these days. Mike Moritz wrote a column in the Financial Times earlier this year, comparing the hard-charging work ethic of Chinese tech entrepreneurs and workers with their Silicon Valley brethren. He didn’t mince words, and the piece ignited a firestorm of criticism.

But he’s right, and not just about Chinese founders. Entrepreneurs in developing and middle-income countries from India and South Korea to Brazil and Nigeria now have access to the same tools that top Valley startups use, with experience to boot. And they are hungry to transform their lot in life into something much more ambitious, much more grand.

We need to re-inject their level of urgency back into the Valley ethos and compete ferociously. We can’t rest on companies from the 1990s like Google, or the 1970s like Apple and Microsoft as the final wave of innovative companies. We need the next massive tech companies to be built, and they’re not going to be created 20-hour workweeks at a time.

Entrepreneurship is a rough and solitary life. Hustling isn’t fun, losing deals isn’t enjoyable, and working around the clock under intense pressure is not for the faint of heart. For those who want the easy road, there are many, many pathways today in the modern American economy that will guarantee it, whether that is a big tech giant, or some other Fortune 100 company.

Yet, the spirit of America is always choosing the bigger gamble, the bolder vision. And it is the people who stand up and demand that we make huge strides today — not tomorrow — that are going to own the future.

Of course, founding a company has to be a voluntary choice. No one should have to work for a pittance, or feel coerced into a high-pressure lifestyle when they aren’t ready and willing. No one should be locked into an economic system where they can’t improve their own income and status through tenacity and strategy. Our tech companies should absolutely be more diverse, and fairer to all people. Equity can and should be more widely distributed.

But when it comes to the true meaning of Labor Day in the American sense, we should celebrate the hard-working founders and entrepreneurs who are taking on the biggest challenges and focusing all of their talents on solving these critical human problems. That’s what made Silicon Valley what it is, and it’s the meaning of Labor Day that every founder and dreamer should center on.

Powered by WPeMatico

Do you worry about the so-called “kill zones” of big tech companies? The Economist thinks you should. The theory basically suggests that if your product or service is anyway threatening or accretive to one of these incumbents, they will either force-buy your company or clone it and destroy your market.

Any entrepreneur that believes this should probably pack up now before it’s too late — if it’s not a “kill-shot,” it will be some other perceived death-knell that ruins your company.

Starting a company has never been easier. But growing a sustainable business is still difficult — as it should be. If you build something customers will pay for , you’re going to attract competition from copycats and incumbents. Consider it another type of validation, like product-market fit: competitors think we’re right.

Welcome to being an entrepreneur — you are going to be constantly battling – lack of cash, lack of customers, aggressive competition, better-funded competitors, underperforming staff, slow-moving sales cycle, or some other as-yet-unknown. The list of pitfalls is long. But enough willpower and perseverance — “blood, sweat and tears” — will get you to the other side. Eventually. Remember – the product of an overnight success is years of hard work.

If this is sounds too daunting – don’t do it!

If you enter a market large enough, with deep pocketed and dominant incumbents, you have your work cut out for you. Maybe a nice UI and faster workflow attracted customers and some early adopters – but guess what – they are copyable features. Features alone are rarely enough to win a defensible market position.

Try to ignore advice that says you should focus on building the best product as your differentiator — this does not set you up with the highest chance of success. Instead, focus on finding and serving a targeted segment of customers, with a unique set of needs, and tailor your product and service experience specifically for them.

It’s easy for features to be copied – but you can’t be both custom and generic at the same time. Custom is a great approach that new entrants can take to get a toehold in a larger market with larger players that must be generic (i.e. Salesforce is a generic CRM, but there are lots of vertical CRMs that successfully compete — Wise Agent for realtors, Lead Heroes for health insurance).

Presenting a Total Addressable Market (TAM) is the bane of potentially good startups that have been schooled in “anything less than a billion-dollar opportunity isn’t interesting.” Maybe we should reframe it as Potentially Ownable Market (POM). What are the details you can build in the beginning — where your tailored approach gives you instant leadership?

Let’s use project management as an example. Maybe a new entrant starts as an app for restaurants, which helps chefs build new menus. Each task list is a “recipe,” each recipe has “ingredients,” with amounts and timing, kitchen location, suppliers, alternatives and “garnishes and sauces.” The app integrates with the stock system and POS, and helps chefs predict inventory needs and staffing based on recipe times/complexity.

The founder has looked around and this is the only project management app that focuses on chefs, giving him an instant potentially ownable market. The business might be able to thrive in this segment alone and become the dominant player with its own kill zone.

Maybe this is the first step; the company gets profitable early growth and becomes sustainable, which funds development to grow the business into other vertical and complementary areas. Over time the business will grow into a large TAM — a far better approach than starting off in a large market with clear winners already.

Avoid the battle entirely by creating your own category.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

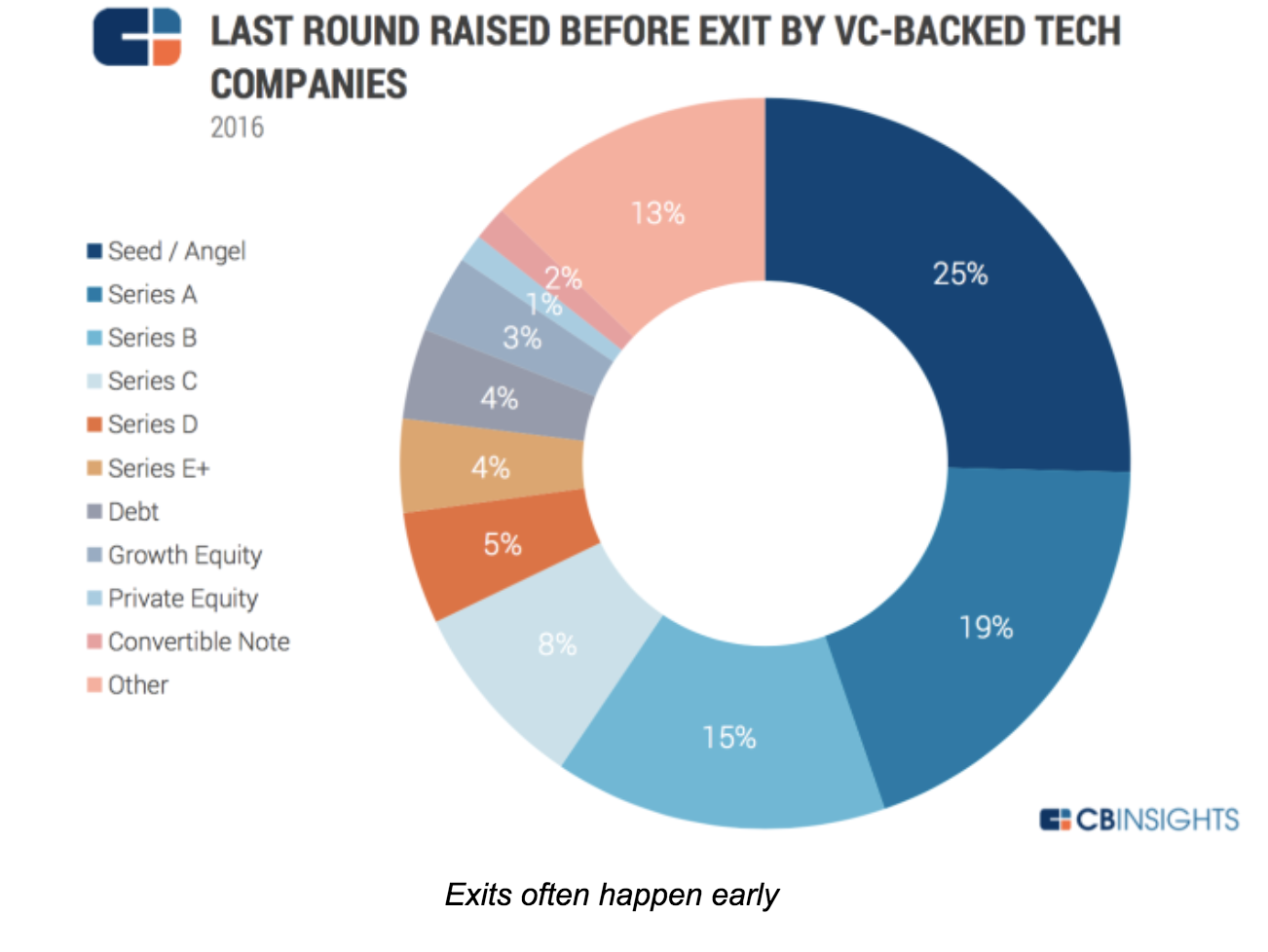

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

Two sites that are actively cataloging failed crypto projects, Coinopsy and DeadCoins, have found that over a 1,000 projects have failed so far in 2018. The projects range from true abandonware to outright scams, and include BRIG, a scam by two “brothers,” Jack and Jay Brig, and Titanium, a project that ended in an SEC investigation.

Obviously any new set of institutions must create their own sets of rules and that is exactly what is happening in the blockchain world. But when faced with the potential for massive token fundraising, bigger problems arise. While everyone expects startups to fail, the sheer amount of cash flooding these projects is a big problem. When a startup has too much fuel too quickly the resulting conflagration ends up consuming both the company and the founders, and there is little help for the investors.

These conflagrations happen everywhere and are a global phenomenon. Scam and dead ICOs raised $1 billion in 2017 with 297 questionable startups in the mix.

There are dubious organizations dedicated to “repairing” broken ICOs, including CoinJanitor from Cape Town, but the fly-by-night nature of many of these organizations does not bode well for the industry.

ICO-funded startups currently use multi-level marketing tactics to build their business. Instead they should take a page from the the Kickstarter and Indiegogo framework. These crowd-funding platforms have made trust an art. By creating collateral that defines the team, the project, the risks and the future of the idea, you can easily build businesses even without much funding. Unfortunately, the lock-ups and pricing scams the current ICO market uses to incite greed rather than rational thinking are hurting the industry more than helping.

The bottom line? Invest only what you can afford to lose and expect any token you invest in to fail. Ultimately, the best you can hope for is to be pleasantly surprised when it doesn’t. Otherwise, you’re in for a world of disappointment.

Powered by WPeMatico

The American Midwest has a long history of making stuff. During the 20th century, it was the manufacturing center for the nation, and indeed much of the world. It’s still where a surpassing majority of agricultural commodities are grown and processed. But is it also a major producer of technology startups? Maybe not as much as the coasts, but the Midwest’s bustling metropoli and vast expanses of rural land prove to be fertile ground for quite a bit of startup activity.

And that’s what we’re going to take a look at here. In a similar vein to our recent analysis of startup fundraising in the South, we’ll break down the region into its constituent parts, assessing deal and dollar volume trends in the Midwest’s two primary sub-regions, some of its individual states and the most active metropolitan areas in the U.S.’s midsection.

And, to be clear, this is not Crunchbase News’s first foray into the region. We’ve covered the region’s seed-stage interest in AI and hard tech, a few notable rounds and have always included the Midwest in all manner of data-spelunking expeditions. And to this, we’ll add a deep dive into the numbers.

Borders and boundaries are a deep well of disputes. To preempt debate, we use the U.S. Census Bureau’s definition of the Midwest region which, unlike its definition of the South, shouldn’t be too controversial. If you have something against Kansas or Ohio being included in this group, take it up with the Feds.

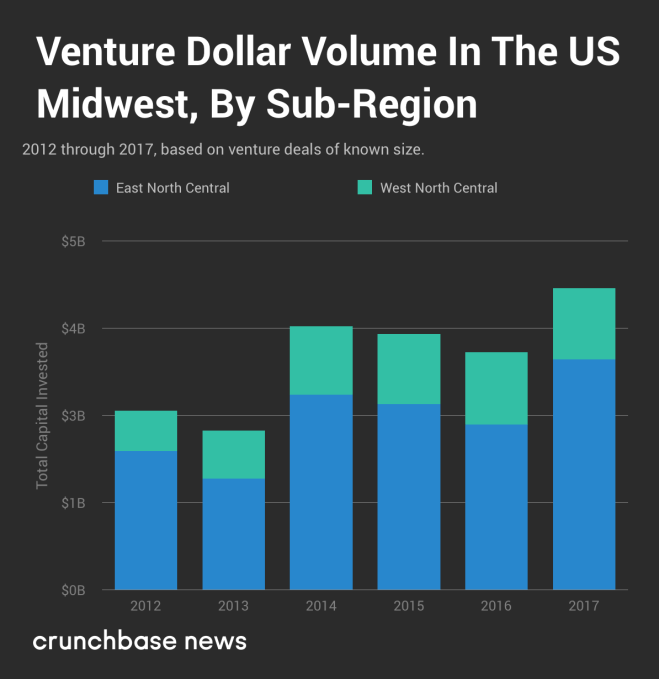

The good folks at the Census Bureau split the Midwest into two distinct — and rather unimaginatively named — sub-regions: the West North Central and East North Central states, which are separated by the Mississippi River. We’ve included the map below.

By splitting the Midwest into two distinct parts, we’ll be able to see where most of the startup and funding activity is concentrated. Spoiler alert: The farther west you go, the startup population (and the population itself) grows more scattered.

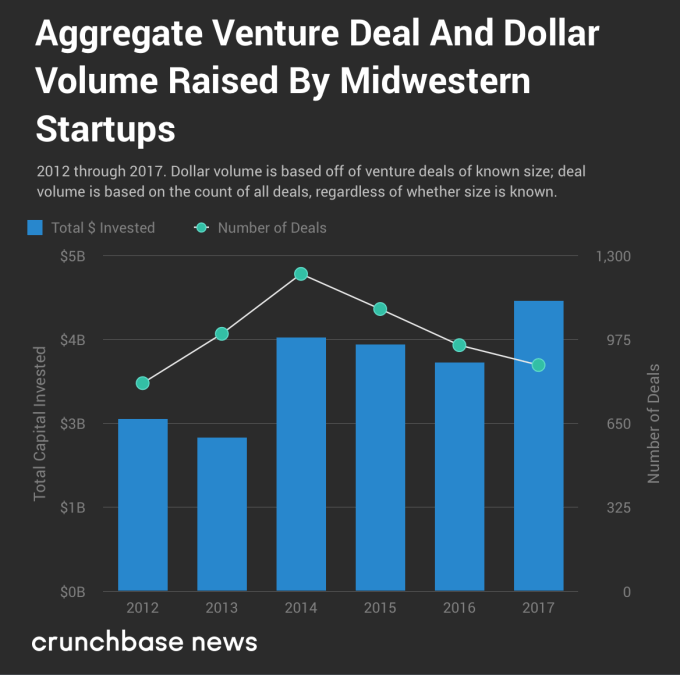

Based only on reported data in Crunchbase, the Midwest appears to be affected by the same phenomenon as the rest of the country. Crunchbase News has previously found that the number of seed and early-stage deals has gone off a cliff in the U.S., resulting in a top-heavy market featuring many large, late-stage deals. And this wouldn’t be a problem if it weren’t for a shortfall in new startups to fill the next cycle of early-stage funding. The “hollowing out” of the Midwestern venture deal pipeline becomes readily apparent when you look at funding data for the past several years, which you can find in the chart below.

To wit, deal volume is down markedly since 2014, as Crunchbase News reported in its Q4 2017 report of startup funding activity in the U.S. and Canada. But somewhat counterintuitively, the amount of money being invested into startups is on the rise in the Midwest and throughout many other parts of the country, reaching fresh multi-year highs in 2017. Almost one full quarter into 2018, the trend appears to continue unabated.

But this chart abstracts away a lot of nuance, so let’s take a closer look at the region and its states.

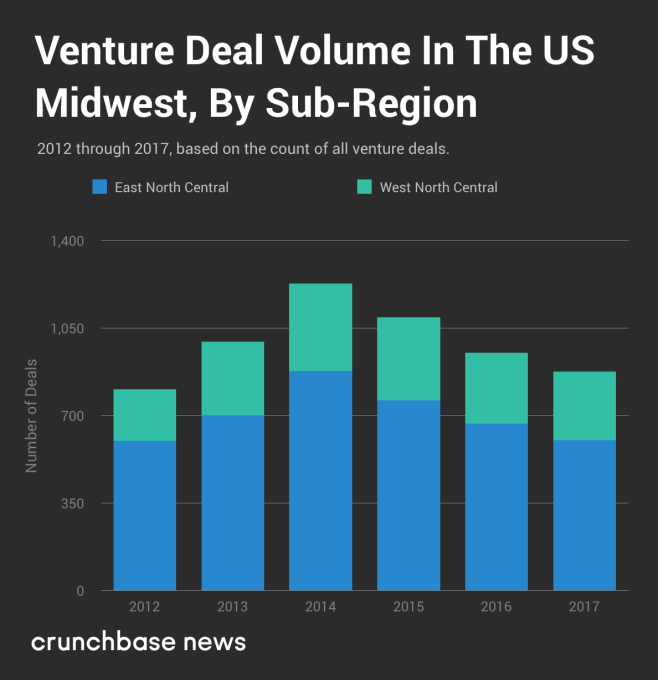

We’ll start first with deal volume, because that’s a fairly decent indicator of a geographic region’s level of startup activity. Below, we’ve plotted venture deal volume, divided by sub-region.

Again, based on the reported data from Crunchbase, we found that deal counts have been on a downward trend for several years. And though some of this may be attributable to reporting delays, projected deal volume data for the whole of the U.S. and Canada (fourth chart down in the Q4 quarterly report) shows a years’-long downtrend. There’s no reason to believe that startup activity in the Midwest is materially different from the rest of the U.S. and Canada.

But what about the relative “balance of power” between the two sub-regions? At least when it comes to deal volume, has one sub-region waxed while the other waned? To a limited extent, the answer is yes. Between 2012 and 2017, the percentage share of all Midwestern dealflow going to West North Central states like the Dakotas, Minnesota and Missouri has grown from 25.4 percent to 31.2 percent, up by nearly one-fifth in relative terms.

Now let’s check out dollar volume. The chart below displays aggregate reported venture capital dollar volume raised by startups in the Midwest.

As far as the amount of money Midwestern startups have raised over time, the trendline is generally up and to the right. But that’s not the only way this differs from the deal volume data we looked at earlier. For dollar volume, there appears to be no appreciable change in the “balance of power” between the two sub-regions since 2012. Depending on the year, East North Central states like Illinois, Michigan and Ohio raked in between 70 and 78 percent of total dollar volume, but that variance doesn’t appear in an orderly trend.

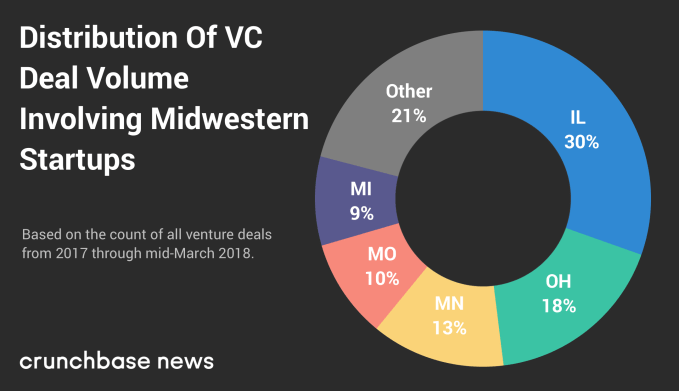

We started first at the regional level, then compared smaller groupings of states. Now, let’s see how deal and dollar volume is distributed on a state-by-state level. Doing so will point to the states that lead the region in venture-backed startup activity. Below, you’ll find a chart of how deal volume is split between the top five Midwestern states.

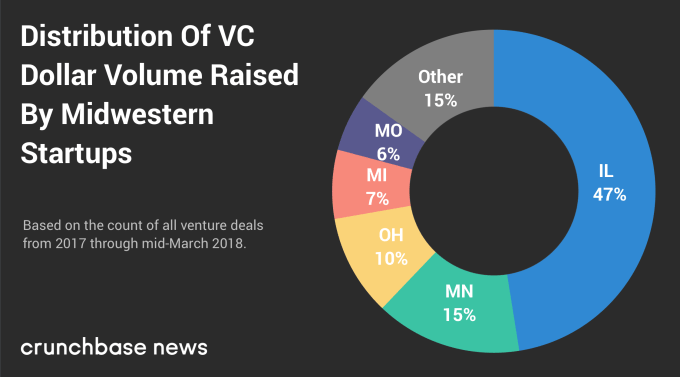

And here is how dollar volume is distributed.

As we saw with our analysis of the South, the top five Midwestern states for deal volume are the same five top-ranked states for dollar volume. But there is some notable variation in how these states rank among each other and the amount of deal and dollar volume they account for.

Considering that Illinois is home to Chicago and a number of downstate universities with deep tech startup roots, the fact that it places first for both metrics shouldn’t come as much of a surprise.

What might be more of a head-scratcher is Minnesota, which ranks third in deal volume but second in dollar volume. Why does it switch places with Ohio? The answer could lie in the industrial mix which, in the case of Minnesota, includes a disproportionately high number of medical device and other life sciences companies, which typically take a lot of capital to get off the ground.

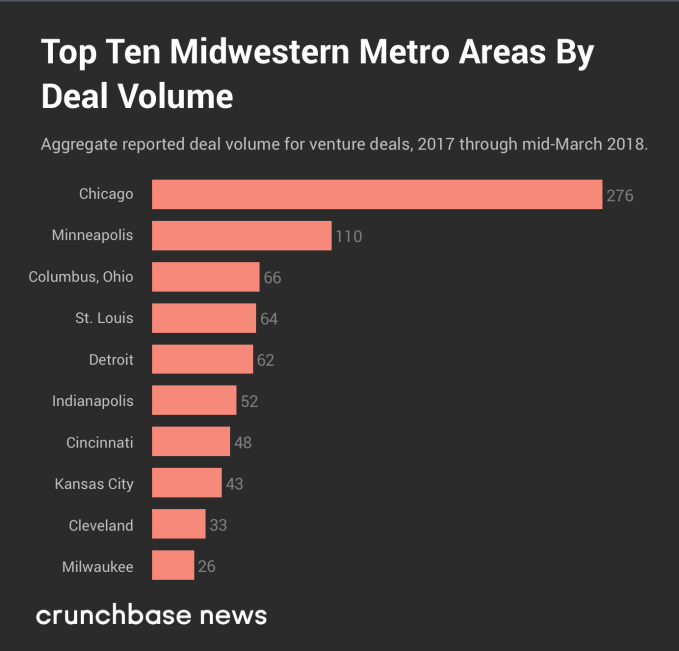

Longtime readers of Crunchbase News may remember a ranking of Midwestern startup cities we wrote back in August 2017. However, here we’re just focusing on deal and dollar volume over the past 15 months, since the start of 2017.

Let’s start first with the top 10 Midwestern cities as measured by number of startup funding rounds.

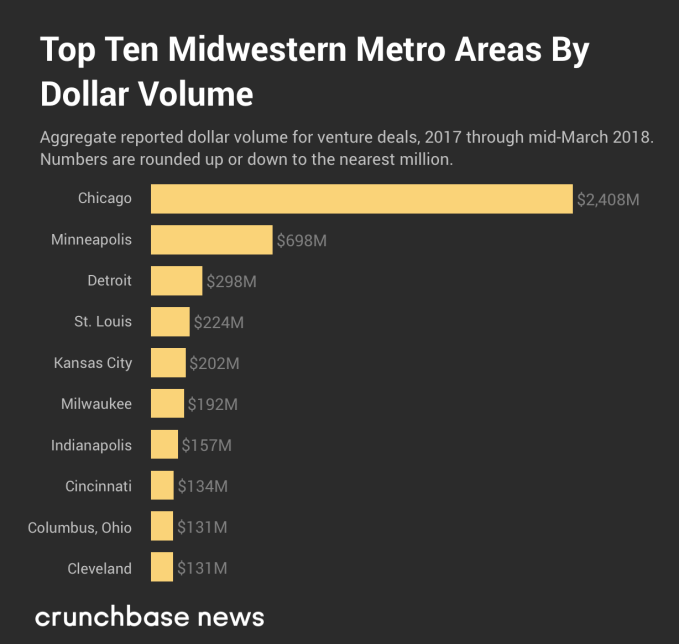

And in the chart below, you can see the top cities, as ranked by venture dollar volume, from the same period of time.

In both rankings, four of the top five cities are the same, but the odd one out appears to be Columbus, Ohio. Although there were a fairly large number of rounds raised by startups in that metro area, most of the rounds were fairly small by national standards. And one of the main reasons why Kansas City, Missouri jumped so much in the dollar volume rankings was a $100 million Series F round raised by C2FO.

But, again, as far as the Midwest goes, everything pales in comparison to Chicago alone.

For many, the Midwest is in a kind of Goldilocks zone. The East and West coasts seem to hold more or less equal sway over the culture and economy and most of its cities are neither too big nor too small. The only extreme it seems to occupy is its winter weather.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.