entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

Are more Theranos -style scandals looming for investors in healthcare startups?

A team of researchers associated with the Meta-Research Innovation Center at Stanford thinks so. They’ve published a paper warning investors in life sciences startups that a systemic lack of transparency exists in their portfolio companies — creating the possibility for more multi-billion-dollar implosions and scandals like the one that toppled Theranos and its charismatic founder, Elizabeth Holmes.

Indeed, one of the study’s authors, Dr. John Ioannidis, the co-director of the Meta-Research Innovation Center at Stanford and director of the University’s PhD program in Epidemiology and Clinical Research, was among the first people to identify the risks associated with Theranos and its “stealth research.”

Now Dr. Ioannidis and his co-authors, Ioana A. Cristea and Eli M. Cahan, have published a study surveying the publicly available research from the largest privately held companies in the healthcare space, and found them lacking.

Most of the highest-valued startups in healthcare have not published any significant scientific literature, the study found. Nearly half of the publications from companies worth more than $1 billion came from only two startups — 23andMe and Adaptive Biotechnologies, according to the paper.

“Many years ago I was the first person to say that Theranos had a problem,” says Ioannidis. “The problem that I had then was that Theranos did not have any peer-reviewed evidence to show.”

In an interview and in their paper, Ioannidis and Cahan warn that investors have overlooked systemic problems created by the lack of transparency among healthcare startups.

They write:

It would be tempting to dismiss the Theranos case as just one rotten apple. However, we worry that the focus on fraud puts aside a more fundamental concern. Fraud is making waves in the news, but stealth research may have a more detrimental impact.

According to the study’s findings, more than half of the healthcare startups that are worth more than $1 billion have published no highly cited papers at all. For companies that were acquired or are publicly traded that number is around 40 percent.

In all, healthcare startups that are currently valued at more than $1 billion published 425 Pubmed papers. And of those papers only 34 (8 percent, including two reviews) were highly cited. For companies with valuations of more than $1 billion that had been acquired or are publicly traded on stock exchanges, the researchers counted 413 papers, of which 47 (11 percent, including nine reviews) were highly cited.

Digging deeper into some of the companies that had high valuations but little or no published research revealed scores of operational and technological issues for the researchers.

For instance, StemCentrx, which was bought for $10.2 billion in 2016 by AbbVie, had published 16 papers — and only one highly cited paper. Since the acquisition, the Food and Drug Administration had imposed a delay on the readout of the company’s phase II trial for its Rova T targeted antibody drug for cancer treatment. In December, a Phase III trial for Rova T as a second-line treatment for patients with advanced small cell lung cancer was halted because the treatment wasn’t working, according to a report in Targeted Oncology.

Acerta Pharma, another healthcare-focused startup focused on cancer treatments, was bought by AstraZeneca for $7.3 billion. That company published nine articles and had one highly cited paper for a very early study of a potential treatment for relapsed chronic lymphocytic leukemia. Acerta received accelerated approval for a drug called acalabrutinib, which treats a rare form of lymphoma called mantle cell lymphoma. Two years ago, AstraZeneca had to retract data and admit that Acerta falsified preclinical data for its drug.

Then there’s Intarcia, the developer of a device for diabetes treatment that’s worth $5.5 billion. That company had its device rejected by the FDA and was forced to lay off staff and halt a couple of later-stage trials. It had only published six papers — none of them very highly cited.

Ultimately, the researchers concluded that highly valued healthcare startups don’t contribute to published research and that the valuation of these companies by investors is divorced from any externally validated data.

For the researchers (and for investors) this should present a problem.

“Many unicorns may be overvalued [21] and subject to unrealistic scientific expectations,” the study’s authors write. And they reject the argument that simply applying for — and receiving — patents is enough to prove that a technology in the healthcare space has been thoroughly vetted. “[Patents] do not offer the same level of documentation as peer-reviewed articles. For example, Theranos had over 100 patents [1], but these were unable to supplant the vacuum in their evidence,” the researchers wrote.

Even if companies want to protect their technology, there are still ways for them to be more transparent about the results or benefits of their technology. The authors acknowledge that publishing isn’t the primary mission of startups. They can, however publish a few high-value articles, secure their technology through patents and then work with researchers, universities or hospitals to validate the technology and have those organizations publish results of the tests, the authors argue.

As the authors conclude:

Start-ups are key purveyors of innovation and disruption. Consequently, holding them to a minimal standard of evaluation from the scientific community is crucial. Participation in peer review, with all its limitations, is the best way we have to uphold this standard. We are not arguing that start-ups should divert excessive resources to having peer-reviewed papers. However, when their products are destined to affect patient health, they should neither be solely doing marketing. Confidential data sharing with potential investors or regulators cannot replace more open scrutiny by the scientific community.

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

About 13 years ago I faced an excruciating decision: whether to sell my company, Pinnacle Systems, to a private equity firm or to another large public company. I felt that both suitors would treat my employees well (and I negotiated hard to make sure that was the case), and both offered a good asking price well above our value on NASDAQ.

After raising what at the time felt like my first child, born in my living room and nurtured into a publicly traded entity, I was ready for it to take its next step and for me to take mine. I ultimately opted for the strategic sale, but I left the process intrigued by what was already an evolving dynamic between private equity firms and tech exits.

In years past, stigma often accompanied private equity sales. I know I felt that way, even under strong deal terms. Plus, private equity exits were only available to companies generating substantial annual revenues and often profits, making this exit option inaccessible for many startups. Today, private equity buyout firms can provide a solid (and on occasion excellent) exit route — as well as an increasingly common one, accounting for 18.5 percent of VC-backed exits in 2017.

Private equity firms are investing in a broad array of technology companies, including highly valued unicorns, but also early- to mid-stage profitable and unprofitable companies that a few years ago would have been unable to secure interest from these buyout firms.

In addition, the lines between venture capital and private equity are increasingly blurring, with more private equity investments in tech, and several-late stage VC firms creating large, billion-dollar plus late-stage growth funds. Further blurring the lines, some of the late-stage VC firms are taking controlling interests in startups, a strategy typically associated with private equity. Recently, one of our portfolio companies received an investment from a late-stage VC firm that acquired a majority stake by providing liquidity to some existing shareholders and investing in the company, utilizing a strategy typically associated with PE buyout firms.

The rise of private equity buyouts within the tech sector presents a viable exit option for founders, given the reality that most startups won’t ultimately IPO. (According to PitchBook, only 3 percent of venture-backed companies in the last decade eventually went public.)

If an IPO is not a realistic long-term option, the remaining primary exit option has typically been a sale to another company (a strategic buyer, in venture parlance). However, in the past few years, private equity firms have become aggressive buyers of private companies, sometimes bidding as high as or higher than strategic buyers. With one of my portfolio companies, a private equity buyer placed the second highest bid ahead of all but one strategic buyer and helped raise the final price from the strategic buyer just by being in the bidding process.

Founders who find themselves in negotiations with strategic buyers should also reach out to PE firms to optimize the outcome. Silver Lake, Francisco Partners, Thoma Bravo and Vista are a few technology-focused PE firms, and PitchBook’s annual liquidity report lists other firms. Vista has been especially active, acquiring many technology companies, including Infoblox, Lithium and Marketo. Not all PE firms are the same, just like not all VCs and strategic buyers are the same.

Years ago, when private equity buyouts were typically only large deals, new management teams were almost always brought in to tweak the edges of already successful companies. Today, each private equity firm has its own strategy — some only buy large profitable companies, others focus on mid-size acquisitions and some only buy early-stage (typically unprofitable) companies, which brings us to the next point.

Even early-stage startups can explore a PE exit, especially if things are not going well

While most readers are familiar with private equity buyers at later stages, what’s new is the emergence of PE activity at early stages. These firms acquire majority stakes in startups that have only raised early-stage investments but are having trouble scaling or raising the next round.

After a buyout, these private equity firms typically provide value by adding the missing elements, such as marketing or sales know-how, in order to kick-start the business and achieve scale. Their goal is to increase the value of the underlying asset by augmenting founder teams with the buyout firm’s own operational experts, sometimes combining newly acquired assets with already existing assets to create a stronger whole, or doubling-down on promising products (while shedding less promising offerings) to unlock potential.

Typically, these PE firms then sell the company to another company (usually a strategic buyer) for greater value. In some cases, these early-stage PE firms sell to another PE buyout firm further up market. In some of these acquisitions, founders can maintain minority ownership in the company (though not a controlling stake), which they can carry through to their “next exit.”

Unlike PE buyouts at later stages, PE buyouts at the earlier stages are not usually high-value exits; they are mostly an avenue to provide the founders some return for their hard work, rather than the disappointing returns they can expect from an acqui-hire or, even worse, a shutdown. If negotiated correctly, a private equity deal can give founders an opportunity to play another hand to the next exit.

Few founders create companies in order to flip them. Strong entrepreneurs create companies to transform their missions into reality and positively impact the world. Steve Jobs said, “I’m convinced that about half of what separates the successful entrepreneurs from the non-successful ones is pure perseverance.” An acquisition — particularly to private equity — may not have been the original goal, but it may fuel the continued pursuit of the founder’s mission. Or, perhaps it will enable the pursuit of a new and worthy mission.

Powered by WPeMatico

Many founders believe in the myth that the first steps of starting a business are the hardest: Attracting the first investment, the first hires, proving the technology, launching the first product and landing the first customer. Although those critical first steps are difficult, they are certainly not the most difficult on the arduous path of building an iconic company. As early and late-stage funding becomes more abundant, founders and their early VC backers need to get smarter about how to position their companies for a looming valley of death in-between. As we’ll learn below, it’s only going to get much, much harder before it gets easier.

Money will have the look, and heft, of dumbbells as the economic cycle turns. Expect an abundance of small, seed checks at one end, an abundance of massive checks for clear, breakout companies at the other, and a dearth of capital for expanding companies with early proof points and market traction. Read more on how to best prepare for this inevitable future. (Image courtesy Flickr/CircaSassy)

There will be an abundance of capital at the two ends of the startup spectrum. At one end, hundreds of seed and micro VCs, each armed with dozens of $250,000-$1 million checks to write every year, are on the prowl for visionary founders with pedigrees and resumes. At the other end, behemoths like SoftBank, sovereigns, as well “early-stage” firms raising larger funds are seeking breakout companies ready for checks that are in the mid-tens to hundreds of millions. There will be a dearth of capital to grow companies from a kernel of a business, to becoming the clear market-defining leader. In fact, we’re already seeing deal volume decreasing significantly as dollars increase, likely evidence of larger checks going into fewer companies.

Even as the overall number of deals decrease below 2012 levels, the overall dollars invested into startups continue to soar. The 200+ “seed-stage” funds formed since 2012 will continue to chase nascent companies. Meanwhile, the increasing number of mega-funds will seek breakout companies into which to make $100 million+ investments. Companies with early traction seeking ~$20 million to grow will be abundant and have difficulty accessing capital.

Founders should no longer assume that their all-star seed and Series A syndicates will guarantee a successful follow-on financing. Progress on recruiting and product development, though necessary, are no longer sufficient for B-rounds and beyond. Founders should be mindful that investors that specialize in leading $20-50 million rounds will have a plethora of well-funded, well-mentored, well-staffed startups with slick presentations, big visions and some early market traction from which to choose.

Today, there is far more capital chasing fewer quality companies. Fewer breakout companies and fear of missing out is making it easy to raise growth rounds with revenue growth, which may not be scalable or even reflective of an attractive business. This is creating false realities and prompting founders to raise big rounds at high prices — which is fine when there is an over-abundance of capital, but can cripple them when capital later becomes scarce. For example, not long ago, cleantech companies, armed with very preliminary sales, raised massive financings from VCs eager to back winners toward scaling into what they characterized as infinite demand. The reality is that the capital required to meet target economics was far greater and demand far smaller. As the private markets turned, access to cash became difficult and most faltered or were acquired for pennies on the dollar.

There is a likely future where capital grows scarce, and investors take a harder look at the underpinnings of revenue, growth and (dis)economies of scale.

What should startup leadership teams emphasize in an inevitable future where the $30 million rounds will be orders of magnitude harder than their $5 million rounds?

Leadership teams put lots of emphasis on revenue. Unfortunately, revenue that’s not representative of the big vision is probably worse than no revenue at all. Companies are initially seeded with the expectation that the founding team can build and sell something. What needs to be proven is the hypothesis that the company can a) build a special product that b) is inexpensive to convince customers to pay for, and c) that those customers represent a massive market. It should be proven that it is unattractive for customers to switch to the inevitable copycats. It should be clear that over time, customers will pay more for additional features, and the cost of acquiring new customers will go down. Simply selling a product to customers that don’t represent that model is worse than not selling anything at all.

Early founding teams are cognitively diverse individuals that can convince early investors that they can overcome the incredible odds of building a company that until now, shouldn’t have existed. They build a unique product, leveraging unique tools satisfying an unmet need. The early teams need to demonstrate the big vision, and that they can recruit the people that can make that vision a reality. Unfortunately, more founders struggle when it comes to recruiting people that have real experience reducing a technology to practice, executing on a product that customers want and charting the path to expand their market with improving unit economics. There are always exceptions of people that do the above for the first time at startups; however, most of today’s iconic startups knew what kind of talent they needed to execute and succeeded in bringing them on board. Who’s on your team?

The attractive SaaS valuation multiples behoove all founders to apply its metrics to their businesses even if they aren’t really SaaS businesses. Sophisticated later-stage investors see right past that and dismiss numbers associated with metrics that are not representative. Semiconductors are about winning dedicated sockets in growing markets. Design tools are about winning and upselling seats in an industry that’s going to be hooked on those tools. Develop a clear understanding of how your business will be measured. Don’t inundate your investor with numbers; present a concise hypothesis for your unfair advantage in a growing market with your current traction being evidence to back it.

“Pouring fuel on the fire” is a misleading metaphor that leads some into believing that capital can grow any business. That’s just as true as watering a plant with a fire hose or putting TNT in your Corolla’s gas tank: most business models and markets simply are not native to the much-sought-after venture growth profile. In fact, most later-stage startups that fail after raising large amounts of capital fail for this reason. Most markets are conducive to businesses with DIS-economies of scale, implying dwindling margins with scale, which is why many businesses are small, serving local, fragmented markets that technology alone cannot consolidate. How do your unit economics improve over time? What are the efficiencies generated by economies of scale? Is there a real network effect that drives these economies?

Image courtesy Getty Images

I expect today’s resourceful founders to seek partners, whether it’s employees, advisors or investors, to help them answer these questions. Together, these cognitively diverse teams will work together to accelerate past any metaphoric valley and build the iconic companies taking humanity to its fantastic future.

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

In a disappointing year for female-founded startups — at least those looking to raise venture capital — The Riveter not only closed its first institutional funding round, but it’s today announcing a $15 million Series A funding, bringing its total backing to $20.5 million.

The Seattle-based co-working startup, led by co-founder and chief executive Amy Nelson (pictured), has raised the capital from lead investor Alpha Edison, with support from Madrona Venture Group, New America president and CEO Anne-Marie Slaughter, fashion designer Liz Lange and TOMS founder Blake Mycoskie .

As of November, startups founded by all-female teams had closed 391 deals worth $2.3 billion, an increase from the $2 billion invested in 2017, though still just 2.2 percent of all VC invested this year.

Nelson, an advocate for female entrepreneurs who’s spoken publicly about women’s struggles in the workplace, the difficulties of launching a business in a man’s world and raising venture dollars as a solo female founder, started The Riveter in 2016 after a decade-long career as a lawyer. Today, the startup operates five locations in the U.S., with ambitious plans to open another 100 female-focused co-working spaces by 2022.

“I want The Riveter to be the place people think of when they think of women and work,” Nelson told TechCrunch.

The Riveter has 2,000 members throughout its locations in Seattle, Bellevue, Wash. and Los Angeles. Its expansion plans include new spots in Texas, Colorado and Portland.

The spaces are built with women in mind but are not exclusive to one gender. Nelson tells us The Riveter’s membership is 25 percent male, setting it apart from spaces like The Wing, which is only available to female-identifying people.

A look inside one of The Riveter’s Seattle co-working spaces

“I don’t think the future is female, I think the future is fluid,” she said. “Gender is becoming an outdated idea but at the same time, it’s important to think of women when we build these spaces … There is a lot of value to women’s only spaces but our take on it is we want to redefine the future of work for women and we want everyone to be part of it.”

The Riveter provides space to work and collaborate; a digital network, currently in beta, for its members to connect; and programming ranging from office hours with venture capitalists to “self-care Saturday.”

Other investors in the startup include Brilliant Ventures, The Helm and X Factor Ventures.

Powered by WPeMatico

Ten years ago the iOS App Store launched — and the mobile revolution was off. Entrepreneurs everywhere rallied to take advantage, building category-defining consumer companies like Twitter, Uber, Lyft and Square, among many others.

There’s no better time for an entrepreneur to start a company than when a new platform like mobile emerges. The rising tide in these moments becomes a tsunami: Eager customers descend on services through word of mouth and new acquisition channels; there’s outsized press interest; and sales take off in part due to growth of the platform itself.

Now is not one of these periods. Mobile appears mature, and the next great enabling platform is still just past the horizon. That’s why many early-stage VCs have shifted their focus away from consumer and to other new enabling technologies, such as autonomous vehicles, blockchain and AI/ML.

I have a different view. I think now is a great time to build consumer companies, even without a new platform. There are three reasons for this. First, the internet has created big problems for humans, organizations and society, which entrepreneurs can attack at scale. Second, the first wave of mobile-enabled companies have laid a foundation — including processes, seasoned executives and business models — that new entrepreneurs can borrow. And third, mobile technology is still changing and evolving.

Let’s take a closer look at all three.

The last wave of breakout companies created interactive platforms (Twitter, Snapchat, Instagram, etc.) that have entertained many. They didn’t solve big societal problems. There’s now a big need — and big opportunity — for companies that can help people save time, money and sanity, even as they build great businesses.

Most of us now realize the major problems that a connected, mobile, always-on world has wrought. These include:

After a decade of building companies for mobile, there are now untold stories, battle scars and people available for future companies to learn from. This makes it easier for startups to assemble playbooks and experienced teams. It also reduces the downside risk for investors, opening new paths to capital for companies that need it.

For instance, it’s now clear that consumer brands must define, own and curate an end-to-end experience. A great new example is GOAT, the online sneakerhead marketplace. Faced with a sneaker market full of rampant knock-offs, the founders invested in a capital- and time-intensive process to manually inspect every shoe for authenticity. The result is an experience that every sneakerhead loves and a breakthrough consumer brand.

Building a breakout consumer platform will be more complex, more challenging and often more capital-intensive than it was for the prior generation.

There are also lots of executives and teams that know how to lead and manage complex operations, especially on the ground. This is crucial to scale logistically complex ideas like Opendoor, Instacart and others.

The other thing needed to help scale these companies is capital. And right now, there are two particularly relevant new kinds of investors: 1) mega equity funds like SoftBank Vision Fund, and 2) alternative lending funds that provide non-dilutive capital to companies to finance the acquisition of traditional assets. Those capital sources enable companies like Opendoor (disclosure: I’m a personal investor) to own and manage a truly delightful end-to-end experience.

Mobile devices have come a long way over the last decade. And there will be many more meaningful improvements in the near future, allowing for new uses and new companies.

I anticipate breakthroughs that will boost the ability of the chips and subsystems on a phone to perform optimally for far longer. Right now, these are throttled due to heating issues and other problems. As companies solve these issues, they’ll create order of magnitude improvements on what our phones are capable of, bringing technologies like VR and AR, to take two examples, far forward into everyday use.

On the network side, 5G and subsequent buildouts will meaningfully change what kinds of bandwidth we can handle, enabling even more data and compute to be in the cloud.

Mobile today is about one-to-many broadcast platforms like Instagram, Twitter and Facebook. Tomorrow’s great consumer companies will leverage a better vector: one-to-one customer intimacy. Companies like Grove Collaborative (disclosure: Mayfield is an investor) are experiencing hypergrowth in part by using real people connecting with consumers over text to bring a curated, personalized experience to shopping for household staples. I expect this to be a major trend, with the companies that earn the right to communicate more with customers the ones that win.

Building a breakout consumer platform will be more complex, more challenging and often more capital-intensive than it was for certain titans of the prior generation. But for those with the vision and substance to bring a valuable service to the world that solves real problems, the resources and emerging technologies will be there to help create the next groundbreaking consumer brand.

Powered by WPeMatico

Many entrepreneurs assume that an invention carries intrinsic value, but that assumption is a fallacy.

Here, the examples of the 19th and 20th century inventors Thomas Edison and Nikola Tesla are instructive. Even as aspiring entrepreneurs and inventors lionize Edison for his myriad inventions and business acumen, they conveniently fail to recognize Tesla, despite having far greater contributions to how we generate, move and harness power. Edison is the exception, with the legendary penniless Tesla as the norm.

Universities are the epicenter of pure innovation research. But the reality is that academic research is supported by tax dollars. The zero-sum game of attracting government funding is mastered by selling two concepts: Technical merit, and broader impact toward benefiting society as a whole. These concepts are usually at odds with building a company, which succeeds only by generating and maintaining competitive advantage through barriers to entry.

In rare cases, the transition from intellectual merit to barrier to entry is successful. In most cases, the technology, though cool, doesn’t give a fledgling company the competitive advantage it needs to exist among incumbents and inevitable copycats. Academics, having emphasized technical merit and broader impact to attract support for their research, often fail to solve for competitive advantage, thereby creating great technology in search of a business application.

Of course there are exceptions: Time and time again, whether it’s driven by hype or perceived existential threat, big incumbents will be quick to buy companies purely for technology. Cruise/GM (autonomous cars), DeepMind/Google (AI) and Nervana/Intel (AI chips). But as we move from 0-1 to 1-N in a given field, success is determined by winning talent over winning technology. Technology becomes less interesting; the onus is on the startup to build a real business.

If a startup chooses to take venture capital, it not only needs to build a real business, but one that will be valued in the billions. The question becomes how a startup can create a durable, attractive business, with a transient, short-lived technological advantage.

Most investors understand this stark reality. Unfortunately, while dabbling in technologies which appeared like magic to them during the cleantech boom, many investors were lured back into the innovation fallacy, believing that pure technological advancement would equal value creation. Many of them re-learned this lesson the hard way. As frontier technologies are attracting broader attention, I believe many are falling back into the innovation trap.

So what should aspiring frontier inventors solve for as they seek to invest capital to translate pure discovery to building billion-dollar companies? How can the technology be cast into an unfair advantage that will yield big margins and growth that underpin billion-dollar businesses?

Talent productivity: In this age of automation, human talent is scarce, and there is incredible value attributed to retaining and maximizing human creativity. Leading companies seek to gain an advantage by attracting the very best talent. If your technology can help you make more scarce talent more productive, or help your customers become more productive, then you are creating an unfair advantage internally, while establishing yourself as the de facto product for your customers.

Great companies such as Tesla and Google have built tools for their own scarce talent, and build products their customers, in their own ways, can’t do without. Microsoft mastered this with its Office products in the 1990s through innovation and acquisition, Autodesk with its creativity tools, and Amazon with its AWS Suite. Supercharging talent yields one of the most valuable sources of competitive advantage: switchover cost. When teams are empowered with tools they love, they will loathe the notion of migrating to shiny new objects, and stick to what helps them achieve their maximum potential.

Marketing and distribution efficiency: Companies are worth the markets they serve. They are valued for their audience and reach. Even if their products in of themselves don’t unlock the entire value of the market they serve, they will be valued for their potential to, at some point in the future, be able to sell to the customers that have been tee’d up with their brands. AOL leveraged cheap CD-ROMs and the postal system to get families online, and on email.

Dollar Shave Club leveraged social media and an otherwise abandoned demographic to lock down a sales channel that was ultimately valued at a billion dollars. The inventions in these examples were in how efficiently these companies built and accessed markets, which ultimately made them incredibly valuable.

Network effects: Its power has ultimately led to its abuse in startup fundraising pitches. LinkedIn, Facebook, Twitter and Instagram generate their network effects through internet and Mobile. Most marketplace companies need to undergo the arduous, expensive process of attracting vendors and customers. Uber identified macro trends (e.g. urban living) and leveraged technology (GPS in cheap smartphones) to yield massive growth in building up supply (drivers) and demand (riders).

Our portfolio company Zoox will benefit from every car benefiting from edge cases every vehicle encounters: akin to the driving population immediately learning from special situations any individual driver encounters. Startups should think about how their inventions can enable network effects where none existed, so that they are able to achieve massive scale and barriers by the time competitors inevitably get access to the same technology.

Offering an end-to-end solution: There isn’t intrinsic value in a piece of technology; it’s offering a complete solution that delivers on an unmet need deep-pocketed customers are begging for. Does your invention, when coupled to a few other products, yield a solution that’s worth far more than the sum of its parts? For example, are you selling a chip, along with design environments, sample neural network frameworks and data sets, that will empower your customers to deliver magical products? Or, in contrast, does it make more sense to offer standard chips, licensing software or tag data?

If the answer is to offer components of the solution, then prepare to enter a commodity, margin-eroding, race-to-the-bottom business. The former, “vertical” approach is characteristic of more nascent technologies, such as operating robots-taxis, quantum computing and launching small payloads into space. As the technology matures and becomes more modular, vendors can sell standard components into standard supply chains, but face the pressure of commoditization.

A simple example is personal computers, where Intel and Microsoft attracted outsized margins while other vendors of disk drives, motherboards, printers and memory faced crushing downward pricing pressure. As technology matures, the earlier vertical players must differentiate with their brands, reach to customers and differentiated product, while leveraging what’s likely going to be an endless number of vendors providing technology into their supply chains.

A magical new technology does not go far beyond the resumes of the founding team.

What gets me excited is how the team will leverage the innovation, and attract more amazing people to establish a dominant position in a market that doesn’t yet exist. Is this team and technology the kernel of a virtuous cycle that will punch above its weight to attract more money, more talent and be recognized for more than it’s product?

Powered by WPeMatico

Now that “utility” tokens have become a popular and international way to fund major blockchain projects, a pair of investors are creating a new way to turn tokens into true equities. The investors, Jonathan Nelson and Laura Nelson, have created Hack Fund, an early stage investment vehicle that allows startups to launch what amounts to “blockchain stock certificates,” according to Jonathan.

“Our previous business model exchanged equity from startup companies for services, and wrapped that equity into funds that we then sold to investors. These fund investors have included family offices, institutions, and high net worth individuals,” said Jonathan. “However, Hack Fund represents a new business model. Because Hack Fund leverages the blockchain, investors all over the world at all levels can participate in startup investing by trading blockchain stock certificates. Also, its SEC compliant structure means that it is also available to a limited number of accredited investors in the US.”

The team originally created Hackers/Founders, a tech entrepreneur group in Silicon Valley, and they now support 300,000 members in 133 cities and 49 countries. Hack Fund is a vehicle to support some of the startups in the Hackers/Founders network.

“HACK Fund, through its Hackers/Founders heritage, has a large, unique global network,” said Jonathan. “This provides Hack Fund with unparalleled reach and deal flow across the global technology market. There are a few blockchain-based funds, but they are limited themselves to blockchain-only investments. Unlike typical venture funds, HACK Fund will provide quick liquidity for investors, leveraging blockchain technology to make typically illiquid private stocks tradeable.”

The idea behind Hack Fund is quite interesting. In most cases investing in a company leads to up to ten years of waiting for a liquidity event. However, with blockchain-based stock certificates investors can buy shares that can be bought and sold instantly while company performance drives the value up or down. In short, startups become liquid in an instant, which can be a good thing or a bad thing, depending on the founding team.

“HACK Fund is a publicly traded closed-end fund. The fund’s venture investments are valued on a quarterly basis by an independent third party, audited and posted to the blockchain for all token holders to review. There are no K-1 statements issued, there is no partnership/LLC, rather HACK Fund is an investment company akin to Berkshire Hathaway which invests in the same manner as early-stage venture capital,” said Jonathan.

The $100 million fund raise has already kicked off across Asia, Middle East, Latin America and to a small number of accredited investors in the US. The fund will be rounded out with $2 million from retail investors who will be able to buy some of the tokens on October 29th through BRD wallet.

Powered by WPeMatico

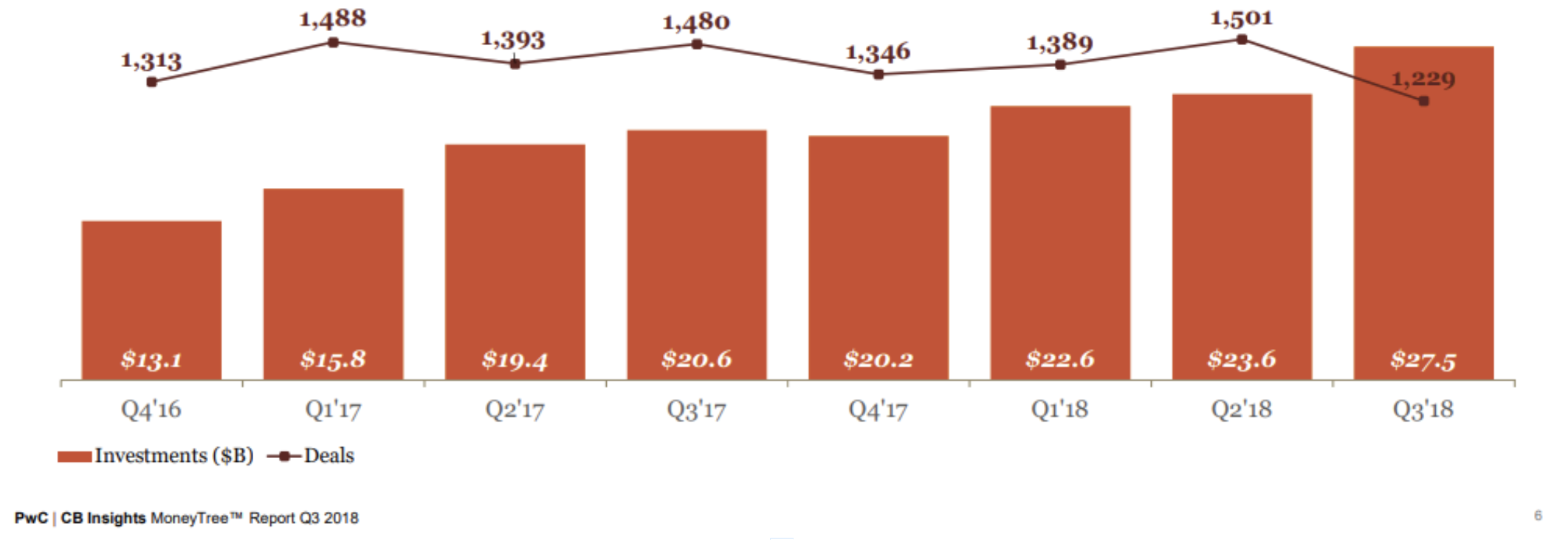

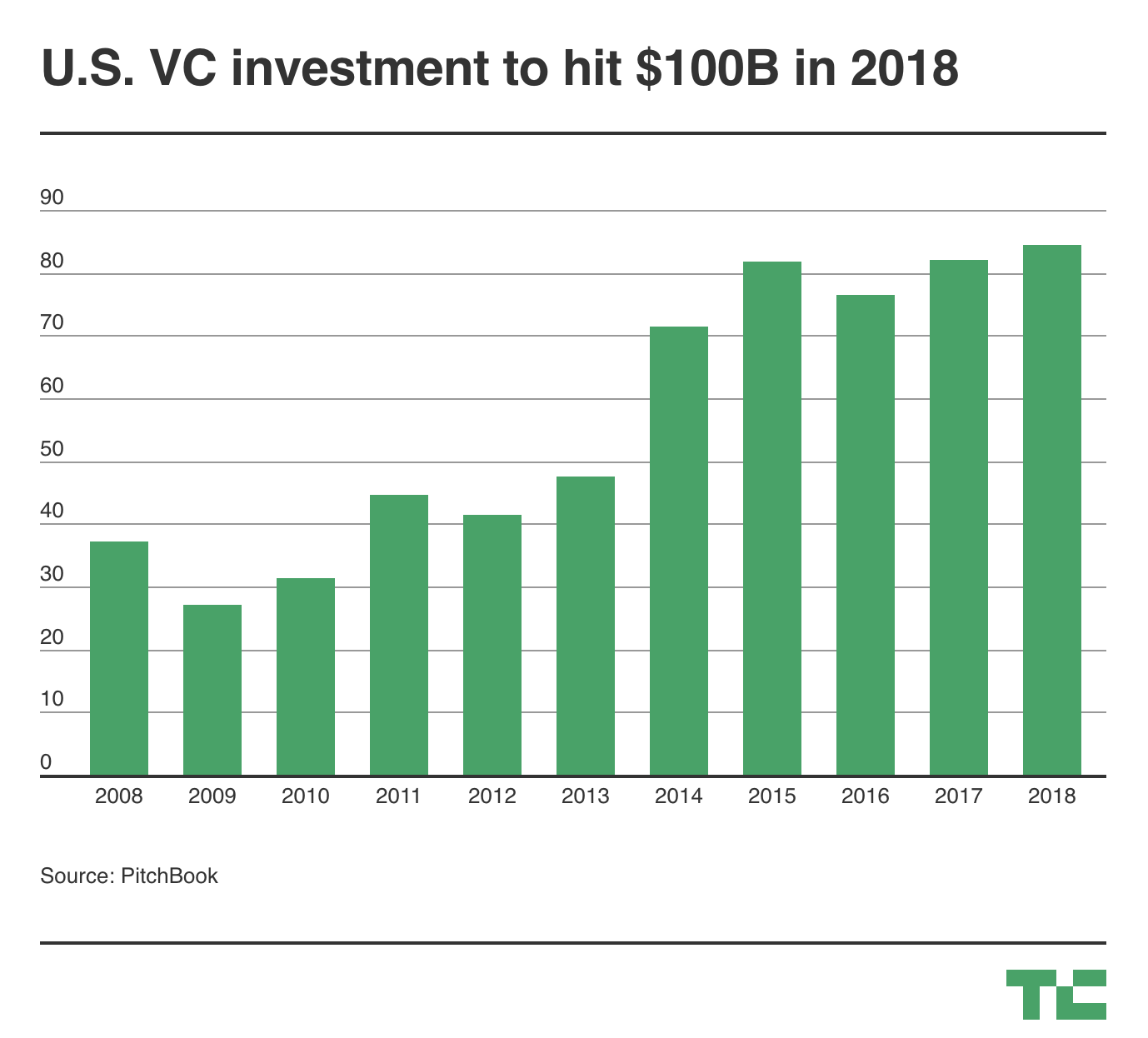

So many new unicorns valued at $1 billion-plus, countless $100 million venture financings, an explosion of giant funds — it’s no surprise 2018 is shaping up to be a banner year for venture capital investment in U.S.-based companies.

There are more than 2.5 months remaining in 2018 and already U.S. companies have raised $84.1 billion — more than all of 2017 — across 6,583 VC deals as of Sept. 30, 2018, according to data from PitchBook’s 3Q Venture Monitor.

Last year, companies raised $82 billion across more than 9,000 deals in what was similarly an impressive year for the industry. Many questioned whether the trend would — or could — continue this year, and oh, boy has it. VC investment has sprinted past decade-highs and shows no signs of slowing down.

Why the uptick? Fewer companies are raising money, but round sizes are swelling. Unicorns, for example, were responsible for about 25 percent of the capital dispersed in 2018. Those companies, which include Slack, Stripe and Lyft, have raised $19.2 billion so far this year — a record amount — up from $17.4 billion in 2017. There were 39 deals for unicorn companies valuing $7.96 billion in the third quarter of 2018 alone.

Some other interesting takeaways from PitchBook’s report on the U.S. venture ecosystem:

Powered by WPeMatico