EC News Analysis

Auto Added by WPeMatico

Auto Added by WPeMatico

A stunning first quarter in venture capital funding was not restricted to the United States; Europe also had one hell of a start to the year.

According to data from Dealroom and Crunchbase News, an investor, and an analyst from PitchBook, European startups put together an impressive fundraising haul. The venture capital world kicked off its 2021 European investing cycle with enough activity to set the continent on the path that would crush yearly records.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Inside the data, there’s lots to unpack, including which sectors of European startups stood out in terms of capital raised, rising seed and late-stage deals, and dollar volume. We’ll also need to discuss exits — the Deliveroo IPO and its various woes was not the only transaction from the period worth understanding.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

As with our prior looks at AI startup fundraising and the United States’ own blistering start to the year, we’ll lean on multiple sources to ensure that we have a wide lens. And we’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

In this case, it makes the numbers all the more impressive. Let’s get into the data.

Dealroom was first out of the gate, reporting that European startups had a record quarter in Q1 2021 back when April just got started. Its preliminary results for the first quarter indicated that startups on the continent raised €16.6 billion, or $19.9 billion at today’s exchange rates.

That total was not only a record, but what Dealroom described as double the results of Q1 2020. While we’ve become slightly inured in recent months to the venture capital market’s rapid pace and capital-rich environment, it’s worth considering for a moment, as the first quarter of last year ended, how few of us would have guessed that just a year later — as COVID-19 still harms public health and disrupts life and business — we’d see numbers like this.

The Dealroom data, however, was not all records. Round volume by the group’s estimates was down from the year-ago period, if slightly better than the last few quarters. The general move toward the later-stage and larger-round venture capital market is alive and well in Europe.

Powered by WPeMatico

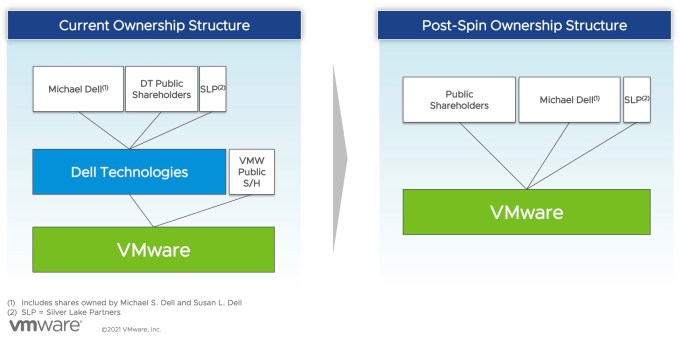

TechCrunch has spilled much digital ink tracking the fate of VMware since it was brought to Dell’s orbit thanks to the latter company’s epic purchase of EMC in 2016 for $58 billion. That transaction saddled the well-known Texas tech company with heavy debts. Because the deal left VMware a public company, albeit one controlled by Dell, how it might be used to pay down some of its parent company’s arrears was a constant question.

Dell made its move earlier this week, agreeing to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence, and in terms of Dell influence? Dell no longer will hold formal control over VMware as part of the deal, though its shareholders will retain a large stake in the virtualization giant. And with Michael Dell staying on VMware’s board, it will retain influence.

Here’s how VMware described it to shareholders in a presentation this week. The graphic shows that under the new agreement, VMware is no longer a subsidiary of Dell and will now be an independent company.

Image Credits: VMware

But with VMware tipped to become independent once again, it could become something of a takeover target. When Dell controlled VMware thanks to majority ownership, a hostile takeover felt out of the question. Now, VMware is a more possible target to the right company with the right offer — provided that the Dell spinout works as planned.

Buying VMware would be an expensive effort, however. It’s worth around $67 billion today. Presuming a large premium would be needed to take this particular technology chess piece off the competitive board, it could cost $100 billion or more to snag VMware from the public markets.

So VMware will soon be more free to pursue a transaction that might be favorable to its shareholders — which will still include every Dell shareholder, because they are receiving stock in VMware as part of its spinout — without worrying about its parent company simply saying no.

Powered by WPeMatico

When Dell announced it was spinning out VMware yesterday, the move itself wasn’t surprising; there had been public speculation for some time. But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

The dividend route, which involves a payment to shareholders between $11.5 billion and $12 billion, has the advantage of being tax-free (or at least that’s what Dell hopes as it petitions the IRS). For Dell, which owns 81% of VMware, the dividend translates to somewhere between $9.3 billion and $9.7 billion in cash, which the company plans to use to pay down a portion of the huge debt it still holds from its $58 billion EMC purchase in 2016.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

VMware was the crown jewel in that transaction, giving Dell an inroad to the cloud it had lacked prior to the deal. For context, VMware popularized the notion of the virtual machine, a concept that led to the development of cloud computing as we know it today. It has since expanded much more broadly beyond that, giving Dell a solid foothold in cloud native computing.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned. Dell CEO Michael Dell will remain chairman of the VMware board, which should help smooth the post-spinout relationship.

But could Dell have extracted more cash out of the deal?

Patrick Moorhead, principal analyst at Moor Insights and Strategies, says that beyond the cash transaction, the deal provides a way for the companies to continue working closely together with the least amount of disruption.

“In the end, this move is more about maximizing the Dell and VMware stock price [in a way that] doesn’t impact customers, ISVs or the channel. Wall Street wasn’t valuing the two companies together nearly as [strongly] as I believe it will as separate entities,” Moorhead said.

Powered by WPeMatico

Coinbase’s direct listing was a massive finance, startup and cryptocurrency event that impacted a host of public and private investors, early employees, and crypto-enthusiasts. Regardless of where one sits in the broader tech and venture world, Coinbase storming north of a $100 billion valuation during its first day of trading was the biggest startup happening of the year.

The transaction’s effects will be felt for some time in the public market, but also among the startups and capital that comprise the private market.

In the buildup to Coinbase’s flotation — and we’d argue especially after it released its blockbuster Q1 2021 results — there was a general expectation that the unicorn’s direct listing would provide a halo effect for other startups in the space. Anthemis’ Ruth Foxe Blader told The Exchange, for example, that “the Coinbase listing shows this great inflection point for crypto,” with another “wave” of startup work in the space coming up.

The widely held perspective raised two questions: Will the success of Coinbase’s direct listing bolster private investment in crypto-focused startups, and will that success help other areas of financially focused startup work garner more investor attention?

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Presuming that Coinbase’s listing will positively impact its niche and others around it is not a stretch. But to make sure we weren’t misreading sentiment, and to get deeper into the why of the concept, The Exchange reached out to venture capitalists who invest in the broader fintech world to get their take. We even roped in an analyst or two to round out our panel.

The answer is not a simple yes. There are several ways to approach investing in the cryptocurrency space — from buying coins themselves, to investing in mainstream-ish institutions like legal exchanges, to the more exotic, like supporting efforts on the forefront of the decentralized blockchain world. And while it is somewhat clear that most folks expect more capital to be available for crypto projects, it’s not clear where it may end up inside the market.

We’ll wrap by considering what impact Coinbase’s direct listing will have, if any, on non-crypto fintech venture capital investing.

We’ll wrap by considering what impact Coinbase’s direct listing will have, if any, on non-crypto fintech venture capital investing.

After yesterday’s examination of how blazingly hot the venture capital market looked in the first quarter, we’re again trying to gauge the private market’s temperature. Let’s talk to some folks on the ground and hear what they are seeing.

Coinbase’s direct listing floated a company that is worth more than all but two major blockchains, namely Ethereum and Bitcoin. Several other chains have aggregate coin values in the 11-figure range, but a 12-digit worth is still rare among crypto assets.

The scale of Coinbase’s valuation post-listing matters, according to Chainalysis Chief Economist Phillip Gradwell. Gradwell told The Exchange that “Coinbase’s $100 billion valuation today demonstrates that venture investors can make great returns from putting money into crypto companies, not just cryptocurrencies. That proof point is good for the entire ecosystem.”

More simply, it is now eminently reasonable to invest in the companies working in the crypto space instead of merely putting capital to work hard-buying coins themselves. The other way to consider the comment is to realize that Coinbase’s share price appreciation is steep enough since its 2012 founding to rival the returns of some coins over the same time frame.

Cleo Capital‘s Sarah Kunst expanded on the point, telling The Exchange in an email that “it’s now credible to say you’re a crypto startup and plan to IPO [versus] having acquisition or ICO be the only proven exit paths in the U.S.”

Powered by WPeMatico

It’s no surprise that the venture capital market was incredibly active in the United States during the first quarter of 2021, but precisely how strong has only recently become clear. This morning, we’re digging into the data.

According to a report from PitchBook, venture capitalists unleashed a wave of capital in the first three months of the year. So much, in fact, that funding in the United States nearly doubled compared to the same quarter of 2020.

We’ll dig into specific numbers and trends regarding aggregate venture capital results in a moment, but what stood out the most while digesting the Q1 dataset was how strong VC results appeared across different states; a solo late-stage boom the quarter was not.

Seed deal volume appeared strong and early-stage venture capital activity could reach new highs in 2021, but late-stage venture capital activity in the United States is already setting records in both deal count and invested dollars.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

We’ll parse the headline numbers and then dive into seed and super late-stage data with the help of Sarah Kunst of Cleo Capital, Jenny Lefcourt of Freestyle Capital, Iris Choi of Floodgate and Laela Sturdy of CapitalG.

With their help, we’ll contextualize the numbers and weave anecdotal observations into what the charts and graphs tell us. Especially in the case of seed data, which is famously laggy, added context is crucial. Let’s go!

According to PitchBook’s report, some 3,987 venture capital rounds were closed in the United States during Q1 2021. Those deals were worth $69 billion, a figure up nearly 93% from 2020’s first-quarter results.

In broad strokes, the United States had a crushing venture capital start to the new year, pandemic be damned. That is especially true when we consider 2020’s full-year figures. Last year, venture capitalists deployed some $166 billion into U.S.-based startups across 12,546 rounds. In contrast, if the first quarter’s pace was maintained during the rest of 2021, the United States would see around 16,000 rounds worth around $280 billion.

Of course, we cannot see the future, so those projections are merely shared to underscore how active the first quarter proved to be; we’ll have to wait for at least another quarter’s data to confidently predict full-year records for 2021.

Powering the rapid start to the venture capital year was a holistic boom: Seed deal volume is forecasted to have set a multiyear high, perhaps matching the historically strong Q2 2018 period. Early-stage venture capital during Q1 2021 was also robust, with $14.5 billion deployed across 1,170 rounds. Both numbers set a pace for fresh records in 2021.

Then there was late-stage dealmaking, which soared in the first quarter. In 2020, late-stage venture capital deals were worth $111.4 billion raised from 3,504 rounds. In the first quarter of 2021, some $51.9 billion was invested into late-stage startups across 1,291 deals.

Valuations and round sizes continued to rise across the board. If there was a better time to raise a big whack of venture capital as a U.S.-based startup, we cannot recall it. And the data seems to scream that the good times are now as good, or gooder, than ever.

Powered by WPeMatico

As expected, Southeast Asian superapp Grab is going public via a SPAC.

The combination, which TechCrunch discussed over the weekend, will value Grab on an equity basis at $39.6 billion and will provide around $4.5 billion in cash, $4 billion of which will come in the form of a private investment in public equity, or PIPE. Altimeter Capital is putting up $750 million in the PIPE — fitting, as Grab is merging with one of Altimeter’s SPACs.

Ride-sharing is a profitable business for Grab, though the segment did take a pandemic-induced whacking.

Grab, which provides ride-hailing, payments and food delivery, will trade under the ticker symbol “GRAB” on Nasdaq when the deal closes. The announcement comes a day after Uber told its investors it was seeing recovery in certain transactions, including ride-hailing and delivery.

Uber also told the investing public that it’s still on track to reach adjusted EBITDA profitability in Q4 2021. The American ride-hailing giant did a surprising amount of work clearing brush for the Grab deal. Extra Crunch examined Uber’s ramp toward profitability yesterday.

This morning, let’s talk through several key points from Grab’s SPAC investor deck. We’ll discuss growth, segment profitability, aggregate costs and COVID-19, among other factors. You can read along in the presentation here.

The impact on Grab’s operations from COVID-19 resembles what happened to Uber in that the company’s deliveries business had a stellar 2020, while its ride-hailing business did not.

From a high level, Grab’s gross merchandise volume (GMV) was essentially flat from 2019 to 2020, rising from $12.2 billion to $12.5 billion. However, the company did manage to greatly boost its adjusted net revenue over the same period, which rose from $1 billion to $1.6 billion.

Powered by WPeMatico

For those who follow the space, LG will be remembered fondly as a smartphone trailblazer. For a decade-and-a-half, the company was a major player in the Android category and a driving force behind a number of innovations that have since become standard.

Perhaps the most notable story is that of the LG Prada. Announced a month before the first iPhone, the device helped pioneer the touchscreen form factor that has come to define virtually every smartphone since. At the time, the company openly accused Apple of ripping off its design, noting, “We consider that Apple copycat Prada phone after the design was unveiled when it was presented in the iF Design Award and won the prize in September 2006.”

This July, the company will stop selling phones beyond what remains of its existing inventory.

LG has continued pushing envelopes — albeit to mixed effect. In the end, however, the company just couldn’t keep up. This week, the South Korean electronics giant announced it will be getting out of the “incredibly competitive” category, choosing instead to focus on its myriad other departments.

The news comes as little surprise following months of rumors that the company was actively looking for a buyer for the smartphone unit. In the end, it seems, none were forthcoming. This July, the company will stop selling phones beyond what remains of its existing inventory.

The smartphone category is, indeed, a competitive one. And frankly, LG’s numbers have pretty consistently fallen into the “Others” category of global smartphone market share figures ruled by names like Samsung, Apple, Huawei and Xiaomi. The other names clustered beneath the top five have been, more often than not, other Chinese manufacturers like Vivo.

Powered by WPeMatico

It appears that the slowdown in tech debuts is not a complete freeze; despite concerning news regarding the IPO pipeline, some deals are chugging ahead. This morning, we’re adding Alkami Technology to a list that includes Coinbase’s impending direct listing and Robinhood’s expected IPO.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We are playing catch-up, so let’s learn about Alkami and its software, dig into its backers and final private valuation, and pick apart its numbers before checking out its impending IPO valuation. After all, if Kaltura and others are going to hit the brakes, we must turn our attention to companies that are still putting the hammer down.

Frankly, we should have known about Alkami’s IPO sooner. One of a rising number of large tech companies based in nontraditional areas, the bank-focused software company is based in Texas, despite having roots in Oklahoma. The company raised $385.2 million during its life, per Crunchbase data. That sum includes a September 2020 round worth $140 million that valued the company at $1.44 billion on a post-money basis, PitchBook reports.

So, into the latest SEC filing from the software unicorn we go!

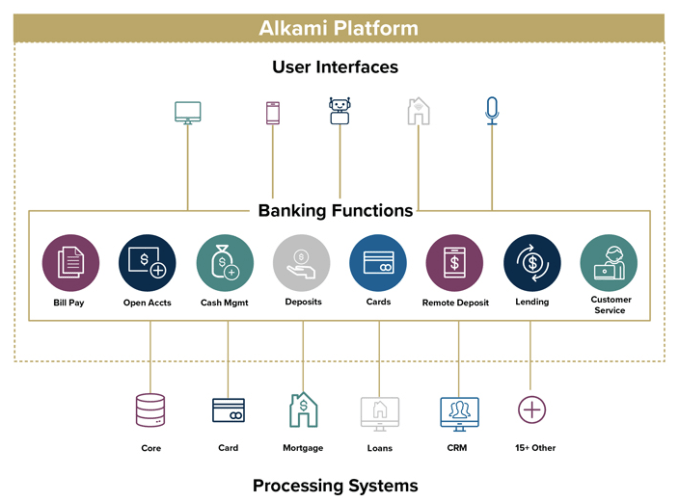

Alkami Technology is a software company that delivers its product to banks via the cloud, so it’s not a legacy player scraping together an IPO during boom times. Instead, it is the sort of company that we understand; it’s built on top of AWS and charges for its services on a recurring basis.

The company’s core market is all banks smaller than the largest, it appears, or what Alkami calls “community, regional and super-regional financial institutions.” Its service is a software layer that plugs into existing financial systems while also providing a number of user interface options.

In short, it takes a bank from its internal systems all the way to the end-user experience. Here’s how Alkami explained it in its S-1/A filing:

Image Credits: Alkami S-1

Simple enough!

Powered by WPeMatico

On a recent morning in downtown Shenzhen, Lingyu queued up to order her go-to McMuffin. As she waited in line with other commuters, the 50-year-old accountant noticed the new vegetarian options on the menu and decided to try the imitation spam and scrambled egg burger.

“I’ve never had fake meat,” she said of the burger — one of five new breakfast items that McDonald’s introduced last week in three major Chinese cities featuring luncheon meat substitutes produced by Green Monday.

Although some investors worry the sudden boom of meat-substitute startups could turn into a bubble, others believe the market is far from saturated.

Lingyu, who works in her family business in Shenzhen, is exactly the type of Chinese customer that imitation meat companies want to attract beyond the young, trendy, eco-conscious urbanites. Her yuan means potentially more to meat replacement companies because it advances their business and climate agendas both. Eating less meat is one of the simplest ways to reduce an individual’s carbon footprint and help fight climate change.

McDonald’s hopes that its pea- and soy-based, zero-cholesterol, luncheon meat substitutes will carve out a piece of China’s massive dining market. Longtime rival KFC, and local competitor Dicos introduced their own plant-based products last year. Partnering with fast food chains is a smart move for companies that want to promote alternative protein to the masses, because these products are often pricey and are usually aimed at wealthy urbanites.

2020 could well have been the dawn of alternative protein in China. More than 10 startups raised capital to make plant-based protein for a country with increasing meat demand. Of these, Starfield, Hey Maet, Vesta and Haofood have been around for about a year; ZhenMeat was founded three years ago; and the aforementioned Green Monday is a nine-year-old Hong Kong firm pushing into mainland China. The competition intensified further last year when American incumbents Beyond Meat and Eat Just entered China.

Although some investors worry the sudden boom of meat-substitute startups could turn into a bubble, others believe the market is far from saturated.

“Think about how much meat China consumes a year,” said an investor in a Chinese soy protein startup who requested anonymity. “Even if alternative protein replaces 0.01% of the consumption, it could be a market worth tens of billions of dollars.”

In many ways, China is the ideal testbed for alternative protein. The country has a long history of imitation meat rooted in Buddhist vegetarianism and an expanding middle class that is increasingly health-conscious and willing to experiment. The country also has a grip on the global supply chain for plant-based protein, which could give domestic startups an edge over foreign rivals.

“I believe, in five years, China will see a raft of domestic plant-based protein companies that could be on par with industry leaders from Europe and North America,” said Xie Zihan, who founded Vesta to develop soy-based meat suitable for Chinese cuisine.

Hey Maet’s imitation meat dumplings. Image Credits: Hey Maet

Lily Chen, a manager at the Chinese arm of alternative protein investor Lever VC, outlines three categories of meat analog companies in China: Western giants such as Beyond Meat and Eat Just; local players; and conglomerates such as Unilever and Nestlé that are developing vegan meat product lines as a defense strategy. Lever VC invested in Beyond Meat, Impossible Foods and Memphis Meats.

“They all have their product differentiation, but the industry is still very early stage,” said Chen.

Powered by WPeMatico

When UIPath filed its S-1 last week, it was a watershed moment for the robotic process automation (RPA) market. The company, which first appeared on our radar for a $30 million Series A in 2017, has so far raised an astonishing $2 billion while still private. In February, it was valued at $35 billion when it raised $750 million in its latest round.

RPA and process automation came to the fore during the pandemic as companies took steps to digitally transform. When employees couldn’t be in the same office together, it became crucial to cobble together more automated workflows that required fewer people in the loop.

RPA has enabled executives to provide a level of workflow automation that essentially buys them time to update systems to more modern approaches while reducing the large number of mundane manual tasks that are part of every industry’s workflow.

When UIPath raised money in 2017, RPA was not well known in enterprise software circles even though it had already been around for several years. The category was gaining in popularity by that point because it addressed automation in a legacy context. That meant companies with deep legacy technology — practically everyone not born in the cloud — could automate across older platforms without ripping and replacing, an expensive and risky undertaking that most CEOs would rather not take.

RPA has enabled executives to provide a level of workflow automation, a taste of the modern. It essentially buys them time to update systems to more modern approaches while reducing the large number of mundane manual tasks that are part of just about every industry’s workflow.

While some people point to RPA as job-elimination software, it also provides a way to liberate people from some of the most mind-numbing and mundane chores in the organization. The argument goes that this frees up employees for higher level tasks.

As an example, RPA could take advantage of older workflow technologies like OCR (optical character recognition) to read a number from a form, enter the data in a spreadsheet, generate an invoice, send it for printing and mailing, and generate a Slack message to the accounting department that the task has been completed.

We’re going to take a deep dive into RPA and the larger process automation space — explore the market size and dynamics, look at the key players and the biggest investors, and finally, try to chart out where this market might go in the future.

UIPath is clearly an RPA star with a significant market share lead of 27.1%, according to IDC. Automation Anywhere is in second place with 19.4%, and Blue Prism is third with 10.3%, based on data from IDC’s July 2020 report, the last time the firm reported on the market.

Two other players with significant market share worth mentioning are WorkFusion with 6.8%, and NTT with 5%.

Powered by WPeMatico