EC Column

Auto Added by WPeMatico

Auto Added by WPeMatico

The technology industry is often thought of as being the domain of the young and the new. We see an emphasis on young founders (“40 Under 40”), innovative ideas and disruptive challenges to legacy brands, incumbent companies and “old” ways of thinking.

But one of the things I’ve learned on my journey in co-founding my latest startup is that technology should be enabling and accessible to all, and nowhere is this more critical than for empowering our older adults.

Older adults are one of the most underrepresented audiences for new technology products and platforms. There is a massive opportunity to provide products and services that will make life better for today’s seniors and future generations of older adults to come. Founders in every space, from edtech to healthcare, from financial services to robotics, can make a bigger impact if we recognize the opportunity of being of service to older adults.

One of the best strategies for tech companies that want to serve the older adult market is to focus your value proposition on empowering older adults.

Older adults often get overlooked by tech companies. In fairness, it can be hard (and insensitive and uninspiring) to market products and services as being “for old people,” because people in this group don’t tend to think of themselves as “old.”

One of the best strategies for tech companies that want to serve the older adult market is to focus your value proposition on empowering older adults. Don’t make a product “for old people” — make a product that helps older adults lead a healthier, more active, more connected life.

Whether it’s the education tech space, financial services, health tech, consumer products or other innovative digital services for seniors, tech companies have big opportunities to empower older adults.

We are seeing some great examples, including:

Older adults have so much to offer. Instead of approaching this market as a “problem” to be solved, startups should engage with older adults as an active, curious, ready-to-learn group of people who are eager to be empowered.

It often seems like so many consumer-facing apps today are created for younger people. But there’s a big disconnect between where so much of the tech industry’s attention and investment is going and the spending power and lifestyle preferences of today’s older adults.

Older adults are the most underserved demographic for the tech world. They’re also one of the fastest-growing age cohorts. The number of people worldwide who are 65 and older is expected to grow from 524 million in 2010 to 1.5 billion in 2050.

The “silver economy,” driven by the spending power of older adults, is expected to grow into the 2030s because the senior population is the wealthiest age group and their numbers are growing 3.2% per year (compared with 0.8% for the overall population).

Powered by WPeMatico

Singapore is home to fewer than six million people, making it one of the smallest ASEAN countries, in terms of population. It is a young country as well — having gained independence in 1963 — and resides in a neighborhood with far larger economies, including China, Indonesia, and Vietnam. When the country first became independent, its mandate was to simply survive rather than thrive.

So how does a country evolve from a position of relative uncertainty, with comparatively few resources, to one that leads the ASEAN region in venture capital investment and has been home to 10 unicorns?

Countries around the world examine Singapore’s ecosystem from a distance, hoping to learn from, and emulate, its story. The World Bank Group recently published a report, The Evolution and State of Singapore’s Start-up Ecosystem, documenting the country’s experience in building its startup ecosystem and the challenges facing it.

This article presents an overview of the report’s key findings and offers a few key recommendations on what other countries can learn from Singapore’s experience, as well as what Singapore itself can do to maintain progress.

As of 2019, Singapore had over $19 billion in PE and VC assets under management, more than twice that of neighboring Indonesia, Philippines, Vietnam, Malaysia, and Thailand combined. In that same year, the country was home to an estimated 3,600 tech startups and nearly 200 different intermediary and supporting organizations (accelerators, co-working spaces, coding academies, etc.) – some which have a multinational presence, such as Blk71, whose Singapore headquarters has been referred to as “the world’s most tightly packed entrepreneurial ecosystem.”

While assessing the size and strength of startup ecosystems is an evolving method, Start-up Genome priced Singapore’s ecosystem at over $25 billion, five times the global median.

Arguably, the most eye-catching hallmark of this ecosystem is its population of current and former unicorns. Collectively, Singapore has been home to ten unicorns, three of which have offered an IPO (Nanofilm, Razer and Sea) and two of which have been acquired – one by giant Alibaba (Lazada) and one by Chinese streaming powerhouse YY (Bigo Live). The remaining five are Trax, Acronis, JustCo, PatSnap, and Grab – the ASEAN region’s largest unicorn to date.

The education sector is also prominent in Singapore’s ecosystem. Universities like the National University of Singapore (NUS) and Nanyang Technological University (NTU) are deeply embedded into this ecosystem, helping with R&D commercialization linkages, incubation, talent/knowledge transfer, and other areas.

Numerous factors have contributed to building Singapore’s startup ecosystem, with government intervention and leadership being the dominant driving forces. The government has spent more than USD60 billion over the past several decades to enhance the country’s R&D infrastructure, create VC funds, and launch accelerators and other support organizations.

Powered by WPeMatico

As a startup founder, there will be three scenarios in which you’ll need to understand how to properly do a quality of earnings (QofE) if you want to maximize value.

The first scenario will be when you decide to raise a Series A and subsequent VC rounds, followed by when you do a strategic acquisition, and lastly, when you sell your company.

This post is a framework for how to think and organize your QofE and go through the most common items that you’ll want to keep top of mind for every M&A and private equity transaction you may be part of.

The goal of a QofE is to adjust the reported EBITDA to calculate a restated EBITDA that best reflects the current state of the company on an ongoing basis. It also presents a historical adjusted EBITDA that is comparable throughout the last two or three years.

QofE can have a significant impact on a company valuation for three main reasons:

With that in mind, every entrepreneur must understand how to properly form a view of what is the proper adjusted EBITDA and adjusted revenue of your company. It is common for founders in an M&A process to be unfamiliar with the notion of QofE and leave value on the table.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room.

This breakdown aims to ensure that you won’t be that founder and that you’ll be armed to negotiate your company valuation on equal ground with your investors. If you are in the seller’s shoes, you will get the advantage of understanding how an experienced investor or buyer thinks. If you’re in the buyer’s shoes, you’ll benefit from understanding and valuing your acquisitions better.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room. These include, but are not limited to: Legal documentation, financial statements (P&L, balance sheet, cash flow), audit reports, management presentation and contracts.

When doing a QofE analysis, it’s key to consistently ask yourself: “Can or should this information translate into an adjustment of revenue or EBITDA, net working capital (NWC) or net debt?”

Why did we include NWC and net debt? That is because they often have an indirect impact on adjusted EBITDA. Think of an adjustment to the historical level of inventory. Less inventory likely means fewer storage costs. So if you adjust historical inventory, you’ll want to also impact your adjusted EBITDA.

On top of reviewing all the aforementioned documents, your QofE analysis will heavily rely on interviewing management. No matter how long you look at the financials, if you can’t have management confirm information or explain trends, you won’t be able to draw proper conclusions and understand the numbers.

Powered by WPeMatico

I worked at Google for six years. Internally, you have no choice — you must use Kubernetes if you are deploying microservices and containers (it’s actually not called Kubernetes inside of Google; it’s called Borg). But what was once solely an internal project at Google has since been open-sourced and has become one of the most talked about technologies in software development and operations.

For good reason. One person with a laptop can now accomplish what used to take a large team of engineers. At times, Kubernetes can feel like a superpower, but with all of the benefits of scalability and agility comes immense complexity. The truth is, very few software developers truly understand how Kubernetes works under the hood.

I like to use the analogy of a watch. From the user’s perspective, it’s very straightforward until it breaks. To actually fix a broken watch requires expertise most people simply do not have — and I promise you, Kubernetes is much more complex than your watch.

How are most teams solving this problem? The truth is, many of them aren’t. They often adopt Kubernetes as part of their digital transformation only to find out it’s much more complex than they expected. Then they have to hire more engineers and experts to manage it, which in a way defeats its purpose.

Where you see containers, you see Kubernetes to help with orchestration. According to Datadog’s most recent report about container adoption, nearly 90% of all containers are orchestrated.

All of this means there is a great opportunity for DevOps startups to come in and address the different pain points within the Kubernetes ecosystem. This technology isn’t going anywhere, so any platform or tooling that helps make it more secure, simple to use and easy to troubleshoot will be well appreciated by the software development community.

In that sense, there’s never been a better time for VCs to invest in this ecosystem. It’s my belief that Kubernetes is becoming the new Linux: 96.4% of the top million web servers’ operating systems are Linux. Similarly, Kubernetes is trending to become the de facto operating system for modern, cloud-native applications. It is already the most popular open-source project within the Cloud Native Computing Foundation (CNCF), with 91% of respondents using it — a steady increase from 78% in 2019 and 58% in 2018.

While the technology is proven and adoption is skyrocketing, there are still some fundamental challenges that will undoubtedly be solved by third-party solutions. Let’s go deeper and look at five reasons why we’ll see a surge of startups in this space.

Docker revolutionized how developers build and ship applications. Container technology has made it easier to move applications and workloads between clouds. It also provides as much resource isolation as a traditional hypervisor, but with considerable opportunities to improve agility, efficiency and speed.

Powered by WPeMatico

With the fourth quarter now upon us, every industry faces a challenge in managing a holiday production calendar that will deliver the goods. The key for startups looking to defend the quarter from disruptions is to adopt a proactive, data-driven approach to inventory management.

Here are five methods we’ve been counseling clients to adopt:

Ultimately, AI will help startups understand how myriad disruptions affect their supply chain so they can better respond with a Plan B when the unthinkable happens.

Powered by WPeMatico

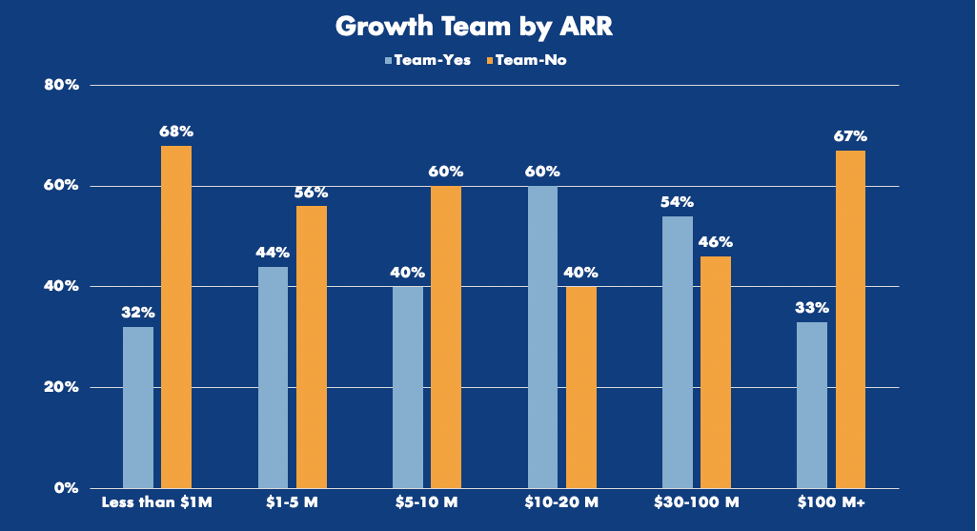

Everyone at an organization should own growth, right? Turns out when everyone owns something, no one does. As a result, growth teams can cause an enormous amount of friction in an organization when introduced.

Growth teams are twice as likely to appear among businesses growing their ARR by 100% or more annually. What’s more, they also seem to be more common after product-market fit has been achieved — usually after a company has reached about $5 million to $10 million in revenue.

Image Credits: OpenView Partners

I’m not here to sell you on why you need a growth team, but I will point out that product-led businesses with a growth team see dramatic results — double the median free-to-paid conversion rate.

Image Credits: OpenView Partners

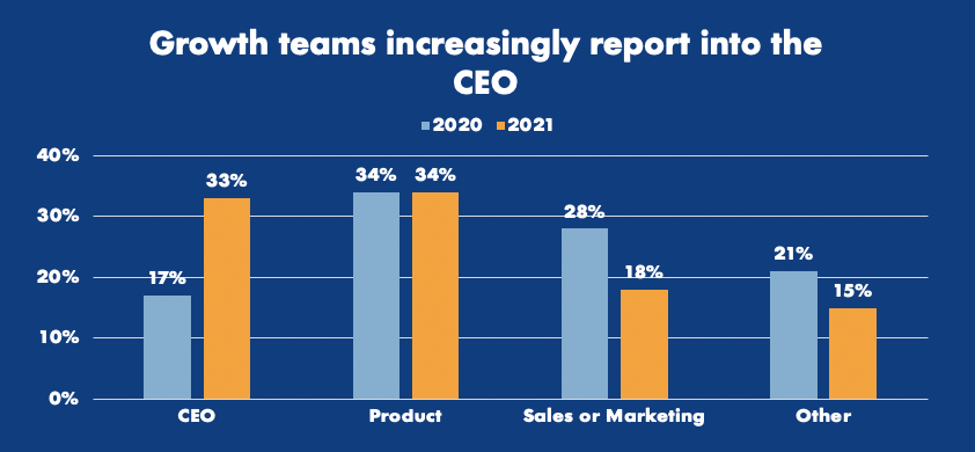

According to responses from product benchmarks surveys, growth teams have transitioned dramatically from reporting to marketing and sales to reporting directly to the CEO.

Some of the early writing on growth teams says that they can be structured individually as their own standalone team or as a SWAT model, where experts from various other departments in the organization converge on a regular cadence to solve for growth.

Image Credits: OpenView Partners

My experience, and the data I’ve collected from business-user focused software companies, has led me to the conclusion that growth teams in business software should not be structured as “SWAT” teams, with cross-functional leadership coming together to think critically about growth problems facing the business. I find that if problems don’t have a real owner, they’re not going to get solved. Growth issues are no different and are often deprioritized unless it’s someone’s job to think about them.

Becoming product-led isn’t something that happens overnight, and hiring someone will not be a silver bullet for your software.

I put early growth hires into a few simple buckets. You’ve got:

Product-minded growth experts: These folks are all about optimizing the user experience, reducing friction and expanding usage. They’re usually pretty analytical and might have product, data or MarketingOps backgrounds.

Powered by WPeMatico

Many VCs tout their mentorship and hands-on approach to founders, especially those who run early-stage startups. But in the recent era of lightning-fast rounds closing at sky-high valuations, the cap tables of early-stage startups are becoming increasingly crowded.

This isn’t to say that the value VCs bring has diminished. If anything, it’s quite the opposite — this new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table. It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.

Founders should definitely pursue big rounds at sky-high valuations, but it’s important that they recognize how important it is to manage who they allow into their mentorship circles. Initially, founders should make sure their first layer consists of the real “doers” — usually angels and early venture investors who founders meet with weekly (or more frequently) to help solve some of the most granular problems.

Everything from hiring to operational hurdles all the way to deeper, more personal challenges like balancing family life with a rapidly growing startup.

This circle is where the real mentorship happens, where founders can be open and vulnerable. For obvious reasons, this circle has to be small, and usually consist of two to six people at most. Anything more simply becomes unwieldy and leaves founders spending more time managing these relationships than actually building their company.

How founders manage their VC circles can mean the difference in success or failure for a thousand different reasons.

The second layer should consist of the “quarterly crowd” of investors. These aren’t necessarily people who are uninterested or unwilling to participate in the nitty gritty of running the company, but this circle tends to consist of VCs who make dozens of investments per year. They, like their founders, aren’t capable of managing 50 relationships on a weekly basis, so their touch points on company issues tend to move slower or less frequently.

Powered by WPeMatico

In a company’s early days, the difference between C-level executives and the rest of the organization is simple — employees can walk away from a failure, but the leaders cannot. Under these conditions, certain kinds of people thrive in leadership roles and can take a company from ideation to production.

While there’s no magic formula for what works and what doesn’t, successful startups share common traits in terms of the way their foundational leadership teams are built.

We’ve all experienced what it looks like on the negative end of the spectrum — people making points simply to hear their own voice, leaders competing for credit and clashing agendas. When people would rather be heard than contribute, the output suffers. Members of a healthy leadership team are unafraid to let others have the limelight, because they trust the mission and the culture they’ve built together.

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of.

We are all imperfect human beings, founders included. There are always going to be moments that leaders can’t predict, and mistakes come with the territory. The right leadership team should be able to mitigate the unexpected, and sometimes make the future easier to predict. Putting the right people in the right roles early on can be the difference between success and failure — and that starts at the top.

Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.

Startup founders should ask themselves a few questions before they lose sleep over the prospect of handing over the reigns:

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of. In many cases, founders decide they need outside help to fill the role. While a CEO may not be your first hire — or even one of the first five — the person you choose will ultimately occupy your organization’s most critical leadership role, so choose wisely.

What to look for: Ambitious vision grounded in execution reality. Your CEO should have hands-on experience that allows them to see around corners, predict pitfalls and identify opportunities.

What to watch out for: Leaders who lack respect for the founding vision or the ability to hire and balance an executive team quickly. A good CEO should be able to manage short-term cash flow and go-to-market needs without compromising the true north, while building a foundation and culture for the long term.

Powered by WPeMatico

Though 2021 is far from over, it’s already witnessed a record level of venture capital activity in the technology sector. With larger round sizes announced daily, founders may have their pick of term sheets — but they need to think critically and strategically about which firms to add to their cap table.

So far this year, we’ve seen $292.4 billion in venture financing across the globe, of which $138.9 billion was raised in the United States. Specific to tech companies, the capital is only accelerating: In Q2, founders raised 157% more capital compared to the same period last year, according to the latest data from CB Insights.

It’s not just that more companies are raising money — they are doing so at a higher valuation. Median seed and Series A stage valuations today stand at $12 million and $42 million, respectively, up 20% to 30% from 2020. This can be partly attributed to growing exits/M&A activity in the technology sector, a record number of IPOs and a general bullishness around technology, as well as low interest rates and liquidity in the market.

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table.

At a time when we are witnessing record VC activity, founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table. Here are a few pointers for founders in that direction:

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table. Typically, such value is created across a few distinct functions — product, sales, domain expertise, business development and recruiting, to name a few — based on the background of the partners of the fund and the composition of their limited partners (investors in the venture fund).

Further, the right VC can serve as an authentic, objective sounding board for CEOs, which can be an asset to have as a startup navigates uncertainty and the typical challenges that come with scaling a young company. As founders assess multiple term sheets, it’s worth thinking through whether they should optimize for VCs who offer the highest valuation, or for ones who bring the most value to the table.

Running an efficient fundraising process, in part, entails holding VCs accountable to their own diligence requests. While it is unfortunately common for VCs to request a lot of data upfront, startups should share information after assessing intent and appetite on the investors’ part.

For every additional data request, founders are well within their rights (and should) check with their potential investors on where the process stands and get indicative timelines for moving forward with next steps. Mark Suster said it best: “Data rooms are where fundraising processes go to die.”

Powered by WPeMatico

What’s the board’s role in an early-stage startup?

Startup founders frequently ask me about the role of a board of directors. A board can be a crucial asset in an early-stage startup.

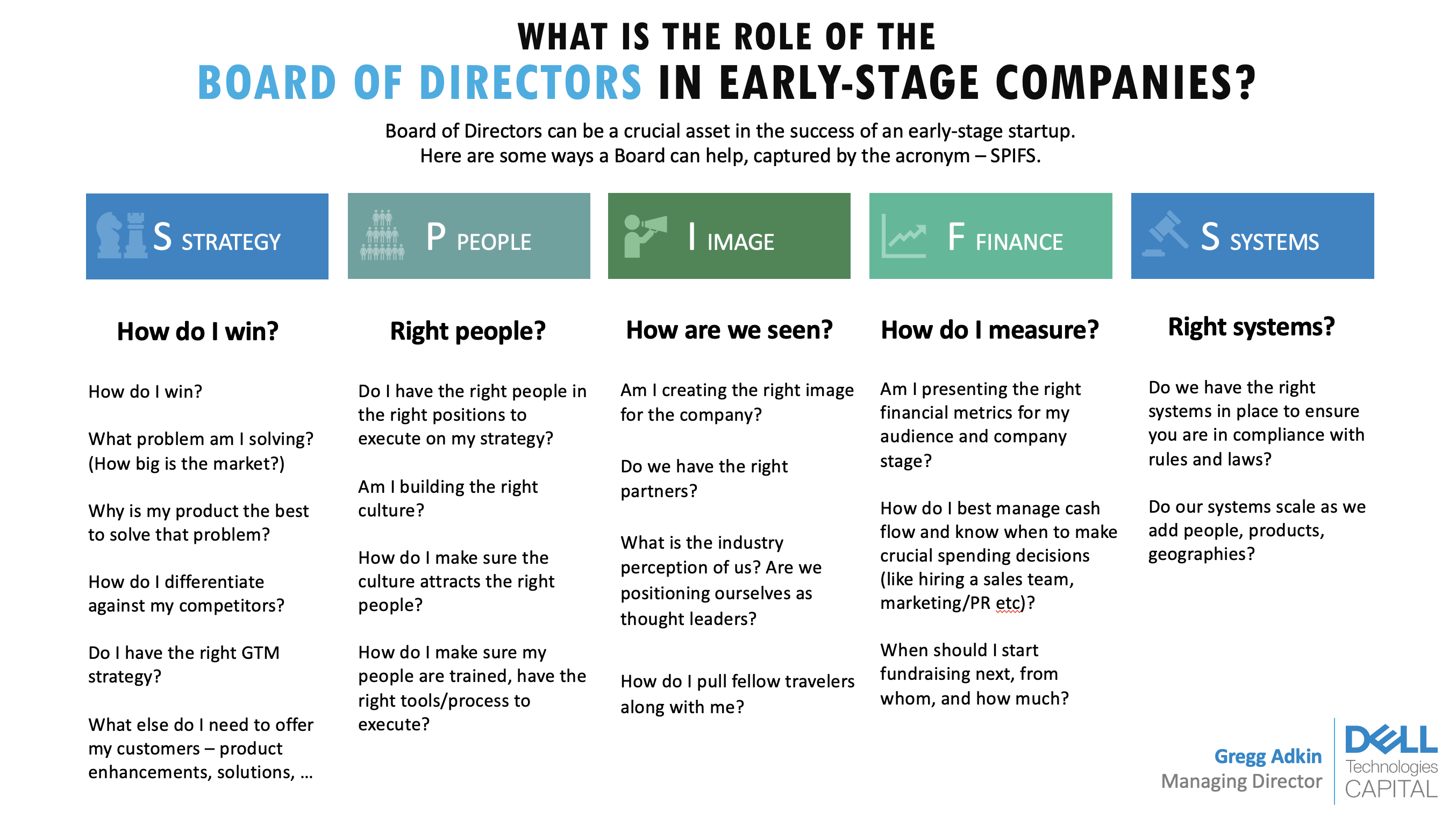

Here’s a framework for how it can help drive success at your company: Strategy, People, Image, Finance and Systems for compliance, or “SPIFS.”

The board of directors helps with governance of the company. U.S. law requires that any company have one, though does not require how big it should be. By generic definition, the board of directors consists of elected individuals that represent shareholders. It is the governing body that provides company oversight and helps set business policy and strategy.

On a more practical level and in a startup environment, the board can aid in creating a successful business strategy, putting together the right management team, developing branding, building good financial habits, and avoiding legal and compliance issues. The needs and composition of the board will change depending on the startup’s stage, management and financing history (e.g., if there are preferred shareholders, investors that require a board seat and more).

Investors often ask founders about their board: It says a lot about their character, their judgment and their willingness to be challenged.

Investors often ask founders about their board for two reasons. First, it says a lot about their character, their judgment and their willingness to be challenged. The founder can typically choose who is on their board (through careful selection of investors and advisers) and negotiate a board structure they prefer.

Typically, a healthy board will have a good balance between common shareholders, preferred shareholders and independents. It also helps investors and analysts understand who will ask critical questions and give important advice to the company’s executive management, especially when the going gets tough (it inevitably does!).

After 20 years as a venture capitalist and board member, I boiled down the value of a board into five main pieces under the acronym SPIFS: Strategy, People, Image, Finance and Systems for compliance.

Image Credits: Dell Technologies Capital

Setting business strategy is one of the main ways that the board helps founders, especially if it’s their first time running a business. It is a valuable sounding board for validating that you have taken a sober account of the market and have the right plan to develop your product and acquire customers.

The board should ask these questions when guiding founders through setting strategy:

Powered by WPeMatico