EC Cloud and Enterprise Infrastructure

Auto Added by WPeMatico

Auto Added by WPeMatico

Robotic process automation unicorn UiPath is set to go public this week, concentrating our focus on its value.

The well-known company was last valued on the private markets at $35 billion in February when it closed a $750 million round. Living up to that price as a public company, however, at least when it comes to its formal IPO price, is proving to be challenging.

In a sense, that’s not too surprising given that the red-hot IPO market cooled as Q1 2021 came to a close. UiPath raised its last private round when the markets were most interested in public offerings and is now going public in a slightly altered climate.

In numerical terms, UiPath raised its IPO range from $43 to $50 per share, to $52 to $54 per share. That’s a 21% jump in the value of the lower end of its range, and an 8% gain to the value of the upper end of its per-share IPO price interval.

UiPath is also selling more shares than before, which should make its total valuation slightly larger at the top end than a mere 8% gain. So let’s go through the math one more time. Afterward, we’ll stack its new simple, fully diluted IPO valuations against its final private price, ask ourselves if our musings on the company’s recent profitability bore out, and close by asking where the company might finally price, and if we expect it to do so above its new price range.

Powered by WPeMatico

Many emerging and mature organizations survive or die based on their ability to scale. Scale quicker. Scale cheaper. Scale right.

Typically the IT team bears that burden — on top of countless other demands. IT teams move mountains for their organizations while scaling the tech platform as fast as possible, putting out the latest infrastructure fire and responding to countless day-to-day requests.

The most helpful gift any chief information officer or chief technology officer can give their IT teams is more time. Many people think that means adding another team member. Maybe it does in some cases (if you can find a developer in this tough job market), but giving my team Boomi’s low-code integration platform was one of the best strategic moves for HealthBridge.

The best time to use low-code is when you need to add something to your organization that isn’t unique or doesn’t drive significant business value.

As the least skilled coder on the team, low-code let me develop and deliver four customer-centric self-service portals a year ahead of schedule while my team focused on building and scaling our revenue-driving, custom platform by hand-writing code.

Low-code is quickly becoming commonplace and a popular topic among IT decision-makers. Over the last few years, the market has exploded. Gartner expects it to total $13.8 billion in 2021. That means low-code technology, which we’ve been hearing about for years, is ready for widespread adoption. Today, low-code enables you to streamline (and scale) everything from integration to artificial intelligence.

It’s a secret only some organizations are clued in on, but it’s a great way to scale fast, save on resources and give your team more time. Here’s how.

The best time to use low-code is when you need to add something to your organization that isn’t unique or doesn’t drive significant business value.

For instance, a customer portal is not unique; don’t waste time hand-coding it.

While it’s certainly an extremely helpful feature for our customers, it’s unlikely to drive significant shareholder or investor value. However, it’s key for scaling. Using low-code for a must-have but undifferentiated feature will allow your team to work on more important projects while scaling.

When we started working on the timeline for a customer portal project at HealthBridge, we estimated it would take several sprints per portal to develop, but more pressing development work kept pushing it down the list in our backlog. Waiting a year for a basic feature didn’t seem reasonable to me, so we looked for a workaround.

Powered by WPeMatico

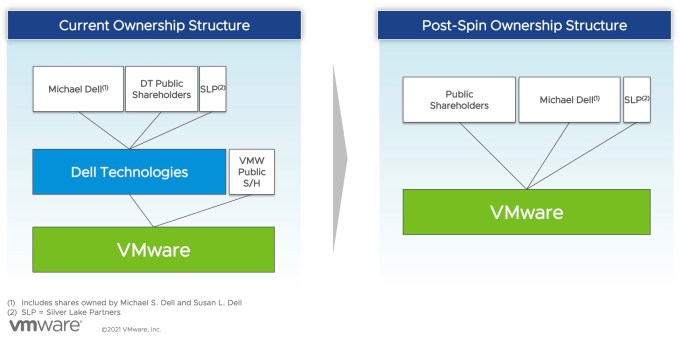

TechCrunch has spilled much digital ink tracking the fate of VMware since it was brought to Dell’s orbit thanks to the latter company’s epic purchase of EMC in 2016 for $58 billion. That transaction saddled the well-known Texas tech company with heavy debts. Because the deal left VMware a public company, albeit one controlled by Dell, how it might be used to pay down some of its parent company’s arrears was a constant question.

Dell made its move earlier this week, agreeing to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence, and in terms of Dell influence? Dell no longer will hold formal control over VMware as part of the deal, though its shareholders will retain a large stake in the virtualization giant. And with Michael Dell staying on VMware’s board, it will retain influence.

Here’s how VMware described it to shareholders in a presentation this week. The graphic shows that under the new agreement, VMware is no longer a subsidiary of Dell and will now be an independent company.

Image Credits: VMware

But with VMware tipped to become independent once again, it could become something of a takeover target. When Dell controlled VMware thanks to majority ownership, a hostile takeover felt out of the question. Now, VMware is a more possible target to the right company with the right offer — provided that the Dell spinout works as planned.

Buying VMware would be an expensive effort, however. It’s worth around $67 billion today. Presuming a large premium would be needed to take this particular technology chess piece off the competitive board, it could cost $100 billion or more to snag VMware from the public markets.

So VMware will soon be more free to pursue a transaction that might be favorable to its shareholders — which will still include every Dell shareholder, because they are receiving stock in VMware as part of its spinout — without worrying about its parent company simply saying no.

Powered by WPeMatico

When Dell announced it was spinning out VMware yesterday, the move itself wasn’t surprising; there had been public speculation for some time. But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

The dividend route, which involves a payment to shareholders between $11.5 billion and $12 billion, has the advantage of being tax-free (or at least that’s what Dell hopes as it petitions the IRS). For Dell, which owns 81% of VMware, the dividend translates to somewhere between $9.3 billion and $9.7 billion in cash, which the company plans to use to pay down a portion of the huge debt it still holds from its $58 billion EMC purchase in 2016.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

VMware was the crown jewel in that transaction, giving Dell an inroad to the cloud it had lacked prior to the deal. For context, VMware popularized the notion of the virtual machine, a concept that led to the development of cloud computing as we know it today. It has since expanded much more broadly beyond that, giving Dell a solid foothold in cloud native computing.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned. Dell CEO Michael Dell will remain chairman of the VMware board, which should help smooth the post-spinout relationship.

But could Dell have extracted more cash out of the deal?

Patrick Moorhead, principal analyst at Moor Insights and Strategies, says that beyond the cash transaction, the deal provides a way for the companies to continue working closely together with the least amount of disruption.

“In the end, this move is more about maximizing the Dell and VMware stock price [in a way that] doesn’t impact customers, ISVs or the channel. Wall Street wasn’t valuing the two companies together nearly as [strongly] as I believe it will as separate entities,” Moorhead said.

Powered by WPeMatico

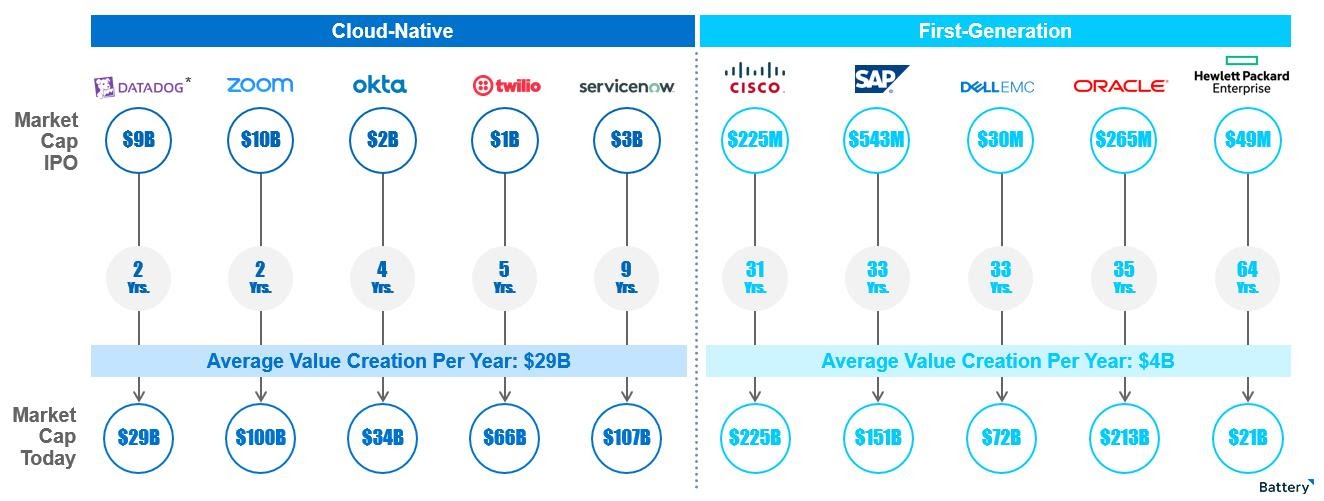

More than half a decade ago, my Battery Ventures partner Neeraj Agrawal penned a widely read post offering advice for enterprise-software companies hoping to reach $100 million in annual recurring revenue.

His playbook, dubbed “T2D3” — for “triple, triple, double, double, double,” referring to the stages at which a software company’s revenue should multiply — helped many high-growth startups index their growth. It also highlighted the broader explosion in industry value creation stemming from the transition of on-premise software to the cloud.

Fast forward to today, and many of T2D3’s insights are still relevant. But now it’s time to update T2D3 to account for some of the tectonic changes shaping a broader universe of B2B tech — and pushing companies to grow at rates we’ve never seen before.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

I call this new paradigm “billion-dollar B2B.” It refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

In the past several years, we’ve seen a pioneering group of B2B standouts — Twilio, Shopify, Atlassian, Okta, Coupa*, MongoDB and Zscaler, for example — approach or exceed the $1 billion revenue mark and see their market capitalizations surge 10 times or more from their IPOs to the present day (as of March 31), according to CapIQ data.

More recently, iconic companies like data giant Snowflake and video-conferencing mainstay Zoom came out of the IPO gate at even higher valuations. Zoom, with 2020 revenue of just under $883 million, is now worth close to $100 billion, per CapIQ data.

Image Credits: Battery Ventures via FactSet. Note that market data is current as of April 3, 2021.

In the wings are other B2B super-unicorns like Databricks* and UiPath, which have each raised private financing rounds at valuations of more than $20 billion, per public reports, which is unprecedented in the software industry.

Powered by WPeMatico

Covering YC Demo Day yesterday was good fun, but I missed a few items while watching several hundred startup pitches. A few years ago, these stories might have been the biggest news of the week.

But with the venture capital market redlining its engines while public markets remain sympathetic to growing, unprofitable companies, there’s lots going on. So, as a follow-up to our first late-stage roundup that we published yesterday morning, here’s another.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

This time we’re discussing IPO news from DigitalOcean (context), Kaltura (context), Robinhood (context) and Zymergen, and big rounds for Lattice and goPuff. That’s a lot to chew on, but I’ll be brief and to the point.

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

Today’s most pressing news is that DigitalOcean, a provider of cloud services to small businesses, priced its IPO at $47 per share last night. That was right at the top of its public-offering price range of $44 to $47. Before counting shares reserved for its underwriters, DigitalOcean is worth just under $5 billion.

And the company raised a gross $775.5 million in the offering, giving DigitalOcean a massive war chest to pursue its vision. As the company has proved increasingly unprofitable on a GAAP basis in recent years, the extra cash isn’t a problem: DigitalOcean plans to reduce its aggregate debt load with some of the proceeds, which will improve its profitability.

The company won’t trade for hours, so we’re done with DigitalOcean for now. File it in your mind as a win, as the company raised $50 million last year at a $1.1 billion valuation (PitchBook data). That’s a quick 5x.

Next up from the IPO treadmill is Kaltura, which released a first guess of its market value as a public company. Targeting $14 to $16 per share in its impending debut, the video software company is worth around $2 billion at the top end of its range, not counting shares reserved for its underwriting banks or other shares tied up in vested options and recruited stock units (RSUs).

Powered by WPeMatico

We’ve reached the end of Y Combinator’s biggest Demo Day, which saw more than 300 companies pitching back-to-back over eight hours.

Earlier, we highlighted some of the companies that caught our eye in the first half of the day. Now we’re back with our favorite companies from the second half. From a marketplace to help you resell formalwear to a startup that offers self-driving street cleaners, it’s quite the mix.

If you’d like to browse all of the companies from this batch YC has a catalog of publicly-launched W21 companies here.

Heading into this particular demo day, I had my eyes peeled for startups focused on delivering services via an API instead of offering managed software. Happily, there have been a number to dig into, including Pitbit.ai, Bimaplan, Enode and Terra.

Terra stood out to me because it solves a problem I care deeply about, namely fitness data siloization. My running data is stuck in one app, biking data in another, and my weight-lifting data is stuck in my head, though I doubt Terra has an API for that interface quite yet.

What Terra does is permit fitness app developers to better connect their services, which permits the sharing of data back and forth. Presenters likened their startup to Plaid — a popular thing to do in recent quarters — saying that what the fintech startup did for banking data, Terra would do for fitness and health information.

Getting developers to sign on will be tricky, as I presume all of the apps I use in an exercise context would prefer to be my main workout home. But I don’t want that, so here’s hoping Terra realizes its vision.

— Alex

Calling itself “Shopify for beauty and wellness” in Latin America, AgendaPro wants to help small businesses in the region book customers online and collect payments.

The company’s idea isn’t as radical as some companies that we heard from today — Carbon capture! Faster drug discovery! — but the company did share several metrics that made us sit up. First, AgendaPro has reached $152,000 in MRR, or just over $1.8 million in ARR. And representatives shared that its gross margins are 89%. As far as software margins goes, that’s pretty damn good.

The startup has more than 3,000 merchants using its service at the moment, and it claims that there are more than four million businesses that it could service. If AgendaPro can get software and payments revenues from even a respectable fraction of those companies, it will be a big, big business. And who doesn’t love vertical SaaS?

— Alex

One of the holy grails of biochemistry is a programmable DNA machine. These tools can essentially “code” a molecule so that it reliably sticks to a specific substance or cell type, which allows a variety of follow-up actions to be taken.

For instance, a DNA machine could lock onto COVID-19 viruses and then release a chemical signal indicating infection before killing the virus. The same principle applies to a cancer cell. Or a bacterium. You get the picture — and it looks like Atom Bioworks has something a lot like this.

Powered by WPeMatico

It’s that time again! Today is Demo Day for Y Combinator’s latest accelerator batch — its largest to date, with more than 300 teams getting a minute each to pitch their companies to an audience of investors.

This is the third time YC has held its Demo Day via a Zoom livestream and the second time the entire program was entirely virtual. YC president Geoff Ralston outlined their thinking for this latest batch — and how/why they’ve expanded the program to over 300 companies — in a post this morning.

Want to see all of the companies? YC has a catalog of the entire Winter 2021 batch here (minus those that haven’t publicly launched), filterable by industry and region.

If you don’t have time to skim through it all, we’ve aggregated some of the companies that really managed to catch our eye. This is part one of two, covering our favorites from the companies that launched in the first half of the day.

As Alex Wilhelm put it last time we did one of these, “we’re not investors, so we’re not pretending to sort the unicorns from the goats.” But we do spend a lot of time talking with startups, hearing pitches and telling their stories; if you’re curious about which companies stood out, read on.

Prospa is building a neobank for small companies in Nigeria. The startup charges customers $7 per month and has reached $50,000 in monthly recurring revenue. That’s some pretty darn good traction. We found Prospa notable because Nigeria’s economy and population are rapidly growing, neobanks have succeeded in a number of markets thus far, and the company’s clear business model and early traction stood out.

And Prospa isn’t targeting a small market. It said during its presentation that there are 37 million so-called “microbusinesses” in its target country. That’s a lot of scale to grow into, and it’s really nice to hear from a neobank that isn’t going to merely pray that interchange revenues will eventually stack to the moon.

— Alex

Image Credits: Blushh

Blushh, built by a team of ex-Google, Amazon, Harvard and BCG professionals, is creating a directory of short, sensual audio stories for women in Asia. The startup believes that there is a massive unmet need for adult content created for women, instead of men, signing up 100 paying subscribers within its first month on the market.

During their pitch, co-founder Soy Hwang said Blushh wants to do for sexual wellness what “Spotify and Audible did for music and audio books.” This startup stands out because it is taking on an untapped market ridden with stigma and lack of innovation. It’s a risk on several levels, and considering the fact that many venture capitalists today still have a “vice” clause that prevents them from investing in sex tech, it will be key to see how Blushh funds itself to keep growing.

— Natasha

TechCrunch caught up with BrioHR a few weeks ago when the startup announced that it had closed a $1.3 million round. During its presentation, the company announced that it had reached $13,000 in monthly recurring revenue (MRR), or $156,000 in annual recurring revenue (ARR).

The company is building human resources software for companies in Southeast Asia, a market it considers fraught with old software and outdated business processes. The company is doing two things. First, building software to help manage and pay workers. The latter part of its work requires lots of localization, so it’s rolling out more slowly than the rest of its software.

If Southeast Asia is as fertile ground for modern HR software as the United States has been shown to be, BrioHR could find more than enough room to grow. I’m excited to see how far the company can scale its ARR with the round that we recently covered.

— Alex

Strava walked so Charge Running could, well, run. The startup, founded by a former Navy SEAL, app connoisseur and kinesiology specialist, is an app that offers live virtual running classes. The consumer play is being framed by the team as a “Peloton for running” with motivation and social engagement during the run.

Powered by WPeMatico

Snowflake announced earlier this month that it would give up its dual-class shareholder structure, a corporate governance setup that often gives founders and executives superior voting rights, typically involving 10 times as many votes for their own shares as others receive. The mechanism can enable founders to maintain control despite later dilution and may sometimes even grant ironclad control to an individual in perpetuity.

For many companies, these supervoting shares represent a highly powerful tool, allowing founders to have their cake and eat it, too — to go public and receive the advantages of being a public company while limiting the power of external shareholders to influence how they run the company once it floats.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted. Dual-class shares are a controversial governance structure, and some wonder if they are setting up an unfair playing field by allowing a cabal to wield outsized power.

Why would Snowflake give up such a powerful tool a mere six months after it went public? We decided to look at the notion of dual-class shares and why Snowflake may have been willing to let them go.

If one of the primary purposes of dual-class shares is to consolidate CEO power, then perhaps Snowflake felt they weren’t necessary, given the history of CEO-shuffling at the company. While Snowflake’s founders are still part of the organization, they hired Sutter Hill investor Mike Speiser to be their first CEO, followed by former Microsoft exec Bob Muglia before finally bringing in veteran CEO Frank Slootman to take their company public.

Without an all-powerful CEO founder in place, perhaps the company felt that supervoting shares weren’t necessary. Regardless, Snowflake CFO Mike Scarpelli framed the move as a decision that works for all parties when he announced that his company would abandon the special shares during its earnings call earlier this month.

“Today, we announced that on March 1st, 2021, our Class B shareholders in accordance with our governing documents converted all of our Class B common stock to Class A common stock, eliminating the dual-class structure of our common stock and ensuring that each share has an equal vote. We view this as operationally beneficial to the company and our shareholders,” Scarpelli said during the call.

Powered by WPeMatico

Data is a gold mine for a company.

If managed well, it provides the clarity and insights that lead to better decision-making at scale, in addition to an important tool to hold everyone accountable.

However, most companies are stuck in Data 1.0, which means they are leveraging data as a manual and reactive service. Some have started moving to Data 2.0, which employs simple automation to improve team productivity. The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation. This is our journey to Data 3.0.

The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation.

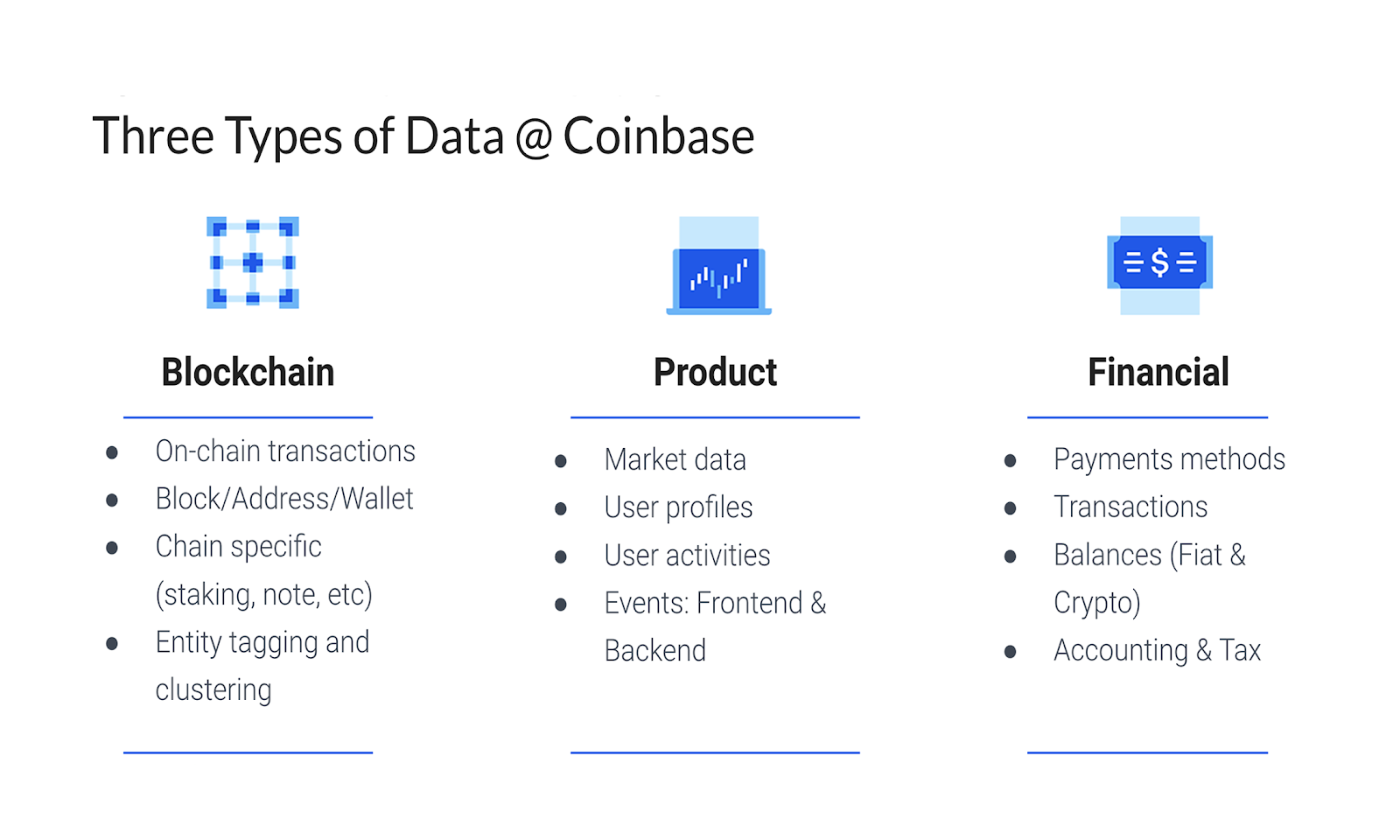

Coinbase is neither a finance company nor a tech company — it’s a crypto company. This distinction has big implications for how we work with data. As a crypto company, we work with three major types of data (instead of the usual one or two types of data), each of which is complex and varied:

Image Credits: Michael Li/Coinbase

Our focus has been on how we can scale value creation by making this varied data work together, eliminating data silos, solving issues before they start and creating opportunities for Coinbase that wouldn’t exist otherwise.

Having worked at tech companies like LinkedIn and eBay, and also those in the finance sector, including Capital One, I’ve observed firsthand the evolution from Data 1.0 to Data 3.0. In Data 1.0, data is seen as a reactive function providing ad-hoc manual services or firefighting in urgent situations.

Powered by WPeMatico