EC Cloud and Enterprise Infrastructure

Auto Added by WPeMatico

Auto Added by WPeMatico

Before he was a partner at Lightspeed Venture Partners, Gaurav Gupta had his eye on Grafana Labs, the company that supports open-source analytics platform Grafana. But Raj Dutt, Grafana’s co-founder and CEO, played hard to get.

This week on Extra Crunch Live, the duo explained how they came together for Grafana’s Series A — and eventually, its Series B. They also walked us through Grafana’s original Series A pitch deck before Gupta shared the aspects that stood out to him and how he communicated those points to the broader partnership at Lightspeed.

Gupta and Dutt also offered feedback on pitch decks submitted by audience members and shared their thoughts about what makes a great founder presentation, pulling back the curtain on how VCs actually consume pitch decks.

We’ve included highlights below as well as the full video of our conversation.

We record new episodes of Extra Crunch Live each Wednesday at 12 p.m. PST/3 p.m. EST/8 p.m. GMT. Check out the February schedule here.

As soon as Gupta joined Lightspeed in June 2019, he began pursuing Dutt and Grafana Labs. He texted, called and emailed, but he got little to no response. Eventually, he made plans to go meet the team in Stockholm but, even then, Dutt wasn’t super responsive.

The pair told the story with smiles on their faces. Dutt said that not only was he disorganized and not entirely sure of his own travel plans to see his co-founder in Stockholm, Grafana wasn’t even raising. Still, Gupta persisted and eventually sent a stern email.

“At one point, I was like ‘Raj, forget it. This isn’t working’,” recalled Gupta. “And suddenly he woke up.” Gupta added that he got mad, which “usually does not work for VCs, by the way, but in this case, it kind of worked.”

When they finally met, they got along. Dutt said they were able to talk shop due to Gupta’s experience inside organizations like Splunk and Elastic. Gupta described the trip as a whirlwind, where time just flew by.

“One of the reasons that I liked Gaurav is that he was a new VC,” explained Dutt. “So to me, he seemed like one of the most non-VC VCs I’d ever met. And that was actually quite attractive.”

To this day, Gupta and Dutt don’t have weekly standing meetings. Instead, they speak several times a week, conversing organically about industry news, Grafana’s products and the company’s overall trajectory.

Dutt shared Grafana’s pre-Series A pitch deck — which he actually sent to Gupta and Lightspeed before they met — with the Extra Crunch Live audience. But as we know now, it was the conversations that Dutt and Gupta had (eventually) that provided the spark for that deal.

Powered by WPeMatico

The recent Databricks funding round, a $1 billion investment at a $28 billion valuation, was one of the year’s most notable private investments so far.

For Databricks signaled its IPO readiness by disclosing to TechCrunch last year that it had scaled its revenue run rate from $200 million to $350 million in a year, so the new capital looked like the capstone on its private fundraising before an eventual public debut.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But I did have a few questions, starting with the price of the round.

At a $28 billion valuation and ARR of $425 million, Databricks is valued at around 66x top line. That’s steep, if not the highest number we can dredge up on the public markets. Of course, for Databricks shareholders, seeing the value of their stock rise so quickly is hardly a bad thing. They are hardly going to complain about having more paper wealth.

But what about the investor perspective? Does the price really make sense? The Exchange caught up with Battery Ventures’ Dharmesh Thakker earlier this week to discuss a number of things, one of which was Databricks’ round and pricing. Thakker is named in the Databricks Series D funding announcement, which brought Battery into the company.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

Intriguing, yeah? So this morning for both of us, I’ve pulled out quotes from our chat to help explain how Thakker views the market for Databricks, unicorns at scale more broadly through the lens of risk-adjusted investing, and the scale of the market some unicorns are playing in.

At the close, we’ll remind ourselves what Databricks CEO Ali Ghodsi told TechCrunch when we asked him the same question. Let’s go!

Here’s how the valuation part of my chat with the Battery Ventures’ investor went down:

The Exchange: I want to talk about Databricks, because I spoke to [CEO] Ali [Ghodsi] yesterday about this round, and hot damn, it’s a lot of money at a valuation that is roughly 64x ARR, give or take. I don’t understand the price, and I know it’s a boring thing to talk about. [It’s a] great company, I get their market, I’ve talked to them a bunch, I know their revenue numbers. [But] I don’t understand the price, and I was hoping you could tell me why I’m being too conservative.

Dharmesh Thakker: I, for what it’s worth, think [the price] fair. If anything, I think it is on the lower end — he could have done better, frankly. But I think it comes down to three major things, right?

One is the addressable market. Just think about the addressable market of data. If there’s a trillion dollars spent in software or technology, I think you and I would be both hard pressed to say, almost all of that [isn’t] influenced by some data-oriented decisioning. Whether it’s digital transformation, whether it’s analytics, data is everywhere. So the TAM is massive … I think you and I both agree on that, whether it is $20 billion or $80 billion — it’s massive.

Powered by WPeMatico

Software buying has evolved. The days of executives choosing software for their employees based on IT compatibility or KPIs are gone. Employees now tell their boss what to buy. This is why we’re seeing more and more SaaS companies — Datadog, Twilio, AWS, Snowflake and Stripe, to name a few — find success with a usage-based pricing model.

The usage-based model allows a customer to start at a low cost, while still preserving the ability to monetize a customer over time.

The usage-based model allows a customer to start at a low cost, minimizing friction to getting started while still preserving the ability to monetize a customer over time because the price is directly tied with the value a customer receives. Not limiting the number of users who can access the software, customers are able to find new use cases — which leads to more long-term success and higher lifetime value.

While we aren’t going 100% usage-based overnight, looking at some of the megatrends in software — automation, AI and APIs — the value of a product normally doesn’t scale with more logins. Usage-based pricing will be the key to successful monetization in the future. Here are four top tips to help companies scale to $100+ million ARR with this model.

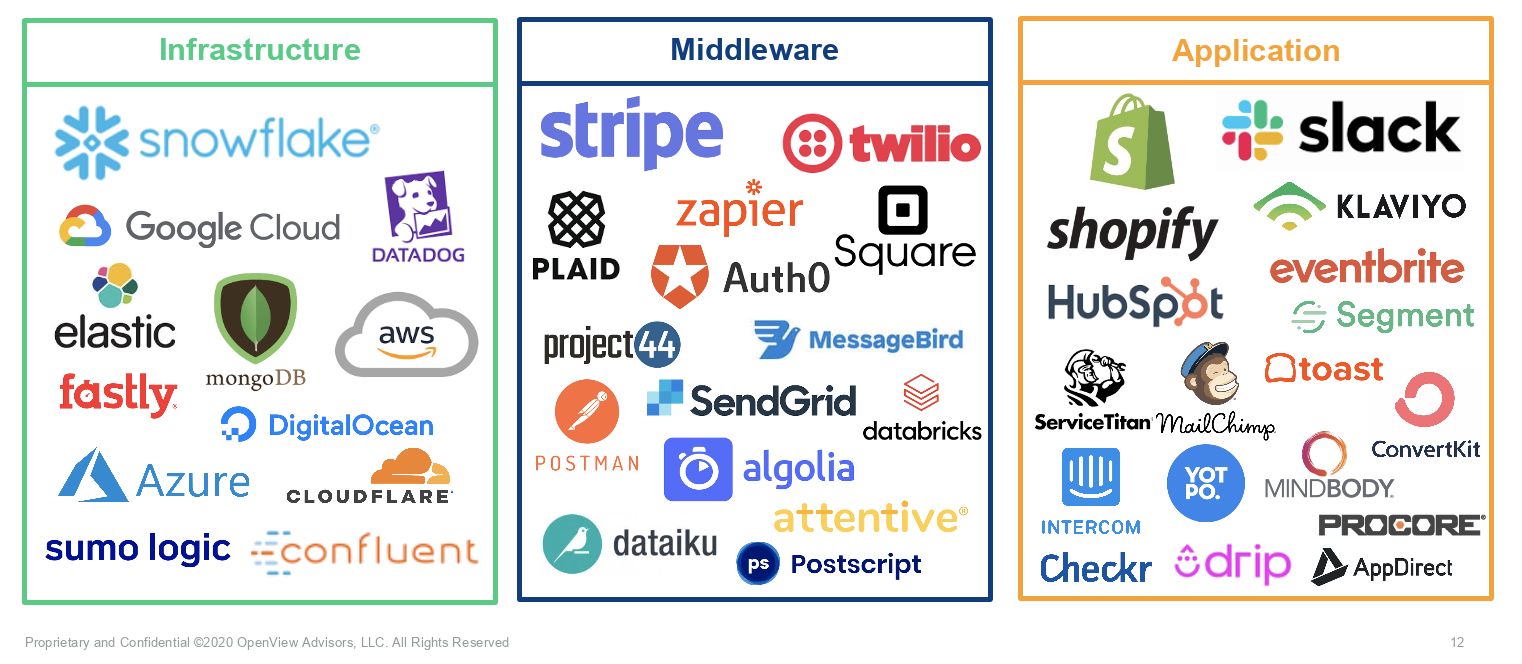

Usage-based pricing is in all layers of the tech stack. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software — across infrastructure, middleware and applications.

Image Credits: Kyle Povar / OpenView

Some fear that investors will hate usage-based pricing because customers aren’t locked into a subscription. But, investors actually see it as a sign that customers are seeing value from a product and there’s no shelf-ware.

In fact, investors are increasingly rewarding usage-based companies in the market. Usage-based companies are trading at a 50% revenue multiple premium over their peers.

Investors especially love how the usage-based pricing model pairs with the land-and-expand business model. And of the IPOs over the last three years, seven of the nine that had the best net dollar retention all have a usage-based model. Snowflake in particular is off the charts with a 158% net dollar retention.

Powered by WPeMatico

Amidst all of the the sturm und drang of l’affaire GameStop, Qualtrics went public today.

After pricing its stock above its raised IPO range, the company received a warm welcome from public investors. After starting its trading life worth $41.85, Qualtrics closed the day worth $45.50, up some 51.67%.

Qualtrics did everything that it said it was going to.

The software company’s debut comes after a lengthy path to the public markets; Qualtrics sold to SAP on the eve of its first run at a public listing back in 2018. Now, SAP has completed spinning the company out, though the software giant remains the Utah unicorn’s largest shareholder.

That Qualtrics’ IPO might perform well was presaged in its pricing run, having prices far above its initial valuation estimates; there was evidence of strong demand even before its shares started to trade.

But did Qualtrics misprice, given its strong first-day performance? TechCrunch spoke with Qualtrics CEO Zig Serafin, and its founder and current executive chairman Ryan Smith about its public offering, hoping to learn a bit about what is next for the company.

Having spoken to myriad folks on IPO days, I’ve learned the best way to kick off is to ask about emotions. Most CEOs and other execs are tied up in what they can (and cannot) say. And they are well-trained by communications experts regarding what to repeat and emphasize. You can sometimes loosen them up a little, however, by asking them how they feel.

In response to that question, Serafin described a feeling of gratitude and Smith brought up the long game. Qualtrics, he said, had been told that it couldn’t bootstrap, that it couldn’t build in Utah, that SAP had overpaid, that SAP had messed up and so forth.

Powered by WPeMatico