energy

Auto Added by WPeMatico

Auto Added by WPeMatico

File ice cream vans under “things I never thought posed a significant risk to the environment but might actually.” Nissan has developed a new concept vehicle that addresses the problem of all the emissions generated by conventional ice cream vans, and older models in particular, which pump out a lot of greenhouse gases while idling in order to just make sure the ice cream on board stays iced.

For the project, Nissan’s working with ice cream company Mackie’s of Scotland, a purveyor of fine frozen treats that has already taken steps to reduce its footprint using dairy from its own, family-run farm that’s powered by energy from renewable sources, including wind and solar. From the sustainably-made product, to the new zero-emission delivery van conceived and built by Nissan, the companies are calling the approach a “sky to scoop” way to reduce their carbon footprint.

To start, Nissan took their e-NV200 light-duty commercial van, which itself is fully electric and provides up to 124 miles of range on a charge. For this ice cream concept, the van was modified with Nissan’s new “Energy Roam,” a lithium-ion power pack that uses battery cells recovered from older Nissan EVs built from 2010 on. These repurposed power packs can each store about 0.7kWh with output of 1kW, and two are used on board to run a built-in soft-serve machine, fridges and freezers. The power packs can be recharged either from a 230v main power outlet (this is designed for U.K. use), or from solar tiles installed on the van’s roof, which can fill up the batteries in two to four hours on their own.

Besides its all-electric power sources, the Nissan concept van includes a number of revisions of the traditional model of mobile ice cream selling, including situating the vendor outside the van with a hatch that opens to expose the ice cream dispensing goodness. It’s also equipped with contactless payment support so you can just pay with Apple Pay or Google Pay on the go, and through an integration with What3Words, the van broadcasts its location via Twitter instead of with a jaunty jingle.

Bonus for ice cream sellers: Nissan notes that van owners could collect and store power using the on-board batteries and sell it back to the grid even when it’s not ideal weather for selling cold confections — though it’s definitely still a concept, so this is all theoretical.

Powered by WPeMatico

Entering into the world of Anthemis is a bit like stepping into the frame of a Wes Anderson film. Eclectic, offbeat people situated in colorful interiors? Check. A muse in the form of a renowned British-Venezuelan economist? Check. A design-forward media platform to provoke deep thought? Check. An annual summer retreat ensconced in the French Alps? Bien sûr.

Sitting atop this most unusual fintech(ish) VC is its ponytailed founder and chairman Sean Park, whose difficult-to-place accent and Philosophy professor aura belie his extensive fixed income capital markets experience. He’s joined by founder and CEO Amy Nauiokas, who in addition to being one of Fintech’s most prominent female investors also owns a high-minded film and television production company.

When Arman Tabatabai and I recently sat down with Park and Nauiokas in their New York office, the firm’s leaders were in an upbeat mood, having blown past the temporary perception-setback associated with the abrupt resignation last year of Anthemis’ former CEO Nadeem Shaikh (for more on this, read TechCrunch writer Steve O’Hear’s coverage of the situation).

And as the conversation below demonstrates, Park and Nauiokas are well poised to bring the quirk into everything they touch, which these days runs the gamut from backing companies involved in sustainable finance, advancing their home-grown media platform and preparing a soon-to-be-announced initiative elevating female entrepreneurs.

Gregg Schoenberg: With the two of you now at the helm, how does Anthemis present itself today?

Sean Park: I’ll step back and say that when Amy and I were working at big financial institutions in the noughties, we saw that the industry was going to change and that existing business models were running into their natural diminishing returns.

We tried to bring some new ideas to the organizations we were working in, but we each had epiphany moments when we realized that big organizations weren’t built to do disruptive transformation — for bad reasons, but also good reasons, too.

GS: Let’s fast forward to today, where you have several strong Fintech VCs out there. But unlike others, Anthemis puts weirdness at the heart of its model.

Yes, you’ve backed some big names like Betterment and eToro, but you’ve done other things that are farther afield. What’s the underlying thesis that supports that?

Amy Nauiokas: Whatever we do at Anthemis has to be a non-zero-sum game. It has to be for good, not for evil. So that means that we aren’t looking in any place where you see predatory opportunities to make money.

Powered by WPeMatico

The Valley’s rocky history with cleantech investing has been well-documented.

Startups focused on non-emitting-generation resources were once lauded as the next big cash cow, but the sector’s hype quickly got away from reality.

Complex underlying science, severe capital intensity, slow-moving customers and high-cost business models outside the comfort zones of typical venture capital ultimately caused a swath of venture-backed companies and investors in the cleantech boom to fall flat.

Yet, decarbonization and sustainability are issues that only seem to grow more dire and more galvanizing for founders and investors by the day, and more company builders are searching for new ways to promote environmental resilience.

While funding for cleantech startups can be hard to find nowadays, over time we’ve seen cleantech startups shift down the stack away from hardware-focused generation plays toward vertical-focused downstream software.

A far cry from past waves of venture-backed energy startups, the downstream cleantech companies offered more familiar technology with more familiar business models, geared toward more recognizable verticals and end users. Now, investors from less traditional cleantech backgrounds are coming out of the woodwork to take a swing at the energy space.

An emerging group of non-traditional investors getting involved in the clean energy space are those traditionally focused on fintech, such as New York and Europe-based venture firm Anthemis — a financial services-focused team that recently sat down with our fintech contributor Gregg Schoenberg and I (check out the full meat of the conversation on Extra Crunch).

The tie between cleantech startups and fintech investors may seem tenuous at first thought. However, financial services have long played a significant role in the energy sector and is now becoming a more common end customer for energy startups focused on operations, management and analytics platforms, thus creating real opportunity for fintech investors to offer differentiated value.

Though the conversation around energy resources and decarbonization often focuses on politics, a significant portion of decisions made in the energy generation business is driven by pure economics — is it cheaper to run X resource relative to resources Y and Z at a given point in time? Based on bid prices for request for proposals (RFPs) in a specific market and the cost-competitiveness of certain resources, will a developer be able to hit their targeted rate of return if they build, buy or operate a certain type of generation asset?

Alternative generation sources like wind, solid oxide fuel cells or large-scale or even rooftop solar have reached more competitive cost levels — in many parts of the U.S., wind and solar are in fact often the cheapest form of generation for power providers to run.

Thus as renewable resources have grown more cost competitive, more infrastructure developers and other new entrants have been emptying their wallets to buy up or build renewable assets like large-scale solar or wind farms, with the American Council on Renewable Energy even forecasting cumulative private investment in renewable energy possibly reaching up to $1 trillion in the U.S. by 2030.

A major and swelling set of renewable energy sources are now led by financial types looking for tools and platforms to better understand the operating and financial performance of their assets, in order to better maximize their return profile in an increasingly competitive marketplace.

Therefore, fintech-focused venture firms with financial service pedigrees, like Anthemis, now find themselves in pole position when it comes to understanding cleantech startup customers, how they make purchase decisions, and what they’re looking for in a product.

In certain cases, fintech firms can even offer significant insight into shaping the efficacy of a product offering. For example, Anthemis portfolio company kWh Analytics provides a risk management and analytics platform for solar investors and operators that helps break down production, financial analysis and portfolio performance.

For platforms like kWh analytics, fintech-focused firms can better understand the value proposition offered and help platforms understand how their technology can mechanically influence rates of return or otherwise.

The financial service customers for clean energy-related platforms extends past just private equity firms. Platforms have been and are being built around energy trading, renewable energy financing (think financing for rooftop solar) or the surrounding insurance market for assets.

When speaking with several of Anthemis’ cleantech portfolio companies, founders emphasized the value of having a fintech investor on board that not only knows the customer in these cases, but that also has a deep understanding of the broader financial ecosystem that surrounds energy assets.

Founders and firms seem to be realizing that various arms of financial services are playing growing roles when it comes to the development and access to clean energy resources.

By offering platforms and surrounding infrastructure that can improve the ease of operations for the growing number of finance-driven operators or can improve the actual financial performance of energy resources, companies can influence the fight for environmental sustainability by accelerating the development and adoption of cleaner resources.

Ultimately, a massive number of energy decisions are made by financial services firms and fintech firms may often know the customers and products of downstream cleantech startups more than most. And while the financial services sector has often been labeled as dirty by some, the vital role it can play in the future of sustainable energy offers the industry a real chance to clean up its image.

Powered by WPeMatico

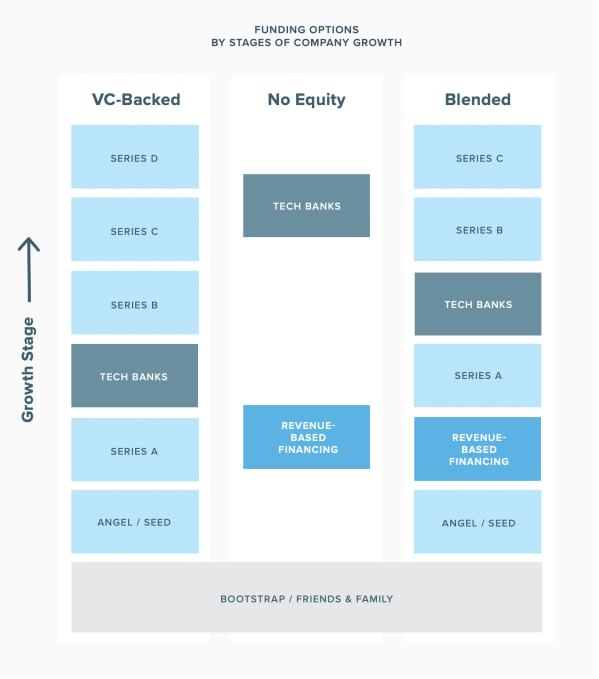

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Innowatts, an automated toolkit for energy monitoring and management targeting utilities, has raised $18.2 million in a new round of funding from investors led by Energy Impact Partners .

Previous investors Shell Ventures, Iberdrola and Energy and Environment Investment participated along with another new investor, Evergy Ventures.

As utilities respond to new, renewable power coming online and adapt to the challenges presented by natural disasters and intermittent energy sources stressing old power grid assets, they are increasingly turning to new software toolkits to adapt.

Innowatts and its software fit squarely into that category of offering.

“Competing in today’s complex and evolving marketplace requires utility companies use data and intelligence to drive business and customer value,” said Siddhartha Sachdeva, founder and chief executive of Innowatts, in a statement.

The company’s technology is used to analyze meter data from 21 million customers globally in 13 regional energy markets.

Innowatts boasts that it’s the largest body of customer intelligence data consumed by a software company. How that data will be used is an open question.

“We invest in companies driving the transformation of the energy sector towards an increasingly decarbonized, digitized, and electrified future – solutions that our utility partners can commercialize at scale and have the greatest impact,” said Michael Donnelly, partner and chief risk officer at EIP, in a statement. “Innowatts is poised to become a key building block in the software-driven, intelligent grid of the future, and we look forward to working closely with them alongside our utility partners.”

The company uses the data it collects to predict the potential for outages or problems created by surges in energy demand so that utilities can dispatch resources to meet that demand without sacrificing reliability for customers.

“Utilities have the opportunity to deliver more value to customers, at lower costs and with greater personalization than ever before, while helping streamline the complex energy marketplace,” said Geert van de Wouw, vice president of Shell Ventures.

Powered by WPeMatico

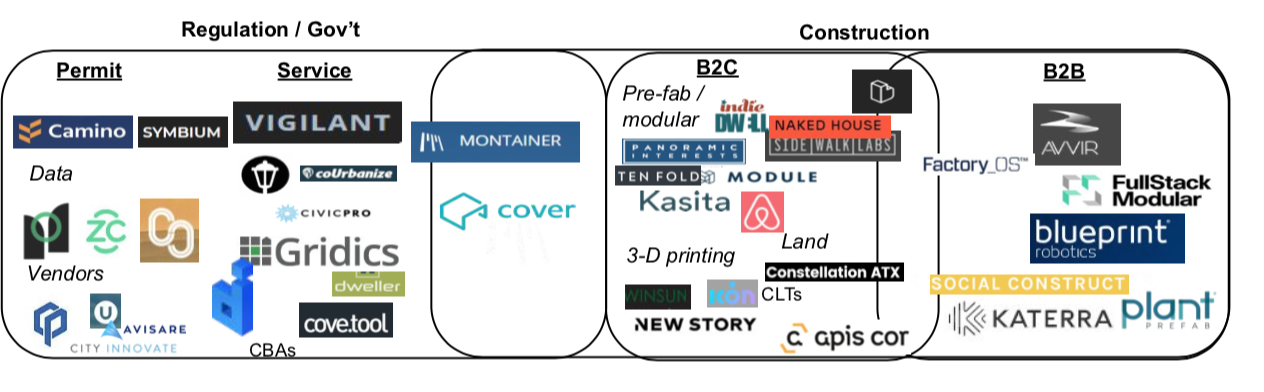

In this section of my exploration into innovation in inclusive housing, I am digging into the 200+ companies impacting the key phases of developing and managing housing.

Innovations have reduced costs in the most expensive phases of the housing development and management process. I explore innovations in each of these phases, including construction, land, regulatory, financing, and operational costs.

This is one of the top three challenges developers face, exacerbated by rising building material costs and labor shortages.

Powered by WPeMatico

Even as its solar business declined in step with its overall earnings, Tesla is bullish on the prospects for the energy side of its business over the course of the year.

The energy business is an unheralded part of Tesla — overshadowed by its headline-grabbing (and much larger) auto exploits — that chief executive Elon Musk thinks will generate an increasing share of revenue for the company over time.

Revenues from its solar power and energy storage business fell by 13 percent from the fourth quarter 2018 and 21 percent from a year ago period, down to $324.7 million from $371.5 million in the fourth quarter of 2018 and $410 million in the year ago quarter.

Solar energy deployments fell from 73 megawatts to 47 megawatts from the fourth to the first quarter, the company said. Those figures were offset by a slight increase in solar deployments.

The company actually introduced a new financing and purchasing model for solar installations in the second quarter — saying in its shareholder letter that residential solar customers can buy directly from the Tesla website, in standardized capacity increments.

“We aim to put customers in a position of cash generation after deployment with only a $99 deposit upfront. That way, there should be no reason for anyone not to have solar generation on their roof,” Musk and chief financial officer Zachary Kirkhorn wrote in the shareholder letter.

Tesla’s battery storage business was hit as the company shifted units from energy storage to installation in its own vehicles.

“Energy storage production in the second half of 2018 was limited by cell production as we routed all available Gigafactory 1 cell capacity to supply Model 3,” the company wrote in its letter. “Some Gigafactory 1 cell production has been routed back to the energy storage business, enabling us to increase production in Q1 by roughly 30% compared to the previous quarter.”

And Musk thinks that the energy business will grow significantly over the course of the year. “We hope that growth rate will continue and battery storage will become a bigger and bigger percentage over time,” Musk said on an analyst call following the earnings release. Potentially, Tesla thinks its energy business could grow by as much as 300 percent, Musk said.

Powered by WPeMatico

In the nine years since private equity and venture capital investments into sustainable technologies last crossed the $6 billion threshold, the problems caused by global carbon emissions have only intensified.

Now, as the world confronts the reality that there’s not much time left to reverse course on carbon emissions and the impact they will have on life on earth, both corporate and private investors are once again stepping up their commitments to startups in the space.

In 2018, global venture capital investment into startups focused on sustainability jumped 127 percent, to $9.2 billion, the highest since 2010, according to a January report from Bloomberg New Energy Finance. Powering that boost was a $1.1 billion investment in the smart window maker, View, and another $795 million for Chinese electric vehicle firm Youxia Motors. In fact, there were no fewer than eight VC/PE financings of Chinese EV specialist companies in 2018, totaling some $3.3 billion.

That stark assessment is coming from more corners of the scientific community, and the reality of the danger is being emphasized by politicians and concerned citizens around the globe.

The simple truth is that things are getting worse. And for the past two years, emissions have been increasing as countries continue to use oil and gas and coal to fuel economic growth, even as the global community realizes that carbon emissions are an increasing threat.

A recent assessment by the U.S. government put the cost of climate change caused by carbon emissions at $500 billion annually by the end of the century. And the financial toll doesn’t begin to assess the cost to the quality of human life and the potential lives that will be lost because of climate-related disasters.

This isn’t the first time the world has realized the threat climate change poses. It’s not even the second. Back in 1979 — and throughout the next decade — the U.S. grappled with how to craft an appropriate response to the coming climate-related crisis. Perhaps unsurprisingly, the government failed, and the issue of imminent climate disaster was set aside.

Former Vice President Al Gore picked up the thread in the mid-2000s in the wake of his defeat to the Connecticut Yankee turned Texas oilman George W. Bush in the contested 2000 presidential election. Through advocacy work and the popular climate-focused documentary “An Inconvenient Truth,” Gore was able to proselytize among a group of technocrats looking for the next big thing in the wake of the internet explosion that had transformed professional and personal lives.

Venture capital investors flocked to invest in renewable technologies — from biofuels to new solar energy generating technologies to new battery chemistries and beyond.

Over the next seven years billion-dollar companies would rise and fall on the back of speculative investment in the promise of a cleaner energy future that would disrupt the oil industry and turn billionaires into multi-billionaires — all while saving the world.

It didn’t work out.

Problems with scaling technologies beyond a controlled laboratory setting; global economic pressures wrought by an explosion of manufacturing capacity in countries like China; and the hubris of investors who thought that their investment acumen in picking winners of the information age could work just as well in centuries-old industries like oil and gas, or electricity, found themselves floundering in complicated, regulated markets with deep-pocketed incumbents and entrenched interests in promoting the status quo.

In the process, investors lost hundreds of millions of dollars in the U.S. alone, and destabilized some of the oldest firms in the investment industry.

Now, companies and investors are returning to the market in a major way. Some of the largest businesses in the food and agriculture industry are investing in new companies that are developing protein replacements and novel cultivation technologies; utilities are investing more heavily in smart grid technologies as electrification and microgrids become more real; automakers and battery manufacturers are backing new energy storage technologies; and frontier investors are backing companies tackling everything from biologically based chemical manufacturing to new construction technologies for smart homes and cities, to new kinds of nuclear power that could transform how the world conceives of energy abundance (along with geo-engineering tech to remove carbon from the atmosphere).

“In the last few years, the number of technologies ripe for investment has expanded dramatically,” Ravi Manghani, research director for energy storage at Wood Mackenzie, an energy research and consultancy firm, told CNBC in March. “It’s no longer just three or four technology verticals.”

While none of these technological advancements are a guaranteed solution to the threats carbon emissions pose, or are surefire commercially viable businesses, the fact that investors are once again looking at sustainability as a viable investment thesis — capable of producing multiple billion-dollar businesses — is a good step forward.

Any plan to address decarbonization has to confront industries as diverse as agriculture, construction, transportation, chemicals and consumer goods from clothes to chemicals.

Failure to confront these challenges would be catastrophic. Even if global warming is restricted to just the 2 degree Celsius target set at the Paris climate agreement, that could mean the extinction of the world’s tropical reefs and several meters of sea-level rise, as The New York Times reported last August. Already the impacts of climate change have meant tens of billions of dollars in damage for the U.S. in 2018 alone.

“The era of incrementalism on climate change is over,” said Massachusetts Senator Ed Markey, one of the architects of the “Green New Deal” legislation, in an interview with Vox. “We are now in the era of the Green New Deal. It’s not going away. It is creating an incentive for governors to do more, for mayors to do more, for companies to do more. The polling says it has political legs that will drive it right into the election of 2020, and when that cycle is done, I think we’re going to see a much greater capacity for us to take the kind of action that we need.”

Powered by WPeMatico

How much does transportation cost you?

In most cities, bus or subway fare might set you back $3 or so. A tank of gas, maybe $30 or $40 depending on your car. An hour of street parking? Sometimes it’s free, sometimes it’s a few bucks. And you can usually snag an economy seat on a round-trip U.S. domestic flight for less than $300.

These numbers probably ring true for most people. There’s just one problem: Everything you know about the cost of transportation is wrong.

Despite a massive infusion of venture capital into the transportation sector over the past few years, mobility startups are starting to learn what every transportation business has known for generations: transportation profits are elusive, and the system is mainly held together by subsidies. Will this be the first generation of transportation businesses to escape history?

Powered by WPeMatico

We profiled HyperSciences in February, when the team had just successfully completed a launch milestone for a small business grant with NASA. The last time we checked in, the hypersonic drilling company had raised about $5 million as part of an untraditional Reg A offering. By the end of March, HyperSciences rounded out its first major round with $9.6 million from 3,552 individual investors on SeedInvest in the equity crowdfunding platform’s second largest raise to date.

The heart of HyperSciences’ work is its hypersonic propulsion system that can fire a projectile at five times the speed of sound. At its most simplistic, HyperSciences’ hypersonic engine can fire upward to power suborbital space launches (HyperDrone) and point downward to penetrate deep pockets of geothermal energy, for example (HyperDrill).

Rather than going the normal venture capital route, HyperSciences decided to raise from regular people who believed in its vision. The way the company sees it, traditional VC would have likely forced HyperSciences to narrow its mission.

“Reg A lets everyone who cares about our planned hypersonic future vote with their checkbook,” HyperSciences founder and CEO Mark Russell told TechCrunch. “I think that’s important.” Russell comes from a family-run mining business and is no stranger to the challenges of a public company.

“I’ve learned a lot from running ops in the back offices,” Russell said. “Based on our public company experiences, we do like that the SEC Reg A process has a clear path to taking your company to the public markets as the next step in the process.”

With infusions of $125,000 from NASA’s Small Business Innovation Research grant and $1 million from Shell’s Global’s GameChanger program, HyperSciences is happy to bounce between research grants with a boost from the Reg A’s special form of “mini-IPO” in order to maintain its autonomy for the time being.

Russell explained that the Reg A’s intensive SEC process requires a fair level of maturity from a company — and enough capital to jump through all the hoops. “You’re not typically a seller of t-shirts in Reg A crowd financing,” Russell said.

HyperSciences’ next milestone will come in May when the company will demo its drilling tech in a field test for Shell. The company plans to leverage its new funding for additional future field testing, pushing its existing business plan forward and moving toward sustainability.

“Our investors are more like smart ‘crowd VCs.’ They’re generally are pretty savvy and see that we went through a stringent process to get here,” Russell said. “We’ve provided them with enough information to make a great decision.”

Powered by WPeMatico