EC News Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

The first quarter of 2021 was a busy season for technology exits. Coming off a hot period in the final quarter of 2020, it was no surprise that tech upstarts pursued liquidity through a variety of mechanisms as the new year began.

There were IPOs, there were direct listings, there were PE deals. Hell, we even saw enough SPACs that we lost track of a few; amid all the noise, you’ll miss the occasional note no matter how well-tuned your ear.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Each path is still open for later-stage startups to pursue exits: The IPO market was welcoming until a few minutes ago and private equity firms are stacked with cash and willing to pay higher multiples than they might in more normal times. And there are sufficient SPACs to take the entire recent Y Combinator class public.

Choosing which option is best from a buffet’s worth of possibilities is an interesting task for startup CEOs and their boards.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

Latch, in contrast, decided that a SPAC was its best route out the gate. The Exchange caught up with the company’s CFO, Garth Mitchell, about the transaction and why it made sense for his company.

And, finally, The Exchange spoke with AlertMedia’s founder and CEO, Brian Cruver, about his decision to sell his Texas-based company to a private equity firm.

To prevent this post from reaching an astronomic word count, we’ll give a brief overview of each deal and then summarize the company’s views about why their liquidity choice was the right one.

Kicking off with DigitalOcean, a few notes: First, the company has been pretty darn public about its growth in the last few years. We knew that it had an annualized run rate of around $200 million in 2018, $250 million in 2019 and around $300 million in the first half of 2020. It later announced that it hit that mark in May of last year.

So when DigitalOcean decided to go public, we weren’t bowled over. The company wound up pricing at $47 per share, the high end of its range. Since then, its stock has struggled somewhat, falling below $37 per share before recovering to $43.80 at the end of trading yesterday.

Enough of all that. Why did the company choose to go public via a traditional IPO? Spruill said his company looked at SPAC deals and direct listings. It selected the IPO route because it fit the company’s goals of generating a broad base of shareholders while creating a branding opportunity.

The cost of an IPO is comparable, he added, to other exit options. Spruill also praised the IPO process itself, noting that its rigorous requirements made DigitalOcean a better company.

Earlier in our chat, I asked Spruill a question that I put to every CEO on IPO day: How are you feeling? It’s a bit of a sop, but it sometimes elicits insights from executives and founders who, after weeks of discussing their companies’ inner workings, are asked a rare personal question.

Spruill said he felt incredible and that nothing could replicate an IPO as the culmination of so much work put into building a company and its team. If you add up the wins and losses over time, with more of the former than the latter, and can cross the finish line with the right metrics and market, you can earn a spot to be “grilled” by the “best investors,” he said.

Those investors put $750 million or so into his company, Spruill added. Funds that it can use to retire debt and free up more cash flow. Not a bad day, I’d say.

Powered by WPeMatico

The Exchange just yesterday discussed a downward revision in the impending Compass IPO and the disappointing Deliveroo flotation as signals that market demand for high-growth, unprofitable tech shares could be slipping. Recent news underscores the possibly chilling conditions. This morning, Kaltura, a technology company that provides video streaming software and services, delayed its IPO. JioForMe reports that the postponement comes after Kaltura’s “valuation demand was lower than expected.”

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

TechCrunch noted yesterday that Kaltura had not released a second, higher IPO price range. The fact stood out given how hot the public markets had proven in recent months for new tech offerings. Kaltura’s S-1 filing detailed accelerating revenue growth, which at the time we thought would be more than enough to fetch the company an attractive initial public valuation.

It appears that Kaltura was also surprised that it was not trending toward a higher IPO price.

In another sign of how quickly the temperature for new tech flotations may have chilled, digital comms firm Intermedia Cloud Communications also delayed its IPO today. In a release, CEO Michael Gold said the decision is due “to challenging current conditions in the market for initial public offerings, especially for technology companies.”

In another sign of how quickly the temperature for new tech flotations may have chilled, digital comms firm Intermedia Cloud Communications also delayed its IPO today. In a release, CEO Michael Gold said the decision is due “to challenging current conditions in the market for initial public offerings, especially for technology companies.”

Challenging current conditions? For IPOs? For tech IPOs? That’s new.

Axios reporter Dan Primack noted this morning that SPAC formation appears to be slowing. Mix that into the delays and yesterday’s anemic-to-awful IPO news, and the market could be seeing a somewhat rapid retrenchment toward more historical valuations and demand levels for unprofitable equities.

Thinking out loud: We should expect SPAC formation and deal volume to fall the fastest of all the signals we’re tracking, including IPO pricing, the pace of S-1 filings and first-day trading performance. Why? Because it’s the most exotic of the various data points we’ve observed on the way up during the tech boom. Therefore, it should also be the thing most vulnerable to rising financial gravity.

Powered by WPeMatico

Substack didn’t invent the paid newsletter, but the startup’s early success with the model is enticing previous backers to more than double down on the media startup.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Last evening, Axios reported that Substack is “raising $65 million in new venture capital” at a valuation of “around $650 million.” As you’ve already guessed, Axios goes on to report that Andreessen Horowitz (a16z) will likely lead the investment.

That we’re seeing a16z pour more capital into what we could call the alt-media space is not a surprise. The investing group is ladling even more cash into its in-house media efforts and has put a small archipelago of capital into audio-based social media app Clubhouse. Its internal publishing schedule is in part an attempt to get around traditional media; the Clubhouse universe is an inverted one in which tech investors are celebrities, producers and gatekeepers. And Substack is a place where publications have bled some well-known talent, shifting the center of gravity in media.

You can detect the theme.

You can detect the theme.

Regardless, Substack’s new valuation and investment are eye-catching. This morning, I want to collect all that we can regarding Substack’s historical growth so that we can chew on its new valuation from the best vantage point. Let’s go!

A little history to kick us off. Crunchbase counts Substack’s total funding to date at $17.4 million. PitchBook puts the number at $21.21 million, inclusive of debt. Both sources agree that the company’s most recent round came in July 2019. PitchBook pegs the company’s valuation at $48.65 million at that date.

Raising $17 million in cash around 20 months ago, regardless of debt, is an amount of capital that the company could easily have burned through by now. Raising more funds is therefore not a surprise.

But the size of the new round is notable, as is its constituent valuation. Series A and B rounds have been growing in size in recent years. But a $65 million Series B would stand out, even by 2021 standards. Not shockingly so, but enough that any company raising that sum at its implied level of maturity would demand our attention. That we’re all familiar with Substack only makes the sum more curious.

Powered by WPeMatico

All successful companies start off as a great idea, scribbled on the back of a cocktail napkin during a late-night meeting of the minds or gleaned from a fleeting inspiration that leaves you with a feeling of “I could do that better.”

For most, that’s as far as entrepreneurship ever goes, because, unfortunately, a great idea can’t raise money, develop a product or disrupt an industry.

It’s only an idea.

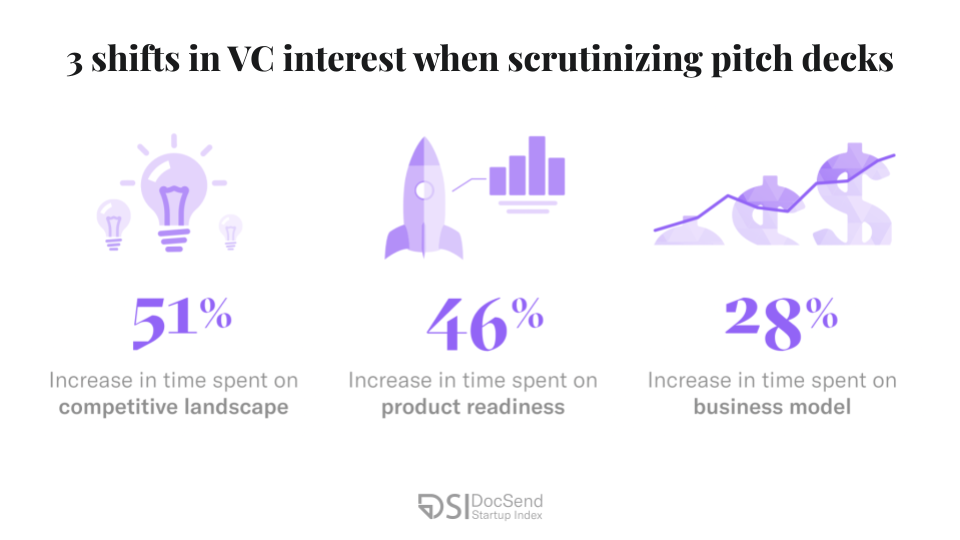

Investors’ heightened expectations for monetization potential and a company’s positioning within its competitive landscape are unlikely to lessen in the years to come, even in a post-COVID economy.

New data from the DocSend Startup Index show that for early-stage fundraising, particularly in the pre-seed round, founders need to approach VCs with much more than a great idea to secure funding. Our newest report on the state of pre-seed fundraising shows that investors became laser-focused on sections of the pitch deck that address monetization and business viability — signs that founders need to come to the table with better-defined businesses in order to succeed.

According to the data, overall founder and VC activity took a nosedive in early 2020 once the serious nature of the pandemic became apparent. But as the year progressed and investors adjusted to the new market conditions and remote dealmaking, overall activity quickly surpassed pre-pandemic levels.

Despite this flurry of activity and an unprecedented appetite for new startup pitches, investors made it very clear that strong positioning in three sections of the pitch deck was nonnegotiable.

Image Credits: DocSend(opens in a new window)

Powered by WPeMatico

It’s demo day for the current Y Combinator class, so we’ll have a largely early-stage focus at TechCrunch today. But there’s also a host of late- and super-late-stage news this morning that matters.

Let’s get to all of it before we start to talk accelerators, overheated pre-seed valuations and the like.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There are three things to discuss. First, the possible $10 billion exit of Discord to Microsoft. Discord is a well-financed unicorn that has raised oodles of capital and reportedly sports rapidly expanding revenues. Our goal will be to vet whether the price tag in question makes any sense, or if it is too low.

Second: Real estate tech company Compass has set an IPO price range we need to explore. Is its resulting valuation strong? Does it line up with its recent financial performance?

And, third, Intermedia Cloud Communications has priced its IPO. We’re behind on this entire debut, so we’ll take a second to riff on what the company does and what it is worth.

It’s a lot. But if we don’t get through it all now, we’ll fall behind and feel silly later. Let’s get to work!

Microsoft might be getting good at community, which is an odd thing to say about the enterprise software and cloud computing giant. The company’s Xbox gaming ecosystem has survived the test of time, Github is doing fine under Microsoft’s auspices, and Minecraft seems unharmed by Redmond’s stewardship.

That means gamers, developers and kids are all content to hang with Satya Nadella and company. Adding Discord to the mix might give Microsoft even more tooling to augment its existing communities, or perhaps tie them more closely together. But that’s all product news, which isn’t our remit. Let’s talk numbers.

The New York Times reported that Discord has “held deal talks with Microsoft for a transaction that could top $10 billion.” That figure has been widely reported, so we’ll use it for our work.

With a possible valuation in hand, we need revenue numbers to figure out if the possible sale price makes any sense. Happily, we have somewhat fresh numbers: The Wall Street Journal reported earlier this month that Discord “generated $130 million in revenue [in 2020], up from nearly $45 million in 2019.”

Powered by WPeMatico

In a new S-1/A filing, Coursera set an initial IPO price range between $30 and $33 a share, signaling the market views its edtech business warmly ahead of its impending public offering.

Coursera will have 130,271,466 shares outstanding after its IPO, or 132,630,966 including its underwriters’ option. At $30 per share, the low end of the company’s IPO range and a share count inclusive of 2,359,500 shares reserved for its underwriting banks, the firm would be worth $3.98 billion. That number rises to $4.38 billion at $33 per share.

Coursera is being valued as a software company, likely a breathe-easy moment for still-private edtech companies, since the debut could be an industry bellwether.

This is a solid increase from Coursera’s last private-market valuation, which was around $2.4 billion when it raised a Series F round in October 2020.

For the bulls in the room, there’s a bigger valuation if you tinker with the numbers. In a fully diluted accounting, including in our calculation, shares that are issuable upon vested options and RSUs, Coursera’s share count rises to 166,006,474, or 168,365,974 if we count its underwriters’ option. At its most generous share count and highest projected price, Coursera’s valuation could reach $5.56 billion.

However, IPO-watching group Renaissance Capital comes to a smaller $5.1 billion figure for a midpoint-range, fully diluted valuation. That result excludes shares reserved for underwriters and equity currently present in vested RSUs.

Using the more modest $5.1 billion midpoint figure, Coursera would be worth around 17.5 times its 2020 revenue of $293.5 million. Using a run-rate figure calculated from the company’s Q4 2020 results, its multiple falls to just over 15x.

Coursera is therefore being valued as a software company, likely a breathe-easy moment for still-private edtech companies, since the debut could be an industry bellwether.

The valuation is also a vote of confidence that Coursera’s rising deficits are not even a valuation risk, let alone an existential threat to its business. In the four quarters of 2020, the edtech giant lost $14.3 million, $13.9 million, $11.9 million and $26.7 million, the final Q4 net loss being the largest among the time interval for which we have data.

From all appearances, investors are valuing Coursera on its growth, not its profitability — or lack thereof.

Helping push its losses higher are rising sales and marketing costs, something TechCrunch has written about in the past. In Q4 2019, for example, the company spent $16.7 million on sales and marketing activities. That figure rose to $35 million in Q4 2020.

Powered by WPeMatico

Earlier this year, 15 top U.S. universities joined forces to launch a one-stop shop where corporations and startups can discover and license patents.

Working in concert, Brown, Caltech, Columbia, Cornell, Harvard, the University of Illinois, Michigan, Northwestern, Penn, Princeton, SUNY Binghamton, UC Berkeley, UCLA, the University of Southern California and Yale formed The University Technology Licensing Program LLC (UTLP) to create a centralized pool of licensable IP.

The UTLP arrives as more higher education institutions are beefing up their investment in the entrepreneurial pipeline to help more students launch startups after graduation. In some instances, schools serve as accelerators, providing students with resources and helping them connect with VCs to find seed funding.

To get a better look at the new program and more insight into the university-to-startup pipeline, we spoke to:

Orin Herskowitz: The UTLP effort is really much more about licensing to the somewhat broken interface between universities and very large companies in the tech space when it comes to licensing intellectual property. But I know USC and Columbia and many of our peers, especially over the last three to seven years, have pivoted in a massive way to helping our faculty students fulfill their entrepreneurial dreams and launch startups around this exciting university technology.

Orin Herskowitz: Universities have traditionally been a source of amazing, life-saving and life-improving inventions, for decades. There’s been a ton of new drugs and medical devices, cybersecurity improvements, and search engines, like Google, that have come out of universities over the years, that were federally funded and developed in the labs, and then licensed to either a startup or the industry. And that’s been great. At least over the last couple of decades, that interface has worked really, really well in some fields, but less well in others. So, in the life sciences, in energy, in advanced materials, in those industries, a lot of the time, these innovations that end up having a huge impact on society are based really on one or two or three core eureka moments. There’s like one or two patents that underlie an enormous new cancer drug, for instance.

In the tech space though, it’s a very different dynamic because, a lot of the time, these inventions are incredibly important and they do launch a whole new generation of products and services, but the problem is that a new device, like an iPhone, or a piece of software, might rely on dozens or even hundreds of innovations from across many different universities, as opposed to just one or two.

Jennifer Dyer: We’ve all had this renewed focus on innovation within the university and really helping our students and faculty that want to start companies, launch those companies. If you look at the space, helping educate our students that launching a company in a high-tech space may mean that they have to go out and acquire 100 different licenses, so maybe it doesn’t make sense. We’re going to be doing nonexclusive licensing, and it doesn’t preclude anyone from moving forward with this technology. This is probably the first pool for nonstandard essential patents in the high-tech space, which makes it somewhat unique. Because if you look back, most of the pools have been around standard essential patents.

Powered by WPeMatico

When Amazon announced last week that founder and CEO Jeff Bezos planned to step back from overseeing operations and shift into an executive chairman role, it also revealed that AWS CEO Andy Jassy, head of the company’s profitable cloud division, would replace him.

As Bessemer partner Byron Deeter pointed out on Twitter, Jassy’s promotion was similar to Satya Nadella’s ascent at Microsoft: in 2014, he moved from executive VP in charge of Azure to the chief exec’s office. Similarly, Arvind Krishna, who was promoted to replace Ginni Rometti as IBM CEO last year, also was formerly head of the company’s cloud business.

Could Nadella’s successful rise serve as a blueprint for Amazon as it makes a similar transition? While there are major differences in the missions of these companies, it’s inevitable that we will compare these two executives based on their former jobs. It’s true that they have an awful lot in common, but there are some stark differences, too.

For starters, Jassy is taking over for someone who founded one of the world’s biggest corporations. Nadella replaced Steve Ballmer, who had taken over for the company’s face, Bill Gates. Holger Mueller, an analyst at Constellation Research, says this notable difference could have a huge impact for Jassy with his founder boss still looking over his shoulder.

“There’s a lot of similarity in the two situations, but Satya was a little removed from the founder Gates. Bezos will always hover and be there, whereas Gates (and Ballmer) had retired for good. [ … ] It was clear [they] would not be coming back. [ … ] For Jassy, the owner could [conceivably] come back anytime,” Mueller said.

But Andrew Bartels, an analyst at Forrester Research, says it’s not a coincidence that both leaders were plucked from the cloud divisions of their respective companies, even if it was seven years apart.

“In both cases, these hyperscale business units of Microsoft and Amazon were the fastest-growing and best-performing units of the companies. [ … ] In both cases, cloud infrastructure was seen as a platform on top of which and around which other cloud offerings could be developed,” Bartels said. The companies both believe that the leaders of these two growth engines were best suited to lead the company into the future.

Powered by WPeMatico

Last week, another container security startup came off the board when Rapid7 bought Alcide for $50 million. The purchase is part of a broader trend in which larger companies are buying up cloud-native security startups at a rapid clip. But why is there so much M&A action in this space now?

Palo Alto Networks was first to the punch, grabbing Twistlock for $410 million in May 2019. VMware struck a year later, snaring Octarine. Cisco followed with PortShift in October and Red Hat snagged StackRox last month before the Rapid7 response last week.

This is partly because many companies chose to become cloud-native more quickly during the pandemic. This has created a sharper focus on security, but it would be a mistake to attribute the acquisition wave strictly to COVID-19, as companies were shifting in this direction pre-pandemic.

It’s also important to note that security startups that cover a niche like container security often reach market saturation faster than companies with broader coverage because customers often want to consolidate on a single platform, rather than dealing with a fragmented set of vendors and figuring out how to make them all work together.

Containers provide a way to deliver software by breaking down a large application into discrete pieces known as microservices. These are packaged and delivered in containers. Kubernetes provides the orchestration layer, determining when to deliver the container and when to shut it down.

This level of automation presents a security challenge, making sure the containers are configured correctly and not vulnerable to hackers. With myriad switches this isn’t easy, and it’s made even more challenging by the ephemeral nature of the containers themselves.

Yoav Leitersdorf, managing partner at YL Ventures, an Israeli investment firm specializing in security startups, says these challenges are driving interest in container startups from large companies. “The acquisitions we are seeing now are filling gaps in the portfolio of security capabilities offered by the larger companies,” he said.

Powered by WPeMatico

Soon all tech news will be fintech news, all fintech news will be trading platform news and all trading platform news will concern the business mechanics of such services.

So, after looking into Robinhood’s fourth-quarter payment for order flow (PFOF) revenues this morning, we’re back with a related story. This time, however, we’re talking about Public.

Public, like Robinhood, is a zero-cost trading service. Its founders have worked to build a community-first platform, including offering ways to let groups chat about their investments.

And like Robinhood, Public has seen its growth skyrocket in recent days. Company representatives told TechCrunch today it was seeing “steady ~30%” month-over-month growth until Thursday, when “new user signups went up 20x.”

Both share strong backing from investors: Robinhood raised billions in new capital this week to ensure it has enough cash to meet clearinghouse deposit requirements. It managed to do so in part because its Q4 2020 numbers show that its PFOF business is ticking along nicely.

Public, flush with a recent $65 million Series C, took a different tack this morning and announced it would “stop participating in the practice of Payment for Order Flow.”

To which we say … all right.

On one level, this is neat. Public is not going to sell its order flow to market makers for fees. That’s good for users, but how will it make up the lost revenue? Tips, which will prove an interesting experiment in monetization.

TechCrunch asked the company if it believes tips will compensate for PFOF revenue, to which founders Leif Abraham and Jannick Malling replied via email that they were “optimistic that the difference will be offset by the optional tipping feature.”

However, dropping payment for order flow is only so brave a move from Public. After all, Public was not making Robinhood-level amounts of fetti from its PFOF business. Indeed, as we wrote when Public raised its Series C:

Before chatting with Public, I dug into its trading partner Apex’s filings to learn about its payment for order flow results from its recent filings. The resulting sums are somewhat modest for Apex’s collected clients. This means that Public’s revenue metrics, a portion of the aggregate sums, are even more unassuming.

Powered by WPeMatico