EC How To

Auto Added by WPeMatico

Auto Added by WPeMatico

Every company wants to be innovative, but innovation comes with its share of difficulties. One key challenge for early-stage companies that are disrupting a particular space or creating a new category is figuring out how to sell a unique product to customers who have never bought such a solution.

This is especially the case when a solution doesn’t have many reference points and its significance may not be obvious.

My view is simple — some buyers could use a walkthrough of the buying process. If you are building a singular product in a nascent market that necessitates forward-looking customers and want to drastically shorten sales cycles, I have a proposal: Create a buyer’s guide.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution. What does your product actually do? Is it secure? How would you implement the technology? What does it replace, if anything? It should be short, simple and speak the customer’s language. It also acts as a sales-enabling tool. Sales teams, especially at smaller startups, can review the guide quarterly and analyze what is and isn’t working as the company goes to market.

Here is how to put together a buyer’s guide, including what to sort out before you type a single word.

From the start, it’s important to think about who the stakeholders are for your product’s buying cycle. One typical issue with early-stage startups is they meet with an enthusiastic buyer — a CIO, CTO or VP of product — but neglect to include the other stakeholders who should be part of the conversation. More importantly, a lot of companies don’t realize the impact of their product on a group or team that they would not typically sell to.

For example, target the security team as an early stakeholder, because they’re probably going to review your product. If the solution is focused toward, say, integration, then hone in on who would be owning the integration process on the buyer’s team.

If you’re selling a martech solution, on a business level, you have to consider a finance business partner for marketing. Think about the problems your customers face and also how others in their company relate to them.

Powered by WPeMatico

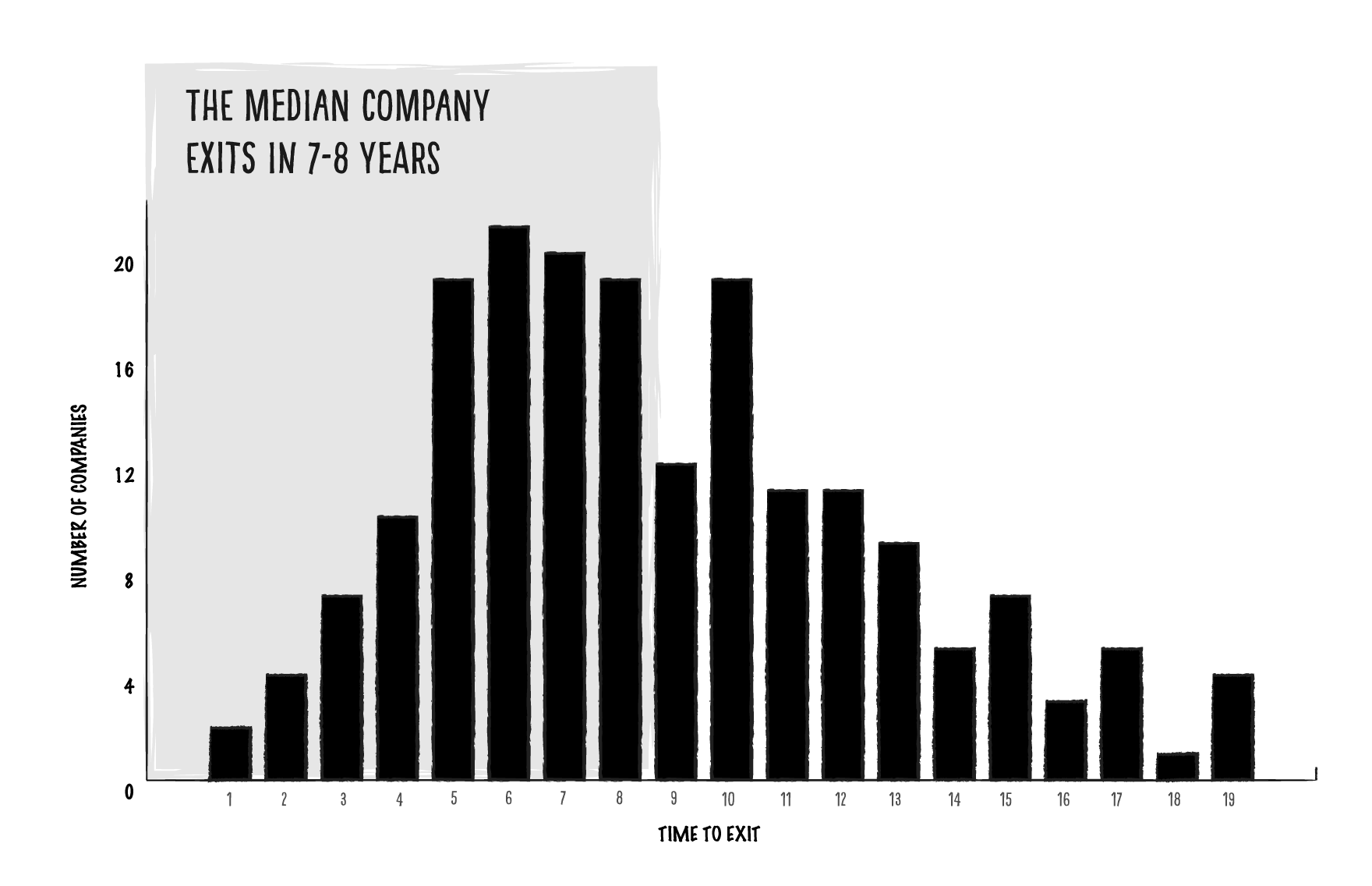

Does it really take an average of seven to eight years for a successful startup to exit? What can early-stage founders do to accelerate outcomes?

We wanted to know if founding teams can execute faster with a higher degree of success if they’re able to take advantage of relevant executive expertise. After all, that’s the thesis we built our venture model around — we purposefully designed M13 so that early-stage founders get access to experienced executives they wouldn’t otherwise have the money to hire or the time to vet, onboard and manage.

Even if companies are doing everything right, they still reduce time to exit when they have multiple founders with prior relevant experience as a senior leader or operator.

We looked at years of data from hundreds of successful startups. As it turns out, the impact of relevant executive expertise is even greater than we had anticipated — to the tune of doubling the rate of return on a venture investment.

When it comes to measuring leadership experience, information about an individual executive’s experience — for example, how long they’ve been an exec — is publicly available. Unfortunately, there isn’t readily available structured data around a founding team’s seniority and how early the founders bring on people with more experience as an operator or leader.

To find out if leadership experience significantly impacts startups’ success, we analyzed nearly 800 executives at more than 200 companies that reached a sizable exit (greater than or equal to a $500 million valuation) via an IPO on a U.S. exchange or an exit via M&A from 2004-2019. About 70% of the companies in our dataset exited between 2016-2019, including notable IPOs like Spotify, Zoom, Uber and Peloton. We decided to exclude companies in the biotech/life sciences space because these companies follow a different growth trajectory than consumer tech and B2B tech and traditionally exit via IPO or M&A at a much earlier stage.

Here’s what our analysis of startups with successful exits revealed.

While there are other intangible variables for startup success, the basic equation is the time and capital required to achieve an exit and the size of that exit.

Our dataset validates the widely accepted statement that successful exits take about seven to eight years:

Image Credits: M13

But could a variable like relevant leadership experience actually accelerate the time to exit? We wondered: Beyond time and capital, are there any factors — like experience as a leader or operator — that can have an exponential impact on the exit outcome? And when is the right time for those human capital resources to be introduced to make that impact?

Powered by WPeMatico

Whether you’re building a company or thinking about investing, it’s important to understand your strategic advantage. In order to determine one, you should ask fundamental questions like: What’s the long-term, sustainable reason that the company will stay in business?

The most important elements for founders to consider when figuring out their strategic advantage(s) include one-sided or “direct” network effects (e.g., with social media sites like Facebook), marketplace network effects (e.g., with two-sided marketplaces like Uber), data moats, first mover and switching costs.

Let’s take a quick look at an example of one-sided network effects. At the very earliest stages of Facebook’s existence, it was just Mark Zuckerberg, a few friends and their basic profiles. The nascent social media platform wasn’t useful beyond a few dorm rooms. They needed a strategic advantage or the company would not make it beyond the edge of campus.

A successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point.

In fact, Facebook only truly became a useful platform — and accelerated as a business — when more users came into the fold and more types of email addresses were accepted. Add to that the introduction of an ad marketplace revenue model and you have a clear strategic advantage — based on one-sided network effects — that gave Facebook a strategic edge over other early social media sites like MySpace.

These one-sided network effects are different from two-sided network effects.

Image Credits: Canvas Ventures

Two-sided network effects are most common in marketplace business models. In a two-sided network, supply and demand are matched, like Uber riders (demand) being matched with Uber drivers (supply). The Uber product is not necessarily more valuable just because more users (riders) join, the way Facebook is more valuable when more users join.

In fact, when more users (riders) join the demand side of the Uber network, it might actually be worse for the user experience — it’s harder to find a driver and wait times get longer. The demand side (riders) gets value from more supply (drivers) joining the platform and vice-versa. That’s why it’s called a two-sided network, or a marketplace.

Regardless of industry, a successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point. Copycats can range in size from startups with similar grit to large companies like Facebook or Google that have limitless resources to drive competition into the market, and potentially run the startup with the original idea out of business. This vulnerability can prove fatal unless a startup’s founding team explores and embraces one or more strategic advantages.

Powered by WPeMatico

There’s a lot of noise out there. The ability to effectively communicate can make or break your launch. It will play a role in determining who wins a new space — you or a competitor.

Most people get that. I get emails every week from companies coming out of stealth mode, wanting to make a splash. Or from a Series B company that’s been around for a while and hopes to improve their branding/messaging/positioning so that a new upstart doesn’t eat their lunch.

You have to stop thinking that what you are up to is interesting.

How do you make a splash? How do you stay relevant?

Worth noting is that my area of expertise is in the DevOps space and that slant may crop up occasionally. But these five specific tips should be applicable to virtually any startup.

This is especially important if you are a small startup that not many people know about. Journalists don’t want to hear opinions from your head of marketing or product — they want to hear from the founders. What problems are they solving? What unique opinions do they have about the market? These are insights that mean the most coming from the people that started the company. So if you don’t have at least one founder that can dedicate time to being the face, then PR is going to be an uphill battle.

That doesn’t mean there isn’t plenty to do to support these efforts. Create a list of all the journalists that have written about your competitors. Read those articles. How can your founder add value to these conversations? Where should you be contributing thought leadership? What are the most interesting perspectives you can offer to those audiences?

This is legwork and research you can do before looping founders into the conversation. Getting your PR going can be like trying to push a broken-down car up the road: If the founders see you exerting effort to get things moving on your own, they’re more likely to get beside you and help.

Here’s an example: It may be unreasonable to ask a founder to sit down and write a 1,000-word thought leadership piece by the end of the week, but they very likely have 20 minutes to chat, especially if you make it clear that the contents of the conversation will make for great thought leadership pieces, social media posts, etc.

The flow looks like:

Powered by WPeMatico

Search engine optimization, PR, paid marketing, emails, social — marketing and communications is crowded with techniques, channels, solutions and acronyms. It’s little wonder that many startups strapped for time and money find defining and executing a sustainable marketing campaign a daunting prospect.

The sheer number of options makes it difficult to determine an effective approach, and my view is that this complexity often obscures the obvious answer: A startup’s best marketing asset is its story. The knowledge and expertise of its team, together with the why and the how of its offering provides the most compelling content.

Leveraging this material with best practice techniques enables any startup, no matter how limited its budget, to run an effective marketing campaign.

Many startups make the mistake of choosing systems and employing procedures to solve the immediate needs of the department that requires them.

I know this approach works, because this is exactly what I did with my co-founder Alex Feiglstorfer when we set up Storyblok. To be clear, we are developers not marketers. However, our previous experience building CMS systems taught us that the main driver of organic engagement for most businesses was customer conversations around content.

Specifically, sharing experiences, expertise and what we learned. We had committed nearly all of our available cash to developing our product, so we knew that the only way to market Storyblok was to do it all ourselves.

As a result, we focused solely on problem-solving content. This took the form of tutorials on web development and opinion pieces on headless CMS and other topics within our areas of expertise. The trick was that what we published wasn’t made just for marketing, it was based on our own internal documentation of problems we encountered as we developed our product. In essence, we were “learning in public.” Through this approach we were able to acquire thousands of customers in our first year.

Retelling this story isn’t to blow my own trumpet, it’s to make clear that you don’t have to be a marketer by training or commit a huge amount of time and resources to successfully market your startup. So, how do you get started?

Although there’s no one-size-fits-all approach to how you organize your startup’s marketing function, there are some basic principles that apply in nearly every situation. A recent survey of 400+ executives from CMS Wire helpfully identified the following factors as the “top digital customer experience challenges” for businesses:

Challenges two to four are the pitfalls that we can focus on avoiding. They are directly related to how a startup produces, organizes and distributes its content.

With regard to the siloing of systems and fragmentation of customer data, the overriding goal is to ensure all your systems are integrated and speak to one another. In practice, this means that the data gathered in different departments — whether its feedback from sales, engagement on your website, customer service responses or product development information — is collected in a uniform and methodical manner and is readily accessible across the business.

Powered by WPeMatico

Domm Holland, co-founder and CEO of e-commerce startup Fast, appears to be living a founder’s dream.

His big idea came from a small moment in his real life. Holland watched as his wife’s grandmother tried to order groceries, but she had forgotten her password and wasn’t able to complete the transaction.

“I just remember thinking it was preposterous,” Holland said. “It defied belief that some arbitrary string of text was a blocker to commerce.”

So he built a prototype of a passwordless authentication system where users would fill out their information once and would never need to do so again. Within 24 hours, tens of thousands of people had used it.

Nothing beats building human networks. That’s the way that you’re going to get this done in terms of fundraising.

Shoppers weren’t the only ones on board with this idea. In less than two years, Holland has raised $124 million in three rounds of fundraising, bringing on partners like Index Ventures and Stripe.

Although the success of Fast’s one-click checkout product has been speedy, it hasn’t been effortless.

For one thing, Holland is Australian, which means he started out as a Silicon Valley outsider. When he arrived in the U.S. in the summer of 2019, he had exactly one Bay Area contact in his phone. He built his network from the ground up, a strategic process he credits to one thing: hard work.

On an episode of the “How I Raised It” podcast, Holland talks about how he built his network, why it’s important — not just for fundraising but for building the entire business — and how to avoid the mistakes he sees new founders make.

Holland’s primary strategy in building networks sounds like an obvious one — reach out to relevant people.

“When I first got to the States, I wanted to build networks,” Holland said, “but I didn’t really know anyone here in the Bay Area. So I spent a lot of time reaching out to relevant people — people working in payments, people working in technology, people working in identity authentication — just really relevant people in the space working in Big Tech who were building large-scale networks.”

One of the people Holland connected with was Allison Barr Allen, then the head of global product operations at Uber. Barr Allen managed her own angel investment fund, but Holland wasn’t actually looking for money when he reached out to her. He was much more interested in her perspective as the leader of an enormous financial services operation.

Powered by WPeMatico

There’s a disconnect between reality and the added value investors are promising entrepreneurs. Three in five founders who were promised added value by their VCs felt duped by their negative experience.

While this feels like a letdown by investors, in reality, it shows fault on both sides. Due diligence isn’t a one-way street, and founders must do their homework to make sure they’re not jumping into deals with VCs who are only paying lip service to their value-add.

Looking into an investor’s past, reputation and connections isn’t about finding the perfect VC, it’s about knowing what shaking certain hands will entail — and either being ready for it or walking away.

Entrepreneurs are increasingly demanding more than a blank check: They want mentorship, product understanding and emotional support, as well as industry connections and expertise. If VCs can’t bring that value, founders now have plenty of other funding routes to choose from, like crowdfunding, angel syndicates, tokenization and SPACs.

To stay competitive, VCs have to at least advertise that they have more than deep pockets. But what if it stops there? Founders have to know exactly what they’re looking for in a VC, which means looking past the front page and vetting their investors.

The ideal investor for modern startups is an operator VC — someone who was a founder or operator at a company before becoming an investor. But even then, ticking boxes isn’t enough to ensure the investor won’t come with their own challenges, like being too hands-on or less strategically minded.

Looking into an investor’s past, reputation and connections isn’t about finding the perfect VC, it’s about knowing what shaking certain hands will entail — and either being ready for it or walking away. There is no single solution to this issue, but here are my recommendations to founders seeking a successful investor relationship in 2021.

No founder-investor relationship can survive misalignment. Because you share responsibility on so many processes, both parties have to be on the same page. So before you even start fundraising, nail down the expectations you need your future investor to meet. What do you need the most? What does your dream investor look like?

Powered by WPeMatico

Last year was a record 12 months for venture-backed biotech and pharma companies, with deal activity rising to $28.5 billion from $17.8 billion in 2019. As vaccines roll out, drug development pipelines return to normal, and next-generation therapies continue to hold investor interest, 2021 is on pace to be another blockbuster year.

The median step up in valuations from seed to Series A is now 2x, higher than in all later rounds. As a result, biotech startups will continue to attract more investment at earlier stages from a larger, more diverse pool of venture capitalists.

This may also change the nature of biotech founders themselves: As a blog post from Y Combinator suggests, these founders are trending younger and perhaps less willing to cede control to VCs and hired executives than they might have in years past (i.e., via the “venture creation” model so predominant among early-stage biotech companies).

Founders are some of the most creative people out there, but legal documentation should be anything but.

As longtime members of the biotech startup community — as executives, entrepreneurs, advisors and legal counsel — we’ve seen our fair share of founder missteps early in the fundraising journey result in severe consequences.

In this exciting moment, when younger founders will likely receive more attention, capital and control than ever, it’s crucial to avoid certain pitfalls.

Founders are some of the most creative people out there, but legal documentation should be anything but. Keep it as simple and clear as possible. That means using National Venture Capital Corporation documents that everyone knows and understands, as well as keeping organized documentation for employee intellectual property (IP) assignment and NDAs, option grants, independent contractor agreements, tax documents and other key contracts and paperwork.

Powered by WPeMatico

The clock begins ticking on a startup the day the doors open. Regardless of a young company’s struggles or success, sooner or later the question of when, how or whether to sell the enterprise presents itself. It’s possibly the biggest question an entrepreneur will face.

For founders who self-funded (bootstrapped) their startup, a boardroom full of additional factors come into play. Some are the same as for investor-funded firms, but many are unique.

Put happiness at the center of the decision, and let your intuition — the instincts that made you the person you are today — be your guide.

After 18 years of bootstrapping a BI software firm into a business that now serves 28,000 companies and three million users in 75 countries, here’s what I’ve learned about myself, my company, about entrepreneurship and about when to grab for that brass ring.

Starting a software company 7,900 miles southwest of Silicon Valley requires some forethought and not a small amount of crazy. When we opened, it didn’t occur to us that one could have an idea and then go knock on someone’s door and ask for money.

Bootstrapping forced us to be a bit more creative about how we would go about building our company. In the early days, it was a distraction to growth, because we were doing other revenue-generating activities like consulting, development work, whatever we could find to keep ourselves afloat while we built Yellowfin. It meant we couldn’t be 100% focused on our idea.

However, it also meant we had to generate income from our new company from Day One — something funded companies don’t have to do. We never got into the mindset that it was okay to burn lots of cash and then cross our fingers and hope that it worked.

Powered by WPeMatico

Your clients might not demand 24/7 customer service yet, but they’re certainly hoping for it. But how can a startup with a lean staff provide round-the-clock customer care? There are several options available, but more than ever, outsourcing is one of them.

When should your startup consider outsourcing its customer care? And what should you look for in a provider? Here are some insights on what customer care as a service (CCaaS) can do for you, and how fast-growing startups have been leveraging this new class of partners to boost customer satisfaction.

Customer care as a service can address several pain points, such as the need to provide support outside of business hours.

If you find the right partner, outsourcing customer service can help you save time over options such as finding and managing your own freelancers, or hiring in-house, which might burden you with fixed costs.

Since online shoppers didn’t have to wait for stores to open during lockdowns, they have increasingly been making purchases on evenings and weekends, and often tend to abandon their carts if nobody is around to answer their doubts. New clients aside, existing customers also hope to get responses outside of typical business hours.

The COVID-19 crisis has significantly increased the share of e-commerce in total retail in recent months, and these new purchasing habits are likely to stick, the OECD pointed out in a report last year. This led many small retailers to discover a reality that e-commerce startups already know well: When you are an online business, working hours aren’t really a thing.

And it’s not just e-commerce — from SaaS to mobility services, there is a growing range of startups for which always-on customer service no longer a luxury. French CCaaS provider Onepilot learned this firsthand: During its beta program, its “support heroes” were available from 7 a.m. to 1 a.m., but it is now moving to 24/7 coverage due to greater demand from clients, co-founder Pierre Latscha told TechCrunch.

French micromobility startup Pony, one of Onepilot’s clients, needed reliable customer care for its dockless bike and scooter fleets in several cities, but couldn’t justify the expense of an in-house hire: “We didn’t have enough demand to have someone take care of customer service full time,” Pony explained to French newspaper Les Échos (translation ours).

In such situations, outsourcing to a partner like Onepilot can save costs when demand isn’t high enough or constant, which is often the case when the business is seasonal or growing faster than the startup can address it.

The latter was the case for SPRiNG, a French subscription service for eco-friendly laundry detergent and cleaning products that has partnered with Onepilot. The startup launched in the summer of 2020, and thanks to €2.1 million in seed funding, its team tripled, but with “tens of thousands of clients,” it soon felt the need for more support to handle the growing volume of requests, co-founder Ben Guerville told us via email.

Powered by WPeMatico