EC How To

Auto Added by WPeMatico

Auto Added by WPeMatico

One of the biggest factors in the success of a startup is its ability to quickly and confidently deliver software. As more consumers interact with businesses through a digital interface and more products embrace those interfaces as the opportunity to differentiate, speed and agility are paramount. It’s what makes or breaks a company.

As your startup grows, it’s important that your software delivery strategy evolves with you. Your software processes and tool choices will naturally change as you scale, but optimizing too early or letting them grow without a clear vision of where you’re going can cost you precious time and agility. I’ve seen how the right choices can pay huge dividends — and how the wrong choices can lead to time-consuming problems that could have been avoided.

The key to success is consistency. Create a standard, then apply it to all delivery pipelines.

As we know from Conway’s law, your software architecture and your organizational structure are deeply linked. It turns out that how you deliver is greatly impacted by both organizational structure and architecture. This is true at every stage of a startup but even more important in relation to how startups go through rapid growth. Software delivery on a team of two people is vastly different from software delivery on a team of 200.

Decisions you make at key growth inflection points can set you up for either turbocharged growth or mounting roadblocks.

The founding phase is the exciting exploratory phase. You have an idea and a few engineers.

The key during this phase is to keep the architecture and tooling as simple and flexible as possible. Building a company is all about execution, so get the tools you need to execute consistently and put the rest on hold.

One place you can invest without overdoing it is in continuous integration and continuous deployment (CI/CD). CI/CD enables developer teams to get feedback fast, learn from it, and deliver code changes quickly and reliably. While you’re trying to find product-market fit, learning fast is the name of the game. When systems start to become more complex, you’ll have the practices and tooling in place to handle them easily. By not having the ability to learn and adapt quickly, you give your competitors a massive edge.

One other place where early, simple investments really pay off is in operability. You want the simplest possible codebase: probably a monolith and a basic deploy. But if you don’t have some basic tools for observability, each user issue is going to take orders of magnitude longer than necessary to track down. That’s time you could be using to advance your feature set.

Your implementation here may be some placeholders with simple approaches. But those placeholders will force you to design effectively so that you can enhance later without massive rewrites.

At 10 to 20 engineers, you likely don’t have a person dedicated to developer efficiency or tooling. Company priorities are still shifting, and although it may feel cumbersome for your team to be working as a single team, keep at it. Look for more fluid ways of creating independent workstreams without concrete team definitions or deep specialization. Your team will benefit from having everyone responsible for creating tools, processes and code rather than relying on a single person. In the long run, it will help foster efficiency and productivity.

Powered by WPeMatico

Robotic process automation (RPA) is rapidly moving beyond the early adoption phase across verticals. Automating just basic workflow processes has resulted in such tremendous efficiency improvements and cost savings that businesses are adapting automation at scale and across the enterprise.

While there is a technical component to robotic automation, RPA is not a traditional IT-driven solution. It is, however, still important to align the business and IT processes around RPA. Adapting business automation for the enterprise should be approached as a business solution that happens to require some technical support.

A strong working relationship between the CFO and CIO will go a long way in getting IT behind, and in support of, the initiative rather than in front of it.

A strong working relationship between the CFO and CIO will go a long way in getting IT behind, and in support of, the initiative rather than in front of it.

More important to the success of a large-scale RPA initiative is support from senior business executives across all lines of business and at every step of the project, with clear communications and an advocacy plan all the way down to LOB managers and employees.

As we’ve seen in real-world examples, successful campaigns for deploying automation at scale require a systematic approach to developing a vision, gathering stakeholder and employee buy-in, identifying use cases, building a center of excellence (CoE) and establishing a governance model.

Your strategy should include defining measurable, strategic objectives. Identify strategic areas that benefit most from automation, such as the supply chain, call centers, AP or revenue cycle, and start with obvious areas where business sees delays due to manual workflow processes. Remember, the goal is not to replace employees; you’re aiming to speed up processes, reduce errors, increase efficiencies and let your employees focus on higher value tasks.

Powered by WPeMatico

“Who should my first marketing hire be?”

This is (by far) the most common question I’ve received since starting as Fuel’s CMO, and for good reason. Your first marketer will have an outsized impact on team dynamics as well as the overall strategic direction of the brand, product and company.

The nature of the marketing function has expanded significantly over the past two decades. So much so that when founders ask this question, it immediately prompts multiple new ones: Should I hire a brand or growth marketer? An offline or an online marketer? A scientific or a creative marketer?

Once upon a time, the number of marketing channels was fairly limited, which meant the function itself fit into a neater, tighter box. The number of ways to reach customers has since grown exponentially, as has the scope of the marketing role. Today’s startups require at least four broad functions under the umbrella of “marketing,” each with its own array of subfunctions.

The reality is that anyone who excels across all marketing functions is a unicorn and nearly impossible to find.

Here’s a sample of the marketing functions at a typical early-stage startup:

Brand marketing: Brand strategy, positioning, naming, messaging, visual identity, experiential, events, community.

Product marketing: UX copy, website, email marketing, customer research and segmentation, pricing.

Communications: PR and media relations, content marketing, social media, thought leadership, influencer.

Growth marketing: Direct response paid acquisition, funnel optimization, retention, lifecycle, engagement, reporting and attribution, word of mouth, referral, SEO, partnerships.

Have you worked with a talented individual or agency who helped you find and keep more users?

Respond to our survey and help us find the best startup growth marketers!

As you can imagine, that’s a lot for one person to manage, let alone be an expert in. What’s more, the skill set and experience required to excel in growth marketing is quite different from the skill set required to succeed in brand marketing. The reality is that anyone who excels across all marketing functions is a unicorn and nearly impossible to find.

Unless you’re lucky enough to nab that unicorn, your first hire should be a generalist who can tend to the full stack of the marketing function, learn what they don’t know, and roll up their sleeves to get things done. Someone smart, savvy and super scrappy who understands how to experiment across marketing channels until they find the right mix.

But this utility player should also bring deeper expertise in one of the big marketing functions: brand, product, communications or growth. Before making this key hire, you need to figure out which marketing priorities are most urgent and, consequently, which marketing “persona” is most appropriate for your business at the earliest stages.

To figure out which skill set you need most in-house, consider these five questions:

If you’ve done some marketing experimentation previously, have there been any bright spots? Which channels are proving the most efficient from a customer acquisition, conversion, retention, engagement, whatever your key KPI is, perspective? If you find a promising area, find a candidate that has expertise in it. For example, if you are seeing good results with Instagram ads, hiring a candidate who has expertise in growth marketing makes sense.

If you don’t have much data from channel testing, consider how your target customers are currently finding competitive products or services. At TaskRabbit, we knew from early customer research that clients were finding help with home services either through recommendations from friends or by asking Google (i.e., SEO and SEM).

So, that was a natural place for us to start. Our focus from a resource and staffing perspective in the early days was on growth marketing — driving more word of mouth, plus optimizing our SEO and SEM.

How competitive is the category you’re playing in? Are there dominant players with strong brands? Do these brands have endless marketing budgets? Are CACs exorbitant because well-capitalized competitors are outbidding each other? If so, you might want to focus on building an exceptional brand and product/customer experience.

That means disseminating a unique story through organic channels (word of mouth, PR, influencers and organic social media). A brand marketer or someone with deep PR and communications experience makes sense in this scenario.

Another aspect to consider is the skills the founder(s) — or other members of the founding/early team — bring to the table. If a founder has a strong vision for the brand and extensive experience building brands, then focus less on a brand marketing hire and rather supplement the branding skill set with another marketing priority (i.e., product marketing). Likewise, if a founder has a strong vision for the brand but no one on the team knows how to build one, that’s a skill gap that your first marketing hire should fill.

Trust building has become an increasingly important aspect for brands as customers become more and more discerning. But trust building tends to be more critical in certain areas than others: New, nascent industries or markets, sectors with a lot of human interaction (services businesses, dating platforms, etc.), industries that are fundamentally changing consumer behavior (ride-sharing in its earliest days), or industries where the stakes or cost is relatively high (luxury goods).

If trust building is critical, consider a branding expert who understands how to build trust and credibility, and build an experience that consumers are passionate about. This person will likely have deep expertise in PR and brand building, as these channels tend to inspire the most trust among consumers.

Once you’ve answered these five questions, you should have a pretty good idea of the type of marketing experience you want. But just how much experience should that person have? I typically recommend that seed-stage founders look for senior manager or director-level candidates at midsized companies.

At this experience level (six to 10 years), these candidates’ salaries tend to be more in line with a young company’s budget. Moreover, at this stage of their career, they tend to be both strategic and tactical. This means they can level up and think strategically about the business and the marketing function, but they are also happy to get their hands dirty and execute — actually dive into the Facebook platform and create ads, plan and host an event, or pitch a journalist.

Powered by WPeMatico

Running a startup can be a complicated, difficult process fraught with pitfalls and ample opportunities to make mistakes. But the logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

The logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

My company, Pulley, has helped more than a thousand founders build their cap table and equity structure.

Here’s a tactical guide to get your startup running in just four days.

It is now standard to incorporate your company at the seed stage itself. In the U.S., startups incorporate as Delaware C Corporations with 10 million authorized shares. This is the standard setup when you use services like Stripe Atlas or Clerky.

Post incorporation, you need to answer a few questions on how to grant equity to founders and future employees.

First, you should determine how you want to split the equity between the founders. There is no standard for doing so — some founders split shares equally, while others do 49/51 splits for control. Some founders even may have an 80/20 equity split because one founder spent an extra year on the idea.

At the end of the day, a good equity split is one that all founders find fair. If you can’t agree on a structure, you should have a deeper discussion on whether this is the right team to work with for the next decade or more.

Powered by WPeMatico

Hey, founders between gigs: What now?

If you exited your last company for airplane money and are now independently wealthy, congratulations! If you want to build another company, just self-fund. If you want outside capital, VCs will chase after you to invest.

Unfortunately, most founders are not in that position: nine out of 10 startups fail. Even if you achieve a high valuation, you might end up like FanDuel’s founders: Their investors got the benefit of a $465 million exit; the founders got zero.

As someone with “founder” on your resume, you face a greater challenge when trying to get a traditional salaried job. You’ve already shown that you really want to lead a company and not just rise up the ladder, which means some employers are less likely to hire you. One research paper found:

[F]ormer founders receive fewer callbacks than non-founders; however, all founders are not disadvantaged similarly. Former founders of successful ventures receive even fewer [emphasis added] callbacks than former founders of failed ventures. Through 20 interviews with technical recruiters, we highlight the mechanisms driving this founder-experience discount: concerns related to the applicant’s capability and ability to fit into and remain committed to the wage employment and the hiring firm.

At my prior firm, ff Venture Capital, we invested in a company co-founded by Nate Jenkins, who had a successful exit, but not quite enough to buy a private plane. He’s now researching his next opportunity and interviewing for some jobs. At the end of a recent interview, the interviewer summarized, “I’ll hire you, but is this what you really want to do?”

That said, Samuel Sabin, CEO of HireBlue, observed, “Some founders who work better with more resources at their disposal may be tapped for intrapreneurship roles. Also, some companies value a self-starter mentality.”

So what should you do? Especially if your life partner and/or bank account are burnt out on the income volatility of startups?

I’ve been in this situation myself when I shut down one startup and exited two others. I think you have six main options:

At Versatile VC, our new VC fund, we’re creating an online community just for founders who are in transition, Founders’ Next Move. We hope you will join us!

If you want to work on your startup idea, the bar for starting a company should always be very high. VCs have a diversified portfolio and most of their investments die. You don’t have a diverse portfolio and so you’re taking far more risk than the VCs. For free resources to help research your ideas, see What startup will you build? Identifying market white space.

Powered by WPeMatico

It was August 2019, and the fundraising process was not going well.

My co-founder and I had left our product management jobs at New Relic several months prior, deciding to finally plunge into building Reclaim after nearly a year of late nights and weekends spent prototyping and iterating on ideas. We had bits and pieces of a product, but the majority of it was what we might call “slideware.”

When you can’t raise big on the vision, you need to raise big on the proof. And the proof comes from building, learning, iterating and getting traction with your first few hundred users.

When we spoke to many other founders, they all told us the same thing: Go raise, raise big, and raise now. So we did that, even though we were puzzled as to why anyone would give us money with little more than a slide deck to our names. We spent nearly three months pitching dozens of VCs, hoping to raise $3 million to $4 million in a seed round to hire our founding team and build the product out.

Initially, we were excited. There was lots of inbound interest, and we were starting to hear a lot of crazy numbers getting thrown around by a lot of Important People. We thought for sure we were maybe a week away from term sheets. We celebrated preemptively. How could it possibly be this easy?

Then in July, almost in an instant, everything started to dry up. The verbal offers for term sheets didn’t materialize into real offers. We had term sheets, but they were from investors that didn’t seem to care much about what we were building or what problems we wanted to solve. We quickly realized that we hadn’t really built momentum around the product or the vision, but were instead caught up in what we later learned to be “deal flow.”

Basically, investors were interested because other investors were interested. And once enough of them weren’t, nobody was.

Fortunately, as I write this today, Reclaim has raised a total of $6.3 million on great terms across a group of incredible investors and partners. But it wasn’t easy, and it required us to embrace our failure and learn three important lessons that I believe every founder should consider before they decide to go out and pitch investors.

In 2019, we were hunting for what some referred to as a “mango seed” — that is, a seed round that was large enough that it was perceptibly closer to a light Series A financing. Being pre-product at the time, we had to lean on our experience and our vision to drive conviction and urgency among investors. Unfortunately, it just wasn’t enough. Investors either felt that our experience was a bad fit for the space we were entering (productivity/scheduling) or that our vision wasn’t compelling enough to merit investment on the terms we wanted.

When we did get offers, they involved swallowing some pretty bitter pills: We would be forced to take bad terms that were overly dilutive (at least from our perspective), work with an investor who we didn’t think had high conviction in our product strategy, or relinquish control in the company from an extremely early stage. None of these seemed like good options.

Powered by WPeMatico

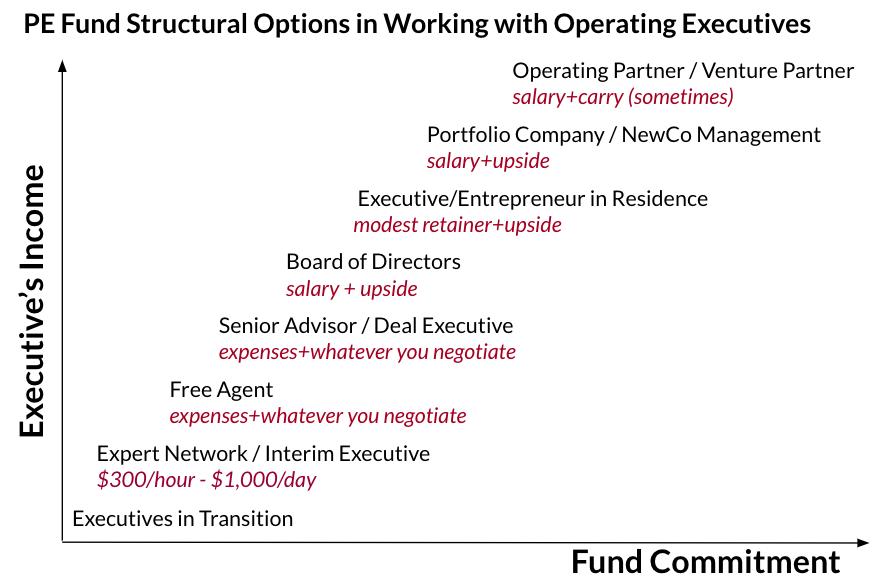

Would you like to work with private equity and venture capital funds?

There are relatively few jobs directly inside private equity and venture capital funds, and those jobs are highly competitive. However, there are many other ways you can work and earn money within the industry — as a consultant, an interim executive, a board member, a deal executive partnering to buy a company, an executive in residence or as an entrepreneur in residence.

Venture capitalists often have an operations background. However, historically most private equity professionals were former investment bankers and other finance professionals. Then private equity players gradually realized that value cannot be created through financial engineering alone. A BCG study of 121 investments found that operational improvement drives 48% of value creation in PE-backed companies. PE funds now almost always require an upgrade in management and change management teams if necessary.

Not surprisingly, the tighter your relationship with the firm, the more money you will earn:

Image Credits: David Teten

At Versatile VC, we’ve used all these models. We are soon launching Founders’ Next Move, a selective, free community for founders researching their next move, which will be a key tool for working with outside talent.

The simplest path forward is to identify funds in your industry of expertise and reach out. You can explore all of the models below with them. First, start by identifying the firms that invest in companies that you’ve worked with. Then, more broadly, look for investors in the industries in which you have expertise. You can identify institutional investors through one of multiple online databases:

| All investors | Private equity | Venture capital |

| Preqin (free demo)

Grey House (free demo) |

PitchBook (free trial)

PrivateEquityFirms.com |

AngelList (free)

CrunchBase (free) PWC MoneyTree (free) VentureDeal (free trial) Asian Venture Capital Journal (free trial) |

Let’s take a look at the different ways you can work with the investment community.

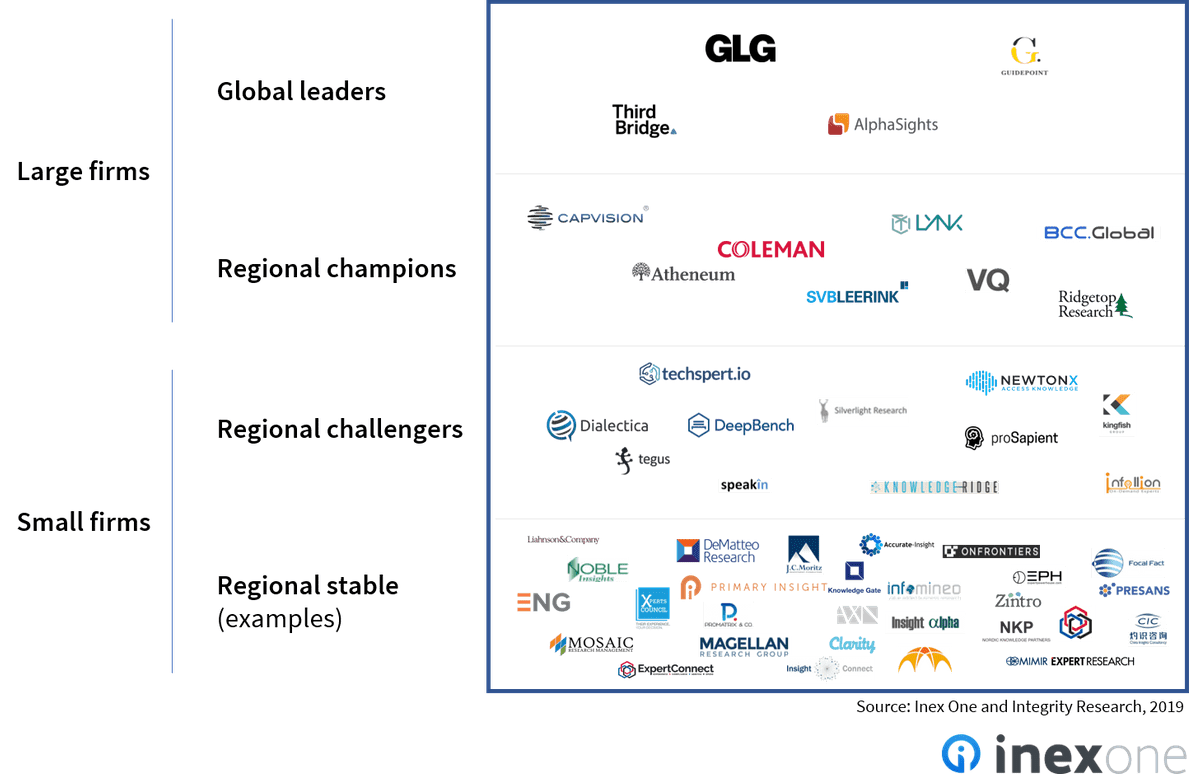

Expert network firms source subject matter experts from various domains and pair them with clients seeking topical or industry insights. They typically charge clients up to $1,200 per hour, and pay the expert $100 to $500 an hour. I founded Circle of Experts, an expert network that I sold to Evalueserve.

The expert network industry has grown an average 4.5% annually between 2015 and 2020, its market size topping $1.3 billion in 2020. While the major clients were initially hedge funds and private equity firms, consulting firms now comprise 32% of total demand for expert network services.

Inex One, an expert network marketplace, has compiled a list of 80 expert networks, summarized in the graphic below:

Image Credits: Inex One and Integrity Research

The largest expert networks include: GLG, which accounts for approximately 50% of the industry’s revenue; AlphaSights is the second biggest generalist expert network; Guidepoint services six major categories of clients globally across several industries; and Third Bridge hires and retains talent to “democratize the world’s human insights and upend the traditional research model.”

Other notable expert networks include Atheneum Partners, Coleman Research Group, Dialectica, ENG, Lynk Global, Mosaic, PreScouter, ProSapient and Tegus. There are also expert networks with sector or geography specialization. For example, SERMO is a global social media network for physicians to exchange knowledge and share challenging patient cases, and Clarity.fm connects startups to experts in building new businesses.

Powered by WPeMatico

As startups and venture capital grow in tandem, fundraising has gone from a formal affair on Sand Hill Road to a process that can happen anywhere from Twitter to Zoom.

While fundraising may no longer require a trip to California, it might depend on whether you got an invite to a private audio app. And while you may not need to be an insider, second-time founders — largely male and white — still have a competitive advantage.

If your intention is to build a company that you want to own and run indefinitely, and/or to grow more slowly and take fewer risks, traditional venture capital is not right for what you want to build.

The growing complexity of fundraising has the opportunity to make tech either inclusive or exclusive. For new founders looking to raise money, let’s dismantle the myths about raising your first check and instead focus on how investors and other successful founders describe the nuance needed to secure money.

This question is existential, but it should be at the forefront throughout your journey as a founder. Elizabeth Yin, founding partner of Hustle Fund, says startups should be able to hit one of two goals: Reach $100 million ARR by its fifth year or get to $1 billion in valuation in the same time period.

“This is hard to do. And most businesses will never get there — not for a lack of trying — but there’s a lot of luck whether your idea has that much demand that quickly,” she added.

“I think you will know in the first year or two how ‘easy’ or ‘hard’ it is to get customers and whether you think on that trajectory you can get to $100 million a year in a few years,” Yin said. “And if it’s really hard, it doesn’t mean you throw in the towel. … There are many great companies that are not VC-backable where the founders will make a lot of money, but it just means you need to think through where to get your financing. Perhaps it’s from angels. Perhaps it’s from revenue-based financing funds. Perhaps it’s from customer crowdfunding.”

While VC is the flashy gold medal, the rapid growth of emerging fund managers means that a first check can be piecemealed together from a variety of different sources. The options for financing are seemingly endless: syndicates, public crowdfunding, VC firms, accelerators, debt financing, rolling funds, and, for the profitable few, bootstrapping.

“When people go around saying, ‘Do you want to run a VC-backable company?’ that feels weird — you don’t necessarily get to pick how fast you can grow — the market just may or may not be there,” Yin said. “There’s a lot of luck with that.”

Leslie Feinzaig, founder of Female Founders Collective, said that beyond economics, the hardest part of knowing whether your startup makes sense as a VC-backed business is understanding your own goals as an entrepreneur.

Powered by WPeMatico

Netflix has two CEOs: Co-founder Reed Hastings oversees the streaming side of the company, while Ted Sarandos guides Netflix’s content.

Warby Parker has co-CEOs as well — its co-founders went to college together. Other companies like the tech giant Oracle and luggage maker Away have shifted from having co-CEOs in recent years, sparking a wave of headlines suggesting that the model is broken.

It’s impossible to be in two places at once or clone yourself. With co-CEOs, you can effectively do just that.

While there isn’t a lot of research on companies with multiple CEOs, the data is more promising than the headlines would suggest. One study on public companies with co-CEOs revealed that the average tenure for co-CEOs, about 4.5 years, was comparable to solitary CEOs, “suggesting that this arrangement is more stable than previously believed.”

The study’s authors also found that co-CEOs were spread across industry types and that splitting the role can “complement each other in terms of educational background or executive responsibilities.”

I serve as co-CEO of an organic meal delivery company with my sister Laureen. Having two CEOs has helped us take Fresh n’ Lean to new heights. We closed 2020 with $87 million in revenue, more than double from the year before, and project similar growth this year.

We complement each other well, and the results bear that out. During the decade that we’ve served as co-CEOs, the company has grown from a very small team to 475 full-time employees and 40 part-time employees. We’ve delivered more than 17 million meals, launched four different meal lines, expanded our retail offerings, partnered with some great names in sports and fitness, and saw our annual revenues climb exponentially.

The leadership structure isn’t for every company, but it’s been a great fit for Fresh n’ Lean. Here’s why.

Laureen launched the company in 2010 out of her one-bedroom apartment.

“Those early years were especially tough,” she said. “I consistently worked 20-hour days as I performed just about every role — cooking dishes, preparing labels, making deliveries and performing customer service duties. I was devoting so much energy into product, packaging and logistics, but in order for the company to grow, I needed help with marketing, tech and finance.”

Those areas happened to be my strengths. There was too much for one person to oversee as CEO and not enough hours in the day. But given the equal challenges that both sides of the company presented and the trust we shared, it made sense for us to be side by side on the organizational chart.

Powered by WPeMatico

Venture capitalists add value in a number of ways. For example, one of my business’ backers has a deep tech “pod” that generates events and content we are always welcomed to be a part of. Another one of our investors gives us full commercial support through its network of mentors that are there to support the business, not the VC.

Due diligence works both ways, and entrepreneurs shouldn’t be in a rush to take investment from anyone that offers it.

I might not expect that from every VC, but if they promise those “assets” by saying that they are here to drive innovation and growth, then I expect them to deliver, just as I have to back up the claim of having a team of supersmart machine learning researchers.

They might know the forks in the road, directions to take, and who to speak to based on having been through the process with similar companies. They might have venture partners that can mentor you and a network of investors that can participate in follow-on rounds. That is where they add value.

The best ones will seek to connect with you personally. They’ll have prepared thoroughly beforehand and are brimming with questions. While they may have preconceived and potentially ill-informed ideas, they demonstrate enthusiasm by starting sentences with “what if,” and they leave me emboldened but contemplative. I fully expect to be provoked in the right way.

However, some also play God. One experience offered up a major warning sign, one that would make me walk on by.

I’m pleased to say my business has some outstanding investors who totally get it. Our investors’ head of investment told representatives at one of New York’s top funds that one of their leading deep tech portfolio companies was coming to town for a “blitz meeting session.” They announced that they were committing to the round I was raising and that we were looking for a new lead investor.

So, put it this way: I wasn’t a guy who walked off the street with a crazy idea, but you might have thought otherwise, given the experience that followed. To be clear, I don’t expect all VCs to open their arms and embrace everyone, but there are rules of engagement.

After a very positive morning meeting, I’d scheduled a couple of hours for a quick chance to grab a breather at my hotel. Flicking through my phone, an email from the associate at the VC I was due to meet next pinged into my inbox.

“Hey Ofri, it’s Jessica [not her real name], really sorry, I’m not feeling great so am thinking I might cut the day short. I know you’re only in New York the next two days, so let’s catch up later on a call and next time you’re over I’m sure we can revisit.”

I started composing a polite response: “Really sorry to hear that. Absolutely fine to reschedule. Let me know your availability, etc., etc.” In truth, I was irritated — this had been in the diary for two months and was one of six meetings scheduled. I was not sorry; I was annoyed.

Powered by WPeMatico